ifrs for small and medium-sized entities perceptions and expectations of nexia-accountants across...

TRANSCRIPT

IFRS for small and medium-sized entitiesperceptions and expectations of Nexia-accountants across Europe

Eric Hutten, KroeseWevers, The Netherlands

14 October 2009

IASB publishes IFRS for SMEs

On 9 July 2009, the International Accounting Standards Board (IASB) has issued International Financial Reporting Standard (IFRS).

Aimed specifically at meeting the needs of (and to be used only by) unlisted entities (the IFRS for SMEs).

The IASB has made international reporting standards accessible for a whole range of companies.

Main changes in final standard

Significant number of changes to the proposals originally contained in the Exposure Draft.

Perhaps the most significant change is that the Final standard IFRS for SMEs is now a stand-alone standard, with no fall back to full IFRS.

Nexia survey

In May 2009 Nexia carried out a European survey Perceptions and expectations of Nexia accountants Nexia network in Europe E-mail with invitation for web-based questionnaire

Main findings of the survey

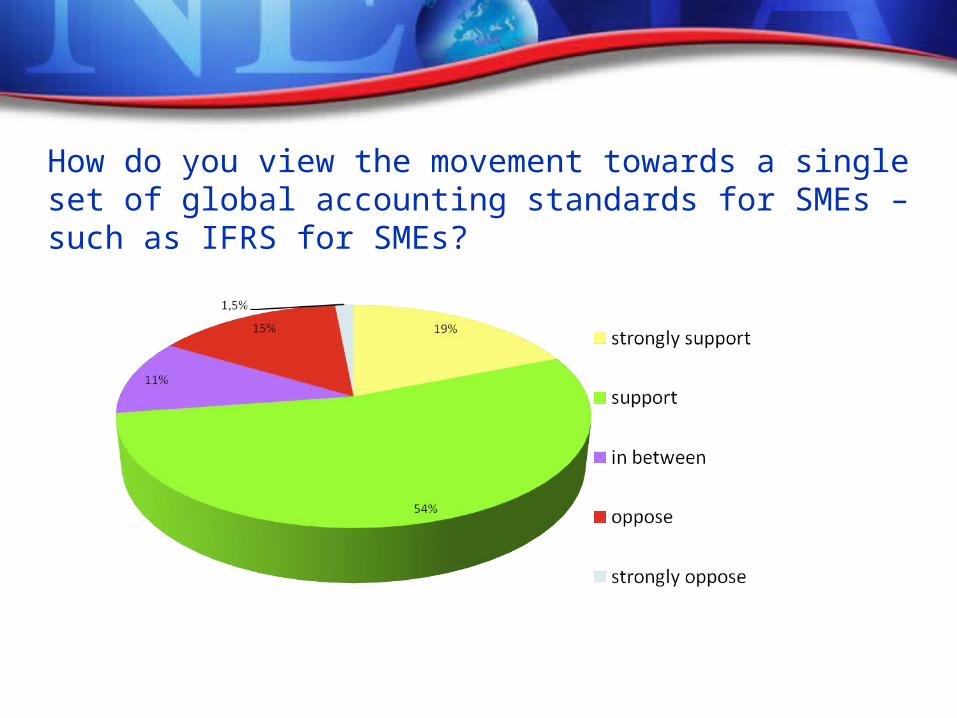

A majority of Nexia accountants in Europe are very much in favour of adoption of a common set of accounting standards throughout Europe

How do you view the movement towards a single set of global accounting standards for SMEs – such as IFRS for SMEs?

Are you aware of IASBs project on “IFRS for SME” (also known as “IFRS for Private Entities” or “IFRS for NPAE”)?

Main findings of the survey

Many Nexia accountants think the entities in their country will have no plans to adopt IFRS for SME until it is mandated

When IFRS for SMEs is finalized, which best describes the direction you think entities in your country will take?

38% Most entities will have no plans to adopt, until IFRS is mandated by the national accounting standard setting body;

23% Most entities will assess the cost/benefits of adoption; 16% Most entities will consider adoption in the near-term; 19% Most entities have no interest in adoption; 4% Don’t know / not applicable.

What aspects of a new global accounting standard (like IFRS for SMEs) do you find most attractive?

43% Simplified, self-contained set of accounting standards that are appropriate for private entities;

15% Reduced financial reporting burden; 35% Enables investors, lenders, and other users to compare financial

performance among SMEs; 6% I don’t find anything particularly attractive; 1% Other.

Main findings of the survey

Nexia accountants expect that a global set of SME accounting standards will not be applicable for the smallest entities

Do you think a global set of accounting Standards, like IFRS for SMEs, can be of use for SMEs in your country?

Strongly NeutralStrongly

agree disagree

Micro 11% 12% 15% 31% 31%

Small 16% 17% 26% 27% 14%

Medium 17% 46% 30% 5% 2% Large 34% 44% 10% 9% 3%

The obligatory reporting standards of entities should be restricted to?

Micro Small Medium Large Listed Tax Law 35% 11% 1% 1% 0%

Local GAAP 42% 53% 30% 11% 4%

IFRS for SME 11% 24% 62% 49% 5%

Full IFRS1% 2% 3% 36% 86%

Unrestricted 10% 10% 4% 3% 5%

Main conclusion of the survey

Public accountants in Europe support the applicability of a global accounting standard for non-listed entities across Europe,

but the size of the entities and the level of simplification and burden reduction affect the necessity of mandating it as an obligatory standard.

Outcomes of other surveys

A majority of finance professionals of European SMEs are very much in favour of adoption of a common set of accounting standards throughout Europe.

Source: Deloitte, Mazars