ifrs results conference call 8 february 2018

TRANSCRIPT

204 / 0 / 0

242 / 220 / 219

119 / 147 / 60

23 / 55 / 94

0 / 176 / 240

198 / 217 / 241

255 / 192 / 0

235 / 241 / 222

127 / 127 / 127

242 / 242 / 242

96 / 74 / 123

8 / 0 / 83

73/ 10 / 61

1/210/255

34/21/124

189/21/80

EuroChem FY 2017 IFRS Results Conference Call 8 February 2018

Start time: 10:00 NY / 15:00 London / 16:00 Zug / 18:00 Moscow Dial-in details https://cossprereg.btci.com/prereg/key.process?key=P9DF3TP9P

204 / 0 / 0

242 / 220 / 219

119 / 147 / 60

23 / 55 / 94

0 / 176 / 240

198 / 217 / 241

255 / 192 / 0

235 / 241 / 222

127 / 127 / 127

242 / 242 / 242

96 / 74 / 123

230 / 224 / 236

This presentation has been prepared by EuroChem Group AG (“EuroChem” or the “Company”) for informational purposes, and may include forward-looking statements or projections, These forward-looking statements or projections include matters that are not historical facts or statements and reflect the Company’s intentions, beliefs or current expectations concerning, among other things, the Company’s results of operations, financial condition, liquidity, performance, prospects, growth, strategies, and the industry in which the Company operates, By their nature, forward-looking statements and projections involve risks and uncertainties as they relate and depend on events and circumstances that may or may not occur in the future, The Company therefore cautions you that forward-looking statements and projections are not guarantees of future performance and that the actual results of operations, financial condition and liquidity of the Company and the development of the industry in which the Company operates may differ materially from those made in or suggested by the forward-looking statements or projections contained in this presentation, Factors that could cause the actual results to differ materially from those contained in forward-looking statements or projections in this presentation may include, among other things, general economic conditions in the markets in which the Company operates, the competitive environment in, and risks associated with operating in, such markets, market change in the fertilizer and related industries, as well as many other risks affecting the Company and its operations, In addition, even if the Company’s results of operations, financial condition and liquidity and the development of the industry in which the Company operates are consistent with the forward-looking statements or projections contained in this presentation, those results or developments may not be indicative of results or developments in future periods, The Company does not undertake any obligation to review or confirm expectations or estimates or to update any forward-looking statements or projections to reflect events that occur or circumstances that arise after the date of this presentation,

This document does not constitute or form part of any advertisement of securities, any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities of the Company in any jurisdiction, nor shall it or any part of it nor the fact of its presentation, communication or distribution form the basis of, or be relied on in connection with, any contract or investment decision, No reliance may be placed for any purpose whatsoever on the information contained in this document or on assumptions made as to its completeness, No representation or warranty, express or implied, is given by the Company, its subsidiaries or any of their respective advisers, officers, employees or agents, as to the accuracy of the information or opinions or for any loss howsoever arising, directly or indirectly, from any use of this presentation or its contents,

Due to rounding, some totals may not correspond with the sum of the separate figures

Participant Joining Details

UK Freefone 0800 389 7473

UK Direct 01296 480 104

2

https://cossprereg.btci.com/prereg/key.process?key=P9DF3TP9P

EuroChem Group Overview

10 Novomoskovskiy Azot

7 Lifosa 11 BMU

8 Phosphorit Nevinnomysskiy Azot 12

Antwerpen 6

Fertilizer production

1 Global headquarters (Zug)

2 Kovdorskiy GOK

5 EuroChem Fertilizers

Raw material mining

17 Tuapse

16 Murmansk

14 Sillamae

15 Ust-Luga (UC)

Logistics

1

2

5 3

4

10 8

11 6

17

16

15

25

20

26

24

28

18

36

35

23

32

12

7

14

13

13 EuroChem-Migao

19 US

20 Brazil

22 Spain

30 Moldova

31 Belarus

29 Bulgaria

18 Mexico

28 Greece

24 Germany

26 Italy

25 Switzerland

Hungary 27

Sales

3 VolgaKaliy (UC)

4 Usolskiy (UC)

9 Northwest (UC)

19

9

UC = under construction

Vertically integrated global business supporting regional market commitment

23 France

32 Ukraine

Serbia

33 Turkey

34 Russia

35 Singapore

36 China

27 29

30

31

33

34

Romania

Expected 1H 18

21 Argentina

21

22

Own raw materials, production facilities, and logistics assets create unique global offering.

Sales to more than 100 countries supported by EuroChem sales platform

Access to international customers through EuroChem Agro and trade companies

Growing global distribution platform with series of acquisitions over the last 24 months:

• Bentrei (US)

• Tocantins (Brazil)

• Agricola (Bulgaria)

• Hispalense de Liquidos (Spain)

• Emerger Fertilizantes (Argentina)

• New offices/centres in Hungary, Moldova, Russia

Months away from start of commissioning operations of 2 potash projects in Russia (8.3 MMT of KCl per year)

Increasing product offering with innovative solutions

2017 total fertilizer production up 2% y-o-y of 10.6 MMT (2016: 10.4 MMT)

Vertical integration: own raw materials, port terminals, rail stock,

construction/repair works, Europe/CIS/Americas distribution capacity

o 3 Nitrogen plants (2 in Russia, 1 in Belgium) – nutrient capacity of

2.6 MMT of N, increasing to 3.4 in 2018 with launch of new NH3

plant.

o 3 Phosphate plants (2 in Russia and 1 in Lithuania) – nutrient

capacity of 1.27 MMT of P2O5 (phosphoric acid)

o Apatite (Russia) - P2O5-rich (37%-38%) and low-MER(1) content

(0.057) apatite ore (2.8 MMT per year) covers c.75% of own

production needs for all phosphate plants and Antwerp, additional

volumes from Kazakhstan: 600 KMT phosphate flour

o Iron ore as a co-product of apatite mining: up to 5.8 MMT of iron ore

(Fe content 63.5%)

o Logistics assets include transshipment capacity of c.10.2 MMT, of

which c.3.5 MMT in the EU, ~ 6,400 own rail stock/depot

o Sales : global platform anchored on EuroChem Agro and CIS position

with expanding footprint across the Americas

Projects

o Potash (K) : 2 greenfield projects in Russia with targeted capacity of

over 8.3 MMT of KCl per year (5 MMT K2O). First product Q1 2018

o Ammonia – 1 MMT facility in close proximity to Phosphorit

(Russia/Baltic Sea), startup 2018

• Total employees: >25,000

3

(1) Minor element ratio

EuroChem Group Overview

Target raw material self-sufficiency (ammonia, phosphate rock, potash)

Enhance cash cost position and reduce risk/volatility of earnings

Cost leadership through vertical integration

Build leading low-cost potash production

Maximize internal processing of potash for NPK, NK, SOP production

Growth through potash

The proximity to customers in key home markets provided via distribution allows the Group to sell at a premium and exploit seasonality patterns

Obtain valuable market knowledge from direct end-user contact with regards to product quality, R&D, and services

Proximity to Customers

Maximize specialty products and

emphasize the de-

commoditization of the Group’s

fertilizer product portfolio

Expand industrial portfolio

Premium product R&D

Value-added product range

Vertically integrated business model

Ongoing and potential investment projects By-products

Phosphate Potash

3 Nitrogen fertilizer

plants

c.12.9MMT of nitrogen

capacity(3)(4)

3 Phosphates fertilizer

plants

c.4.0 MMT of phosphates capacity(2)(4)

2 potash projects underway in Russia

with a combined targeted capacity

of over 8MMT MOP

Phosphoric acid

Phosphate rock

Nitrogen

Iron ore

Ammonia (NH3)

1mmt pa project

Maritime transhipment facilities in Russia, Estonia, Belgium and c.6k rail cars and 43 locomotives

Sales to more than 100 countries supported by own distribution

Natural gas (access to several

deposits in proximity to Group assets)

Potash ore reserves & resources in excess

of 10 BMT(1)

Ust-Luga

Source: Company data; (1) MI&I resources in accordance with Russian classification system; (2) Phosphate and complex mineral fertilizers; (3) Nitrogen mineral fertilizers and organic synthesis products; (4) The capacity data represents theoretical capacity as certain production units can produce several types of products, for example, certain production units can be configured to produce either DAP or MAP – but not both at the same time. Final production volumes ultimately depend on how the production units are configured

Key strategy pillars

4

Fertilizer Sector Market backdrop

Averages are derived from weekly prices

Nitrogen (US$/tonne)

Phosphates (US$/tonne)

Iron ore (US$/tonne)

Average market prices for key products (US$/tonne)

Key themes: • India / Brazil subsidy

and currency • MEA capacity • Producer discipline

Key themes: • Chinese costs /

exports / capacity rationalization

• New capacity • Indian subsidies • Acreage plans

Key themes: • China steel demand • Global supply

dynamics • CNY movements

2017 Backdrop

Q4-17 Q4-16 Y-o-Y,

chng % 2017 2016

Y-o-Y, chng %

Ammonia

(FOB Yuzhny) $283 $190 +49% $265 $236 +12%

Prilled urea

(FOB Yuzhny) $246 $206 +19% $220 $198 +11%

AN

(FOB Black Sea) $216 $179 +21% $191 $165 +15%

MAP

(FOB Baltic) $360 $320 +13% $348 $338 +3%

MOP

(FOB Baltic, spot) $235 $221 +7% $228 $235 -3%

Iron ore

(63.5% Fe, CFR China) $67 $72 -7% $73 $60 +22%

• More supportive fertilizer pricing backdrop following launch of new

capacity

• Chinese fertilizer production rates decline on rising input costs and

stricter environmental controls – exports significantly lower

year-on-year.

o Urea exports down 47% y-o-y to 4.7 MMT, (2015: 13.7 MMT)

o DAP exports 6% lower y-o-y to 6.4 MMT , (2015: 8 MMT)

o Structural changes in Chinese cash costs (higher domestic

tariffs/prices for electricity, rail/truck transportation, coal)

• Global nutrient demand

• N: slight increase to 106.5 MMT of N

• P: stable at 48.2 MMT P2O5

• K: up 2% to 35.4 MMT K2O

$ 0

$ 100

$ 200

$ 300

$ 400

$ 500

Prilled urea (FOB Yuzhniy) Ammonia (FOB Yuzhniy)

AN (FOB Black Sea) UAN (FOB Black Sea)

$ 200

$ 250

$ 300

$ 350

$ 400

$ 450

$ 500

MAP (FOB Baltic) DAP (FOB Baltic) NPK 16:16:16 (FOB Baltic)

$ 0

$ 40

$ 80

$ 120

Iron ore (CFR China)

5

EuroChem Group Overview

20

16

2

01

7

Completed tender on 2017 LPNs ($426m) and placed $500m Eurobonds issue

Brazil Distribution Acquisition of Fertilizantes Tocantins with blending facilities and established network of 2,000 customers in the North, Northeast and Mid-West of Brazil.

Strategically located in Brazil’s emerging fertile farming regions in the North, Northeast and Mid-West. Blending facilities, market expertise and established network of 2,000 customers. Double digit sales growth for 7 consecutive years.

Distribution Centre in Hungary New center to mainly distribute EuroChem products and specialty fertilizers from Fertilia Ltd., a leading Hungarian producer and distributor.

First Ural-20 mining machine starts at Usolskiy

Selected key events

Acquisition of a minority interest (50%-1 share) in Hispalense de Liquidos

EuroChem sells Severneft-Urengoy

EuroChem Group AG obtains Unsecured $750 Million Facility

EuroChem acquires Argentinian Fertilizer Distributor Emerger Fertilizantes

The acquisition of the privately-owned distributor of premium and standard fertilizers in Argentina will further strengthen EuroChem’s footprint in Latin America which is an important region currently accounting for 11% of the Group’s fertilizer sales. The market for fertilizers in Argentina is expected to increase by 40% to 5.5 MMT in 2020.

In November 2017 the Group divested its Severneft-Urengoy gas operator – future oil & gas focus to center on the exploration and development of gas condensate fields in the Astrakhan and Saratov regions in Russia, and the Kamenkovsky gas field in Kazakhstan.

EuroChem launches new subsidiary in Bulgaria

EuroChem Places US$ 500m Eurobond

Acquisition of a minority interest (50%-1 share) in Hispalense de Liquidos, a family-owned producer of liquid NPK blends located in the south of Spain. The deal gives EuroChem access to additional production capability and technical know-how, enabling the Group to expand the scope of its premium product offering.

EuroChem Usolskiy Potash readies for commissioning of MOP production mill

20

18

Usolskiy beneficiation system filled with ore and brine as of early February. Initial production to begin in the second half of February/early March, with regular production and sustained ramping-up of operations to follow from early May.

6

EuroChem Group Overview

20,534 20,909

2016 2017

Group

• Diversified presence in non-domestic markets

• Top 2 in Russia/CIS with more than 55% of Russian domestic sales directly to farmers

• Top 2 in Europe, anchored by Europe EuroChem Antwerpen / Agro

• Growing presence in the Americas and Europe supported by several acquisitions

Group sales volumes (KMT)

From 2018, added focus on Brazilian market with world’s lowest cost potash

• Entering transformational stage with potash

• Mining products split between Russia and Asia

Group sales geography (2017)

Global market presence

+2%

32%

20% 17%

12% 10%

7%

2%

• Growing industrial product offering

1 663

2016 2017

Latin America

2602 +56%

5 516 5 181

2016 2017

Europe

-6%

2 396 2 125

2016 2017

North America

-11%

319

2016 2017

Africa

498 +56%

5638 5460

2016 2017

Russia

-3%

1389 1300

2016 2017

CIS

-6%

3872 3659

2016 2017

Asia

-6%

7

EuroChem Group Overview

Geography of sales (% of total)

Revenues (US$bn), Gross margin (%) EBITDA (US$m), EBITDA margin (%)

Key ratios (LTM)

(1) Defined as per bank covenants.

Key 2017 figures

12M-16 3M-17 6M-17 9M-17 12M-17

Net debt1 / EBITDA 2.85x 2.82x 2.87x 2.90x 2.88x

Funds from operations / Gross debt1 20% 18% 18% 17% 18%

EBITDA / interest coverage 5.36x 5.00x 4.80x 4.46x 4.43x

Return on capital employed 17% 16% 16% 16% 17%

$402

$210 $234 $286 $349 $241 $254 $286

$1,133 $1,130

32%

21% 22%

27% 26%

23% 22% 22%

26%

23%

EBITDA ($m) EBITDA margin (%)

$1,255 $1,013 $1,054 $1,053

$1,336 $1,061 $1,172 $1,296

$4,375

$4,866

41%

34% 35% 36%

40%

35% 35% 37% 37% 37%

Q1-16 Q2-16 Q3-16 Q4-16 Q1-17 Q2-17 Q3-17 Q4-17 2016 2017

Revenues ($m) Gross margin (%)

44% 31% 34% 35% 35%

25% 33% 32% 36% 32%

16%

18% 20% 21% 19%

24% 19% 17%

18% 20%

6% 15% 12% 8% 10%

9% 12%

9% 10%

10%

20% 18% 11% 10%

14% 15% 8%

11%

15% 12%

4% 11% 13% 15%

12% 15% 16% 22%

11% 17%

7% 5% 10% 10% 6% 8% 8% 7% 8% 7% 2% 1% 1% 2% 3% 3% 3% 1% 1% 2%

Europe Russia Asia Pacific North America Latin America CIS Africa

8

EuroChem Group Overview

$1,133 $1,130

+170

+34

-18

-21

-30

-66 -5

-67

EBITDA12M-16

Salesvolumes and

mix(EuroChem)

Prices (incl.FX)

Other sales(incl. 3rd

partyproducts)

Variableproduction

costs

Fixed costs(excl. effectsof FX rates)

Effects of FXrates on

fixed costs

FX gain/lossfrom

operations

EBITDA12M-17

Other

items

net*

Rouble appreciation overshadowing stronger product pricing environment

EBITDA development

Product 2017 2016 Y-o-Y,

chng %

Ammonia

(FOB Yuzhny) $265 $236 +12%

Prilled urea

(FOB Yuzhny) $220 $198 +11%

AN

(FOB Black Sea) $191 $165 +15%

MAP

(FOB Baltic) $348 $338 +3%

Iron ore

(CFR China) $73 $60 +22%

• EBITDA remained in line y-o-y at $1,130m

• Despite higher prices, profitability adversely affected by impact of rouble appreciation and one off items.

Selected sales volumes (KMT)

2017 2016 Y-o-Y,

chng % 2017 2016

Y-o-Y, chng %

Fertilizer products 13,470 13,415 +0% 9,678 10,022 -3%

Feed phosphates 348 300 +16% 336 289 +16%

Mining products 5,927 6,029 -2% 5,916 6,022 -2%

Industrial products 1,512 1,494 +1% 1,512 1,494 +1%

EuroChem products only

EBITDA, $m

40

45

50

55

60

65

70

75

80

85

90

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18

RUB/USD Exchange rate

* Other items (net) mainly comprised of bad debt provisions of $14.3m, VolgaKaliy write-off of $5.7m, iron ore swap losses of $3.9m, and Murmansk Port disposal effect of $23m.

9

EuroChem Group Overview

249

858

344

1 136

745

410

Cash and equiv. 2018 2019 2020 2021 2022

Unsecured syndicated facility Eurobonds Rouble bonds Bilateral loans

2.34x

2.75x 2.85x 2.82x 2.87x 2.90x 2.88x

Q2-16 Q3-16 Q4-16 Q1-17 Q2-17 Q3-17 Q4-17

Covenant debt(1) maturity profile as of 31 December 2017, $m

Debt(1) mix as of 31 December 2017

Net covenant debt(1)/ EBITDA dynamics (x)

(1)Defined as per bank covenants (does not include project finance facilities)

3.5x

Bank debt covenant level

Highlights / recent developments

$100m

• Commitment to conservative financial policy:

• To keep Net debt/LTM EBITDA within a conservative range throughout the various stages in the fertilizer cycle

• Ample liquidity proportionate to short-term debt

• Debt structure with a balanced maturity and interest rate profile

• EuroChem’s LT ratings (Fitch/S&P): «BB» (negative) / «BB-» (stable) recently affirmed

• Very modest refinancing needs in 2018-2019; in 2020 new EBITDA from new projects should exceed $300m

• Sizeable and committed shareholder support:

• Agreement with AIM Capital SE for perpetual debt financing with a limit of up to $1.5bn ($250mm drawn as of now)

• 2 significant investment projects financed through non-recourse project financing facilities (Northwest and Usolskiy)

Covenant debt: $3.48n

78% 22% Covenant/Off-covenant

Project finance repayment ($m) 2019 2020 2021 2022 and beyond

Total

Usolskiy Project Finance 150 200 200 200 750

Northwest (Baltic ammonia) 40 71 73 483 666

46.0%

75%

99%

64%

34%

33%

25%

1%

36%

66%

1%

21% Bond/bilateral loans/syndicated

facility

Long-term/short-term

Unsecured/secured

$/RUB/BRL

Float/Fixed

As of 31 Jan-2017: • c.$203m undrawn committed lines • c.$356m cash

Undrawn committed lines

+$296m

10

History of prudent financial policy backed by shareholder commitment

EuroChem Group Overview Strategic projects largely funded

Group CAPEX (US$m)

$286m

$270m

CAPEX spent todate

Remaining CAPEX Total estimatedCAPEX

$680m

c.$297m c.$977m

Amount of total investment funded to date c. 68%

$750m

CAPEX spent to date CAPEX outstanding2018 - 2026

Totalestimated CAPEX²

$1,809m

c. $3,000m

Amount of total investment funded to date: c. 60%

c. $1,191m

EuroChem-Northwest ammonia project

Usolskiy potash project

Project Finance (US$m)

Excluding temporarily unallocated CAPEX 2- including all development phases and all social infrastructure

PF Usolskiy

PF Northwest

74

110 156 186 216 211 208 194 182

355

610

312

160

257

91

177 185 140 102 100

211 221

519

378

224

341

395 380

274 326

443 458

1,323

1,496

Q1-16 Q2-16 Q3-16 Q4-16 Q1-17 Q2-17 Q3-17 Q4-17 2016 2017

Mining PF Usolskiy PF Northwest Fertilisers Oil&Gas Logistics Sales OtherP

roje

ct f

inan

ce

$4

17

m

• Despite large-scale projects the Group maintains the flexible CAPEX outlay

• 29% of 2017 CAPEX from non-recourse project financing

• $160m: EuroChem Usolskiy (potash) • €221m : EuroChem Northwest (ammonia)

• Annual Group sustaining CAPEX requirements: c.$150m

11

EuroChem Group Overview

$378

$0

$100

$200

$300

$400

$500

Jan

-16

Feb

-16

Mar

-16

Ap

r-16

May

-16

Jun

-16

Jul-

16

Au

g-16

Sep

-16

Oct

-16

No

v-16

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-17

May

-17

Jun

-17

Jul-

17

Au

g-17

Sep

-17

Oct

-17

No

v-17

Dec

-17

PhosRock Apatite AmmoniaSulphur Sulphuric acid Conversion cost

Lifosa DAP costs (FOB Baltic), US$/tonne, with iron ore credit

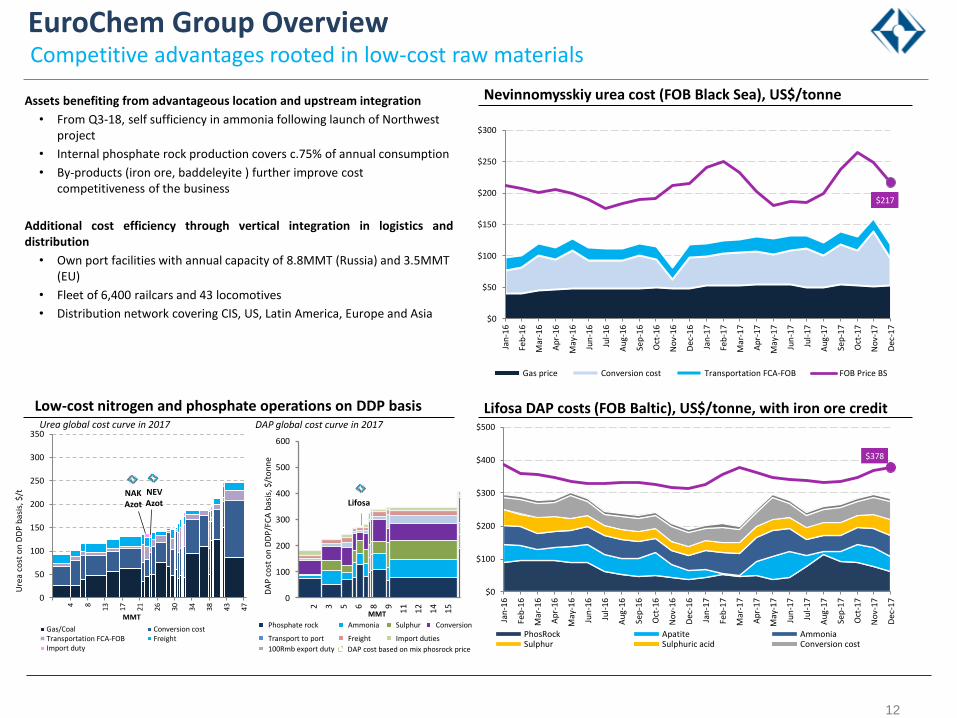

Assets benefiting from advantageous location and upstream integration

• From Q3-18, self sufficiency in ammonia following launch of Northwest project

• Internal phosphate rock production covers c.75% of annual consumption

• By-products (iron ore, baddeleyite ) further improve cost competitiveness of the business

Additional cost efficiency through vertical integration in logistics and distribution

• Own port facilities with annual capacity of 8.8MMT (Russia) and 3.5MMT (EU)

• Fleet of 6,400 railcars and 43 locomotives

• Distribution network covering CIS, US, Latin America, Europe and Asia

Nevinnomysskiy urea cost (FOB Black Sea), US$/tonne

Low-cost nitrogen and phosphate operations on DDP basis

Phosphate rock Ammonia Sulphur Conversion

Transport to port

DAP cost based on mix phosrock price

Freight Import duties

100Rmb export duty

DAP global cost curve in 2017 Urea global cost curve in 2016

$217

$0

$50

$100

$150

$200

$250

$300

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Dec

-17

Gas price Conversion cost Transportation FCA-FOB FOB Price BS

0

50

100

150

200

250

300

350

4 8

13 17 21 26 30 34 38 43 47

Ure

a co

st o

n D

DP

bas

is, $

/t

MMT

Gas/Coal Conversion costTransportation FCA-FOB FreightImport duty

NAK Azot

NEV Azot

Urea global cost curve in 2017

0

100

200

300

400

500

600

2 3 5 6 8 9

11

12

14

15

DA

P c

ost

on

DD

P/F

CA

bas

is, $

/to

nn

e

MMT

Fe

Lifosa

12

Competitive advantages rooted in low-cost raw materials

Potash projects

Potash

14

126

184

145

310

c.440

NevinnomysskiyAzot

EuroChemAntwerpen

Trading of3rd-party product

MOP SOP

Production to initially phase out current 3rd party purchases for processing

- 580

2,100

3,500

4,600

6,000

7,100

8,300

2017 2018 2019 2020 2021 2022 2023 2024/25

Usolskiy VolgaKaliy

Potash sourcing, 2017 (KMT)

Expected capacity ramp-up (KMT)

• Usolskiy initial start-up sequence delayed to mid-Q1 2018, VolgaKaliy online from summer 2018.

• Base case ramp-up assumes 3 years for each development phase to reach full capacity

• Long-term target to channel over 1 million tonnes of potash for downstream complex fertilizer production

• Balanced approach - the Group will seek to maximize shareholder returns, while remaining mindful of market dynamics as capacity is commissioned and operationally tested

Potential for higher internal consumption from complex fertilizer production in Kazakhstan and China

Gradual introduction of potash

Key considerations

2017/18 capacity and production estimates impacted by delayed start at Usolskiy.

Limited revision to ramp-up plan beyond that.

Potash

15

Expected average price range 2018-2022

Ch

ina

AP

C

ICL

(EU

)

Ura

lkal

i

Bel

aru

skal

i Pota

shC

orp

Agr

ium

ICL

(DSW

)

0

50

100

150

200

250

300

350

0 5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

Po

tash

co

st o

n D

DP

bas

is, $

/t

Global potash capacity, MMT

Potash global cost curve (delivered to market, 2022)

Site Cost Delivery to port Freight Capacity additions

Mo

saic

K+S

Oth

ers

Po

tash

Co

rp

Vo

lgaK

aliy

Uso

lski

y

SQM

Intr

epid

K+S

Leg

acy

Ura

lkal

i

Bel

aru

skal

i

64 MMT estimated 2017 KCl demand*

69 MMT : estimated 2022 KCl demand

Favorable positioning

Oil and gas

Mining

Fertilizers

Logistics

Distribution

Global HQs

CIS HQs

Sales market in 2017

Potash assets conveniently located for intragroup logistics… …and beyond within global EuroChem sales network…

…supporting expected global cost leadership position

*Interger: 62.4 MMT, IFA: 66.5 MMT

VolgaKaliy Update

2.3 2.3

2.3 2.3

4.6

Phase 1 Phase 2

Capacity (KCL, MMT)

• Average KCl content of 39.5% and modern mining operations • Approximately 500km to EuroChem’s Tuapse port facilities

16

Usolskiy Update

Eight continuous mining machines operating underground

2.3 2.3

1.4 2.3

3.7

Phase 1 Phase 2

Capacity (KCL, MMT)

17

Usolskiy Update

Ore in storage prior to beneficiation

18

Thank you – and now time for our Q&A session….

Please visit www.eurochemgroup.com for further details or contact our Investor Relations. [email protected]