i n g u i l d u n i building native communities guide chapter d_6... · committee for writing the...

TRANSCRIPT

Building Native CommunitiesFINANCIAL SKILLS FOR FAMILIES

Fifth Edition

INSTRUCTOR GUIDEP A R T I C I P A N T ’ S W O R K B O O K

Buildi

ng NativeCommunities

Financial Skills for Families

F O U R T H E D I T I O N

Chapter DFinancial Education Program Design

AcknowledgmentsThis 2016 version of the Building Native Communities: Financial Skills for Families - Intructor Guide was compiled and written by Krystal Langholz, Caleb Selby, Sarah Dewees, and Shawn Spruce. A debt is owed to Vickie Oldham-John and Natasha Shulman and their Advisory Committee for writing the previous edition of this guide. We thank The Rose Foundation and the Paul G. Allen Foundation for funding this project and we thank the Fannie Mae Foundation for supporting this project in its earliest phases.

In 2000, First Nations Development Institute and the Fannie Mae Foundation developed the personal financial education curriculum Building Native Communities: Financial Skills for Families. The curriculum has been revised several times, and in 2016 First Nations Development Institute and First Nations Oweesta Corporation finalized the 5th edition of the Building Native Communities: Financial Skills for Families curriculum and this Instructor Guide. First Nations Development Institute and First Nations Oweesta Corporation thank The Rose Foundation and the Paul G. Allen Foundation for funding this revision. To accompany the revised participant workbook, First Nations Development Institute and First Nations Oweesta Corporation worked with an Advisory Committee of practitioners led by Caleb Selby, Krystal Langholz, Sarah Dewees, and Shawn Spruce to create this Instructor Guide. We would like to thank the following individuals for their assistance, careful reading, and feedback: Arnold Blum, Gallup Central High School; Lisa Garcia, Salt River Financial Service Institution; Sunny Guillory, Northwest Indian College; Christopher Hansen, First Nations Oweesta Corporation; Spawn Spruce, Independent Consultant; Dawn Wesley, Tlingit-Haida Housing Authority; Tawny Wilson, First Nations Development Institute; and Shawn Winters, Chi. Ishobak, Inc. A special thanks also to TM Design for providing design and layout services.

DisclaimerAll names and examples provided in the Building Native Communities: Financial Skills for Families 5th Edition Instructor Guide are fictional. Any resemblance to actual individuals or their financial situations is coincidental. The Building Native Communities curriculum is intended to be used as guidance and should not be relied on as legal or tax advice. Please seek the counsel of a qualified attorney or tax professional for further assistance. The authors and publisher are solely responsible for the accuracy of the statements and interpretations contained in this publication.

More InformationTo obtain additional copies of this workbook, more information about training opportunities for your community, or to become a certified instructor, please visit the First Nations Oweesta Corporation website at www.oweesta.org or email [email protected]. You can also access these materials at www.BNCweb.org.

© First Nations Development Institute and First Nations Oweesta Corporation 2016.

35

Chapter D: Financial Education Program Design

for Building Native Communities: Financial Skills for Families

This chapter will provide an overview of some basic techniques you can follow to design an effective financial education program. Ideas for both planning and conducting your financial education program will be shared.

Financial Education Program Design

When creating a new financial education program or altering a pre-existing program, trainers should follow the five stages of development outlined below:

A. Needs Assessment B. Planning C. Capitalization D. EvaluationE. Report Impacts

This session will take you through each stage of the program design process and give suggestions on best practices for each.

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

36

A. Needs Assessment

A Needs Assessment is a systematic process for determining and addressing gaps between current conditions and the desired conditions. It can also help you collect information and identify the best path forward for your program. Perhaps it is known that your community needs a financial education program, but simply knowing is not enough. Documenting the specific needs and resources for financial education in your community will help ensure the success of your program. Knowing these needs and resources will be useful in several ways:

· It will help you to tailor your program to your community.

· It will help you identify community programs that you can partner with.

· It will help you identify where there is the biggest need for financial education (adults, youth, tribal employees, TANF recipients, etc.)

· It can also help you spread the word out to the community that you are starting a financial education program.

· Once you document the need, this information can be useful for fundraising.

There are many different methods of needs assessment, ranging from more to less formal.

Community ScanSome needs assessments are informal, and can be a simple community scan. You can ask the following questions of community leaders:

· Do you see a need for financial education in this community? · Who would benefit from financial education (adults, youth, tribal employees, TANF recipients,

etc.)? · Are there any financial education programs that are already in existence?· Are there any programs we could work with to offer financial education?

A Deeper Scan: Knowing Your Community Through a Market Study A market study is comprehensive research on your community that can be used to detail the intricacies of the need for financial education in your community. They engage stakeholders, potential partners, and clients. They also serve to develop broader community buy-in. Market studies almost always include detailed data collection such as surveys, interviews and secondary community data analysis. It is often then written up as a formal report.

If you don’t already have a market study for your community, you may wish to hire a consultant or identify a way to conduct your own market study for your program.

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

37

Take a moment to brainstorm…

If you already have a market study, answer the following questions…..

What kind of information was collected in the market study? Were surveys and/or interviews completed? Did these interviews capture the voices of a diverse array of community members?

How can you use the information collected in a market study to develop or expand your financial education program?

IF you don’t have a market study, identify some next steps in your needs assessment...

What are some preliminary steps you may want to take as a responsible trainer before starting a financial education program in your community?

Why is it important to take time to do, at least, a community scan?

38

B. Planning After a needs assessment has been conducted, you will have a better idea of what exactly it is that your community needs – what kind of financial education, and for whom. Now you can begin to plan a more detailed program.

The planning section of financial education program design can be split up into six different parts. Those six sections are:

· Mission and Vision · Course Development · Recruitment· Establishing Partnerships· Policies and Procedures · Goals, Objectives, and Action Planning

1. Mission and VisionAny strong organization or program has a clear mission and vision as well as the framework to carry out that mission and vision. Use the checkboxes below to make sure that you have all the necessary components of infrastructure for your financial education program. Do you have a:

· Vision Statement? o Yes o Not Yet· Mission Statement? o Yes o Not Yet

If you do not have a mission or vision statement yet, take some time to think through what the mission and vision of your program is. If you have a Board of Directors, this is a great way to get their feedback on the direction of your program. There are many resources on the internet that can help you develop a mission or vision statement. If you have difficulties composing a mission and vision statement, it can be helpful to answer the following question: What impact do you foresee your financial education program having after 10 years of existence? You can use this answer to form your vision statement. If doing this exercise as a team, it can be helpful to draw your vision together. Take a moment to brainstorm…

What will your vision statement be?

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

39

To form your mission statement, work backwards from your vision statement.

Take a moment to brainstorm…

What do you need to do to accomplish your vision? Write your mission statement here:

2. Course Development Now that you know the mission and vision for your program, you still need to develop specific lesson plans. That is to say, what content will be offered in your financial education program? A good needs assessment will have helped you identify whom the program is serving (youth, adults, TANF participants, housing authority clients, etc.) and the best way to deliver it.

Things to consider: · There are many financial education curricula in addition to the Building Native Communities:

Financial Skills for Families curriculum. Shop around to see what works for you. You can build upon work already done - you do not need to completely reinvent your financial education curriculum. Instead you can adapt an existing curriculum for use in your community.

· You can also blend existing curricula together and take the best parts of many pieces of curricula to create a curriculum that best fits your community.

Take a moment to brainstorm…

In addition to Building Native Communities, list other curricula that you can use in your financial education program.

SUGGESTED CURRICULUM COST HOW CAN I GET ONE?

First Nations Oweesta Corporation and First Nations Development Institute try very hard to make our Building Native Communities: Financial Skills for Families curriculum easily accessible and affordable. See Appendix D-1 of this session for information on ordering that curriculum.

40

Determining Your Delivery StrategyEach community has different needs and therefore demands different forms of financial education. Depending on the knowledge level and experience of your group, a session can take anywhere from an hour to a week. On average, instructors take two to three hours per session. It is your job to allow enough time for discussion and questions from your participants for each session. If you are concerned about the length or frequency of your sessions, be sure to approach participants and ask them for their opinion during breaks in between sessions. All of these needs should be considered when you choose frequency, length and location of each course.

Take a moment to brainstorm…

How long will your class take to complete? A week? A month? How often do you plan to teach? Twice per week? Twice per month?

Selecting a SiteIt is important to conduct the sessions at a site that is both comfortable and convenient for participants. Consider selecting a site with childcare available. In some communities, available childcare significantly increases participation. Another issue to consider is transportation. You may want to coordinate car-pools or find a way to ensure that the sessions are in a location that is highly accessible.

41

Take a moment to brainstorm…

Is there any specific location that will work best for your participants? If not, what is the best available choice?

Selecting Your TrainersWhen selecting trainers, it is good to find someone who has experience teaching some form of financial education, budgeting, or credit counseling. If you don’t have partners who have experience, First Nations Oweesta Corporation (Oweesta) offers periodic trainings - check their website at www.oweesta.org. These trainings offer a chance for you and your staff to become certified in teaching the BNC:FSF.

Take a moment to brainstorm…

What are some considerations when selecting trainers?

Will you be a trainer? If so, will you have a co-trainer?

42

3. RecruitmentThis section provides some ideas about how to recruit participants for your workshops. You will need to think through a variety of marketing strategies to recruit people for your class. Historically, the best marketing and recruitment strategies involve repeated communication and follow-up that is approached from a number of different perspectives.

Consider using any of the following marketing and recruitment strategies:

· Flyers. Post flyers in community facilities. Flyers can also be sent to individuals as both invita-tions and reminders about each session.

· E-mail reminders. If participants are online, send e-mails about the class. · Telephone calls. While making calls is time-consuming, nothing is more effective than speaking to

someone. Getting personal commitments and reminding community members to attend sessions is a very successful way of ensuring attendance and assessing participant’s interests and experience with personal finance.

· Newspaper or Newsletter stories. Articles can be published to introduce the program and market individual sessions. You can feature past-trainees in these articles and therefore have a commu-nity member speak on your behalf.

· Social Media. Use social networking sites like Facebook, Twitter, etc. to market your services and classes.

· Word of Mouth. Word of mouth is one of the best forms of advertising available to you. Be sure to encourage advertising by word of mouth not only through your partners but your clients as well. Ideally you have clients take your class and then pass along to other community members how much they learned and recommend your financial education program.

· Develop a community contest. Involve the community in coming up with a name for your finan-cial skills session. Publicize the contest throughout tribal media. If possible, offer a prize to the winner. The contest will get community members talking and curious about the program.

· Focus Groups. Conduct focus groups with prior participants to get feedback about classes for improvement. Ask them about when would be the best time for classes.

· Radio. If your comunity has a popular radio station, consider using that as a marketing tool.

Some instructors choose to make this curriculum part of an existing program while others develop stand-alone workshops. If your sessions are not part of an existing program, you will need to devote energy to marketing.

43

Take a moment to brainstorm…

Fill out the chart below to identify marketing strategies you will employ to promote your program, and those tactics that you will not.

MARKETING STRATEGY

WHAT WILL WORK WHAT WON’T WORK

Is there one particular form of marketing that works extremely well in your community?

Assessing Student Needs and InterestsAs participants sign up for your sessions, you may consider requiring a pre-course survey. Your preparation for sessions will be greatly enhanced if you are aware of participants’ level of knowledge about the content that you are offering. This information will help you tailor the sessions to participants’ needs. It will help you be able to talk in-depth about those subjects which you know your participants are not aware of and you can skim over sessions that participants have indicated they know sufficiently well. You may want to know if some participants may lack basic reading and math skills. All of this information can be gleaned by a pre-course survey.

4. Establishing PartnershipsDepending on your community and circumstances, you may want to partner with other organizations to offer this educational opportunity. Every partner brings different strengths to a project. Consider your program needs and which partners can fulfill those needs. For example, if you feel that you do not possess the financial skills necessary to provide detail-oriented support to participants, perhaps seeking out a partner in the banking or finance industry would be helpful. Also consider what partners stand to gain from partnering with you. Reach out to potential partners that could gain a lot by working with you. You will find that getting organizations to partner with you is much easier if partnering with you is good for their business.

Your relationship to the community is important, and it influences whether or not you need partners. If you are from outside the community, whether that means you are non-Native or have simply been outside the community for a time, you will almost certainly need to identify a community partner to help you customize your training to fit the specific needs of the target community.

44

Who Will you Partner With?You may also want to identify existing programs into which you can embed your financial education training. For example, TANF programs, housing authorities, casino human resources departments, and tribal colleges are often looking for a financial education program for their clients. Consider whether you can make your program mandatory in order to receive certain benefits such as housing assistance or per capita payments. Consider requesting permission from your tribal or organizational leadership to hold classes for employees during business hours – if people get time off work they are more likely to come to your class.

Take a moment to brainstorm…

Use the chart below to identify potential partners and to show how you will contact them.

POTENTIAL PARTNER

HOW CAN THEY SUPPORT YOUR

INITIATIVE?HOW WILL YOU

CONTACT THEM?HOW WILL THEY

BENEFIT?

Fill out the chart below to highlight the benefits of partnerships.BENEFITS

Consortium of Social ServicesSometimes a number of organizations will join together to offer a Building Native Communities: Financial Skills for Families training to their constituents. This can be particularly effective for community service organizations (e.g., social services, housing department) that can provide an incentive to their clients to attend the sessions. For instance, this program can become part of a homeownership program or a required part of living in tribal housing.

45

5. Policies and Procedures It is important to establish policies and procedures for your class. No matter how exceptional and engaging of a trainer you are, you will always have some participants who start but do not finish your classes and sessions. This can be for any number of reasons, but it is important for you to establish policies and certification standards for your classes.

Take a moment to brainstorm…

· What do I do when a participant misses a session for a legitimate reason?· Will I provide an extra day for participants who missed sessions to come in and make up what

they did not complete the first time around?· Do participants have to complete 100% of the program to receive a certificate?

The answers to these questions are not absolute; they will vary from community to community. What you decide should depend upon the weather, infrastructure in your community, community events, and many other factors. If this is a new program in your community, these questions are of the utmost importance. Inconsistency in this section will cost you and your program credibility.

6. Goals, Objectives, and Action PlanningPlanning your financial education program can be a huge task. Make sure to assign members of your team specific responsibilities so that things continue to move forward. Remember to use SMART goals as you think through next steps.

· Specific. The tasks you assign need to be narrow; do not make them broad.· Measurable. It is valuable to know how long someone has spent on a task and how much longer

it will take to finish.· Attainable. Make the tasks you assign doable. Take into account the capability of the staff person

you have assigned the project to.· Relevant. The task must be worthwhile to your program. · Time-bound. Assign a due date to have each task done.

However, don’t let the enormity of the task overwhelm you! It is always possible to start small with a simple to-do list, offering just one class to gauge community response. Feel free to use the action steps workbook featured below, or the digital version that can be found in your trainer’s toolkit, to do your planning.

Take a moment to brainstorm…

46

Use the following table to assign tasks to yourself or to staff memeber. ACTION STEPS SAMPLE WHO WHEN

1.

2.

3.

4.

5.

6.

7.

RESOURCES

Staff:

Consultant:

Equipment:

Budget:

NOTES

47

III. Capitalization

This section will cover some ideas about how to raise money for your program. Fundraising is a complicated process, but this section provides you with a few pointers.

Starting a financial education program from scratch can be very expensive. While you may have considered staff time as a cost, the reality is that the costs are much more diverse than that. For example, what does it cost to have meals provided at your trainings? What will it cost to conduct a market study?

Use the table below to list the costs necessary to get your financial education program off the ground. Do these costs fit your budget?

EXPENSE COST

Meals $300

Childcare ??

Snacks ??

Incentives & Items to Give Away ??

Total Estimated Cost ??

Now that you have estimated the cost to run your financial education program you must decide how to cover those costs. Does your organization already have a budget for this? Below is a list of organizations you can approach to ask for funding or donations for your program:

· Grants· Foundations· Fundraisers· Financial Institutions· Community Colleges· Tribal Enterprises· Federal, state and local programs· Schools

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

48

Take a moment to brainstorm…

Are there any unique resources in your community that can function as a funder or donate items for your program?

Elevator SpeechOne very important aspect of capitalization is having an effective elevator speech. An elevator speech is a practiced and effective 30 seconds or less pitch to someone who may be interested in funding your program. It is not a ‘one-size-fits-all’ pitch, but rather a general idea; you should present it differently depending on who you are talking to (Tribal council member, elder, foundation, etc.).Write a short elevator speech below that you can use to describe your program to others.

49

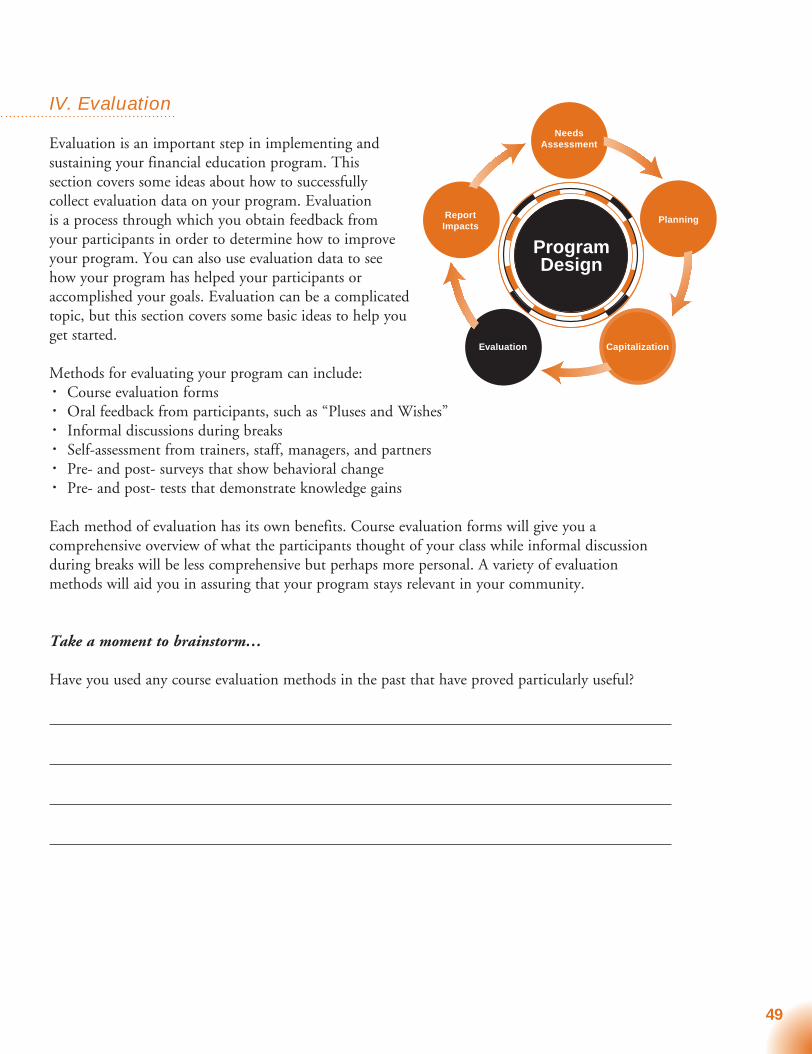

IV. Evaluation

Evaluation is an important step in implementing and sustaining your financial education program. This section covers some ideas about how to successfully collect evaluation data on your program. Evaluation is a process through which you obtain feedback from your participants in order to determine how to improve your program. You can also use evaluation data to see how your program has helped your participants or accomplished your goals. Evaluation can be a complicated topic, but this section covers some basic ideas to help you get started.

Methods for evaluating your program can include: · Course evaluation forms· Oral feedback from participants, such as “Pluses and Wishes” · Informal discussions during breaks· Self-assessment from trainers, staff, managers, and partners · Pre- and post- surveys that show behavioral change· Pre- and post- tests that demonstrate knowledge gains

Each method of evaluation has its own benefits. Course evaluation forms will give you a comprehensive overview of what the participants thought of your class while informal discussion during breaks will be less comprehensive but perhaps more personal. A variety of evaluation methods will aid you in assuring that your program stays relevant in your community.

Take a moment to brainstorm…

Have you used any course evaluation methods in the past that have proved particularly useful?

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

50

Do you feel that a particular method of evaluation is vital to your programs longevity?

Pluses and Wishes “Pluses and Wishes” is an exercise that assures that you get feedback from your participants regarding what they enjoy in your program and what they hope for in the coming sessions. It also provides a way to close out each session. You can even draw the table below on a page of your flip chart so that when a session ends you simply flip to that page. Conduct the pluses and wishes exercise thereby obtaining feedback on the day’s session and suggestions for improvement in the upcoming sessions.

Pluses Wishes+ -

51

Qualitative and Quantitative DataThere are two general forms of evaluation: · Qualitative data is best described as descriptive data. It is often the stories behind the individu-

als in your programs. · Quantitative data is often numerical. It is data that can be represented in charts and graphs,

and is easier to analyze than qualitative data. With quantitative data, you can produce sentences like “30% of the individuals who take our classes increase their credit score within a year.”

Both categories of data are important in evaluation. Qualitative data does not tell the whole story on its own, and neither does quantitative data. Together they are more comprehensive. Funders will be more willing to fund your program if you are armed with qualitative and quantitative data. When you are designing surveys and exercises, make sure that you are providing space for the collection of both forms of data.

Take a moment to brainstorm…

What types of surveys and exercises can be conducted to ensure that you collect both forms of data?

What questions can you ask in your surveys that will aid you in reporting impact?

52

IndicatorsIndicators are measures of what you are trying to change. An indicator is a specific, observable and measurable characteristic that can be used to show changes, or progress a program is making toward achieving a specific outcome or goal.

Here are some ideas for indicators you may wish to track for your financial education program: · Increase in participant FICO scores. · Increase in savings rates or number of Individual Development Accounts opened.· Number of participants who become homeowners or start small businesses. · Amount of debt reduction.

These are general indicators and your community may have an indicator that funders find particularly appealing. Whatever the case may be, you should do two things when deciding which indicators you want to measure:

1) Record a benchmark so that you have a starting point to compare to, and 2) Create a client intake and tracking system which allows you to collect and monitor data to measure increase in financial management skills and changes in participant behavior.

Ultimately, funders are interested in behavior change of your participants. It is important to think about how you will track that, and other indicators, before you even begin teaching.

Data Collection TechniquesLongitudinal assessment, or the repeated gathering of data from the same individuals over time, is a powerful tool. We recommend client surveys at the following timeframes:· Surveys filled out before a training. · Surveys filled out at the conclusion of training.· Surveys filled out 6 months or 1 year after training.

Compare the differences on key indicators, measuring the increase in knowledge or change in behaviors from your baseline.

Different Uses of EvaluationEvaluation data can be used for different things: · To improve your teaching. · To track progress or results. · To measure change or impact.

Here are some examples: 1) Evaluation Response: “You did not spend enough time during class on the budgeting exercise.”

Action: Modify and improve course delivery.

53

2) Tracking Results: “We trained 57 tribal members in financial education basics this year.”

Action: Compare this data to your goals – Did you educate as many people as you wanted to? Report program results to funders, Tribal council, board of commissioners, etc. By highlighting impacts of the program to other potential funders you are making a case that the program is worthy of investment.

3) Measuring Impact: “As a result of our program, participants increased their credit scores by an average of 20 percent over the previous year.”

Action: Compare this data to your goals – Did your clients improve their scores as much as you expected? If not, do you need to provide additional support services such as credit coaching?

V. Report Impacts

Community leaders, funders, potential funders, partners and sponsors will want to know the effectiveness of your program and the short-term and long-term impact that it has had. It is therefore vital that you find a way to record and report this impact. So often, we get so wrapped in up in doing our great work, and we forget to communicate our successes. Remember to allocate time and resources to recording, sharing, and celebrating your successes! If your evaluation plan was set up with the reporting of impacts in mind, the logistics of reporting your impacts are simple. All you have to do is let the data talk for itself. You should, however, know that there are many different ways you can report the results of your program:

· Newsletters. If your organization has a newsletter, consider having a section of that newsletter focus on your financial education program. You can share the success stories of your program in your newsletter. If your organization does not already have a newsletter, you can start one that goes out monthly, quarterly, or annually to clients, partners, and community members. What-ever the case may be, make sure to include qualitative and quantitative data in your stories about your program. If possible, include a quote from a client and important data points like number of participants certified in that respective period of time and improved credit score of partici-pants that have successfully completed your class.

· Annual Reports. Annual reports are far more comprehensive than newsletters. They offer read-ers in-depth analysis on not only successes, but areas you intend to improve in your financial education program next year. Your annual report should contain one clear message: my finan-cial education program was effective in carrying out its mission statement. How you intend to prove that statement is up to you. Just as with the newsletters, first-person testimonies are very important. It is easy to forget qualitative data in annual reports, but important that you do not. Finally, be sure to thank funders in these reports. It is likely that they will read your report.

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

54

· Success Stories. One of the most effective ways to document the impact your program has is to follow a participant from start to finish. Meet with a participant before s/he goes through your program. Gather information from that participant with a pre-test, survey, or interview. Note the financial problems and questions that your participant has reported. If possible, document what the participant thinks of your class, and what positive things they have to say about the class. Be sure to record the participation and attendance rate of that participant relative to other participants. Record the test scores of that participant and track the financial indicators of that participant at staggered time intervals after the class. Hopefully, you will have a powerful and moving story to tell about someone who learned financial skills and was able to get out of debt, help their family, or change their life for the better. This type of personal impact reporting can only benefit your program. Success stories are great to go in annual reports or newsletter once approved by the participant.

Wrap Up

Remember, program planning is an iterative process. Your financial education program is never perfect. As you hear back from your clients, you will learn what tweaks to make to your classes. You will travel around this circle many times, and have many opportunities to collect information to improve your program. This will lead to a more successful program over time, and eventually a chance to report all the successes of your financial education program!

NeedsAssessment

PlanningReport Impacts

CapitalizationEvaluation

Program Design

55

Appendix D-1

Appendix D-2

Templates for SurveysFirst Nations Oweesta Corporation has a Trainers Portal that is a great resource for trainers who are a part of a financial education program in their own communities. To enter this portal, you will first have to have become certified in Building Native Communities curriculum. Your certificate number will function as a password to the portal which contains numerous surveys and supporting documents.

Visit this portal for: · Course Evaluation Surveys. · Pre- and Post-Assessment Surveys. · Follow-up Surveys at the 6 week, 6 month, and 1 year intervals. · Sample PowerPoints.· Sample Games

Building Native CommunitiesFINANCIAL SKILLS FOR FAMILIES

Fifth EditionPARTICIPANT’S WORKBOOK

P A R T I C I P A N T ’ S W O R K B O O K

Buildin

g Native Communities

Financial Skills for Families

F O U R T H E D I T I O N

Ordering Instructions forBuilding Native Communities: Financial Skills for Families

· Call Oweesta at 303-774-8838 to order or order on First Nations website, www.firstnations.org.

· The cost is $10 per book; shipping is covered in the price.

· Typically shipped in batches of 25 booklets.

56

Appendix D-3

Readiness Checklist for Trainers Are you ready?

For Community-based Classes:o Have you talked with your community contact to arrange the session? Do any of the

participants have special needs (e.g. wheelchair access, hearing impaired)?o Have you arranged for snacks or coordinated a potluck meal for the session?o Are you sure that the facility meets your needs? Does the room have electrical outlets? o Are there tables and chairs? Are you going to have the space to yourself during the session?o Have you sent flyers to potential participants?o Have you posted flyers in the community? Have you done adequate marketing?o Do you have an agenda that lists the curriculum purpose and the session objectives?o Do you have a participant sign-in sheet?o Do you have an evaluation form for the session?o Is someone ready to lead the group in an opening prayer, if appropriate?

For all Trainers:o Have you reviewed the session?o Have you practiced your presentation?o Have you collected traditional examples from your communities for this session?o Have you prepared all needed PowerPoint slides or overheads for this session?o Are you prepared to facilitate the session?o Have you selected an icebreaker?o Have you selected an introductory exercise?o Are the discussion questions pre-written on a flip chart?o Do you have an annotated agenda?