ifrs roadshows 2012 - …doc.housing.org.uk.s3.amazonaws.com/presentations... · ifrs roadshows...

TRANSCRIPT

IFRS Roadshows 2012

BREAKOUT A and C:

Accounting for multi-employer

pension fund deficits

&

Accounting for financial instruments

Speaker: Jonathan Pryor

Partner Smith and Williamson

Chair: Sarah Smith

Executive Director, Finance and Resources AmicusHorizon

FRS102: pensions and financial instruments

Presentation by Jonathan Pryor

Partner, Smith & Williamson

IFRS Roadshows 2012

IFRS Roadshows 2012

1. Pensions accounting

2. Main accounting changes on financial instruments

3. Hedge accounting

4. Potential changes from IFRS 9

5. Challenges

1. Pensions accounting: Summary of

changes

• DC schemes: no change

• DB schemes: similar principles but

– interest calculated using discount rate on net balance whereas FRS 17 requires “interest” on assets to be calculated using investment return and liabilities using discount rate

1. Pensions accounting: Summary of

changes: Interest calculation

E.g.

Amount Return/discount

Scheme information

Assets £10m 8%

Liabilities £20m 4%

Interest calculation

FRS 17 Net liability £10m

Interest charge £nil

FRED48 Net liability £10m

Interest charge £400k

1. Pensions accounting

Multi-employer schemes

• E.g. SHPS

• FRED48 (amendment) requires the liability to be recognised for a contractual agreement to fund the deficit

– if due in more than one year then discount

– if less than one year recognise in full

– prior year adjustment in 1st year of adoption: Impact on reserves not I&E

– when amounts are revised there will be an I&E impact for the full increase

1. Pensions accounting: Multi

employer schemes (continued)

• FRS 17 exemption (currently)

• FRS 17 is no longer proposed to be amended

1. Pensions example

An Association has obligations in respect of past service to pay to SHPS various amounts over a number of years. The NPV of these payments at 1 April 2014 is £1m, using a discount rate of 5% (the rate applicable at that time). It is a March year end and the Association had not previously recognised this liability. Payments in 2015 and 2016 will be £120,000 and £140,000 respectively

1. Pensions example

1 April 2014: prior year adjustment

£k

Dr Reserves 1,000

Cr Creditors (1,000)

Year ended 31 March 2015

£k

Dr I&E account 50

Dr Creditors 70

Cr Cash (120)

1. Pensions example

Year ended 31 March 2016

£k

Dr I&E account 46.5

Dr Creditors 93.5

Cr Cash (140)

1. Pensions example

During the year ended 31 March 2017, SHPS announces a new funding obligation in respect of past service of an additional NPV of £400,000

1. Pensions example

In addition to a similar entry to the ones already described, we then have

So quite an impact in the year any additional contributions are agreed

£k

Dr I&E account 400

Cr Creditors (400)

2. Main accounting changes on

financial instruments

• Horribly complex and subject to change when (if!) IFRS 9 is finalised

• Requires recognition at fair value of many instruments not presently recognised at all

• Recognition is based on a different basis from current UK GAAP

• Splits instruments into either “basic” or “other”

• “Basic” is defined tightly

• “Basic” is further split depending on whether it is a financing transaction or not

2. Main accounting changes on

financial instruments

• “A financing transaction may take place in connection with the sale of goods and service, e.g. if payment is deferred beyond normal business terms or is financed at a rate of interest that is not a market rate”

2. Main accounting changes on

financial instruments

2. Main accounting changes on

financial instruments

Basic financial instruments (11.8)

a) Cash

b) A debt instrument meeting definition on next slide

c) A commitment to receive a loan …… meeting definition on next slide

d) An investment in non-convertible preference shares and non-puttable ordinary or preference shares

2. Main accounting changes on

financial instruments

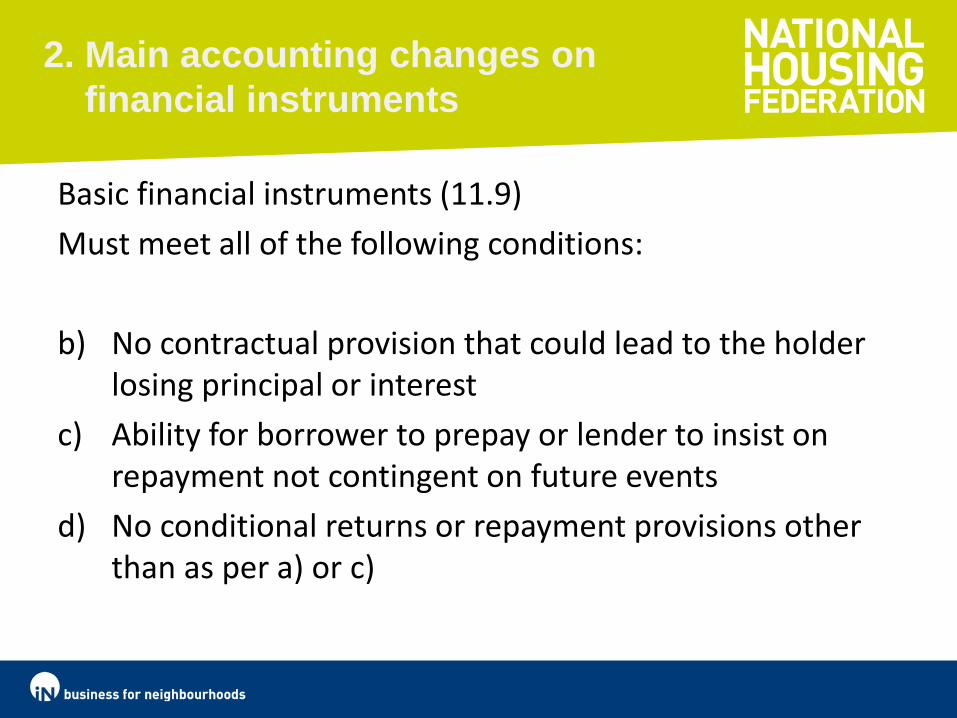

Basic financial instruments (11.9)

Must meet all of the following conditions:

a) Returns to the holder are one of the following:

i. A fixed amount

ii. At a fixed rate of return

iii. A variable rate equal to a single quoted or observable interest rate

iv. A combination of the above (provided all positive)

2. Main accounting changes on

financial instruments

Basic financial instruments (11.9)

Must meet all of the following conditions:

b) No contractual provision that could lead to the holder losing principal or interest

c) Ability for borrower to prepay or lender to insist on repayment not contingent on future events

d) No conditional returns or repayment provisions other than as per a) or c)

2. Examples of basic financial

instruments

• Trade debtors

• Loans from subsidiaries repayable on demand

• Debt instrument that would be repayable if there was a covenant breach

2. Examples of financial instruments

that are not basic

• An interest rate swap that returns a cash flow that is positive or negative

• An option

2. Main accounting changes on

financial instruments

Basic

• If not a financing transaction, then initially recognise at transaction price

• If a financing transaction, then recognise at present value of the future payments discounted at a market rate of interest for a similar instrument

2. Financial instruments

Eg.

• Loan of £10m at 10% interest rate (the then market rate)

• Current market rate 5%

• Agree with bank a new loan of £20m at 7½%

2. Financial instruments

Accounting entries

• Derecognise existing £10m loan

• Recognise new £20m loan at PV of future payments discounted by 5%

• Assuming annual interest payment and 20 year loan: NPV is £26,231k

2. Financial instruments

Before £k

After £k

Cash 10,000 20,000

Loans (10,000) (26,231)

- (6,231)

I&E - (6,231)

(loss)

2. Financial instruments

Basic: subsequent measurement

Amortised cost except publicly traded shares (usually benign)

2. Financial instruments

Other

• Initial measurement: fair value (not including transaction costs)

• Subsequent measurement: fair value (minor exceptions)

• Changes in income and expenditure account (unless hedge accounting applies)

• Highly complex rules and documentation required

2. Financial instruments

Other

• Some loans will fail hedge accounting criteria (eg. RPI linked instruments)

• May need to opt up for full IAS 39/IFRS 9

2. Financial instruments

Other

Eg:

Loan £10m paying 3 month LIBOR plus 100 bp: 20 year life bullet repayment

No issue costs

Stand alone swap: same period and matched cash flows,

Overall effect: 6% fixed

2. Financial instruments

At inception of the swap:

Fair value £nil (presumably)

Loan £10m

At next reporting date:

Fair value of swap £1m in the money

(Assume no hedge accounting)

2. Financial instruments

Loan is a basic instrument:

Therefore still a £10m liability

Swap: £1m asset

Cr: Interest receivable £1m

2. Financial instruments

At second reporting date:

Fair value swap is say £1m out of the money (still no hedge accounting)

Loan still at £10m

Swap: now a £1m liability

Dr: Interest payable £2m

2. Financial instruments

What if the swap was embedded?:

Answer: Loan (including the swap) is a basic instrument and therefore at amortised cost i.e. £10m

No I&E account effect

2. Financial instruments

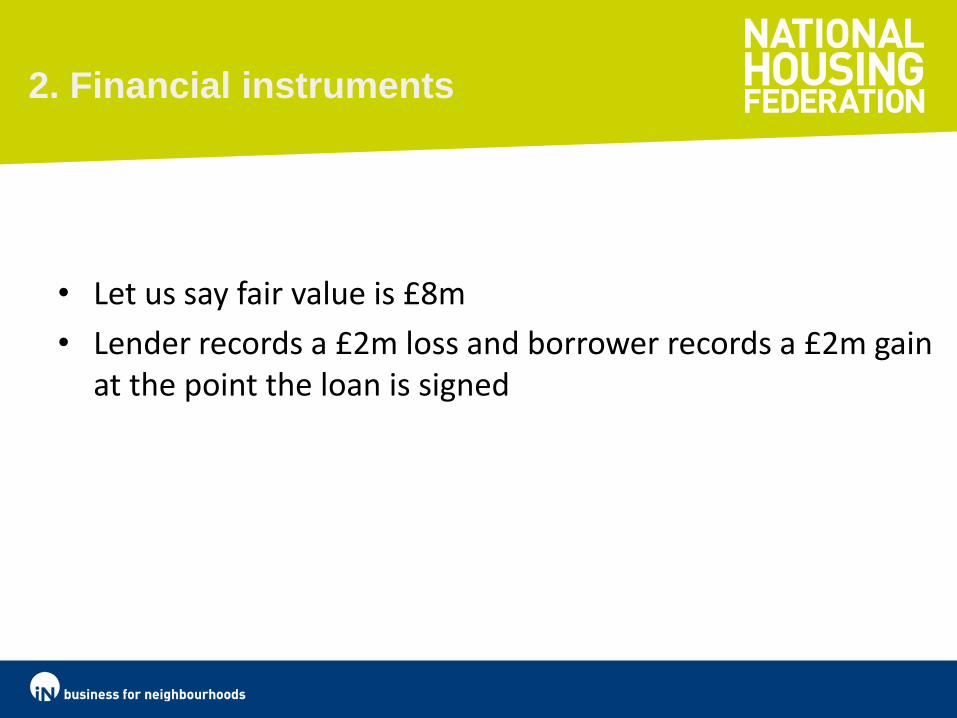

Another example:

• Intragroup loan £10m interest free

• Bullet repayment in 10 years time

• Need to discount using market rate of interest for a similar loan

2. Financial instruments

• Let us say fair value is £8m

• Lender records a £2m loss and borrower records a £2m gain at the point the loan is signed

3. Hedge accounting

• Overview

• When it can be applied

• Examples

• Pitfalls

3. Hedge accounting – overview

• If accounting for financial instruments is horribly complex, hedge accounting is even worse

3. Hedge accounting – overview

• Normally, movements in fair value of financial instruments go through the income and expenditure account; hedge accounting permits the gain or loss on the hedging instrument and on the hedge item to be recognised in the I&E account at the same time

• In practice this means movements posted directly to reserves (in most cases)

3. Hedge accounting – overview

• However

– There are strict conditions for when it can be applied

– Effectiveness testing has to be performed (prospective)

3. Hedge accounting – overview

• Text in grey potentially to change when IFRS 9 is finalised and EU adopted

• Entities can opt to apply the recognition and measurement provisions of IAS 39 (ie. full IFRS) instead of sections 11 and 12 of FRS 102

3. Hedge accounting – when it can be

applied

• Clear designation and documentation

• Hedging instrument is expected to be highly effective in offsetting the designated hedged risk

• The hedged risk is a permitted risk (next slide)

• The hedging instrument is a permitted instrument (next slide after that)

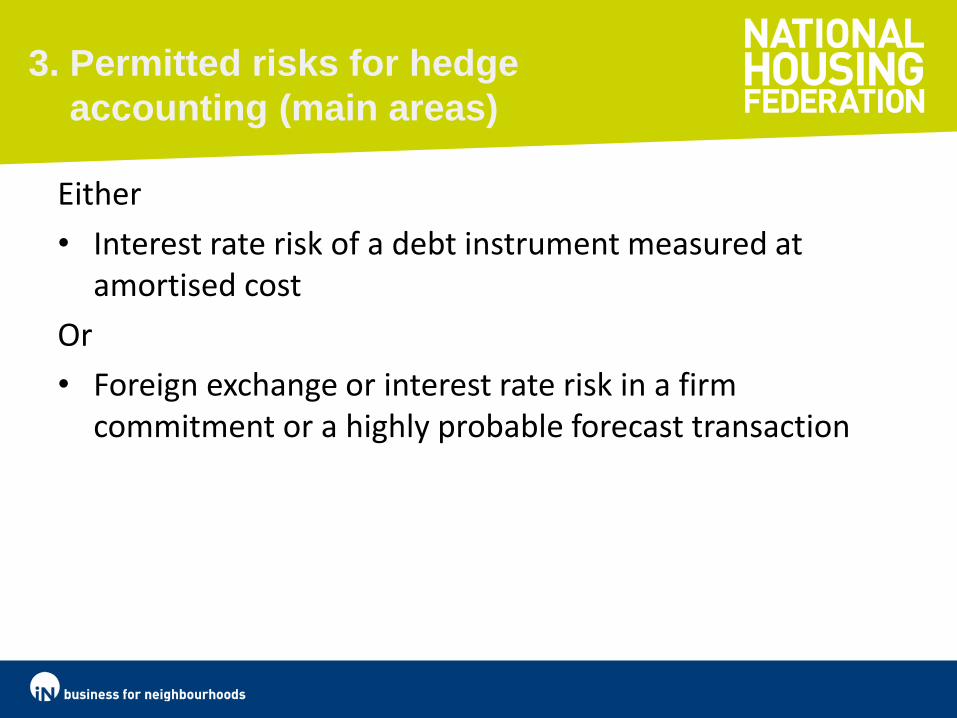

3. Permitted risks for hedge

accounting (main areas)

Either

• Interest rate risk of a debt instrument measured at amortised cost

Or

• Foreign exchange or interest rate risk in a firm commitment or a highly probable forecast transaction

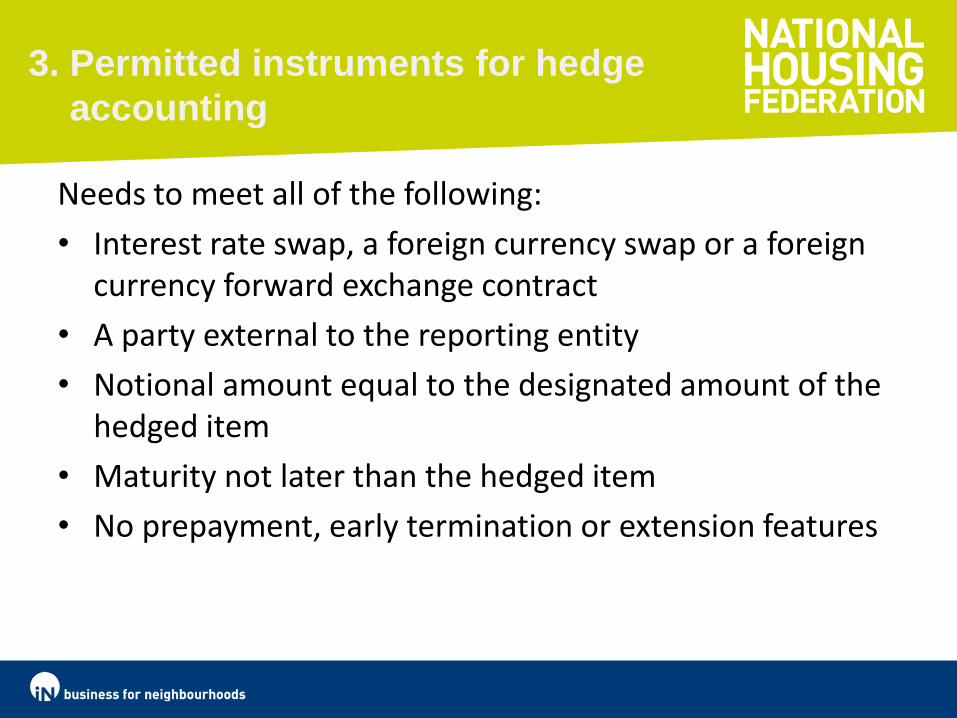

3. Permitted instruments for hedge

accounting

Needs to meet all of the following:

• Interest rate swap, a foreign currency swap or a foreign currency forward exchange contract

• A party external to the reporting entity

• Notional amount equal to the designated amount of the hedged item

• Maturity not later than the hedged item

• No prepayment, early termination or extension features

3. Cease to apply hedge

accounting if …

• Hedging instrument expires or is sold

• Conditions no longer met

• The entity revokes the designation

3. Examples: first question

• Floating rate loan (3m LIBOR) £10m 25 years left; qualified as basic instrument and held at amortised cost

• 5 year swap (1m LIBOR) £5m nominal

• Designated as hedge

3. Examples: answer

• Provided it passes the effectiveness test, hedge accounting should be applied on £5m of the loan

3. Examples: second question

• Same as above but loan has only 4 years left to run

3. Examples: answer

• Not eligible for hedge accounting (swap expires after hedged item)

3. Examples: third question

• Same as above but loan has a feature which makes it “other” and therefore accounted for at fair value. Hedge is highly effective

3. Examples: answer

• Not eligible for hedge accounting (hedged item is not at amortised cost)

3. Examples: fourth question

• Same as first but only documented the designation as a hedge on 1 October (March year end)

3. Examples: answer

• First six months not eligible, but is eligible from 1 October onwards

4. IFRS 9

• Intention that new UK GAAP will be revised once (if!) IFRS 9 is finalised and amended to be based on IFRS 9

4. IFRS 9

Approximate sequence but subject to change:

• Various bits about to go on consultation, other bits still to be drafted

• Published timetable states for accounting periods starting 1 January 2015

• EU not even looking at until issued in final form

• FRS 102 to be updated?

• SORP to be updated?

• Cows come home?

4. IFRS 9

• Presently hedge accounting rules are a long way from being finalised

• Likely to be simple and based more on the way in which treasury risks are managed

4. IFRS 9

• However will almost certainly have unintended consequences and lead to some instruments being treated in a worse manner

• Not a panacea, not able to comment conclusively

5. Challenges

• Increasing familiarity with highly complex accounting rules

• Requirements not yet finalised

• Assessing full portfolio of loans and other instruments for risks on financial reporting

• Choosing advisors carefully