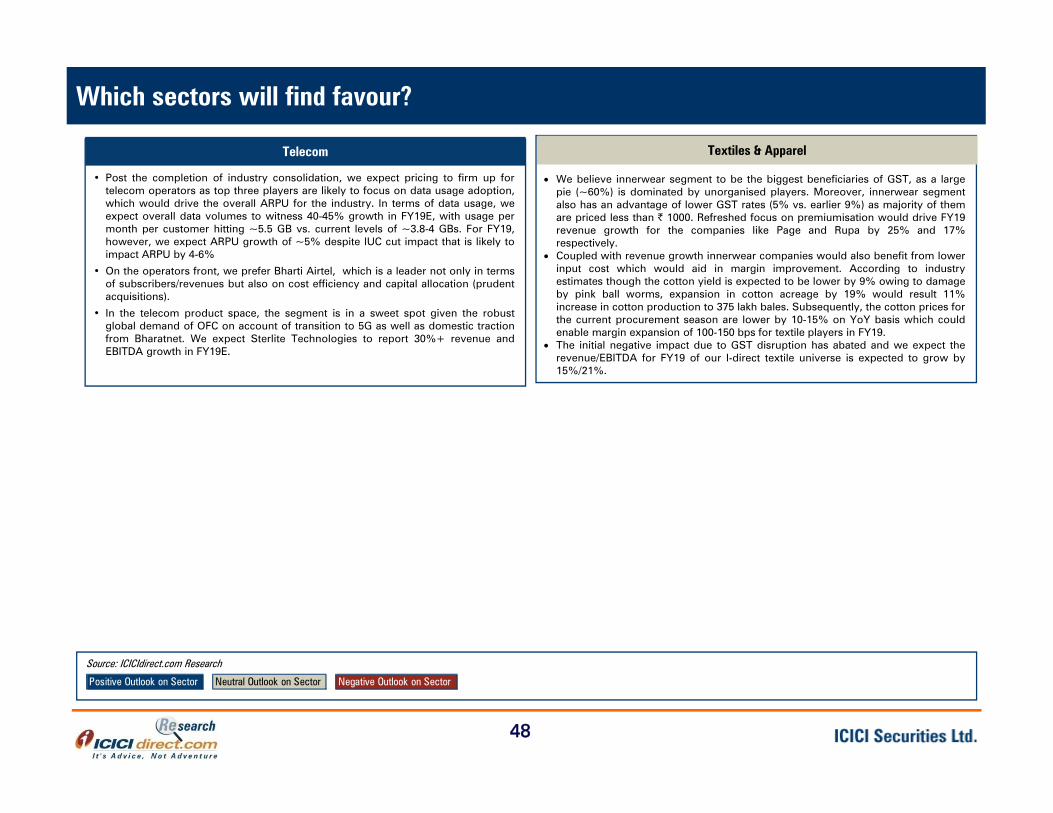

idirect marketstrategy 2018 - content.icicidirect.comcompany idirect code cmp (|)target price...

TRANSCRIPT

2018Market Strategy

1

Deal Team – At Your ServiceMarket Strategy 2018

Agrarian focused consumption push to alleviate rural stress

2

Capex revival to be key theme in 2018

3

Amid limited domestic challenge, risks to originate outside

4

Sectoral Outlook

5

Fiscal policy: Limited space for big bang reform

6

Monetary space: Limited respite on rate cuts ahead

7

Consumption, GFCE to drive GDP growth

8

Market Outlook – 2018 to be the year of Stabilisation1

Top Picks for Strategy 20189

Market OutlookEarnings to break shackles post four years of flattish trend?In sync with the flip flop in commodity prices, unexpected one offs likedemonetisation, GST, weak capex cycle, base of earnings remained flat in the range of| 1365‐1403 in FY14‐17. However, normalisation in commodity prices, a gradualadjustment to the GST regime, increased thrust of government in reviving capex cycleand peak NPA provisioning behind us, we feel that earnings will break the shackles ofone offs and stage a robust comeback at 17.4% CAGR in FY17‐20E.Our confidence on a durable recovery in earnings stems from the fact that assetturnover ratio of India Inc. marked their bottom in FY16 at 1x while same improvedmarginally to 1.1x in FY17. A smart recovery in the earnings profile of companies inQ2FY18 and ensuing management commentary indicates a robust H2FY18. Thiscoupled with stable margins (rising utilisation level will cushion rising input costs) areexpected to lead to a recovery in RoCE of Corporate India. We expect RoCE of Sensexcompanies (ex‐financials) to improve 220 bps by FY20E to 24.4%, which will help thebroader markets to trade at a premium vis‐à‐vis its historical premium multiples.Sectorally, in terms of earnings growth, the recovery baton will be taken by thebanking space (33% CAGR) with the share of incremental index earnings at ~58%Growth in earnings to drive Sensex as most multiple expansion behind usOur prognosis for CY18 suggest that the Sensex P/E expansion has been driven byfalling yields, which is behind us as the interest rate improvement cycle has playedout. Going ahead, the key driving force for the market would be earnings recovery,which would be backed by a rise in asset turn thereby improving the RoCE profile.Based on bottom up approach by using a sum of the parts (SoTP) evaluation ofindividual index constituents, we assign a fair value for Sensex at 37,600 withconsequent target for Nifty at 11,725 offering 12% upside from current levels.

CY17 was a remarkable year for equities as liquidity across the globe ensured that itwas the most favoured asset class. Back home in India, the story was no different asSensex delivered a handsome 29% return, aided further by the falling yields whichled to decline in cost of capital and consequent expansion of P/E multiples. Amid allthese, the year was also marked by one‐offs such as Demonetisation andimplementation of GST, which temporarily led to a down tick in corporate earningsand GDP growth.CY18 will be the year of Stabilisation as we believe that various steps taken by thegovernment may start bearing fruit, going ahead. Key theme, which is expected toplay out is an uptick in capacity utilisation across sectors. This, in turn, will call foran uptick in capex cycle. Also, with course corrections in private sector balancesheet, mending of banking sector and robust government policies in place, privatesector investments may start revving up in CY18. All this, in our view, will lead to aresurrection of GDP growth. Hence, we believe sectors like corporate banks, capitalgoods, infrastructure are likely to witness robust business activity in CY18.Government to lead capex, its policies to break private investment jinx…Based on our bottom up approach, infrastructure investment may jump up to ~| 48lakh crore led by housing, roads and railways in the next five years, which implies10% CAGR in infrastructure spending in the next five years. Hence, we expectinfrastructure spending as percentage of GDP to inch up to 6.0% in the next five yearsvs. 5.6% in the previous five years. In our view, increased infrastructure spending mayinch up GDP growth rate by 80 to 100 bps. Government’s “Housing for All by 2022”scheme (total opportunity of ~| 20 lakh crore) is expected to be a key catalyst in theeconomic recovery. Furthermore, an improvement in policy reform makes thebusiness environment conducive for private investment in infrastructure.…which will provide impetus to GFCF & trigger GDP normalisationGoing ahead, private sector capex (~38% of GFCF) will play a more important role inrecovery of GFCF growth, mainly on account of the full blown effect of affordablehousing initiatives. Hence, with above recovery setting in coupled with stable growthin private consumption, we expect nominal GDP growth to bounce from 9.9% inFY18E to 11.8% in FY19E.Rural focus ahead of elections…In the wake of a mere one and half years being left for general elections, thegovernment’s thrust will be on increasing farmer’s income considerably next year byway of supporting better crop realisation. Initiatives like eNam and setting up of megafood parks is likely to reduce the disintermediation cost by 25‐30%, which could wellbe the single most important factor in increasing farmer’s income immediately.

2

Economic Endurance to reinforce steady returns

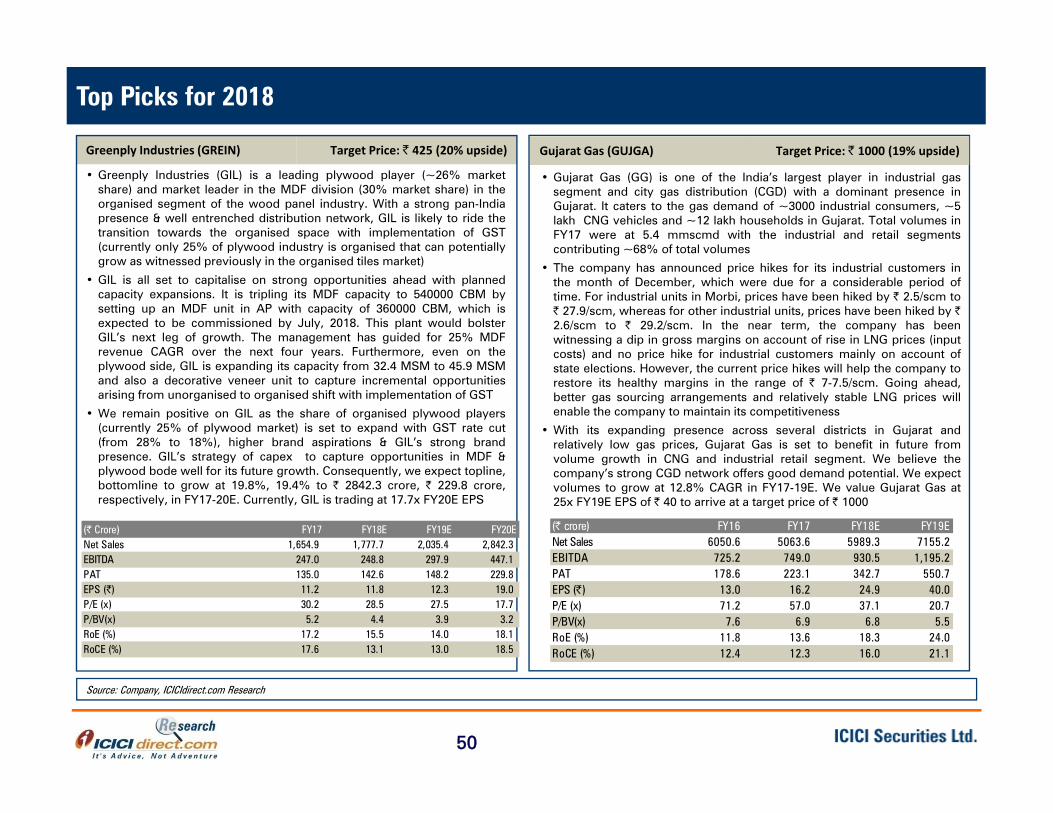

Company Idirect Code CMP (|) Target Price (|) Upside (%)Bajaj Electricals BAJELE 489 575 18Greenply Industries GREIN 355 425 20Gujarat Gas GUJGA 843 1000 19Kalpataru Power KALPOW 471 600 27KSB Pumps KSBPUM 867 1080 25Narayana Hrudayalaya NARHRU 298 360 21Simplex Infrastructure SIMINF 575 750 31South Indian Bank SOUBAN 31 40 27

Stock Picks for 2018

128359

113136

97054

17808 20568

45450

0

20000

40000

60000

80000

100000

120000

140000

2012

2013

2014

2015

2016

2017

(| C

rore

)

33

Deal Team – At Your ServiceTINA factor locally, globally to continue amid shrinking investible bond pool

0

1

2

3

4

‐1‐0 0‐1

1‐2

2‐3

3‐4

4‐5

5‐6

6‐7

7‐8 >8

In US $ trillion

Yield %

2007 : US $ 15.8 tln yielding >4%

Corporate QuasiSecuritized Soverign

0

1

2

3

4

‐1‐0 0‐1

1‐2

2‐3

3‐4

4‐5

5‐6

6‐7

7‐8 >8

In US $ trillion

Yield %

2017 : US $ 1.8 tln yielding >4% Corporate QuasiSecuritized Soverign

Bond market returns continue to get sub optimal: bonds yielding more than 4% shrink by 90% since 2007

In hunt for yield, equities still more attractive vs. bonds: US equities have 210 bps better yields

Earnings yields more attractive for EMs vs. DM: This is likely to keep EM equites sheen intact

The overarching theme for equity remains “There is no alternative” (TINA) better than equities. In the yield starved world, the case for equities isgetting more compelling as earnings yields for equites continue to remain attractive compared to bond yields. A similar trend of higher earnings yieldalso remains for EMs. Indian equities may gain on the back of this trend as FIIs have been on the sidelines in the last couple of years.

EM’s attractiveness may push FIIs to reconsider India as inflows in 2017 still 40% lower than their five year average

Trailing five year average : | 75400 cr

Source:: Bloomberg, ICICIdirect.com Research

0

2

4

6

8

0

2

4

6

8

10

Mar/09

Sep/09

Mar/10

Sep/10

Mar/11

Sep/11

Mar/12

Sep/12

Mar/13

Sep/13

Mar/14

Sep/14

Mar/15

Sep/15

Mar/16

Sep/16

Mar/17

Sep/17 Earnings Yield ‐1

0‐Year Yield

Yeild

in %

Earnings Yield ‐ 10‐Year YieldS&P 500 Index Earnings Yield (RHS)US Generic Govt 10‐Year Yield

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Sep/09

Mar/10

Sep/10

Mar/11

Sep/11

Mar/12

Sep/12

Mar/13

Sep/13

Mar/14

Sep/14

Mar/15

Sep/15

Mar/16

Sep/16

Mar/17

Sep/17 Ea

rnings Yield Sprea

d (EM ‐DM )

Earnings Yeild in %

Spread (RHS) EM Yield DM Yield

Quaterly Fed ECB BoJ Total LiquidityQ1CY18 ‐60 105 180 225Q2CY18 ‐90 105 180 195Q3CY18 ‐120 105 180 165Q4CY18 ‐150 0 180 30Q1CY19 ‐150 0 180 30Q2CY19 ‐150 0 180 30Q3CY19 ‐150 0 180 30

In US $ billion

4

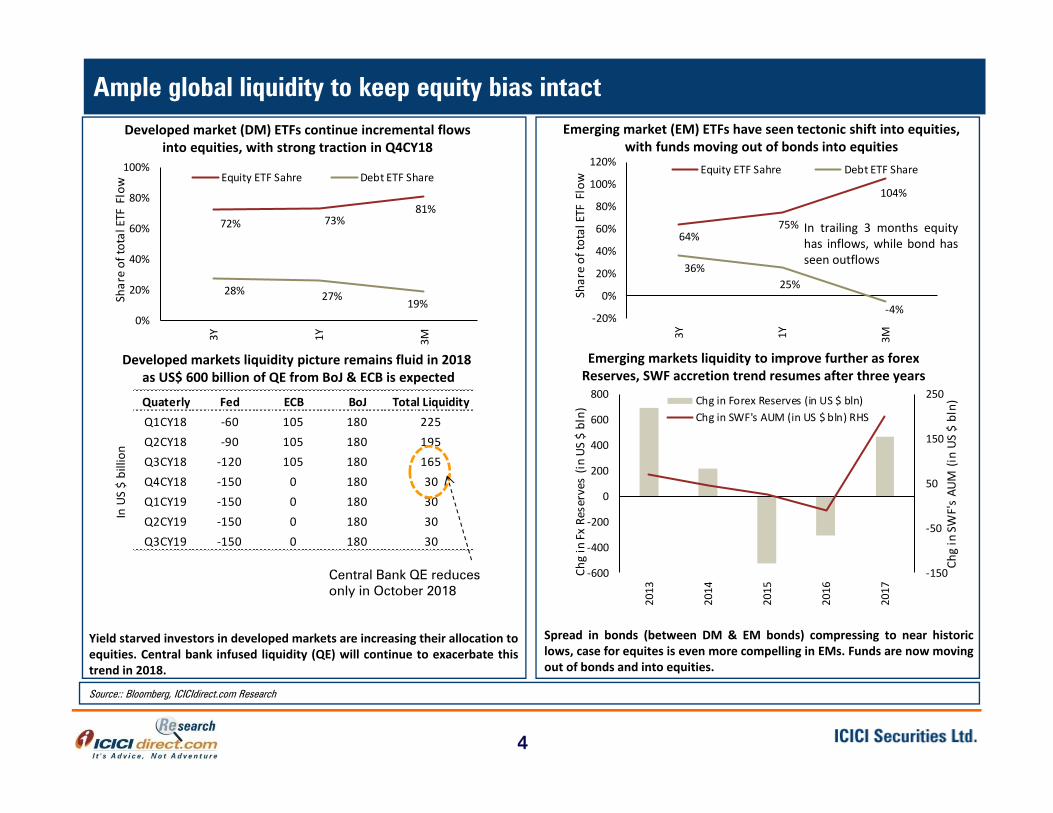

Deal Team – At Your ServiceAmple global liquidity to keep equity bias intactDeveloped market (DM) ETFs continue incremental flows

into equities, with strong traction in Q4CY18Emerging market (EM) ETFs have seen tectonic shift into equities,

with funds moving out of bonds into equities

Yield starved investors in developed markets are increasing their allocation toequities. Central bank infused liquidity (QE) will continue to exacerbate thistrend in 2018.

Developed markets liquidity picture remains fluid in 2018 as US$ 600 billion of QE from BoJ & ECB is expected

Emerging markets liquidity to improve further as forex Reserves, SWF accretion trend resumes after three years

Central Bank QE reduces only in October 2018

Spread in bonds (between DM & EM bonds) compressing to near historiclows, case for equites is even more compelling in EMs. Funds are now movingout of bonds and into equities.

Source:: Bloomberg, ICICIdirect.com Research

72% 73%81%

28% 27%19%

0%

20%

40%

60%

80%

100%

3Y 1Y 3M

Share of to

tal ETF Flow Equity ETF Sahre Debt ETF Share

64%75%

104%

36%25%

‐4%‐20%

0%

20%

40%

60%

80%

100%

120%

3Y 1Y 3M

Share of to

tal ETF Flow

Equity ETF Sahre Debt ETF Share

‐150

‐50

50

150

250

‐600

‐400

‐200

0

200

400

600

800

2013

2014

2015

2016

2017

Chg in SW

F's AU

M (in US

$ bln)

Chg in Fx

Reserves (in

US $ bln)

Chg in Forex Reserves (in US $ bln)Chg in SWF's AUM (in US $ bln) RHS

In trailing 3 months equityhas inflows, while bond hasseen outflows

‐10%‐5%0%5%

10%15%20%25%30%35%

US

German

y

Japa

n

Brazil

S.Ko

rea

Russia

South Afric

a

Malaysia

Indo

nesia

India

% Return

2017 3 Year Average

0

5

10

15

20

25

30

35

40

Jan‐07

Jun‐07

Nov

‐07

Apr‐0

8Se

p‐08

Feb‐09

Jul‐0

9De

c‐09

May

‐10

Oct‐10

Mar‐11

Aug‐11

Jan‐12

Jun‐12

Nov

‐12

Apr‐1

3Se

p‐13

Feb‐14

Jul‐1

4De

c‐14

May

‐15

Oct‐15

Mar‐16

Aug‐16

Jan‐17

Jun‐17

Nov

‐17

Trailin

g P/E

5

10

15

20

25

30

35

40

45

Jan‐07

Jun‐07

Nov

‐07

Apr‐0

8Se

p‐08

Feb‐09

Jul‐0

9De

c‐09

May

‐10

Oct‐10

Mar‐11

Aug‐11

Jan‐12

Jun‐12

Nov

‐12

Apr‐1

3Se

p‐13

Feb‐14

Jul‐1

4De

c‐14

May

‐15

Oct‐15

Mar‐16

Aug‐16

Jan‐17

Jun‐17

Nov

‐17

Trailin

g P/E

5

India not alone, P/E based valuation picture globally above long term average…

Source: Bloomberg, ICICIdirect.com Research

Developed market : Trail P/E based valuation, higher for US

Emerging Market: India, tracking EMs trend of trading at higher than their average

Germany : Current 19.2, Avg 18.1

US : Current 22.4, Avg 17.4

France : Current 18.4, Avg 17.6

S.Africa : Current 18.8, Avg 18.3 Russia : Current 8.5, Avg 8.1

Indonesia : Current 22.4, Avg 21 India : Current 23.4 Avg 18.44

Global Equity returns in 2017 were the best in recent memory

2017 average return of 16% is almost 1.75x of trailing 3 year average returns

6

Deal Team – At Your ServiceYields led P/E re-rating largely done; earnings recovery to be key driver now

Source: Bloomberg, ICICIdirect.com Research

• We highlight that Sensex P/E expansion has been driven by falling yields. The relationship between the P/E ratio and 10 year G‐sec yield isinverse. The key reason for the same is that falling yields lead to lower cost of capital. Hence, this drives the valuation multiple (i.e. high P/Eratio) for the market. We pointed out the above thesis in our last strategy report (find here).

• We expect inflation levels in 2018 at ~4.5%. Adding to it a normalised real interest rate of ~175 bps and further 75‐100 bps markup for 10year G‐sec, we expect the 10 year G‐sec yield to hover close to 7‐7.25% (similar to current levels). Therefore, we believe much of the yieldbased re‐rating is largely done.

• However, going ahead, the key driving force for the market would be earnings recovery (earnings CAGR of ~17.4% in FY17‐20), which willlargely be the function of improving capacity utilisation at corporate level (currently at five year low).

10

13

16

19

22

25

6

7

8

9

10

Sep‐13

Dec‐13

Mar‐14

Jun‐14

Sep‐14

Dec‐14

Mar‐15

Jun‐15

Sep‐15

Dec‐15

Mar‐16

Jun‐16

Sep‐16

Dec‐16

Mar‐17

Jun‐17

Sep‐17

Dec‐17

(x)

(%)

10 Year yield Trailing P/E ratio (RHS)

Earnings growth YoY (%) Avg Trailing P/E (%) Avg 10 yr yield (%)

FY15 ‐0.4 18.9 8.3

FY16 1.2 20.4 7.7

FY17 2.0 19.9 7.5

FY18YTD ‐1.6 22.4 6.7

FY17‐20E 17.4 ~7‐7.25

Sensex companies ex‐ BFSI

22.7 22.0

24.322.5 21.9

15.0

20.0

25.0

FY03 FY04 FY05 FY06 FY07

(%)

EBITDA Margin

Sensex companies ex‐ BFSI

19.220.9

28.625.6 26.8

15.0

20.0

25.0

30.0

FY03 FY04 FY05 FY06 FY07

(%)

ROCE

7

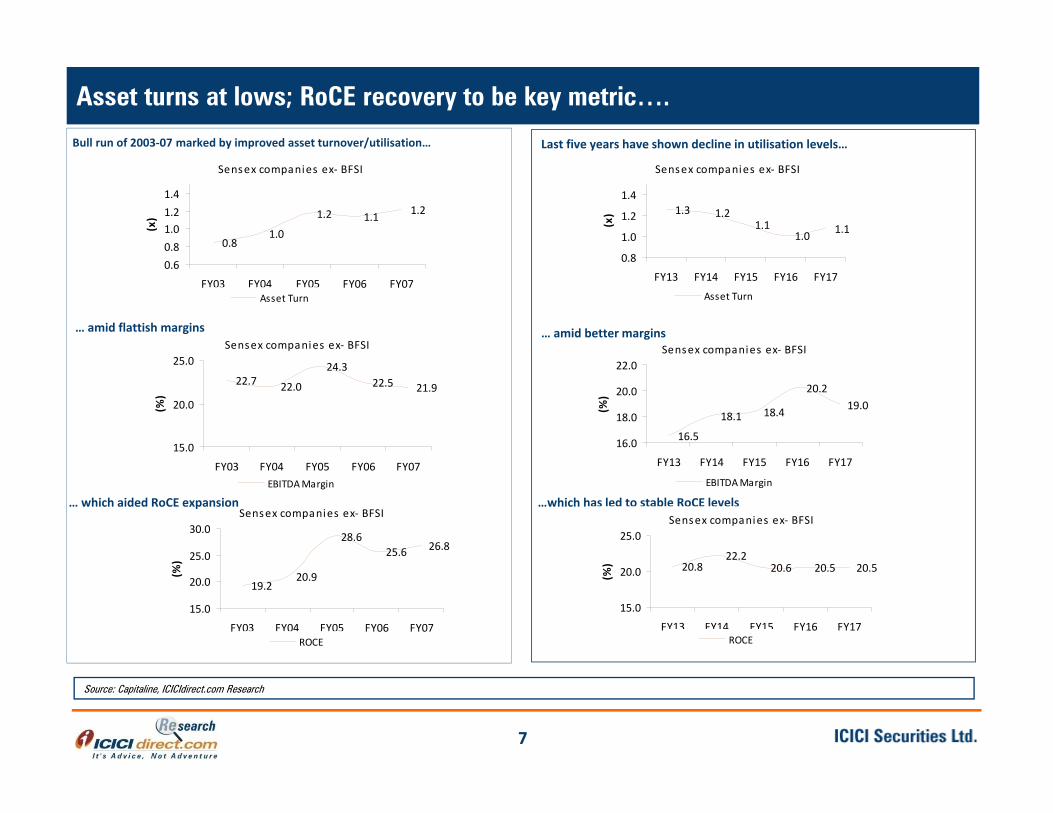

Asset turns at lows; RoCE recovery to be key metric….

Source: Capitaline, ICICIdirect.com Research

Bull run of 2003‐07 marked by improved asset turnover/utilisation…

… which aided RoCE expansion

Last five years have shown decline in utilisation levels…

…which has led to stable RoCE levels

Sensex companies ex‐ BFSI

0.81.0

1.2 1.1 1.2

0.60.81.01.21.4

FY03 FY04 FY05 FY06 FY07

(x)

Asset Turn

… amid flattish margins

Sensex companies ex‐ BFSI

1.3 1.21.1

1.0 1.1

0.8

1.0

1.2

1.4

FY13 FY14 FY15 FY16 FY17

(x)

Asset Turn

Sensex companies ex‐ BFSI

16.5

18.1 18.4

20.219.0

16.0

18.0

20.0

22.0

FY13 FY14 FY15 FY16 FY17

(%)

EBITDA Margin

… amid better margins

Sensex companies ex‐ BFSI

20.822.2

20.6 20.5 20.5

15.0

20.0

25.0

FY13 FY14 FY15 FY16 FY17

(%)

ROCE

3.1 3.1

3.2

3.3

3.0

3.1

3.2

3.3

FY17 FY18E FY19E FY20E

%

Sensex financials core RoAs

22.5

23.6

24.2

24.7

21

22

22

23

23

24

24

25

25

FY17 FY18E FY19E FY20E

%

Sensex RoCE (Ex‐financials)

Sensex RoCE to expand as utilisation levels of India Inc improve

8

• Ex‐financials, Sensex RoCE is expected to expand 220 bps in FY17‐20E to 24.7% by FY20E vs. 22.5% in FY17, leading to earningsCAGR of ~11% over FY17‐20E

• Improvement is envisaged on account of higher sweating of assets and consequent better asset turnovers coupled withoperational leverage benefits in terms of improved EBITDA margin profile

• For financials; core RoAs are expected to improve gradually to 3.3% in FY20E vs. 3.1% in FY17 primarily tracking a revival of creditgrowth. Consequently, BFSI is expected to report a robust ~33% earnings CAGR over FY17‐20E.

338 393 466 506377

168199

222 228241

225236

211 20825679

6955 47

61153200 98

17914538

10279

2153164

165 228 204 2681,165

1,365 1,359 1,375 1,403

‐100

100

300

500

700

900

1,100

1,300

1,500

FY13 FY14 FY15 FY16 FY17

(|)

Banking and NBFC IT Oil and Gas Capital Goods Auto Metals and Mining Others*

Sensex before new stocks addition

Others14%

Auto11%

Capital Goods5%

FMCG10%

Oil and Gas12%

IT12%

Banking and NBFC

37%

Sensex earnings: Sector specific headwinds impacted growth over FY14-17

9

In December 2017, banking stocks replaced two of thepharma stocks in the Index. Consequently, banking sectorweightage in the index increased to ~40% vs. ~37%previously)

Consequently, BFSI is expected to anchor indexperformance

Sensex post stocks additionsOthers 12%

IT11%

Oil and Gas12%

FMCG9%

Capital Goods4%

Auto11%

Banking and NBFC

40%

Earnings during FY14‐17 was largely flat primarily on the back ofthe global meltdown in commodity prices, delay in executionpick‐up in the domestic infrastructure space which led to higherNPAs of Banks and Consequently, higher provisioning leading todecline in their profitability.

New stocks addition to Sensex

338 393 466 506 377540

717883168 199

222 228241

225243

268

225236

211 208256

261

289

323

7969 55 47 61

61

70

83

153200 98 179 145

183

251

282

38102 79

21 5357

72

84

164

165 228 204 268233

271

346

1,165

1,365 1,359 1,375 1,4031,560

1,913

2,269

0

400

800

1,200

1,600

2,000

2,400

FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

(|)

Banking and NBFC IT Oil and Gas Capital Goods Auto Metals and Mining Others*

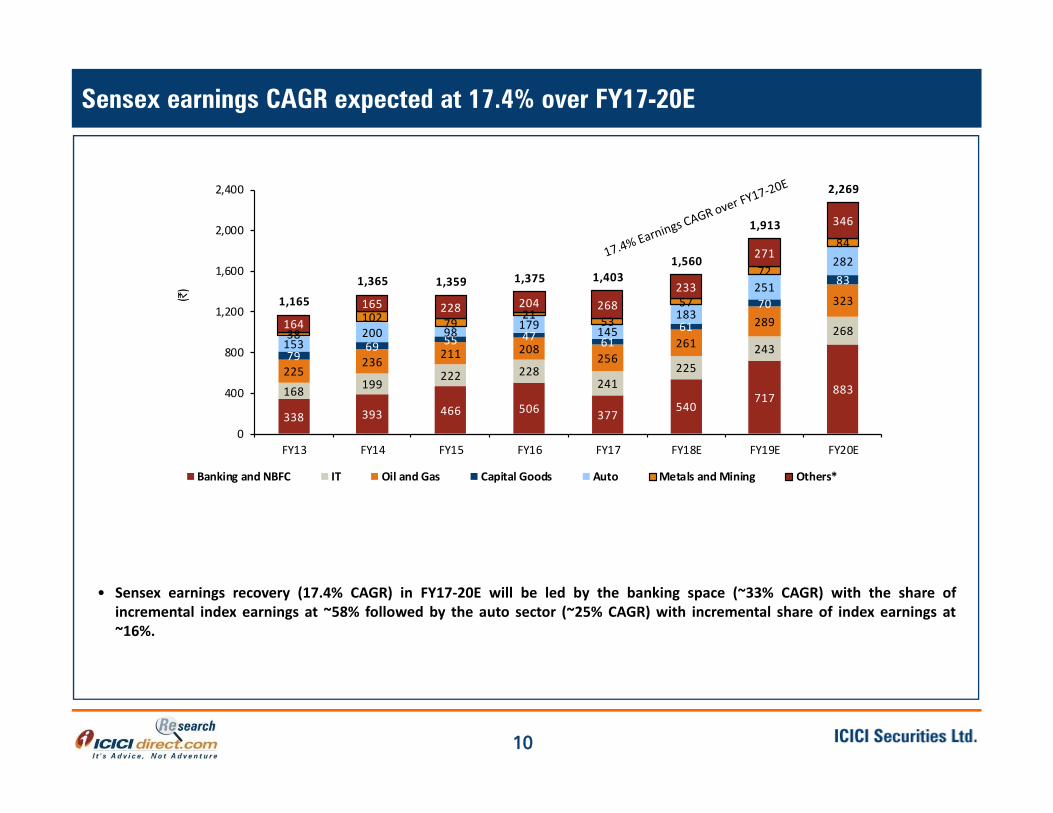

Sensex earnings CAGR expected at 17.4% over FY17-20E

10

• Sensex earnings recovery (17.4% CAGR) in FY17‐20E will be led by the banking space (~33% CAGR) with the share ofincremental index earnings at ~58% followed by the auto sector (~25% CAGR) with incremental share of index earnings at~16%.

Measuring Nifty fair value: SoTP methodology intersects P/E valuation at 11,725

11

• We have tried to evolve 2018 Index target based on bottoms up approach by using a sum of the parts (SoTP) evaluation ofindividual index constituents

• The rationale of such methodology stems from the fact that over the period of time, companies, within the index, with presencein various verticals/businesses have witnessed value unlocking and in such case the concept of SoTP captures the value in a betterway than purely P/E based valuations (especially for businesses where earnings are yet to mature). Moreover, we also note thatsuperior businesses, exhibiting consistent RoCEs, within the index now command higher valuations, while certain businesseswithin the index continue to trade at/below average index multiple .

• Therefore, given the above mentioned limitations of using a P/E purely on overall earnings of index, we have used the sum of theparts (SOTP) technique thereby using our research based target market capitalisation to index constituents and furthermore,taking the average based on the respective free float weightage in the index, to come to targeted index market capitalisation. Theresultant exercise has given us the fair value of Sensex at 37,600 with consequent target for Nifty at 11,725 offering a healthy12% upside from current levels.

• It should be noted that our Sensex target implies target P/E of ~18x on average of FY19 and FY20 earnings(i.e. 1x PEG), which ison the higher end of historical average P/E of ~16‐17x commanded by the market. However, we highlight that improving RoCE isa better metric than PE dissonance during an economic upturn.

FY15 FY16 FY17 FY18E FY19E FY20ESensex EPS 1359 1375 1403 1560 1913 2269Growth (%) ‐0.4% 1.2% 2.0% 11.2% 22.7% 18.6%Earnings CAGR over FY17‐20E 17.4xTarget Multiple (~1.0x PEG) 18.0xSensex Target (using avg FY19‐20E EPS) 37600Corresponding Nifty Target 11725

12.4%

Sensex & Nifty Target

Potential Upside

12

Deal Team – At Your ServiceMarket Strategy 2018

Agrarian focused consumption push to alleviate rural stress

2

Capex revival to be key theme in 2018

3

Amid limited domestic challenge, risks to originate outside

4

Sectoral Outlook

5

Fiscal Policy: Limited space for big bang reform

6

Monetary space: Limited respite on rate cuts ahead

7

Consumption, GFCE to drive GDP growth

8

Market Outlook – 2018 to be the year of Stabilisation1

Top Picks for Strategy 20189

13

GST collections yet to stabilise

Source: Finance Ministry, RBI Handbook of Statistics 2016-17, CBDT, ICICIdirect.com research

GST collections thus far are below our estimate, and we suspect below the revenue neutral rate required. Lower than expected GST collections (and thus, lowerindirect taxes) would be an overhang on fiscal deficit financing. In absence of official estimates for the targeted collections, we arrived at a revenue neutral figureof GST collections by working backwards from combined FY17 indirect tax revenues of the Central and State governments. GST collections would need to matchcomparable indirect tax revenues to ensure zero revenue loss under the new system. According to our estimate, FY17 revenues from indirect tax on items whereGST is now applicable (i.e. excluding petroleum, alcohol and real estate) works out to ~₹ 11.9 lakh crore, or ~ ₹1 lakh crore per month. Post GST implementation inJuly, monthly collection thereof has averaged ~₹ 88000 crore. If collections continue on this path, there would be a shortfall of ~₹ 60000 crore in indirect taxcollections, assuming 8% YoY growth in duties on petroleum and 9% YoY growth in stamp duty collection.However complete clarity is yet to emerge on the implication of initial GST collection from official sources. A possible encouraging aspect to future collections isthe implementation of interstate e‐way bill system on goods valued above ₹ 50000 with effect from February 1, 2018. E‐way bill implementation in states underthe previous system (pre‐GST) had helped boost tax revenues by 15‐20%. E‐way bills on intrastate goods movement will be rolled out from June 1, 2018.Additionally, the impact of composition scheme taxpayers required to file returns on a quarterly basis is yet to accrue.

2.6 2.9 3.7 4.6 5.0

8.6 9.3 11.7 11.9 10.8

1.1 1.2

0.02.04.06.08.0

10.012.014.016.018.020.0

FY14 FY15 FY16 FY17 Hypothetical fullyear post GST

(|lakh

crore)

Duties on petroleum products Combined Indirect Tax collections Stamp duties and registration

Income tax collections boosted

Demonetisation‐impacted H2FY17 saw a rise of 16% in direct tax collections YoY. In comparison, H1FY17 (six months before demonetisation) had recorded a 9%YoY growth over the comparable period. Apart from crackdown on black money, voluntary income declaration schemes, increase in surcharges for higher incomeslabs (above |50 lakh and |1 crore) and fear of action from authorities seem to have provided a boost to collections. In terms of personal income tax collections,the government managed to rake in ~ |3.5 lakh crore from individual tax payers in FY17, a rise of 21% YoY from FY16 collection of ~ |2.9 lakh crore. The totalnumber of tax returns filed by individual assesses during FY17 was 5.43 crore, up 17.3% YoY. 1.26 crore new taxpayers (i.e. return filers and non filers making taxpayments) were added to the tax base. Additionally, FY18 (as of August 5th) has recorded 41.79% YoY growth in personal advance tax collections YoY and 34.25%YoY growth in personal self assessment tax collections.

Month GST collections (₹ crore)

July 94063

August 90669

September 92150

October 83346

November 80808

Total 441036

322.8

356.3

394.7

428.9

453.2

493.9

22.9 22.4 23.224.7

28.2 28.2

‐

100

200

300

400

500

600

FY12 FY13 FY14 FY15 FY16 FY17RE

(In '0

00 cr)

‐

5.0

10.0

15.0

20.0

25.0

30.0

Corporate taxes (In '000 cr) Effective Tax rate (%)

14

Deal Team – At Your ServiceCorporate tax rates to decline gradually as near term fisc is challenged…

Source: Budget documents, ICICIdirect.com Research

Corporate tax cuts to happen gradually with phasing out of various exemptions…•The Finance Minister in his previous Budget 2015 had made clear his intention to cut corporate taxes to 25% gradually over a period to encourage foreign investments and jobs. Inthis direction, the government in the last Budget reduced the tax rate for companies with an annual turnover up to | 50 crore to 25% to promote MSME and encourage firms tomigrate to the company format.•The government had also proposed a gradual phasing out of deductions available to corporate Inc. from FY18 onwards like restricting the benefits of accelerated depreciation to40% from 100%with effect from FY18, limiting the benefit of deductions for research to 100% from 150%w.e.f. FY21, etc.•At present, total incentives availed by corporate Inc. stands at |83,492 crore which is the available headroom for the government to bring down the tax rate. Assuming corporateprofit CAGR of 15% for next three years, the government can still manage to grow its revenue from corporate taxes at 10.4% CAGR even by cutting down the tax rate to 25% asshown in the below mentioned table.•However, in the coming Budget, there is little room for the government to reduce corporate tax rates as clarity is yet to emerge on GST revenue collections. With the phasing out ofmajor profit linked deductions like accelerated depreciation, SEZ, area based deductions, etc., and plugging loopholes in the direct tax systems, the government can gradually bringdown corporate taxes to the desired levels of 25% over a period of time

Breakup of major incentives availed by companies Expected growth in corporate tax revenue @ 25%Tax rate

FY17RECorporate taxes (In cr) ‐ A 493923Effective Tax rate (%) ‐ B 28.2Implied PBT (In cr) ‐ [A/B = C] 1749019Tax tax revenue foregone (| cr) ‐ D 83492Total implied tax revenue ‐ [A+D] ‐ E 577415Expected PBT after 3 years (assuming 15% CAGR growth)

2660039

Tax rate Assumed (%) ‐ G 25.0Corporat tax revenue (F/G) ‐ H 665010Corporate Tax CAGR over 3 years (%) 10.4

(In Cr)Exemption Type FY17

SEZ & Area based 23048

Accelerated depreciation 54345

Scientific Research 10980

Infrastructure 5502

Power 12624

Mineral Oil & Natural Gas 6502

Telecom 1339

Others 10778

Total 125118Recoveries through MAT 41626Net Revenue forgone 83492

Trends in corporate taxes and effective tax rates

15

Deal Team – At Your ServiceGrowth supportive expenditure to lead to fiscal slippages …

Source: ICICIdirect.com Research

Particulars A FY16 FY17RE YoY (%) FY18BE YoY (%) FY18IE YoY (%) CommentsGross Tax Revenues 1455648 1703243 17.0 1911579 12.2 1889702 10.9 Clarity on net revenue from GST is yet to emerge. GST collections of the past three

months have witnessed some moderation due to refunds under IGST. Hence, weexpect shortfall of over ~| 21000 crore in tax revenues from the budgeted target.

Less: State Shares 511883 614450 20.0 684565 11.4 641947 4.5 Net Tax revenue 943765 1088793 15.4 1227014 12.7 1247755 14.6 Non Tax RevenuesDividend 112127 153223 36.7 142430 (7.0) 114684 (25.2) Dividend income to be lower at | 1,14,684 crore mostly lower dividend from RBI

and ONGCEconomic services 91000 129889 42.7 92235 (29.0) 90000 (30.7) Others 48133 51658 7.3 54092 4.7 49500 (4.2) Total Revenue Receipts 1195025 1423563 19.1 1515771 6.5 1505040 5.7 Capital ReceiptsRecovery of Loans 20835 11071 (46.9) 11932 7.8 11000 (0.6) Disinvestments 42132 45500 8.0 72500 59.3 108000 137.4 Disinvestment proceeds are likely to surpass the budgeted target by | 40,500

crore mainly due to extensive stake sales and buybacks of PSEs during this fiscal.This would provide significant cushion in bridging the fiscal gap

Total 62967 56571 (10.2) 84432 49.2 119000 110.4 Total Receipts 1257992 1480134 17.7 1600203 8.1 1624040 9.7

Scheme Expenditure: 725114 869847 20.0 945078 8.6 989624 13.8 The government has planned an additional expenditure of | 66113 crore ( of which | 20532 crore is for fertiliser, | 15908 crore for road transport & highway, etc).Hence, we expect the total expenditure to overshoot the budgeted estimates thisfiscal

On Revenue Account 545619 631511 15.7 674057 6.7 NA NAOn Capital Account 179495 238336 32.8 271021 13.7 NA NAExp other than Schemes: 624010 661491 6.0 678579 2.6 678579 2.6 On Revenue Account 550483 619980 12.6 639799 3.2 NA NAOn Capital Account 73527 41511 (43.5) 38780 (6.6) NA NAInterest payments 441659 483069 9.4 523078 8.3 523078 8.3 Total Expenditure 1790783 2014407 12.5 2146735 6.6 2191281 8.8

On Revenue Account 1537761 1734560 NA 1836934 NA NA NA

On Capital Account 253022 279847 NA 309801 NA NA NAFiscal deficit 532791 534273 NA 546532 NA 567241 NAPrimary Deficit 91132 51204 NA 23454 NA 44163 NAGDP estimates 13567192 15251028 12.4 16847455 10.5 16689300 9.4 Fiscal deficit as % of GDP 3.9% 3.5% 3.2% 3.4% With high focus on inftrastructure, we expect the fiscal deficit to slide marginally

by 20 bps to 3.4% from the budgeted target of 3.2% for this fiscal

16

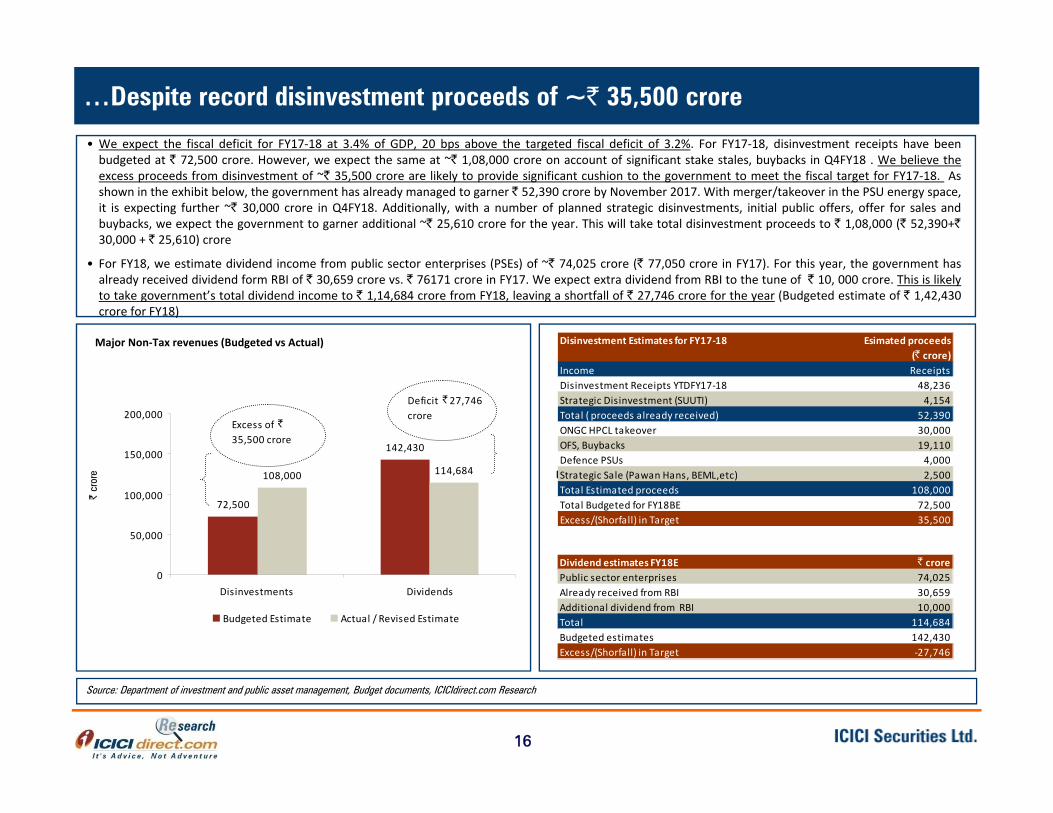

Deal Team – At Your Service…Despite record disinvestment proceeds of ~| 35,500 crore

• We expect the fiscal deficit for FY17‐18 at 3.4% of GDP, 20 bps above the targeted fiscal deficit of 3.2%. For FY17‐18, disinvestment receipts have beenbudgeted at | 72,500 crore. However, we expect the same at ~| 1,08,000 crore on account of significant stake stales, buybacks in Q4FY18 . We believe theexcess proceeds from disinvestment of ~| 35,500 crore are likely to provide significant cushion to the government to meet the fiscal target for FY17‐18. Asshown in the exhibit below, the government has already managed to garner | 52,390 crore by November 2017. With merger/takeover in the PSU energy space,it is expecting further ~| 30,000 crore in Q4FY18. Additionally, with a number of planned strategic disinvestments, initial public offers, offer for sales andbuybacks, we expect the government to garner additional ~| 25,610 crore for the year. This will take total disinvestment proceeds to | 1,08,000 (| 52,390+|30,000 + | 25,610) crore

• For FY18, we estimate dividend income from public sector enterprises (PSEs) of ~| 74,025 crore (| 77,050 crore in FY17). For this year, the government hasalready received dividend form RBI of | 30,659 crore vs. | 76171 crore in FY17. We expect extra dividend from RBI to the tune of | 10, 000 crore. This is likelyto take government’s total dividend income to | 1,14,684 crore from FY18, leaving a shortfall of | 27,746 crore for the year (Budgeted estimate of | 1,42,430crore for FY18)

Source: Department of investment and public asset management, Budget documents, ICICIdirect.com Research

72,500

142,430

108,000 114,684

0

50,000

100,000

150,000

200,000

Disinvestments Dividends

| cr

ore

Budgeted Estimate Actual / Revised Estimate

Excess of | 35,500 crore

Deficit | 27,746 crore

Disinvestment proceeds YTD FY18 at | 52,390 crore

Major Non‐Tax revenues (Budgeted vs Actual) Disinvestment Estimates for FY17‐18 Esimated proceeds (| crore)

Income ReceiptsDisinvestment Receipts YTDFY17‐18 48,236Strategic Disinvestment (SUUTI) 4,154Total ( proceeds already received) 52,390ONGC HPCL takeover 30,000OFS, Buybacks 19,110Defence PSUs 4,000Strategic Sale (Pawan Hans, BEML,etc) 2,500Total Estimated proceeds 108,000Total Budgeted for FY18BE 72,500Excess/(Shorfall) in Target 35,500

Dividend estimates FY18E | crorePublic sector enterprises 74,025Already received from RBI 30,659Additional dividend from RBI 10,000Total 114,684Budgeted estimates 142,430Excess/(Shorfall) in Target ‐27,746

17

Deal Team – At Your ServiceMarket Strategy 2018

Agrarian focused consumption push to alleviate rural stress

2

Capex revival to be key theme in 2018

3

Amid limited domestic challenge, risks to originate outside

4

Sectoral Outlook

5

Fiscal Policy: Limited space for big bang reform

6

Monetary space: Limited respite on rate cuts ahead

7

Consumption, GFCE to drive GDP growth

8

Market Outlook – 2018 to be the year of Stabilisation1

Top Picks for Strategy 20189

18

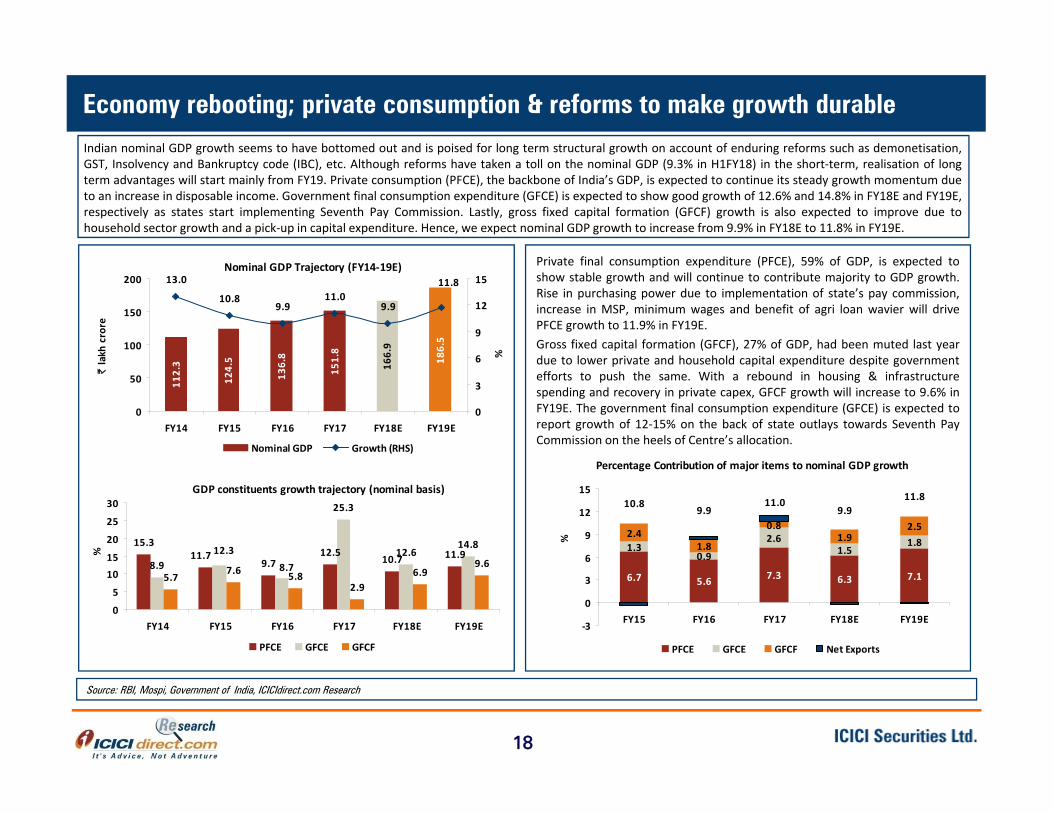

Deal Team – At Your ServiceEconomy rebooting; private consumption & reforms to make growth durable

Source: RBI, Mospi, Government of India, ICICIdirect.com Research

Indian nominal GDP growth seems to have bottomed out and is poised for long term structural growth on account of enduring reforms such as demonetisation,GST, Insolvency and Bankruptcy code (IBC), etc. Although reforms have taken a toll on the nominal GDP (9.3% in H1FY18) in the short‐term, realisation of longterm advantages will start mainly from FY19. Private consumption (PFCE), the backbone of India’s GDP, is expected to continue its steady growth momentum dueto an increase in disposable income. Government final consumption expenditure (GFCE) is expected to show good growth of 12.6% and 14.8% in FY18E and FY19E,respectively as states start implementing Seventh Pay Commission. Lastly, gross fixed capital formation (GFCF) growth is also expected to improve due tohousehold sector growth and a pick‐up in capital expenditure. Hence, we expect nominal GDP growth to increase from 9.9% in FY18E to 11.8% in FY19E.

Private final consumption expenditure (PFCE), 59% of GDP, is expected toshow stable growth and will continue to contribute majority to GDP growth.Rise in purchasing power due to implementation of state’s pay commission,increase in MSP, minimum wages and benefit of agri loan wavier will drivePFCE growth to 11.9% in FY19E.Gross fixed capital formation (GFCF), 27% of GDP, had been muted last yeardue to lower private and household capital expenditure despite governmentefforts to push the same. With a rebound in housing & infrastructurespending and recovery in private capex, GFCF growth will increase to 9.6% inFY19E. The government final consumption expenditure (GFCE) is expected toreport growth of 12‐15% on the back of state outlays towards Seventh PayCommission on the heels of Centre’s allocation.

Nominal GDP Trajectory (FY14‐19E)

112.3

124.5

136.8

151.8

166.9

186.5

13.0

10.89.9

11.09.9

11.8

0

50

100

150

200

FY14 FY15 FY16 FY17 FY18E FY19E

| lakh

crore

0

3

6

9

12

15

%

Nominal GDP Growth (RHS)

GDP constituents growth trajectory (nominal basis)

15.3

9.712.5

10.7 11.98.9

25.3

12.614.8

5.77.6 5.8

2.96.9

9.611.7

8.712.3

0

5

1015

20

25

30

FY14 FY15 FY16 FY17 FY18E FY19E

%

PFCE GFCE GFCF

Percentage Contribution of major items to nominal GDP growth

6.7 5.6 7.3 6.3 7.1

1.30.9

2.61.5

1.82.4

1.8

0.81.9

2.5

10.89.9

11.09.9

11.8

‐3

0

3

6

9

12

15

FY15 FY16 FY17 FY18E FY19E

%

PFCE GFCE GFCF Net Exports

19

Deal Team – At Your ServiceTraction in disposable income & state pay commission to drive consumption…

Source: RBI, Mospi, Government of India, media articles, ICICIdirect.com Research

Private financial consumption expenditure (PFCE) has been the key growth driver of GDP last year driven by the central government’s Seventh Pay Commissionand a steady rise in rural income. In FY18E, we expect marginally lower PFCE growth at 10.7% given the GST transition phase and higher base of last year. Thestate pay commission is expected to result in government final consumption expenditure (GFCE) growth at 14.8% in FY19E. This, in turn, is expected to lead to anuptick in consumer spending. In addition, agri loan waiver, likely hike in minimum support price and rural wages are likely to drive PFCE growth to 11.9% in FY19E.

Agri loan waiver and increase in disposable income are expected to providesupport to food & beverages consumption and basic housing needs, whichcontribute ~45% to PFCE. Also, robust growth in consumption of clothing &footwear (7% of PFCE), transport & communication (18%) among others areexpected to lead to improvement in private consumption growth.

State/ Center Outstanding agri loans Waiver Amount

UP 86241 36359

Maharashtra 252062 30500

Punjab 70141 10000

Karnataka 95557 8165TOTAL 504001 85024

States where farm loan waiver is announced (| crore)

PFCE growth will continue to remain strong110.6

98.889.3

79.372.3

64.8

22.919.917.714.113.011.6

0

25

50

75

100

125

FY14 FY15 FY16 FY17 FY18E FY19E

| lakh

crore

0

6

12

18

24

30

%

PFCE GFCE PFCE growth (RHS) GFCE growth (RHS)

State Total ex‐chequer (| crore)

Uttar Pradesh 27000

Maharashtra 18000

Tamil Nadu 14700

Rajasthan 10400

TOTAL 70100

States which has announced implementation of 7th Pay commission

% Increase YoY % of GDP FY13 FY14 FY15 FY16 FY17 FY18E FY19EEmployees Compensation 7.6 12.0 11.8 10.9 12.2 28.8* 14.5 17.5GFCE 11.7 9.7 8.9 12.3 8.7 25.3 12.6 14.8

Government expenditure on employees

* Icicidirect.com estimates

After the central government’s implementation of Seventh Pay Commission,states are also likely to follow suit by increasing expenditure towards salariesand pension. Some of the states have already announced the budget forincremental salaries and wages. Initial figures suggest the release ofincremental | 70,000 crore from some of major states. This can go up to | 2lakh crore with implementation across all states. We expect expenditure ofstates on salaries and wages to increase sharply at 19.3% in FY19E.Also, HRA dues to the tune of | 30000 crore and | 10000 crore for teachers inUGC funded universities and colleges, respectively, lined up for paymentbetween H2FY18 and FY19E is likely to increase the quantum of GFCE. Assalaries and wages constitutes ~65% of the GFCE, hike in the same wouldstimulate consumption over the next couple of years. Hence, we expect theGFCE to increase at 12.6% and 14.8% in FY18E and FY19E, respectively.

20

Deal Team – At Your ServicePickup in private investments will start recovery in the capex cycle

Source: RBI, Mospi, Government of India, ICICIdirect.com Research

The Gross Fixed Capital Formation (GFCF) component in GDP has witnessed slower growth in the last few years due to subdued investments from privatesector & household sector which constitute ~38% and ~37% of the GFCF, respectively. Majority of the growth in GFCF over the last few years was contributedby the increased spending by the government. The public sector spending which is ~25% of GFCF had played a vital role in the growth. The public sector GFCFpie in overall GFCF has grown from ~21% in FY13 to ~25% in FY16 on the back of government’s thrust on infrastructure. However, given the fiscal constraints ofthe government, we expect the growth rate of government’s public spending to get normalised in the coming years.

Going ahead, we expect private sector capex (~38% of the GFCF) and spending on the household sector and will play a more important role in recovery of GFCFgrowth. The private sector growth revival is on the cards due to recovery in the manufacturing sector which accounts for 35% of private GFCF. Manufacturingcapex will pick up on the back of pent‐up demand post the disruption caused by demonetisation and GST implementation. The private investment could seeuptick in investment possibly in late 2018 as there are early signs of corporate balance sheet repairs. Furthermore, relatively lower interest rate along withimprovement in policy reforms makes the business environment conducive for private investment in infrastructure. The public sector spending will continue togrow steadily on account of planned investments in infrastructure projects besides defence & public administration. Overall, we expect GFCF growth torecover to 9.6% in FY19E.

35.2 37.8

40.0

41.2

44.0

48.35.7

7.6

5.8

2.9

6.9

9.6

0

2

4

6

8

10

0

10

20

30

40

50

FY14 FY15 FY16 FY17 FY18E FY19E

%

|lakh

crore

GFCF on the road to recovery

Gross Fixed Capital Formation (GFCF) Growth (RHS)

(| lakh Crore)FY08‐12Actual

FY13‐17NITI Aayog

FY18‐22E I‐direct estimates

Power 7.8 12.7 7.1

Railways 2.0 3.8 8.6

Airports & Ports 0.8 0.9 2.0

Highways 4.6 7.6 7.0

Urban & Others 8.6 12.2 24.2

TOTAL 23.8 37.2 48.8

GFCF drivers going ahead

21

Deal Team – At Your ServiceMarket Strategy 2018

Agrarian focused consumption push to alleviate rural stress

2

Capex revival to be key theme in 2018

3

Amid limited domestic challenge, risks to originate outside

4

Sectoral Outlook

5

Fiscal Policy: Limited space for big bang reform

6

Monetary space: Limited respite on rate cuts ahead

7

Consumption, GFCE to drive GDP growth

8

Market Outlook – 2018 to be the year of Stabilisation1

Top Picks for Strategy 20189

22

Real interest rate within RBI range, to maintain status quo on Repo rate

Source: Bloomberg, ICICIdirect.com Research

• Inflation over the last year has been significantly impacted by many one‐offevents like demonetisation, GST and HRA. RBI has categorically mentionedthat they will look through the impact of these one‐off events. RBI expectsCPI inflation to average ~4.7% in FY19 including central HRA impact. Ourestimates suggest HRA impact to be around 30 bps. Therefore, normalisedinflation at ~4.4% may not be a significant concern given its durable targetof 4.0%. We draw comfort from the fact that when inflation wasundershooting RBI’s expectation in recent months, it refrained fromfurther rate cuts. Hence, RBI should not hike rates for minor overshoot also

• We have tried to analyse the future rate action by RBI with real rateassumption of 1.75% and average inflation range for year 2018 at 4.25% to4.75%

• We expect RBI to maintain status quo on repo rate at 6.0% during CY18.While we do not expect a further rate cut, we also do not expect a reversalin the interest rate cycle in the near future

• The recent up move in G‐sec yield with 10 year yield moving to ~7.30% ismore of a retracement of bullish positioning as investors adjust from adeclining rate cycle to a prolonged status quo phase in benchmark rates.Considering the 10 Year G‐Sec yield spread over repo at 100‐125bps, weexpect 10 year G‐Sec yield to trade in the range of 7.0%‐7.25%

• RBI has indicated to maintain real interest rate in the range of 1.25%‐2.00%.RBI earlier said the equilibrium real interest rate in India was 1.5‐2.0% but itsubsequently brought down the range to 1.25%

• Real interest rate is the difference between nominal interest rate andinflation. Nominal interest rate as indicated by RBI is the yield on 1‐YearGovernment security while headline CPI is being considered as inflation

• Currently with one‐year T‐bill rate at 6.4%, implied real interest rate is at1.9% assuming average CPI inflation for 2018 at 4.5%. Historically, 1‐year G‐Sec yield has traded 25bps above Repo rate indicating normalised level of6.25% at current Repo rate of 6.0%. Therefore on a normalised basis, realrate comes to 1.75%, in line with RBI’s expectation.

0

100

200

300

2014 2015 2016 2017 2018E

Current normalised real rate at 1.75% is within the RBI indicated range of 1.25% to 2.00% Best Case Base Case Worst Case

Real interest rate as indicated by RBI 1.75 1.75 1.75Average inflation expectation for 2018 4.25 4.50 4.75Impl ied nominal rate (Inflation + Real rate) 6.00 6.25 6.50Indicated nomina l rate by RBI (1Yr G‐Sec) 6.25 6.25 6.25Impl ied Repo rate (Impl ied nominal rate minus 25bps , his torica l ly lower than 1 Yr G‐Sec by 25bps) 5.75 6.00 6.25Current Repo rate 6.00 6.00 6.00Further Repo rate action by RBI (bps) ‐25 0 25

RBI Repo rate projection (%)

• India is still evolving in terms of fixing real interest rate regime. Given thewide range, scope of subjectivity in terms deciding Repo rate level hasincreased.

23

Scope for banking system to lower rates remains…deposit repricing effect still at play

Source: RBI, Bloomberg, ICICIdirect.com Research

New external benchmarking of MCLR to lead to faster transmission:The banking system in India has lagged timely and effective transmission of RBIbenchmark rate movement into lending rates. While moving from base rate toMCLR has resulted in slightly better transmission, external benchmarking rulemay have a far better effective transmission mechanism.Though term deposits re‐pricing has happened to the tune of 195 bps,transmission through MCLR is restricted to ~110 bps by banks. Repo rate cutduring the same period of December 2014‐September 2017 was 200 bps.

The proposed external benchmarking of MCLR rate warrants banks to use externalrates (T‐bill/ CD rates/repo rate) rather than current internal rates like banks owncost of funds while determining their lending rates. Also, the reset period is beinglowered to a month/quarter from a year to ensure faster transmission of anychange seen in external rates..

(200)

(150)

(100)

(50)

-Repo rate

Wtd Avg term deposit rate

Wtd Avg term o/s rupee loans

(bps)

Deposit growth to continue even at lower rates, re-pricing to persistDeposits are expected to continue to be repriced lower on renewals with freshgrowth continuing at ~8‐10% even at current lower rates. Savings bank interestrate reduction of 50 bps by banks also resulted in a decline in their cost ofdeposits. Therefore, a consistent decline in deposit costs for banks along withinitial lower transmission can offer scope for lowering lending rates by ~15‐20bps (within overall 40 bps expected), going forward.The medium term effect of demonetisation and other digital reform initiativesby the government in moving towards a less cash economy is likely to continueto fuel growth in low cost deposit in the banking and financial system.Declining share of physical assets is expected to keep deposit inflows high.

While repo & deposit rates are down 200bps, lending rates are down only 110 bps

Market rates like treasury yield/CD rate largely move with repo rate

While we expect RBI to maintain status quo on benchmark rates for most of year 2018, we believe there is still scope of lower lending rates in the banking system. Lowercredit cost in terms of lower provisioning, repricing of deposits at lower rates and structural reforms like lower cash to GDP ratio, increased digital transactions, increase inmerchant discount rate (MDR) rates expected to cut losses, benchmarking of lending rates to marginal cost lending rate (MCLR) provide scope for further rate transmission.We estimate scope of further reduction of ~40 bps in the banking system in a gradual manner particularly in corporate lending rate. {assumed 40 bps = 20 bps fromdeposits + 15 bps from provisions + 5 bps from lower opex}

These external benchmarks reflect RBI’s Repo rate & liquidity changes fasterMarket rates like treasury yield or bank CD rates move faster with change inrepo rate. Therefore, the new proposed external benchmarking mechanism, ifimplemented, will lead to effective and timely transmission of interest ratechanges by the banking system to the borrowers.

0

5

10

15

20

25

30

35

May‐10 May‐11 May‐12 May‐13 May‐14 May‐15 May‐16 May‐17

(%)

12M CD 1Yr T‐bill Repo (RHS)

24

Higher NPA provisions impact bank’s ability to lower rates, resolutions at IBC eyed

Source: RBI, Bloomberg, ICICIdirect.com Research

Apart from deposits, higher credit cost (provisions) largely prevented faster and higher rate cuts by the banking system. Expected IBC resolutions may offer room,wherein our hypothetical analysis offers 15‐20 bps room due to the same.

Higher credit cost prevent rate cut transmission: While pre‐provisioning profitsof the banking system continue to grow at a steady growth of ~12%,provisioning have increased significantly from around | 90000 crore in FY15 to| 222000 crore in FY18E. Provision as percentage of pre‐provisioning profithas nearly doubled to 81% from 46% in the last three years as a result ofhigher provisioning. Higher credit cost or provisioning has prevented banksfrom taking higher lending rate cuts hampering the transmission of lowerrates to the system.

Accordingly, the government and regulator have pressed the pedal toaccelerate resolutions, to resolve asset quality concerns pushing banks to fileRBI specified cases to NCLT under IBC code.

Of ~ | 8.4 lakh crore bad loans currently, the top 12 accounts by valuecontribute ~| 2.5 lakh crore and have been referred to NCLT (‘NCLT ‐ RBI List 1accounts’). Majority of these accounts are from the steel sector. An uptick indomestic prices and steel demand over the last couple of years has improvedthe sector outlook making it more appealing for potential bidders.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

50000

100000

150000

200000

250000

300000

FY13 FY14 FY15 FY16 FY17 FY18E

(%)

| cr

ore

Provision PPOP Prov/PPP (%)

Provision/PPOP at ~81% seems to have peaked out….

Sensitivity analysis of NCLT List 1 accounts on banking networthIn the banking context, we have tried to do a sensitivity analysis ofimpact of haircuts on the net worth of banks. Currently, bankshave provided ~50% of the hit required in NCLT ‐ RBI List 1 cases.According to our estimates, every 10% reduction/increase in thehaircut, achieved through resolution process will impact net worthof banks to the tune of +3%/‐3%, respectively. This gain/hit inprofitability through write‐back or higher provisions (and thus networth) would reflect on financials of banks within a subsequentquarter or two.

HaircutNetworth (₹ lakh crore) Impact on Net Worth

30% 8.90 6%40% 8.65 3%50% 8.40 0%60% 8.15 -3%70% 7.90 -6%

25

…lower incremental provisions, digitisation to aid further transmission

Source: RBI, Bloomberg, ICICIdirect.com Research

The amount of provisions from FY19E onwards is largely expected to decline as resolutions from IBC kick in while probability of fresh large scale NPA additionsalso remain meagre. Lower incremental provisions are expected to lead to lower credit cost. Assuming credit cost at 2.1% (similar levels in FY15)from 3.1% now,provisioning amount reduces by ~| 40000 crore. Assuming NIMs and other variables constant, this factor alone leads to an impact of lowering ~30 bps onlending rates by banks. Factoring that provisions were higher for PSU banks than private peers, a 15 bps cut can be expected at the industry level led by thesavings on provisions alone.

Expected lower provisioning to lead to reduction in lending rates

Push towards digitisation likely to lower cost of funds structurally

The cost of cash to the financial system such as handling, security and opportunity cost is around 1.3% of GDP. The government agreeing to bear merchantdiscount rate (MDR) charges for two years on transactions up to | 2000 likely to expedite usage of digital modes like cards/ UPI/ wallets, etc. A reduction in usageof cash will lead to saving of this cost (operational overheads) to the banking system.

3.1

2.1

~100 bps decline in credit cost at 2.1%....

10.0%

9.6%

...factoring in higher provisionborne by PSB, on reversals atsystem level, scope for ~15 bpstransmission exist

..assuming other variables constant, banking yield onadvances can be brought down by ~30 bps

Hypothetical case study of 100bps fall in credit cost (provisions as a % of advances)

26

Deal Team – At Your ServiceMarket Strategy 2018

Agrarian focused consumption push to alleviate rural stress

2

Capex revival to be key theme in 2018

3

Amid limited domestic challenge, risks to originate outside

4

Sectoral Outlook

5

Fiscal policy: Limited space for big bang reform

6

Monetary space: Limited respite on rate cuts ahead

7

Consumption, GFCE to drive GDP growth

8

Market Outlook – 2018 to be the year of Stabilisation1

Top Picks for Strategy 20189

1201

93

1125

07

1047

63

9141

6

7913

7

1236

5

2418

8

2614

6

2403

86

0

50000

100000

150000

200000

250000

300000

1993

‐94

1999

‐00

2004

‐05

2011

‐12

2012

‐13

2013

‐14

2014

‐15

2015

‐16

2022

‐23E

( |)

95 9580 75

40 38

2.4 3.914.4 14.8

5565

0

20

40

60

80

100

US WesternEurope

Russia Brazil India China

(%)

Mechanization Rate Population engaged in agriculture

2924

2229

1908

1338

1046

0500

10001500200025003000

Uttar

Prad

esh

Mad

hya

Prad

esh

Andh

raPrad

esh

Tamil

Nad

u

Karnataka

( | Bn)

27

The consumption story in India would be supported by rural income levels, which are still a fifth of the national average. In the wake of a mere one and half yearsbeing left for general elections, the government’s thrust will be on increasing farmer’s income considerably next year by way of supporting better crop realisation.Initiatives like eNam and setting up of mega food parks is likely to reduce the disintermediation cost by 25‐30%, which could well be the single most important factorin increasing farmer’s income immediately. However, the initiatives towards increasing the yield like micro irrigation, farm mechanisation are a long drawn process,which would yield results over the next decade. Moreover, the government’s thrust on warehousing and cold storage would indirectly benefit large agri states in Indiaby eliminating the agri waste. India’s five major agri states contribute >40% of the total net state value added (NSVA). Given the higher contribution of agriculture inthese states coupled with the large rural population, the difference between the rural per capita household income is much lower than the national average. Webelieve effective implementation of these initiates in top agri states would boost rural income levels

Deal Team – At Your ServiceFocus on productivity to boost rural income

Source: Government of India, World bank, Ministry of Agriculture, ICICIdirect.com research

Target to double the farm household income

Per hectare yield of different crops in India vis‐à‐vis other countries

Rice/ Paddy

(tonnes/hec)

Wheat(tonnes/hec)

Coarse Grain

(tonnes/hec)

Corn Area

(tonnes/hec)

Barley(tonnes/hec)

Egypt 8.2 Egypt 6.4 USA 10.3 USA 11.0 USA 4.2USA 8.1 China 5.3 Argentina 7.1 Argentina 8.4 China 4.0China 6.9 US 3.5 China 5.8 China 6.0 SA 4.0Vietnam 5.7 Brazil 3.2 Vietnam 4.6 Brazil 5.6 Brazil 3.9Indonesia 4.8 India 2.9 Philippines 3.0 Vietnam 4.6 Argentina 3.8India 3.8 Pakistan 2.8 Brazil 5.5 Indonesia 3.2 Mexico 3.0Thailand 2.8 Iran 2.3 India 1.8 India 2.7 India 2.7World 4.5 World 3.4 World 4.2 World 5.8 World 3.06

Mechanisation rate vs. Population engaged in agriculture

India’s major agri led states which account >40% of total NSVA* (FY17)

AP7%

Gujurat5%

KA5%

MP7%

MH7%

TN2%

Others67%41

905

1015202530354045

Sanc

tion

ed

Ope

ration

al

(Nos)

28

Deal Team – At Your ServiceCreating requisite infra to improve agri demand supply dynamics

Source: MoFPI , ICICIdirect.com Research

Investment in food processing industry to minimise agri products wastage

34% of mega food parks have been sanctioned in six major agri states

In India, ~20% of the crop produced by the farmer does not reach the end consumer, which leads to a loss of ~ | 92,000 crore. This translates to an urgent need forcold storage facilities across major agri producing states in India. Some of the major initiatives to boost the demand for agri products and reduce wastage isinvestment in cold chain facilities & mega food parks. The government has allocated land for 41 mega food parks out of which nine are operational (remaining 32parks to be operational by 2019). Simultaneously, 100 cold chain stores are operational since 2008 while further 136 are under implementation. Total investment inmega food park and cold chain storage has been more than | 10000 crore. Setting up of mega food park and cold chain storage facility would not only reduce thecrop wastage significantly but also result in additional agri produce demand and better realisation through food processing sector.

Total 60% of cold chain capacity concentrated in five states

13.6

5.9

2.3 2.0

1.6

42.3

05

1015202530354045

UttarPradesh

WestBengal

Gujarat Punjab AndhraPradesh

India

(million tonn

es)

Operational Projects Under Implementation No of Projects No of Projects

Fruits & Vegetables 66 72Dairy 19 41Meat / Poultry / Fish 7 18Mixed (Horti & Non Horti) 4 5Irradiation 4 0Total 100 136

Sector

Food Processing Industry

Fruits & Vegetable

Milk FisheriesMeat Poultry

35%

21%

6% 6%2%1% 2%

5% 4%

18%

Processing level Wastage

Higher Processing level

Lower Wastage

Upcoming cold chain facilities to reduce crop wastage

The new cold chain projects will create additional capacity of 2.76 lakh MT of cold storage

29

Deal Team – At Your ServiceUniversal basic income: To boost farm income, benefitting rural economy…

Source: Budget Documents , ICICIdirect.com Research

•Over the years, one of the primary objectives of the Government of India hasbeen to alleviate poverty. India has been able to reduce the number of peopleunder poverty line from 70% at the time of independence to 22% in 2011‐12(according to Tendulkar Committee). However, 22% still counts for more than 25crore people under the poverty line, which is equivalent to fourth largest countryin the world. Hence, India is currently looking at UBI from an angle of povertyelimination. UBI (when implemented) has the potential to reduce the incomeinequality, especially in rural areas. UBI has the capability to increase the famer’sincome thereby benefiting the rural economy at large. In current context, in thelonger run UBI has the potential to play role of a catalyst in eliminating poverty inone leap.•Universal basic income is guaranteed income that acts as a cushion to surviveeven under extreme circumstances. By definition, UBI has three components,universality, un‐conditionality & agency. Putting it simply, it is a periodicunconditional cash payment to all individuals without any work requirement. UBIis also a natural extension after the success of direct benefit transfers (DBT) forsome centrally sponsored schemes. Simultaneously, it is advocating efficacy byreducing waste in implementing government welfare schemes

•According to 2011‐12 Tendulkar Committee, poverty line was defined as | 893per month, which comes to | 5400 per year. Adjusting for inflation, the sameshould be | 7620 per year in 2016‐17. Hence, to reduce the poverty line from22% to 0.5%, the government is required to provide per year basic income at |7620, which would translate into government outgo of | 9.9 lakh crore (6.5% ofGDP). However, with the targeted 75% of the population, the outgo will be | 7.4lakh crore, which is 4.9% of the 2016‐17 GDP.

•One of the biggest benefits of UBI is eliminating poverty completely at one gogiven minimum basic income (an amount that keeps people above poverty line)would be provided to every citizen. The government needs to spend ~5% of GDPto implement universal basic income. To garner the resources for this, it iscrucial to replace the various welfare schemes with UBI•The Union Government spends 5.2% of GDP, which accounts for ~ | 7.8 lakhcrore, in various welfare schemes & subsidies. It also spends 1.0% of GDP on themiddle class as subsidy in railways fares, LPG, personal income tax exemption,etc. Moreover, the government also spends 0.7% of GDP on education, publichealth, sanitation & family welfare. In total, the government spends more than7% of GDP on various schemes. While the government needs to continue someschemes, which are inherently essential for social development, the resourcesallocated to some of the other subsidies and welfare schemes can be utilisedtowards UBI•One of the concerns of UBI is that a minimum guarantee could make people lazyand lead them to opt out of labour market. Hence, UBI, with an exclusion list,could be a solution to this problem. The government can create an exclusion liston the basis of ownership of key assets like automobile, air conditioners or bankbalance beyond a certain amount. It can also appeal to people to ‘give it up’similar to the LPG ‘give it up’ programme. The other option could be toimplement UBI only for women. This would not only reduce the fiscal cost inproviding basic income to half but would also empower women and can be usedas a deterrent toward discrimination against women. Giving money to womenalso improves their bargaining power within households and reduces concernson money being splurged on conspicuous goods (liquor, tobacco, etc)•UBI, if implemented appropriately, can revolutionise the structure ofgovernment welfare schemes, subsidy distribution and eradicate poverty, to agreat extent

63.5

49.6

72.3

58.8

40

50

60

70

80

90

Electric Fan Television

(%)

Rural India

30

Deal Team – At Your ServiceRise in rural income to spur consumption through agri heavy states

Source: Government of India, ICICIdirect.com Research

NSVA growth in agri & allied activity vs. tractor growth in FY17

6.817.5

31.3

3.8

16.37.9

20.2

51.7

29.9

4.2

19.7 18.0

0102030405060

Tamil

Nad

u

Andh

raPrad

esh

Mad

hya

Prad

esh

Karnataka

Uttar

Prad

esh

India

(%)

Agriculture, Forestry and Fishing Tractor sales growth

4.0

6.0 6.1

8.6

12.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

MadhyaPradesh

Karnataka AndhraPradesh

UP Tamil Nadu

(%)

02468101214161820

(%)

India

Household penetration of refrigerator in agri led states vs. India

16.719.4

23.825.7

32

0

5

10

15

20

25

30

35

MadhyaPradesh

Karnataka AndhraPradesh

UP Tamil Nadu

(%)

0

5

10

15

20

25

30

(%)

India

Household penetration of motorised wheeler in agri led states vs. India

The household penetration of consumer goods (refrigerator, fans, television) & motorised vehicles in major agri states is abysmally low, as lower rural per capitaincome in these states (vs. the national average) is impacting discretionary spending. The increase in rural income through various government initiatives, bettermonsoon in the last two years & possible implementation of UBI would simultaneously result in higher rural demand for consumables. We believe the first levelsof consumption growth would be visible in tractors, two‐wheelers and household appliances in these major agri states. With ~35% of consumption coming fromrural areas and more than 70% of the workforce employed in rural India, lifting rural economic growth is critical for overall growth of the durable industry.

Household penetration of consumer durable goods

31

Deal Team – At Your ServiceMarket Strategy 2018

Agrarian focused consumption push to alleviate rural stress

2

Capex revival to be key theme in 2018

3

Amid limited domestic challenge, risks to originate outside

4

Sectoral Outlook

5

Fiscal Policy: Limited space for big bang reform

6

Monetary space: Limited respite on rate cuts ahead

7

Consumption, GFCE to drive GDP growth

8

Market Outlook – 2018 to be the year of Stabilisation1

Top Picks for Strategy 20189

3.7 3.5 4.5 6.6 4.5 100.0

2.5

5.0

7.5

10.0

12.5

15.0

FY14 FY15 FY16 FY17 8MFY18 Over next 3yrs

(| la

kh c

rore

)

Trend in Tendering Activity

Looking at historical trend and goverment spending targets, our rough calculation indicates that tendering activity should pick up to | 10 lakh crore pa over next three years

21.0% CAGR

With government's focus on infrastructure, a pick-up in tendering activity at a CAGR of

21% was witnessed in last few years

7.0 16.823.9 26.5

46.5

48.4

1.3

8.67.1

2.620.0

1.9

Roads Ports Railway Power Urban Infra Housing Defense Total

| la

kh c

rore

Possible Infrastructure spend over the next 5 years

Verticalwise break up of Tendering

11

17

7

13

0.7

56

58

58

57

49

8

9

12

10

11

3

2

2

1

2

5

2

2

10

5

4

7

24

8

6

12

9

12

2 5

0 20 40 60 80 100

FY14

FY15

FY16

FY17

8MFY18

(%)

Power & Distribution

Renewable Energy

Roads

Railways

Airports

Ports

Real Estate

Irrigation

32

Infrastructure investment could jump up to ~| 48 lakh crore based on our bottom up approach mainly led by investment in housing, roads and railways over thenext five years . This implies 10% CAGR in infrastructure spending in the next five years. Consequently, we expect infrastructure spending as percentage of GDP toinch up to 6% in the next five years vs. 5.6% in previous five years. However, we believe tendering activity needs to jump up to | 10 lakh crore over next threeyears to achieve desired infrastructure spending outcome. In our view, increased infrastructure spending could improve the GDP growth rate by 80 to 100 bps.

Tendering all set to firm up amid mega infrastructure spending!!!

Source: Niti Aayog, Project Today ICICIdirect.com Research *Derived from Niti Aayog *assuming GDP growth rate of 7% pa

1.0

1.5

2.0

2.5

3.0

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

(x)

Debt to equity (x) of Infra & Engg Universe of 66 companies

Tendering break-up by ownership (%)

99.8 99.7 99.7 99.8

0.2 0.3 0.3 0.20

25

50

75

100

FY15 FY16 FY17 8MFY18

(%)

Government share Private share

33

Private investment in infra – Revival on the cards…

Source:Project Today, Capitaline, Press reports, ICICIdirect.com Research

Private Investment

Strong Economic Growth

Banks Recapitalization to boost investment

Favorable Business & Regulatory Environment

Low Interest Rate

Corporate Balance

Sheet Repair

Triggers for revival in private investment are in place

While tendering activity was dominated by the government, participation of privateplayers in tendering activity was very limited in the last three to four years due tohigh leverage and elevated interest rate scenario along with uncertainty over policyframework. However, we believe private investment could see uptick in investmentpossibly in late 2018 as there are early signs of corporate balance sheet repairs.Furthermore, relatively lower interest rate along with improvement in policy reformsmakes the business environment conducive for private investment in infrastructure.

Sector Key reforms making business enviroment conducive for pvt. investment

Road Introduction of hybrid annuity model leading to lower equity requirement for private players

To improve liquidity of private players, the government passed ordinance for payment of 75% of arbitration claims where initial ruling is in favour of private players

Introduction of new funding avenues such as investment trusts (InVITs) to free up capital

PowerThe government is planning to amend National Electricity Act to keep cross subsidy below 20% and transfer power subsidies to farmers directly through DBT schemeUday scheme would lead to reduction in stressed assets and financial & operational turnaround for state electricity board (SEB)

Real Estate Infrastructure status to affordable housing leading to lower cost of debt

100% tax deduction for affordable housing projects making project viable for private playersPort Infrastructure status to shipyard industry leading to lower cost of debt

Tendering activity in the real estate sector

*up to August, 2017

Note: Above data includes all tenders in real estate sector. Given the lack of interest of private players due to issues like RERA, we presume majority of tendering activity would be from the government side.

2092

0

21 900

317

463

1367

5

289

191

548

227

3835

5 7550

7514

6446

717

4925

5 1116

2

4963

6186 10

671

0

10000

20000

30000

40000

50000

60000

Real Estate Telangana Maharashtra Madhya Pradesh Andhra Pradesh

(| c

rore

)

2014 2015 2016 YTD 2017*

The tendering activity for real estate indicates housing momentum to remain strong ahead.

34

Housing for All – investment cornerstone

Source: Project Today, Press reports, KPMG NAREDCO, ICICIdirect.com Research

Government’s “Housing for All by 2022” scheme is expected to be a key catalyst ineconomic recovery. There is a shortage of ~1.2 crore houses in urban areas, ~4.4crore houses in rural areas that government is addressing through Pradhan MantriAwas Yojana‐Gramin (PMAY‐G ) & Pradhan Mantri Awas Yojana‐Urban (PMAY‐U ).We expect the government to construct ~1 crore urban houses and ~3 crore ruralhouses entailing overall investment of ~| 20 lakh crore in next five years.

We believe Housing for All scheme will revive the economy with 250+ sectorsforward and backward linkages. Beside this, it would result in huge employmentgeneration. According to a Credai CBRE report, jobs in the real estate sector arelikely to witness 80% growth from 9.2 million in 2016 to 17.2 million in 2025.

Tendering activity in the real estate sector has picked up significantly in the pasttwo years across major states of India with Telangana topping with tenders worth~| 11162 crore in YTD2017.

Several government initiatives to boost PMAY‐U executionAccording infrastructure status to affordable housing

100% tax deduction for affordable housing projects

PPP models to develop affordable housing projects with private participation

So far, ~1.6 lakh houses have been constructed under PMAY – U since the inceptionof the scheme. However, several government initiatives and strong momentum intendering activity gives us the confidence that the execution would improve, ahead.

On a positive note, strong traction was witnessed in execution of PMAY – Gscheme with the government sorting out operational & approval issues like linkingBelow Poverty Line beneficiary data with socio economic & caste census (SECC).Furthermore, to build a pucca house, the government is giving ~| 1.3 lakh throughDirect Benefit Transfer (DBT), ~| 12000 for toilet construction under Swachh BharatMission and ~| 18000 under MNREGA (~90‐95 days wages) to eligible beneficiaries.Consequently, we expect this execution momentum to sustain given the strongbudgetary allocations for the scheme by several state governments.

Particulars Urban

(crore units) Rural

(crore units) Total

(crore units)

Programme housing target 1.2 4.4 5.6

Delivered till date 0.0 0.6 0.6

Yet to be delivered 1.2 3.8 5.0

Anticipated completion over next 5 years 1.0 3.0 4.0

Anticipated investment (| lakh crore) 5.0 15.0 20.0

Tendering activity in Railway

29.7 30.554.9 67.5

49.8

191.2

0

100

200

300

FY14 FY15 FY16 FY17 8MFY18 Over Next 3year

| 00

0 crore

Looking at historical trend in tendering activity and goverment spending targets, our rough calculation indicates that tendering activity should pick up ~2x to |1.9 lakh crore pa over next three years helping it to achieve railway investment target to |8.6 lakh crore over next 5 years.

35

The government has chalked out a rail infrastructure investment plan of ~| 8.6 lakh crore over the next five years. There has been a quantum jump in investment outlay‐ | 1.1 lakh crore in FY17 against ~| 0.6 lakh crore in FY15. Looking at historical trend in tendering activity, we believe tendering activity needs to jump 2x to | 1.9 lakh crore over the next three years to achieve the five year target

Quantum jump in Railway investment

Source: Indian Railway, Project Today, ICICIdirect.com Research

Government's plan of Rail investment in next 5 years (in | crore)

Network decongestion (DFC+electrification; Doubling+electrification) 199320

Network expansion (including electrification) 193000

National projects (North Eastern & Kashmir connectivity projects) 39000

Safety (Track renewal & bridge work) 127000

Information Technology/Research 5000

Rolling stock(Locomotives, coaches, wagons) 102000

Passenger amenities 12500

High Speed & elevated corridor 65000

Station redevelopment+logistics park 100000

Others 13200

Total 856020

1528

2828

2857

3500

1184

1730

2013

4000

0

1000

2000

3000

4000

5000

AVG 2009‐14 2015‐16 2016‐17 2017‐18 (PLAN)

(km)

Broad gauge lines commissioned (km) Electrification completed (km)

Almost doubled the pace of infrastructure

• Broad gauge lines commissioned could increase to 19 km/day & can rise up to 25 km/day in partnership with state governments

• Two dedicated freight corridors (DFCs) to be commissioned by 2019. Three new DFCs are in the pipeline

• Increased pace of rail infrastructure at almost 4000 km/year. Target is to electrify 11,000 km in three years

Reforms agenda for rail infrastructure

0.0 2.0 4.0 6.0

FY14

FY15

FY16

FY17

8MFY18

| lakh crore

Tendering activity in road vertical

Tendering activity of ~| 12 lakh crore in last four to five years is sufficient for goverment target. However, focus will be on execution & physical milestones to complete road projects

36

Road – Bharatmala to provide next fillip to investments…

Source: Government reports, ICICIdirect.com Research

Road sector certainly remains the key focus area for government. Road awarding haspicked up from 3225 km during FY12 to ~16271 km in FY17. We expect this strongtraction in awarding/construction activity to continue with the government’sannouncement of historic road building programme to construct 83677 km of roadsover next five years.

Bharatmala Phase - I•Road length: 34,800 km

•Investment: | 5,35,000 crore

Other roads•Road length: 48,777 km

•Investment: | 1,56,000 crore

PMGSY•Road length: 1,09,302 km

•Investment: | 88,185 crore

•Upgradation work: | 11,725 crore

The government has announced its historic road building programme to construct83677 km of roads over the next five years with a total outlay of | 6.92 lakh crore whichis expected to generate 14.2 crore man‐days of jobs. This also includes the phase 1 ofBharatmala project which includes construction of 34800 km of roads at an investmentof | 5.35 lakh crore in the next five years. Additionally, the government is also lookingto construct 1.1 lakh km roads in rural areas with investment of | 88185 crore in thenext three years. This rapid completion of road construction is to be ensured by variousagencies including NHAI, MoRTH, NHIDCL and state PWDs.

Clear road map for funding mega-road construction plan Funds (in | lakh crore)Funding for Bharatmala (34800 km) 5.35