ifrs 4 / ifrs 9 pre- study allianz se · pdf file1/1/2018 · ifrs 4 / ifrs 9...

TRANSCRIPT

IFRS 4 / IFRS 9 Pre-study Allianz SE Major challenges and architectural conclusions

Dr. Jens Hanker, Executive Vice President, Allianz SE Vaike Metzger, Partner, KPMG SAP Financial Services Forum London, September 9, 2014

2 Pre-Study IFRS 4/9

Agenda

1 IFRS 4 / IFRS 9 challenges

2 Allianz Group pre-study

3 Major gaps identified

4 Conclusions for a future finance architecture

5 Audit perspective: Compliance in the context of IFRS 4 / 9

3 Pre-Study IFRS 4/9

Agenda

1 IFRS 4 / IFRS 9 challenges

2 Allianz Group pre-study

3 Major gaps identified

4 Conclusions for a future finance architecture

5 Audit perspective: Compliance in the context of IFRS 4 / 9

4 Pre-Study IFRS 4/9

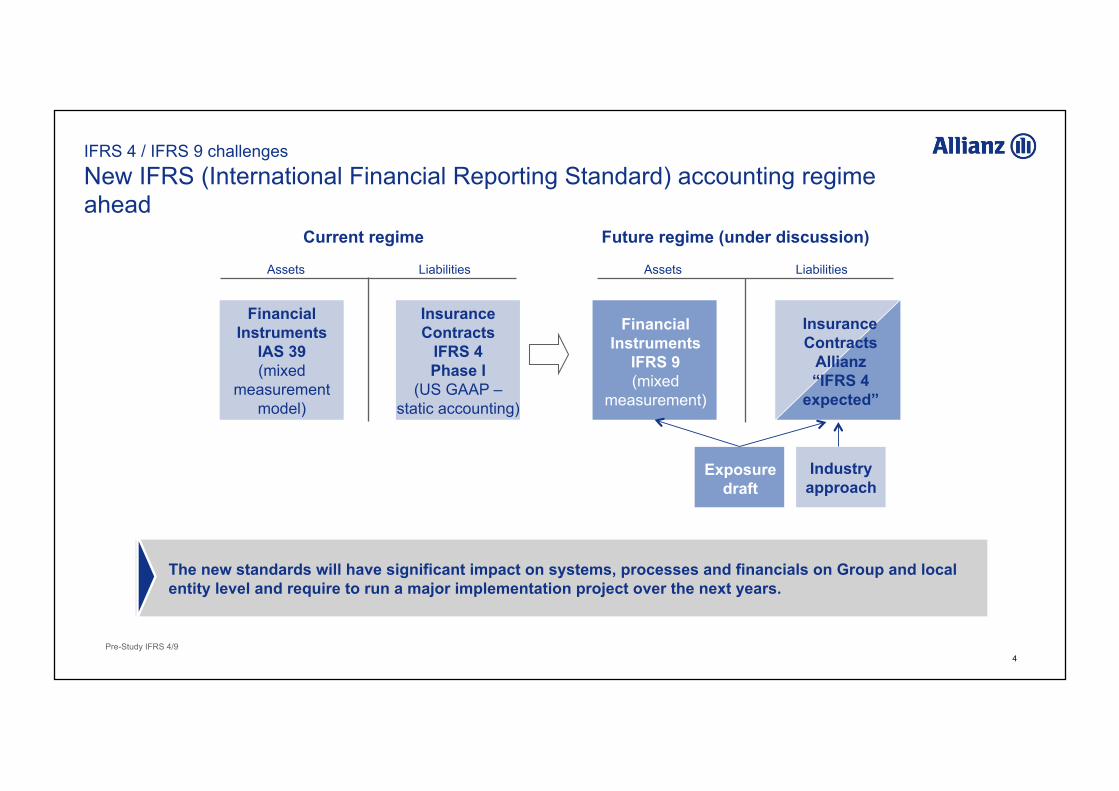

Insurance Contracts

IFRS 4 Phase I

(US GAAP – static accounting)

Current regime Future regime (under discussion)

Financial Instruments

IAS 39 (mixed

measurement model)

Financial Instruments

IFRS 9 (mixed

measurement)

Assets Liabilities Assets Liabilities

The new standards will have significant impact on systems, processes and financials on Group and local entity level and require to run a major implementation project over the next years.

Exposure draft

Industry approach

Insurance Contracts

Allianz “IFRS 4

expected”

IFRS 4 / IFRS 9 challenges New IFRS (International Financial Reporting Standard) accounting regime ahead

5 Pre-Study IFRS 4/9

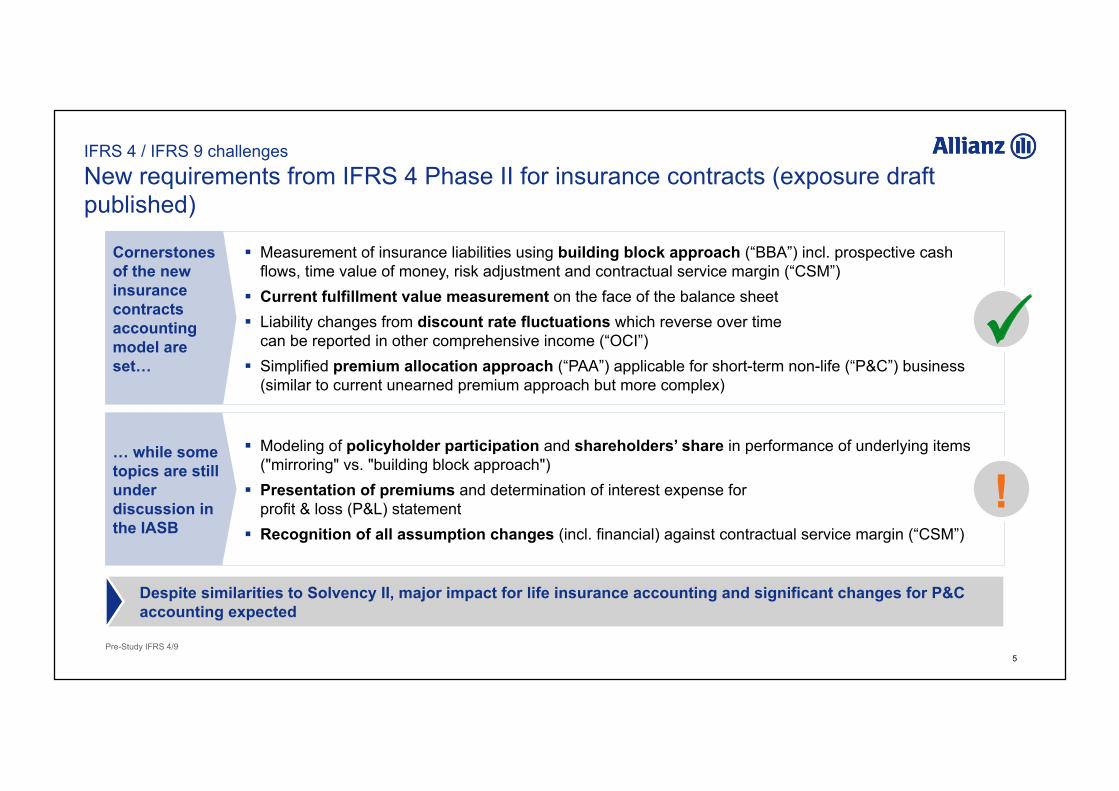

§ Measurement of insurance liabilities using building block approach (“BBA”) incl. prospective cash flows, time value of money, risk adjustment and contractual service margin (“CSM”)

§ Current fulfillment value measurement on the face of the balance sheet § Liability changes from discount rate fluctuations which reverse over time

can be reported in other comprehensive income (“OCI”) § Simplified premium allocation approach (“PAA”) applicable for short-term non-life (“P&C”) business

(similar to current unearned premium approach but more complex)

Cornerstones of the new insurance contracts accounting model are set…

§ Modeling of policyholder participation and shareholders’ share in performance of underlying items ("mirroring" vs. "building block approach")

§ Presentation of premiums and determination of interest expense for profit & loss (P&L) statement

§ Recognition of all assumption changes (incl. financial) against contractual service margin (“CSM”)

… while some topics are still under discussion in the IASB

Despite similarities to Solvency II, major impact for life insurance accounting and significant changes for P&C accounting expected

!

IFRS 4 / IFRS 9 challenges New requirements from IFRS 4 Phase II for insurance contracts (exposure draft published)

6 Pre-Study IFRS 4/9

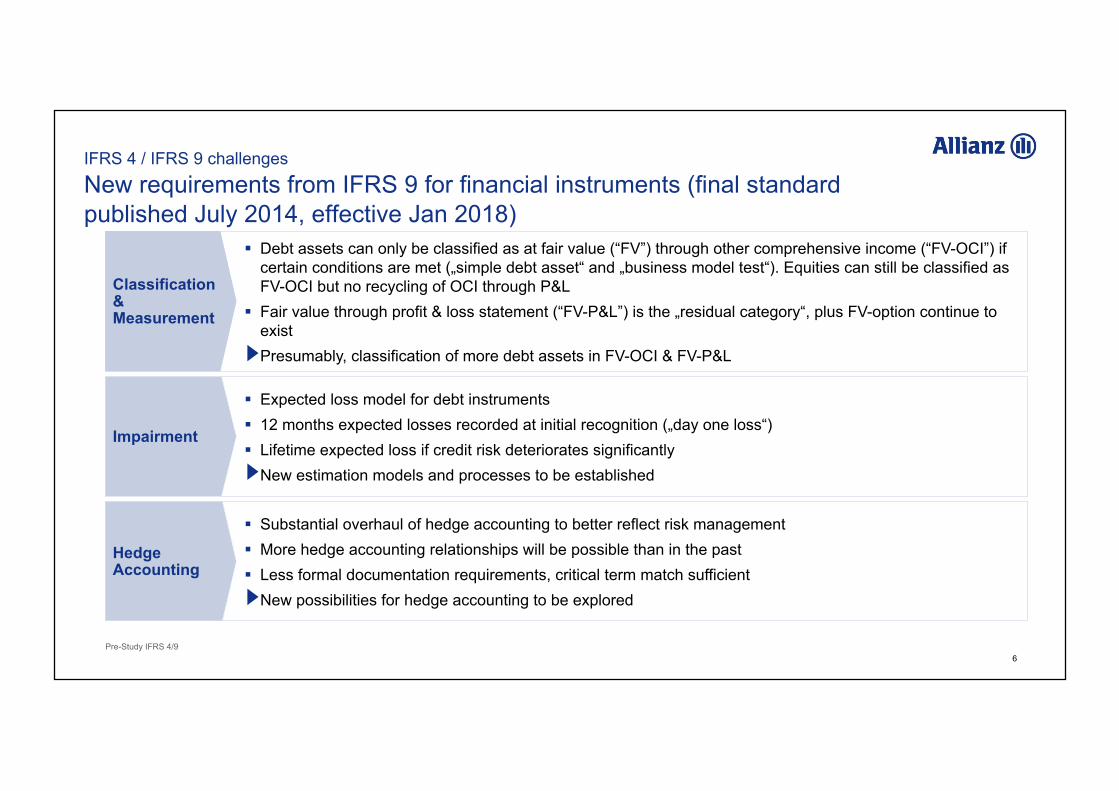

Classification & Measurement

§ Debt assets can only be classified as at fair value (“FV”) through other comprehensive income (“FV-OCI”) if certain conditions are met („simple debt asset“ and „business model test“). Equities can still be classified as FV-OCI but no recycling of OCI through P&L

§ Fair value through profit & loss statement (“FV-P&L”) is the „residual category“, plus FV-option continue to exist

Presumably, classification of more debt assets in FV-OCI & FV-P&L

Impairment

§ Expected loss model for debt instruments § 12 months expected losses recorded at initial recognition („day one loss“) § Lifetime expected loss if credit risk deteriorates significantly

New estimation models and processes to be established

Hedge Accounting

§ Substantial overhaul of hedge accounting to better reflect risk management § More hedge accounting relationships will be possible than in the past § Less formal documentation requirements, critical term match sufficient

New possibilities for hedge accounting to be explored

IFRS 4 / IFRS 9 challenges New requirements from IFRS 9 for financial instruments (final standard published July 2014, effective Jan 2018)

7 Pre-Study IFRS 4/9

Agenda

1 IFRS 4 / IFRS 9 challenges

2 Allianz Group pre-study

3 Major gaps identified

4 Conclusions for a future finance architecture

5 Audit perspective: Compliance in the context of IFRS 4 / 9

8 Pre-Study IFRS 4/9

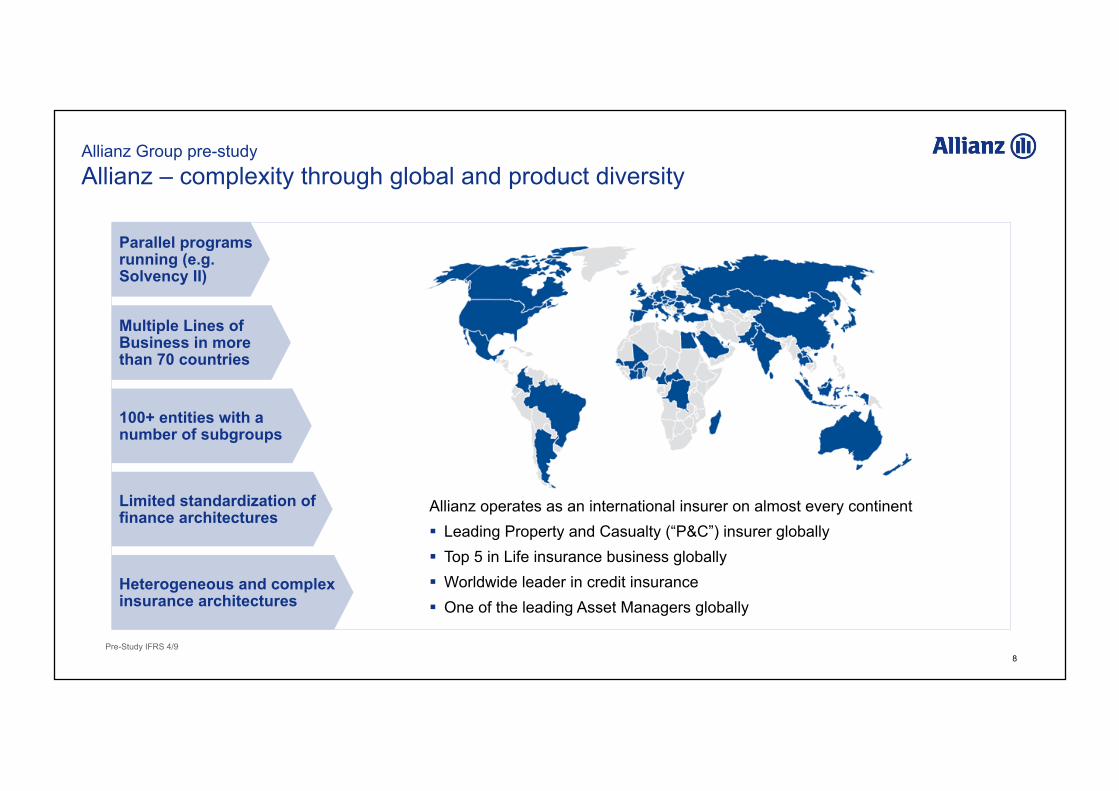

Allianz operates as an international insurer on almost every continent § Leading Property and Casualty (“P&C”) insurer globally § Top 5 in Life insurance business globally § Worldwide leader in credit insurance § One of the leading Asset Managers globally

Parallel programs running (e.g. Solvency II)

Heterogeneous and complex insurance architectures

Limited standardization of finance architectures

100+ entities with a number of subgroups

Multiple Lines of Business in more than 70 countries

Allianz Group pre-study Allianz – complexity through global and product diversity

9 Pre-Study IFRS 4/9

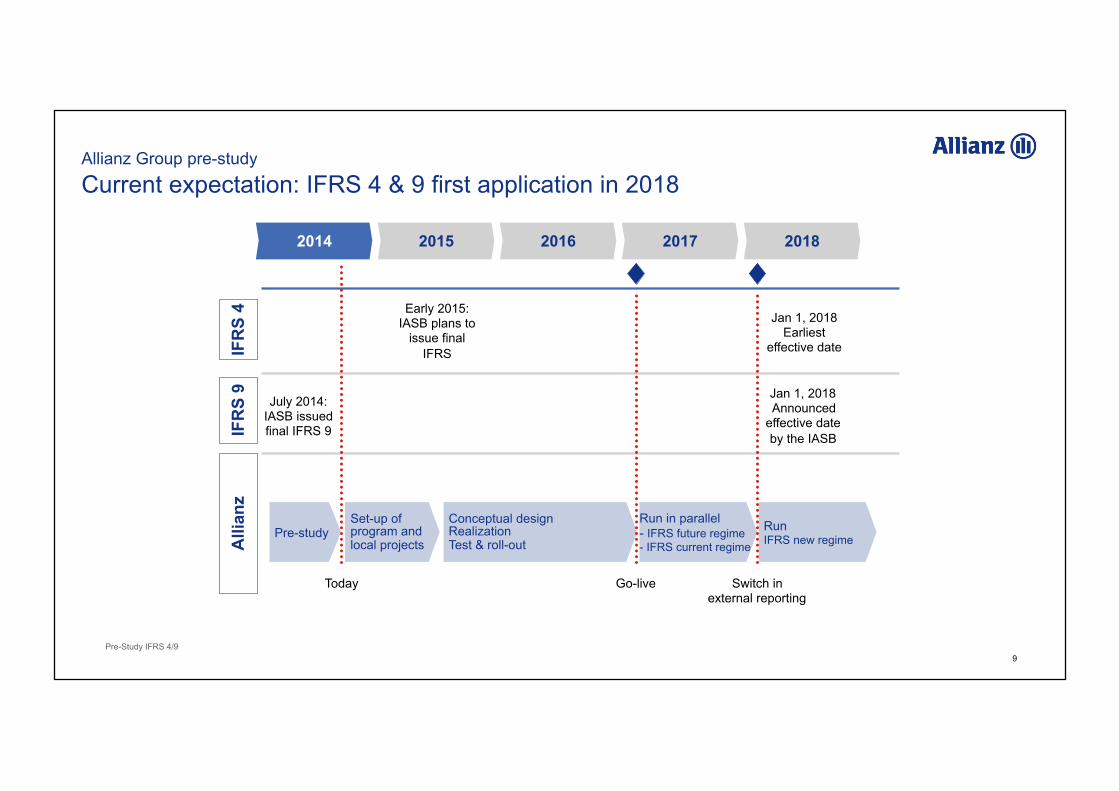

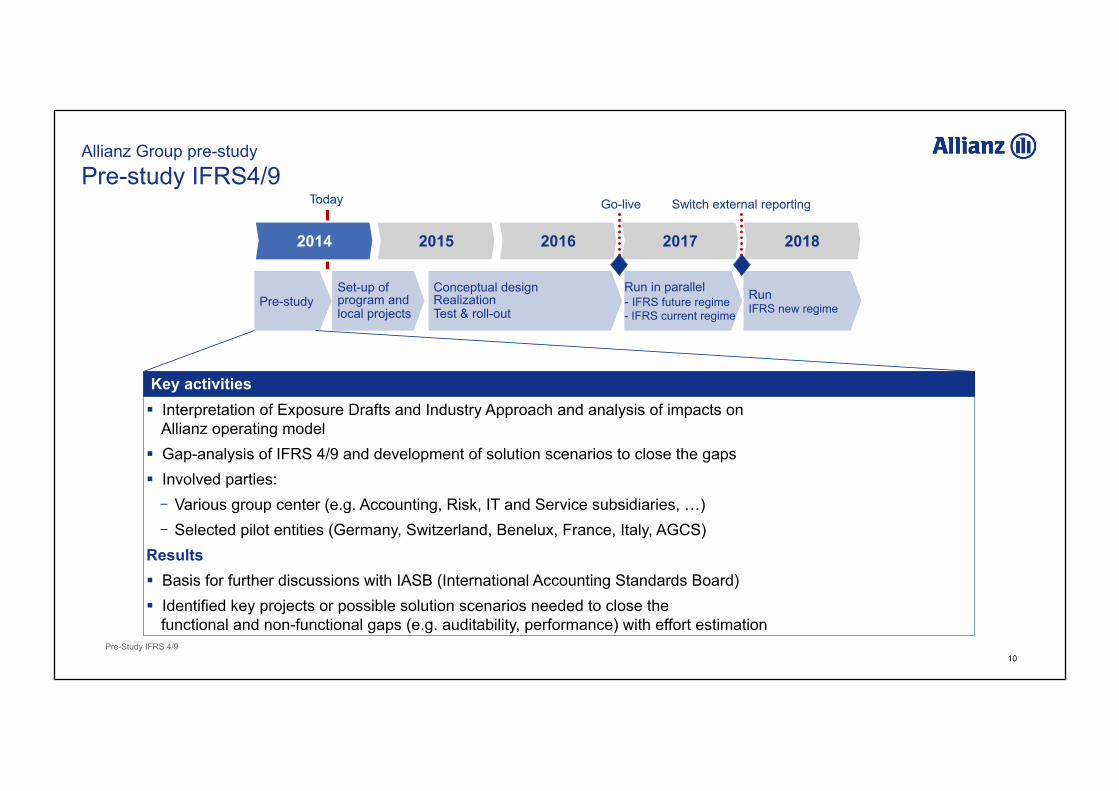

July 2014: IASB issued final IFRS 9

Pre-study Set-up of program and local projects

Conceptual design Realization Test & roll-out

Run IFRS new regime

Run in parallel - IFRS future regime - IFRS current regime

Today

IFR

S 4

IFR

S 9

Early 2015: IASB plans to

issue final IFRS

Jan 1, 2018 Earliest

effective date

Jan 1, 2018 Announced

effective date by the IASB

Alli

anz

Go-live Switch in external reporting

2014 2015 2018 2017 2016

Allianz Group pre-study Current expectation: IFRS 4 & 9 first application in 2018

10 Pre-Study IFRS 4/9

2018

§ Interpretation of Exposure Drafts and Industry Approach and analysis of impacts on Allianz operating model

§ Gap-analysis of IFRS 4/9 and development of solution scenarios to close the gaps § Involved parties: - Various group center (e.g. Accounting, Risk, IT and Service subsidiaries, …) - Selected pilot entities (Germany, Switzerland, Benelux, France, Italy, AGCS)

Results § Basis for further discussions with IASB (International Accounting Standards Board) § Identified key projects or possible solution scenarios needed to close the

functional and non-functional gaps (e.g. auditability, performance) with effort estimation

2014 2015 2017 2016

Today

Pre-study Set-up of program and local projects

Conceptual design Realization Test & roll-out

Run IFRS new regime

Go-live

Key activities

Switch external reporting

Run in parallel - IFRS future regime - IFRS current regime

Allianz Group pre-study Pre-study IFRS4/9

11 Pre-Study IFRS 4/9

Agenda

1 IFRS 4 / IFRS 9 challenges

2 Allianz Group pre-study

3 Major gaps identified

4 Conclusions for a future finance architecture

5 Audit perspective: Compliance in the context of IFRS 4 / 9

12 Pre-Study IFRS 4/9

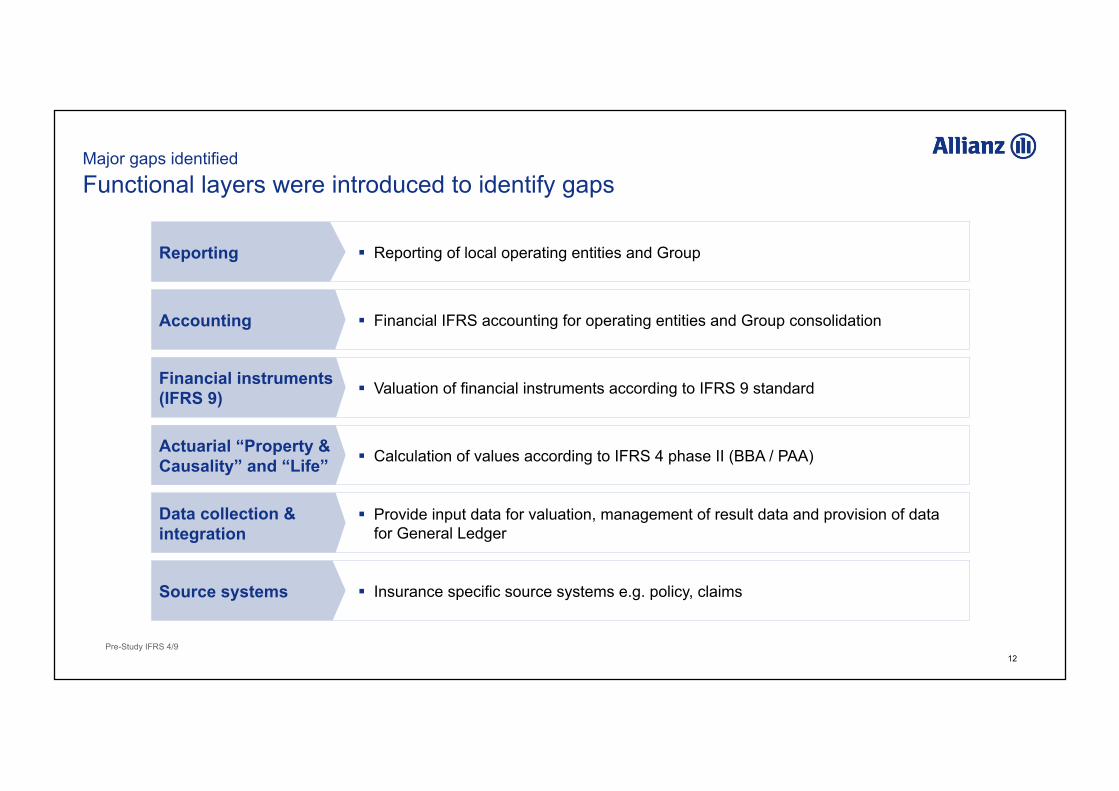

Accounting

Reporting

Actuarial “Property & Causality” and “Life”

Financial instruments (IFRS 9)

Data collection & integration

Source systems

§ Reporting of local operating entities and Group

§ Financial IFRS accounting for operating entities and Group consolidation

§ Valuation of financial instruments according to IFRS 9 standard

§ Calculation of values according to IFRS 4 phase II (BBA / PAA)

§ Provide input data for valuation, management of result data and provision of data for General Ledger

§ Insurance specific source systems e.g. policy, claims

Major gaps identified Functional layers were introduced to identify gaps

13 Pre-Study IFRS 4/9

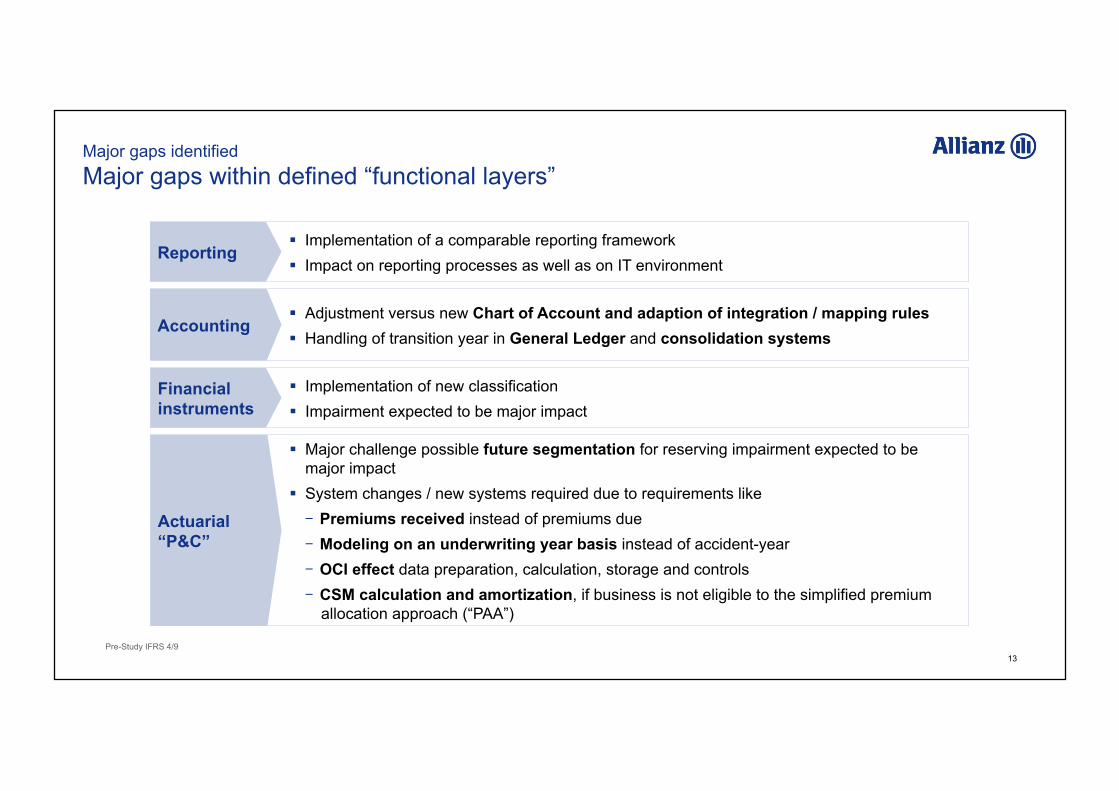

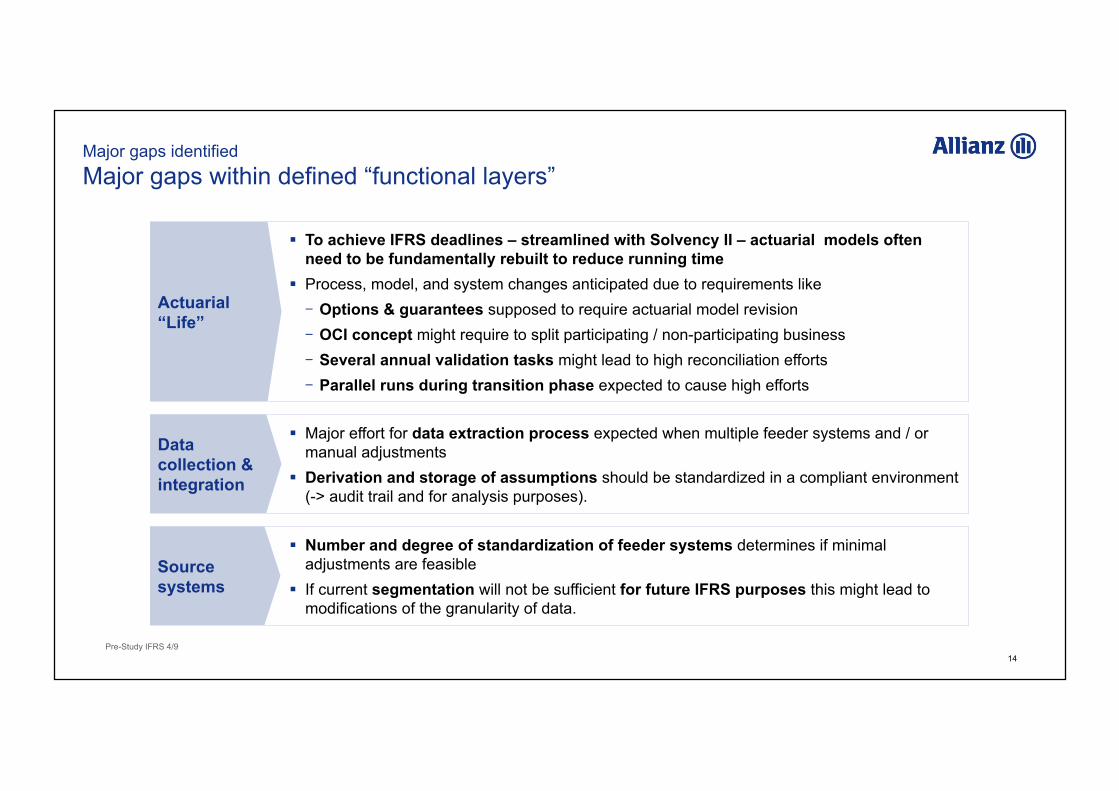

Major gaps identified Major gaps within defined “functional layers”

§ Implementation of a comparable reporting framework § Impact on reporting processes as well as on IT environment

Reporting

§ Adjustment versus new Chart of Account and adaption of integration / mapping rules § Handling of transition year in General Ledger and consolidation systems

§ Implementation of new classification § Impairment expected to be major impact

Financial instruments

Accounting

§ Major challenge possible future segmentation for reserving impairment expected to be major impact

§ System changes / new systems required due to requirements like - Premiums received instead of premiums due - Modeling on an underwriting year basis instead of accident-year - OCI effect data preparation, calculation, storage and controls - CSM calculation and amortization, if business is not eligible to the simplified premium

allocation approach (“PAA”)

Actuarial “P&C”

14 Pre-Study IFRS 4/9

§ Number and degree of standardization of feeder systems determines if minimal adjustments are feasible

§ If current segmentation will not be sufficient for future IFRS purposes this might lead to modifications of the granularity of data.

Major gaps identified Major gaps within defined “functional layers”

§ To achieve IFRS deadlines – streamlined with Solvency II – actuarial models often need to be fundamentally rebuilt to reduce running time

§ Process, model, and system changes anticipated due to requirements like - Options & guarantees supposed to require actuarial model revision - OCI concept might require to split participating / non-participating business - Several annual validation tasks might lead to high reconciliation efforts - Parallel runs during transition phase expected to cause high efforts

Actuarial “Life”

§ Major effort for data extraction process expected when multiple feeder systems and / or manual adjustments

§ Derivation and storage of assumptions should be standardized in a compliant environment (-> audit trail and for analysis purposes).

Data collection & integration

Source systems

15 Pre-Study IFRS 4/9

Agenda

1 IFRS 4 / IFRS 9 challenges

2 Allianz Group pre-study

3 Major gaps identified

4 Conclusions for a future finance architecture

5 Audit perspective: Compliance in the context of IFRS 4 / 9

16 Pre-Study IFRS 4/9

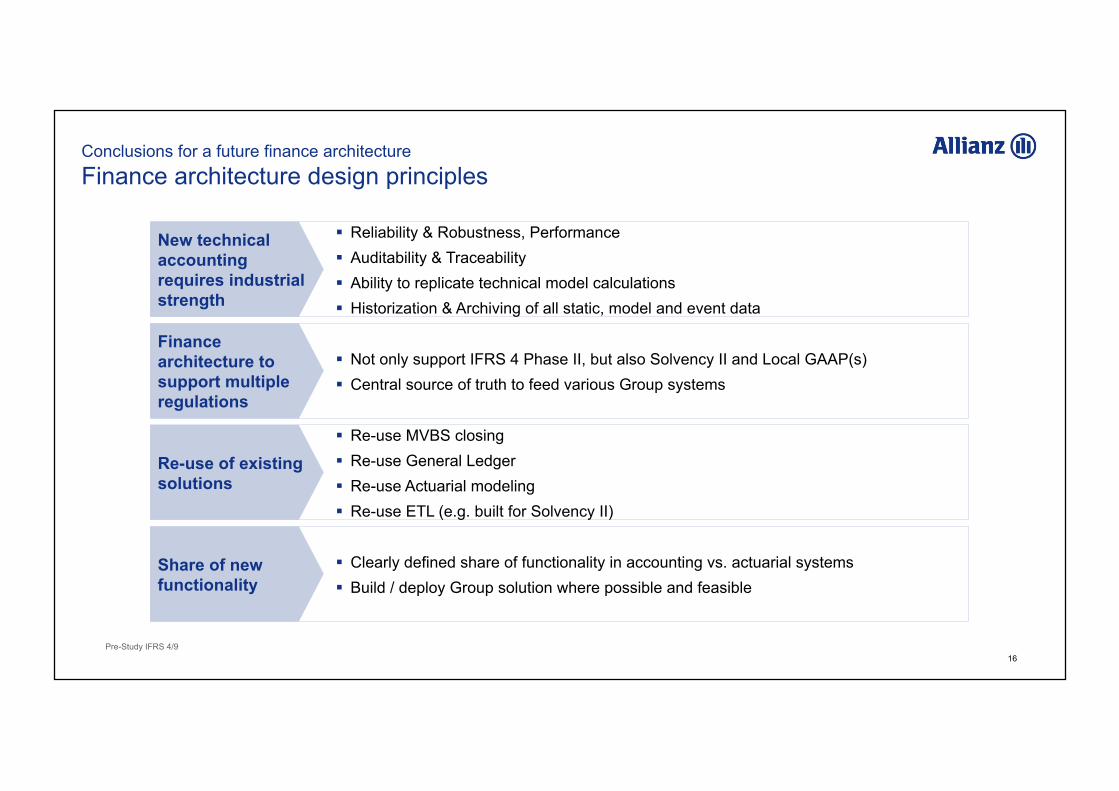

§ Reliability & Robustness, Performance § Auditability & Traceability § Ability to replicate technical model calculations § Historization & Archiving of all static, model and event data

New technical accounting requires industrial strength

§ Not only support IFRS 4 Phase II, but also Solvency II and Local GAAP(s) § Central source of truth to feed various Group systems

Finance architecture to support multiple regulations

§ Re-use MVBS closing § Re-use General Ledger § Re-use Actuarial modeling § Re-use ETL (e.g. built for Solvency II)

Re-use of existing solutions

§ Clearly defined share of functionality in accounting vs. actuarial systems § Build / deploy Group solution where possible and feasible

Share of new functionality

Conclusions for a future finance architecture Finance architecture design principles

17 Pre-Study IFRS 4/9

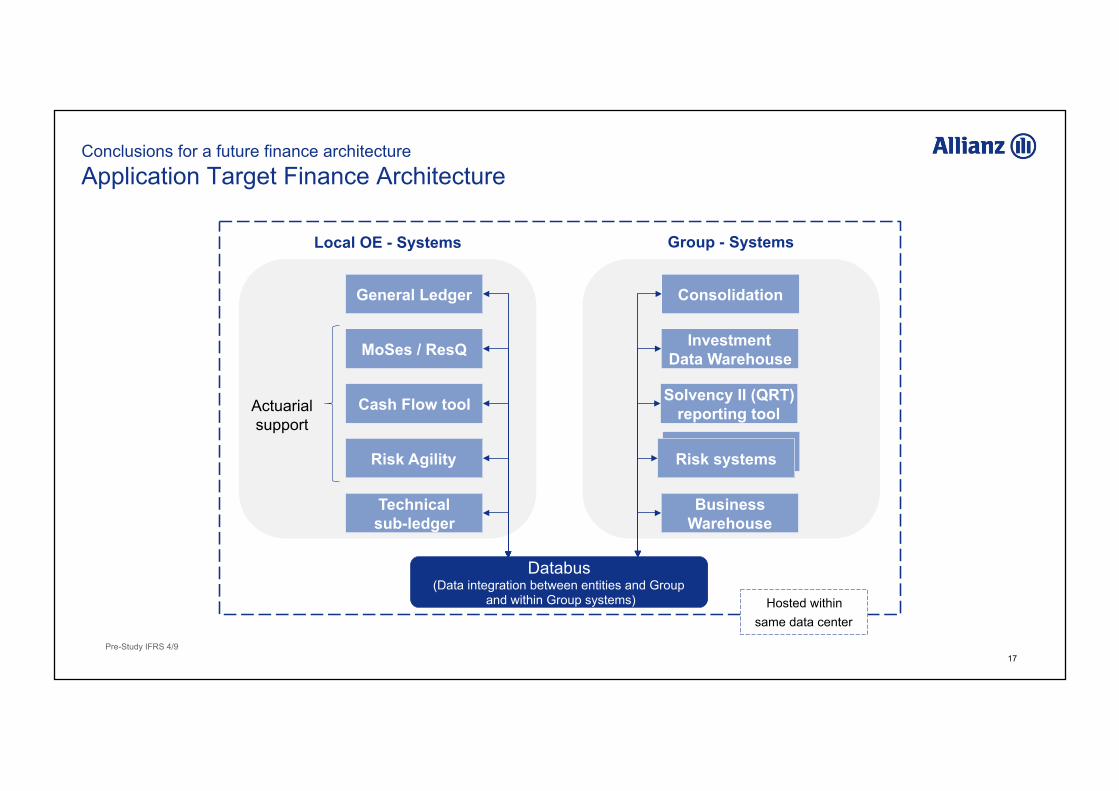

Conclusions for a future finance architecture Application Target Finance Architecture

General Ledger

Cash Flow tool

Risk Agility

MoSes / ResQ

Databus (Data integration between entities and Group

and within Group systems) Hosted within same data center

Local OE - Systems Group - Systems

Investment Data Warehouse

Solvency II (QRT) reporting tool

Risk systems

Consolidation

Technical sub-ledger

Business Warehouse

Actuarial support

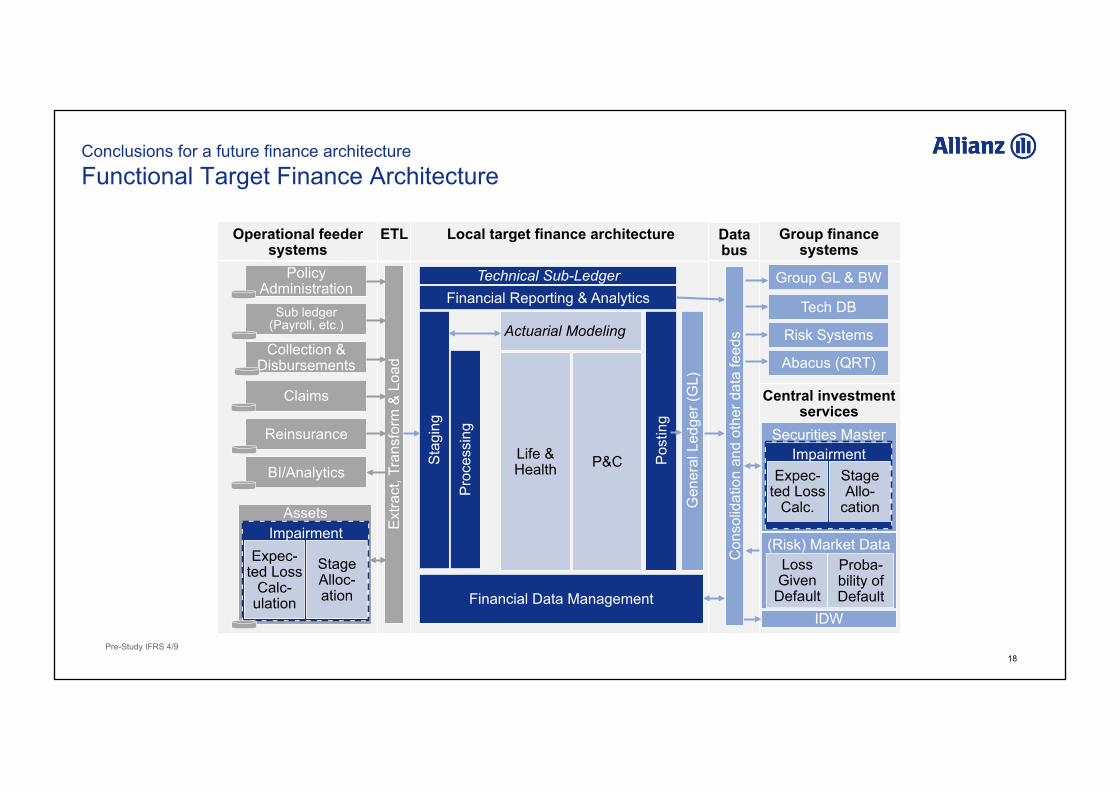

18 Pre-Study IFRS 4/9

ETL Operational feeder systems

Policy Administration

Assets

Collection & Disbursements

Claims E

xtra

ct, T

rans

form

& L

oad

Local target finance architecture Group finance systems

Central investment services

Group GL & BW

Tech DB

IDW

Sub ledger (Payroll, etc.)

Data bus

Risk Systems

Abacus (QRT)

(Risk) Market Data

Securities Master

Life & Health P&C

Actuarial Modeling

Sta

ging

Pos

ting

Technical Sub-Ledger

Pro

cess

ing

Financial Data Management

Financial Reporting & Analytics

Gen

eral

Led

ger (

GL)

Impairment Expec-

ted Loss Calc-

ulation

Stage Alloc-ation

Proba-bility of Default

Loss Given

Default

Reinsurance

BI/Analytics Impairment

Expec-ted Loss

Calc.

Stage Allo-

cation

Con

solid

atio

n an

d ot

her d

ata

feed

s

Conclusions for a future finance architecture Functional Target Finance Architecture

19 Pre-Study IFRS 4/9

Agenda

1 IFRS 4 / IFRS 9 challenges

2 Allianz Group pre-study

3 Major gaps identified

4 Conclusions for a future finance architecture

5 Audit perspective: Compliance in the context of IFRS 4 / 9

Audit perspective: Compliance in the context of IFRS 4 / 9

Vaike Metzger, Partner, KPMG

SAP Financial Services Forum London, September 9, 2014

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

21

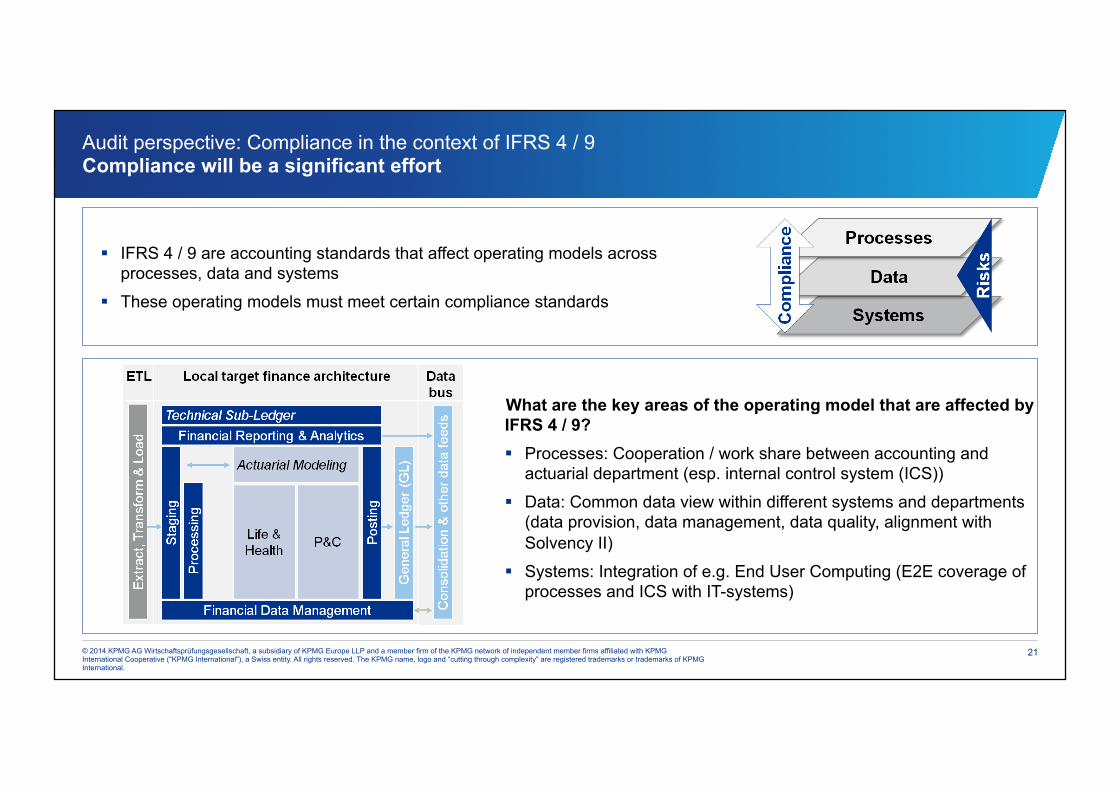

Audit perspective: Compliance in the context of IFRS 4 / 9 Compliance will be a significant effort

§ IFRS 4 / 9 are accounting standards that affect operating models across processes, data and systems

§ These operating models must meet certain compliance standards

What are the key areas of the operating model that are affected by IFRS 4 / 9? § Processes: Cooperation / work share between accounting and

actuarial department (esp. internal control system (ICS))

§ Data: Common data view within different systems and departments (data provision, data management, data quality, alignment with Solvency II)

§ Systems: Integration of e.g. End User Computing (E2E coverage of processes and ICS with IT-systems)

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

22

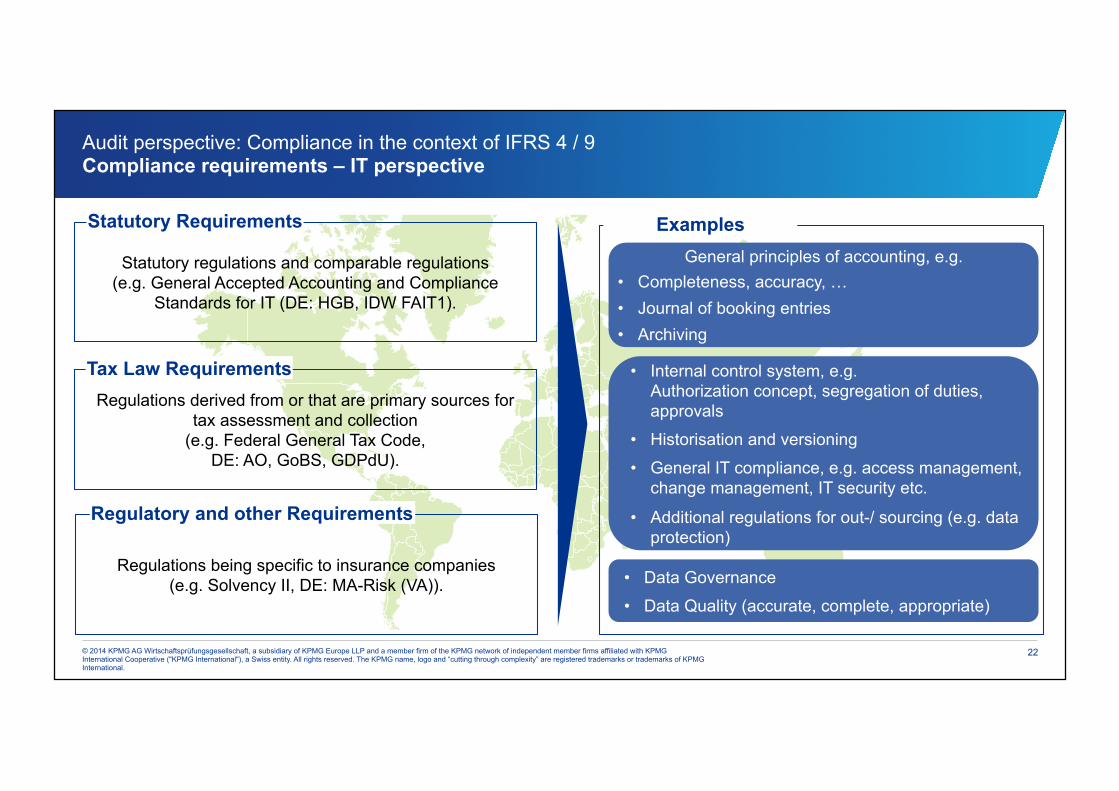

Audit perspective: Compliance in the context of IFRS 4 / 9 Compliance requirements – IT perspective

Statutory regulations and comparable regulations (e.g. General Accepted Accounting and Compliance

Standards for IT (DE: HGB, IDW FAIT1).

Statutory Requirements

Regulations being specific to insurance companies (e.g. Solvency II, DE: MA-Risk (VA)).

Regulatory and other Requirements

Regulations derived from or that are primary sources for tax assessment and collection

(e.g. Federal General Tax Code, DE: AO, GoBS, GDPdU).

Tax Law Requirements

Examples General principles of accounting, e.g.

• Completeness, accuracy, … • Journal of booking entries • Archiving

• Internal control system, e.g. Authorization concept, segregation of duties, approvals

• Historisation and versioning

• General IT compliance, e.g. access management, change management, IT security etc.

• Additional regulations for out-/ sourcing (e.g. data protection)

• Data Governance

• Data Quality (accurate, complete, appropriate)

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

23

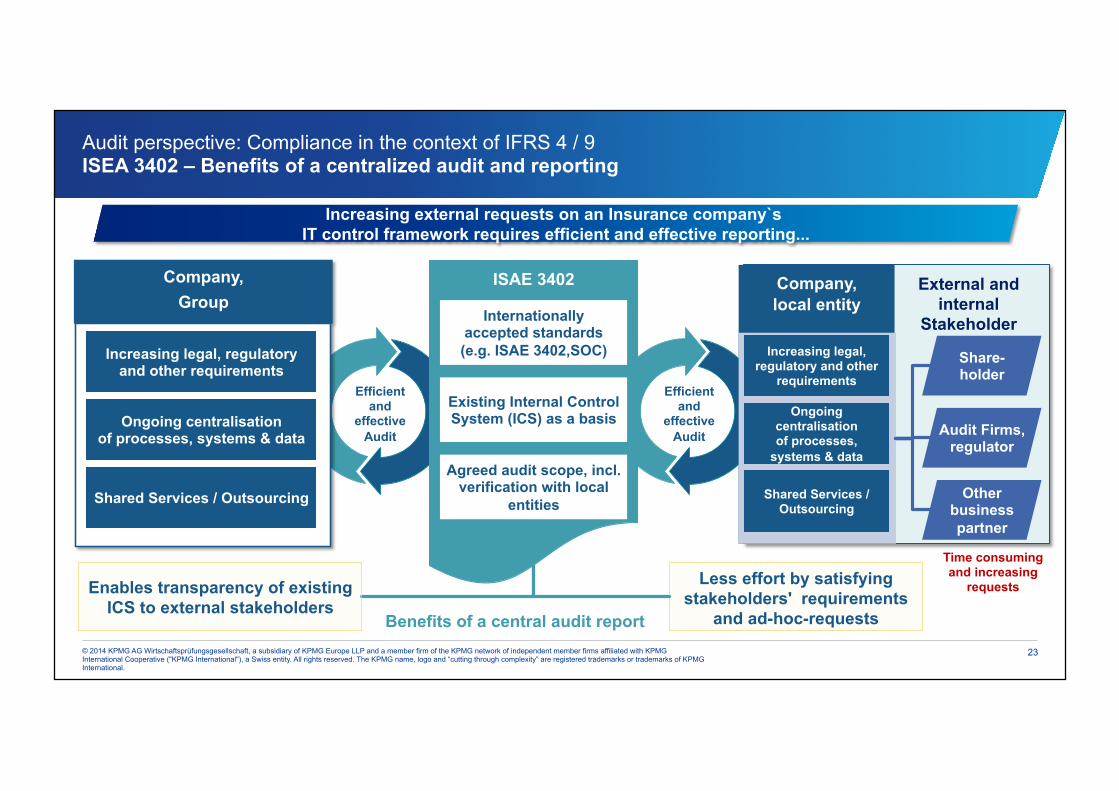

Audit perspective: Compliance in the context of IFRS 4 / 9 ISEA 3402 – Benefits of a centralized audit and reporting

Efficient and

effective Audit

Efficient and

effective Audit

Time consuming and increasing

requests Less effort by satisfying stakeholders' requirements

and ad-hoc-requests

External and internal

Stakeholder

Share-holder

Audit Firms, regulator

Other business partner

Company, local entity

ISAE 3402

Internationally accepted standards (e.g. ISAE 3402,SOC)

Existing Internal Control System (ICS) as a basis

Agreed audit scope, incl. verification with local

entities

Company, Group

Ongoing centralisation of processes, systems & data

Increasing legal, regulatory and other requirements

Shared Services / Outsourcing

Ongoing centralisation of processes,

systems & data

Increasing legal, regulatory and other

requirements

Shared Services / Outsourcing

Enables transparency of existing ICS to external stakeholders

Benefits of a central audit report

Increasing external requests on an Insurance company`s IT control framework requires efficient and effective reporting...

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

24

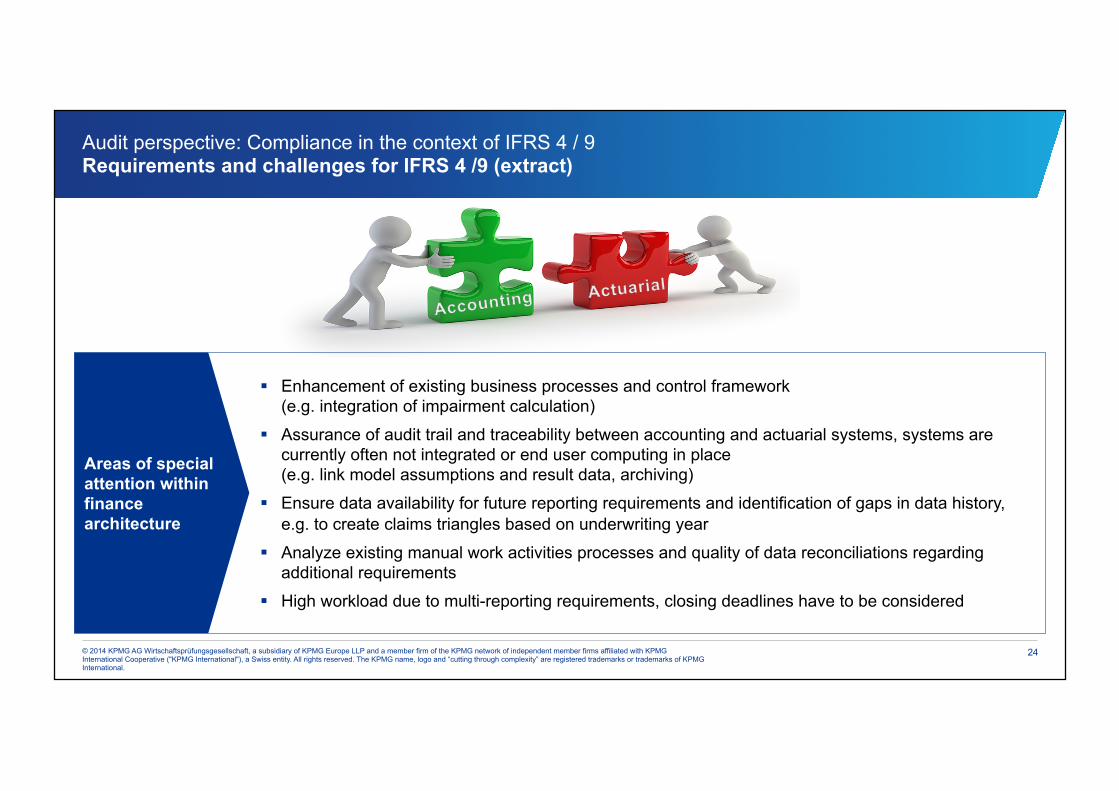

Audit perspective: Compliance in the context of IFRS 4 / 9 Requirements and challenges for IFRS 4 /9 (extract)

§ Enhancement of existing business processes and control framework (e.g. integration of impairment calculation)

§ Assurance of audit trail and traceability between accounting and actuarial systems, systems are currently often not integrated or end user computing in place (e.g. link model assumptions and result data, archiving)

§ Ensure data availability for future reporting requirements and identification of gaps in data history, e.g. to create claims triangles based on underwriting year

§ Analyze existing manual work activities processes and quality of data reconciliations regarding additional requirements

§ High workload due to multi-reporting requirements, closing deadlines have to be considered

Areas of special attention within finance architecture

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

25

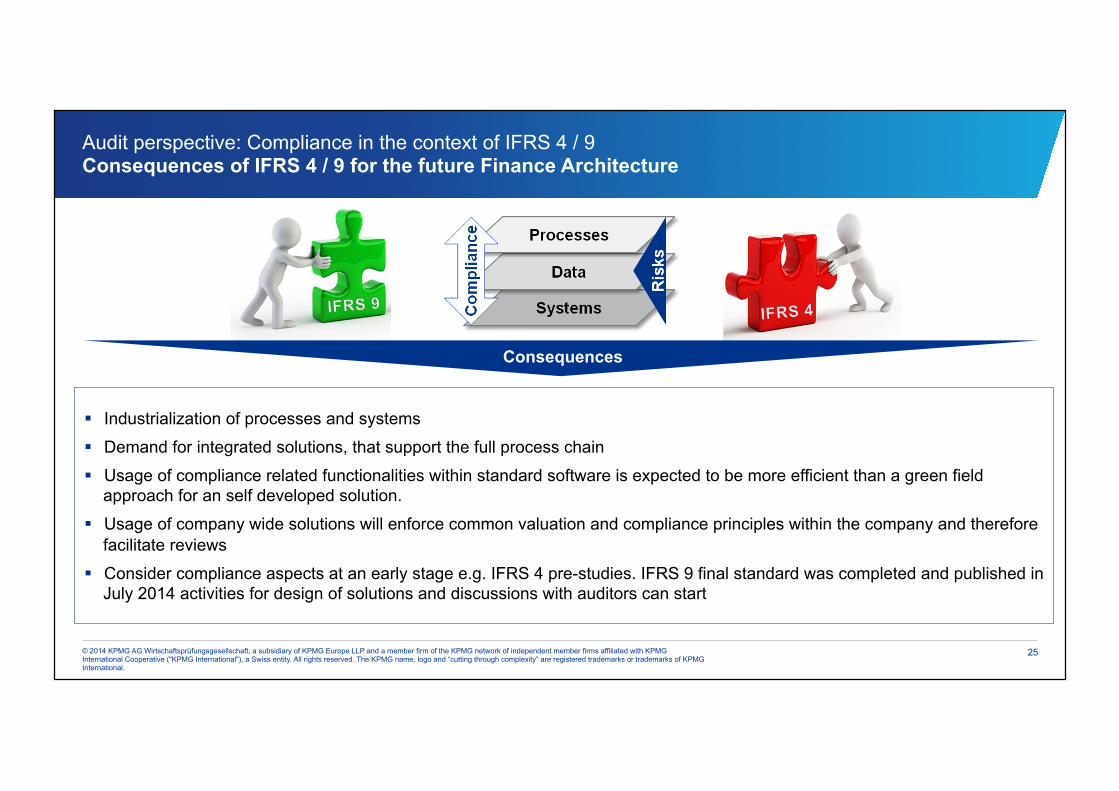

Audit perspective: Compliance in the context of IFRS 4 / 9 Consequences of IFRS 4 / 9 for the future Finance Architecture

§ Industrialization of processes and systems

§ Demand for integrated solutions, that support the full process chain

§ Usage of compliance related functionalities within standard software is expected to be more efficient than a green field approach for an self developed solution.

§ Usage of company wide solutions will enforce common valuation and compliance principles within the company and therefore facilitate reviews

§ Consider compliance aspects at an early stage e.g. IFRS 4 pre-studies. IFRS 9 final standard was completed and published in July 2014 activities for design of solutions and discussions with auditors can start

Consequences

Thanks!

© 2014 KPMG AG Wirtschaftsprüfungsgesellschaft, a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (KPMG International), a Swiss entity. All rights reserved. The KPMG name, logo and ‘cutting through complexity’ are registered trademarks or trademarks of KPMG International Cooperative (KPMG International).

KPMG and Allianz Group have a process in place to comply with the pre-approval provisions of the US Securities and Exchange Commission (SEC) and the Public Company Accounting Oversight Board (PCAOB). The Allianz Group Audit Committee has established pre-approval policies and procedures, and has pre-approved audit and non-audit services of KPMG in a detailed Positive List. The other non-audit service described in this engagement letter is contained within the scope of the service category 4.1.2 (SIN) "Advisory Actuarial" on the Audit Committee Positive List.