ian p. da costa, manager ucla/ucop/ucm accounts payable new procurement card process

TRANSCRIPT

Ian P. Da Costa, ManagerUCLA/UCOP/UCM Accounts Payable

New Procurement Card Process

Agenda

• Introduction•Responsibilities•Understanding System Logic•Navigating the System•PAN Notice•Processing Credits•Example•System Generated E-mails•Common Vendors•Sales & Use Tax Rules•Q & A

Introduction

•Data feed from bank pre-populates a CatBuy cart

•Banking system responsible for income tax reporting

• Process will temporarily exempt vendors from the upcoming 3% withholding requirement for a certain time period

•Expenses hit the ledger in a timely manner•Not subject to the $500 reimbursement limit• Immediate accruals of use tax •Sampling methodology for auditing•Expand program without additional staffing

Responsibilities•Cardholder or preparer allocates the

transactions in CatBuy•Cardholder or preparer is responsible for

identifying taxable and non-taxable components of a transaction

•Department managers are encouraged to ensure that tax reporting is accurate

•Central units will perform sample audits for compliance

•Department is responsible for assessments

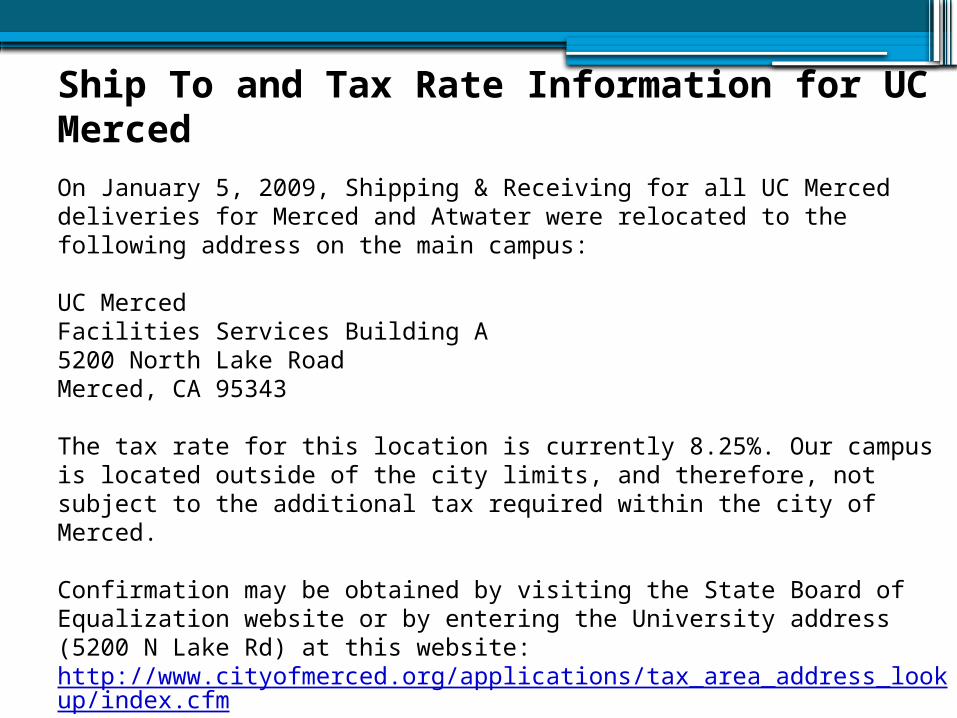

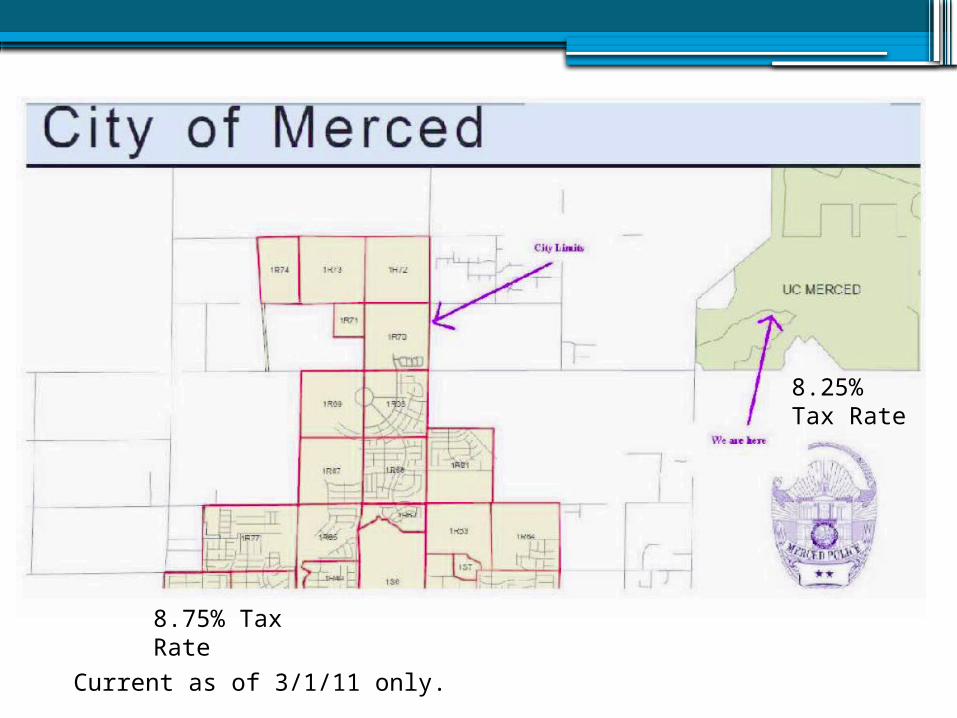

Ship To and Tax Rate Information for UC Merced

On January 5, 2009, Shipping & Receiving for all UC Merced deliveries for Merced and Atwater were relocated to the following address on the main campus:

UC MercedFacilities Services Building A5200 North Lake RoadMerced, CA 95343

The tax rate for this location is currently 8.25%. Our campus is located outside of the city limits, and therefore, not subject to the additional tax required within the city of Merced.

Confirmation may be obtained by visiting the State Board of Equalization website or by entering the University address (5200 N Lake Rd) at this website: http://www.cityofmerced.org/applications/tax_area_address_lookup/index.cfm(This link will validate that our address is not within the city limits.)

Please update your database/files with the correct tax rate. Also, reference Purchase Order Numbers on all shipments to ensure delivery to the right location.

8.75% Tax Rate

8.25% Tax Rate

Current as of 3/1/11 only.

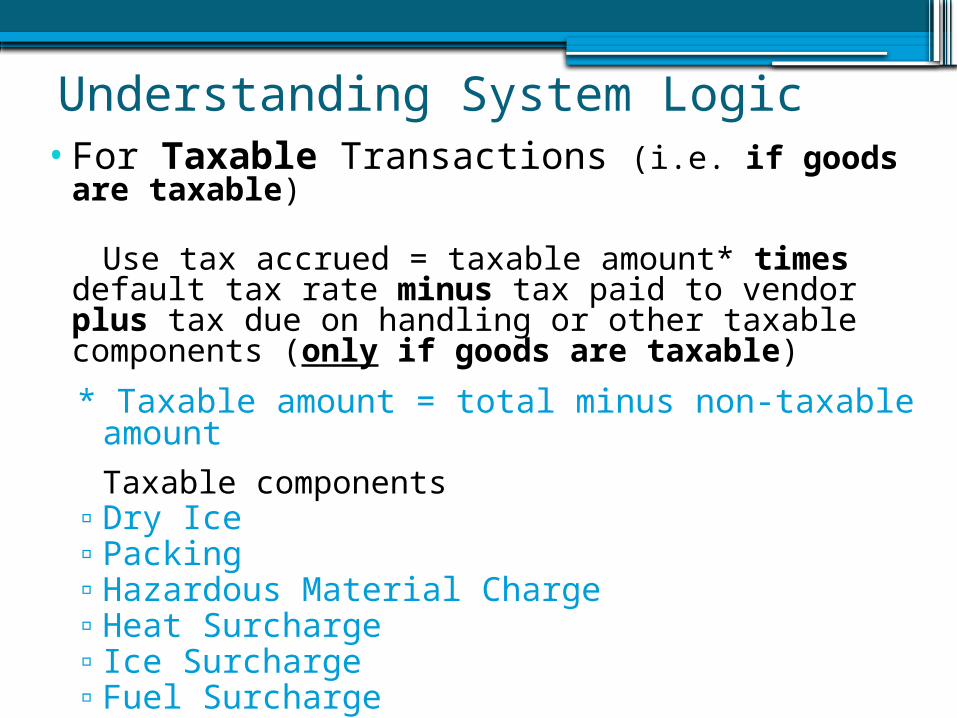

Understanding System Logic•For Taxable Transactions (i.e. if goods are

taxable) Use tax accrued = taxable amount* times default

tax rate minus tax paid to vendor plus tax due on handling or other taxable components (only if goods are taxable)

* Taxable amount = total minus non-taxable amount

Taxable components▫Dry Ice▫Packing▫Hazardous Material Charge▫Heat Surcharge▫ Ice Surcharge▫Fuel Surcharge▫P & H

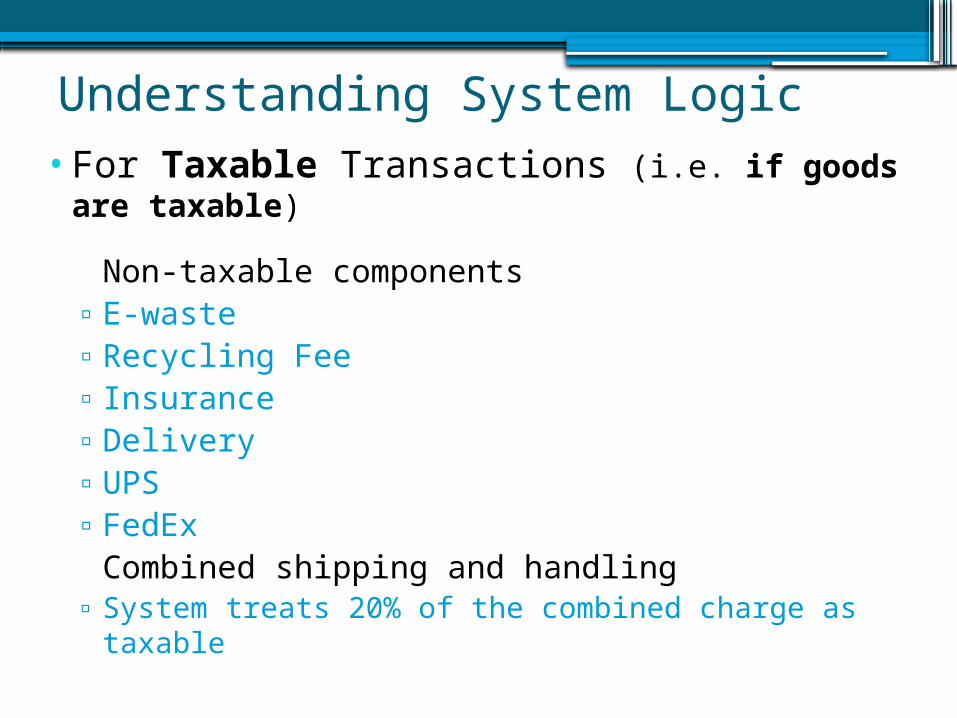

Understanding System Logic•For Taxable Transactions (i.e. if goods are

taxable)

Non-taxable components▫E-waste▫Recycling Fee▫ Insurance▫Delivery▫UPS▫FedEx

Combined shipping and handling ▫ System treats 20% of the combined charge as taxable

Navigating the System

• Select PCard Transactions

Navigating the System

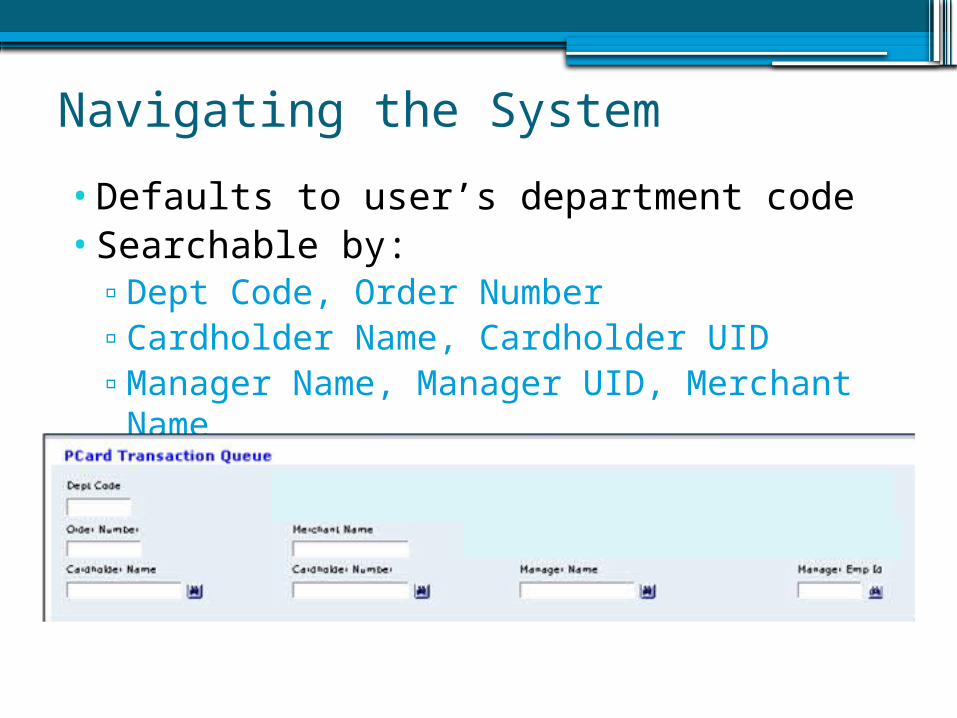

•Defaults to user’s department code•Searchable by:▫Dept Code, Order Number▫Cardholder Name, Cardholder UID ▫Manager Name, Manager UID, Merchant

Name

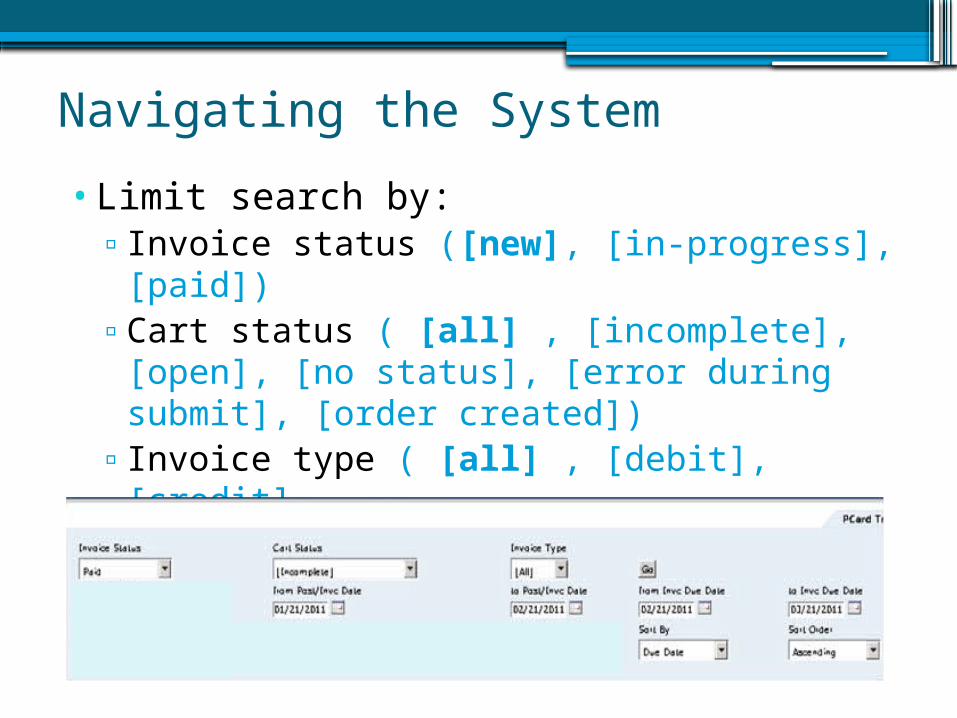

Navigating the System

•Limit search by: ▫Invoice status ([new], [in-progress], [paid]) ▫Cart status ( [all] , [incomplete], [open], [no

status], [error during submit], [order created])

▫Invoice type ( [all] , [debit], [credit]▫Date ranges ([Post/Invc Date to], [Post/Invc

Date from] and/or [Invc Due Date] to [Invc Due Date])

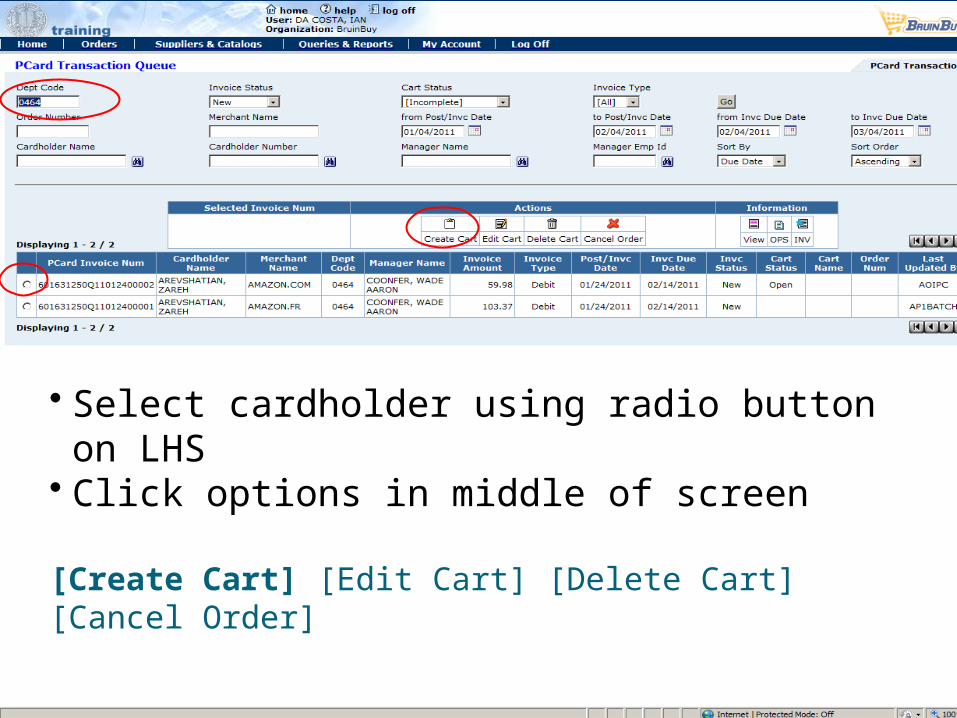

• Select cardholder using radio button on LHS• Click options in middle of screen

[Create Cart] [Edit Cart] [Delete Cart] [Cancel Order]

Navigating the System

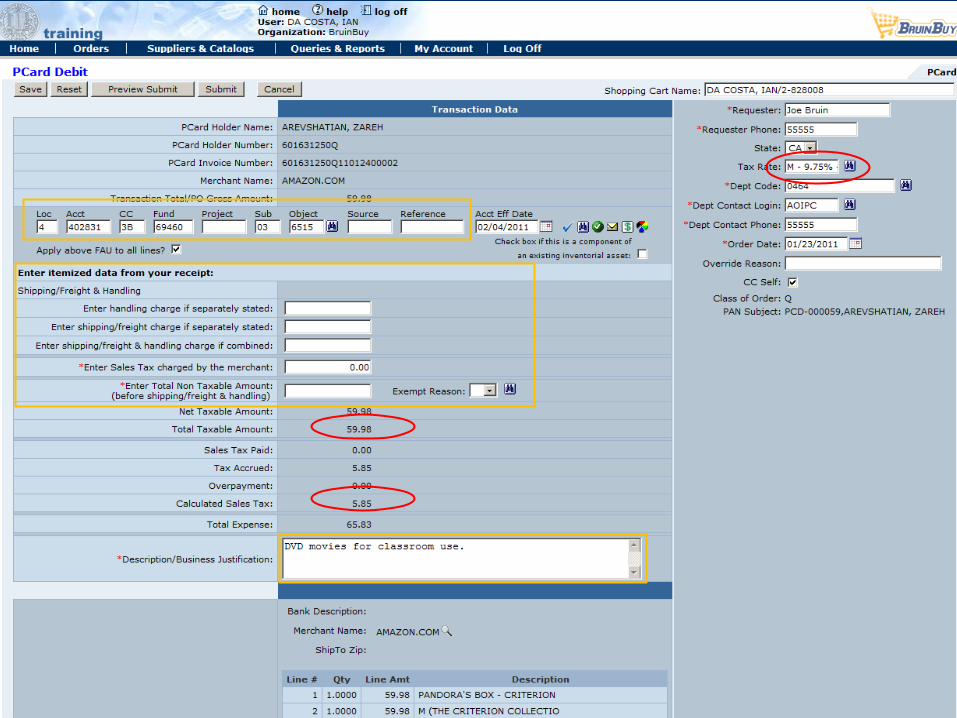

•Check preparer defaults

Requester: Requester Phone: State: Tax Rate: Dept Code: Dept Contact

Login: Dept Contact

Phone:

Navigating the System

•Change defaults as neededOrder Date: [today’s date]

[calendar]Override Reason: CC Self: Class of Order: Q PAN Subject: PCD-000007,CAT, JANE

•Remember tax calculations are based on defaults for preparer

•Change tax rate if creating orders for cardholders in different districts (i.e. location of where goods will be used)

Navigating the System

BRUIN, JOE

• Adjust FAU and enter correct object code

Navigating the System

Navigating the System

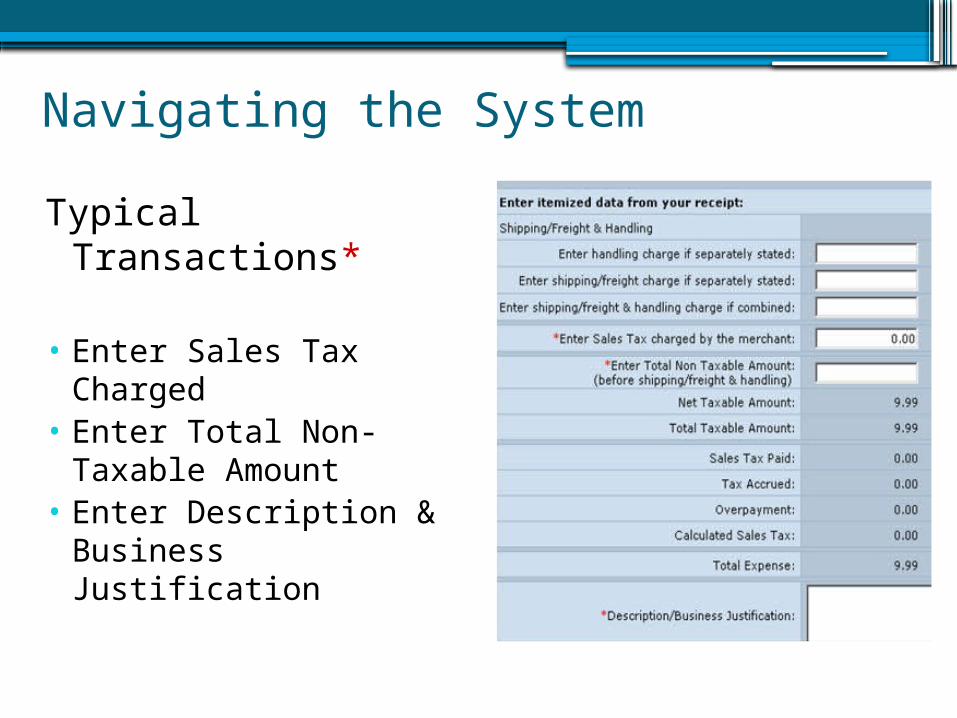

Typical Transactions*

• Enter Sales Tax Charged• Enter Total Non-Taxable

Amount• Enter Description &

Business Justification

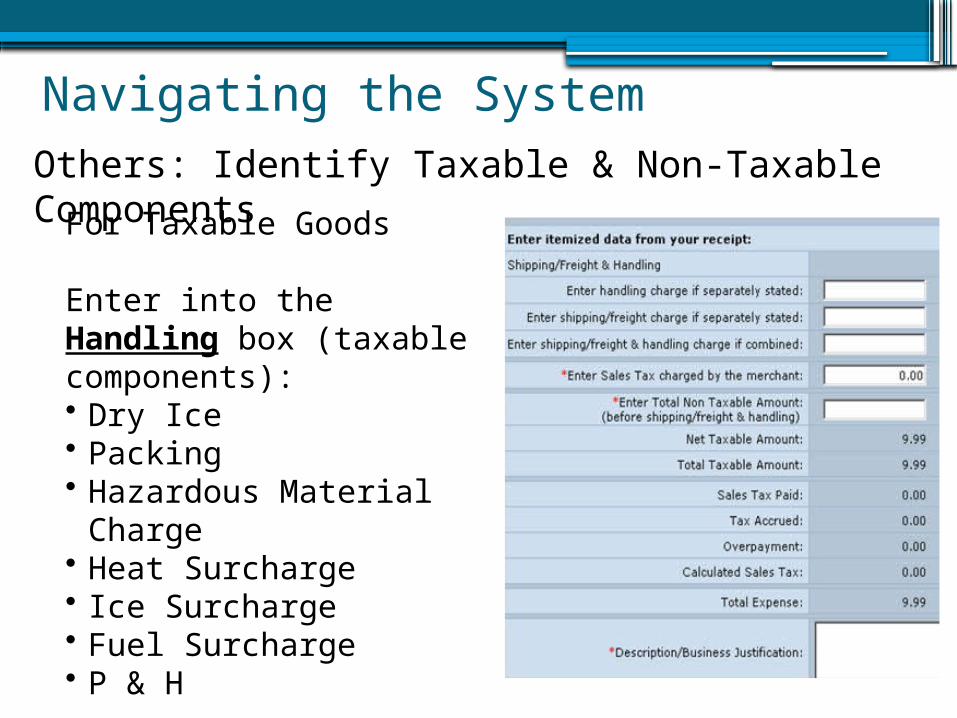

Navigating the SystemOthers: Identify Taxable & Non-Taxable Components

For Taxable Goods

Enter into the Handling box (taxable components):• Dry Ice• Packing• Hazardous Material

Charge• Heat Surcharge• Ice Surcharge• Fuel Surcharge• P & H

Navigating the System Others: Identify Taxable & Non-Taxable Components

For Taxable Goods

Enter into the Shipping/Freight box (nontaxable components):• E-waste• Recycling Fee• Insurance• Delivery• UPS• FedEx

Navigating the System Others: Identify Taxable & Non-Taxable Components

For Non-Taxable Goods

• Enter amount in Non-Taxable Box• Select Exempt Reason Code

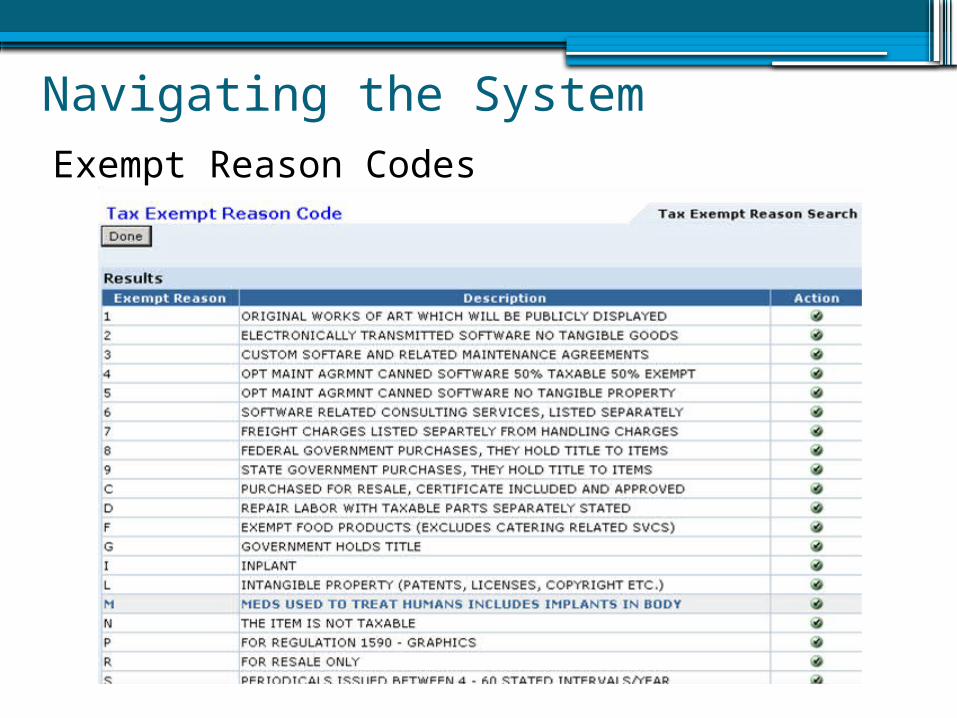

Navigating the System Exempt Reason Codes

Navigating the System• Review the Transaction

• Click [Save] and then [Submit]

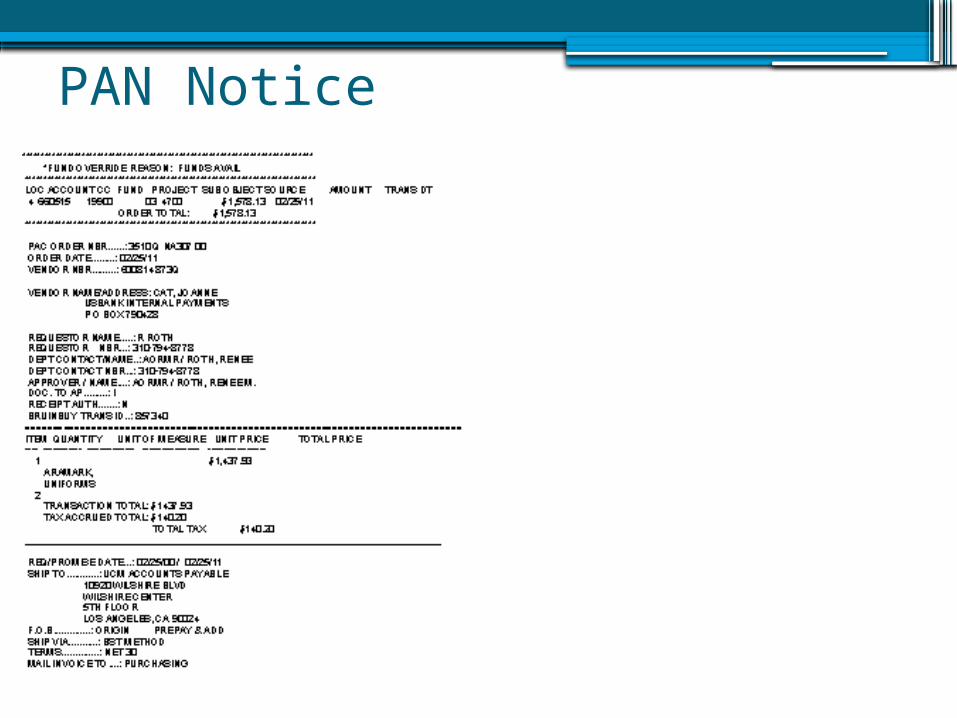

PAN Notice

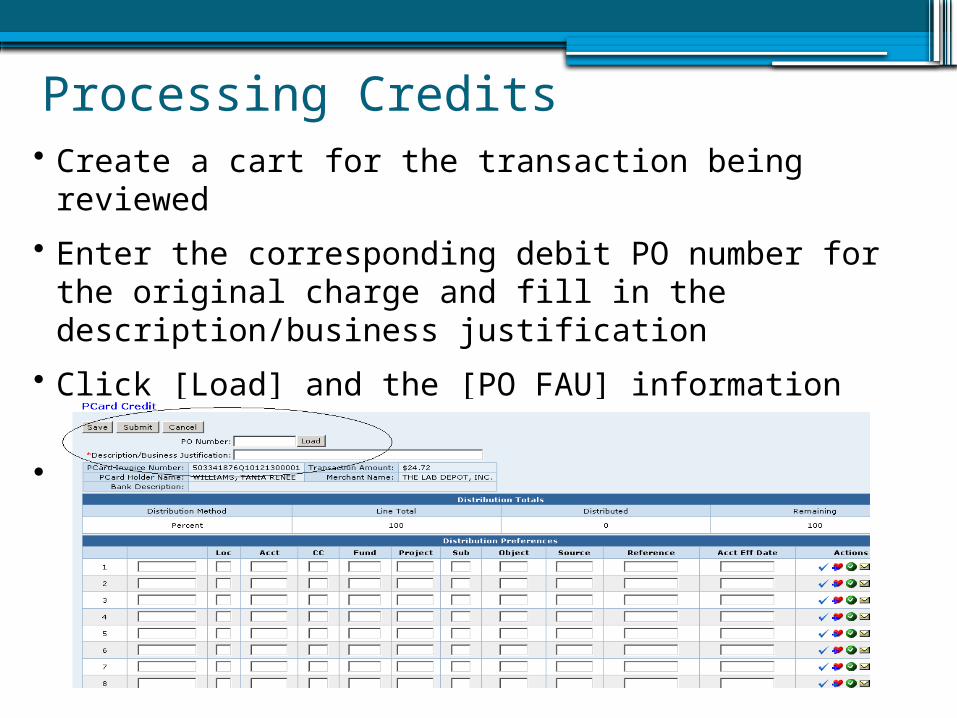

Processing Credits• Create a cart for the transaction being reviewed

• Enter the corresponding debit PO number for the original charge and fill in the description/business justification

• Click [Load] and the [PO FAU] information will be populated

• Click [Save] and [Submit]

ExampleLocal stores in same district should charge the correct rate

• Identify taxable transactions▫T (other variations)

• Identify non-taxable transactions▫N or F (other variations)

•Some vendors provide taxable or non-taxable sub-totals•Calculate the non-taxable portion (note: maybe faster to add taxable items and subtract from the total)

Sample System Generated E-mails

• RE: Create Cart for Pcard debit transactionU.S. Bank has transmitted a Visa credit card transaction to UCM for payment into the Pcard Transaction Queue. Pcard procedures require the cardholder/preparer to create a cart in the CatBuy system within three business days, or preferably immediately upon receipt of this email. Please remember to provide sufficient detail of the purchase for business justification on the order. Thank you.

• RE: Enter order for Pcard credit transactionU.S. Bank has issued a credit in the amount shown in your Pcard Transaction Queue. Go to your Pcard Transaction Queue, select the credit, and enter the Order Number associated with the original debit charge within three business days of receipt of this email. Thank you.

• RE: Debit applied with default FAUThe default FAU specified in your Pcard user profile was debited for a transaction that did not have a "Q" class order created in your Pcard Transaction Queue. Pcard controls require "Q" class orders to be created in CatBuy to validate appropriate accounting information and provide business justification. Pcard Administration will be contacting you shortly for follow-up action. Thank you.

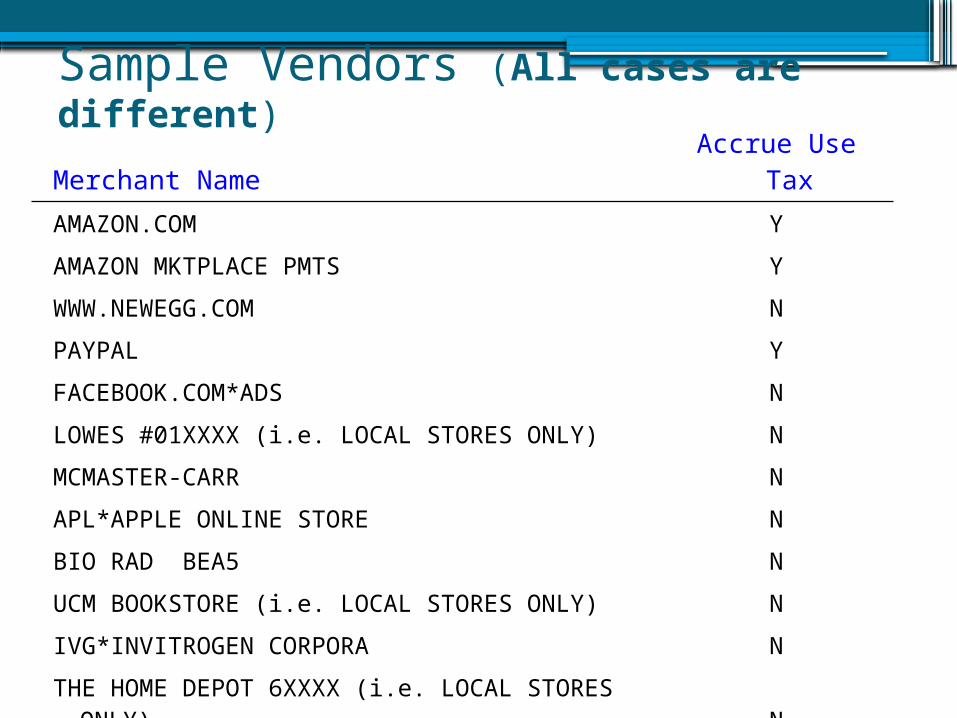

Sample Vendors (All cases are different)Merchant Name Accrue Use Tax

AMAZON.COM Y

AMAZON MKTPLACE PMTS Y

WWW.NEWEGG.COM N

PAYPAL Y

FACEBOOK.COM*ADS N

LOWES #01XXXX (i.e. LOCAL STORES ONLY) N

MCMASTER-CARR N

APL*APPLE ONLINE STORE N

BIO RAD BEA5 N

UCM BOOKSTORE (i.e. LOCAL STORES ONLY) N

IVG*INVITROGEN CORPORA N

THE HOME DEPOT 6XXXX (i.e. LOCAL STORES ONLY) N

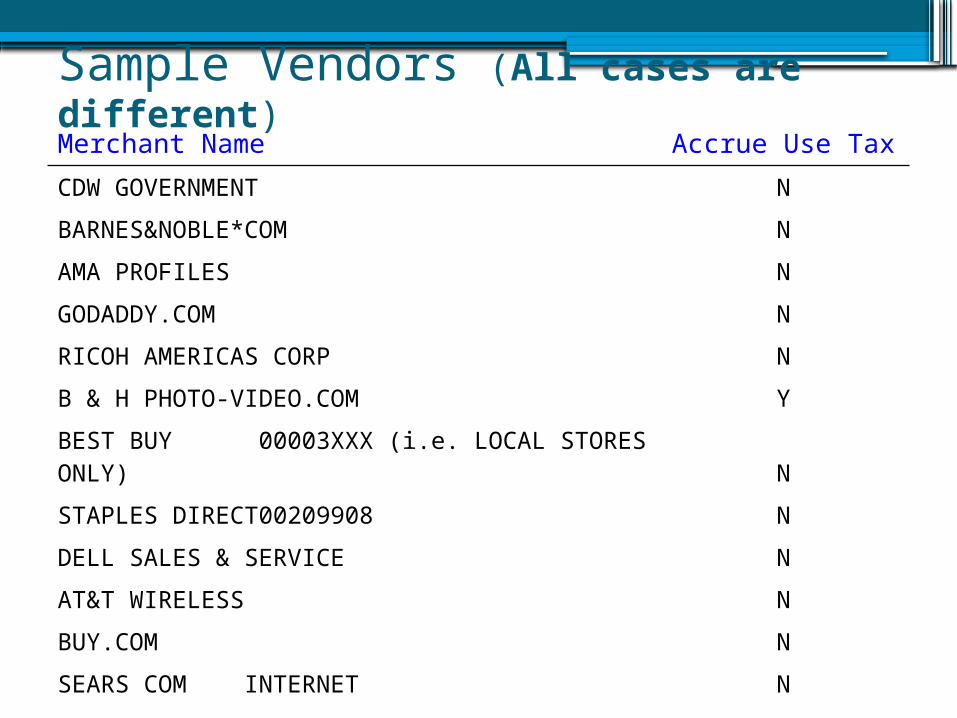

Sample Vendors (All cases are different)Merchant Name Accrue Use TaxCDW GOVERNMENT NBARNES&NOBLE*COM NAMA PROFILES NGODADDY.COM NRICOH AMERICAS CORP NB & H PHOTO-VIDEO.COM YBEST BUY 00003XXX (i.e. LOCAL STORES ONLY) NSTAPLES DIRECT00209908 NDELL SALES & SERVICE NAT&T WIRELESS NBUY.COM NSEARS COM INTERNET N

Erica Fernandez, Tax Director

Sales and Use Tax

Sales and Use Tax

•Sales tax ▫Imposed on every retailer (seller) for the

privilege of making retail sales of tangible personal property (TPP) in CA

•Use tax ▫Imposed on the purchaser for the storage,

use or consumption of TPP in CA

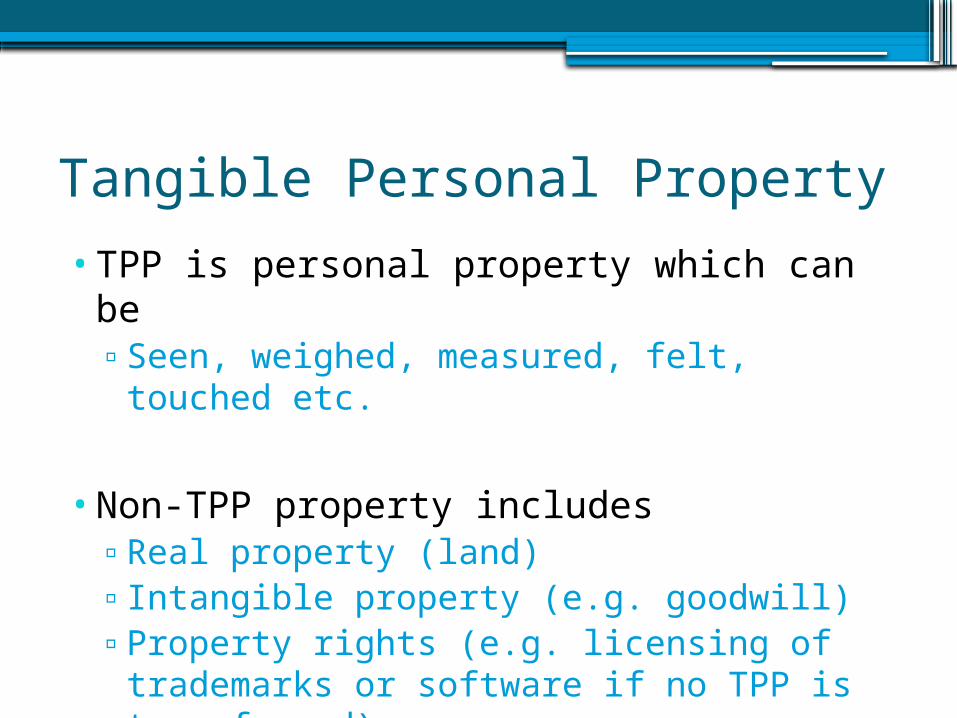

Tangible Personal Property

•TPP is personal property which can be▫Seen, weighed, measured, felt, touched etc.

•Non-TPP property includes▫Real property (land)▫Intangible property (e.g. goodwill)▫Property rights (e.g. licensing of trademarks

or software if no TPP is transferred)

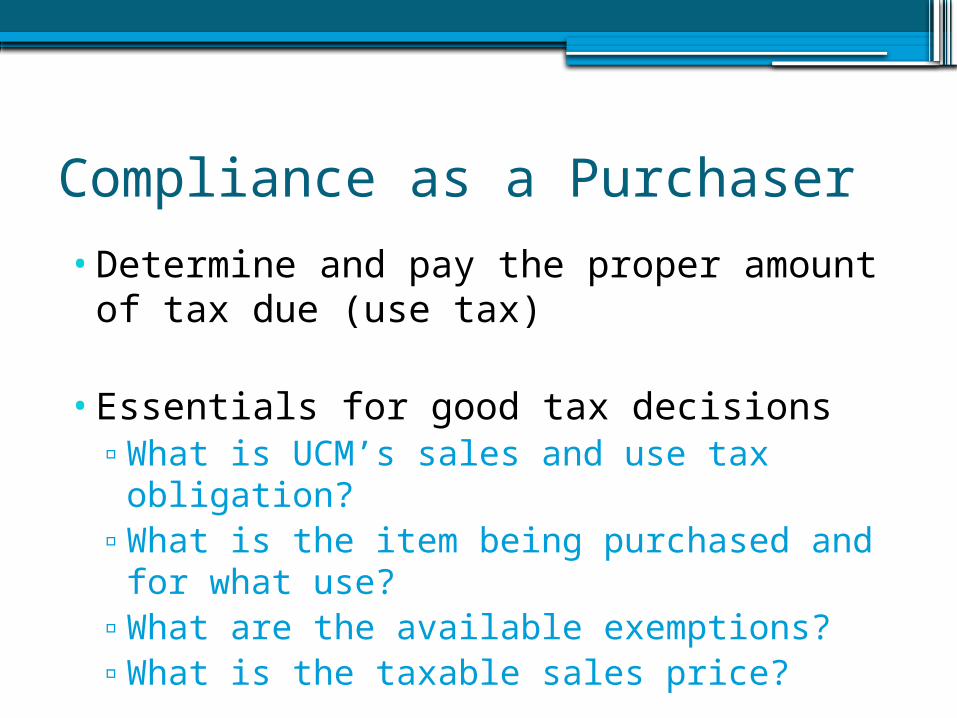

Compliance as a Purchaser

•Determine and pay the proper amount of tax due (use tax)

•Essentials for good tax decisions▫What is UCM’s sales and use tax obligation?▫What is the item being purchased and for

what use?▫What are the available exemptions?▫What is the taxable sales price?

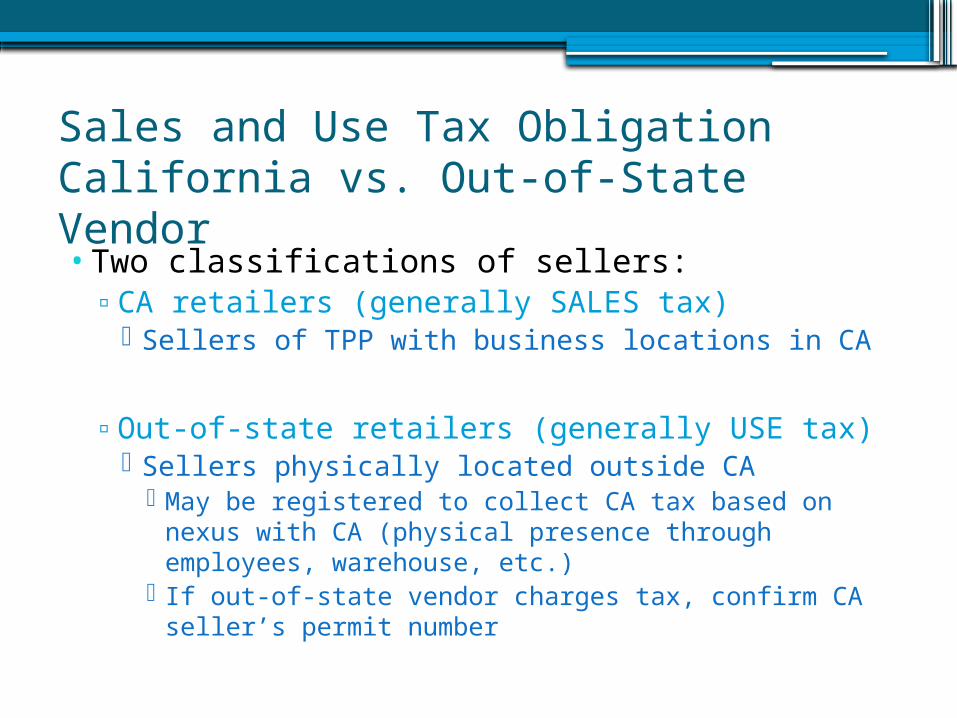

Sales and Use Tax ObligationCalifornia vs. Out-of-State Vendor•Two classifications of sellers:▫CA retailers (generally SALES tax)

Sellers of TPP with business locations in CA

▫Out-of-state retailers (generally USE tax) Sellers physically located outside CA

May be registered to collect CA tax based on nexus with CA (physical presence through employees, warehouse, etc.)

If out-of-state vendor charges tax, confirm CA seller’s permit number

Sales and Use Tax ObligationCalifornia vs. Out-of-State Vendor (cont)• The purchase of TPP from a retailer (not registered

to collect CA taxes) for use in CA is subject to use tax

• Identifying use tax transactions:• Vendor has non-CA address• Invoice is for tangible property• Charge for shipping indicating something was shipped

• Note – purchases from other states or their instrumentalities, including state universities are not subject to sales and use tax.

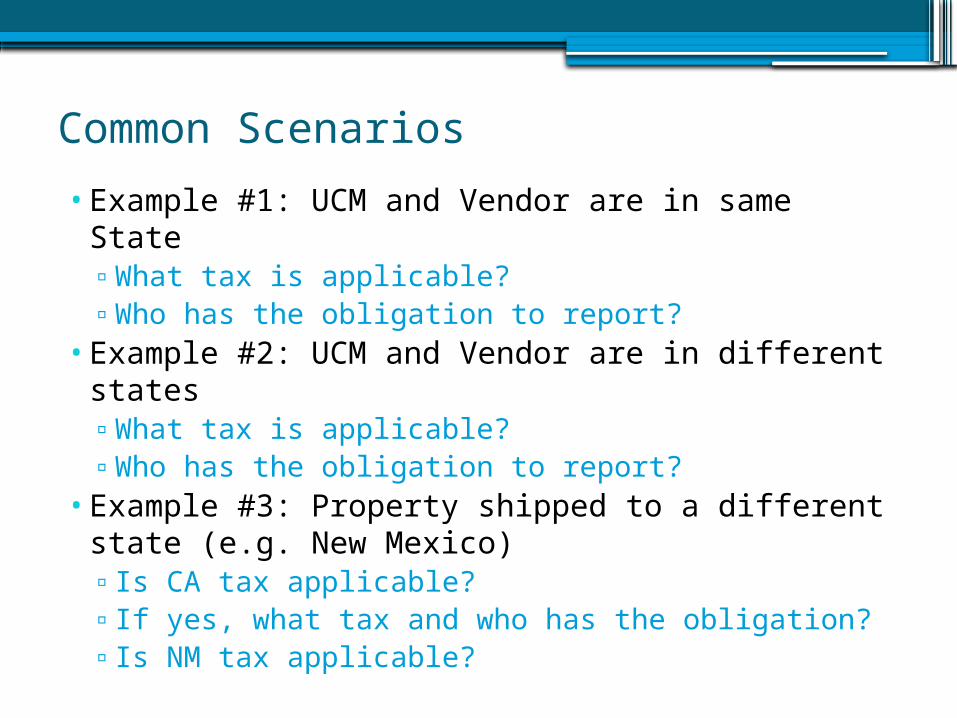

Common Scenarios

•Example #1: UCM and Vendor are in same State▫What tax is applicable?▫Who has the obligation to report?

•Example #2: UCM and Vendor are in different states▫What tax is applicable?▫Who has the obligation to report?

•Example #3: Property shipped to a different state (e.g. New Mexico)▫Is CA tax applicable?▫If yes, what tax and who has the obligation?▫Is NM tax applicable?

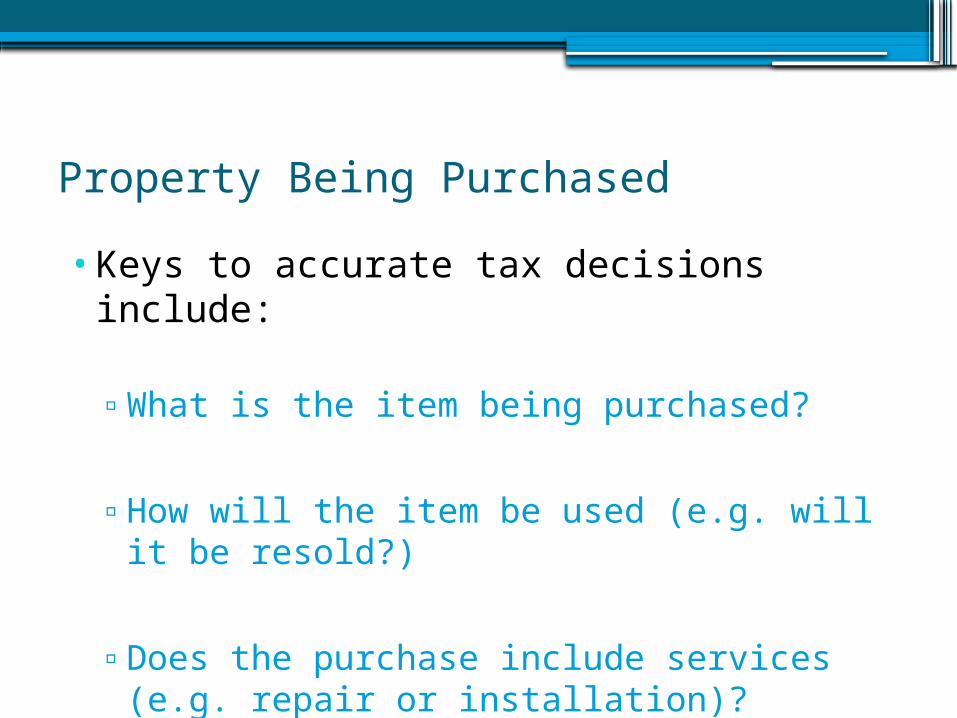

Property Being Purchased

•Keys to accurate tax decisions include:

▫What is the item being purchased?

▫How will the item be used (e.g. will it be resold?)

▫Does the purchase include services (e.g. repair or installation)?

Determining the .0000000000000000000000000000000000000001

Taxable Gross Receipts (Sales Price)

111

…………………..1……………..0000000000000000000……….Correct Amount of Tax

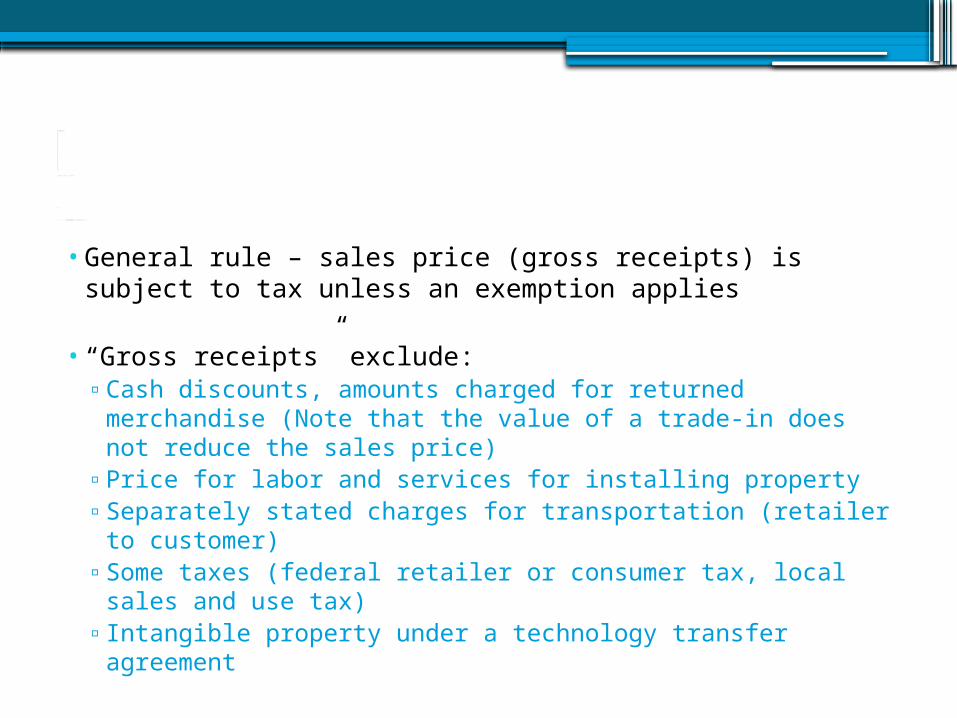

• General rule – sales price (gross receipts) is subject to tax unless an exemption applies

• “Gross receipts” exclude:▫ Cash discounts, amounts charged for returned

merchandise (Note that the value of a trade-in does not reduce the sales price)

▫ Price for labor and services for installing property▫ Separately stated charges for transportation (retailer to

customer)▫ Some taxes (federal retailer or consumer tax, local sales

and use tax)▫ Intangible property under a technology transfer agreement

Exemptions

•Common exemptions include▫Property shipped outside CA▫Purchase for resale▫Services and labor unrelated to the sale of TPP▫Freight / Shipping▫Software delivered electronically▫Original works of art▫Occasional sales▫Newspapers and periodicals▫Printed sales messages▫Prescription medicines

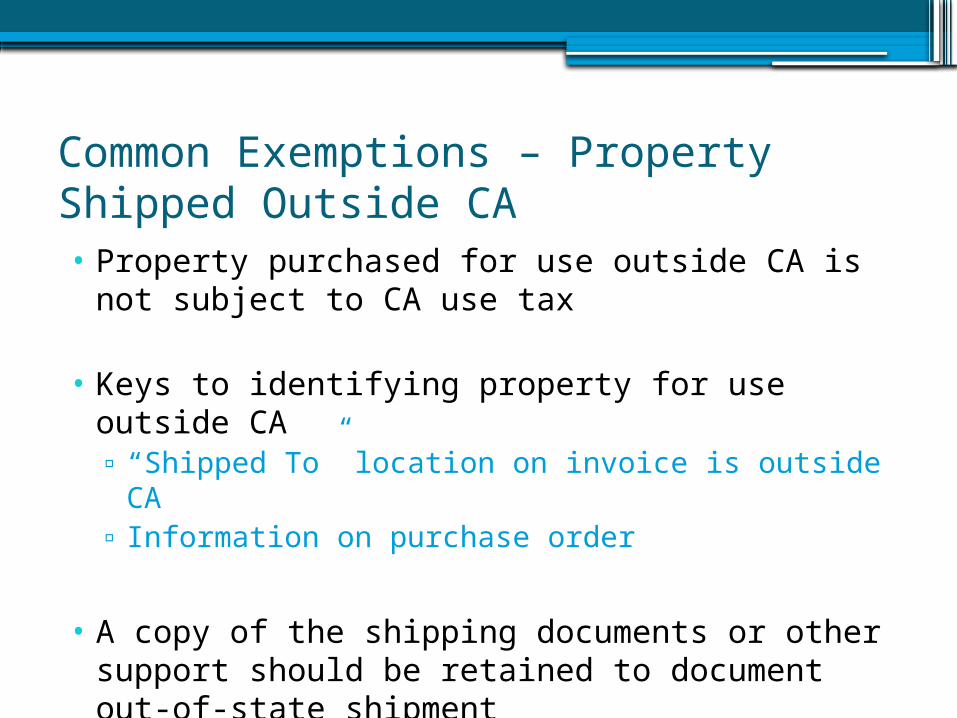

Common Exemptions – Property Shipped Outside CA• Property purchased for use outside CA is not

subject to CA use tax

• Keys to identifying property for use outside CA▫ “Shipped To” location on invoice is outside CA▫ Information on purchase order

• A copy of the shipping documents or other support should be retained to document out-of-state shipment

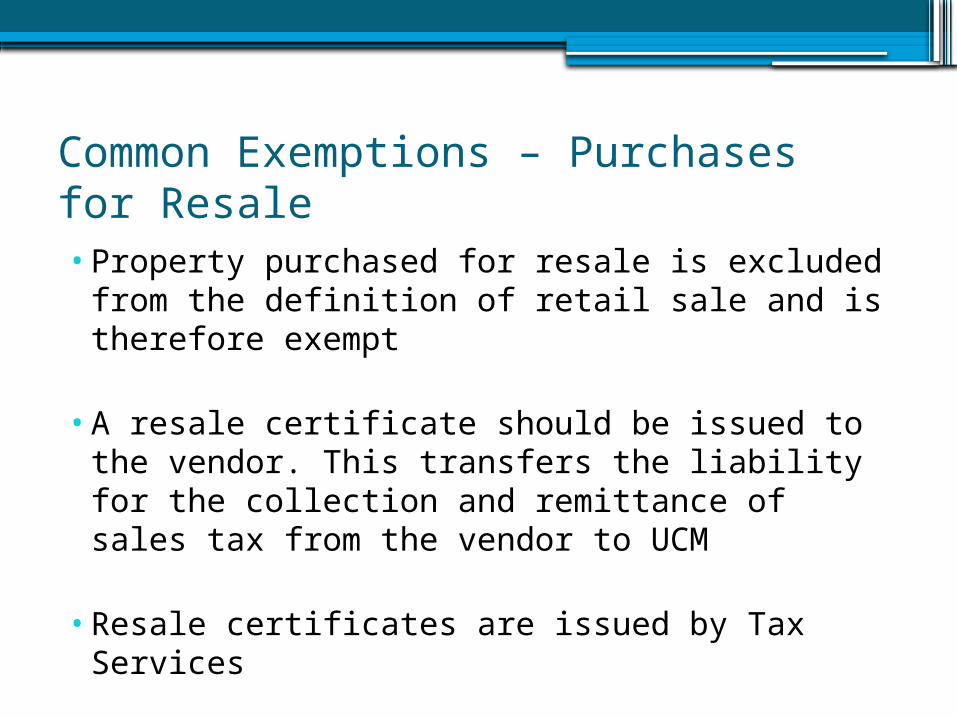

Common Exemptions – Purchases for Resale•Property purchased for resale is excluded

from the definition of retail sale and is therefore exempt

•A resale certificate should be issued to the vendor. This transfers the liability for the collection and remittance of sales tax from the vendor to UCM

•Resale certificates are issued by Tax Services

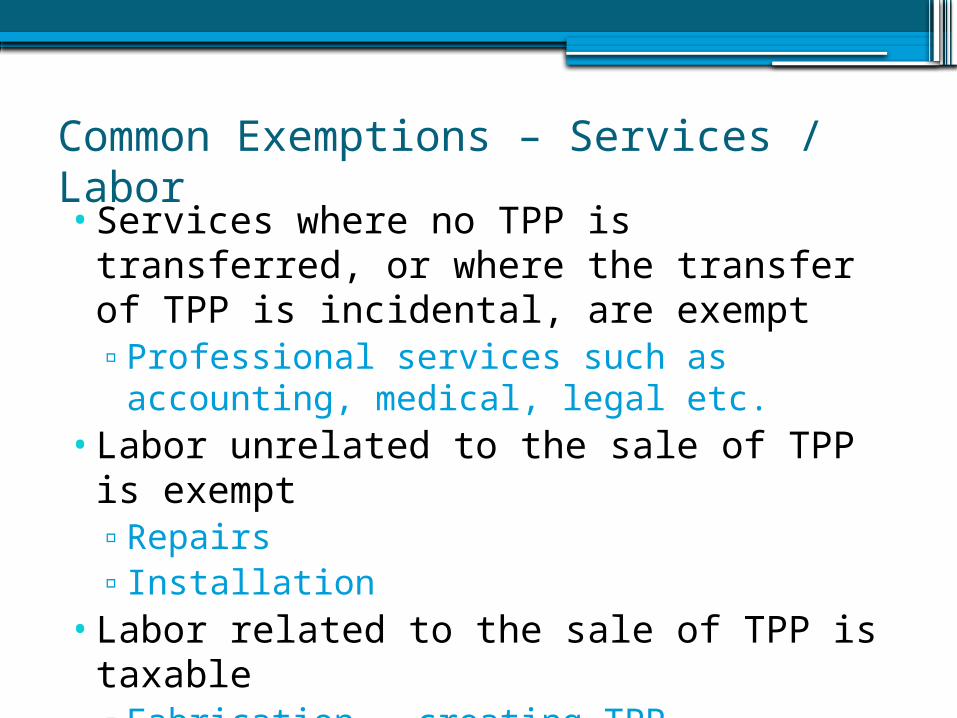

Common Exemptions – Services / Labor•Services where no TPP is transferred, or

where the transfer of TPP is incidental, are exempt ▫Professional services such as accounting,

medical, legal etc.•Labor unrelated to the sale of TPP is

exempt▫Repairs ▫Installation

•Labor related to the sale of TPP is taxable▫Fabrication - creating TPP▫Assembly - charges for assembling new

products

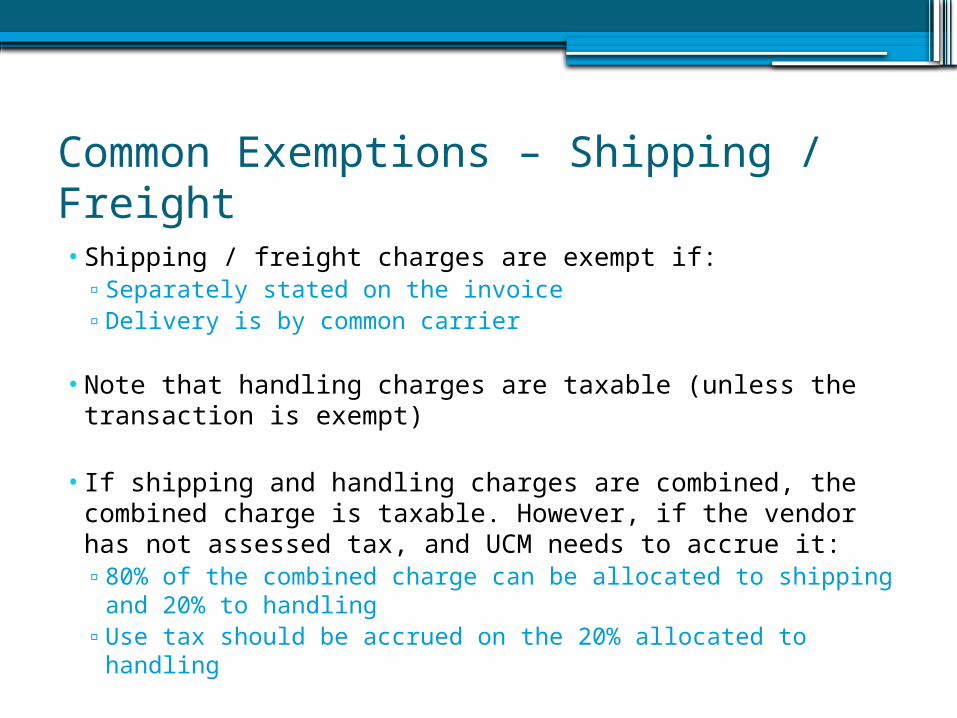

Common Exemptions – Shipping / Freight• Shipping / freight charges are exempt if:▫ Separately stated on the invoice▫Delivery is by common carrier

• Note that handling charges are taxable (unless the transaction is exempt)

• If shipping and handling charges are combined, the combined charge is taxable. However, if the vendor has not assessed tax, and UCM needs to accrue it:▫ 80% of the combined charge can be allocated to shipping

and 20% to handling▫Use tax should be accrued on the 20% allocated to handling

Common Exemptions – Software

•Canned (off-the shelf) software is exempt if it is delivered electronically and no tangible property is shipped▫Shipping / handling charges on the invoice indicate

that TPP (such as a DVD) was shipped

•Custom software (developed specifically for the user)▫More than 50% custom – exempt▫Less than 50% custom – partially exempt

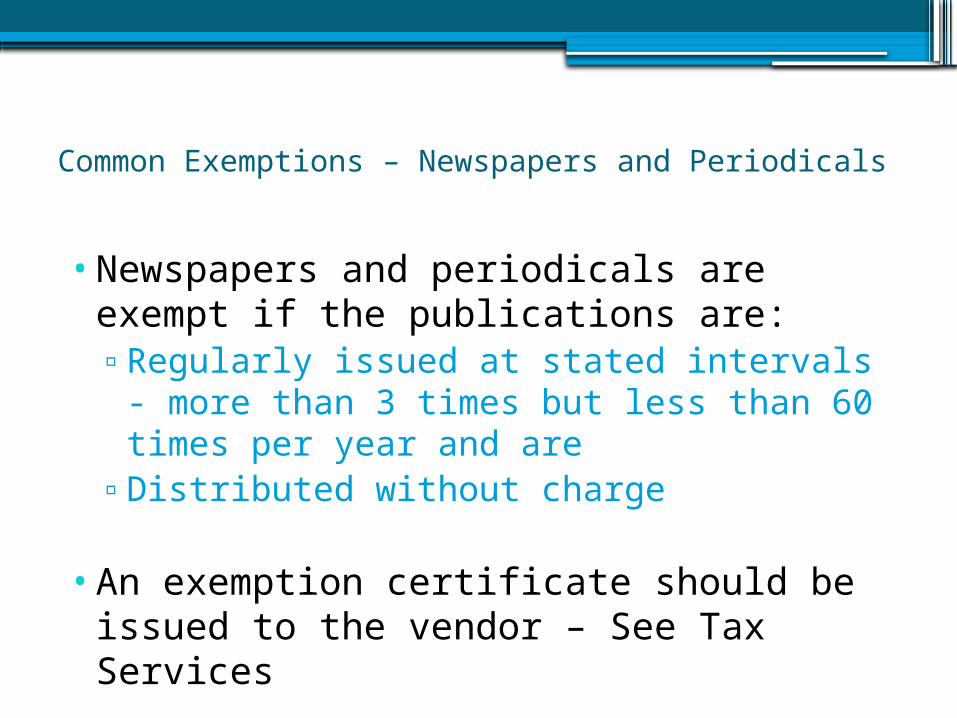

Common Exemptions – Newspapers and Periodicals

•Newspapers and periodicals are exempt if the publications are:▫Regularly issued at stated intervals - more

than 3 times but less than 60 times per year and are

▫Distributed without charge

•An exemption certificate should be issued to the vendor – See Tax Services

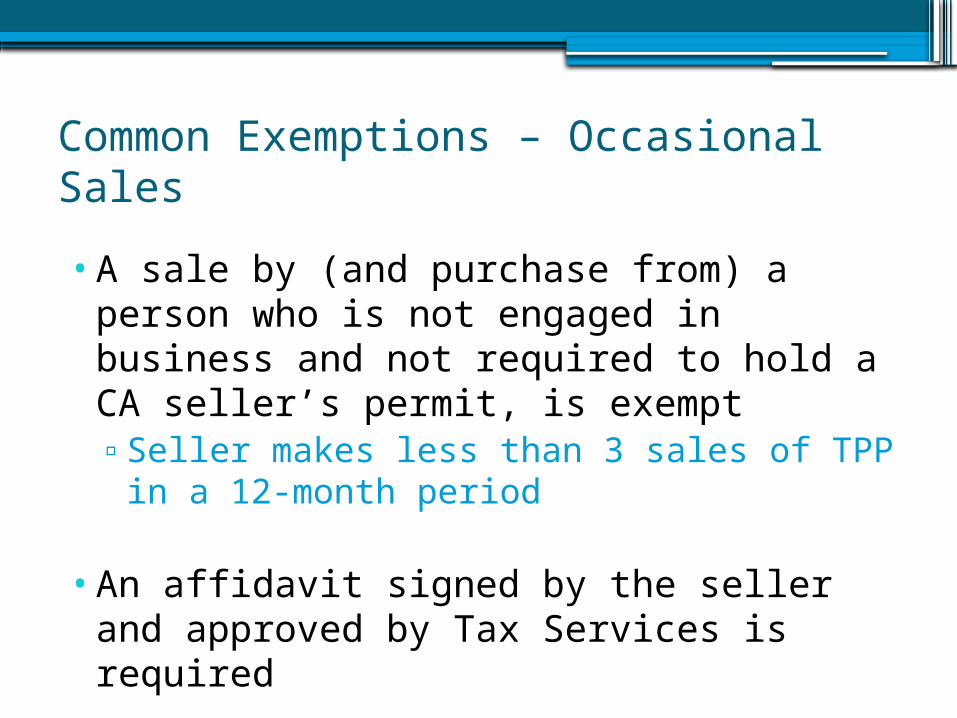

Common Exemptions – Occasional Sales

•A sale by (and purchase from) a person who is not engaged in business and not required to hold a CA seller’s permit, is exempt ▫Seller makes less than 3 sales of TPP in a

12-month period

•An affidavit signed by the seller and approved by Tax Services is required

Common Exemptions – Printed Sales Messages• Printed sales messages are exempt if the printed

material:▫Advertises a good or service ▫ Is delivered directly to the user by the vendor or mailing

house, by common carrier or mail, at no cost to the user

• Examples are Med Center pamphlets regarding medical services or UNEX postcards regarding course announcements.

•An exemption certificate should be issued to the vendor – contact Tax Services

Common Exemptions – Original Works of Art•An original work of art purchased for display in

a museum or public place▫Must be TPP which is created as a unique object▫Includes visual arts, crafts and mixed media▫Must be purchased for display in a museum or

other place which is open to the public without charge for at least 20 hours per week, and for at least 35 weeks of the calendar year

•Example – original artwork purchased by the Fowler Museum for display

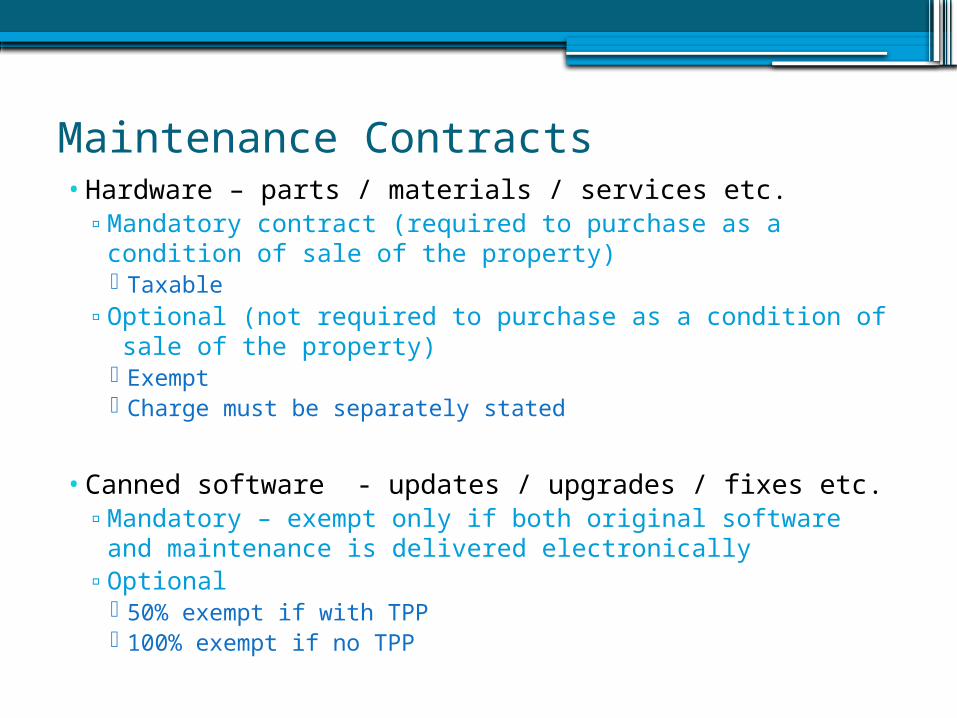

Maintenance Contracts•Hardware – parts / materials / services etc.▫Mandatory contract (required to purchase as a

condition of sale of the property) Taxable

▫Optional (not required to purchase as a condition of sale of the property) Exempt Charge must be separately stated

•Canned software - updates / upgrades / fixes etc.▫Mandatory – exempt only if both original software and

maintenance is delivered electronically▫Optional

50% exempt if with TPP 100% exempt if no TPP

Medicine

•Exempt “medicine” means any substance or preparation intended for use by external or internal application to the human body▫Must be used for the diagnosis, cure,

mitigation, treatment or prevention of disease

▫Commonly recognized as intended for that use

▫Must be prescribed or▫Furnished by a health care facility

Medicine (cont.)•Exempt medicine▫Prescription medicine▫Implants▫Medical gases (used for patient treatment)

•Medical laboratory items - taxable▫Animals for research▫Liquids▫Gases

•Vitamins (supplements)▫Generally taxable unless furnished under

qualifying criteria

District Taxes – UCM Purchases

• Generally vendors are required to collect district taxes only in districts where they do business

• If TPP is purchased from a California vendor who is not required to collect LA County district tax and charges the 8.25% state-wide rate

• Accrue the 1.5% difference (9.75% minus 8.25%)

• If TPP is purchased at a lower district rate (e.g. in San Bernadino where the combined rate is 8.75%) for use at UCM

Accrue the 1% difference (9.75% minus 8.75%)

Miscellaneous Fees and Charges

• Fully taxable, partially taxable or exempt depending on the taxability of the item(s) purchased

▫ Dry ice

▫Hazardous material charge▫Heat surcharge▫ Ice surcharge▫ Fuel surcharge▫ Packaging and handling

• Not Taxable▫ E-waste recycling fee▫ Insurance▫ UPS and Fed Ex delivery charges

Where To Go For Help

Tax Services Portal - http://www.tax.ucla.edu Sales and Use Tax at UCLA -

http://map.ais.ucla.edu/go/1004447 UC Sales & Use Tax Manual UC AMC T-182-73

UCLA Tax Contactso Accounts Payable transactions:

Campus – Renee Roth– [email protected], x 48778o All other transactions:

Scott Monatlik – [email protected], x 46724 Upma Budhraja – ubudhraja@finance .ucla.edu x 49868

State Board of Equalization (SBE) Web Siteo http://www.boe.ca.gov

Sales and Use Tax Case Studies

Case Study 1

The Math Department received the following invoice from Computer Corporation in Kansas:

Notebook computer $ 996 Consulting services 200 Shipping and Handling 20 CA sales tax 0 Total $ 1,216

1. What is the total non-taxable amount (before shipping and handling)?

2. Does an exemption apply? If so, which one?3. What amounts should be entered on the P-card screen and

where? 4. What is the tax due on this invoice?

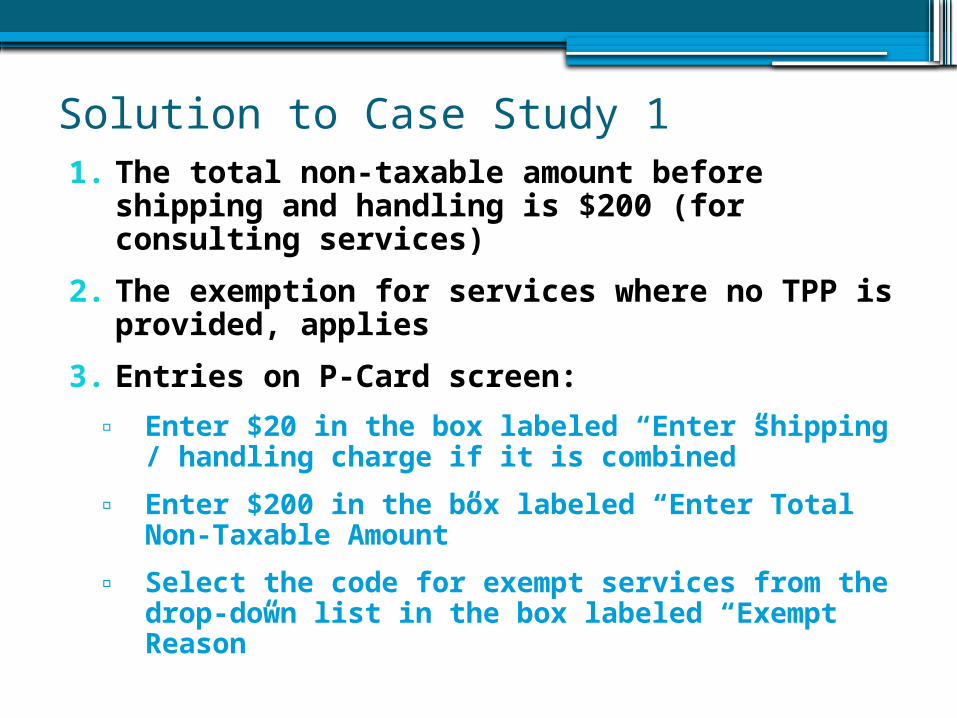

Solution to Case Study 1 1. The total non-taxable amount before

shipping and handling is $200 (for consulting services)

2. The exemption for services where no TPP is provided, applies

3. Entries on P-Card screen:

▫ Enter $20 in the box labeled “Enter shipping / handling charge if it is combined”

▫ Enter $200 in the box labeled “Enter Total Non-Taxable Amount”

▫ Select the code for exempt services from the drop-down list in the box labeled “Exempt Reason”

Solution to Case Study 1 (cont.)

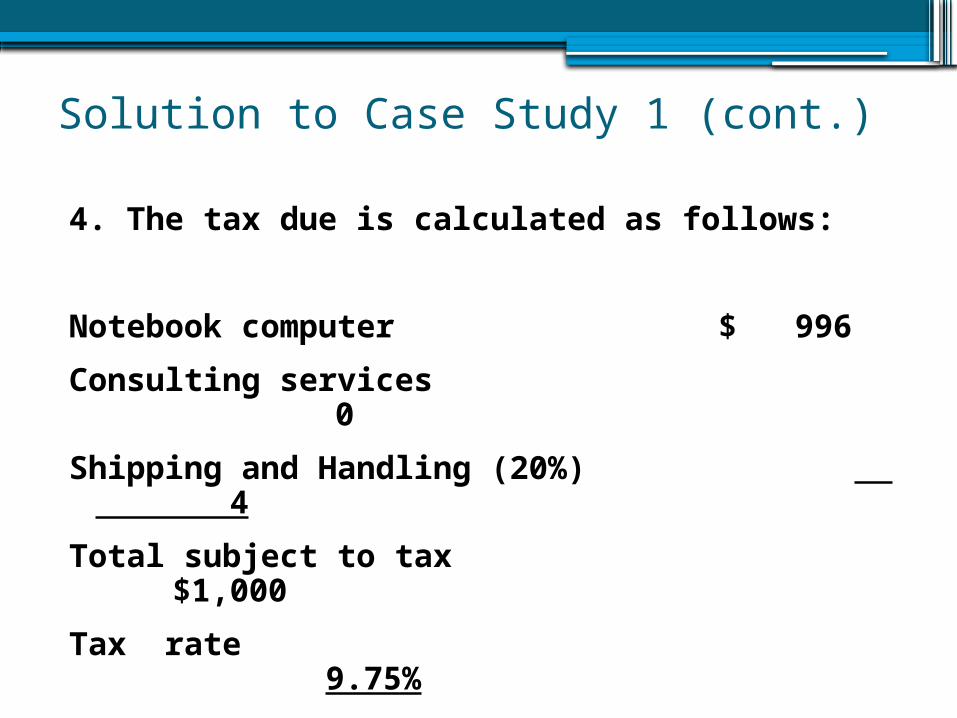

4. The tax due is calculated as follows:

Notebook computer $ 996

Consulting services 0

Shipping and Handling (20%) 4

Total subject to tax $1,000

Tax rate 9.75%

Total tax $ 97.50

Case Study 2The Events Office purchased canned (off-the-shelf) software from a vendor in Texas to track the number of film permits issued annually. The software was delivered via CD and installed on the Department’s server. The purchase includes mandatory maintenance (i.e. upgrades, updates and fixes) to be delivered electronically over the period of the contract. The following invoice was received:

Software $ 800 Maintenance (1/1/11 – 12/31/11) 200 Shipping 10 CA sales tax 0 Total $ 1,010

1. What is the total non-taxable amount (before shipping and handling)?

2. Does an exemption apply? If so, which one?3. What is the tax due on this invoice? 4. How would your answers to questions 1-3 change if the software

was delivered electronically?

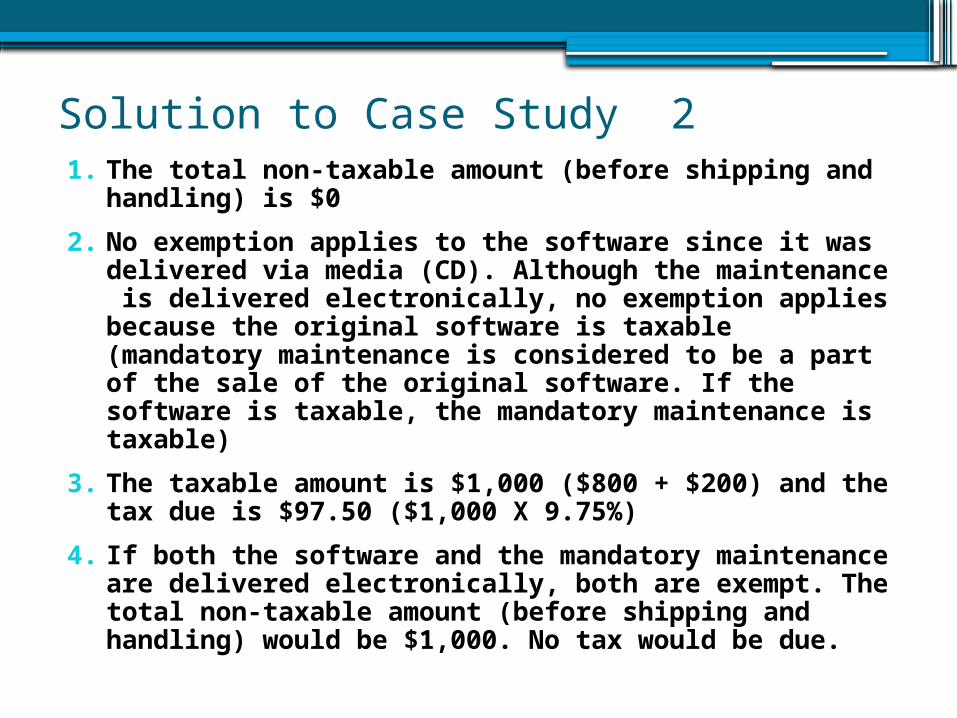

Solution to Case Study 21. The total non-taxable amount (before shipping and

handling) is $0

2. No exemption applies to the software since it was delivered via media (CD). Although the maintenance is delivered electronically, no exemption applies because the original software is taxable (mandatory maintenance is considered to be a part of the sale of the original software. If the software is taxable, the mandatory maintenance is taxable)

3. The taxable amount is $1,000 ($800 + $200) and the tax due is $97.50 ($1,000 X 9.75%)

4. If both the software and the mandatory maintenance are delivered electronically, both are exempt. The total non-taxable amount (before shipping and handling) would be $1,000. No tax would be due.