ih 2009 financial results - gas plusir.gasplus.it/file_upload/pres.090807gasplusih0.pdf · tender...

TRANSCRIPT

IH 2009 Financial Results

Milan, 7th August 2009

www.gasplus.it

Market Environment General

Eni Gas Release PriceBrent Price

0

20

40

60

80

100

120

140

160

lug ago set ott nov dic gen feb mar apr mag giu

$/bbl - 2007/2008 $/bbl - 2008/2009

0

5

10

15

20

25

30

35

40

45

lug ago set ott nov dic gen feb mar apr mag giu

(€/MWh) - 2007/2008 (€/MWh) - 2008/2009

Euro – Us Dollar Exchange rate

1

TTF Gas Price

1,2

1,25

1,3

1,35

1,4

1,45

1,5

1,55

1,6

1,65

lug ago set ott nov dic gen feb mar apr mag giu

EUR - USD 2007/2008 EUR - USD 2008/2009

0

5

10

15

20

25

30

35

lug ago set ott nov dic gen feb mar apr mag giu

Gas TTF (€/MWh) - 2007/2008 Gas TTF (€/MWh) - 2008/2009

IH09 Results Highlights

Domestic Production: 102 MSmc (- 16.4% vs IH08) due to expected extraordinary maintenance on some wells, now the production is achieving yearly target.Reserves replacement due to workover activities near to 100%Under evaluation acquisition opportunity of Italian Assets;

Italian+Int. E&P

StorageSinarca: near to complete the process to obtain the concession;

The Group reacts in a complex macroeconomic scenari o bearing the economic reasults: Revenues 224.5M€ (+19.4% vs IH08), EBITDA 23.9 M€ (-27.6% vs I H08), EBIT 14.6 (-29.7% vs IH08).

Higher Net Profit 10.2 M€ (+15.1 % vs IH08).

2

Sales 586.3 MScm (+8.3% vs IH08);

Positive operating profitability (EBITDA 4.1 M€) notwithstanding the negative economic scenario;

S&S

Network

Transport

Retail Volume of gas sold : 197.6 MScm (-0.3% vs IQH8);Lower consumption individual customers due to slowdown of industrial customers;Thin margins led to a negative global result, expected recovery in IIH09: EBITDA -1,1M€ (€ IH08 : +0,5M)

Distributed volumes: 107 MSmc (-3.2% vs IQH8) due to the consumption slowdown

Gas Plus Reti S.r.l. became fully owned by Gas Plus.

Signed the agreement with the local municipalities in order to spinoff pipeline asset in 3Q and start-up the operations of BU Transport in 4Q09.

San Benedetto: begining the JV’s operative activities;

IH09 Results Fin. Overview

% %

IH09 on sales IH08 on sales % change

Total Revenues 224.5 188.0 +19.4%Operating Costs 200.6 +89.3% 154.9 +82.4% +29.5%EBITDA 23.9 +10.7% 33.1 +17.6% -27.6%EBIT 14.6 +6.5% 20.8 +11.1% -29.8%

Profit before Tax 17.1 +7.6% 19.0 +10.1% -9.8%

(Euro M)

33

Profit before Tax 17.1 +7.6% 19.0 +10.1% -9.8%Net Profit 10.2 +4.5% 8.9 +4.7% +15.1%EPS 0.23 0.20 +15.1%

44,909,620 44,835,000 Net Debt 22.0 -24.1Equity 218.8 215.3Fixed assets 225.6 217.8

IH09 Financial Data Fin. Overview

EBITDA by Business UnitEBIT by Business Unit

-1.074

-1.095-0.282

-0.077

26,808

19,366

3,383

4,101

0,508 2,131

3,402

0,244

IH08 IH09

M€

Other Activities Network Retail Supply & Sales Exploration & Production

33.074

25.718

- 22%

15,759

11,85314,179

8,615

3,383

4,101

3,383

4,101

0,494

0,494

1,063

1,837

1,063

1,837

0,148

0,148

IH08 IH09 IH08 adj. IH09 adj.

M€

Other Activities Network Retail Supply & Sales Exploration & Production

20.847

16.414

19.267

13.176

- 21%- 32%

4

Balance Sheet Net Debt and Cash Flow30th June 2009 31st December 2008

Inventories 41,190 48,663Receivables 133,930 138,472Payables (55,481) (102,213)Other working credits/debts (41,622) (8,792)Net work ing capital 78,017 76,130

Non current assets 225,574 223,474

Tax, Abandonment, Severance and other provisions (62,810) (62,849)

Net Invested Capital 240,781 236,755

Net financial Position 22,010 20,746Equity 218,771 216,009

Total sources 240,781 236,755

(20,746)

23,929

(6,919)

(1,926)

(11,806)

(6,578) 2,036

(22.010)

(30.000)

(25.000)

(20.000)

(15.000)

(10.000)

(5.000)

0

5.000

Initial NFP @ 1st Jan

2009Ebitda

Taxes

Change in funds and WC

Net Capex / Disposal

Dividends Financial profit/loss

Final NFP @ 30th

June 2009

Other Activities Network Retail Supply & Sales Exploration & Production

E&P E&P

IH09 IH08 ∆∆∆∆%

Gas Production (MScm) 101.6 121.5 - 16.3%

Transfer Price (€cent/Scm) 28.4 28.6 - 0.8%

Exploration Capex Italy (M€) 0.8 3.7 - 78.6%

Exploration Capex International (M€) 0.9 4.2 - 77.8%

Development Capex Italy (M€) 8.6 1.6 + 437.2%

EBITDA 19.4 26.8 - 27.8%

55

Production IH09Production IH09

Successful Workover: Metaponto 1, Accettura 2;

Setting up of the compression station in Poggiofiorito;

Restablished the interrupted production at Muzza 4.

International Activities E&P

Romania (15% )

UKBlock P001-Monkwell expected drill in 2H09

PolandAssigned Block 106 on DecemberTender for assigment of 3D seismic survey

NLJVS on Blocks E15c, E13, D9 with Tullow oil (op)

66

Romania (15% )Change of operator (IQ09) with Melrose;Slowdown of formal permitting procedure due to the authorization process

Romania

Storage Storage

SINARCA PROJECT (60% GPS)SINARCA PROJECT (60% GPS)

MSE convened the “Conferenza deiServizi”, last stage in authorization procedure;

Published EIA Ministry Decree (2008), under implement the prescription enclosed in the Decree;

Assignment of EPIC underway;

Poggiofiorito (100% GPS)Working Gas : 157 MSmc

San Benedetto (49% GPS)Working Gas : 522 MSmc

Sinarca (60% GPS)Working Gas : 324 MSmc

Total Working Gas 1,003 MSmc

Gas Plus is operator in all the projects

7

SAN BENEDETTO (49% GPS)SAN BENEDETTO (49% GPS)

JV operating and technical bodies began the activities;

Ongoing the setting up of the EIA study;

POGGIOFIORITO (100%GPS)POGGIOFIORITO (100%GPS)

Ongoing the setting up of the EIA study.

Projects Schedule20

08

2009

2010

2011

2012

2013

2014

Poggiofiorto

San Benedetto

Sinarca

Total Working Gas 1,003 MSmcTotal Gas Plus Share 607 MSmc

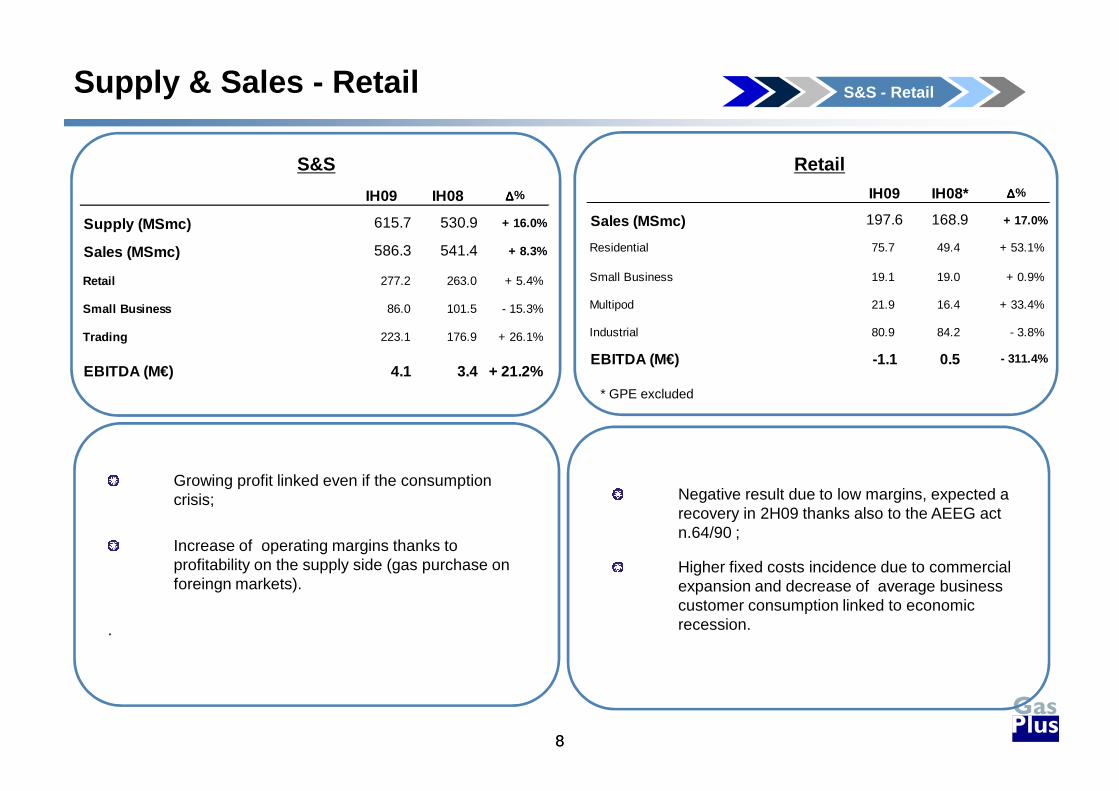

Supply & Sales - Retail S&S - Retail

S&S Retail

IH09 IH08* ∆∆∆∆%

Sales (MSmc) 197.6 168.9 + 17.0%

Residential 75.7 49.4 + 53.1%

Small Business 19.1 19.0 + 0.9%

Multipod 21.9 16.4 + 33.4%

Industrial 80.9 84.2 - 3.8%

EBITDA (M€) -1.1 0.5 - 311.4%

* GPE excluded

IH09 IH08 ∆∆∆∆%

Supply (MSmc) 615.7 530.9 + 16.0%

Sales (MSmc) 586.3 541.4 + 8.3%

Retail 277.2 263.0 + 5.4%

Small Business 86.0 101.5 - 15.3%

Trading 223.1 176.9 + 26.1%

EBITDA (M€) 4.1 3.4 + 21.2%

88

Growing profit linked even if the consumption crisis;

Increase of operating margins thanks to profitability on the supply side (gas purchase on foreingn markets).

.

Negative result due to low margins, expected a recovery in 2H09 thanks also to the AEEG act n.64/90 ;

Higher fixed costs incidence due to commercial expansion and decrease of average business customer consumption linked to economic recession.

* GPE excluded

Network Network

* Former Salso Servizi Netwok business unit excluded

IH09 IH08* ∆∆∆∆%

Distributed volumes (MSmc) 107.0 85.9 n.a.Direct end users (#k) 89.8 71.3 n.a.Pipeline 1.5 1.5 n.a.

EBITDA (M€) 3.4 2.1 + 59.6%

99

Gas Plus Reti S.r.l. became fully owned by Gas Plus;

Still applied the old tariff mechanism and assumed as yearly budget reference. Uncertain the applicationof the new tariff mechanism approved by the AEEG. (act #159/08);

Signed the agreement with local municipalities in order to spin off in 3Q09 of almost 30km of network to Gas Plus Trasporto S.r.l., new company that operates in the regional transport business unit.

Company Profile Annex

Shareholding Share information

N. of share: 44,909,620

IPO price: € 8.5 per share

Price as of 08/03/09: € 7.25 per share

Mkt capitalization: € 324M

Italian Stock Exchange – segment MTA

Specialist: Banca IMI S.p.A.

Own shares as of 08/03/09 : 1,104,073.

Share price performance

10500

12500

14500

16500

18500

20500

22500

24500

26500

28500

30500

32500

5

5,5

6

6,5

7

7,5

8

8,5

€

73,62%

12,74%13,64%

Us.fin. S.r.l. (Davide Usberti) Findim S.A. Market (included own shares)

1010

Group structure Management

Davide Usberti Chief Executive Officer

Paolo Tedesco Chief Financial Officer and responsible for the preparation of the company’s financial reporting

Giovanni Baroni Director Corporate Business Development and Investor Relator

Achille Capelli Director of Network Business Unit

Davide Cornaggia Director of Supply&Sales and Retail Business Units

Luigi Diamante Director of Exploration&Production Business Unit

Cinzia Triunfo Responsable of General Affairs and Storage Business Unit

Gian Maria Viscardi Network CEO

Giovanni Dell'Orto Chairman International B&P

Other Group's Executives

GAS PLUS MIBTEL

Gas Plus SpA

Gas PlusItaliana SpA

Gas PlusEnergia Srl

Gas PlusVendite Srl

Gas PlusReti Srl

Gas PlusStorage Srl

E&PBusiness

Unit

S&SBusiness

Unit

StorageBusiness

Unit

NetworkBusiness

Unit

RetailBusiness

UnitOther

100% 100% 100% 96.1% 85%

Disclaimer

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Gas Plus. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involveknown and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from thoseexpressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Gas Plus to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘intend’’, ‘‘may’’, ‘‘plan’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘probably’’, ‘‘project’’, ‘‘will’’, ‘‘seek’’, ‘‘target’’, ‘‘risks’’, ‘‘goals’’, ‘‘should’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Gas Plus and could cause those results to differ materially from those expressed in the forward-looking statements included in this Report, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for the Group’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserve estimates; (f) loss of market and industry competition; (g)

1111

currency fluctuations; (d) drilling and production results; (e) reserve estimates; (f) loss of market and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including potential litigation and regulatory effects arising from recategorisation of reserves; (k) economic and financial market conditions in various countries and regions; (l) political risks, project delay or advancement, approvals and cost estimates; and (m) changes in trading conditions.All forward-looking statements contained in this presentation are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Each forward-looking statement speaks only as of the date of this presentation. Neither Gas Plus nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated,implied or inferred from the forward-looking statements contained in this presentation.