ifc jd power paris roundtable 27 sep 06 06 09 22 ep

TRANSCRIPT

International Finance Corporation

Provider of Long-term Financing

with Global Expertise

and Industry Knowledge

in Emerging Markets

July 2005

International Finance Corporation

Support from Strategy to Implementation:

Financing the Automotive Sector in Emerging Markets

1

The Landscape in 2006

• Flat markets in the developed world …

Western Europe

North America

Japan

• … while emerging markets are surging

2

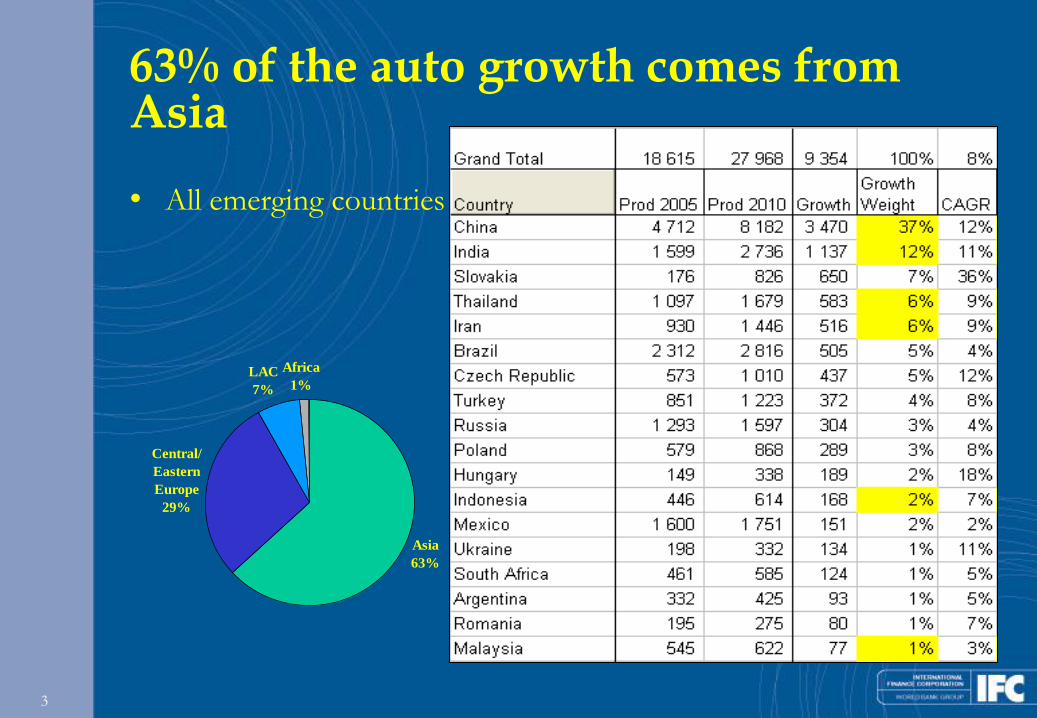

Emerging countries projections

• Yearly 4 wheelers output expected to grow from 18.6 M in 2005 to

28 M vehicles in 2010 (8% CAGR)(*)

• 82% of the growth will come from 7 countries

China 37%

India 12%

Czech+Slovak Republic 12%

Thailand 6%

Iran 6%

Brazil 5%

Turkey 4%

• 64% of the growth comes from Asia; 18% from Eastern Europe; 8%

from Latin America

(*) Sources: JD-Power, CSM

3

63% of the auto growth comes from Asia

Asia

63%

Central/

Eastern

Europe

29%

LAC

7%

Africa

1%

• All emerging countries

4

Is Asia a global threat ???

• China now 2nd global market and still growing

• India catching up, was 10 year behind, now 8

years

• American Big Three tumbling at home

… The end of the Old Auto World ???

5

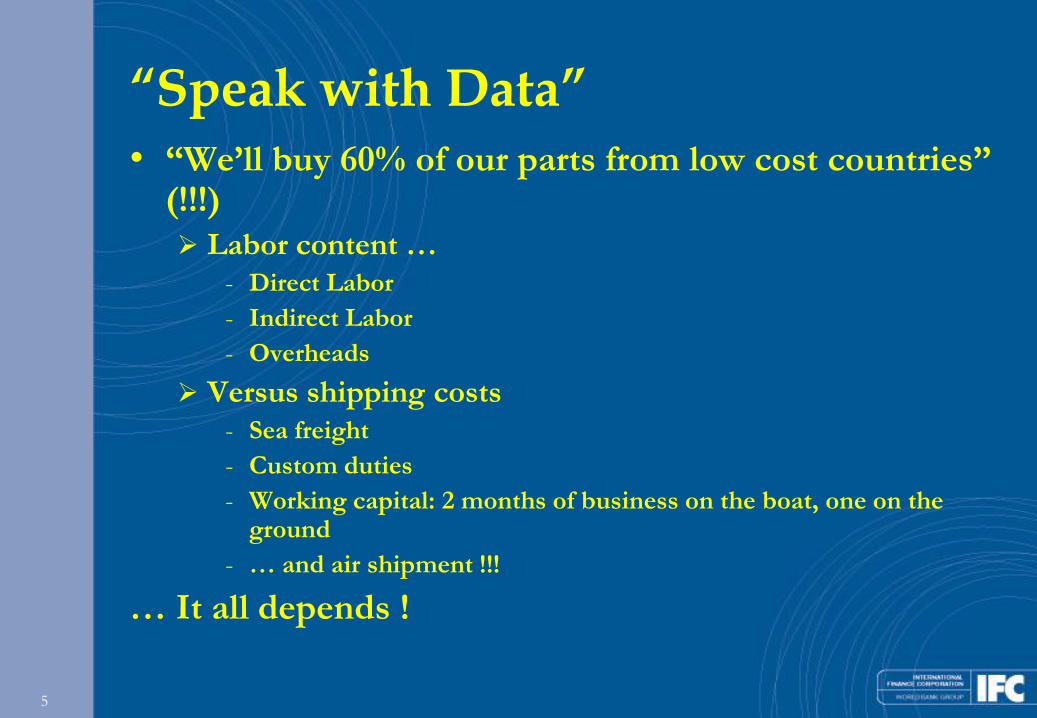

“Speak with Data” • “We’ll buy 60% of our parts from low cost countries”

(!!!)

Labor content … - Direct Labor

- Indirect Labor

- Overheads

Versus shipping costs - Sea freight

- Custom duties

- Working capital: 2 months of business on the boat, one on the ground

- … and air shipment !!!

… It all depends !

6

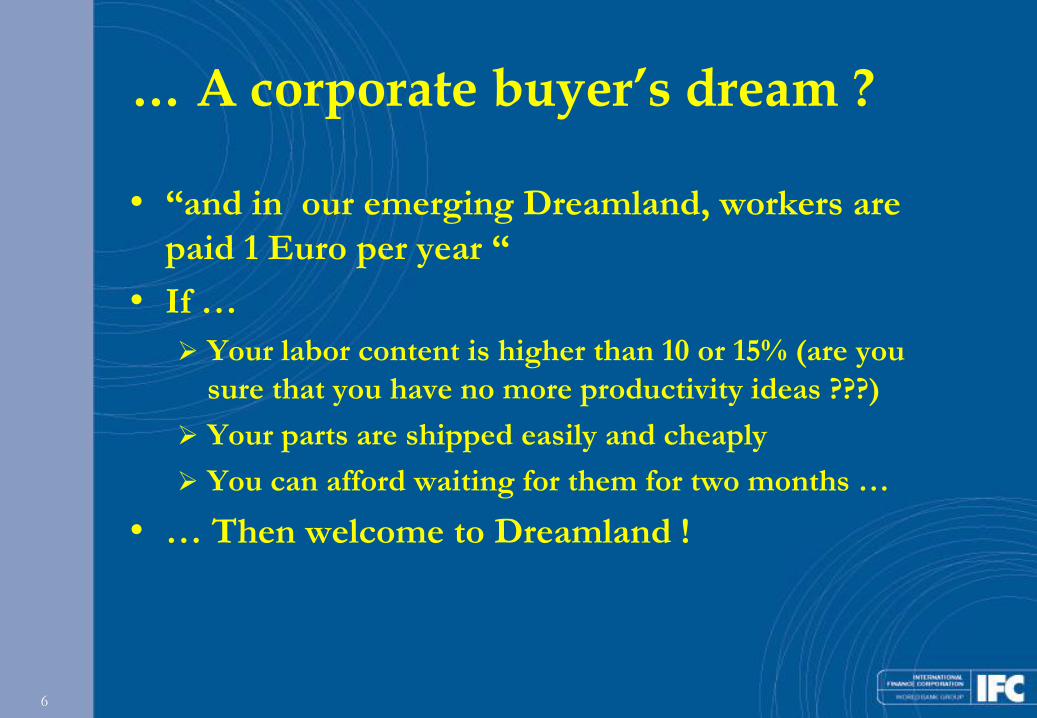

… A corporate buyer’s dream ?

• “and in our emerging Dreamland, workers are

paid 1 Euro per year “

• If …

Your labor content is higher than 10 or 15% (are you

sure that you have no more productivity ideas ???)

Your parts are shipped easily and cheaply

You can afford waiting for them for two months …

• … Then welcome to Dreamland !

7

A corporate buyer’s nightmare ? • In Nightmareland:

Labor costs are probably the highest in the world

One would not fire workers

Cost of land is extremely high

Road are most often congested

Culture is a high barrier to import and exports …

Q: How can one make cars and car parts profitably there ???

A: Welcome to Japan !

(… and Korea will soon follow …)

8

Get to be globally competitive …

• Step 1: Know your shop floor, look for Muda

Cut labor, cut labor, cut labor !

- SMED

- Flows (from your supplier to your customer !)

- Automation, (as a last resort !)

• Step 2: Know your project process, look for Muda

Cut labor, cut labor, cut labor !

- Design sobriety

- Computer aided prototyping

- Computer aided testing

… at home, at the supplier’s, at the customer’s

9

Thou shall love your neighbors !

• Step 3: Leverage your continent

Western/Eastern Europe

U.S.A./Mexico

Korea/China (remember Korea ?)

• The future is in tandems

West now and later:

- Best productivity

- Better cars and parts design

- Closest to western customer

East or South:

- Now: Push to productivity (remember Korea ?)

- Later: Better cars and parts design, closest to customer …

10

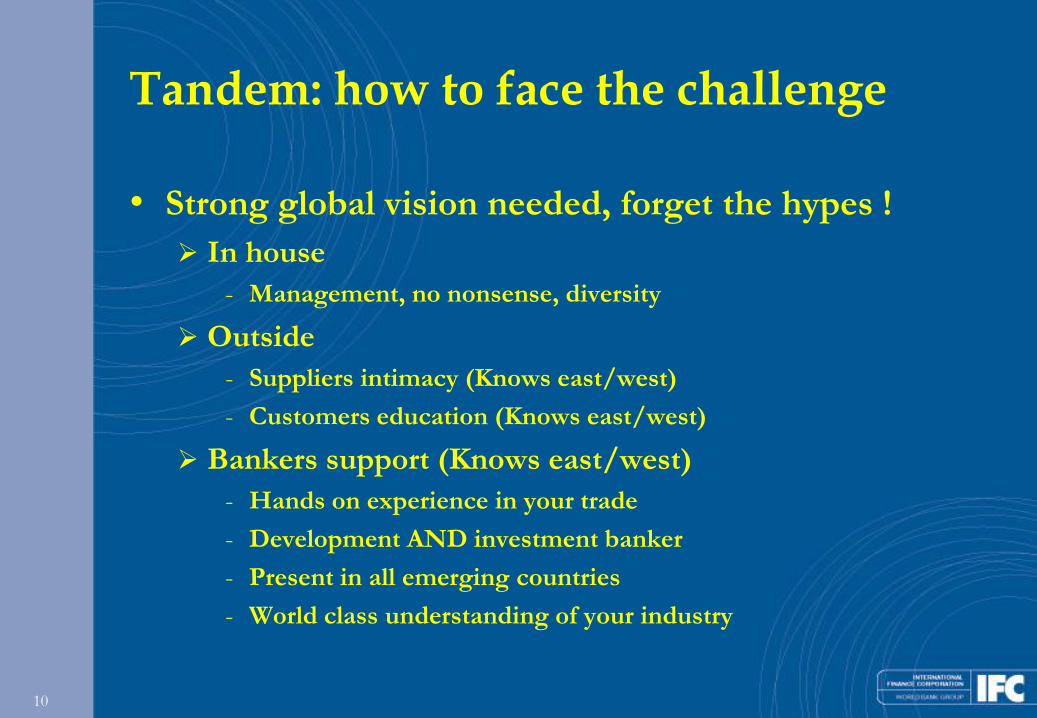

Tandem: how to face the challenge

• Strong global vision needed, forget the hypes !

In house

- Management, no nonsense, diversity

Outside

- Suppliers intimacy (Knows east/west)

- Customers education (Knows east/west)

Bankers support (Knows east/west)

- Hands on experience in your trade

- Development AND investment banker

- Present in all emerging countries

- World class understanding of your industry

11

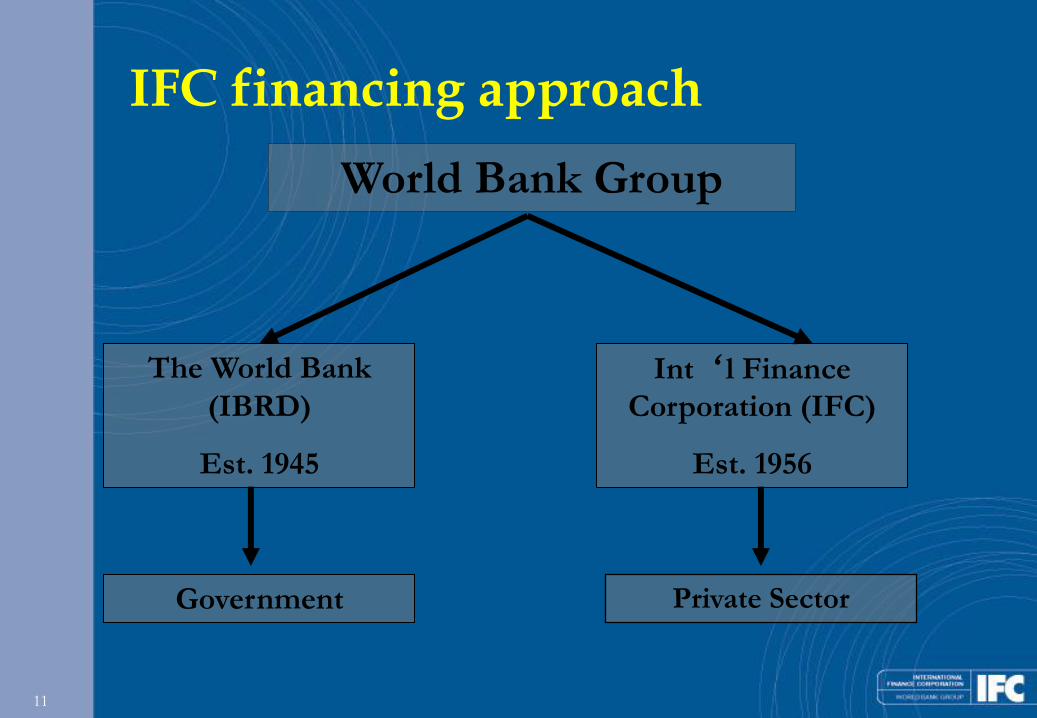

Private Sector

World Bank Group

Int‘l Finance

Corporation (IFC)

Est. 1956

The World Bank

(IBRD)

Est. 1945

Government

IFC financing approach

12

IFC is A Member of the World Bank Group

• World Bank Group institutional roles:

• IBRD lends to governments of middle-income developing countries

• IDA provides concessional loans to governments of the poorest developing countries

•MIGA provides guarantees to foreign investors against noncommercial risk

• IFC is the private sector investment arm

13

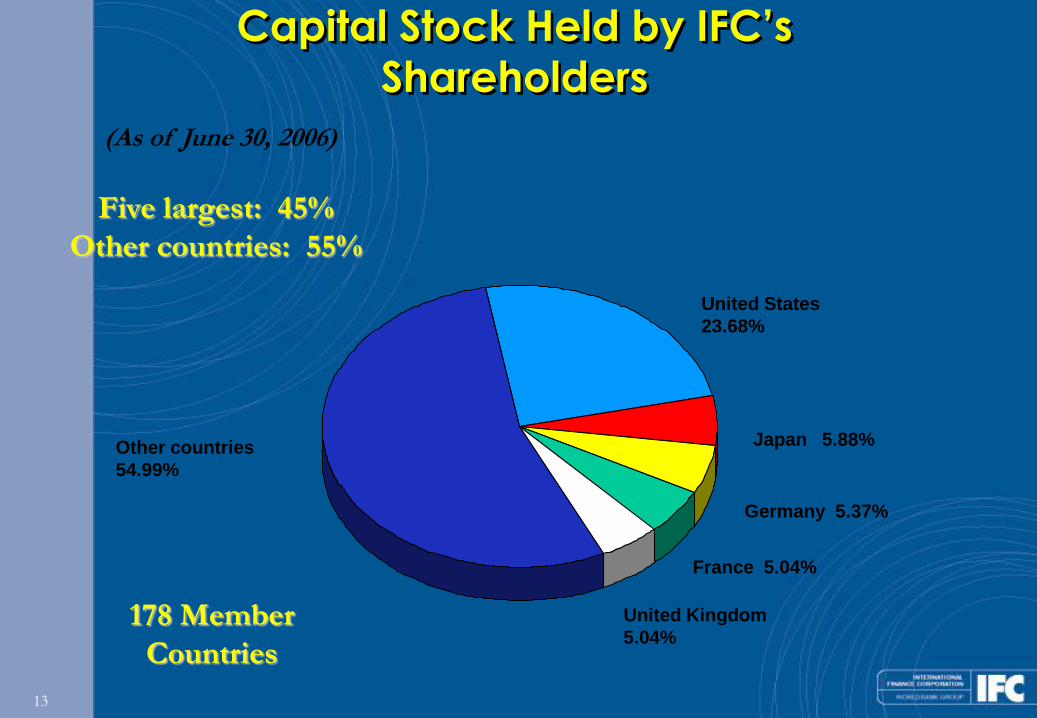

Capital Stock Held by IFC’s

Shareholders

Five largest: 45%

Other countries: 55%

United States

23.68%

Japan 5.88%

Germany 5.37%

France 5.04%

United Kingdom

5.04%

Other countries

54.99%

178 Member

Countries

(As of June 30, 2006)

14

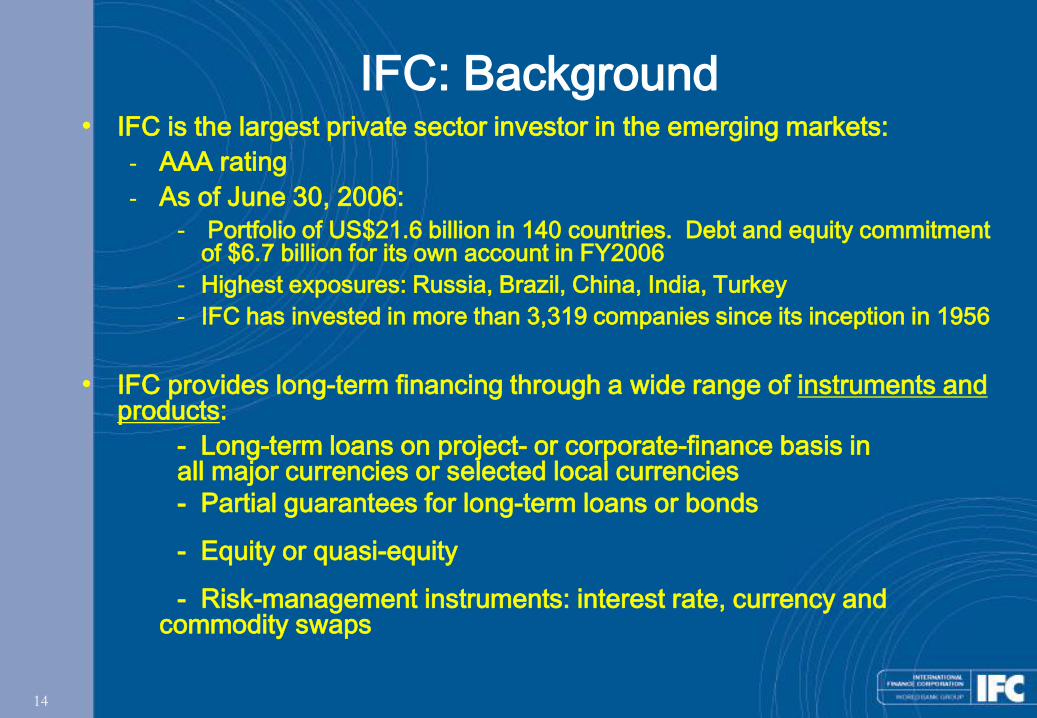

IFC: Background • IFC is the largest private sector investor in the emerging markets:

- AAA rating

- As of June 30, 2006:

- Portfolio of US$21.6 billion in 140 countries. Debt and equity commitment of $6.7 billion for its own account in FY2006

- Highest exposures: Russia, Brazil, China, India, Turkey

- IFC has invested in more than 3,319 companies since its inception in 1956

• IFC provides long-term financing through a wide range of instruments and products:

- Long-term loans on project- or corporate-finance basis in all major currencies or selected local currencies

- Partial guarantees for long-term loans or bonds

- Equity or quasi-equity

- Risk-management instruments: interest rate, currency and commodity swaps

15

IFC IS A LONG-TERM PARTNER

• Involvement from project concept through to completion and beyond through follow-on projects

• Combines the resources of a development bank with the flexibility of an investment bank

• Delivers benefits beyond those purely commercial entities are able to offer

• Experience in working with other financial institutions (commercial banks, international financial institutions, export credit agencies, etc.)

Strengths of IFC as an Investment Partner

16

IFC Offers …

TAILORED FINANCING

• Long tenor debt financing (8-12 years) with flexible grace periods

• Currency of choice (many currencies available, e.g.: Brazilian real, Mexican peso, Thai baht, Indian rupee, South African rand)

• Fixed or floating market-rate pricing

• Ability to mobilize financing

• Equity investments based on anticipated return

• Always a passive investor and never the largest shareholder

17

IFC Offers …

IN-HOUSE EXPERTISE

• In-depth knowledge of regions and markets

• Sector expertise

• Environmental, social and insurance specialists

• Expertise on linkages with small and medium enterprises

(SME)

18

Typical IFC Partners

Western companies expanding into emerging markets seeking:

• Political risk mitigation and country knowledge

• Leveraging of scarce resources

• Lowering financing pressure on parent company’s balance sheet

• Long-term financing for multiple projects in several countries

• Local currency financing

• Local SME supplier financing

19

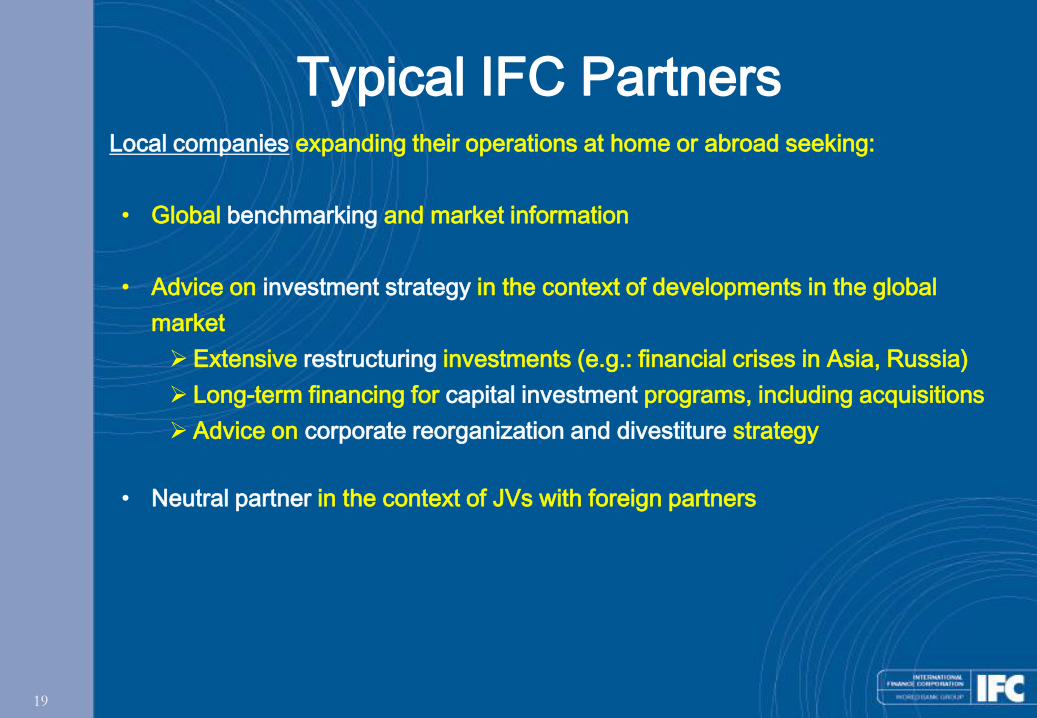

Typical IFC Partners Local companies expanding their operations at home or abroad seeking:

• Global benchmarking and market information

• Advice on investment strategy in the context of developments in the global

market

Extensive restructuring investments (e.g.: financial crises in Asia, Russia)

Long-term financing for capital investment programs, including acquisitions

Advice on corporate reorganization and divestiture strategy

• Neutral partner in the context of JVs with foreign partners

20

IFC and

the Automotive Sector

21

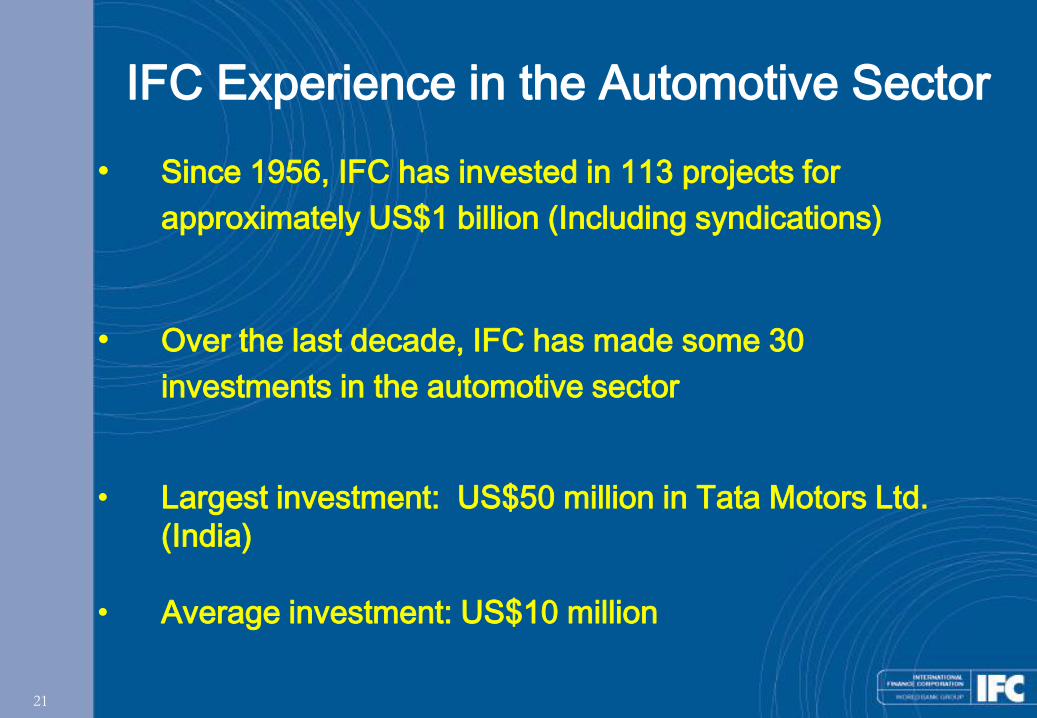

IFC Experience in the Automotive Sector

• Since 1956, IFC has invested in 113 projects for

approximately US$1 billion (Including syndications)

• Over the last decade, IFC has made some 30

investments in the automotive sector

• Largest investment: US$50 million in Tata Motors Ltd.

(India)

• Average investment: US$10 million

22

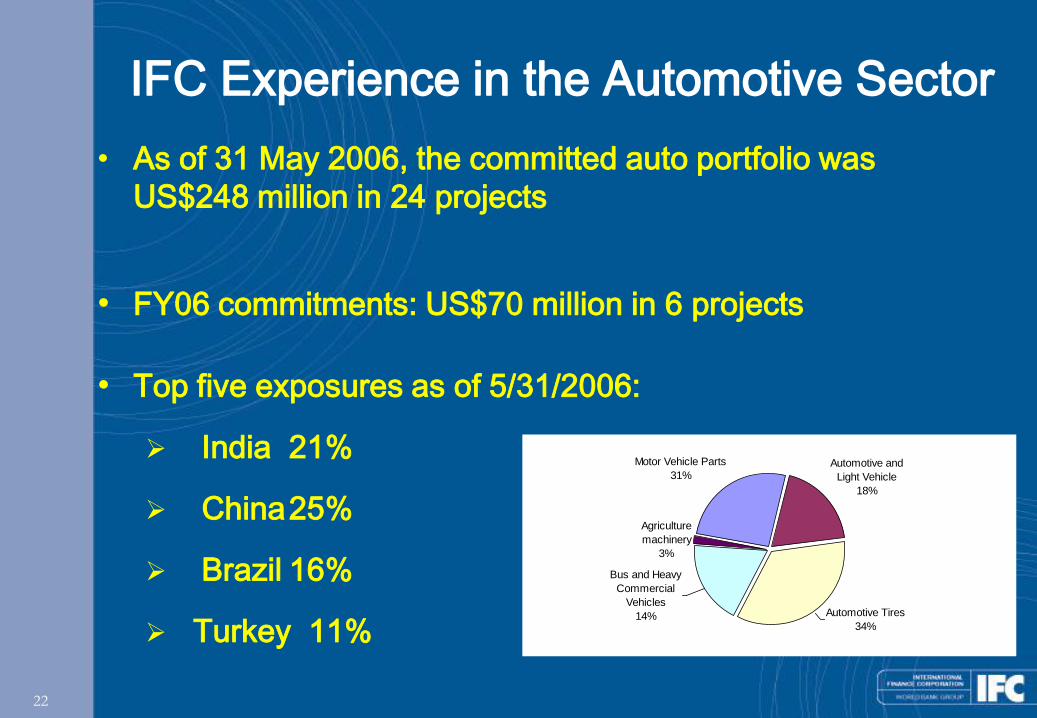

IFC Experience in the Automotive Sector

• As of 31 May 2006, the committed auto portfolio was

US$248 million in 24 projects

• FY06 commitments: US$70 million in 6 projects

• Top five exposures as of 5/31/2006:

India 21%

China 25%

Brazil 16%

Turkey 11%

Agriculture

machinery

3%

Automotive and

Light Vehicle

18%

Motor Vehicle Parts

31%

Automotive Tires

34%

Bus and Heavy

Commercial

Vehicles

14%

23

IFC and the Automotive Sector

• IFC has supported both vehicle and component manufacturers, including:

ThyssenKrupp (JVs in Romania)

Standard Profil (Turkey)

Randon (Brazil)

Marcopolo (Latin America region)

Nemak (Mexico)

Telco (India)

Astra (Indonesia)

Kumho Tires (China)

… and many more …

24

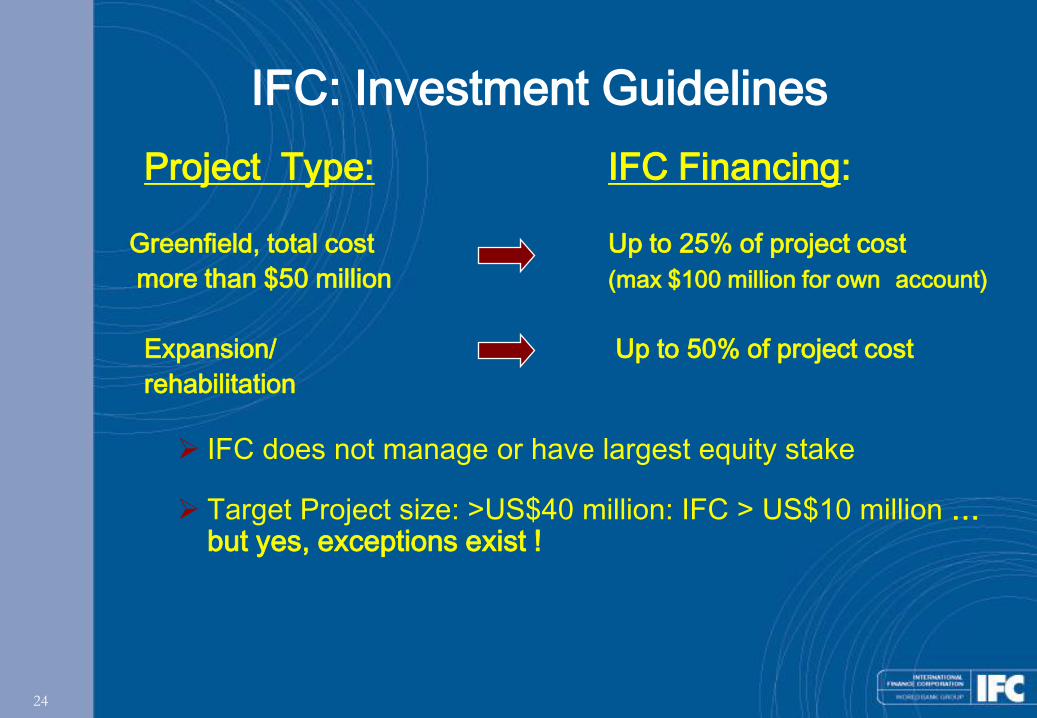

IFC: Investment Guidelines

Project Type: IFC Financing:

Greenfield, total cost Up to 25% of project cost

more than $50 million (max $100 million for own account)

Expansion/ Up to 50% of project cost

rehabilitation

IFC does not manage or have largest equity stake Target Project size: >US$40 million: IFC > US$10 million …

but yes, exceptions exist !

25

Thank you for your attention !

Emmanuel POULIQUEN

Senior Industry Specialist

+1 202 473 9114