ifp 29 tax planning

TRANSCRIPT

7/30/2019 Ifp 29 Tax Planning

http://slidepdf.com/reader/full/ifp-29-tax-planning 1/5

197Financial Planning HandbookPDP

Chapter 29

7/30/2019 Ifp 29 Tax Planning

http://slidepdf.com/reader/full/ifp-29-tax-planning 2/5

198 Financial Planning Handbook PDP

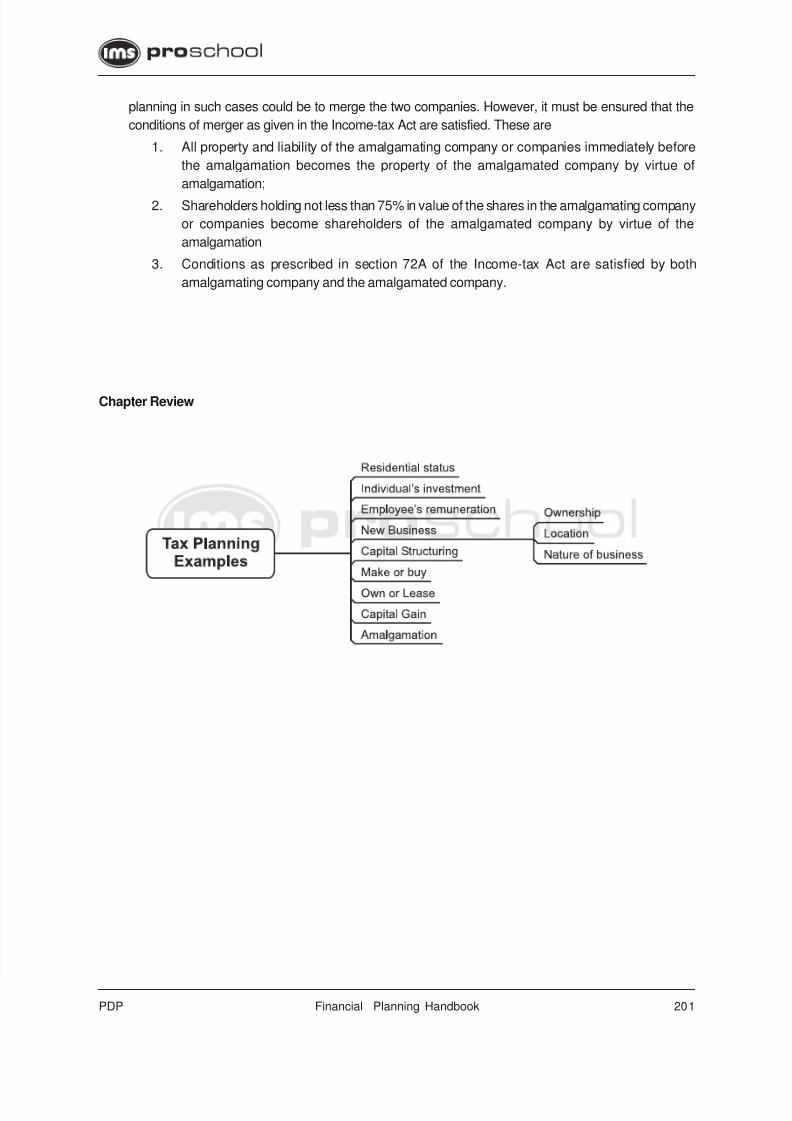

Tax Planning

There is nothing which hurts more than payment of taxes. One question that goes through every tax

payer’s mind is “how can I reduce my tax liability?” Reducing tax liability is not always a bad or illegal

exercise. There are legitimate ways to reduce taxes through proper tax planning and such methods are

always encouraged. But unfortunately, there is also a tendency to reduce tax through illegal or colourable

methods. They are not accepted practice and can invite problems.

There are three methods which are commonly used by the taxpayers to reduce their tax liabilities

Tax evasion,

Tax Avoidance and

Tax Planning

Tax evasion: Dishonest taxpayers try to reduce their taxes by concealing income, inflation of expenses,

falsification of accounts and willful violation of the provisions of the Income-tax Act. Such unethical

practices often create problems for the tax evaders. Tax department not only imposes huge penalties but

also initiates prosecution in such cases.

Tax Avoidance: Tax avoidance is minimizing the incidence of tax by adjusting the affairs in such a

manner that although it is within the four corners of the laws, it is done with a purpose to defraud the

revenue. It is the act of dodging without directly breaking the law. For example if A gives gift to his wife,

the income from the asset gifted will be clubbed in the hand of A. But to avoid this clubbing provision “A”

decides to give gift to B’s wife and B reciprocates it by giving gift to A’s wife. This is not tax planning buttax avoidance.

Such practices are not acceptable. In the words of Justice Rangnath Misra of Supreme Court in the case

of McDowell & Co Limited v CTO [1985] 154 TR 148,

“Tax planning may be legitimate provided it is within the framework of law. Colourable devices cannot be

part of tax planning and it is wrong to encourage or entertain the belief that it is honorable to avoid

payment of tax by resorting to dubious methods.”

Tax Planning: Tax planning is arrangement of financial activities in such a way that maximum tax

benefits, as provided in the income-tax act are availed of. It envisages use of certain exemption,

deductions, rebates and reliefs provided in the act.

Some examples of tax planning are given below:

Residential status: Sometime by better tax planning a taxpayer can avoid becoming resident in a

particular year. The advantage of this is that if he is non-resident in a particular year, he is not liable

to be taxed for his overseas income in India. In case he becomes resident in India for tax purpose,

he is taxed for his worldwide income. However, this may not have any effect if the tax paid abroad on

overseas income is equal to more than the tax payable on such income in India, as the taxpayer is

entitled to get credit of taxes paid abroad in case that income gets taxed in India.

7/30/2019 Ifp 29 Tax Planning

http://slidepdf.com/reader/full/ifp-29-tax-planning 3/5

199Financial Planning HandbookPDP

Individual’s investment: Taxpayer can plan investment in a manner so that overall return is optimum.

This may involve analyzing different investment options taken into consideration, availability of tax

deduction u/s 80C, exemption of interest/dividend income on a particular investment, capital gain,

possibility of exemption from capital gain, rate of return, risk factor, liquidity etc.

Employee’s remuneration: There is no effect on the tax liability in the hand of the employer on

account of designing of salary package of employees. Still, every employer wants to design the

salary package in a way so that the incidence of tax on the employee is kept to minimum. By doing

this, the take home pay of the employee is increased. To design such a package it is necessary to

understand how perquisites and benefits are taxed and which are those perquisites or benefits which

are not taxed or taxed at concessional rate. It is also necessary to understand the how Fringe

Benefit tax is payable, as it may be advisable for the employer to pay FBT instead of letting that

benefit be taxed in the hand of the employee through allowances.

New Business, What should be the form of ownership? : While starting his business, taxpayer

can plan his taxes by evaluating tax implication in different choices available like individual

proprietorship, partnership firm or company.

Proprietorship is easy to establish with less cost and with no restriction on enjoyment of profit. The taxrate is also less because of slab system of taxation. However, it is suitable for small business only.

Partnership firm: If there is more than one person having common interest in the business then it

makes sense to incorporate as partnership firm. The tax liability may be a little more than proprietorship

but firm can reduce this tax liability by taking advantage of initial exemption available in the hand of

various individual partners by providing for their salary and interest within the given limit. This will

work if the partners have no other source of income.

In the case of company the tax rate is highest and the dividend is further subjected to tax. However,

the limited liability and ability to raise finance are also important factors other than taxes. Also there

is no limitation on the salary payable to Director.

New Business, Location of Business: the correct selection of location of business also plays animportant role in Management decision making. There are a few locational tax advantages in the

Income Tax Act which must be considered while arriving at the decision. In other words, when one is

trying to start a new business or start a new unit in the existing business, it can consider locating

business in a place so that it get some tax exemption which will reduce the tax liability. Important

sections of income-tax act which will help in this tax planning are:

1. Section 10A: Newly established undertaking in Free Trade Zone, Electronic Hardware

Technology Park or Software Technology Park.

2. Section 10AA: Newly established undertaking in Special Economy Zone.

3. Section 10B: Newly established 100% Export Oriented Undertaking.

4. Section 10BA: Newly established manufacturing unit producing hand made article or thingsor artistic value with wood (not being imported) as the main raw material. At least 90% must

be exported.

5. Section 80IB: Industrial undertaking located in industrial backward state or district.

6. Section 80IC: Undertakings or enterprises located in notified area in North Eastern State,

State of Sikkim, Himachal Pradesh, Uttranchal.

New Business: Nature of business: Before starting a business it is important to know various tax

incentives available under the Income Tax Act for some specific types of business. Most of such

exemptions have now become non-existent. However, in the following cases, fresh business may

still get tax exemption.

7/30/2019 Ifp 29 Tax Planning

http://slidepdf.com/reader/full/ifp-29-tax-planning 4/5

200 Financial Planning Handbook PDP

1. Export Business : Under Section 10A, 10AA, 10B, 10BA,

2. Developer of SEZ: 80IAB

3. Infrastructure Development: 80IA

4. Business of Scientific Research & development, production/refining of mineral oil,

development and building of housing project approved by a local authority, operation &maintenance of hospital in rural area, processing, preservation & packaging of fruits or

vegetables: Section 80IB

Management Decision - Capital Structuring: In Financial Management Course, students are taught

to understand the basis of arriving at the decision about capital structure, i .e. debt, equity or preference

shares. The factors like risk, cost and control are relevant. In addition one must understand the tax

implication and should also consider this while deciding the best mix to optimize shareholder’s

return. Dividend on share is not allowable deduction in the hand of the company; however, interest on

debt paid is allowable deduction. The cost of raising equity is a capital expenditure which can only be

capitalized and amortized in certain conditions (may not be amortized in all cases). However, the

cost of raising debt is allowed as deduction. This has direct implication in calculating corporate tax

liability. On dividend from Indian company, the company is liable to pay DWT and then such dividendis exempt in the hand of the shareholders.

Management Decision: Make or buy: In Financial management course, students are taught to

understand the basis of arriving at the make or buy decision considering capacity utilization, inadequacy

of fund, cost of fund, latest technology, variable cost of manufacturing etc. While arriving at this decision

due consideration must also be given to tax implication as this will certainly influence the decision. One

must consider that if one decides to make, there is less outflow due to tax benefit on depreciation/

interest and tax advantage available due to location of manufacturing in a particular area. These tax

advantages have already been listed earlier. If the company is able to take advantage of any of these

tax incentives, the decision to make may come out better in comparison to decision to buy.

Management Decision: Own or Lease: Concept of leasing is gaining immense popularity. One privateairline has recently sold and taken back the same aircraft on lease. In the process it got some funds in

its account. One factor which influenced its decision was that the lease rental paid to foreign enterprise

is not subject to withholding tax if the lease agreement has been approved by the Central Government.

Other factors which must be considered for tax implications are that in case of buying the asset, the

assessee will be entitled to deduction on the account of depreciation and interest, while in case of lease

he will be entitled to deduction on account of lease rental which will be higher in the initial years. Hence,

tax consideration will also influence management decision to own or lease.

Capital Gain: It is important to understand that long term capital gain tax is less than normal tax on

business or interest income. Further in case of equities, where security transaction tax is paid, there

is no long-term capital gain and short-term capital gain is only charged at 10%. Even if the taxpayer

has long term capital gain he has the opportunity to reduce it by properly investing it in approved

bonds of National Highway Authority or Rural electrification Corporation under section 54EC or investing

in house property under section 54 and 54F. Thus if some one has an option to earn regularly or

through capital gain, the earning through capital gain will attract less tax. This will influence the

investment decision of the taxpayer.

Amalgamation: There is limitation in the Income-tax Act for carry forward of losses. It is quite possible

that one of the group companies is making profit and another group company is making losses. Some

of these losses may be getting lapsed due to time limitation. One can not transfer profit of one Group

Company to another just like that as it would amount to tax avoidance and can invite trouble. The tax

7/30/2019 Ifp 29 Tax Planning

http://slidepdf.com/reader/full/ifp-29-tax-planning 5/5

201Financial Planning HandbookPDP

Chapter Review

planning in such cases could be to merge the two companies. However, it must be ensured that the

conditions of merger as given in the Income-tax Act are satisfied. These are

1. All property and liability of the amalgamating company or companies immediately before

the amalgamation becomes the property of the amalgamated company by virtue of

amalgamation;

2. Shareholders holding not less than 75% in value of the shares in the amalgamating company

or companies become shareholders of the amalgamated company by virtue of the

amalgamation

3. Conditions as prescribed in section 72A of the Income-tax Act are satisfied by both

amalgamating company and the amalgamated company.