hsbc asset management september 2004 hsbc asset management (hong kong) limited level 22, hsbc main...

TRANSCRIPT

HSBC Asset Management

September 2004

HSBC Asset Management (Hong Kong) LimitedLevel 22, HSBC Main Building, 1 Queen’s Road Central, Hong KongTelephone: +852 2284 1111 Facsimile: +852 2845 0226Web site: www.assetmanagement.hsbc.com.hk

Hong Kong Baptist University1998 Superannuation FundInvestment review

2

hkb

u2

8e_w

h0

8

HSBC Asset Management

Agenda

Investment performance

Market outlook and investment strategy

Factors for consideration before switching

hkb

u2

8e_w

h0

8

HSBC Asset Management

3

Investment performance

4

hkb

u2

8e_w

h0

8

HSBC Asset Management

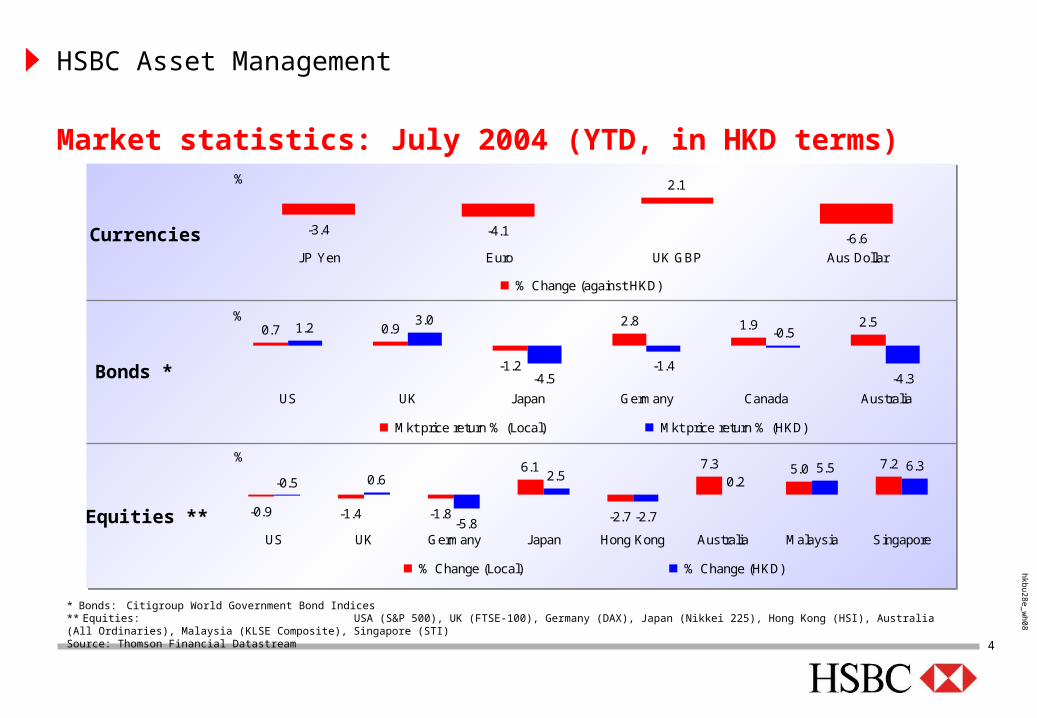

Currencies

Bonds *

Equities **

* Bonds: Citigroup World Government Bond Indices** Equities: USA (S&P 500), UK (FTSE-100), Germany (DAX), Japan (Nikkei 225), Hong Kong (HSI), Australia (All Ordinaries), Malaysia (KLSE Composite), Singapore (STI)Source: Thomson Financial Datastream

Market statistics: July 2004 (YTD, in HKD terms)

-4.1

2.1

-6.6-3.4

JP Yen Euro UK GBP Aus Dollar

%

% Change (against HKD)

2.8 1.9

-1.4

-0.50.9 2.5

-1.2

0.7 1.23.0

-4.3-4.5

US UK Japan Germany Canada Australia

%

Mkt price return % (Local) Mkt price return % (HKD)

-1.4

6.1

-2.7

7.25.07.3

-1.8-0.9

0.6 2.5

-2.7

6.35.5-0.5

-5.8

0.2

US UK Germany Japan Hong Kong Australia Malaysia Singapore

%

% Change (Local) % Change (HKD)

5

hkb

u2

8e_w

h0

8

HSBC Asset Management

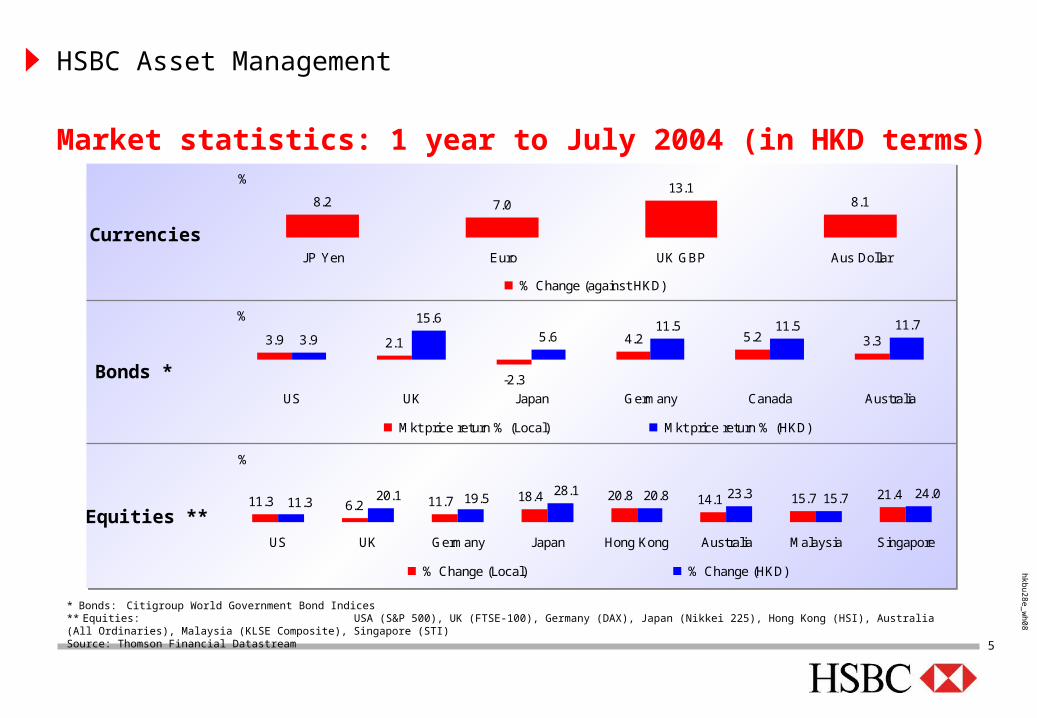

Currencies

Bonds *

Equities **

* Bonds: Citigroup World Government Bond Indices** Equities: USA (S&P 500), UK (FTSE-100), Germany (DAX), Japan (Nikkei 225), Hong Kong (HSI), Australia (All Ordinaries), Malaysia (KLSE Composite), Singapore (STI)Source: Thomson Financial Datastream

Market statistics: 1 year to July 2004 (in HKD terms)

7.013.1

8.18.2

JP Yen Euro UK GBP Aus Dollar

%

% Change (against HKD)

4.2 5.23.9

15.611.5 11.5

2.1 3.3

-2.3

3.911.7

5.6

US UK Japan Germany Canada Australia

%

Mkt price return % (Local) Mkt price return % (HKD)

6.218.4 20.8 21.415.714.111.711.3 20.1 28.1 20.8 24.015.711.3 19.5 23.3

US UK Germany Japan Hong Kong Australia Malaysia Singapore

%

% Change (Local) % Change (HKD)

6

hkb

u2

8e_w

h0

8

HSBC Asset Management

More suitable forrisk tolerant staff

Balanced FundMore suitable forrisk averse staff

High Growth Fund

Growth Fund

Risk (short-term volatility)

Global Money Funds (HKD/USD)

High

Low High

Stable Fund

Lo

ng

-ter

m p

ote

nti

al r

etu

rn

Risk profile of various investment options

7

hkb

u2

8e_w

h0

8

HSBC Asset Management

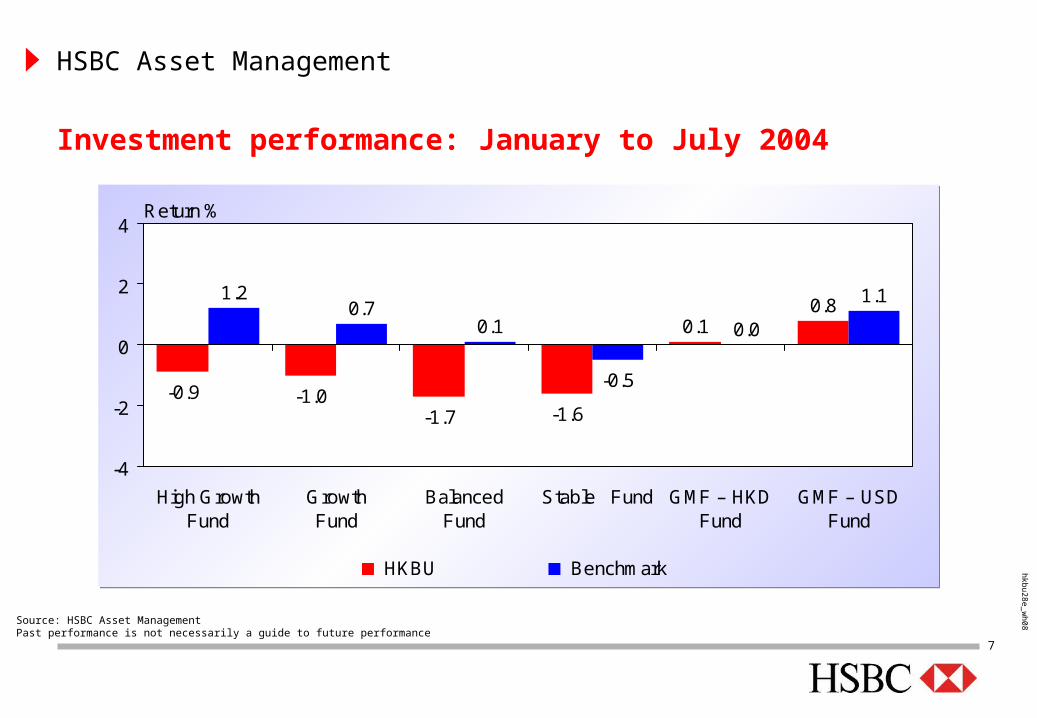

-0.9 -1.0-1.7 -1.6

0.10.8

1.20.7

0.1

-0.5

0.0

1.1

-4

-2

0

2

4

High GrowthFund

Growth Fund

BalancedFund

Stable Fund GMF – HKDFund

GMF – USDFund

Return %

HKBU Benchmark

Investment performance: January to July 2004

Source: HSBC Asset ManagementPast performance is not necessarily a guide to future performance

8

hkb

u2

8e_w

h0

8

HSBC Asset Management

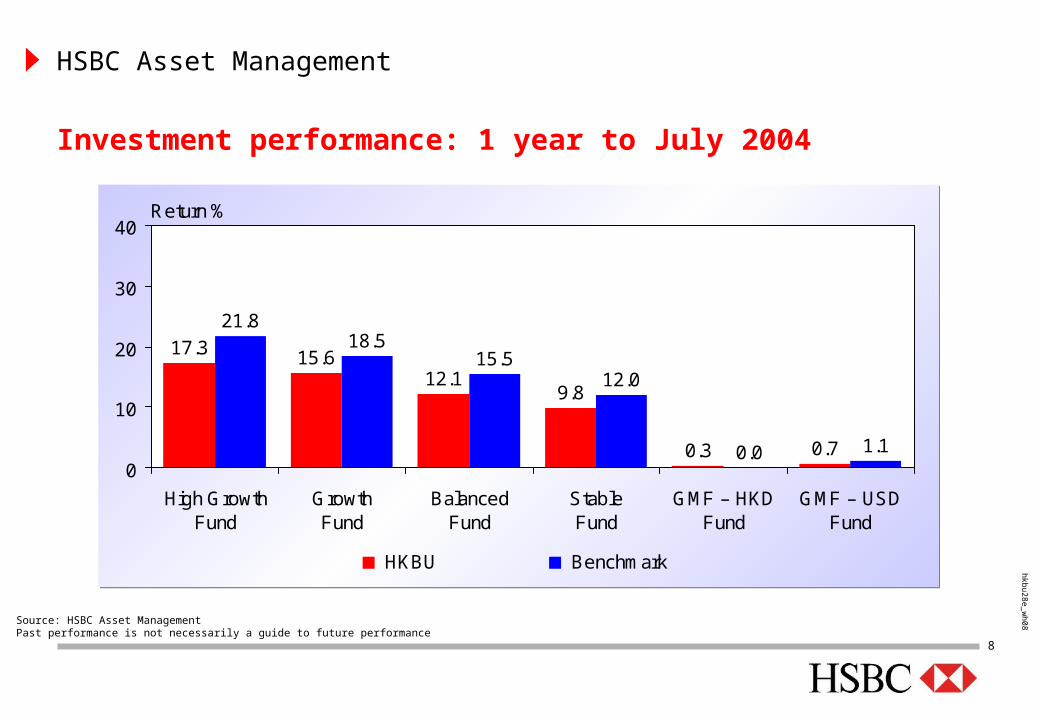

17.3 15.612.1

9.8

0.3 0.7

21.818.5

15.512.0

0.0 1.10

10

20

30

40

High GrowthFund

Growth Fund

BalancedFund

Stable Fund

GMF – HKDFund

GMF – USDFund

Return %

HKBU Benchmark

Investment performance: 1 year to July 2004

Source: HSBC Asset ManagementPast performance is not necessarily a guide to future performance

9

hkb

u2

8e_w

h0

8

HSBC Asset Management

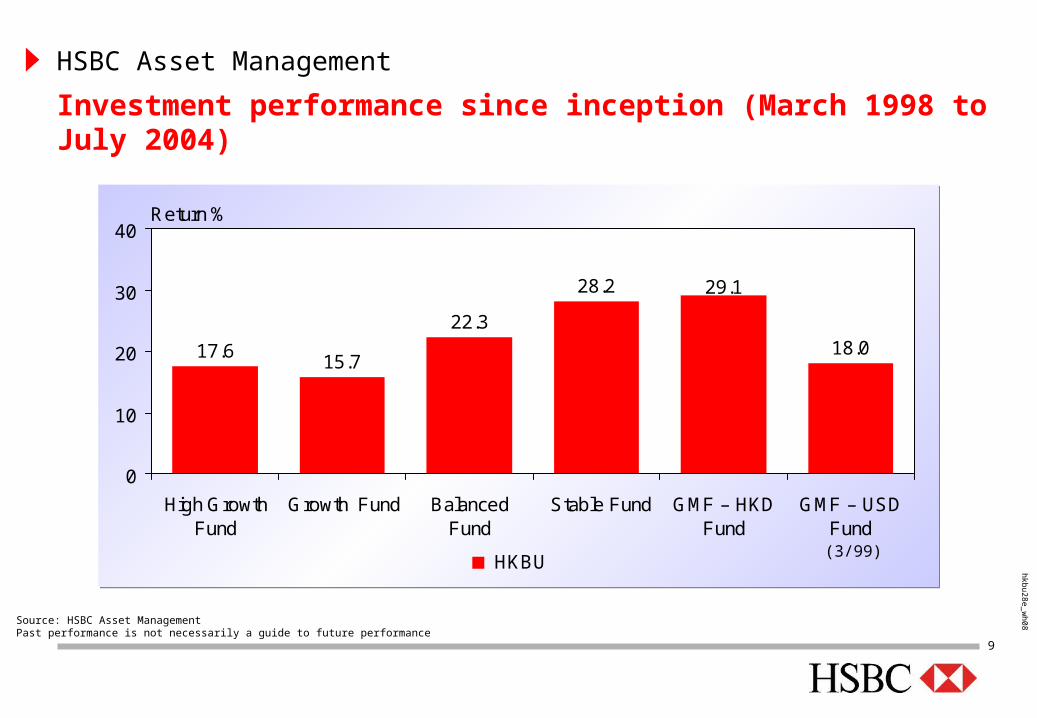

17.615.7

22.3

28.2

18.0

29.1

0

10

20

30

40

High GrowthFund

Growth Fund BalancedFund

Stable Fund GMF – HKDFund

GMF – USDFund

Return %

HKBU(3/99)

Investment performance since inception (March 1998 to July 2004)

Source: HSBC Asset ManagementPast performance is not necessarily a guide to future performance

10

hkb

u2

8e_w

h0

8

HSBC Asset Management

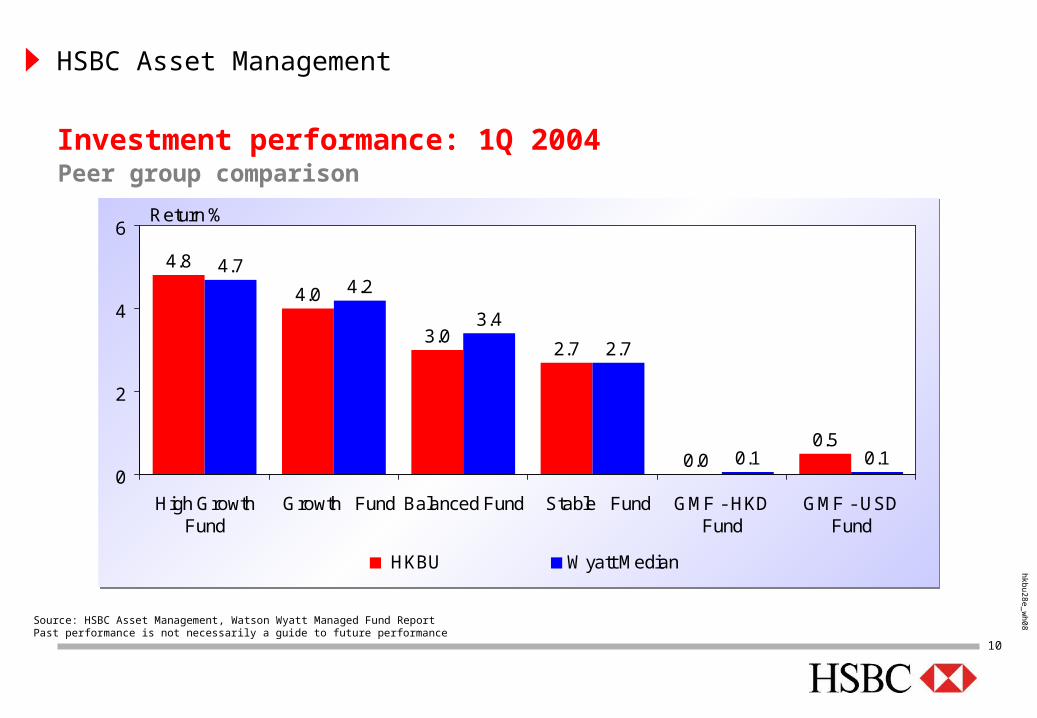

4.8

4.0

3.02.7

0.00.5

4.74.2

3.4

2.7

0.1 0.10

2

4

6

High GrowthFund

Growth Fund Balanced Fund Stable Fund GMF - HKDFund

GMF - USDFund

Return %

HKBU Wyatt Median

Source: HSBC Asset Management, Watson Wyatt Managed Fund ReportPast performance is not necessarily a guide to future performance

Investment performance: 1Q 2004Peer group comparison

11

hkb

u2

8e_w

h0

8

HSBC Asset Management

-3.5 -3.3 -3.3 -3.1

0.0 0.3

-2.9 -2.8 -2.8 -2.9

0.0 0.0

-5

-2.5

0

2.5

5

High GrowthFund

Growth Fund

BalancedFund

Stable Fund GMF - HKDFund

GMF - USDFund

Return %

HKBU Wyatt Median

Source: HSBC Asset Management, Watson Wyatt Managed Fund ReportPast performance is not necessarily a guide to future performance

Investment performance: 2Q 2004Peer group comparison

12

hkb

u2

8e_w

h0

8

HSBC Asset Management

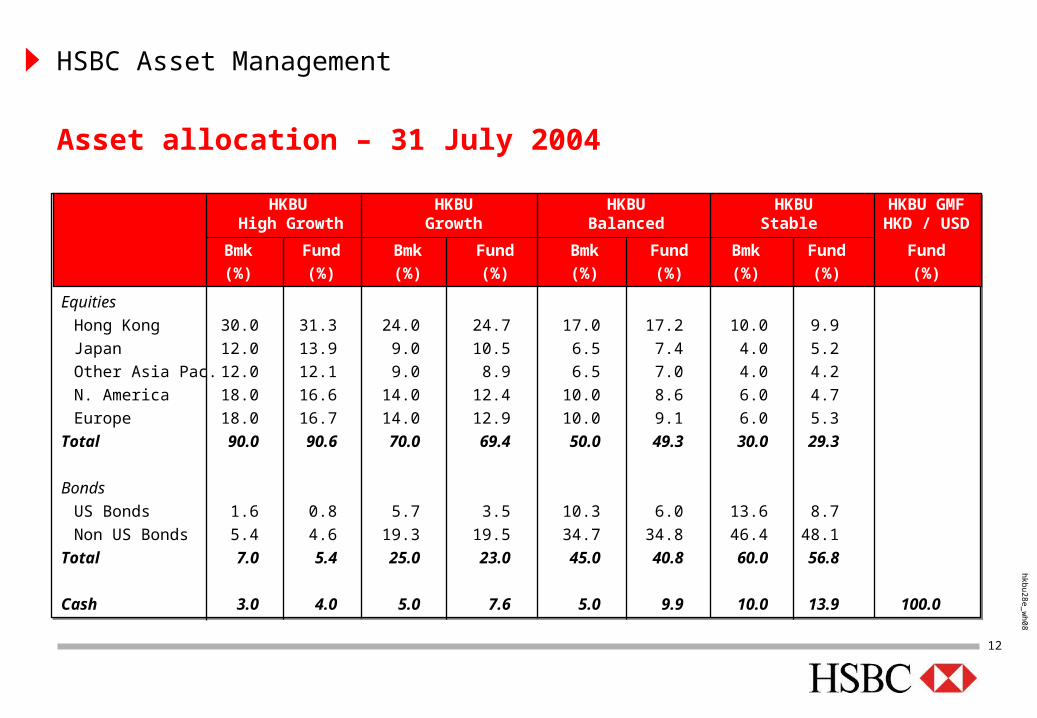

Asset allocation – 31 July 2004

Equities

Hong Kong 30.0 31.3 24.0 24.7 17.0 17.2 10.0 9.9

Japan 12.0 13.9 9.0 10.5 6.5 7.4 4.0 5.2

Other Asia Pac. 12.0 12.1 9.0 8.9 6.5 7.0 4.0 4.2

N. America 18.0 16.6 14.0 12.4 10.0 8.6 6.0 4.7

Europe 18.0 16.7 14.0 12.9 10.0 9.1 6.0 5.3

Total 90.0 90.6 70.0 69.4 50.0 49.3 30.0 29.3

Bonds

US Bonds 1.6 0.8 5.7 3.5 10.3 6.0 13.6 8.7

Non US Bonds 5.4 4.6 19.3 19.5 34.7 34.8 46.4 48.1

Total 7.0 5.4 25.0 23.0 45.0 40.8 60.0 56.8

Cash 3.0 4.0 5.0 7.6 5.0 9.9 10.0 13.9 100.0

Equities

Hong Kong 30.0 31.3 24.0 24.7 17.0 17.2 10.0 9.9

Japan 12.0 13.9 9.0 10.5 6.5 7.4 4.0 5.2

Other Asia Pac. 12.0 12.1 9.0 8.9 6.5 7.0 4.0 4.2

N. America 18.0 16.6 14.0 12.4 10.0 8.6 6.0 4.7

Europe 18.0 16.7 14.0 12.9 10.0 9.1 6.0 5.3

Total 90.0 90.6 70.0 69.4 50.0 49.3 30.0 29.3

Bonds

US Bonds 1.6 0.8 5.7 3.5 10.3 6.0 13.6 8.7

Non US Bonds 5.4 4.6 19.3 19.5 34.7 34.8 46.4 48.1

Total 7.0 5.4 25.0 23.0 45.0 40.8 60.0 56.8

Cash 3.0 4.0 5.0 7.6 5.0 9.9 10.0 13.9 100.0

HKBU HKBU HKBU HKBU HKBU GMFHigh Growth Growth Balanced Stable HKD / USD

Bmk Fund Bmk Fund Bmk Fund Bmk Fund Fund

(%) (%) (%) (%) (%) (%) (%) (%) (%)

hkb

u2

8e_w

h0

8

HSBC Asset Management

13

Market outlook

14

hkb

u2

8e_w

h0

8

HSBC Asset Management

US

– Slowdown in second quarter of 2004 GDP growth and worse than expected consumption

– Residential and business investment remained strong

– Falling unemployment, and rising household income

– Budget deficit could be slightly lower than expected due to increased revenues

– But geopolitical issues and strong oil price weigh on markets

– Margins at 40-year highs, earnings may come under pressure

– Valuations are looking more attractive

– Balance sheet repair makes meaningful increases in dividends possible

Outlook– US - Moderate Underweight

– GDP growth forecast for 2004 (+4.3%); 2005 (+3.6%)

Data as at 4 August 2004

15

hkb

u2

8e_w

h0

8

HSBC Asset Management

Europe

Euroland– Recovery continues although at a gradual pace– Sluggish domestic demand; but growth driven by exports– Earnings growth revised upwards on higher forecast revenues, not cost cutting– More attractive valuations but oil price concern still lingers

UK– Annualised second quarter of 2004 growth at 3.7%, fastest seen in four years – Impact of higher interest rates on consumption is key– Generally strong earnings report, but profit-taking to continue in the short term– Valuations not stretched

Outlook– Europe - Neutral; UK - Neutral– GDP growth forecast for 2004 and 2005: Europe (+2.0%, +2.4%); UK (+3.5%, +2.4%)

Data as at 4 August 2004

16

hkb

u2

8e_w

h0

8

HSBC Asset Management

Japan

– June data pointed to a slowing pace of growth

– Official view still positive; consensus for 2004 GDP growth forecasts increased slightly to 4.2%

– Deflation continues to ease, consensus predicts zero inflation in 2005

– Good quarterly earnings, but cautious company guidance due to higher energy and materials costs

– Market is becoming more sensitive to potential risks

– Valuation is reasonable with markets trading at 18 times of price earning

Outlook– Japan - Neutral

– GDP growth forecast for 2004 (+4.0%) and 2005 (+2.0%)

Data as at 4 August 2004

17

hkb

u2

8e_w

h0

8

HSBC Asset Management

Asia (ex-Japan)

– Trade and retail data still indicate that Asia, including China, is heading for a soft landing

– Moderation in growth momentum expected in second half of 2004 following US slowdown

– However, growth still remains strong driven by domestic consumption

– Despite rising oil prices, inflationary pressures still benign

– Recent market weakness was due to sector specific issues

– Investors are concerned about earnings growth next year

– Due to overcapacity, Technology drags the market most

– Asia still seems cheap, in both relative and absolute terms

Outlook– Asia (ex-Japan) – Moderate Overweight

Data as at 4 August 2004

18

hkb

u2

8e_w

h0

8

HSBC Asset Management

Asia (ex-Japan)

Hong Kong (moderate overweight)– Falling unemployment rate, easing deflationary and strong retail sales– Upward earnings revisions to resume with positive management guidance– Successful property launches rejuvenate the sagging property sector

– Market consolidation may continue in the coming month – Remain sanguine on the Hong Kong on a 12-month view

Korea (underweight)– Market unlikely to turn around in near future despite historical low market valuations– Suffering from high crude oil prices– Negatives: second half of 2004 export growth might decline, earnings forecast reductions, struggling local

consumption

Taiwan (underweight)– Market still lacks catalysts – Negatives: PC seasonality trend yet to confirm, earnings downgrades, weak investor confidence – Valuation becomes more attractive

Data as at 4 August 2004

19

hkb

u2

8e_w

h0

8

HSBC Asset Management

Bond market outlook

US– Economy retains a strong underlying momentum despite soft data– Expect 0.5% of rate hikes in 3 months, and 2% total over 12 months

Euroland– Improving domestic economic activity prompts Central Bank to reduce policy stimulus– Expect the European Central Bank to commence tightening monetary policy in 12 months

Japan– No policy changes within the next 3 or 12 months– Possible measured reduction in quantitative stimulus should current economic recovery

continue

Data as at 4 August 2004

20

hkb

u2

8e_w

h0

8

HSBC Asset Management

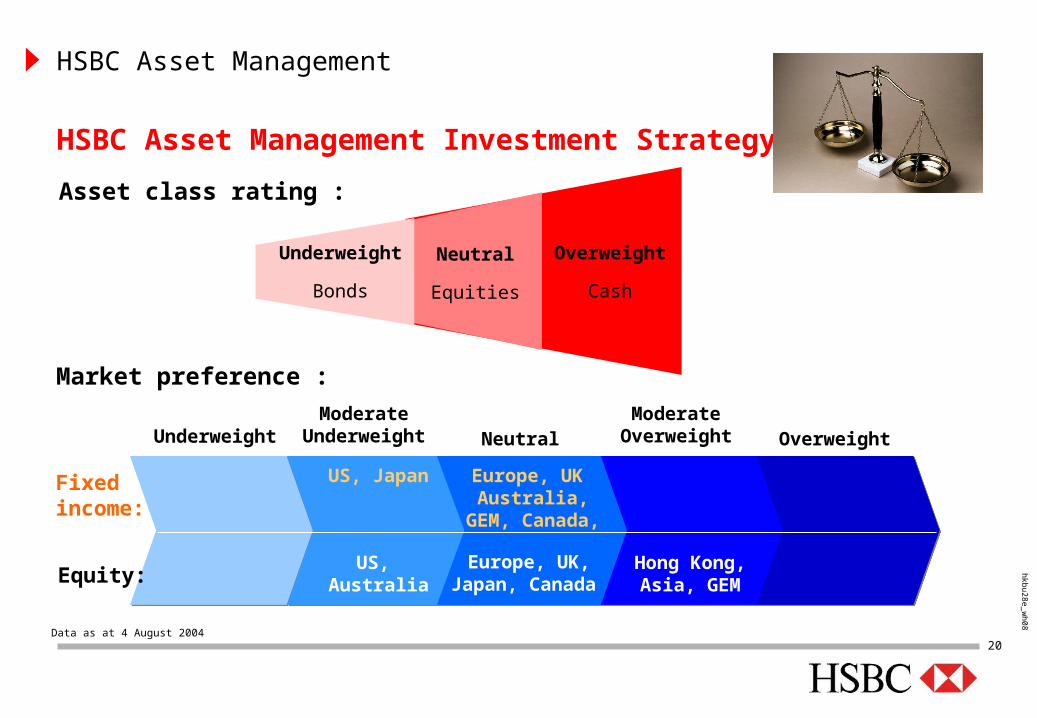

US, JapanUS, Japan Europe, UK Australia,

GEM, Canada,

Europe, UK Australia,

GEM, Canada,

Asset class rating :

HSBC Asset Management Investment Strategy

Fixed income:

Equity:

Market preference :

UnderweightModerate

Underweight NeutralModerate

Overweight Overweight

Hong Kong,Asia, GEM

Europe, UK,Japan, Canada

US, Australia

Underweight

Bonds

Neutral

Equities

Overweight

Cash

Data as at 4 August 2004

hkb

u2

8e_w

h0

8

HSBC Asset Management

21

Factors for consideration before switching

22

hkb

u2

8e_w

h0

8

HSBC Asset Management

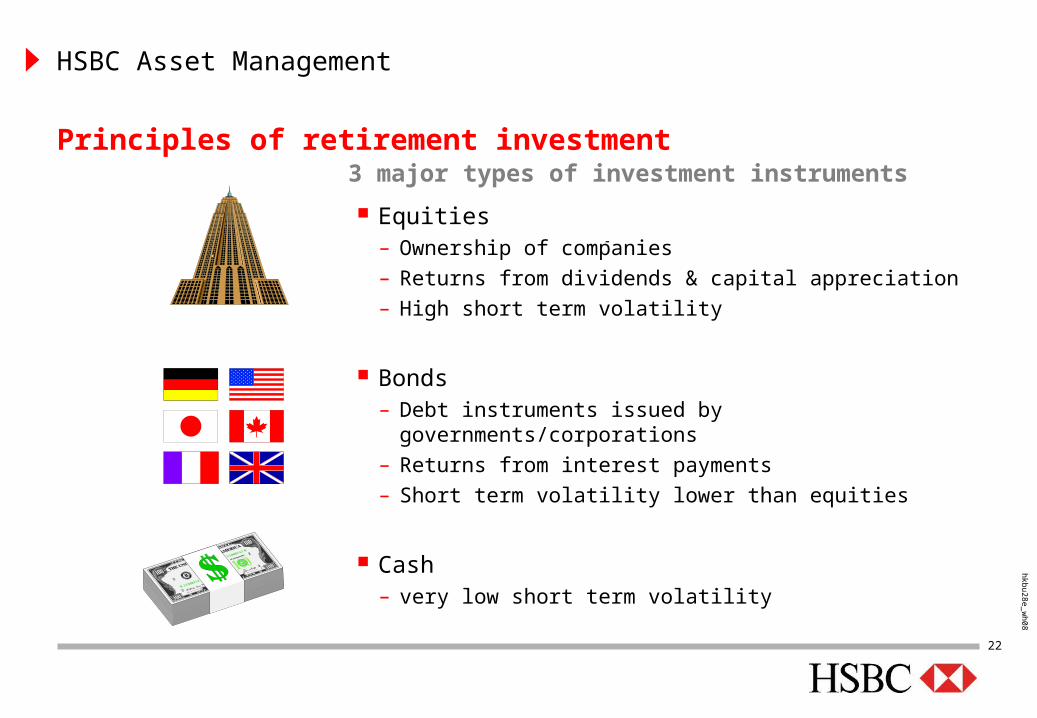

Principles of retirement investment3 major types of investment instruments

Equities– Ownership of companies

– Returns from dividends & capital appreciation

– High short term volatility

Bonds– Debt instruments issued by governments/corporations

– Returns from interest payments

– Short term volatility lower than equities

Cash– very low short term volatility

23

hkb

u2

8e_w

h0

8

HSBC Asset Management

Do not time / chase markets!Do not time / chase markets!

Please remember

Identify personal factors

– Establish risk / return profile

– Understand investment choices

– Make investment decisions using a long-term approach

24

hkb

u2

8e_w

h0

8

HSBC Asset Management

Different people have different needs!!Different people have different needs!!

A guide to investing

Factors to consider

– Years to retirement

– Other personal assets

– Planned uses for retirement assets

– Financial and other personal circumstances

25

hkb

u2

8e_w

h0

8

HSBC Asset Management

Therefore Therefore

Different people have different needs

Investment choices are provided for different risk profilesInvestment choices are provided for different risk profiles

Range of investment choices

26

hkb

u2

8e_w

h0

8

HSBC Asset Management

Explanatory notes and disclaimers

The document is confidential and is supplied to you solely for your information. This document should not be reproduced or further distributed to any person or entities, whether in whole or in part, for any purpose.

Please also note that investment involves risk and past performance is not indicative of future performance.

The opinions expressed herein should not be considered to be a recommendation by HSBC Asset Management (Hong Kong) Limited to any reader of this material to buy or sell securities, commodities, currencies or other investments referred to herein. HSBC Asset Management (Hong Kong) Limited, its ultimate and intermediate holding companies, subsidiaries, affiliates, clients, directors and/or staff may, at any time, have a position in the markets referred to herein, and may buy or sell securities, currencies, or any other financial instruments in such markets.

HSBC Asset Management (Hong Kong) Limited has based this document on information obtained from sources it believes to be reliable but which it has not independently verified. HSBC Asset Management (Hong Kong) Limited and the HSBC Group make no guarantees, representations or warranties and accept no responsibility or liability as to its accuracy or completeness. Information in this report is subject to change without notice.

27

hkb

u2

8e_w

h0

8

HSBC Asset Management

HSBC Asset Management (Hong Kong) Limited