ifrs update nov 28 2016

TRANSCRIPT

1Audit | Tax | Advisory

IFRS UpdateBy Paul RhodesNovember 28, 2016

2Audit | Tax | Advisory

Big shiny new standards: Financial instruments (IFRS 9) Revenue (IFRS 15) Leases – which is not covered here (IFRS 16)

Other standards update Disclosure initiative (IAS 1) Cash flow statements (IAS 7) Income tax (IAS 12) Business combinations (IFRS 3) Joint arrangements (IFRS 11) Share-based payments (IFRS 2)

3Audit | Tax | Advisory

Financial instrument – new rules (IFRS 9) Session is going to cover the recognition of financial instrument assets and their

impairment only.

The significant changes introduced by IFRS 9 from the previous IAS 39 are:

The classification of financial instrument assets – which is now based on the entity’s business model for holdings assets

The impairment model for financial instrument assets – which in the current environment may lead to higher impairment losses than would be required under IAS 39.

4Audit | Tax | Advisory

Financial instrument – new rules (IFRS 9) The standard is effective for annual periods beginning on or after January 1,

2018. Earlier adoption is permitted.

The standard is applied retrospectively. Prior periods are only restated if restatement is possible without the use of hindsight.

5Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) Measurement Financial assets and liabilities are initially recognized at their fair value plus or

minus, for instruments not at fair value through P&L (FVP&L), transaction costs that are directly attributable to their acquisition or issue (5.1.1).

Measurement on initial recognition is practically the same as it was under IAS 39.

6Audit | Tax | Advisory

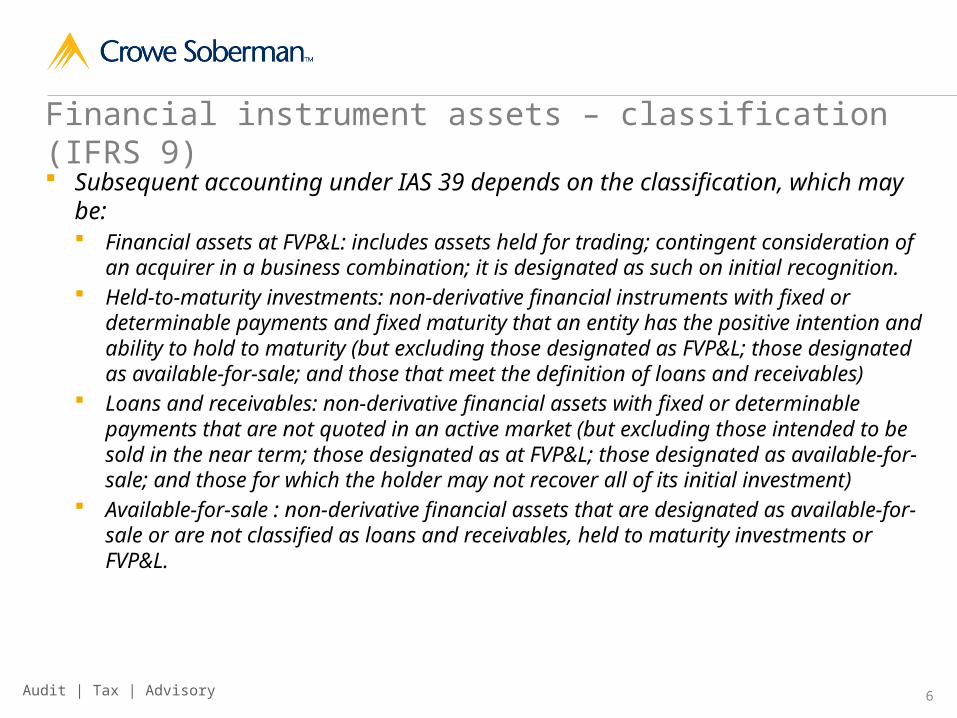

Financial instrument assets – classification (IFRS 9) Subsequent accounting under IAS 39 depends on the classification, which may

be: Financial assets at FVP&L: includes assets held for trading; contingent consideration of

an acquirer in a business combination; it is designated as such on initial recognition. Held-to-maturity investments: non-derivative financial instruments with fixed or

determinable payments and fixed maturity that an entity has the positive intention and ability to hold to maturity (but excluding those designated as FVP&L; those designated as available-for-sale; and those that meet the definition of loans and receivables)

Loans and receivables: non-derivative financial assets with fixed or determinable payments that are not quoted in an active market (but excluding those intended to be sold in the near term; those designated as at FVP&L; those designated as available-for-sale; and those for which the holder may not recover all of its initial investment)

Available-for-sale : non-derivative financial assets that are designated as available-for-sale or are not classified as loans and receivables, held to maturity investments or FVP&L.

7Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) To be held for trading under IAS 39 an asset needs to be:

i. Acquired for the purpose of sale in the near term; andii. Part of a portfolio of identified financial instruments that are managed together and for

which there is evidence of a recent pattern of short-term profit taking; oriii. It is a derivative (except for a derivative that is a financial guarantee contract or a

designated and effective hedging instrument). (IAS 39.9)

Subsequent measurement under IFRS 9 may be either: amortized cost fair value through OCI (FVOCI) or FVP&L (4.1.1)

Which is used depends on the assets’ classification which itself depends on the business model and the contractual cash flow characteristics.

The methods of subsequent measurement of assets are comparable to IAS 39, except for the addition of FVOCI.

8Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) Amortized cost is used if the objective of the business model is to collect

contractual cash flows and the terms of the asset only give rise to payments of principal and interest on the principal outstanding, on specified dates (4.1.2(a) & 9B))

If the business model allows for the collection of contractual cash flows and the sale of the financial asset, then they are measured at fair value through OCI (4.1.2A)

Principal means the fair value of the financial asset on initial recognition. Interest is the consideration for the time value of money taking into account credit risk, other risks and costs and a profit margin. (4.1.3)

9Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) The business model:

The determination is made at the level of groups of financial assets. An entity may have more than one model for managing different groups of instrument: one portfolio of loans may be managed to collect contractual cash flows and another may be managed to trade and realize fair value gains. The determination need not be made at the reporting entity level.

The management scenarios for portfolios of assets must be reasonably expected to occur. The intention to sell a particular portfolio only in a stress case scenario does not affect the assessment of the business model.

Similarly realizing cash flows in a way that is different from expectations when the business model was assessed does not give rise to a prior period error and does not change the classification of the remaining financial assets in that business model.

10Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) An entity’s business model is typically observable through actions taken to achieve

objectives. An entity has to use all available evidence, such as: how performance is evaluated and reported; the risks that affect the performance and how those risks are managed; and how management is compensated

Judgement is required. (B4.1.2 to 2B)

11Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) Examples that would result in contractual cash flows not representing a basic

lending arrangement, so contractual cash flows are not solely payments of principal and interest, include: Contractual terms that introduce exposure to other risks or volatility, such as exposure

to changes in equity or commodity prices, including an interest rate that is reset to a higher rate if an equity index reaches a particular level. (B.1.7A & B4.1.10)

An imperfect relationship between the element of interest that represents consideration for the time value of money, such as an interest rate that is reset monthly to a one-year interest rate. A quantitative assessment of how different the contractual cash flows are from the unmodified time value of money element of interest may be required. (4.1.9B&C)

A financial instrument that includes a clause allowing early settlement, and the prepayment amount includes an unreasonable amount of additional compensation (such as a fixed amount of compensation regardless of the timing of the early termination) for the early termination of the contract. (B4.1.11(b))

The instruments’ contractual cash flows represent an investment in an underlying asset or cash flows, for example where cash flows are linked to sales. (B4.1.16)

12Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) Measurement at fair value through P&L is the default for instruments that do not

fall into the amortized cost or FVOCI buckets, including when the principal and interest criterion is not met.

FVP&L was also the default bucket under IAS 39.

13Audit | Tax | Advisory

Financial instrument assets – classification (IFRS 9) Irrevocable elections are available at initial recognition:

For particular equity instruments that would otherwise be measured at FVP&L to present subsequent changes in fair value in OCI (4.1.4).

To designate a financial asset at FVP&L to avoid an accounting mismatch from accounting for assets and liabilities on different bases. (4.1.5)

The election for mismatches of accounting treatment was also available under IAS 39.

14Audit | Tax | Advisory

Financial instrument assets – old rules (IAS 39) Example 1 Lender A has concerns that some of its borrowers will not be able to make all

principal and interest payments due under their borrowing agreement in a timely manner. Therefore it negotiates a restructuring of these loans.

Lender A believes that each borrower will be able to meet their obligations under the restructured terms.

Would Lender A recognize an impairment loss in each of the following restructured loans:

a) Customer V will pay the full amount of the principal of the original loan five years after the original due date, but none of the interest under the original terms.

15Audit | Tax | Advisory

Financial instrument assets – old rules (IAS 39) Example 1 Cntd.

b) Customer W will pay the full principal amount of the original loan on the original due date, but none of the interest due under the original terms.

c) Customer X will pay the full principal amount of the original loan on the original due date with interest only at a lower interest rate than the interest rate inherent in the original loan.

d) Customer Y will pay the full principal amount of the original loan five years after the original due date and all interest accrued during the original loan term, but no interest for the extended term.

e) Customer Z will pay the full amount of the original loan five years after the original due date and all interest, including interest for both the original term of the loan and the extended term.

16Audit | Tax | Advisory

Financial instrument assets – old impairment rules (IAS 39) Under IAS 39 a financial asset is impaired if, and only if, there is objective

evidence of impairment as a result of one or more events that occurred after initial recognition of the asset and that loss event has an impact on the estimated future cash flows that can be reliably estimated. The loss may be caused by the combined effect of several events.

IAS 39 explicitly states: losses expected as a result of future events, no matter how likely, are not recognized.

IAS 39 examples of objective evidence of impairment includes: Significant financial difficulty of the borrower Default or delinquency in interest or principal payments The probable bankruptcy of the borrower For a group of financial assets: adverse changes in the payment status of borrowers in

the group (increased number of borrowers reaching their credit limit) or national or local economic conditions that correlate with defaults on the assets in the group (for example unemployment rate or a decrease in property prices)

17Audit | Tax | Advisory

Financial instrument assets – old impairment rules (IAS 39) The amount of the impairment loss is measured as the difference between:

The assets carrying amount at the reporting date and The present value of estimated future cash flows (excluding future credit losses that

have not been incurred) discounted at the financial asset’s original effective interest rate. Using the current market rate would impose fair value measurement on an asset that is measured at amortized cost.

The amount of the loss and reversals are recognized in P&L. (63 & 65)

An impairment loss may be either a single amount or a range. If a range is determined the best estimate is used. (AG86)

The impairment test is first carried out individually for significant assets, and individually or collectively for assets that are not individually significant. Assets are grouped on the basis of similar credit risk characteristics, which may include credit grading, industry, geographical location, type of collateral, past-due status.

18Audit | Tax | Advisory

Financial instrument assets – old impairment rules (IAS 39) If the entity determines that there is no objective evidence of impairment for an

asset that is assessed individually, the asset is then considered for impairment as part of a group. (63 & 64 & AG87)

Once an impairment loss is recognized, interest income is recognized using the original effective interest rate of the asset. (AG93)

An impairment loss on a financial asset carried at cost is not reversed.

Declines in the fair value of available-for-sale financial assets are recognized in OCI. Where there is objective evidence that the asset is impaired, the cumulative loss that was previously recognized in OCI is reclassified from equity to P&L. (67)

19Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9)

20Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) Scope of the impairment rules An expected credit loss allowance is recognized for financial instrument assets

measured at amortized cost or at FVOCI in accordance with IFRS 9, plus the following, some of which are otherwise outside the outside the scope of the standard: Lease receivables (IAS 17) Contract assets (IFRS 15) Loan commitments and Financial guarantee contracts (IAS 4)

The scope is broadly the same as under IAS 39, which required any financial debit to be considered. IFRS 9 has added guidance on specific contracts such as guarantees and commitments.

21Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) An allowance on a financial asset at FVOCI is recognized in OCI but does not

reduce the carrying amount of the asset in the statement of financial position. (5.5.2)

If at the reporting date there has not been any significant increase in credit risk since initial recognition, the loss allowance is recognized at an amount equal to the 12-month expected credit loss. (5.5.5)

Note that the new test is future looking, unlike IAS 39.

22Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) If the credit risk of a financial instrument increases significantly since initial

recognition then the loss allowance recognized is equal to the lifetime expected credit loss. The assessment can be made individually or collectively. (5.5.3 & 4)

The assessment is based on the change in the risk of a default occurring over the expected life of the

financial instrument must consider all reasonable and supportable information including forward looking information, that is available without undue cost or effort and that is indicative of significant increases in credit risk (5.5.9)

23Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) If reasonable and supportable information is available, an entity cannot rely

solely on past due information, and vice versa.

There is a rebuttable presumption that the credit risk has increased significantly when contractual payments are more than 30 days past due. This can be rebutted with reasonable and supportable information that proves otherwise. (5.5.11)

The changes in credit loss allowance is recognized in P&L as an impairment gain or loss. (5.5.8)

24Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) Example 2 Company C is the holding company of a group that operates in a cyclical

industry. Bank B provides a loan to Company C. At that time prospects for the industry were positive, even though input prices were volatile and a potential decrease in sales is anticipated given the point in the cycle.

In the past Company C has focused on external growth, acquiring investments in companies in related sectors, making the group structure complex and reducing the ability to forecast the cash that will be available at the holding company level.

When the loan was advanced leverage was at an acceptable level, but there was concern over Company C’s ability to refinance due to the short remaining life until maturity, and over the ability to service the debt using dividends from operating subsidiaries.

25Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) Example 2 continued Company C’s leverage was in line with other customers of Bank B with similar

credit risk. Based on projections over the expected life of the loan the remaining capacity on its coverage ratios was high. When the loan was advanced Bank B determines there is significant credit risk and that uncertainties affecting cash availability could lead to default. The loan is not considered to be originated credit-impaired.

Subsequent to recognition, three of Company C’s five key subsidiaries had a significant reduction in sales due to market conditions, but sales are expected to improve with the industry cycle. Sales in the other two subsidiaries are stable. Company C has announced a restructuring to increase the flexibility for refinancing existing debt and for payment of dividends.

Has there been a significant increase in credit risk since initial recognition?

26Audit | Tax | Advisory

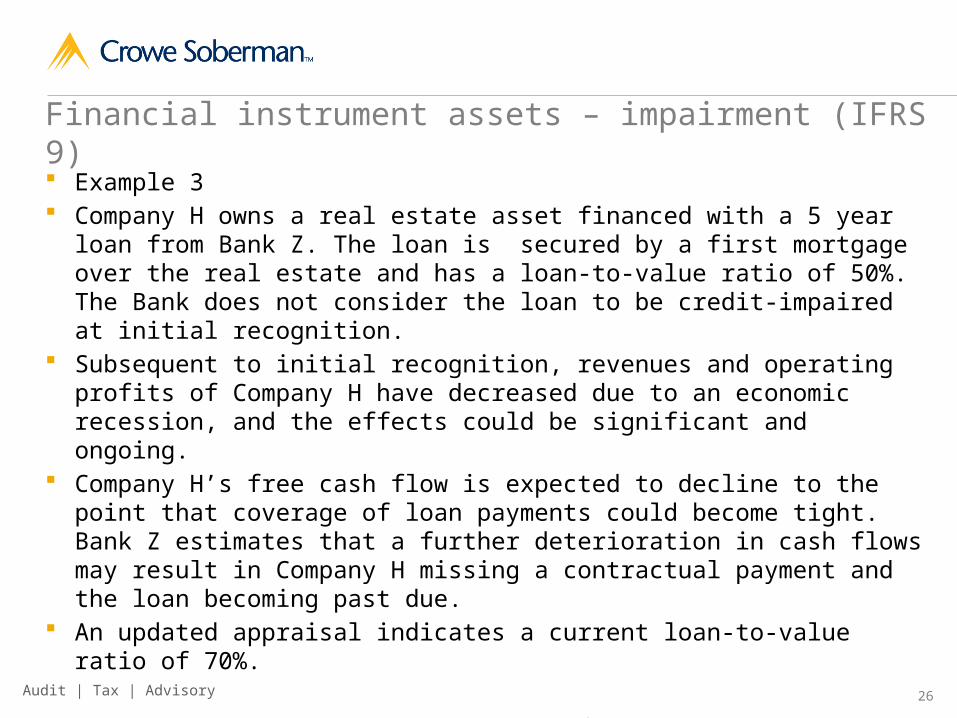

Financial instrument assets – impairment (IFRS 9) Example 3 Company H owns a real estate asset financed with a 5 year loan from Bank Z.

The loan is secured by a first mortgage over the real estate and has a loan-to-value ratio of 50%. The Bank does not consider the loan to be credit-impaired at initial recognition.

Subsequent to initial recognition, revenues and operating profits of Company H have decreased due to an economic recession, and the effects could be significant and ongoing.

Company H’s free cash flow is expected to decline to the point that coverage of loan payments could become tight. Bank Z estimates that a further deterioration in cash flows may result in Company H missing a contractual payment and the loan becoming past due.

An updated appraisal indicates a current loan-to-value ratio of 70%.

Has the credit risk increased significantly? What effect does the collateral have?

27Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) The measurement of expected credit losses must reflect:

An unbiased probability weighted amount by evaluating a range of possible outcomes. At a minimum the assessment should consider the possibility that a credit loss occurs and the possibility that no credit loss occurs.

The time value of money Reasonable and supportable information that is available without undue cost and effort

at the reporting date about Past events Current conditions and Forecasts of future economic conditions (5.5.17 & 18)

The maximum period to consider is the maximum contractual period over which the entity is exposed. The entity’s ability to demand repayment and cancel any undrawn commitment does not limit the exposure to credit losses to the contractual notice period.

The expected credit loss is measured over the period that the entity is exposed to credit risk and expected credit losses would not be mitigated by credit risk management actions. (5.5.20)

28Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) For renegotiated or modified financial instruments that have not been

derecognized the change in credit risk at the reporting date is assessed by comparing the risk of default based on the modified contractual terms with the risk of default at initial recognition based on the original contractual terms. (5.5.12)

If a financial instrument was assessed as having low credit risk at initial recognition then the entity may presume that credit risk has not increased significantly. (5.5.10)

If at a subsequent reporting date the entity concludes that the significant increase in credit risk condition is no longer met, then the loss allowance is measured at the 12-month expected credit loss at that date. (5.5.7)

29Audit | Tax | Advisory

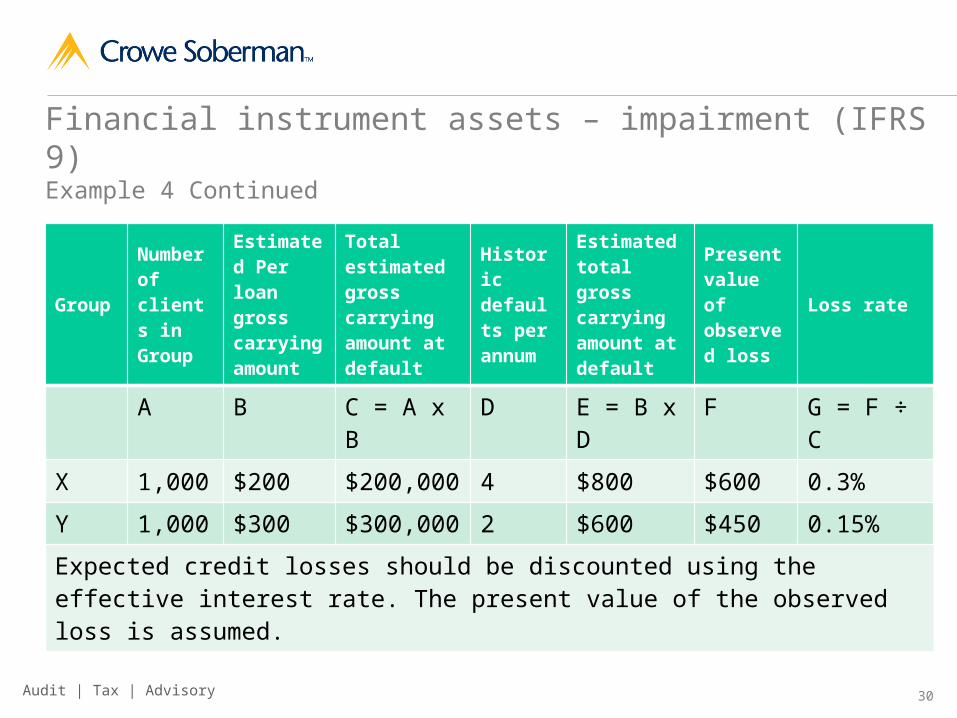

Financial instrument assets – impairment (IFRS 9) Example 4 MIC M originates 2,000 loans with gross carrying amount of $500,000. The

portfolio can be split into two groups based on the credit risk characteristics of each. Group X comprises 1,000 loans with gross carrying amount of $200 each, and Group Y comprises 1,000 loans with gross carrying amount of $300 each. There are no transaction costs or options.

MIC M measures expected credit losses based on a loss rate approach for each group, using samples of historical default and loss experience plus forward looking information for forecast economic conditions.

Historically loss rates are 0.3% based on four defaults for Group X and 0.15% based on two defaults for Group Y. The portfolio can be described as:

30Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9)Example 4 Continued

Group

Number of clients in Group

Estimated Per loan gross carrying amount

Total estimated gross carrying amount at default

Historic defaults per annum

Estimated total gross carrying amount at default

Present value of observed loss

Loss rate

A B C = A x B D E = B x D F G = F ÷ C

X 1,000 $200 $200,000 4 $800 $600 0.3%

Y 1,000 $300 $300,000 2 $600 $450 0.15%

Expected credit losses should be discounted using the effective interest rate. The present value of the observed loss is assumed.

31Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9)Example 4 Continued At the reporting date MIC M expects an increase in defaults over the next 12

months: five in Group X and three in Group Y. The present value of the observed loss per loan is estimated to remain consistent with historical losses. The expected increase in defaults is not considered to represent a significant increase in credit risk.

What are the present values of the loss allowance and the loss rates for each group?

32Audit | Tax | Advisory

Financial instrument assets – impairment (IFRS 9) Stuff worth remembering The accounting treatment of financial instruments is aligned with the business

model, including the model for managing and pricing risk

Calculation of impairment losses now looks to future events and evidence

Therefore, in a downward economic cycle (the current environment?), loss allowances are expected to increase

The standard and related guidance are very detailed and includes questions addressed by the Transition Resource Group (TRG). Implementation will be complex, involving a degree of analysis and judgement calls, such as: What economic data is correlated with past losses How is a significant increase in credit risk defined

33Audit | Tax | Advisory

Revenue (IFRS 15) Scope The standard applies to all contracts with customers except:

Leases Insurance contracts Financial instruments Non-monetary exchanges

The standard also specifies the accounting for: costs incurred to obtain a contract with a customer and the costs incurred to fulfill a contract if not dealt with by another standard

34Audit | Tax | Advisory

Revenue (IFRS 15) Effective date and transition Standard is applicable for years commencing January 1, 2018.

Adoption can either be: full retrospective, so restatement of January 1, 2017 statement of financial position or Restatement of 2018 only with adjustment to opening statement of financial position at

January 1, 2018

Practical measures are available for each method to make transition less onerous

35Audit | Tax | Advisory

Revenue (IFRS 15) Five steps1. Identify the contract with the customer

The following criteria must be met for a contract with a customer to be within the scope of the standard: The parties have approved the contract (may be verbal or implied if that is the

customary business practice) and the contract creates enforceable rights between the parties

Each parties rights regarding the goods or services to be transferred can be identified Payment terms can be identified The contract has commercial substance (meaning the risk, timing or amount of future

cash flows is expected to change as a result) and It is probable the entity will collect the consideration it is entitled to in exchange for the

goods or services that will be transferred to the customer, considering only the customer’s ability and intention

36Audit | Tax | Advisory

Revenue (IFRS 15) Several contracts entered into at the same or similar time are combined if the

criteria listed at 17 are met.

Contract modifications are specifically dealt with in the standard. A modification is treated as a separate contract if: The scope increases due to additional distinct goods and services The price of the contract increases by an amount of consideration reflecting stand-alone

selling prices (as opposed to prices blended with the previous contract) plus or minus appropriate adjustments in relation to the new contract

If a modification is not treated as a separate contract in accordance with methods specified by the standard. (21)

37Audit | Tax | Advisory

Revenue (IFRS 15)2. Identify performance obligations

At contract inception each separate promise to transfer to the customer, either: A good or service (or bundle of goods or services) that is distinct; or A series of distinct goods or services that are substantially the same and that have the

same pattern of transfer to the customer (as defined in the standard)

A good or service is distinct if: The customer can benefit from the good or service either on its own or together with

other resources that are readily available to the customer; and The entity’s promise to transfer the good or service is separately identifiable from other

promises in the contract. For example, the entity does not provide a significant service of integrating the good or service with other promises in the contract.

Any non-distinct goods or services are combined with other promises until a group is identified that is distinct.

38Audit | Tax | Advisory

Revenue (IFRS 15)3. Determine the transaction price

The transaction price is the amount of consideration the entity expects to be entitled to in exchange for contract promises. The following are considered: Variable consideration, which is estimated using either the expected value or the most

likely amount method Constraining estimates of variable consideration: variable consideration is included

only to the extent that it is highly probably that a significant reversal will not occur when the uncertainty is resolved

A significance financing components Non-cash consideration, which is measured at fair value, or, if that is not possible,

using the stand alone selling price of the goods exchanged Consideration payable to a customer

39Audit | Tax | Advisory

Revenue (IFRS 15)4. Allocate the transaction price to performance obligations

In making the allocation the goal is to allocate an amount to depict the amount of consideration the entity expects to be entitled to in exchange for the promised goods or service.

The allocation is made on a relative stand-alone sales price basis, adjusted for discounts and variable consideration. If stand alone prices are not observable they are estimated.

40Audit | Tax | Advisory

Revenue (IFRS 15)5. Recognize revenue when or as performance obligations are satisfied

Revenue is recognized when or as performance obligations are satisfied. For an asset, that point is when the customer takes control of the asset.

The satisfaction occurs over time when one of the following criteria is met: The customer simultaneously receives and consumes the benefit as the entity performs; The entity’s performance creates or enhances an asset that the customer controls; or The entity’s performance does not create an asset with an alternative use to the entity

(either due to contractual or practical limitations to direct the completed asset to another use) and the entity has an enforceable right to payment for performance completed to date

41Audit | Tax | Advisory

Revenue (IFRS 15) Progress is measured by either output methods (cubic feet) or input methods

(labour hours). If progress cannot be reliably measured but the entity expects to recover the costs, then revenue is recognized to the extent of costs incurred.

If performance obligations are not satisfied over time then they are satisfied at a point in time. Guidance is provided to determine at what date that occurs. For example, a present right to payment may indicate that obligations have been satisfied.

42Audit | Tax | Advisory

Revenue (IFRS 15)Accounting for licenses

43Audit | Tax | Advisory

Revenue (IFRS 15) Example 5

44Audit | Tax | Advisory

Revenue (IFRS 15)Construction industry effects

45Audit | Tax | Advisory

Revenue (IFRS 15) Example 6

46Audit | Tax | Advisory

Revenue (IFRS 15) Stuff to remember

The transition will be complicated for some industries with significant effects on revenues (construction, software licenses)

Significant estimation will be required

The standard and related guidance are very detailed and includes questions addressed by the Transition Resource Group (TRG). Application will be time consuming in some cases.

47Audit | Tax | Advisory

Other standards update Disclosure initiative (IAS 1) Cash flow statements (IAS 7) Income tax (IAS 2) Business combinations (IFRS 3) Joint arrangements (IFRS 11) Share-based payments (IFRS 2)

48Audit | Tax | Advisory

Disclosure initiative - Amendment to IAS 1

Response to information overload Encourage use of judgment Materiality considerations apply to disclosures Presentation of specific line items and sub-totals – understandable, consistent Structure notes in an orderly and logical manner Examples of SAP notes re income taxes and foreign exchange gains/losses

removed

Effective for fiscal periods beginning on or after January 1, 2016

49Audit | Tax | Advisory

Disclosure initiative - Amendment to IAS 1Application of materiality Specific or minimum requirements in an IFRS not required if resulting disclosure

is not material (e.g. carrying amount of inventory by classifications, write-downs) Immaterial information can obscure understandability of f/s Do not aggregate material items that is of different nature or function

Headings and subtotals More flexibility in presenting additional line items Must be recognized and measured in accordance with IFRS Labelled and presented in a manner that makes it clear and understandable what

is included Can’t give more prominence than totals and subtotals required in an IFRS E.g. ‘operating profit’

50Audit | Tax | Advisory

Disclosure initiative - Amendment to IAS 1Notes to f/s More flexibility in notes structure – ‘ a systematic manner’ Disclosure of significant accounting policies (not ‘summary’) Removed specific reference to income taxes and foreign exchange as expected

accounting policies Removed requirement ‘normally present in the following order’ (now it’s only 1

possible example) Examples of systematic ordering:

Prominence to those considered most relevant to understanding entity’s financial performance/ position

Order of line items in statement of financial position and income statement Grouping items measured similarly (such as assets measured at fair value)

51Audit | Tax | Advisory

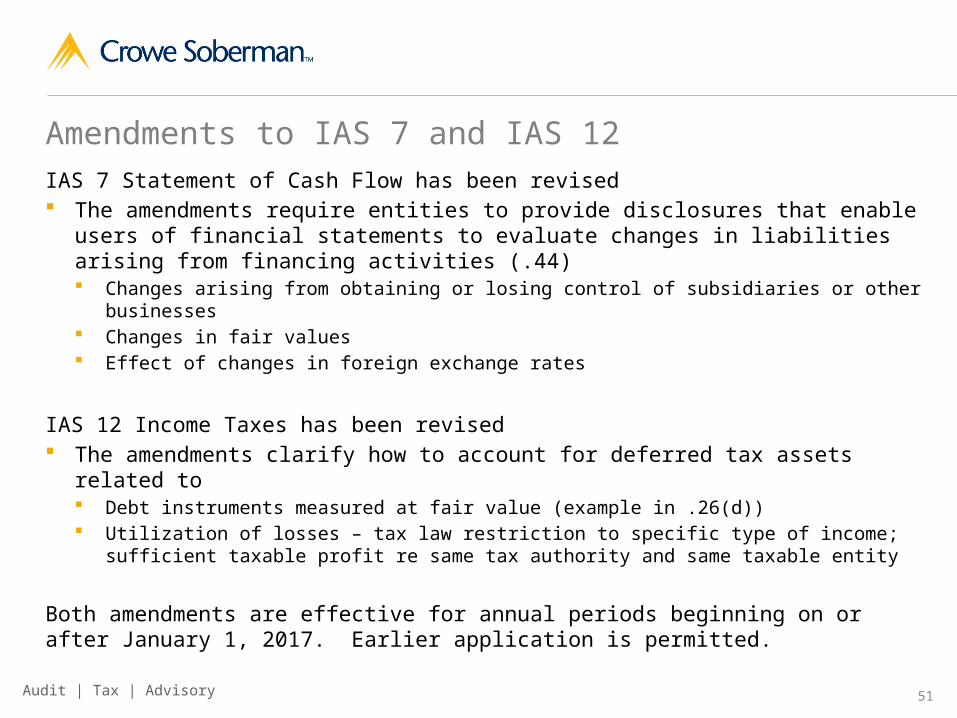

Amendments to IAS 7 and IAS 12IAS 7 Statement of Cash Flow has been revised The amendments require entities to provide disclosures that enable users of financial

statements to evaluate changes in liabilities arising from financing activities (.44) Changes arising from obtaining or losing control of subsidiaries or other businesses Changes in fair values Effect of changes in foreign exchange rates

IAS 12 Income Taxes has been revised The amendments clarify how to account for deferred tax assets related to

Debt instruments measured at fair value (example in .26(d)) Utilization of losses – tax law restriction to specific type of income; sufficient taxable profit re same

tax authority and same taxable entity

Both amendments are effective for annual periods beginning on or after January 1, 2017. Earlier application is permitted.

52Audit | Tax | Advisory

Amendments to IFRS 3 and IFRS 11DEFINITION OF A BUSINESS AND ACCOUNTING FOR PREVIOUSLY HELD INTERESTS As part of the IFRS 3 post-implementation review, the Board noted that entities

find it difficult to apply the definition of a business and many acquisitions result in business combinations, despite that not seeming logical.

The Board also noted difficulties encountered when accounting for previously held interests when an entity: Obtains control of a business that is a joint operator; and Obtains joint control of a business that is a joint operation.

In June 2016, the IASB issued an Exposure Draft on amendments to IFRS 3 and 11 to clarify these issues.

Comments on the Exposure Draft closed on October 31, 2016.

53Audit | Tax | Advisory

Amendments to Share-based payments (IFRS 2) Three amendments to IFRS 2 to clarify:

Effects of vesting conditions on the measurement of cash-settled share-based payments;

Accounting for a modification to the terms and conditions of a share-based payment that changes the classification of the transaction from cash-settled to equity-settled; and

Classification of share-based payment transactions with net settlement features for withholding tax obligations.

Amendments are effective for periods beginning on or after January 1, 2018. Earlier adoption is permitted.