idc securities lending teleconference (2009-01-29) final

TRANSCRIPT

29 January 200929 January 2009

Securities LendingSecurities Lending

A Primer for Independent DirectorsA Primer for Independent Directors

29 January 200929 January 2009 11

Panelists

Robert A. WittiePartner

K&L Gates LLP

Charles C.S. ParkPrincipal, Chief Compliance Officer – US Funds

Barclays Global Investors, N.A.

Donald W. SmithPartner

K&L Gates LLP

Leslie S. NelsonManaging Director, Global Securities Lending

Goldman, Sachs & Co.

Davey S. ScoonIndependent Chair

Allianz Funds

Amy B.R. LancellottaManaging Director

Independent Directors Council

29 January 200929 January 2009 22

Agenda

• Overview• Regulatory Framework• Board Oversight and Framework• SEC Concerns

29 January 200929 January 2009 33

Securities Lending OverviewWhy Do Funds Lend?

• Realize additional revenue by lending portfolio securities• Generated income represents alpha in addition to the securities’

market value• Transparent to fund portfolio managers

• Loaned holdings still owned by the fund• Portfolio managers can place instructions to sell securities in normal

market transactions• Not lending foregoes this potential revenue

29 January 200929 January 2009 44

Securities Lending OverviewTraditional Program Structure

• Key parties in a traditional securities lending program:• Fund (Lender)• Lending Agent• Borrowers

• Also involved:• Custodian

(if different from the Lending Agent)• Fund’s Investment Adviser• Cash Collateral Manager

(often either the Lending Agent or the Fund’s Investment Adviser)

29 January 200929 January 2009 55

BorrowerBorrower

Securities Lending OverviewTraditional Program Structure

Lending Agent

(Custodian OR Third Party)

Lending or Agency Agreement

Loan Agreements

Portfolio Securities Portfolio Securities

Cash Collateral (≥100%)

Cash Collateral Investments

Fund

Earnings from investment of cash collateral net of rebatefees divided between fund andlending agent according to apredetermined formula (the “fee split”).

Negotiated rebate from cash collateral (the “rebate rate”);

varies per security and borrower

Borrower

Borrower

Borrower

Collateral Manager

Investment Adviser

29 January 200929 January 2009 66

Securities Lending OverviewAlternatives• Direct Lending

• No lending agent, so the Investment Adviser handles securities lending

• Exclusive Agreements• Lender agrees to lend all or a designated part of the fund on an exclusive basis to a single

borrower• Directly negotiated with exclusive borrower OR• Lending Agent-facilitated auction

Must have expertise and resources in-house to lendUtilization rates and returns could be lower without adequate in-house expertise and resourcesLending could be a distraction from portfolio managementWill lose borrower default indemnification absent a separate credit arrangement (e.g., wrap)

Could be cheaper – no agency feesCan more closely tie lending to investment strategy

Potential DisadvantagesPotential Advantages

Potentially higher risk concentration with one borrowerCould lose borrower default indemnification (if done directly)Potentially lower yield (in exchange for downside protection)

Lender has ability to compare returns at time of engagementUtilization rates could be higherPotentially more stable income, since pre-agreedBorrower can access large block of securities

Potential DisadvantagesPotential Advantages

29 January 200929 January 2009 77

Securities Lending OverviewRisks – Securities Lending Transactions

• Borrower/Counterparty Default• Failure to respond to a mark-to-market call for collateral• Trade settlement risks when individual securities are occasionally returned late• Failure to return securities or make payments due to borrower insolvency or other

general defaultsLending agents generally provide indemnification against losses from non-return of securities if collateral is inadequate

• Operational Risk• Lending agent does not administer the program per agreements

• Mark-to-market collateralization levels• Post corporate actions and income

• Lending Agent must have appropriate systems and, in the case of third party agents, must be able to properly interface with fund’s custodian

• Legal Risk• Program structure, lending documents and transactions must satisfy regulatory

and fund policy requirements• Requires policies, compliance procedures, document review and performance

monitoring

29 January 200929 January 2009 88

Securities Lending OverviewRisks – Investing Cash Collateral

• Types of Risks• Investment Risk - Securities in which cash collateral is invested

• Must generate income sufficient to cover rebates• Can lose value

• Liquidity Risk• Loaned securities may be returned by borrowers at any time• Must be able to liquidate (without loss) sufficient collateral investments to

return cash collateral to borrowers when loaned securities are returned

• Risks can be affected by vehicle type• Unregistered money market funds/collective pools• Registered money market funds• Joint accounts• Fund-by-fund individual investments

• Materialized most acutely in 2008

29 January 200929 January 2009 99

Securities Lending OverviewThe Landscape of the Securities Lending Market

• Borrowers (i.e., Broker-Dealers)• Lenders - Any Long Investor, including:

• 1940 Act Funds• Pensions• Foundations

• Routes to market• Custodian banks acting as agent lenders • Non-custodial (third party) agent lenders• “Beneficial owners” lending directly• Exclusive lending relationships with broker-dealers

• OTC Market; programs and transactions are privately arranged

29 January 200929 January 2009 1010

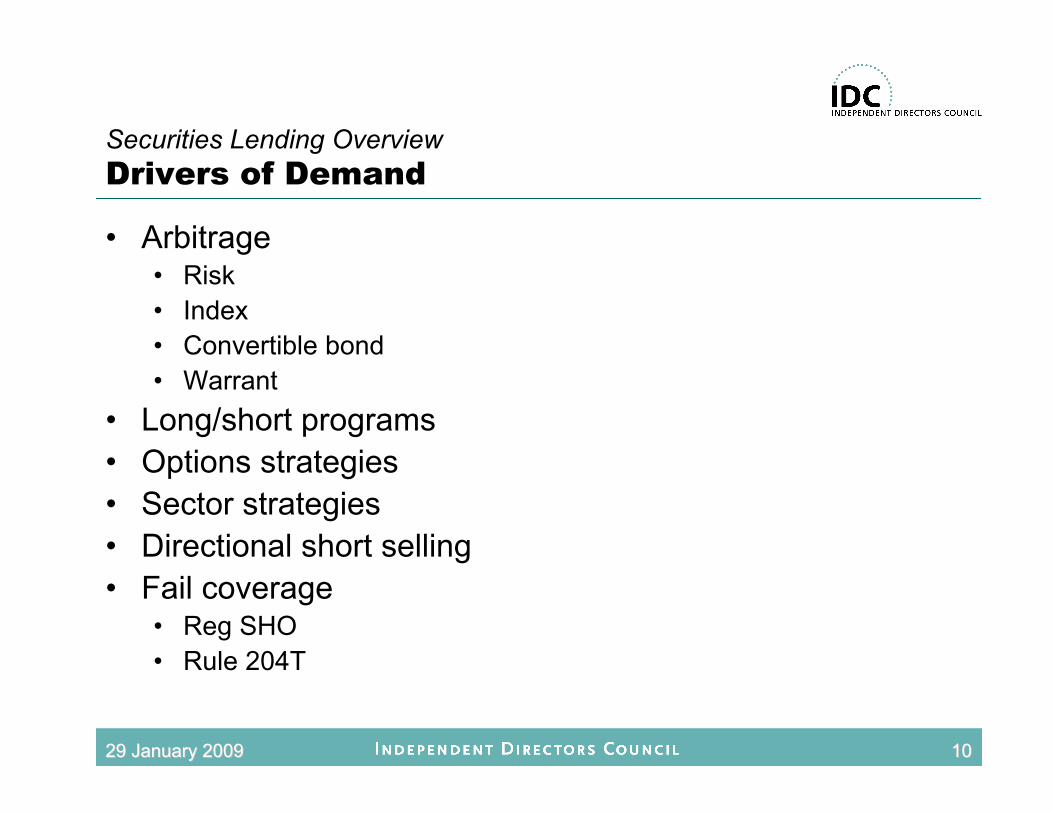

Securities Lending OverviewDrivers of Demand

• Arbitrage• Risk • Index• Convertible bond• Warrant

• Long/short programs• Options strategies• Sector strategies• Directional short selling• Fail coverage

• Reg SHO• Rule 204T

29 January 200929 January 2009 1111

Securities Lending OverviewIndustry Trends – Common Misperceptions

• “Lenders are leaving the market”• Most stayed• Those that suspended their lending programs appear to be

returning

• “Short side demand has decreased significantly”• Demand is still robust • Dollar value of securities on loan is lower, partially due to lower

markets

• “Lending against cash collateral (‘GC Lending’) is a low risk means of generating income”• Cash collateral losses surprised some participants• Liquidity risk also materialized in 2008

29 January 200929 January 2009 1212

Securities Lending OverviewIndustry Trends – Demand Side Themes

• Size and distribution of hedge fund balances

• Continued demand for “hard-to-borrow” securities

• Impact of regulatory changes

• Borrowing to meet Rule 204T requirements

29 January 200929 January 2009 1313

Securities Lending OverviewIndustry Trends – Other Market Factors

• Industry consolidation• Merrill Lynch into Bank of America• Wachovia into Wells Fargo• Bear Stearns into JPMorgan Chase• Bank of America Prime Brokerage into BNP Paribas• Lehman Brothers (mostly) into Barclays Capital (North America)

29 January 200929 January 2009 1414

Securities Lending OverviewIndustry Trends – Going Forward

• Review of current providers and program structures• Distinguish securities lending process from cash collateral

reinvestment

• Final Form of Rule 204T?

• Other regulatory changes?

29 January 200929 January 2009 1515

Regulatory FrameworkSEC Requirements

1. Collateral/Reinvestment of Cash Collateral2. Termination Rights3. Reasonable Interest or Return4. Payment of Compensation5. Maximum Amount Loaned6. Permissible Activity7. Approval of Borrowers and Agreements8. Disclosure9. Policies and Procedures; Oversight

29 January 200929 January 2009 1616

Regulatory Framework1. Collateral/Reinvestment of Cash• Minimum is 100% of value of loaned securities

(but norm is higher: 102–105%)• Includes interest accruals on loaned bonds• Does not include dividends if paid through to fund on a current basis

• Permissible Types (more limited than for other lenders)• Cash (most common)• U.S. government/agency securities• Irrevocable bank letter of credit

• Marked-to-market on a daily basis• Borrowers must add to collateral when value of loaned securities rises; collateral

returned when loaned security values fall• This daily requirement is the reason that collateralization levels remain low

• Cash collateral may be invested only in investments in which the fund is authorized to invest directly

• Government bond fund could not invest cash collateral in corporate bonds• Expectation, however, is that cash will be invested in high quality, short-term

debt• Investment in ordinary portfolio securities can raise leverage and other issues

29 January 200929 January 2009 1717

Regulatory Framework2. Termination Rights

• Funds must be able to terminate a loan within normal settlement period for the security involved• 3 days for domestic equity securities• Up to 5 days for foreign securities

• Purpose is to enable fund to recall securities for sale, voting or acting on corporate actions without disrupting ordinary way portfolio management

29 January 200929 January 2009 1818

Regulatory Framework3. Reasonable Interest or Return

• Funds must receive "reasonable interest" on loaned securities

• Acceptable Forms:• the return on the reinvestment of cash collateral (less rebate fees)• the receipt of loan premiums or similar fees

29 January 200929 January 2009 1919

Regulatory Framework4. Payment of Compensation

• Funds, like other securities lenders, can pay lending agents fees representing a portion of lending revenues• Was not always clear• Fee amount/proportion is subject to board approval and must be

reasonable• Special requirements for affiliated lending agents

• Exemptive relief under 1940 Act §17(d) required to pay lending agent on traditional percentage of revenue (“split”) basis

• Such relief is not currently available• Payments can be made on “fee for service” basis pursuant to

Norwest no-action letter• Both types of payment arrangements require special findings by

fund boards and enhanced monitoring by persons not involved in affiliate’s securities lending process

29 January 200929 January 2009 2020

Regulatory Framework5. Maximum Amount Loaned

• SEC policies prohibit any fund from lending securities having a value that exceeds 33 1/3% of its total assets• This 33 1/3% limit is based upon the §18(f) limitation on fund borrowings• The staff recognized that securities lending is distinctly different than

borrowing• Securities lending limit applies when the loan is made but also

requires ongoing compliance• "Total assets" are grossed up by the amount of the collateral

• Cash collateral is accounted for as part of fund’s total assets, but staff allows securities collateral to be included in calculation for this purpose

• Since collateral must always be at least equal to the value of the loaned securities, this effectively increases the portion of a fund's portfolio that may be loaned to approximately 50% of a fund’s net assets

29 January 200929 January 2009 2121

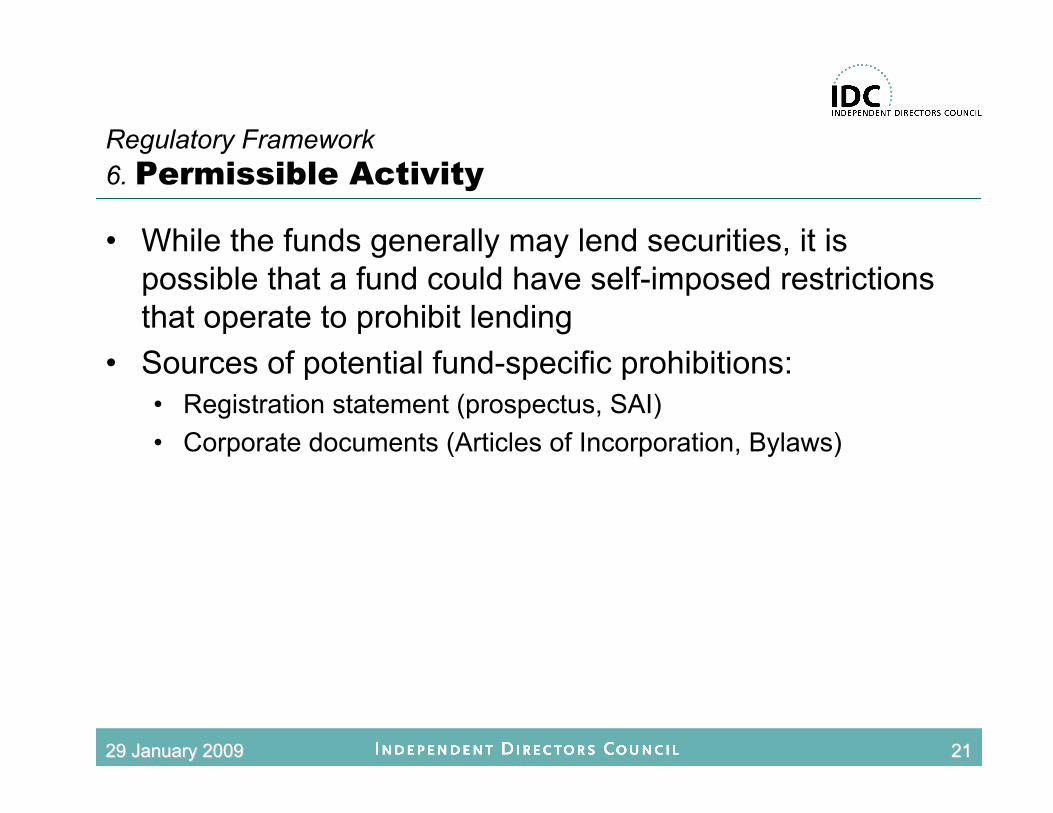

Regulatory Framework6. Permissible Activity

• While the funds generally may lend securities, it is possible that a fund could have self-imposed restrictions that operate to prohibit lending

• Sources of potential fund-specific prohibitions:• Registration statement (prospectus, SAI)• Corporate documents (Articles of Incorporation, Bylaws)

29 January 200929 January 2009 2222

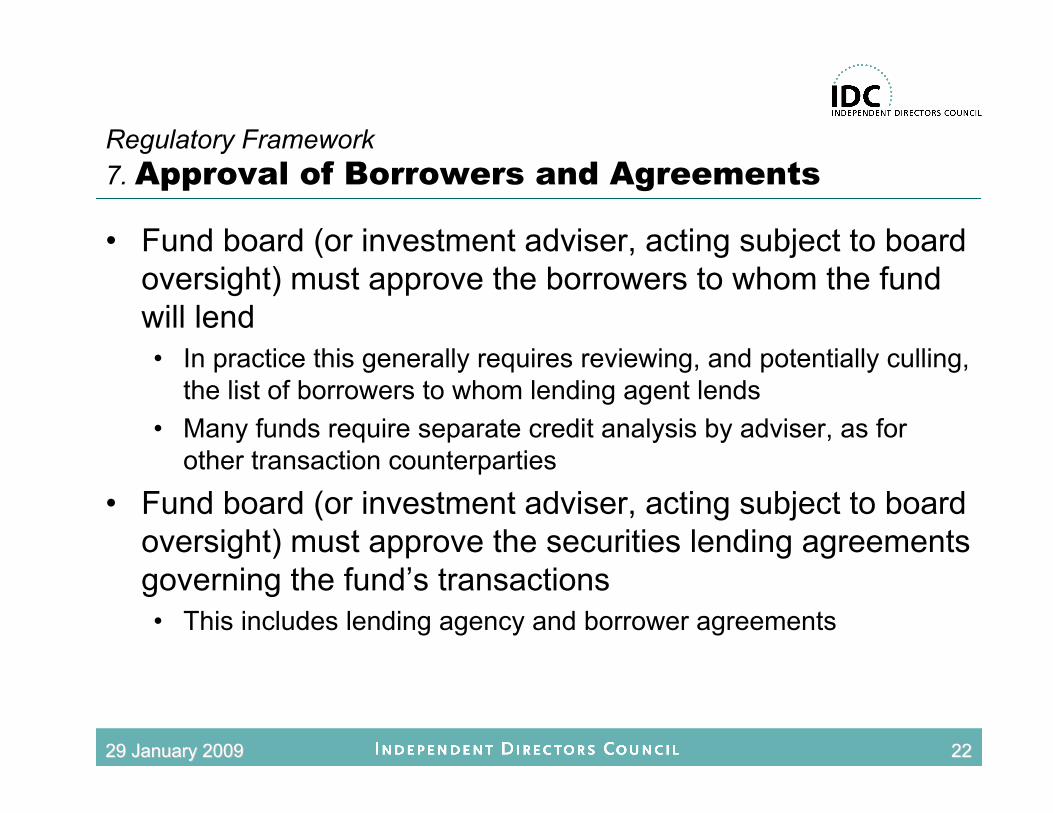

Regulatory Framework7. Approval of Borrowers and Agreements

• Fund board (or investment adviser, acting subject to board oversight) must approve the borrowers to whom the fund will lend• In practice this generally requires reviewing, and potentially culling,

the list of borrowers to whom lending agent lends• Many funds require separate credit analysis by adviser, as for

other transaction counterparties

• Fund board (or investment adviser, acting subject to board oversight) must approve the securities lending agreements governing the fund’s transactions• This includes lending agency and borrower agreements

29 January 200929 January 2009 2323

Regulatory Framework8. Disclosure

• A fund may only lend its portfolio securities if it is permittedto do so under its investment policies, as stated in its prospectus or SAI• Generally, in order for a fund to lend more than 5% of its assets,

there needs to be some risk disclosure in its prospectus (as opposed to its SAI)

• It is important to verify that the fund does not have a fundamental policy against lending securities

• Funds are required to state a fundamental policy regarding their ability to make loans

• Some funds may prohibit lending generally without carving out anexception for securities lending

• A fund's investment policies also must specify the portion of the fund's total assets that may be loaned at any time

29 January 200929 January 2009 2424

Regulatory Framework9. Policies and Procedures; Oversight

• Funds need to adopt written securities lending policies that establish the parameters for their securities lending programs• At a minimum these policies should address the points covered by the

SEC’s securities guidelines• Policies may also set more stringent requirements• Policies should address the topic of recalling loaned securities (or blocking

securities from being loaned) in order to vote proxies• Policies should address

• Choice of route to market• Approval of lending agent or other providers and• Fee structures.

• Policies should establish compliance and monitoring procedures, as well as require periodic reports on lending performance

• Policies and program should be reviewed at least annually

29 January 200929 January 2009 2525

Board Oversight and ReviewGeneral Description

• The decision to participate in a securities lending program• Not just money otherwise left on the table• Evaluation as a new investment category

• Economic considerations• Risk management considerations – risk v. reward• Who will “own” the program within fund management• Adequacy of related compliance resources

29 January 200929 January 2009 2626

Board Oversight and Review Lending Agent

• Evaluation of the proposed lending program• Process for selection• Experience and track record• Compliance resources and staffing• Due diligence on past problems• Willingness to provide guarantees and indemnification• Special issues with regard to affiliated lending agents

including the possible need for exemptive relief

29 January 200929 January 2009 2727

Board Oversight and Review Program Parameters

• Fee arrangements• What comparative information is provided?• Is there an arms length negotiation?

• Investment of collateralHas there been a careful evaluation of the safety of the vehicle used to invest collateral?

• Performance reportingWhat will be the type and frequency of reports provided by fund management and the lending agent?

• Proxy recallsWhat procedures are in place?

29 January 200929 January 2009 2828

Board Oversight and ReviewCompliance Issues

• Core CompetenciesMust have systems and processes in place to daily monitor:• Percentage of fund total assets loaned• Collateral coverage for fund assets loaned• Counterparty exposure limits

• Ancillary IssuesMust assess impacts on other testing and monitoring:• Fund restrictions expressed as percentage of total assets (instead

of “net assets”) can be impacted by securities lending• Investment restrictions imposed on cash collateral investments• Assessment of valuation processes must include cash collateral• Integrity and confidence in total asset calculations

29 January 200929 January 2009 2929

Board Oversight and ReviewTax Issues

• The Qualified Dividend Income (“QDI”) considerations• Under most lending arrangements, dividend income is delivered to the

ultimate holder of borrowed securities; to compensate, most arrangements call for the fund to receive “manufactured” income so the fund retains the economic benefit of owning the security

• Under tax law, however, this rebate is received by the fund as “manufactured income,” and does not receive the same preferential tax treatment

• QDI applies a rate to certain dividend income that is substantially lower than the ordinary income rate

• A fund that holds securities with a significant amount of QDI may distribute to investors a higher taxable distribution if it lends securities through the dividend ex-dates of its portfolio companies

• Funds must analyze tax sensitivity of shareholders and incorporate this as a factor into the securities lending process

• In the case of foreign securities, foreign tax credits may be lost for securities while on loan

29 January 200929 January 2009 3030

Board Oversight and ReviewAnnual Review

• Components of Annual Review• Fee structure summary/overview• Cash collateral investment processes/performance• Lending agent performance assessment• Credit quality of any indemnification providers• Regulatory requirement coverage and developments• Compliance determination representation

29 January 200929 January 2009 3131

SEC Concerns – Examination Results

• SEC Sweep Examinations of Affiliated Securities Lending Agent Arrangements• The 2004 sweep focused on complexes that used affiliated lending

agents – obviously an area of increased sensitivity• The Staff issued a series of deficiency letters

• Some of the problems that OCIE identified related to the specialrequirements that are imposed by affiliated lending exemptive orders and no-action letters

• The unusually long interval between the sweep itself and the issuance of deficiency letters was due, at least in part, to the Staff’s desire to assess all results and determine whether there were notable trends or patterns

• Not coincidentally, there has been an informal moratorium on theprocessing of most affiliated lending exemptive orders since early 2004

29 January 200929 January 2009 3232

SEC Concerns – Key Topics

• Most concerns not limited to affiliated lending agent arrangements

• The principal areas of concern have been as follows:1. Initial Fund Board Approval Process2. Performance Reporting and Review3. Lending Agent Fees4. Compliance Procedures5. Periodic Review and Approval Process

29 January 200929 January 2009 3333

SEC Concerns1. Initial Fund Board Approval Process

Deficiencies in the fund board’s process for approving lending arrangements

• In at least one instance, the Staff specifically criticized the board for what the Staff believed was an inadequate process that resulted in the board having insufficient information to assess alternatives to a proposed affiliated arrangement or to discharge its more general responsibilities in selecting an agent.

• In essence, the Staff seemed to be criticizing the board for failing to sufficiently “kick the tires” of the securities lending agency or other arrangement proposed by the adviser. In the context of affiliated arrangements, the Staff sometimes felt that the adviser had pre-determined that its affiliate should be the lending agent.

For a more complete discussion of board oversight of securities lending providers, see “Board Oversight of Certain Service Providers,” IDC Task Force Report (June 2007) (http://www.idc1.org/getPublicPDF.do?file=21229).

29 January 200929 January 2009 3434

SEC Concerns2. Performance Reporting and Review

• Inadequate monitoring by fund boards, and inadequate monitoring and reporting by fund advisers with respect to securities lending performance.

• Particular focus on: • Whether the lending program is compliant with policies and is

generating profits consistent with those anticipated at the time of approval

• Negative spreads, particularly when the compensation arrangement was not merely a split of net lending income and thus allowed loans to be profitable to the lending agent, even if they were not profitable to the fund

29 January 200929 January 2009 3535

SEC Concerns3. Lending Agent Fees

• Inadequate attention to the level of compensation relative to the market, especially when an affiliated lending agent is being considered

• In some instances the Staff found that a board approved compensation for an affiliated agent that was: • higher than what the fund had previously paid to an unaffiliated

agent OR• higher than what the affiliated agent charges to comparable,

unaffiliated lending customers

In both cases, these facts did not appear to be adequately disclosed to and discussed with the board

29 January 200929 January 2009 3636

SEC Concerns4. Compliance Procedures

• Failures of funds and fund boards to approve written securities lending policies and compliance procedures

• Failures in complying with: • SEC Staff’s securities lending guidelines• Exemptive orders/no-action letters governing the affiliated

arrangement• Of particular concern were:

• failures to set sufficient parameters for lending transactions, including the terms (including permissible rebate rates and spreads) on which loans would be made AND

• failures to have adequate procedures in place to monitor performance and to protect against conflicts of interest

29 January 200929 January 2009 3737

SEC Concerns5. Periodic Review and Approval Process

Failures to reassess securities lending programs and performance periodically, particularly to ensure that:

• The contract with lending agent is in the best interests of the fund and its shareholders

• The services to be performed by lending agent are appropriate for the fund

• The nature and quality of the services provided by lending agent(particularly affiliated agents) are at least equal to those provided by other lending agents offering the same or similar services for similar compensation AND

• The lending agent’s fees are fair and reasonable in light of the usual and customary charges imposed by other lending agents for services of the same nature and quality