IELD CURVES AND INTEREST FORECASTS - Madison · Yield Curves and Interest Forecasts. ... Fed sold T -bills from its portfolio. ... “subsidiaries” Maiden Lane II and III to purchase,

38

Lecture Materials TOPIC 3: YIELD CURVES AND INTEREST FORECASTS ECONOMICS, MONEY MARKETS AND BANKING James M. Johannes Interim Associate Dean for Executive and Evening MBA Programs Aschenbrener Chair of Banking & Finance Graduate School of Banking-Prochnow Professor of Banking Director, Puelicher Center for Banking Education Director, Officer Education Program University of Wisconsin-Madison Madison, Wisconsin [email protected]608-265-2323 August 2-5, 2016

James M Johannes Interim Associate Dean for Executive and Evening MBA Programs

Aschenbrener Chair of Banking amp Finance Graduate School of Banking-Prochnow Professor of Banking

Director Puelicher Center for Banking Education Director Officer Education Program

University of Wisconsin-Madison Madison Wisconsin

jjohannesbuswiscedu 608-265-2323

August 2-5 2016

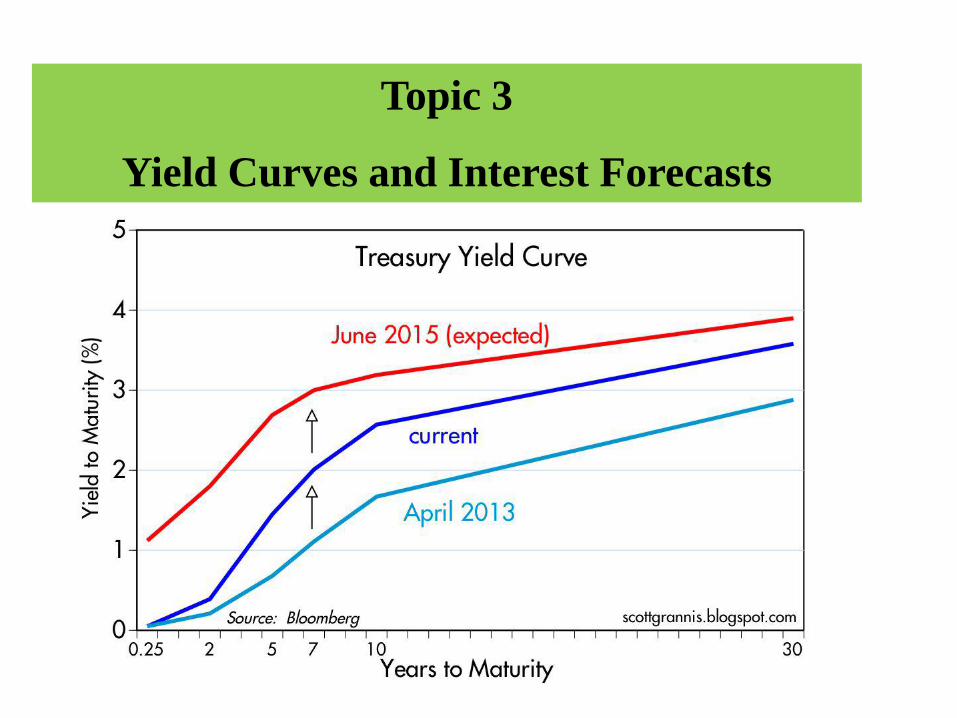

Topic 3

Yield Curves and Interest Forecasts

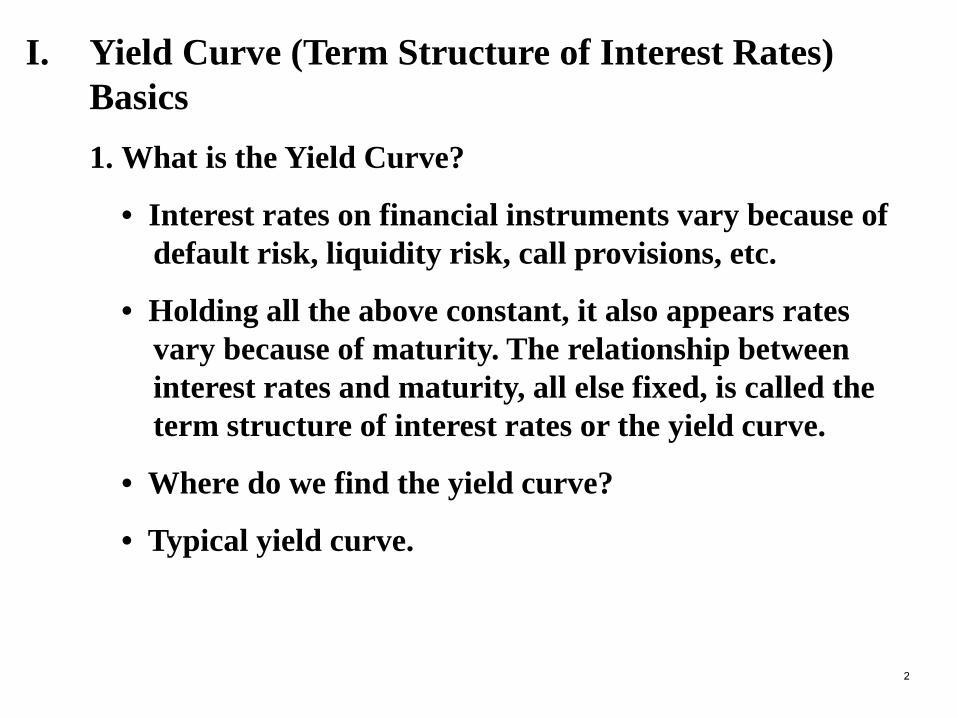

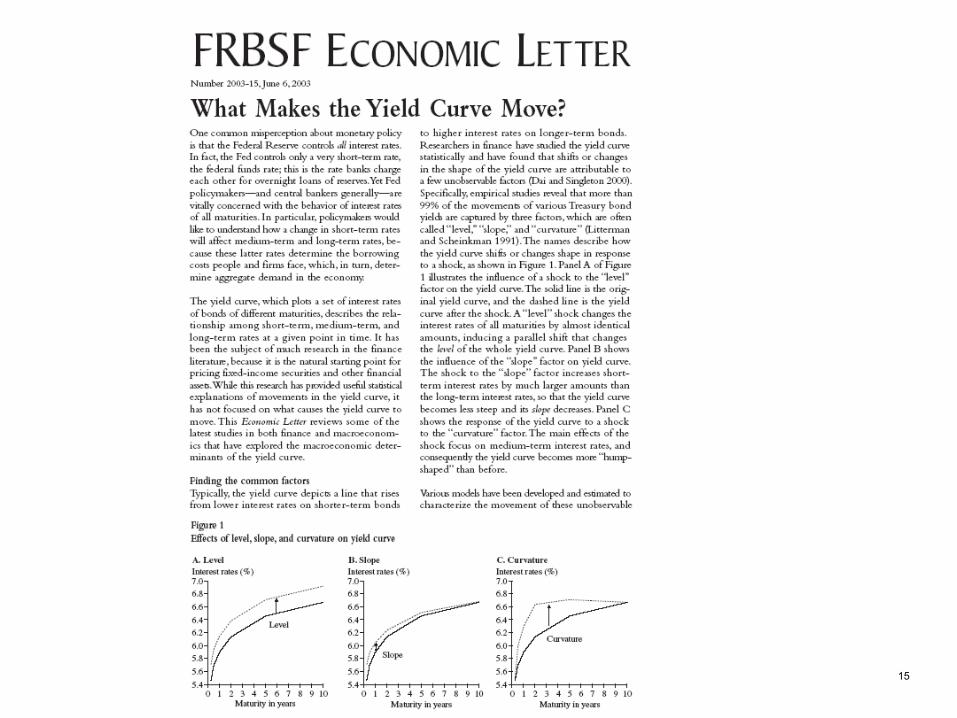

I Yield Curve (Term Structure of Interest Rates) Basics1 What is the Yield Curve

bull Interest rates on financial instruments vary because of default risk liquidity risk call provisions etc

bull Holding all the above constant it also appears rates vary because of maturity The relationship between interest rates and maturity all else fixed is called the term structure of interest rates or the yield curve

bull Where do we find the yield curve

bull Typical yield curve

2

Yield Curves are Important so Found Everywhere

3

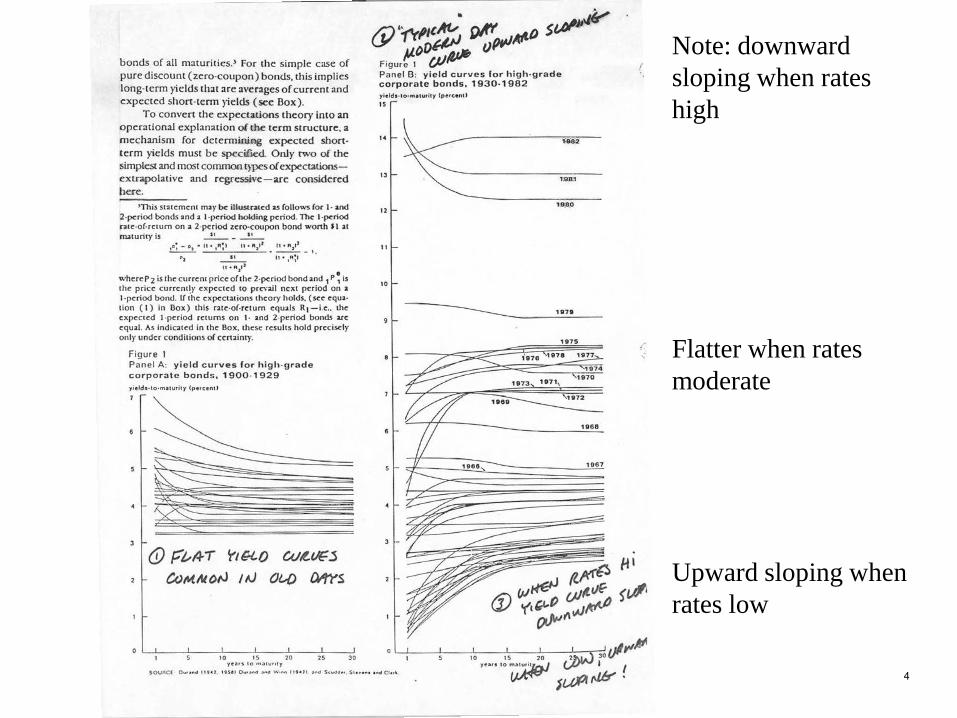

Note downward sloping when rates high

Flatter when rates moderate

Upward sloping when rates low

4

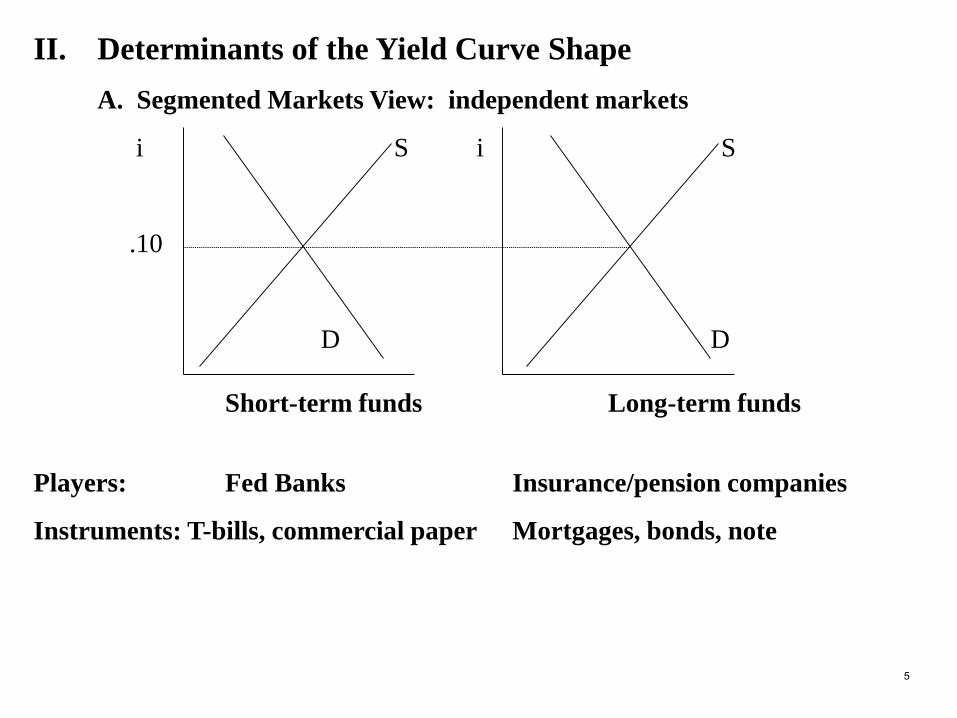

II Determinants of the Yield Curve ShapeA Segmented Markets View independent markets

i S i S

10

D D

Short-term funds Long-term funds

Players Fed Banks Insurancepension companies

Instruments T-bills commercial paper Mortgages bonds note

5

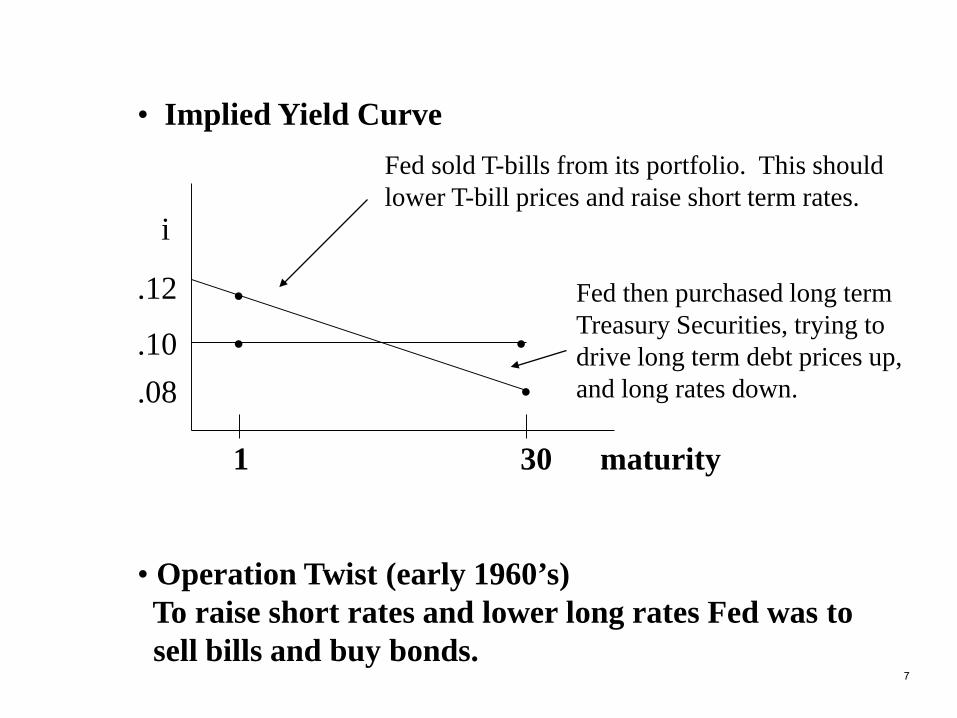

bull Implied Yield Curve

i

10 bull bull

1 30 maturity

bull Operation Twist (early 1960rsquos) To raise short rates and lower long rates Fed was to sell bills and buy bonds

12

6

bull Implied Yield Curve

i

10

1 30 maturity

bull Operation Twist (early 1960rsquos) To raise short rates and lower long rates Fed was to sell bills and buy bonds

12

08bull bull

bull

bull

Fed sold T-bills from its portfolio This should lower T-bill prices and raise short term rates

Fed then purchased long term Treasury Securities trying to drive long term debt prices up and long rates down

7

Observation 1 Twist does not change ldquomoneyrdquo in circulation-if the Fed sells one thing and buys another the ldquomoneyrdquo stays the same

technically the monetary base more on this friday 8

Government Yield Curve

0

1

2

3

4

5

6

7

8

9

10

1 2 3 4 5 6 7 8

Maturity (years)

Inte

rest

Rat

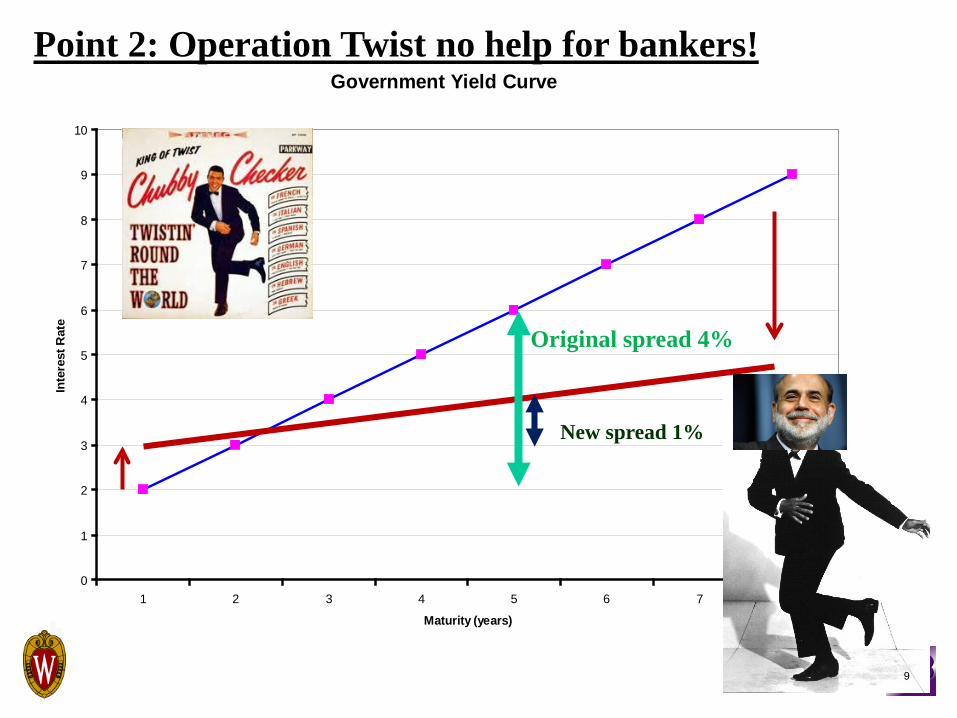

ePoint 2 Operation Twist no help for bankers

Original spread 4

New spread 1

9

Chart1

Maturity (years)

Interest Rate

Government Yield Curve

2

3

4

5

6

7

8

9

Sheet1

Sheet2

Sheet3

Credit Policy (like a pure twist operation) can be neutral as far as the money supply goes but can also be a credit policy that is not neutral in outcome For example suppose the Fed ldquotwistsrdquo by selling Treasury securities and buying Mortgage backed securities Money supply stays the same but the Fed provides ldquocreditrdquo directlyand specifically to the housing sector Credit policy is not ldquomonetaryrdquo policy because it does not increase bank reserves or the monetary base

Fiscal policy (ldquogovernment spendingrdquo) Fed lending $ it earned off investing bank reserves in treasury securities ($ it could have given back to the Treasury)to JPMorgan to purchase Bear Stearns or the $50 billion dollars the Fed loaned its ldquosubsidiariesrdquo Maiden Lane II and III to purchase residential mortgage-backed securities from AIG and multi-sector collateralized debt obligations on which AIG has written credit default swap contracts to keep AIG afloat

Good point to bring up the many different dimensions of ldquomonetary policyrdquo

Pure Monetary policy is usually viewed as something that affects the money supply monetary base or bank reserves or maybe basic interest rate levels

10

BPure Expectations View (sometimes called the Rational Expectations View)1 Example Suppose an investor has a two-year time

horizon (holding period) Suppose further that 1-year and 2-year deposits exist Suppose further that the current 1-year rates is 4 and the depositor thinks the 1-year rate one year from now will be 10 What rate would you have to offer to get this depositor to put money in a 2-year deposit

bull What does the depositor expect to make on two 1-year deposits (Letrsquos ignore compounding)

First year return + expected second year return

04 + 10 = 14 = 1411

bull What would seller of 2-year deposithave to offer to attract a buyer

R2 + R2 = 14

2 R2 = 14

R2 = 07 = 7

12

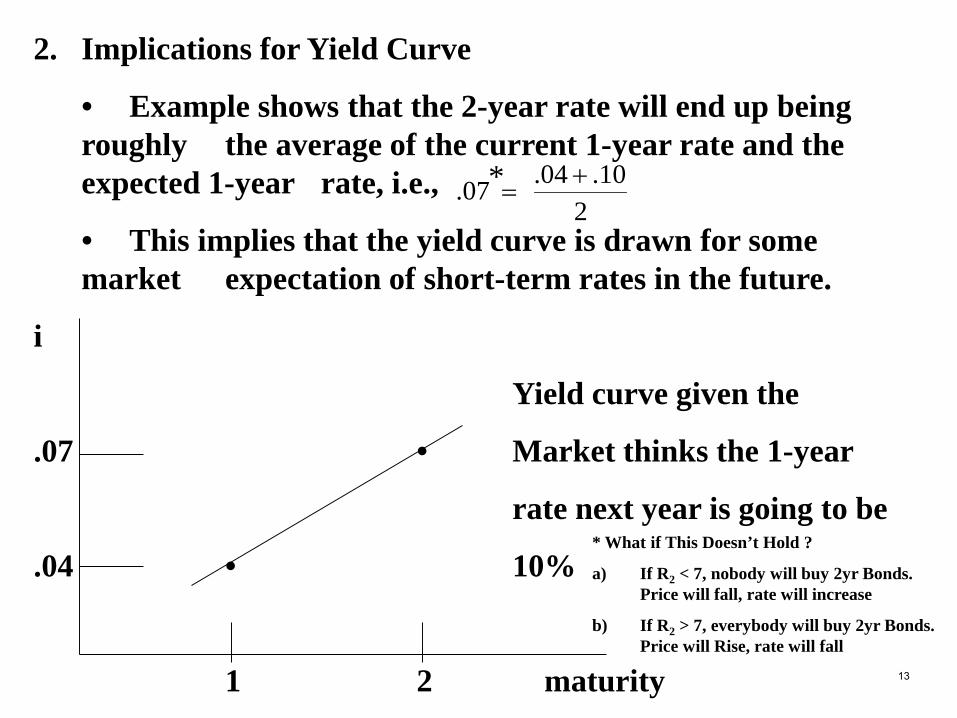

2 Implications for Yield Curve

bull Example shows that the 2-year rate will end up being roughly the average of the current 1-year rate and the expected 1-year rate ie

bull This implies that the yield curve is drawn for some market expectation of short-term rates in the future

i

Yield curve given the

07 bull Market thinks the 1-year

rate next year is going to be

04 bull 10

1 2 maturity

2100407 +

=

What if This Doesnrsquot Hold

a) If R2 lt 7 nobody will buy 2yr Bonds Price will fall rate will increase

b) If R2 gt 7 everybody will buy 2yr Bonds Price will Rise rate will fall

13

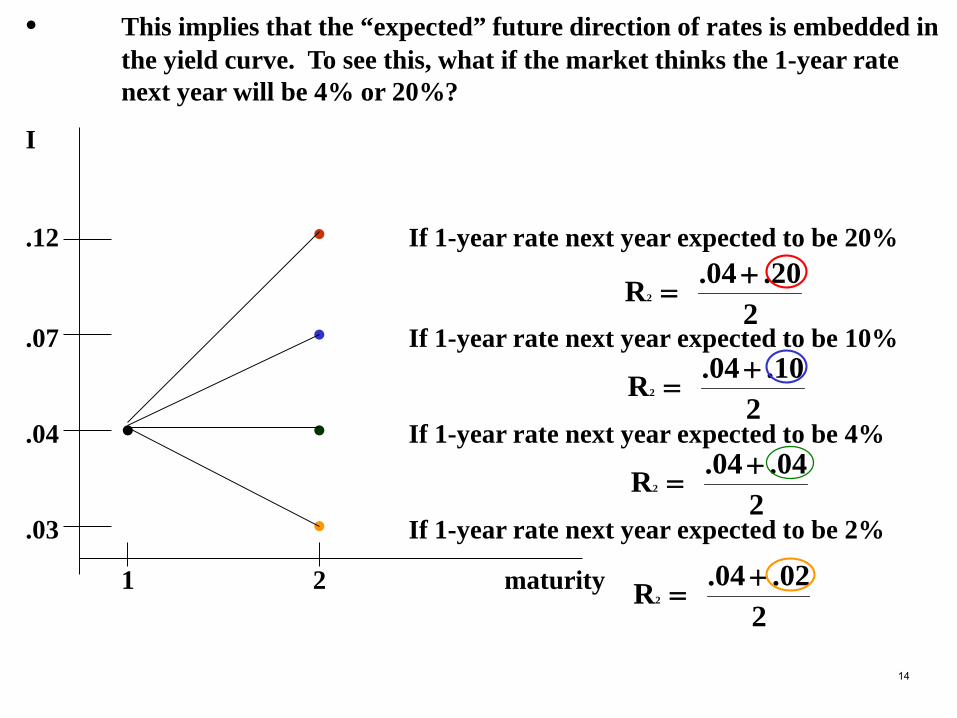

bull This implies that the ldquoexpectedrdquo future direction of rates is embedded in the yield curve To see this what if the market thinks the 1-year rate next year will be 4 or 20

I

12 bull If 1-year rate next year expected to be 20

07 bull If 1-year rate next year expected to be 10

04 bull bull If 1-year rate next year expected to be 4

03 bull If 1-year rate next year expected to be 2

1 2 maturity

22004R2

+=

21004R2

+=

20404R2

+=

20204R2

+=

14

15

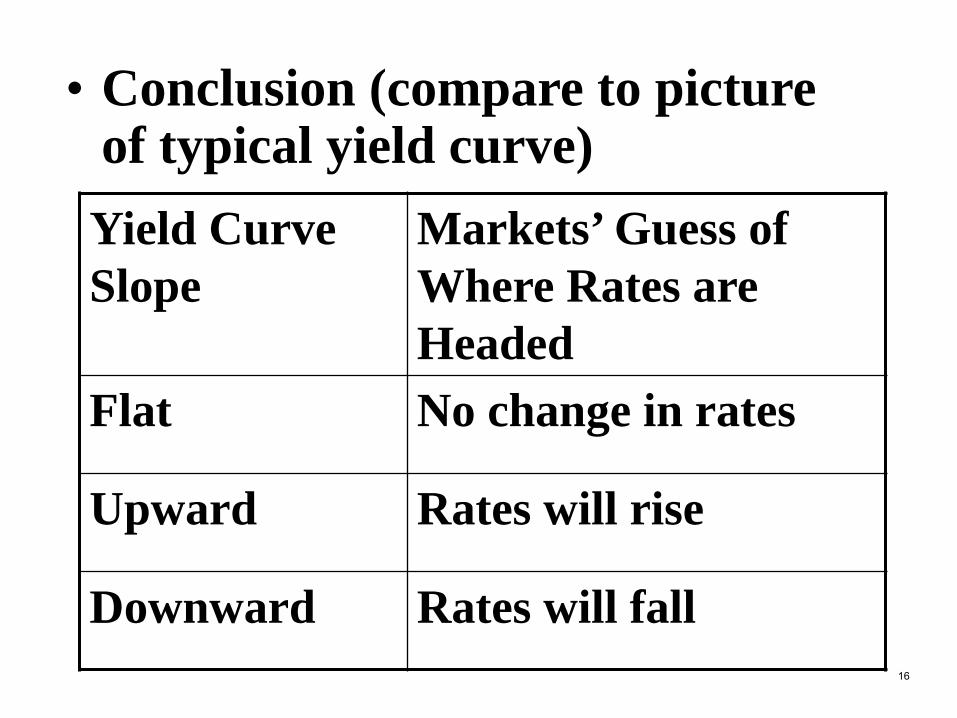

bull Conclusion (compare to picture of typical yield curve)

Yield Curve Slope

Marketsrsquo Guess of Where Rates are Headed

Flat No change in rates

Upward Rates will rise

Downward Rates will fall16

bull Formal yield curve forecasts

Let Ri = current known rate from the WSJ on i period

Investments

tFi = forward rates = marketsrsquo guess of rate on i

period investments t periods from now

Then

2R2 = R1 + 1F1 (invest in a 2 yr or two 1 yrs)

3R3 = R1 + 21F2 (invest in a 3 yr or a one and a two)

3R3 = 2R2 + 2F1 (invest in a 3 yr or a two and a one)

Solutions

3F2RR

3F2RR

2FRR

12

2

11

11

3

1

2

+=

+=

+=

2

317

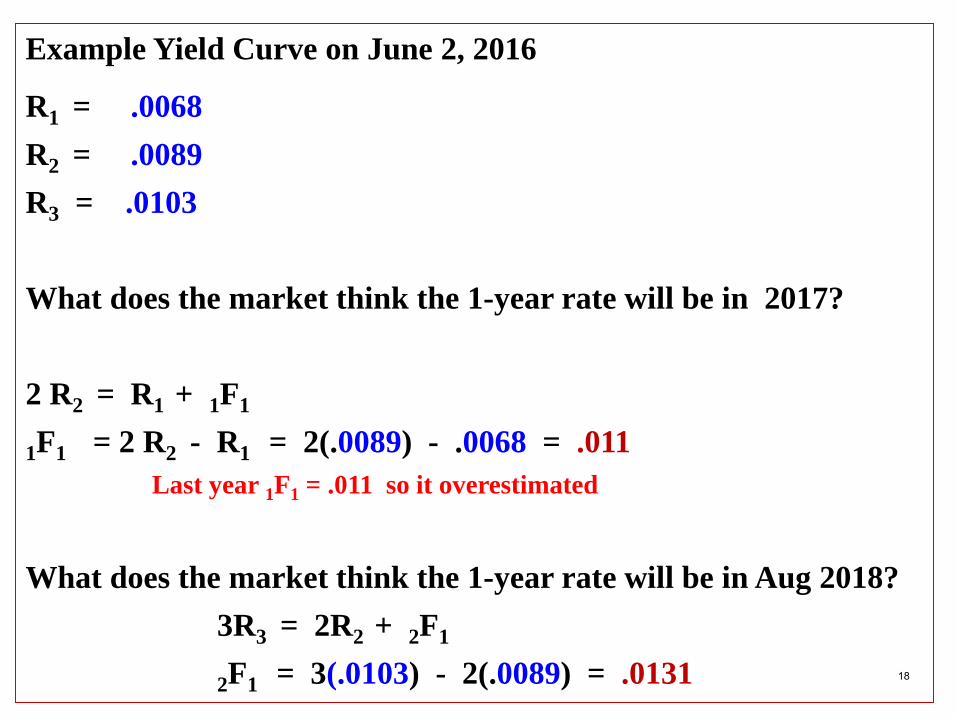

Example Yield Curve on June 2 2016

R1 = 0068 R2 = 0089R3 = 0103

What does the market think the 1-year rate will be in 2017

2 R2 = R1 + 1F1

1F1 = 2 R2 - R1 = 2(0089) - 0068 = 011Last year 1F1 = 011 so it overestimated

What does the market think the 1-year rate will be in Aug 20183R3 = 2R2 + 2F1

2F1 = 3(0103) - 2(0089) = 0131 18

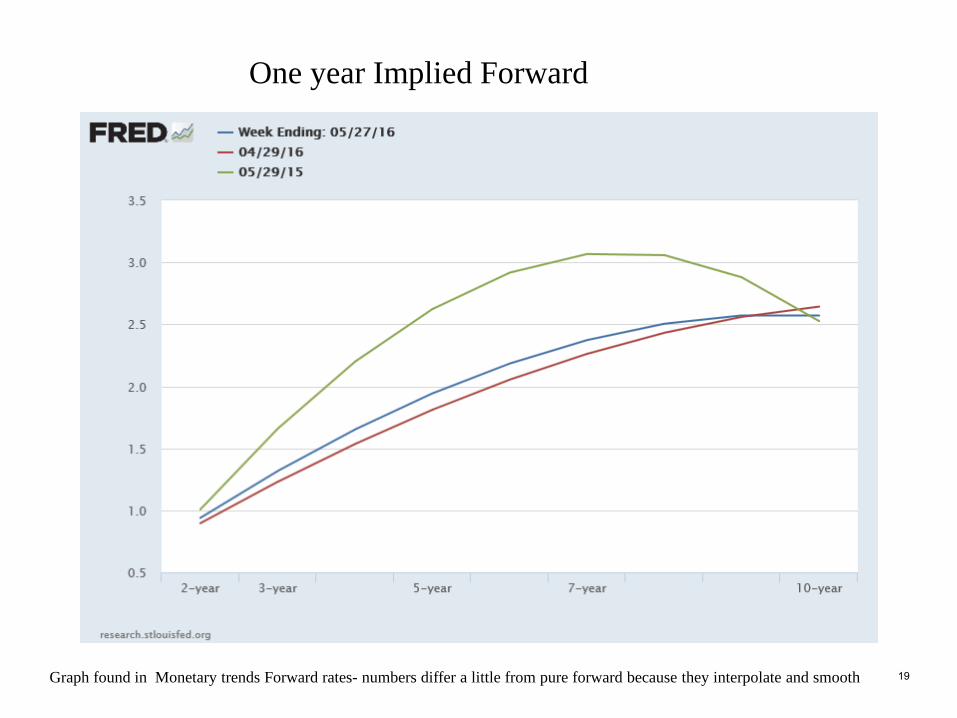

One year Implied Forward

Graph found in Monetary trends Forward rates- numbers differ a little from pure forward because they interpolate and smooth 19

Four Applications of this Theory

1 Riding the yield curve

2 Loan interest swaps

3 QErsquos and ldquoTwistrdquo

4 Forecasting rates

20

21

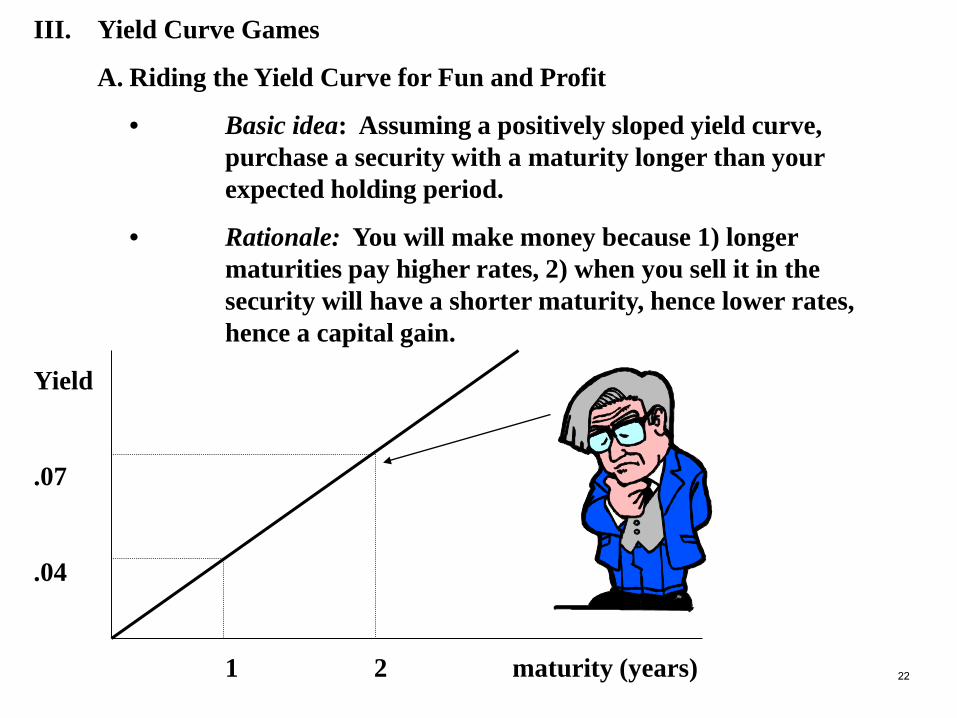

III Yield Curve Games

A Riding the Yield Curve for Fun and Profit

bull Basic idea Assuming a positively sloped yield curve purchase a security with a maturity longer than your expected holding period

bull Rationale You will make money because 1) longer maturities pay higher rates 2) when you sell it in the security will have a shorter maturity hence lower rates hence a capital gain

Yield

07

04

1 2 maturity (years) 22

bull Example You want to invest for 1 year Current 1-year rate is 4 2-year rate is 7

-- If you buy 1-year security make 4

-- If ldquoriderdquo price per dollar of face of 2-year security is 8734 If sell in one year when 1-year rate is 4 get 9615

10110098734

87349615Profit ==minus

=

87342(107)

100Price

100 2

(107) Price

==

=

9615(104)100Price

100 (104) Price

==

=

23

bull Will this work in an ldquoefficient marketrdquo

-- What will you be able to sell the security at next year The market expects the rate on 1-year securities to be 10 This implies the price will be 9090

bull NOTE You will make money riding the yield curve as long as the 1-year rate next year turns out to be less than the market forecast If the rate turns out to be more than the market forecast you will lose money The market forecast is a ldquobreakevenrdquo rate

40408734

87349090Profit ==minus

=minus

24

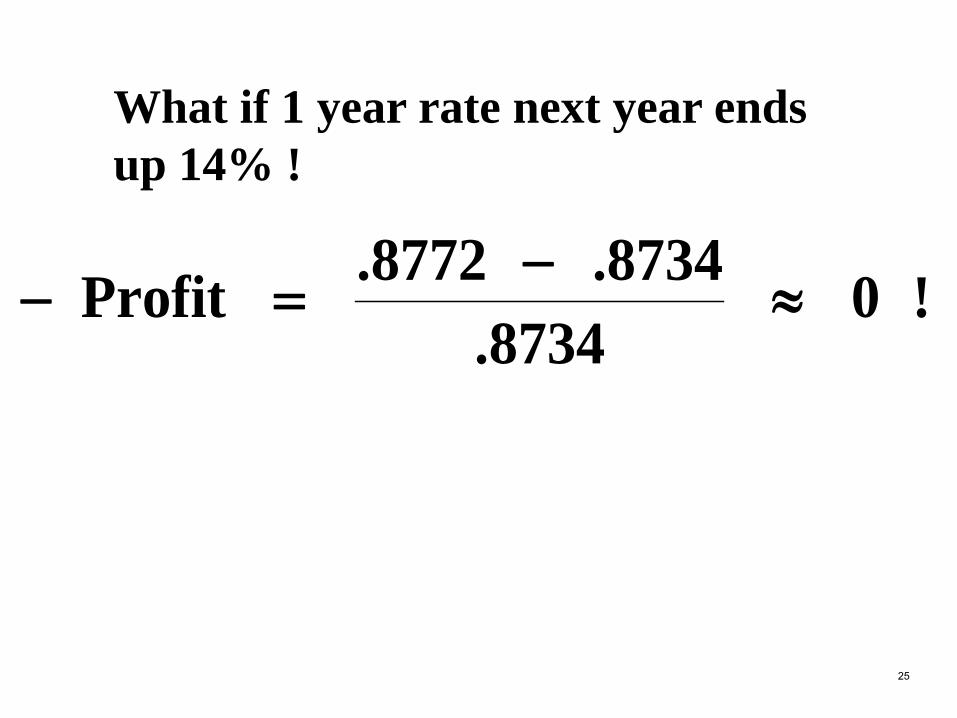

What if 1 year rate next year ends up 14

08734

87348772Profit asympminus

=minus

25

Forward Rate - Actual Rate

-40

-30

-20

-10

00

10

20

30

40

061976

061978

061980

061982

061984

061986

061988

061990

061992

061994

061996

061998

062000

062002

Rates went up more than the market thought ie got burned is you rode

(markets underestimated inflation)

Article recom -mands riding

If positive market overestimated what rates would be ie rate ended up less than the market expected

Forwards over estimate in part because the risk premium is not netted out of the long rate before the calculation is done 26

Chart1

Forward Rate - Actual Rate

00140273751

00000020816

00065300388

00163140265

0017161465

00136189731

00082271281

00066057817

002337434

00111413793

00094226916

00027011479

00071090515

00182610665

Sheet2

27

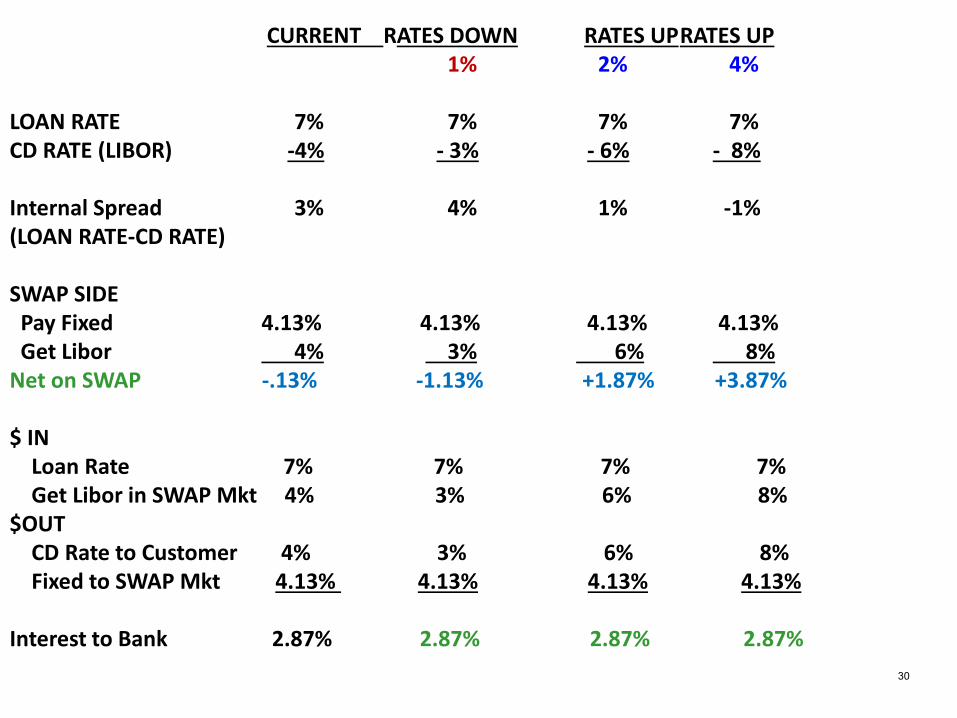

LIBOR SWAPS

Suppose the banker wants to receive variable rate interest but the customer wants to pay fixed

Impasse No Deal

Solution Let the customer pay fixed then swap the fixed for Libor (variable) in the interest swap market

The curve on the next page says the market will trade about 413 fixed each year for two years in exchange for 3 month Libor each quarter for two years

28

So letrsquos use a somewhat far fetched example to show the principle The customer pays fixed 7 and our bank SWAPs it out by paying 413 to get whatever Libor turns out to be 29

$OUTCD Rate to Customer 4 3 6 8Fixed to SWAP Mkt 413 413 413 413

Interest to Bank 287 287 287 28730

How does the market come up with this tradeoff (Letrsquos use annual Libor for simplicity)

)7(2104yearstwoforyearnextnow

ratefixedTheLiborLiborR2FR 2111

=+

=+

Then market will add a risk premium in case customer defaults

31

Real World

Suppose a customer knows that the market typically overestimates short-term rates

In our example suppose customer thinks rate next year on 1 year stuff is going to be 8 not 10

Then they will prefer the variable to the fixed because 4 + 8 lt 7 + 7

32

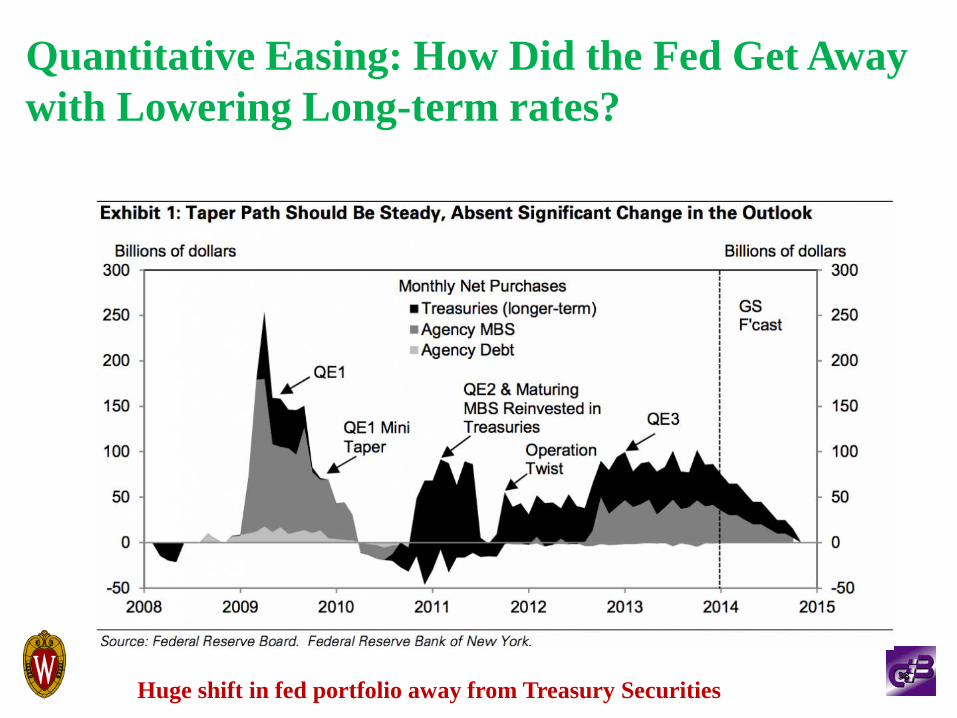

Quantitative Easing How Did the Fed Get Away with Lowering Long-term rates

Huge shift in fed portfolio away from Treasury Securities33

Total Assets held by the Federal Reserve $ tillions

$4

$3

$2

$1

$0

QE1 QE2 QE3

2006 2007 2008 2009 2010 2011 2012 2013 2014

34

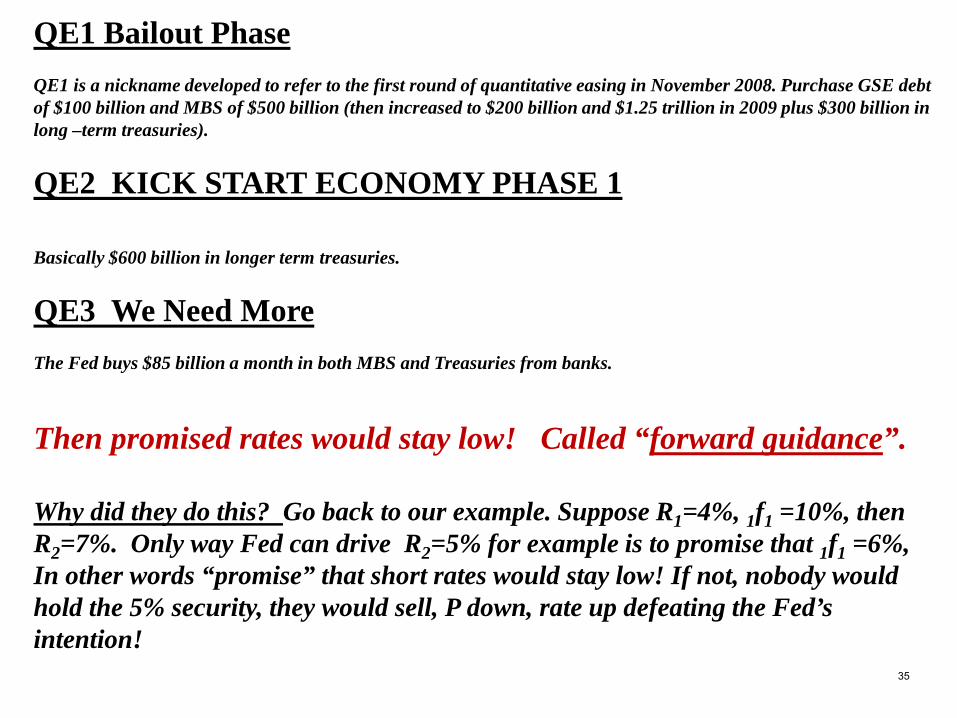

QE1 Bailout PhaseQE1 is a nickname developed to refer to the first round of quantitative easing in November 2008 Purchase GSE debt of $100 billion and MBS of $500 billion (then increased to $200 billion and $125 trillion in 2009 plus $300 billion in long ndashterm treasuries)

QE2 KICK START ECONOMY PHASE 1

Basically $600 billion in longer term treasuries

QE3 We Need MoreThe Fed buys $85 billion a month in both MBS and Treasuries from banks

Then promised rates would stay low Called ldquoforward guidancerdquo

Why did they do this Go back to our example Suppose R1=4 1f1 =10 then R2=7 Only way Fed can drive R2=5 for example is to promise that 1f1 =6 In other words ldquopromiserdquo that short rates would stay low If not nobody would hold the 5 security they would sell P down rate up defeating the Fedrsquos intention

Note the following when rates rose1) Pos GAP would cause NII to increase Neg GAP would cause NII to fall2) But had you had a Neg GAP you could have made more $

GAP Managementbull Suppose assets marked up 2 liabilities down 2 rArr spread 4 a yearbull R1 = 04 R2 = 07 1r1 = 04

So standard GAP games are all about making more $ not maximizing earnings

36

Interest ForecastingThere are three ways to forecast interest rates

1 Roll your own

Nominal rate = real rate + expected inflation

Forecast Real GDP Forecast inflation

2 Use implied forward rates

3 Look at the futures market

Suppose you (I) think a bushel of corn will sell for $100 a year from now Would you agree now to sell it to me then for less than $100 Would I agree to pay more than $100

So the price will end up being close to our ldquobestrdquo guess of the price

Same is true for the t-bills fed funds bonds

37

Slide Number 1

Slide Number 2

Slide Number 3

Slide Number 4

Slide Number 5

Slide Number 6

Slide Number 7

Slide Number 8

Slide Number 9

Slide Number 10

Slide Number 11

Slide Number 12

Slide Number 13

Slide Number 14

Slide Number 15

Slide Number 16

Slide Number 17

Slide Number 18

Slide Number 19

Slide Number 20

Slide Number 21

Slide Number 22

Slide Number 23

Slide Number 24

Slide Number 25

Slide Number 26

Slide Number 27

Slide Number 28

Slide Number 29

Slide Number 30

Slide Number 31

Slide Number 32

Slide Number 33

Slide Number 34

Slide Number 35

GAP Management

Slide Number 37

1 yr T- notes - mat constants

2yr T- notes - mat constants

Source

httpwwwfederalreservegovreleasesh15datamtcm2ytxt

Date

Rate

Date

Rate

Implied one year forward rate

Forecast error

061976

652

061976

706

1076

62

071976

685

1075

14

6

081976

663

1073

15

584

091976

642

1070

14

55

101976

598

1065

15

529

111976

581

1063

12

489

121976

538

1059

14

529

011977

59

1065

06

547

021977

609

1067

10

55

031977

609

1067

12

544

041977

596

1065

12

584

051977

625

1067

06

58

061977

613

1065

09

594

071977

627

1066

05

637

081977

661

1069

02

653

091977

671

1069

03

697

101977

711

1073

-01

695

111977

714

1073

03

696

121977

718

1074

04

728

011978

749

1077

01

734

021978

757

1078

04

731

031978

758

1079

05

745

041978

774

1080

04

782

051978

801

1082

02

061978

809

061978

824

1084

01

839

071978

849

1086

00

831

081978

837

1084

03

864

091978

857

1085

-02

914

101978

885

1086

-06

1001

111978

942

1088

-14

103

121978

972

1091

-15

1041

011979

986

1093

-13

1024

021979

972

1092

-09

1025

031979

979

1093

-10

1012

041979

978

1094

-08

1012

051979

978

1094

-07

957

061979

922

1089

-01

964

071979

914

1086

-08

998

081979

946

1089

-13

1084

091979

1006

1093

-19

1244

101979

1149

1105

-32

1239

111979

1181

1112

-18

1198

121979

1139

1108

-07

1206

011980

115

1109

-13

1392

021980

1342

1129

-30

1582

031980

1488

1139

-29

133

041980

125

1117

06

939

051980

945

1095

23

061980

816

061980

873

1093

14

865

071980

903

1094

07

1024

081980

1053

1108

-08

1152

091980

1157

1116

-07

1249

101980

1209

1117

-09

1415

111980

1351

1129

-25

1488

121980

1408

1133

-20

1408

011981

1326

1124

-08

1457

021981

1392

1133

-21

1371

031981

1357

1134

-04

1432

041981

1415

1140

-09

162

051981

1546

1147

-22

1486

061981

1451

1142

-01

1572

071981

1535

1150

-16

1672

081981

1628

1158

-17

1652

091981

1646

1164

-07

1538

101981

1554

1157

10

1241

111981

1288

1134

33

1285

121981

1329

1137

05

1432

011982

1457

1148

-06

1473

021982

1482

1149

01

1395

031982

1419

1144

10

1398

041982

142

1144

05

1334

051982

1378

1142

11

061982

1407

061982

1447

1149

02

1324

071982

138

1144

16

1143

081982

1232

1132

29

1085

091982

1178

1127

24

932

101982

1019

1111

34

916

111982

98

1104

19

891

121982

966

1104

15

862

011983

933

1100

18

892

021983

964

1104

11

904

031983

966

1103

13

898

041983

957

1102

13

89

051983

949

1101

13

966

061983

1018

1107

04

102

071983

1069

1112

05

1053

081983

1107

1116

07

1016

091983

1079

1114

15

981

101983

1057

1113

16

994

111983

1066

1114

14

1011

121983

1084

1116

13

99

011984

1064

1114

17

1004

021984

1079

1115

13

1059

031984

1131

1120

10

109

041984

1169

1125

11

1166

051984

1247

1133

08

061984

1208

061984

1291

1137

12

1203

071984

1288

1137

17

1182

081984

1243

1130

19

1158

091984

122

1128

15

109

101984

116

1123

19

982

111984

1065

1115

25

933

121984

1018

1110

22

902

011985

993

1108

20

929

021985

1017

1111

16

986

031985

1071

1116

12

914

041985

1009

1110

24

846

051985

939

1103

26

78

061985

869

1096

25

786

071985

877

1097

17

805

081985

894

1098

16

807

091985

898

1099

18

801

101985

886

1097

19

788

111985

858

1093

18

767

121985

815

1086

16

773

011986

814

1086

09

761

021986

797

1083

09

703

031986

721

1074

13

644

041986

67

1070

10

665

051986

707

1075

03

061986

673

061986

718

1076

08

627

071986

667

1071

14

593

081986

633

1067

11

577

091986

635

1069

10

572

101986

628

1068

12

58

111986

628

1068

10

587

121986

627

1067

09

578

011987

623

1067

09

596

021987

64

1068

07

603

031987

642

1068

08

65

041987

702

1075

03

7

051987

776

1085

05

68

061987

757

1083

17

668

071987

744

1082

17

703

081987

775

1085

12

767

091987

834

1090

08

759

101987

84

1092

14

696

111987

769

1084

23

717

121987

786

1086

13

699

011988

763

1083

16

664

021988

718

1077

16

671

031988

727

1078

10

701

041988

759

1082

08

74

051988

8

1086

08

061988

749

061988

803

1086

11

775

071988

828

1088

08

817

081988

863

1091

06

809

091988

846

1088

10

811

101988

835

1086

07

848

111988

867

1089

01

899

121988

909

1092

-01

905

011989

918

1093

01

925

021989

937

1095

01

957

031989

968

1098

-01

936

041989

945

1095

04

898

051989

902

1091

06

844

061989

841

1084

06

789

071989

782

1078

05

818

081989

814

1081

-04

822

091989

828

1083

-01

799

101989

798

1080

04

777

111989

78

1078

02

772

121989

778

1078

01

792

011990

809

1083

-01

811

021990

837

1086

02

835

031990

863

1089

03

84

041990

872

1090

05

832

051990

864

1090

07

061990

81

061990

835

1086

09

794

071990

816

1084

07

778

081990

806

1083

06

776

091990

808

1084

06

755

101990

788

1082

09

731

111990

76

1079

09

705

121990

731

1076

08

664

011991

713

1076

09

627

021991

687

1075

14

64

031991

71

1078

11

624

041991

695

1077

16

613

051991

678

1074

15

636

061991

696

1076

11

631

071991

692

1075

13

578

081991

643

1071

18

557

091991

618

1068

15

533

101991

591

1065

15

489

111991

556

1062

16

438

121991

503

1057

19

415

011992

496

1058

15

429

021992

521

1061

15

463

031992

569

1068

15

43

041992

534

1064

25

419

051992

523

1063

22

061992

417

061992

505

1059

21

36

071992

436

1051

23

347

081992

419

1049

17

318

091992

389

1046

17

33

101992

408

1049

13

368

111992

458

1055

12

371

121992

467

1056

18

35

011993

439

1053

21

339

021993

41

1048

19

333

031993

395

1046

15

324

041993

384

1044

13

336

051993

398

1046

11

354

061993

416

1048

11

347

071993

407

1047

13

344

081993

4

1046

12

336

091993

385

1043

12

339

101993

387

1044

10

358

111993

416

1047

08

361

121993

421

1048

11

354

011994

414

1047

13

387

021994

447

1051

09

432

031994

5

1057

08

482

041994

555

1063

09

531

051994

597

1066

10

061994

527

061994

593

1066

14

548

071994

613

1068

11

556

081994

618

1068

12

576

091994

639

1070

10

611

101994

673

1074

09

654

111994

715

1078

08

714

121994

759

1080

06

705

011995

751

1080

10

67

021995

711

1075

13

643

031995

678

1071

11

627

041995

657

1069

09

6

051995

617

1063

09

564

061995

572

1058

07

559

071995

578

1060

02

575

081995

598

1062

02

562

091995

581

1060

06

559

101995

57

1058

04

543

111995

548

1055

04

531

121995

532

1053

02

509

011996

511

1051

02

494

021996

503

1051

02

534

031996

566

1060

-02

554

041996

596

1064

04

564

051996

61

1066

07

061996

581

061996

63

1068

08

585

071996

627

1067

09

567

081996

603

1064

10

583

091996

623

1066

06

555

101996

591

1063

11

542

111996

57

1060

09

547

121996

578

1061

05

561

011997

601

1064

05

553

021997

59

1063

09

58

031997

622

1066

05

599

041997

645

1069

07

587

051997

628

1067

10

569

061997

609

1065

10

554

071997

589

1062

10

556

081997

594

1063

07

552

091997

588

1062

08

546

101997

577

1061

08

546

111997

571

1060

06

553

121997

572

1059

04

524

011998

536

1055

07

531

021998

542

1055

02

539

031998

556

1057

01

538

041998

556

1057

04

544

051998

559

1057

03

061998

541

061998

552

1056

03

536

071998

546

1056

03

521

081998

527

1053

04

471

091998

467

1046

06

412

101998

409

1041

05

453

111998

454

1046

-05

452

121998

451

1045

00

451

011999

462

1047

-00

47

021999

488

1051

00

478

031999

505

1053

03

469

041999

498

1053

06

485

051999

525

1057

04

51

061999

562

1061

06

503

071999

555

1061

11

52

081999

568

1062

09

525

091999

566

1061

09

543

101999

586

1063

06

555

111999

586

1062

07

584

121999

61

1064

03

612

012000

644

1068

02

622

022000

661

1070

05

622

032000

653

1068

08

615

042000

64

1067

07

633

052000

681

1073

03

062000

617

062000

648

1068

11

608

072000

634

1066

07

618

082000

623

1063

04

613

092000

608

1060

02

601

102000

591

1058

00

609

112000

588

1057

-03

56

122000

535

1051

01

481

012001

476

1047

03

468

022001

466

1046

00

43

032001

434

1044

03

398

042001

423

1045

04

378

052001

426

1047

07

358

062001

408

1046

12

362

072001

404

1045

10

347

082001

376

1041

10

282

092001

312

1034

12

233

102001

273

1031

11

218

112001

278

1034

10

222

122001

311

1040

12

216

012002

303

1039

18

223

022002

302

1038

17

257

032002

356

1046

12

248

042002

342

1044

21

235

052002

326

1042

20

062002

22

062002

299

1038

20

196

072002

256

1032

18

176

082002

213

1025

14

172

092002

2

1023

08

165

102002

191

1022

06

149

112002

192

1024

07

145

122002

184

1022

09

136

012003

174

1021

09

13

022003

163

1020

08

124

032003

157

1019

07

042003

127

042003

162

1020

06

061976

00150397834

00142374434

00150317838

00117218389

00144256815

00058228906

00104353405

00121364464

00124329953

00064256449

00086158825

0005210293

00023102794

00032054151

-00007969586

00030018323

00037033754

00012045251

00036041107

00049049283

00040067934

00021078269

00011033482

061978

00028009226

-00020996676

-0006399549

-00144922943

-00146683574

-00126695014

-00092726021

-00104754717

-00078808073

-00067895024

-00012895024

-00076888199

-00133771981

-00189754137

-00315451101

-0018419735

-00074700685

-00125689141

-0029772015

-00289780548

00064762908

00231564872

00135003291

061980

-00082867096

-00069923712

-00086997758

-00245857765

-00200641174

-00079442897

-00212410589

-0004363123

-00088982763

-0022197472

-00013528744

-00155893348

-00173881697

-00067834133

0010200309

00329022188

00050196513

-00058828445

00009054671

0009600706

00045050548

00108042464

00015170813

061982

00293276934

0023671085

00339780244

00190692371

00153375229

00179516481

00112464095

00132475946

00130352531

00126319416

00042319651

0005024658

00065217877

0014526382

00161360294

00139525999

0012747153

00167483971

00134498271

00095511178

00113468758

00082562759

00120587587

061984

00191644917

00146332767

00192344506

00248441839

00215627299

00201660843

00155759585

00119708574

00242657655

0025882692

00252797437

00172734787

00163767754

00176733087

00188766263

0018366892

00161454208

00090213987

00094156038

00130120435

00095030272

0003106351

00076165401

061986

0011415056

00096151043

00121318049

00104296633

00089217769

00089151129

00072191435

0008118271

0003114345

00054253897

00172539813

0016655515

00117541432

0008048435

00142416922

00225609815

00125498224

00156444247

0016338284

00101273443

00082293881

00077314363

00111335196

061988

00064260696

00100195618

00072126654

00011053279

-00012966722

00014009175

00006015497

-00007986819

00043011043

00056007407

00062001468

0004900083

-00042995458

-00011998521

00035003327

00020000093

00011000835

-00007996658

00015026779

00028062529

00051072358

00072094465

00086094535

061990

0006004484

00058072741

00085095026

00090101255

00084078371

00093063148

0013522515

0010733876

00156460526

00153474492

00107398097

00125338473

00175350014

00151399414

00146352468

00160319377

00185427972

00153404771

00148629957

00150811583

00246073879

00220037009

00211038103

061992

00165557529

00173501015

00130488564

00118588964

0017778125

00213888632

00189765314

00148487571

00133372012

00108348702

00106371904

00131371257

00123347927

00120303171

00095232295

00077222846

00113324773

00127347457

00087347692

00075346587

00086443252

00097508395

00136413636

061994

0012240055

00104364153

00091375284

00081362266

00062349258

00099189005

00127197665

00109157545

00086115099

0008708469

00070027264

00021006058

00022034189

00059050024

00041034179

00038011459

00022002371

00024000095

00019000381

-00021992281

00044097209

0007416714

00075200303

061996

00102166651

00056122646

00108151186

00085122785

00051074369

00048091116

00088151501

00047129726

0006516673

00104199641

0010015878

00095151386

0006811607

00080136794

0007812282

00062091125

00043059264

00067034208

00017013683

0001401149

00035027422

00030030746

00033021339

061998

00035009491

00062003422

00051001528

-00046999136

00003000096

-00000999904

00003011578

00028030946

00063069574

00042080332

00055152599

00111257279

0008725745

00091219011

00064159715

00074175377

00033091047

0002406387

00054096495

00078143193

00069090473

00032058879

00112216684

062000

00042063725

00015002354

00002002356

-00027990567

00007041568

00029059186

00003002385

00034000382

00040001534

00070060108

00116222008

00096241359

00099170237

0012308128

00109087532

00095156357

00116352319

00184774897

00167740897

00124610486

00207955543

00201862217

00197809086

062002

0014035308

00078134532

00063077074

00068066503

00090182185

00087149926

00082142463

00072107502

00063107566

1

2

2

3

3

4

4

5

5

6

6

7

7

8

8

9

1

2

3

4

5

6

7

8

Topic 3

Yield Curves and Interest Forecasts

I Yield Curve (Term Structure of Interest Rates) Basics1 What is the Yield Curve

bull Interest rates on financial instruments vary because of default risk liquidity risk call provisions etc

bull Holding all the above constant it also appears rates vary because of maturity The relationship between interest rates and maturity all else fixed is called the term structure of interest rates or the yield curve

bull Where do we find the yield curve

bull Typical yield curve

2

Yield Curves are Important so Found Everywhere

3

Note downward sloping when rates high

Flatter when rates moderate

Upward sloping when rates low

4

II Determinants of the Yield Curve ShapeA Segmented Markets View independent markets

i S i S

10

D D

Short-term funds Long-term funds

Players Fed Banks Insurancepension companies

Instruments T-bills commercial paper Mortgages bonds note

5

bull Implied Yield Curve

i

10 bull bull

1 30 maturity

bull Operation Twist (early 1960rsquos) To raise short rates and lower long rates Fed was to sell bills and buy bonds

12

6

bull Implied Yield Curve

i

10

1 30 maturity

bull Operation Twist (early 1960rsquos) To raise short rates and lower long rates Fed was to sell bills and buy bonds

12

08bull bull

bull

bull

Fed sold T-bills from its portfolio This should lower T-bill prices and raise short term rates

Fed then purchased long term Treasury Securities trying to drive long term debt prices up and long rates down

7

Observation 1 Twist does not change ldquomoneyrdquo in circulation-if the Fed sells one thing and buys another the ldquomoneyrdquo stays the same

technically the monetary base more on this friday 8

Government Yield Curve

0

1

2

3

4

5

6

7

8

9

10

1 2 3 4 5 6 7 8

Maturity (years)

Inte

rest

Rat

ePoint 2 Operation Twist no help for bankers

Original spread 4

New spread 1

9

Chart1

Maturity (years)

Interest Rate

Government Yield Curve

2

3

4

5

6

7

8

9

Sheet1

Sheet2

Sheet3

Credit Policy (like a pure twist operation) can be neutral as far as the money supply goes but can also be a credit policy that is not neutral in outcome For example suppose the Fed ldquotwistsrdquo by selling Treasury securities and buying Mortgage backed securities Money supply stays the same but the Fed provides ldquocreditrdquo directlyand specifically to the housing sector Credit policy is not ldquomonetaryrdquo policy because it does not increase bank reserves or the monetary base

Fiscal policy (ldquogovernment spendingrdquo) Fed lending $ it earned off investing bank reserves in treasury securities ($ it could have given back to the Treasury)to JPMorgan to purchase Bear Stearns or the $50 billion dollars the Fed loaned its ldquosubsidiariesrdquo Maiden Lane II and III to purchase residential mortgage-backed securities from AIG and multi-sector collateralized debt obligations on which AIG has written credit default swap contracts to keep AIG afloat

Good point to bring up the many different dimensions of ldquomonetary policyrdquo

Pure Monetary policy is usually viewed as something that affects the money supply monetary base or bank reserves or maybe basic interest rate levels

10

BPure Expectations View (sometimes called the Rational Expectations View)1 Example Suppose an investor has a two-year time

horizon (holding period) Suppose further that 1-year and 2-year deposits exist Suppose further that the current 1-year rates is 4 and the depositor thinks the 1-year rate one year from now will be 10 What rate would you have to offer to get this depositor to put money in a 2-year deposit

bull What does the depositor expect to make on two 1-year deposits (Letrsquos ignore compounding)

First year return + expected second year return

04 + 10 = 14 = 1411

bull What would seller of 2-year deposithave to offer to attract a buyer

R2 + R2 = 14

2 R2 = 14

R2 = 07 = 7

12

2 Implications for Yield Curve

bull Example shows that the 2-year rate will end up being roughly the average of the current 1-year rate and the expected 1-year rate ie

bull This implies that the yield curve is drawn for some market expectation of short-term rates in the future

i

Yield curve given the

07 bull Market thinks the 1-year

rate next year is going to be

04 bull 10

1 2 maturity

2100407 +

=

What if This Doesnrsquot Hold

a) If R2 lt 7 nobody will buy 2yr Bonds Price will fall rate will increase

b) If R2 gt 7 everybody will buy 2yr Bonds Price will Rise rate will fall

13

bull This implies that the ldquoexpectedrdquo future direction of rates is embedded in the yield curve To see this what if the market thinks the 1-year rate next year will be 4 or 20

I

12 bull If 1-year rate next year expected to be 20

07 bull If 1-year rate next year expected to be 10

04 bull bull If 1-year rate next year expected to be 4

03 bull If 1-year rate next year expected to be 2

1 2 maturity

22004R2

+=

21004R2

+=

20404R2

+=

20204R2

+=

14

15

bull Conclusion (compare to picture of typical yield curve)

Yield Curve Slope

Marketsrsquo Guess of Where Rates are Headed

Flat No change in rates

Upward Rates will rise

Downward Rates will fall16

bull Formal yield curve forecasts

Let Ri = current known rate from the WSJ on i period

Investments

tFi = forward rates = marketsrsquo guess of rate on i

period investments t periods from now

Then

2R2 = R1 + 1F1 (invest in a 2 yr or two 1 yrs)

3R3 = R1 + 21F2 (invest in a 3 yr or a one and a two)

3R3 = 2R2 + 2F1 (invest in a 3 yr or a two and a one)

Solutions

3F2RR

3F2RR

2FRR

12

2

11

11

3

1

2

+=

+=

+=

2

317

Example Yield Curve on June 2 2016

R1 = 0068 R2 = 0089R3 = 0103

What does the market think the 1-year rate will be in 2017

2 R2 = R1 + 1F1

1F1 = 2 R2 - R1 = 2(0089) - 0068 = 011Last year 1F1 = 011 so it overestimated

What does the market think the 1-year rate will be in Aug 20183R3 = 2R2 + 2F1

2F1 = 3(0103) - 2(0089) = 0131 18

One year Implied Forward

Graph found in Monetary trends Forward rates- numbers differ a little from pure forward because they interpolate and smooth 19

Four Applications of this Theory

1 Riding the yield curve

2 Loan interest swaps

3 QErsquos and ldquoTwistrdquo

4 Forecasting rates

20

21

III Yield Curve Games

A Riding the Yield Curve for Fun and Profit

bull Basic idea Assuming a positively sloped yield curve purchase a security with a maturity longer than your expected holding period

bull Rationale You will make money because 1) longer maturities pay higher rates 2) when you sell it in the security will have a shorter maturity hence lower rates hence a capital gain

Yield

07

04

1 2 maturity (years) 22

bull Example You want to invest for 1 year Current 1-year rate is 4 2-year rate is 7

-- If you buy 1-year security make 4

-- If ldquoriderdquo price per dollar of face of 2-year security is 8734 If sell in one year when 1-year rate is 4 get 9615

10110098734

87349615Profit ==minus

=

87342(107)

100Price

100 2

(107) Price

==

=

9615(104)100Price

100 (104) Price

==

=

23

bull Will this work in an ldquoefficient marketrdquo

-- What will you be able to sell the security at next year The market expects the rate on 1-year securities to be 10 This implies the price will be 9090

bull NOTE You will make money riding the yield curve as long as the 1-year rate next year turns out to be less than the market forecast If the rate turns out to be more than the market forecast you will lose money The market forecast is a ldquobreakevenrdquo rate

40408734

87349090Profit ==minus

=minus

24

What if 1 year rate next year ends up 14

08734

87348772Profit asympminus

=minus

25

Forward Rate - Actual Rate

-40

-30

-20

-10

00

10

20

30

40

061976

061978

061980

061982

061984

061986

061988

061990

061992

061994

061996

061998

062000

062002

Rates went up more than the market thought ie got burned is you rode

(markets underestimated inflation)

Article recom -mands riding

If positive market overestimated what rates would be ie rate ended up less than the market expected

Forwards over estimate in part because the risk premium is not netted out of the long rate before the calculation is done 26

Chart1

Forward Rate - Actual Rate

00140273751

00000020816

00065300388

00163140265

0017161465

00136189731

00082271281

00066057817

002337434

00111413793

00094226916

00027011479

00071090515

00182610665

Sheet2

27

LIBOR SWAPS

Suppose the banker wants to receive variable rate interest but the customer wants to pay fixed

Impasse No Deal

Solution Let the customer pay fixed then swap the fixed for Libor (variable) in the interest swap market

The curve on the next page says the market will trade about 413 fixed each year for two years in exchange for 3 month Libor each quarter for two years

28

So letrsquos use a somewhat far fetched example to show the principle The customer pays fixed 7 and our bank SWAPs it out by paying 413 to get whatever Libor turns out to be 29

$OUTCD Rate to Customer 4 3 6 8Fixed to SWAP Mkt 413 413 413 413

Interest to Bank 287 287 287 28730

How does the market come up with this tradeoff (Letrsquos use annual Libor for simplicity)

)7(2104yearstwoforyearnextnow

ratefixedTheLiborLiborR2FR 2111

=+

=+

Then market will add a risk premium in case customer defaults

31

Real World

Suppose a customer knows that the market typically overestimates short-term rates

In our example suppose customer thinks rate next year on 1 year stuff is going to be 8 not 10

Then they will prefer the variable to the fixed because 4 + 8 lt 7 + 7

32

Quantitative Easing How Did the Fed Get Away with Lowering Long-term rates

Huge shift in fed portfolio away from Treasury Securities33

Total Assets held by the Federal Reserve $ tillions

$4

$3

$2

$1

$0

QE1 QE2 QE3

2006 2007 2008 2009 2010 2011 2012 2013 2014

34

QE1 Bailout PhaseQE1 is a nickname developed to refer to the first round of quantitative easing in November 2008 Purchase GSE debt of $100 billion and MBS of $500 billion (then increased to $200 billion and $125 trillion in 2009 plus $300 billion in long ndashterm treasuries)

QE2 KICK START ECONOMY PHASE 1

Basically $600 billion in longer term treasuries

QE3 We Need MoreThe Fed buys $85 billion a month in both MBS and Treasuries from banks

Then promised rates would stay low Called ldquoforward guidancerdquo

Why did they do this Go back to our example Suppose R1=4 1f1 =10 then R2=7 Only way Fed can drive R2=5 for example is to promise that 1f1 =6 In other words ldquopromiserdquo that short rates would stay low If not nobody would hold the 5 security they would sell P down rate up defeating the Fedrsquos intention

Note the following when rates rose1) Pos GAP would cause NII to increase Neg GAP would cause NII to fall2) But had you had a Neg GAP you could have made more $

GAP Managementbull Suppose assets marked up 2 liabilities down 2 rArr spread 4 a yearbull R1 = 04 R2 = 07 1r1 = 04

So standard GAP games are all about making more $ not maximizing earnings

36

Interest ForecastingThere are three ways to forecast interest rates

1 Roll your own

Nominal rate = real rate + expected inflation

Forecast Real GDP Forecast inflation

2 Use implied forward rates

3 Look at the futures market

Suppose you (I) think a bushel of corn will sell for $100 a year from now Would you agree now to sell it to me then for less than $100 Would I agree to pay more than $100

So the price will end up being close to our ldquobestrdquo guess of the price

Same is true for the t-bills fed funds bonds

37

Slide Number 1

Slide Number 2

Slide Number 3

Slide Number 4

Slide Number 5

Slide Number 6

Slide Number 7

Slide Number 8

Slide Number 9

Slide Number 10

Slide Number 11

Slide Number 12

Slide Number 13

Slide Number 14

Slide Number 15

Slide Number 16

Slide Number 17

Slide Number 18

Slide Number 19

Slide Number 20

Slide Number 21

Slide Number 22

Slide Number 23

Slide Number 24

Slide Number 25

Slide Number 26

Slide Number 27

Slide Number 28

Slide Number 29

Slide Number 30

Slide Number 31

Slide Number 32

Slide Number 33

Slide Number 34

Slide Number 35

GAP Management

Slide Number 37

1 yr T- notes - mat constants

2yr T- notes - mat constants

Source

httpwwwfederalreservegovreleasesh15datamtcm2ytxt

Date

Rate

Date

Rate

Implied one year forward rate

Forecast error

061976

652

061976

706

1076

62

071976

685

1075

14

6

081976

663

1073

15

584

091976

642

1070

14

55

101976

598

1065

15

529

111976

581

1063

12

489

121976

538

1059

14

529

011977

59

1065

06

547

021977

609

1067

10

55

031977

609

1067

12

544

041977

596

1065

12

584

051977

625

1067

06

58

061977

613

1065

09

594

071977

627

1066

05

637

081977

661

1069

02

653

091977

671

1069

03

697

101977

711

1073

-01

695

111977

714

1073

03

696

121977

718

1074

04

728

011978

749

1077

01

734

021978

757

1078

04

731

031978

758

1079

05

745

041978

774

1080

04

782

051978

801

1082

02

061978

809

061978

824

1084

01

839

071978

849

1086

00

831

081978

837

1084

03

864

091978

857

1085

-02

914

101978

885

1086

-06

1001

111978

942

1088

-14

103

121978

972

1091

-15

1041

011979

986

1093

-13

1024

021979

972

1092

-09

1025

031979

979

1093

-10

1012

041979

978

1094

-08

1012

051979

978

1094

-07

957

061979

922

1089

-01

964

071979

914

1086

-08

998

081979

946

1089

-13

1084

091979

1006

1093

-19

1244

101979

1149

1105

-32

1239

111979

1181

1112

-18

1198

121979

1139

1108

-07

1206

011980

115

1109

-13

1392

021980

1342

1129

-30

1582

031980

1488

1139

-29

133

041980

125

1117

06

939

051980

945

1095

23

061980

816

061980

873

1093

14

865

071980

903

1094

07

1024

081980

1053

1108

-08

1152

091980

1157

1116

-07

1249

101980

1209

1117

-09

1415

111980

1351

1129

-25

1488

121980

1408

1133

-20

1408

011981

1326

1124

-08

1457

021981

1392

1133

-21

1371

031981

1357

1134

-04

1432

041981

1415

1140

-09

162

051981

1546

1147

-22

1486

061981

1451

1142

-01

1572

071981

1535

1150

-16

1672

081981

1628

1158

-17

1652

091981

1646

1164

-07

1538

101981

1554

1157

10

1241

111981

1288

1134

33

1285

121981

1329

1137

05

1432

011982

1457

1148

-06

1473

021982

1482

1149

01

1395

031982

1419

1144

10

1398

041982

142

1144

05

1334

051982

1378

1142

11

061982

1407

061982

1447

1149

02

1324

071982

138

1144

16

1143

081982

1232

1132

29

1085

091982

1178

1127

24

932

101982

1019

1111

34

916

111982

98

1104

19

891

121982

966

1104

15

862

011983

933

1100

18

892

021983

964

1104

11

904

031983

966

1103

13

898

041983

957

1102

13

89

051983

949

1101

13

966

061983

1018

1107

04

102

071983

1069

1112

05

1053

081983

1107

1116

07

1016

091983

1079

1114

15

981

101983

1057

1113

16

994

111983

1066

1114

14

1011

121983

1084

1116

13

99

011984

1064

1114

17

1004

021984

1079

1115

13

1059

031984

1131

1120

10

109

041984

1169

1125

11

1166

051984

1247

1133

08

061984

1208

061984

1291

1137

12

1203

071984

1288

1137

17

1182

081984

1243

1130

19

1158

091984

122

1128

15

109

101984

116

1123

19

982

111984

1065

1115

25

933

121984

1018

1110

22

902

011985

993

1108

20

929

021985

1017

1111

16

986

031985

1071

1116

12

914

041985

1009

1110

24

846

051985

939

1103

26

78

061985

869

1096

25

786

071985

877

1097

17

805

081985

894

1098

16

807

091985

898

1099

18

801

101985

886

1097

19

788

111985

858

1093

18

767

121985

815

1086

16

773

011986

814

1086

09

761

021986

797

1083

09

703

031986

721

1074

13

644

041986

67

1070

10

665

051986

707

1075

03

061986

673

061986

718

1076

08

627

071986

667

1071

14

593

081986

633

1067

11

577

091986

635

1069

10

572

101986

628

1068

12

58

111986

628

1068

10

587

121986

627

1067

09

578

011987

623

1067

09

596

021987

64

1068

07

603

031987

642

1068

08

65

041987

702

1075

03

7

051987

776

1085

05

68

061987

757

1083

17

668

071987

744

1082

17

703

081987

775

1085

12

767

091987

834

1090

08

759

101987

84

1092

14

696

111987

769

1084

23

717

121987

786

1086

13

699

011988

763

1083

16

664

021988

718

1077

16

671

031988

727

1078

10

701

041988

759

1082

08

74

051988

8

1086

08

061988

749

061988

803

1086

11

775

071988

828

1088

08

817

081988

863

1091

06

809

091988

846

1088

10

811

101988

835

1086

07

848

111988

867

1089

01

899

121988

909

1092

-01

905

011989

918

1093

01

925

021989

937

1095

01

957

031989

968

1098

-01

936

041989

945

1095

04

898

051989

902

1091

06

844

061989

841

1084

06

789

071989

782

1078

05

818

081989

814

1081

-04

822

091989

828

1083

-01

799

101989

798

1080

04

777

111989

78

1078

02

772

121989

778

1078

01

792

011990

809

1083

-01

811

021990

837

1086

02

835

031990

863

1089

03

84

041990

872

1090

05

832

051990

864

1090

07

061990

81

061990

835

1086

09

794

071990

816

1084

07

778

081990

806

1083

06

776

091990

808

1084

06

755

101990

788

1082

09

731

111990

76

1079

09

705

121990

731

1076

08

664

011991

713

1076

09

627

021991

687

1075

14

64

031991

71

1078

11

624

041991

695

1077

16

613

051991

678

1074

15

636

061991

696

1076

11

631

071991

692

1075

13

578

081991

643

1071

18

557

091991

618

1068

15

533

101991

591

1065

15

489

111991

556

1062

16

438

121991

503

1057

19

415

011992

496

1058

15

429

021992

521

1061

15

463

031992

569

1068

15

43

041992

534

1064

25

419

051992

523

1063

22

061992

417

061992

505

1059

21

36

071992

436

1051

23

347

081992

419

1049

17

318

091992

389

1046

17

33

101992

408

1049

13

368

111992

458

1055

12

371

121992

467

1056

18

35

011993

439

1053

21

339

021993

41

1048

19

333

031993

395

1046

15

324

041993

384

1044

13

336

051993

398

1046

11

354

061993

416

1048

11

347

071993

407

1047

13

344

081993

4

1046

12

336

091993

385

1043

12

339

101993

387

1044

10

358

111993

416

1047

08

361

121993

421

1048

11

354

011994

414

1047

13

387

021994

447

1051

09

432

031994

5

1057

08

482

041994

555

1063

09

531

051994

597

1066

10

061994

527

061994

593

1066

14

548

071994

613

1068

11

556

081994

618

1068

12

576

091994

639

1070

10

611

101994

673

1074

09

654

111994

715

1078

08

714

121994

759

1080

06

705

011995

751

1080

10

67

021995

711

1075

13

643

031995

678

1071

11

627

041995

657

1069

09

6

051995

617

1063

09

564

061995

572

1058

07

559

071995

578

1060

02

575

081995

598

1062

02

562

091995

581

1060

06

559

101995

57

1058

04

543

111995

548

1055

04

531

121995

532

1053

02

509

011996

511

1051

02

494

021996

503

1051

02

534

031996

566

1060

-02

554

041996

596

1064

04

564

051996

61

1066

07

061996

581

061996

63

1068

08

585

071996

627

1067

09

567

081996

603

1064

10

583

091996

623

1066

06

555

101996

591

1063

11

542

111996

57

1060

09

547

121996

578

1061

05

561

011997

601

1064

05

553

021997

59

1063

09

58

031997

622

1066

05

599

041997

645

1069

07

587

051997

628

1067

10

569

061997

609

1065

10

554

071997

589

1062

10

556

081997

594

1063

07

552

091997

588

1062

08

546

101997

577

1061

08

546

111997

571

1060

06

553

121997

572

1059

04

524

011998

536

1055

07

531

021998

542

1055

02

539

031998

556

1057

01

538

041998

556

1057

04

544

051998

559

1057

03

061998

541

061998

552

1056

03

536

071998

546

1056

03

521

081998

527

1053

04

471

091998

467

1046

06

412

101998

409

1041

05

453

111998

454

1046

-05

452

121998

451

1045

00

451

011999

462

1047

-00

47

021999

488

1051

00

478

031999

505

1053

03

469

041999

498

1053

06

485

051999

525

1057

04

51

061999

562

1061

06

503

071999

555

1061

11

52

081999

568

1062

09

525

091999

566

1061

09

543

101999

586

1063

06

555

111999

586

1062

07

584

121999

61

1064

03

612

012000

644

1068

02

622

022000

661

1070

05

622

032000

653

1068

08

615

042000

64

1067

07

633

052000

681

1073

03

062000

617

062000

648

1068

11

608

072000

634

1066

07

618

082000

623

1063

04

613

092000

608

1060

02

601

102000

591

1058

00

609

112000

588

1057

-03

56

122000

535

1051

01

481

012001

476

1047

03

468

022001

466

1046

00

43

032001

434

1044

03

398

042001

423

1045

04

378

052001

426

1047

07

358

062001

408

1046

12

362

072001

404

1045

10

347

082001

376

1041

10

282

092001

312

1034

12

233

102001

273

1031

11

218

112001

278

1034

10

222

122001

311

1040

12

216

012002

303

1039

18

223

022002

302

1038

17

257

032002

356

1046

12

248

042002

342

1044

21

235

052002

326

1042

20

062002

22

062002

299

1038

20

196

072002

256

1032

18

176

082002

213

1025

14

172

092002

2

1023

08

165

102002

191

1022

06

149

112002

192

1024

07

145

122002

184

1022

09

136

012003

174

1021

09

13

022003

163

1020

08

124

032003

157

1019

07

042003

127

042003

162

1020

06

061976

00150397834

00142374434

00150317838

00117218389

00144256815

00058228906

00104353405

00121364464

00124329953

00064256449

00086158825

0005210293

00023102794

00032054151

-00007969586

00030018323

00037033754

00012045251

00036041107

00049049283

00040067934

00021078269

00011033482

061978

00028009226

-00020996676

-0006399549

-00144922943

-00146683574

-00126695014

-00092726021

-00104754717

-00078808073

-00067895024

-00012895024

-00076888199

-00133771981

-00189754137

-00315451101

-0018419735

-00074700685

-00125689141

-0029772015

-00289780548

00064762908

00231564872

00135003291

061980

-00082867096

-00069923712

-00086997758

-00245857765

-00200641174

-00079442897

-00212410589

-0004363123

-00088982763

-0022197472

-00013528744

-00155893348

-00173881697

-00067834133

0010200309

00329022188

00050196513

-00058828445

00009054671

0009600706

00045050548

00108042464

00015170813

061982

00293276934

0023671085

00339780244

00190692371

00153375229

00179516481

00112464095

00132475946

00130352531

00126319416

00042319651

0005024658

00065217877

0014526382

00161360294

00139525999

0012747153

00167483971

00134498271

00095511178

00113468758

00082562759

00120587587

061984

00191644917

00146332767

00192344506

00248441839

00215627299

00201660843

00155759585

00119708574

00242657655

0025882692

00252797437

00172734787

00163767754

00176733087

00188766263

0018366892

00161454208

00090213987

00094156038

00130120435

00095030272

0003106351

00076165401

061986

0011415056

00096151043

00121318049

00104296633

00089217769

00089151129

00072191435

0008118271

0003114345

00054253897

00172539813

0016655515

00117541432

0008048435

00142416922

00225609815

00125498224

00156444247

0016338284

00101273443

00082293881

00077314363

00111335196

061988

00064260696

00100195618

00072126654

00011053279

-00012966722

00014009175

00006015497

-00007986819

00043011043

00056007407

00062001468

0004900083

-00042995458

-00011998521

00035003327

00020000093

00011000835

-00007996658

00015026779

00028062529

00051072358

00072094465

00086094535

061990

0006004484

00058072741

00085095026

00090101255

00084078371

00093063148

0013522515

0010733876

00156460526

00153474492

00107398097

00125338473

00175350014

00151399414

00146352468

00160319377

00185427972

00153404771

00148629957

00150811583

00246073879

00220037009

00211038103

061992

00165557529

00173501015

00130488564

00118588964

0017778125

00213888632

00189765314

00148487571

00133372012

00108348702

00106371904

00131371257

00123347927

00120303171

00095232295

00077222846

00113324773

00127347457

00087347692

00075346587

00086443252

00097508395

00136413636

061994

0012240055

00104364153

00091375284

00081362266

00062349258

00099189005

00127197665

00109157545

00086115099

0008708469

00070027264

00021006058

00022034189

00059050024

00041034179

00038011459

00022002371

00024000095

00019000381

-00021992281

00044097209

0007416714

00075200303

061996

00102166651

00056122646

00108151186

00085122785

00051074369

00048091116

00088151501

00047129726

0006516673

00104199641

0010015878

00095151386

0006811607

00080136794

0007812282

00062091125

00043059264

00067034208

00017013683

0001401149

00035027422

00030030746

00033021339

061998

00035009491

00062003422

00051001528

-00046999136

00003000096

-00000999904

00003011578

00028030946

00063069574

00042080332

00055152599

00111257279

0008725745

00091219011

00064159715

00074175377

00033091047

0002406387

00054096495

00078143193

00069090473

00032058879

00112216684

062000

00042063725

00015002354

00002002356

-00027990567

00007041568

00029059186

00003002385

00034000382

00040001534

00070060108

00116222008

00096241359

00099170237

0012308128

00109087532

00095156357

00116352319

00184774897

00167740897

00124610486

00207955543

00201862217

00197809086

062002

0014035308

00078134532

00063077074

00068066503

00090182185

00087149926

00082142463

00072107502

00063107566

1

2

2

3

3

4

4

5

5

6

6

7

7

8

8

9

1

2

3

4

5

6

7

8

I Yield Curve (Term Structure of Interest Rates) Basics1 What is the Yield Curve

bull Interest rates on financial instruments vary because of default risk liquidity risk call provisions etc