ideas for increasing rural incomes: what does the theory tell us? richard j. sexton

TRANSCRIPT

Ideas for Increasing Rural Incomes:What Does the Theory Tell Us?

Richard J. Sexton

A classification scheme for income-generating ideas

Ideas that expand the size of the pie Ideas that increase the share of the pie going

to producers and rural communities

Ideas that expand the pie

New product introductions Organic production Eco friendly and animal friendly production Geographic designations Brand labels and other means of product

differentiation Niche markets such as products targeted to specific

ethnic groups.

Ideas that increase the share of the pie going to producers and rural communities

Downstream integration into “value-added production”

Vertical coordination with downstream marketers Bargaining and other forms of collective action

intended to increase producer market power Legislation intended to increase competition and the

balance of power in agricultural markets

Some key stylized facts

Demand U.S. and European consumers demands for food are

very inelastic, and many of these consumers are willing to pay a lot to consume the “right” foods. Tastes are heterogeneous.

The fastest growth markets are in developing countries, and these demands are more elastic and place less emphasis on quality and differentiation.

Some key stylized facts

Production Barriers to entry into agricultural production are

usually low or nonexistent. The main barrier to entry is the lag time from planting

to harvest for perennial crops or the conversion process required for organic certification.

Do geographic designations create a meaningful barrier to entry?

Pursuing a product differentiation and niche marketing strategy will involve higher per-unit production costs.

Some key stylized facts

Marketing New and better food products may create substantial

short-run rents, but if downstream markets are not competitive, a large share of these rents may not be captured by producers.

Producer-marketer vertical coordination may improve market efficiency and improve information flow, but there may also be unintended market-power consequences.

Some alternative market morphologies and their consequences

The traditional competitive food marketing sector and spot markets– short run profits or losses, but the long-run

equilibrium is zero profits– Probably no modern agricultural market fits this

paradigm, i.e., market power, product differentiation, and information issues are integral elements of these markets nowadays.

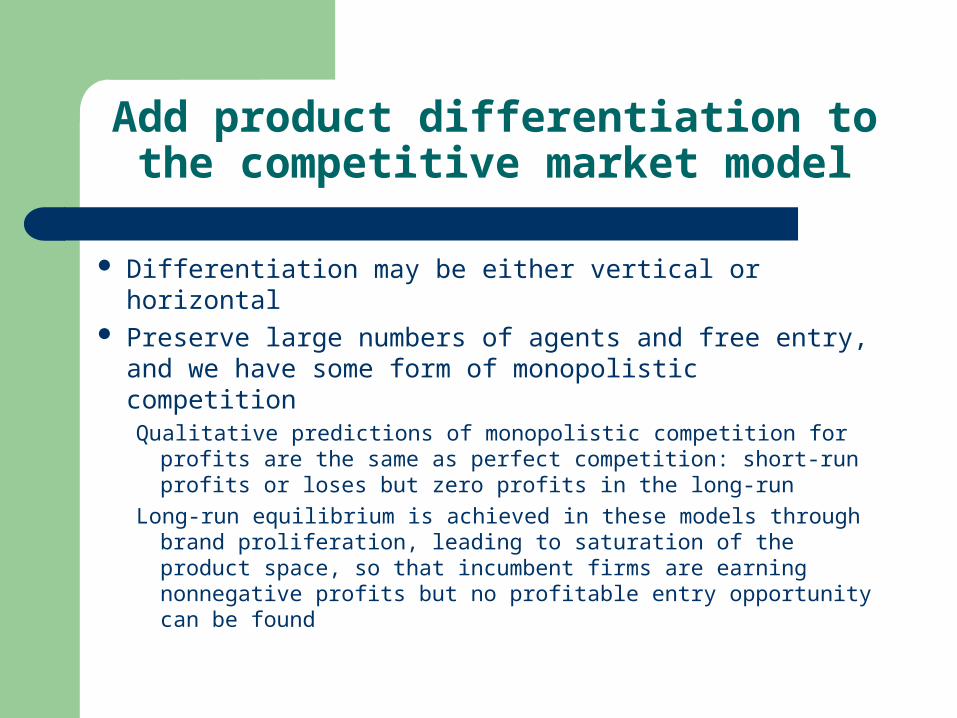

Add product differentiation to the competitive market model

Differentiation may be either vertical or horizontal Preserve large numbers of agents and free entry,

and we have some form of monopolistic competitionQualitative predictions of monopolistic competition for profits

are the same as perfect competition: short-run profits or loses but zero profits in the long-run

Long-run equilibrium is achieved in these models through brand proliferation, leading to saturation of the product space, so that incumbent firms are earning nonnegative profits but no profitable entry opportunity can be found

Example of geographic designations as product differentiation

The designation provides an immutable barrier to entry outside the designated region

Free entry within the designated region But designation can attempt to impose supply controls

—how successfully remains an open question Producers outside of the designated region can

respond by creating their own designations, thereby saturating the product space and creating in the long run a classic zero-profit, long-run monopolistically competitive equilibrium

Geographic designations (cont.)

Crespi notes 450 appellations for medium-priced French wines—entry is not just at the high end of the product space, an example of the principle of maximum differentiation

Retailers generally only carry a few brands. Proliferation of brands gives retailers great power to use competition for shelf space and slotting decisions to capture rents from producers and marketers

Store brands can be used to counteract market power of shipper/processor brands

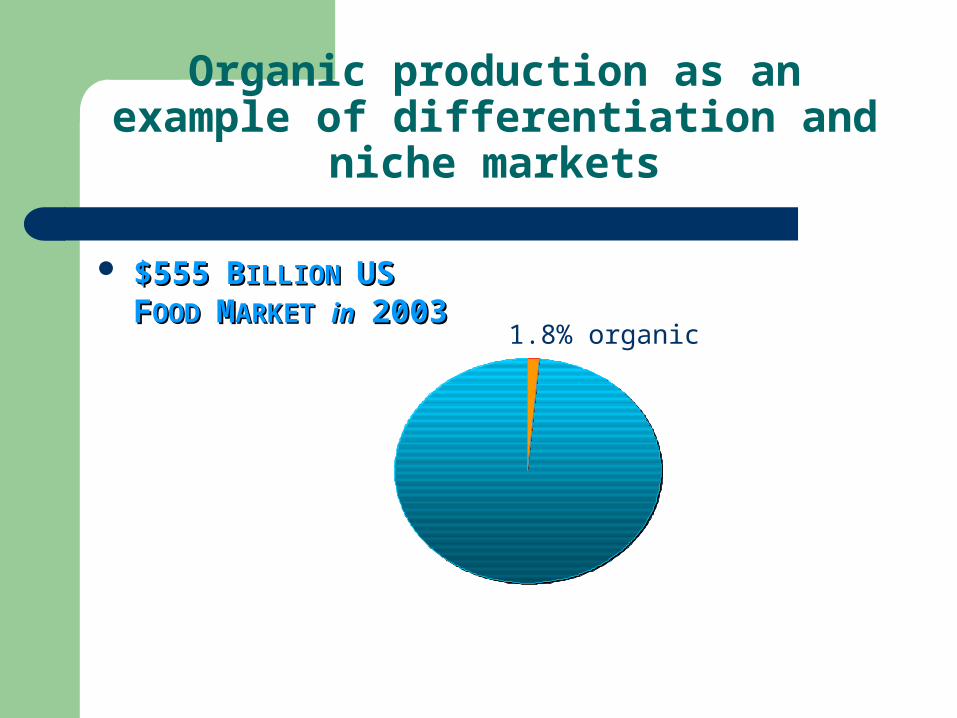

Organic production as an example of differentiation and niche markets

$555$555 BBILLION ILLION US US FFOOD OOD MMARKET ARKET inin

20032003 1.8% organic

Acres of organic commodities in Acres of organic commodities in CALIFORNIA 1992 - 2002CALIFORNIA 1992 - 2002

020406080

100120140160180200

1992 1994 1996 1998 2000 2002

1,0

00 A

cres

Nursery &flowers

livestock, poultry& products

field crops

Vegetables

fruit & nuts

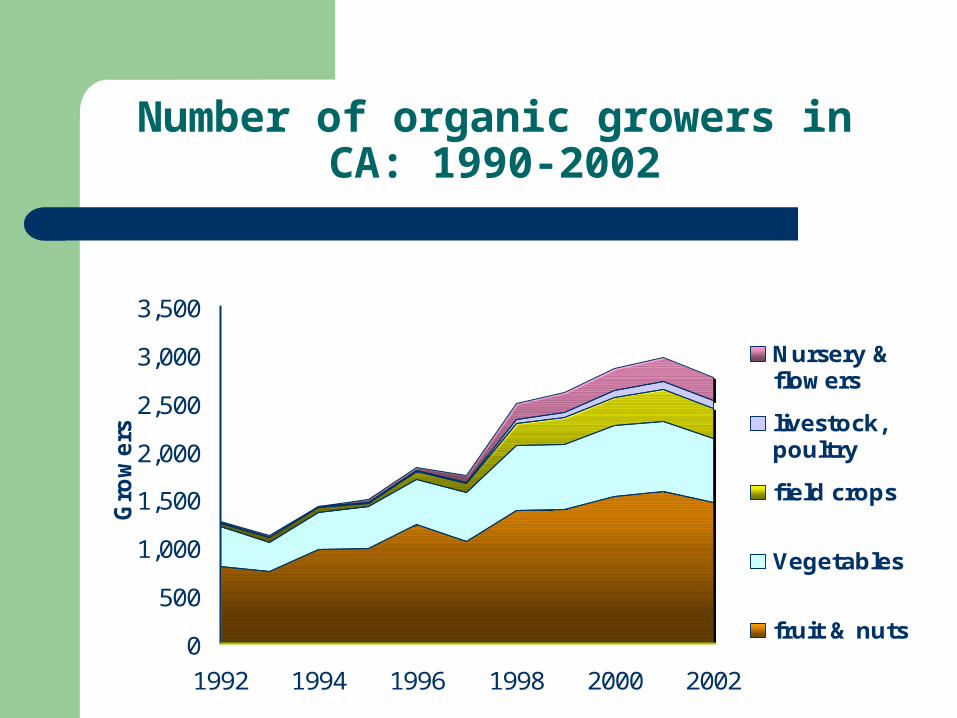

Number of organic growers in CA: 1990-2002

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1992 1994 1996 1998 2000 2002

Gro

wers

Nursery &flowers

livestock,poultry

field crops

Vegetables

fruit & nuts

Distribution of Organic Production by Income Category

42

10

21 22

7 4 3 31 1 4 612 14

55

9

$0-$4,999 $5,000-$9,999

$10,000-$49,999

$50,000-$99,999

$100,000-$249,999

$250,000-$499,000

$500,000-$999,999

$1,000,000and above

Pe

rce

nt

of

To

tal

Growers Sales

The bottom line from organic agriculture

Even a good niche, as organic has turned out to be, has a very small impact on the overall agricultural sector

Large-scale agriculture has come to dominate the organic sector, and many of the spillover benefits associated with organic are probably lost in the process

The vertical-control, contract-agriculture model

Principal-agent paradigm applies to this model: market power imbalances suggest designating marketing firms as principals and depicting producers as the agents.

Contracts can solve information problems in market and provide efficient risk sharing, and thus expand the size of the pie, but . . .

Unless competitive forces are strong, contracts can be very effective devices for downstream firms to extract profits from producers, thereby generating zero profit equilibria in both the short and long run—participation constraints usually bind in these models

The prototype oligopoly/oligopsony model of an ag market

Put the focus on competition issues, and accordingly abstract away from issues of technology, product differentiation, and information

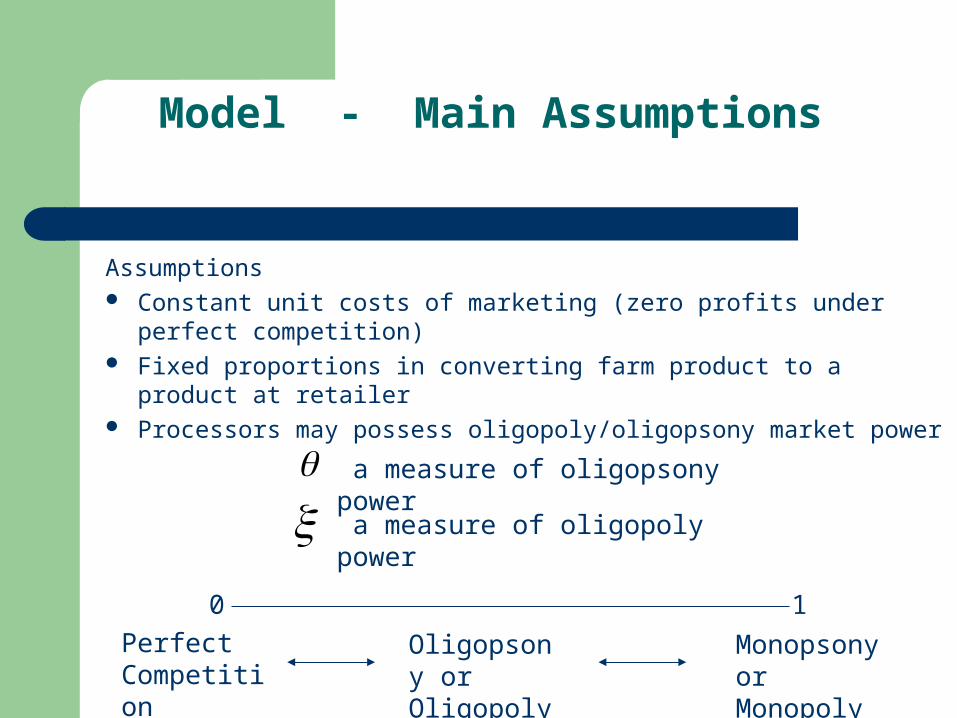

Assumptions Constant unit costs of marketing (zero profits under perfect

competition) Fixed proportions in converting farm product to a product at retailer Processors may possess oligopoly/oligopsony market power

Model - Main Assumptions

a measure of oligopsony power

0 1

Perfect Competition

Oligopsony or Oligopoly

Monopsony or Monopoly

a measure of oligopoly power

Key predictions from the model

Both oligopsony power and oligopoly power by downstream firms are bad for producers because they reduce output and, hence, income, employment, etc.

Marketing sector firms with market power can capture a large share of the surplus generated from a demand-expanding initiative

This means that even really good ideas that increase the size of the pie may not increase by much the income that flows back to farmers and rural communities

The Impact of Downstream Market Power on Producer Benefits from Advertising

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014

0.016

0.018

0.02

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Market Power IndexOligopoly Oligopsony Oligopoly/Oligopsony

What about cooperatives and other forms of producer collective action?

Traditional agricultural marketing cooperatives have significant competitive disadvantages in modern markets

– Cooperatives that provide a ‘home’ to member production for the most part lose the power to influence price

– Cooperatives that market a single product face disadvantages in light of retailers preference for suppliers who can fill an entire product category.

– Cooperatives have a disadvantage in providing the quality and value-added dimensions critical in today’s market due to the horizon problem and difficulties raising investment capital and adverse selection problems created by pooling practices.

Can “advanced” forms of cooperation fare better?

New generation structure is intended to surmount many of the problems of traditional cooperatives: closed membership, delivery rights are tied to stock equity contributions, tradable equity shares, and delivery obligations.

Other “limited liability” corporations merge some ideas of cooperation with concepts of limited partnerships and subchapter S corporations—enable producers to capture appreciation in the value of the downstream enterprise

Are producers able to “cooperate” in even limited ways, such as funding advertising programs and supporting geographic designations?

Limitations on collective action of any form

Today’s agricultural producer is probably less ‘cooperative’ than predecessors.

– Concepts such as brands and monopolistic competition sharpen the focus of the other guy as a competitor and not a cooperator and are antithetical to traditional cooperation

– U.S. producers are having trouble cooperating in even limited ways, such as commodity promotion

– Would geographic designations be any different? Would success cause some producers to want to opt out?

Some pessimistic conclusions

Trend in nonsubsidized agriculture towards fewer and larger farms are likely to continue

Most production will involve substantial vertical coordination between the production stage and downstream stages—accordingly less “freedom to farm”, but greater efficiency and matching of production to consumer preferences.

Without substantial outside intervention, rural communities will continue to decay, involve substantial poverty, be populated mainly by those who work on the large-scale farms, and in general represent a societal problem

Some pessimistic conclusions

Grocery retailers will increasingly become the dominant players in the food marketing chain, with grains continuing to be dominated by powerful manufacturers

New ideas, concepts, and innovations may produce substantial short-term rents for small groups of producers but won’t have much impact on the aforementioned major trends