iiarf research report contrasting grc and erm documents/contrasting grc... · iiarf research report...

TRANSCRIPT

I I A R F R e s e A R c h R e p o R t

Contrasting GRC and ERM

Perceptions and Practices Among Internal Auditors

The IIA Research Foundation 2

Copyright © 2013 by The Institute of Internal Auditors Research Foundation (IIARF). All rights reserved.

Published by The Institute of Internal Auditors Research Foundation, 247 Maitland Avenue, Altamonte Springs, Florida, 32701-4201. (www.theiia.org/research)

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any means—electronic, mechanical, photocopying, recording, or otherwise—without prior written per-mission of the publisher. Requests to the publisher for permission should be sent electronically to: [email protected] with the subject line “reprint permission request.”

Limit of Liability: The IIARF publishes this document for informational and educational purposes and is not a substitute for legal or accounting advice. The IIARF does not provide such advice and makes no warranty as to any legal or accounting results through its publication of this document. When legal or accounting issues arise, professional assistance should be sought and retained.

The Institute of Internal Auditors’ (IIA’s) International Professional Practices Framework (IPPF) compris-es the full range of existing and developing practice guidance for the profession. The IPPF provides guid-ance to internal auditors globally and paves the way to world-class internal auditing.

The IIA and The IIARF work in partnership with researchers from around the globe who conduct valuable studies on critical issues affecting today’s business world. Much of the content presented in their final reports is a result of IIARF-funded research and prepared as a service to The IIARF and the internal audit profession. Expressed opinions, interpretations, or points of view represent a consensus of the researchers and do not necessarily ref lect or represent the official position or policies of The IIA or The IIARF.

eISBN-13: 978-0-89413-808-9

18 17 16 15 14 13 1 2 3 4 5 6 7 8 9

www.theiia.org/research 3

Contents

Acknowledgments 4

About the Authors 6

Executive Summary 7

Chapter 1 From Internal Controls to Risk 8

Chapter 2 A Global Survey about GRC and ERM 11

Chapter 3 The Evolution of Internal Audit Toward Governance 15

Chapter 4 The Many Definitions of GRC 18

Chapter 5 The Many Definitions of ERM 24

Chapter 6 Developing a Working Relationship Between

Governance and ERM 27

Chapter 7 Perceived Meanings of GRC and ERM 29

Chapter 8 GRC and ERM Maturity 36

Chapter 9 Value Perception of GRC and ERM 42

Chapter 10 Improving GRC and ERM 47

Chapter 11 Internal Audit Involvement in GRC and ERM 53

Chapter 12 Audit Planning 62

Chapter 13 Risk Assessments 65

Chapter 14 Frameworks and Tools 69

Chapter 15 Conclusion and Implications 74

Appendix A Survey Questions 76

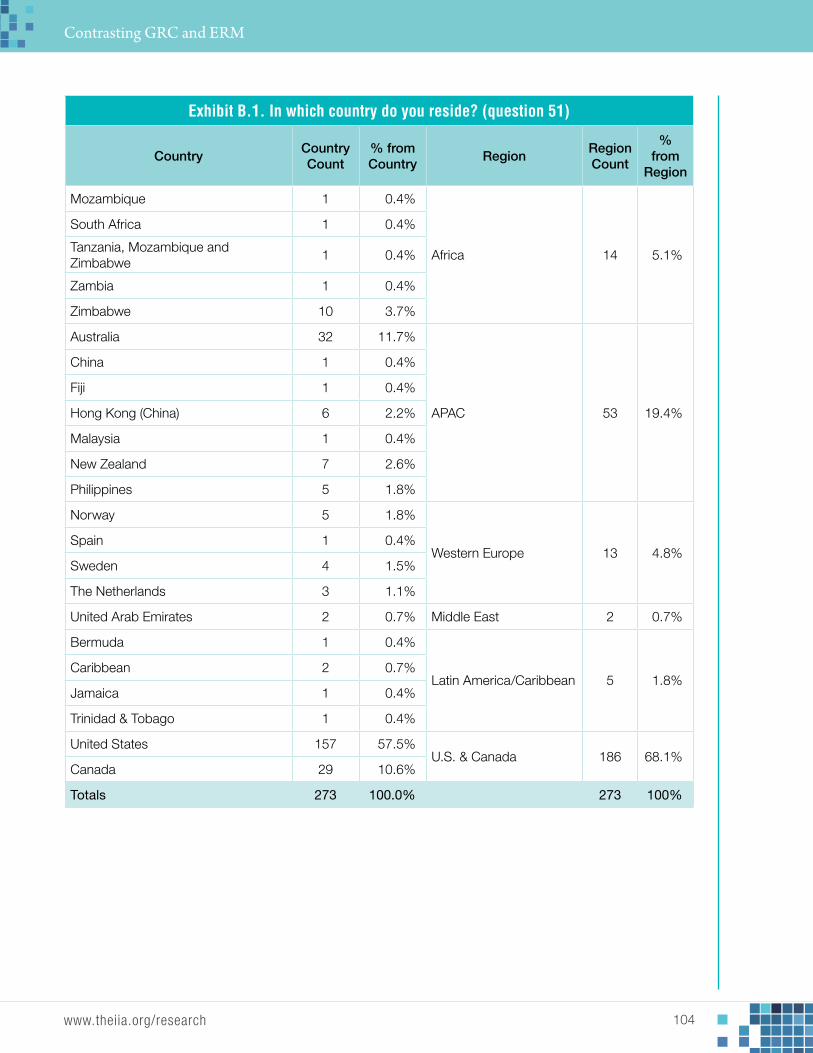

Appendix B Demographics of Research Participants 103

Appendix C Execution and Oversight Responsibilities 109

Appendix D Areas Identified/Referenced in the Internal Audit Charter 111

Appendix E Extent of Your Internal Audit Function’s Involvement in GRC 113

Appendix F Extent of Your Internal Audit Function’s Involvement in ERM 115

Appendix G Frequency that Internal Audit Function Reports on

GRC to Audit Committee 117

Appendix H Frequency of Internal Audit Function Assessment of

GRC and ERM 119

Notes 121

Reference List 124

Research Sponsor Recognition 125

The IIA Research Foundation Board of Trustees 126

The IIA Research Foundation Committee of Research and Education Advisors 127

www.theiia.org/research 4

ACknowledgments

We thank the following Institute of Internal Auditors’ (IIA) chapters for their generous donations in support of this project:

Albany (Gold Partner)

Southern New England (Silver Partner)

Westchester-Fairfield (Silver Partner)

Downeast Maine (Silver Partner)

We are also thankful for the active and ongoing contributions of multiple IIA institutes who supported the research by distributing the survey within their regions, including:

Australia

Hong Kong

Netherlands

New Zealand

North America

Norway

Philippines

South Africa

Sweden

United Arab Emirates (UAE)

Zimbabwe

We would like to thank the following reviewers for their comments and suggestions for this project:

Lal Balkaran, Risk, Governance, and Internal Audit Consultant, LBA Consulting

Adil Buhariwalla, Vice President Internal Audit, Emirates Airline

Jack Gazlay, Principal, Risk Assessment Services, LLC

Bruce C. Lynn, Managing Partner, The FECG, LLC

The IIA Research Foundation 5

In addition, Urton Anderson, professor of accounting at the University of Texas and current chairman of The IIA’s Committee of Research and Education Advisors (CREA), provided significant top-down comments that were important to the overall completion of the project.

We also offer special thanks to Selma Kuurstra, Stra Global Consulting, who coordinated meetings and feedback and managed the project schedule. We also appreciate Mike Scotchie of The IIA for survey distribution, monitoring, and data collection. For editorial support, we appreciate Deborah Poulalion, IIARF project content developer, for valuable suggestions regarding organization and presentation.

Several individuals accepted our invitation to answer follow-up questions regarding the survey instrument and results, and their insights are included in this report. These respondents include:

Richard Anderson, Clinical Professor of Strategic Risk Management, DePaul University

Steven Casazza, Vice President and Controller, Nestlé Purina PetCare, Global Strategic Business Unit

Todd Freeman, Vice President, Internal Audit, CB&I (Chicago Bridge & Iron Company N.V.)

Michael Head, Vice President and Managing Director of Corporate Audit, TD Ameritrade, Inc.

Joel Kramer, Managing Director, Internal Audit Division, MIS Training Institute

Barry S. Leithhead, Risk Professional, Australia

Roger McDaniel, President, Audit Services

Betty McPhilimy, Associate Vice President, Audit and Advisory Services, Northwestern University

José Luis Rojas, Business Advisory Services Managing Partner, Grant Thornton, Mexico

Anton Van Wyk, Partner, PwC, South Africa

Joyce Vassiliou, Head of Internal Audit, Coca-Cola Hellenic Bottling Company S.A., Greece

Finally, we extend our appreciation to current and former IIA team members who helped develop and distribute the survey and our sincere thanks to the hundreds of internal audit professionals who took the time to respond.

Acknowledgments

www.theiia.org/research 6

About the Authors

Lydia M. Lafleur, CIA, is assistant director of the Center for Internal Auditing at Louisiana State University where she teaches financial accounting and internal auditing. Lydia has more than 10 years of professional experience in public accounting and the banking industry. She has co-authored several articles about internal audit topics and conducted Certified Internal Auditor (CIA) exam reviews and presentations for organizations and chapters of The Institute of Internal Auditors (IIA) throughout the United States.

Jared S. Soileau, PhD, CIA, CPA, CISA, CCSA, CRMA, is assistant professor of accounting at Louisiana State University where he teaches accounting information systems and internal auditing. Jared’s academic credentials include a bachelor of science degree in accounting with a concentration in internal auditing, a master of business administration with a concentration in internal auditing from Louisiana State University, and a doctorate in business administration with a concentration in accounting from the University of Memphis. He received The IIA’s Esther R. Sawyer Award in 2003 and the Michael J. Barrett Doctoral Dissertation Award in 2010. His research interests include internal auditing, corpo-rate governance, and enterprise risk management.

Prior to receiving his advanced degrees, Jared had an extensive career in internal auditing and infor-mation systems auditing in both public accounting and industry, working at Ernst & Young LLP, Alcatel Inc., Avery Dennison, and FedEx Services. Jared also provides CIA exam training throughout the United States. He is an active member of The IIA and currently serves on the Academic Relations Committee.

Glenn E. Sumners, DBA, CIA, CFE, CRMA, is on the faculty of Louisiana State University and serves as the director of the Louisiana State University Center for Internal Auditing (LSUCIA). Glenn was named Educator of the Year in 1987 by The IIA and received the LCPA Lifetime Achievement in Accounting Education Award in 1999. In 2006, he received The IIA’s Bradford Cadmus Memorial Award, and in 2012, he was inducted into The IIA’s American Hall of Distinguished Audit Practitioners. Glenn is a member of The IIA Society Emeritus. He is an honorary faculty member at the University of Pretoria. Five LSUCIA students have received the Esther R. Sawyer Award and 18 have won interna-tional awards for the highest score on the CIA exam. In 2012, the CIA Student Award for the top score on the exam by a student was named the Dr. Glenn E. Sumners Award.

Glenn has been actively involved with The IIA for more than 30 years and has served on numerous committees. He provides quality assurance reviews, consulting, and training to internal audit groups and audit committees internationally, and has made more than 1,300 presentations over the last 25 years.

The IIA Research Foundation 7

exeCutive summAry

Governance, risk, and control (GRC) and enterprise risk management (ERM) are two topics frequently discussed within the business community. This research study explores the perceptions

about the meanings of GRC and ERM and internal audit’s involvement. The findings provide insight into strategic steps for the internal audit profession as a whole, plus useful perspectives for practitioners.

Researchers used The IIA’s extensive network of internal audit contacts around the world to conduct a survey involving 23 countries. Many of the results were interpreted through follow-up interviews with internal audit experts in the field of GRC. Finally, the researchers conducted a review of current publica-tions about GRC and ERM to describe current thinking on the topic.

Key findings include:

While most internal auditors describe ERM as a component of GRC (60%), a significant proportion had the opposite viewpoint—that GRC was a component of ERM (24%).

Approximately four out of 10 respondents described ERM (39%) or GRC (44%) in their organizations as ad hoc or preliminary.

Significant percentages of respondents indicated that their internal audit functions did not conduct assessments of governance (25%) or ERM (34%).

Seventy-seven percent of respondents indicated that their organizations have a process for establishing risk tolerance levels, whether formal or informal.

Approximately two-thirds (63%) of respondents used a top-down, risk-based approach for internal audit planning compared to one-third (33%) who used a risk-ranked units, bottom-up approach.

For many questions in the survey, respondents gave almost identical answers for GRC and ERM, suggesting a lack of differentiation between the concepts.

In conclusion, this report provides a snapshot of internal audit’s expanding roles in risk, ERM, and governance. To meet existing and future challenges, the internal audit profession would benefit by clar-ifying the concepts and language relative to GRC and ERM.

www.theiia.org/research 8

Chapter 1

From internAl Controls to risk

“If you wish to converse with me, define your terms.”

—VoltaIre

In 1984, The IIA Research Foundation (IIARF) commissioned a study titled Internal Auditing: Directions and Opportunities. The foremost conclusion of the study was that the profession of internal

auditing was “well-established but not well-defined.” The only consistent similarity among practitioners was that internal auditors everywhere were involved in the evaluation of internal controls. 1

During the same time frame, business leaders began to look at ways to define internal controls. The Report of the National Commission on Fraudulent Financial Reporting, published in 1987, noted that management, audit committees, internal auditors, external auditors, and other groups varied greatly in their perceptions and definitions of internal control. The commissioners recommended that the Committee of Sponsoring Organizations of the Treadway Commission (COSO) establish a language of internal controls.

In 1992, COSO published Internal Control – Integrated Framework, which is now used worldwide to provide a common language about internal control for internal auditors, management, and others.2 This common language is an important tool for evaluating and facilitating communication about internal controls between different groups and individuals.

As the internal audit profession has evolved, new job enrichment responsibilities have been added, especially increased involvement in governance and risk. As a result, governance, risk, and control (GRC) and enterprise risk management (ERM) are concepts increasingly discussed and communicated in the business community. The interpretation of these terms differs across entities and geographies, creating a challenge for sharing knowledge and identifying best practices.

For example, the acronym ERM is often used interchangeably with GRC by many practitioners and software vendors. This lack of distinction decreases the transparency to external parties relative to the scope of professional services and responsibilities of internal auditors.

In the same way that COSO’s Internal Control – Integrated Framework established a language for controls, internal auditors and stakeholders need a clear and concise definition of GRC and ERM and a related language of governance.

As a result, nearly 30 years after the need to define internal control was identified, The IIARF commissioned this research study to determine whether the same definitional challenges exist with GRC and ERM. This research report is based on:

A review of current publications regarding GRC and ERM.

The IIA Research Foundation 9

A global survey of GRC and ERM with participants from 23 countries.

Interviews with leading internal audit experts to interpret survey results.

researCh QuestIons

This study was designed to answer the following questions about perceptions and practices related to GRC and ERM:

Perception from Key Sources

How has the evolution of risk and governance impacted the internal audit profession? (chapter 3)

How do key sources define GRC and ERM? (chapters 4 and 5)

How do key sources describe the relationship between GRC and ERM? (chapter 6)

Perception from Internal Auditors

How do internal auditors define GRC and ERM? (chapter 7)

How do internal auditors perceive the maturity of GRC and ERM in their organizations? (chapter 8)

How do internal auditors define the value of GRC and ERM? (chapter 9)

How do internal auditors think GRC structures and ERM processes can be improved? (chapter 10)

Practices among Internal Auditors

What is the current level of internal audit involvement in GRC and ERM? (chapter 11)

How do internal auditors incorporate ERM into their audit planning? (chapter 12)

Which risk assessment approaches do internal auditors use? (chapter 13)

What frameworks, tools, and technology do internal auditors currently use for GRC and ERM? (chapter 14)

BenefIts of the researCh for PraCtItIoners

Practitioners can use the results of this research project to:

Manage Perceptions

Learn how internal audit has evolved toward risk and governance. (chapters 3–6)

Communicate the meaning of GRC and ERM more clearly to management. (chapter 7)

From Internal Controls to Risk

www.theiia.org/research 10

Contrasting GRC and ERM

Benchmark their organization’s GRC and ERM maturity. (chapter 8)

Communicate the value of GRC and ERM to stakeholders. (chapter 9)

Learn how other internal auditors say GRC structures and ERM processes can be improved. (chapter 10)

Improve Practices

Compare the level of internal audit involvement in GRC and ERM with other respondents worldwide. (chapter 11)

Learn how other audit functions incorporate ERM into their audit plans. (chapter 12)

Learn what risk assessment approaches other audit functions use. (chapter 13)

Determine what frameworks, tools, and technologies other organizations use for GRC and ERM. (chapter 14)

The IIA Research Foundation 11

Chapter 2

A globAl survey About grC And erm

This research report was written based on the results of a global survey using The IIA’s extensive network of internal audit contacts. Researchers interpreted many of the survey results by conducting

follow-up interviews within the field of governance, risk, and control. Finally, they conducted a review of current literature on the topic to present current thinking. This chapter describes the characteristics of the global survey respondents and lists the internal audit leaders who were interviewed.

CharaCterIstICs of the GloBal surVey

The IIA Research Foundation (IIARF) administered the survey to chief audit executives (CAEs) and managers in 23 countries during the six-week period between February 7, 2012, and March 19, 2012. The survey language was English. (For the complete text of the survey, see appendix A.)

Of the 1,055 individuals who accessed the survey, 931 answered at least one question and 273 completed the survey in its entirety (see exhibit 2.1).

Exhibit 2.1. Countries Participating in the Survey

United Arab Emirates

The Netherlands

Sweden

South Africa

Philippines

Norway

New Zealand

Malaysia

Hong Kong (China)

Caribbean

Canada

Australia

Other

United States

The "Other" category includes Bermuda, Fiji, Jamaica, Mozambique, Spain, Trinidad & Tobago, Zambia, and Tanzania.

57%

7%12%

11%

1%

0%

2%

2%

1% 1%

1%0%

2%

3%

www.theiia.org/research 12

Contrasting GRC and ERM

Job TitlesIn terms of job title, 89% of respondents held positions of audit manager or higher (see exhibit 2.2).

The survey was directed toward chief audit executives (CAEs), but they also had the option to delegate it to a lower staff member for completion. The high percentage of executives among respondents is a benefit for this study because this indicates that the results ref lect a higher level of experience.

Exhibit 2.2. What is your current role in the internal audit function? (question 52)

title Percentage of respondents

Chief audit executive 55%

director of audit* 13%

Audit manager* 21%

other 11%

* Includes IT audit with respective title (for example, IT audit director or manager). Note: This question had 273 respondents.

Organization TypesCAEs of publicly traded companies comprised the greatest percentage of respondents completing

the survey (39%), while privately held organizations and public sector/government classified organiza-tions represented 21% and 22% respectively. In addition, nonprofit, service providers/consultants, and other organization types provided 11%, 4%, and 3% of the survey responses respectively, as noted in exhibit 2.3.

Exhibit 2.3. For which type of organization do you currently work? (question 48)

organization type Percentage of respondents

Publicly traded (listed) organization 39%

Public sector/government 22%

Privately held (non-listed) organization 21%

nonprofit 11%

service provider/consultant 4%

other 3%

Note: This question had 272 respondents.

Additional detailed information related to the respondents’ demographics is provided in appendix B, including:

Geographic composition

Size of organization (based on revenues)

Industry grouping

The IIA Research Foundation 13

Size of internal audit function

Limitations

A Note about Response Counts on Tables and FiguresResponse counts differ from question to question because all respondents did not answer every

question. Results provided in the main text of the paper are reported in aggregate for all responses received (not just completed surveys).

follow-uP InterVIews wIth Internal audIt exPerts

In addition to the global survey, the research team interviewed or surveyed prominent internal audit and risk management professionals during the 2012 IIA International Conference. Additional interviews were conducted remotely. These professionals represented multiple countries, including the United States, Australia, Mexico, and South Africa.

Researchers obtained feedback by presenting respondents with specific summarized results and asking for their perspective. Their insights are included throughout the study. The researchers are grateful to the following professionals for their participation:

Richard Anderson, Clinical Professor of Strategic Risk Management, DePaul University

Steven Casazza, Vice President and Controller, Nestlé Purina PetCare, Global Strategic Business Unit

Todd Freeman, Vice President, Internal Audit, CB&I (Chicago Bridge & Iron Company N.V.)

Michael Head, Vice President and Managing Director of Corporate Audit, TD Ameritrade, Inc.

Joel Kramer, Managing Director, Internal Audit Division, MIS Training Institute

Barry S. Leithhead, Risk Professional, Australia

Roger McDaniel, President, Audit Services

Betty McPhilimy, Associate Vice President, Audit and Advisory Services, Northwestern University

José Luis Rojas, Business Advisory Services Managing Partner, Grant Thornton, Mexico

Anton Van Wyk, Partner, PwC, South Africa

Joyce Vassiliou, Head of Internal Audit, Coca-Cola Hellenic Bottling Company S.A., Greece

A Global Survey about GRC and ERM

www.theiia.org/research 14

Contrasting GRC and ERM

reVIew of PuBlIshed MaterIals

Researchers reviewed internal audit history and current publications to identify and describe the most current trends related to GRC and ERM. The next section describes those trends and provides essential background information for interpreting the survey results presented later in this report.

The IIA Research Foundation 15

Chapter 3

the evolution oF internAl Audit towArd governAnCe

how has the evolution of risk and governance impacted the internal audit profession?

Governance has become increasingly important for the internal audit profession. Society recog-nizes that weak governance allows fraud, corruption, and man-made disasters to adversely impact

individuals and organizations. Accordingly, boards are looking for ways to increase their oversight of governance, and they are asking internal audit to assess and report on their organizations’ gover-nance practices.

As stated in IIA guidance:

In today’s political and business environment, there is increasing focus on governance, risk management, and control. Strong governance systems are needed to better ensure that organizations will meet their objectives and stakeholder expectations… In fulfilling its oversight responsibilities, [the board] will look to the internal audit activity to provide it with assessments on the organization’s governance practices.1

This increased need for governance oversight has provided another opportunity for internal audit to add value to an organization.

uPdates In IIa StandardS

The 2013 changes to The IIA’s International Standards for the Professional Practice of Internal Auditing (Standards) also support the observation that internal audit is evolving from controls to risk to governance.2

For example, regarding the objectives that must be established for each engagement, Standard 2210.A3 now states:

Adequate criteria are needed to evaluate governance, risk management, and controls. (Underlined words were added in 2013.)

Also, Standard 2201 now states that in planning the engagement, internal auditors must consider:

www.theiia.org/research 16

Contrasting GRC and ERM

The adequacy and effectiveness of the activity’s governance, risk management, and control processes compared to a relevant control framework or model… (Underlined and deleted words were changed in 2013.)

a Model for InCreasInG Internal audIt Value

These important changes are illustrated in exhibit 3.1, which shows that as maturity in controls, risk, and governance increases, internal audit value also increases.

Exhibit 3.1. The Evolution Toward Increasing Value for Internal Audit

Controls

GovernanceRisk

GRC

Governanceexpertise integrated

with mature riskassessment andinternal controls

Already Mature

Integration of Governance, Risk, and Controls

Incr

easi

ng V

alue

of

Inte

rnal

Aud

it

Source: Adapted from Sumners Audit Services, GRC presentation materials.

ERM

Entity

Process

Unit

ControlEnvironment

Management

Controls

Control Activities

Now Developing Future Challenge

As illustrated, the evolution of the profession is to add value by integrating risk and governance expertise with mature internal controls. Let’s look at the three elements of the graphic individually.

ControlsThe graphic shows how controls have matured as internal audit has taken the following progression:

1. Control activities

2. Management controls (plan, organize, staff, direct, and monitor)

3. The control environment (ethical tone at the top, corporate culture, integration of policy and procedures into the employee mindset)

Control maturity impacts staffing competencies, report content, and ability to add value.

The IIA Research Foundation 17

RiskRisk is still somewhat in the developing stage and the goal is to move up the risk scale in the

following progression:

1. Unit risk

2. Process risk

3. Entity-level risk

4. Integration of the three risk components

The key is to develop a systematic continuous process that integrates ERM, entity risk, process risk, and unit risk from the top down to the bottom up and across the organization.

Integration of risk includes a systematic method for identifying, evaluating, and managing the plan of action. Ensuring that the risk universe captures risk throughout the organization helps communicate the assessed level of risk within various areas that may impact other units or divisions of the organiza-tion. Based on such integration, duplicate efforts should be minimized and increased information should result in better decision-making.

GovernanceAddressing governance is a future challenge of the profession, and the integration of GRC and ERM

is key to the progress of the profession. This is another reason why a common language and understanding of these concepts is critical. As ref lected in the updates to the Standards, the importance of adding value lies in internal audit’s ability to evaluate and report on organizational governance. Although governance failures have been the underlying commonality in significant organizational failures, this area remains a challenge to the continuing progress of the internal audit profession.

The next two chapters describe the many meanings that are currently being assigned to GRC and ERM, starting with GRC.

The Evolution of Internal Audit Toward Governance

www.theiia.org/research 18

Contrasting GRC and ERM

Chapter 4

the mAny deFinitions oF grC

how do key sources define GrC?

Imagine that you just met four internal audit practitioners who graduated in the last 10 years, and you have asked them to describe their education and careers. Here is what you might find:

Two have accounting degrees, one has a finance degree, and the fourth has a computer science degree.

One went to work for a Big 4 firm, two started in industry, and one went to work in government.

Two became Certified Internal Auditors (CIAs), one achieved the Certified Public Accountant (CPA) and Certified Information Systems Auditor (CISA) designations, and one is a Certified Government Auditing Professional (CGAP).

One primarily conducts Sarbanes-Oxley work, one performs external attest assignments, one performs operational audits, and one audits regulatory compliance.

Two belong to The IIA, one joined ISACA, and one joined the Association of Government Accountants (AGA).

Only two of the four are IIA members and attend IIA meetings and training.

One has changed jobs three times.

This example, in a simplistic way, ref lects the diversity and vitality of the internal audit profession across many facets. However, the challenge with this scenario is that diverse experiences typically do not lead to a common viewpoint. This would be especially true for complex risk and governance challenges. In fact, perspectives on these topics in professional literature vary widely.

This chapter discusses the primary viewpoints regarding the meaning of GRC.Key points include:

How governance is defined

How risk is defined

The IIA Research Foundation 19

Whether the “C” in GRC stands for controls or compliance

A succinct definition for GRC

Let’s start by looking at how professional organizations define governance.

workInG defInItIons of GoVernanCe

The meaning of governance lies at the heart of understanding GRC. The IIA’s definition:

Governance—The combination of processes and structures implemented by the board to inform, direct, manage, and monitor the activities of the organization toward the achievement of its objectives.

—From the Standards1

Another recent publication from The IIA, Advancing Organizational Governance by Dean Bahrman, provides a good summary of other important definitions of governance from around the world:2

Governance is the culture, values, mission, structure, and layers of policies, processes, and measures by which organizations are directed and controlled. Governance, in this context, includes but is not limited to the activities of the Board…

—From the Open Compliance and Ethics Group (OCEG)3

Corporate governance is the system by which companies are directed and controlled. Boards of directors are responsible for the governance of their companies… The responsibilities of the board include setting the company’s strategic aims, providing the leadership to put them into effect, supervising the management of the business, and reporting to shareholders on their stewardship…

—Cadbury Committee (1992)4

[Governance involves] a set of relationships between a company’s management, its board, its shareholders, and other stakeholders. Corporate governance also provides the structure through which the objectives of the company are set, and the means of attaining those objectives and monitoring performance are determined. Good corporate governance should provide proper incentives for the board and management to pursue objectives that are in the interests of the company and its shareholders and should facil-itate effective monitoring.

—The Organisation for Economic Co-Operation and Development (OECD)5

The Many Definitions of GRC

www.theiia.org/research 20

Contrasting GRC and ERM

Corporate governance is “the framework of rules, relationships, systems, and processes within and by which authority is exercised and controlled in corporations.” It encom-passes the mechanisms by which companies, and those in control, are held to account.6 Corporate governance inf luences how the objectives of the company are set and achieved, how risk is monitored and assessed, and how performance is optimized.”7

—Australian Securities Exchange8

It is interesting to note the variations in the definitions. While these definitions are based on several sources, they can be summarized effectively in this way:

Governance is the manner in which a board of directors (trustees) ensures an organiza-tion has structural integration to meet its objectives.

workInG defInItIons of rIsk

The next component of GRC is risk. To recognize the meaning of risk, it will suffice to review The IIA definitions from the Standards glossary:

Risk—The possibility of an event occurring that will have an impact on the achievement of objec-tives. Risk is measured in terms of impact and likelihood.

Risk Management—A process to identify, assess, manage, and control potential events or situa-tions to provide reasonable assurance regarding the achievement of the organization’s objectives.9

does the “C” stand for Controls or CoMPlIanCe?

The final component of GRC is the “C,” the meaning of which is a source of some debate. Some say it refers to controls, while others prefer compliance. A helpful comment on the relationship between controls and compliance in GRC was provided by Anton van Wyk, PwC advisory services leader in South Africa. He stated:

A properly integrated GRC (compliance) enhances the overall control environment allowing management to demonstrate to the board that the business is in control. So a strong interrelationship does exist between GRC and control.

In essence, van Wyk said that compliance “enhances” control, therefore implying that compliance is a subset of control. If that is the case, then the “C” in GRC would refer to control (with compliance as a subset of control).

A careful reading of the definitions of control and compliance in The IIA’s Standards is consistent with this perspective.

Control—Any action taken by management, the board, and other parties to manage risk and increase the likelihood that established objectives and goals will be achieved.

The IIA Research Foundation 21

Management plans, organizes, and directs the performance of sufficient actions to provide reasonable assurance that objectives and goals will be achieved.

Compliance—Adherence to policies, plans, procedures, laws, regulations, contracts, or other requirements.

Note that controls are defined broadly as actions to mitigate risk, while compliance indicates a specific type of action—adherence to criteria. Therefore, compliance represents a subset of controls.

In addition, the 2013 revisions to the Standards use the phrase “governance, risk management, and control processes” in multiple places.10

Enterprise Risk Management by Paul Sobel and Kurt Reding offers a helpful diagram that shows internal control as a subset of ERM and governance.11

Exhibit 4.1. Governance, ERM, and Internal Control

Governance

ERM

InternalControl

Source: Paul Sobel and Kurt Reding, Enterprise Risk Management (The Institute of Internal Auditors Research Foundation, 2012), 20.

The Many Definitions of GRC

www.theiia.org/research 22

Contrasting GRC and ERM

The following exhibit provides a visual model of the integration of ERM within the GRC structure.

Exhibit 4.2. GRC — ERM Integration Overview

Governance

Risk

ERM

ComplianceControls

Residual Risk

Source: Louisiana State University, Center for Internal Auditing, GRC course materials.

The Control EnvironmentThere is one other term related to control that is often not understood—the control environment.

It is important to recognize the difference between hard controls (such as regulations) and soft controls (such as the control environment). Following is The IIA’s definition of control environment:

Control Environment—The attitude and actions of the board and management regarding the importance of control within the organization. The control environment provides the discipline and structure for the achievement of the primary objectives of the system of internal control. The control environment includes the following elements:

Integrity and ethical values

Management’s philosophy and operating style

Organizational structure

Assignment of authority and responsibility

Human resource policies and practices

Competence of personnel

The quality of governance, risk, and control is dependent upon the control environment.

The IIA Research Foundation 23

a suCCInCt defInItIon of GrC

Based on the discussion above, GRC could be succinctly defined as follows:

GRC is the manner in which a board of directors (trustees) ensures an organization attempts to meet its objectives by identifying and managing risks and obtaining assur-ance that controls (including compliance) are in place and efficiently and effectively mitigating risk.

As noted within our previous definition, risk management is a component of GRC. With perhaps an acceptable definition of GRC in place, the next chapter addresses the chal-lenge of defining ERM and discusses the debate about whether ERM fits under the broad governance umbrella of GRC.

The Many Definitions of GRC

www.theiia.org/research 24

Chapter 5

the mAny deFinitions oF erm

how do key sources define erM?

The definitions of ERM are more challenging to identify than the definitions of governance. In 2006, the authors of The Essentials of Risk Management stated:

For all the hype, however, ERM continues to be an elusive concept that varies widely in definition and implementation…1

In 2010, the authors of Enterprise Risk Management: An Introduction and Overview concluded that:

Our final observation is that the ERM concept is still a new concept and is likely to take a while to get the emerging country firms to reach the desirable level of risk management practices for sound business reasons rather than as a new responsibility that needs to be practiced because of law.2

how do ProfessIonal orGanIzatIons defIne erM?

Following are the most visible definitions of ERM available today. The Risk Management Society (RIMS) defines ERM as:

Enterprise Risk Management (“ERM”) is a strategic business discipline that supports the achievement of an organization’s objectives by addressing the full spectrum of its risks and managing the combined impact of those risks as an interrelated risk portfolio.

ERM represents a significant evolution beyond previous approaches to risk management in that it:

1. Encompasses all areas of organizational exposure to risk (financial, operational, reporting, compliance, governance, strategic, reputational, etc.);

2. Prioritizes and manages those exposures as an interrelated risk portfolio rather than as individual “silos”;

3. Evaluates the risk portfolio in the context of all significant internal and external environments, systems, circumstances, and stakeholders;

The IIA Research Foundation 25

4. Recognizes that individual risks across the organization are interrelated and can create a combined exposure that differs from the sum of the individual risks;

5. Provides a structured process for the management of all risks, whether those risks are primarily quantitative or qualitative in nature;

6. Views the effective management of risk as a competitive advantage; and

7. Seeks to embed risk management as a component in all critical decisions throughout the organization.3

Other definitions of ERM from around the world include:

[Risk management is] an integral part of all organizational processes. [It] is not a stand-alone activity that is separate from the main activities and processes of the organization. Risk management is part of the responsibilities of management and an integral part of all organizational processes, including strategic planning and all project and change management processes.

—The Council of Standards Australia (November 2009) and the Council of Standards New Zealand (October 2009)4

[ERM is] a structured, consistent and continuous process across the whole organization for identifying, assessing, deciding on responses to and reporting on opportunities and threats that affect the achievement of its objectives.

—The IIA–UK and Ireland5

Enterprise risk management is a process, effected by an entity’s board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives.

—COSO’s Enterprise Risk Management – Integrated Framework, 20046

a suCCInCt defInItIon of erM

Based on the current literature, following is a succinct definition for ERM:

ERM is an integrated systematic process of identifying major risk to achieving the specific goals and objectives of the organization. These risks should be analyzed by like-lihood and impact and mitigated to an acceptable level of residual risk.

The Many Definitions of ERM

www.theiia.org/research 26

Contrasting GRC and ERM

ConClusIon

Though there may be a lack of consensus on the meaning of GRC and ERM, these terms are being used extensively, and the relationship between these concepts is also being developed. The next chapter suggests a future working relationship for these two concepts.

The IIA Research Foundation 27

Chapter 6

develoPing A working relAtionshiP between governAnCe And erm

how do key sources describe the relationship between GrC and erM?

Because the definitions of GRC and ERM are so varied, the understanding of the relationship between the two concepts is extremely varied as well. Some practitioners propose that when ERM is fully

implemented, it would include GRC. Others feel strongly that the “R” (Risk) in GRC includes ERM.A diplomatic observation about the relationship between ERM and GRC is provided in The IIA’s

classic reference book, Sawyer’s Guide for Internal Auditors:

It is not appropriate to think that one is superior to the other or that either ERM or GRC is right or wrong from a professional perspective. GRC is not complete without abun-dant, reliable information about risk, nor is ERM relevant or useful unless it is rooted in governance, compliance, and business performance.1

Sawyer’s guide also indicates that ERM comes under the umbrella of GRC, stating, “Internal audi-tors should recognize the value of ERM and how it can be integrated with GRC.”

Paul Sobel, vice president/chief audit executive at Georgia-Pacific LLC and a known leader in ERM research, firmly states that ERM is a component of governance:

ERM is an important component of governance [just as] internal control is an important component of ERM.2

If ERM is a component of governance, then ERM would also be a component of GRC. Michael Rasmussen, vice president of enterprise risk and compliance for Forrester Research,

summarized the roles of GRC and ERM as follows:

GRC is really a philosophy, and a framework for communicating around governance and compliance issues; ERM, on the other hand, is the measurement and qualification of risk, and the establishment of individual risk ownership. In effect, GRC encompasses ERM.3

Stated another way, ERM varies based on the quality of governance; however, the quality of gover-nance is not based on the quality of ERM. The quality of the ERM process is more dependent on the quality of governance than governance is dependent on ERM.

www.theiia.org/research 28

Contrasting GRC and ERM

Risk management expert Douglas Hubbard noted that governance has control over ERM because governance determines “where risk management sits in the organization.”4

GoVernanCe as a struCture and erM as a ProCess

Another way to understand the relationship between governance and risk is to look carefully at The IIA’s definitions (note italicized words).

Governance—The combination of processes and structures implemented by the board to inform, direct, manage, and monitor the activities of the organization toward the achievement of its objectives (italics added).

Risk Management—A process to identify, assess, manage, and control potential events or situations to provide reasonable assurance regarding the achievement of the organiza-tion’s objectives (italics added).5

Note that governance is defined as “a combination of processes and structures.” On the other hand, risk management is described only as a “process.”

One can therefore infer that the process of risk management is managed through the structure of governance. In other words, governance provides the cultural infrastructure for the process of ERM. As the results of the survey will demonstrate, this perspective on the relationship between GRC and ERM is not universal, creating confusion for stakeholders and internal auditors.

The IIA Research Foundation 29

Chapter 7

PerCeived meAnings oF grC And erm

how do internal auditors define GrC and erM?

One of the impetuses of this study was the frequent and interchangeable use of the acronyms GRC and ERM. As a result, attempting to capture the current understanding of these terms within the

profession provides a starting point to fulfill the research objectives.

Is erM a CoMPonent of GrC or VICe Versa?

As mentioned earlier, it is possible to make a strong case for ERM being a component of GRC. However, this point of view is not necessarily a consensus among practitioners. Although 60% of survey respondents indicated ERM is a component of GRC, approximately 25% indicated the opposite—that GRC is a component of ERM; 14% chose “neither,” which indicates that they may not have established a defined relationship between GRC and ERM (see exhibit 7.1).

Exhibit 7.1: In your opinion, is ERM a component of GRC, or GRC a component of ERM? (question 28)

Other, please specify:

Neither

ERM is a component of GRC

GRC is a component of ERM

60%

14% 24%

2%

www.theiia.org/research 30

Contrasting GRC and ERM

Several respondents chose the “other” option and provided comments, including:

They are equal.

They should be combined in one process.

[I] would probably not label the approaches as discrete.

Todd Freeman, vice president of internal audit at CB&I (Chicago Bridge & Iron Company N.V.), offered the following statement as a potential explanation for the significant number of respondents indi-cating GRC as a component of ERM:

Whether a person is in internal audit or not, ERM is the phrase used by many to discuss initiatives by many organizations. For those not familiar with GRC, it may be a natural inclination to believe GRC and its risk component is a subset of an ERM initiative. Those more familiar with these terms may surmise that risk identification, assessment, and mitigation are a component of governance, risk, and control.

CoMMonalItIes and dIfferenCes Between GrC and erM

The survey obtained more insight into respondents’ viewpoints by asking them to subjectively identify commonalities and differences between GRC and ERM.

Commonalities between GRC and ERMQuestion 29 of the survey asked participants to “identify five commonalities of GRC and ERM.”

Respondents overwhelmingly indicated the commonalities were:

Risk

Risk identification

Risk assessment

The risk management process

The emphasis on risk was expected because both acronyms include the letter “R” for the word Risk. Other commonalities listed by respondents included:

Specific types of compliance

External audit

Internal audit

Code of ethics

The IIA Research Foundation 31

Several respondents said that there is no difference between GRC and ERM, one specifi-cally responding:

The distinction is entirely brought about as a consequence of consultants or experts wishing to sell a product…

One respondent summarized by stating:

Both concepts have generated a lot of frustration and confusion.

Differences between GRC and ERMRespondents were also asked to “Identify five differences between GRC and ERM” (survey ques-

tion 30). Since the respondents could not depend on the commonality of the word risk for their responses, their answers varied significantly. Here is a sample of the comments received:

GRC is tactical or operational (lower level); whereas ERM is strategic (higher level).

GRC also promotes positives such as ethical behavior as opposed to only managing risk.

[The difference is the] parties responsible for execution and oversight.

GRC is more encompassing as it includes governance and compliance.

GRC is corporate; ERM can be applied at a lower level.

ERM is periodic; GRC is continuous.

GRC is primarily a software vendor driven invention that has had little practical success or value. ERM, if done right, can be a major source of success for any organization.

GRC creates the control environment and its activities, while ERM complements GRC with respect to best performance.

ERM is detailed; GRC is overarching and less detailed. GRC can happen unintentionally while ERM is deliberate.

You can cover ERM through a fully functional GRC, but you couldn’t cover GRC with a fully functional ERM.

The lack of consensus on the differences provides additional evidence as to the lack of a common understanding for these two concepts.

Perceived Meanings of GRC and ERM

www.theiia.org/research 32

Contrasting GRC and ERM

To summarize, respondents appear to consider GRC to be associated with:

Ethical behavior

Evolving infrastructure

The control environment

Overarching scope

In contrast, respondents appeared to view ERM as:

Periodic rather than a continuous process

Applied at lower levels

Not including governance and compliance

These responses also indicate that some respondents align GRC with COSO’s Internal Control – Integrated Framework, and ERM with COSO’s ERM framework. While there are alternatives to the COSO models, the high response rate from the United States and Canada and the association of COSO with U.S.-based organizations may contribute to this observation. The lack of commonalities in the iden-tified differences again illustrates the lack of consensus regarding integration between ERM and GRC.

aCtIVItIes ClassIfIed as GrC, erM, or Both

Another way to determine how respondents defined GRC and ERM was to ask them to decide whether certain activities were part of GRC, ERM, or both.

As noted in exhibit 7.2, in general, most of the activities were classified as a component of both GRC and ERM. Several of the items indicated as both GRC and ERM were expected to only be identified as either GRC or ERM. Specifically, “independent internal audit function” was not expected to be asso-ciated with ERM. However, 66% of respondents indicated that an independent internal audit function was either ERM (9%) or Both (57%). Several other activities that were unexpectedly classified as both include “external audit process,” “establishment of code of conduct/ethics/corporate policy,” and “moni-toring of fraud hotline.”

Even general topics such as governance, risk, compliance, and internal controls were most frequently categorized as both GRC and ERM. While risk should clearly fall within both GRC and ERM, one would expect that governance, compliance, and internal controls should be more aligned with GRC.

The IIA Research Foundation 33

Exhibit 7.2. Indicate whether the following is a component of GRC, ERM, or both [and identify the person or group with execution and oversight responsibilities for each of the following]: (question 5)

activity GrC erM Both

Alignment of company actions with shareholder value 28% 15% 56%

Compliance 36% 9% 55%

ensuring ethical business transactions 42% 8% 50%

establishment of code of conduct/ethics/corporate policy 47% 7% 46%

external audit process 47% 8% 45%

evaluation of controls to ensure proper risk management 21% 24% 55%

governance 45% 7% 48%

independent internal audit function 34% 9% 57%

internal controls 26% 10% 64%

management of environmental, health, and safety concerns 26% 23% 51%

management of regulatory compliance 36% 10% 54%

management of risk within established tolerance levels 13% 33% 54%

monitoring of effective fraud hotline process 47% 13% 40%

risk 8% 27% 65%

setting and monitoring of organizational risk tolerance level 13% 36% 51%

organizationwide assurance 30% 11% 59%

Quality control process 32% 14% 53%

Note: Percentage totals may not equal 100% due to rounding. Between 432 and 517 responses were received for each activity.

Perceived Meanings of GRC and ERM

www.theiia.org/research 34

Contrasting GRC and ERM

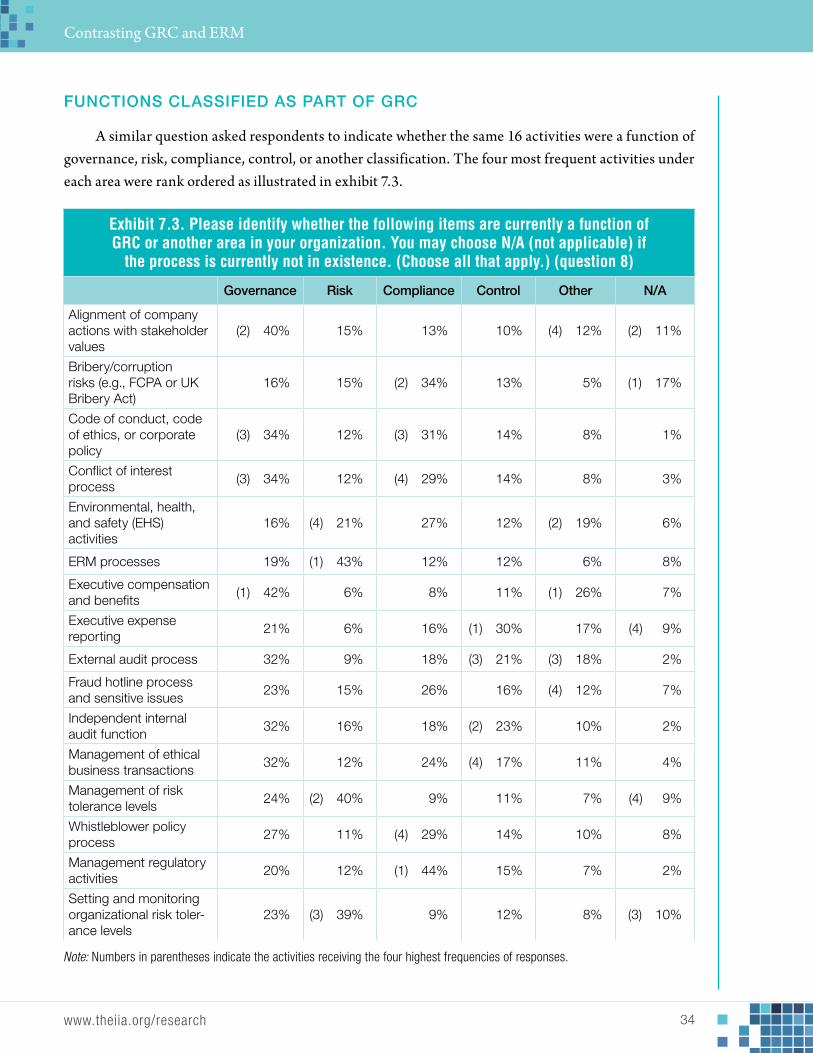

funCtIons ClassIfIed as Part of GrC

A similar question asked respondents to indicate whether the same 16 activities were a function of governance, risk, compliance, control, or another classification. The four most frequent activities under each area were rank ordered as illustrated in exhibit 7.3.

Exhibit 7.3. Please identify whether the following items are currently a function of GRC or another area in your organization. You may choose N/A (not applicable) if

the process is currently not in existence. (Choose all that apply.) (question 8)

Governance risk Compliance Control other n/a

Alignment of company actions with stakeholder values

(2) 40% 15% 13% 10% (4) 12% (2) 11%

bribery/corruption risks (e.g., FCPA or uk bribery Act)

16% 15% (2) 34% 13% 5% (1) 17%

Code of conduct, code of ethics, or corporate policy

(3) 34% 12% (3) 31% 14% 8% 1%

Conflict of interest process

(3) 34% 12% (4) 29% 14% 8% 3%

environmental, health, and safety (ehs) activities

16% (4) 21% 27% 12% (2) 19% 6%

erm processes 19% (1) 43% 12% 12% 6% 8%

executive compensation and benefits

(1) 42% 6% 8% 11% (1) 26% 7%

executive expense reporting

21% 6% 16% (1) 30% 17% (4) 9%

external audit process 32% 9% 18% (3) 21% (3) 18% 2%

Fraud hotline process and sensitive issues

23% 15% 26% 16% (4) 12% 7%

independent internal audit function

32% 16% 18% (2) 23% 10% 2%

management of ethical business transactions

32% 12% 24% (4) 17% 11% 4%

management of risk tolerance levels

24% (2) 40% 9% 11% 7% (4) 9%

whistleblower policy process

27% 11% (4) 29% 14% 10% 8%

management regulatory activities

20% 12% (1) 44% 15% 7% 2%

setting and monitoring organizational risk toler-ance levels

23% (3) 39% 9% 12% 8% (3) 10%

Note: Numbers in parentheses indicate the activities receiving the four highest frequencies of responses.

The IIA Research Foundation 35

Following are some of the notable observations regarding the responses:

“Management of regulatory activities” was most frequently classified as compliance (by 44% of respondents). Respondents probably reasoned that while this activity could be viewed as a risk, management’s need to comply with a regulation should most likely be classified as a compliance (with regulation) activity.

The “alignment of company actions with stakeholder values” is, to a large extent, the definition of governance; therefore, it would be expected that respondents would be much less likely to give a response other than governance. However, only 40% of the respondents selected governance.

“Executive compensation and benefits” was considered a governance activity by 42% of respondents, while “executive expense reporting” was viewed as a control activity by 30%.

Although the “independent internal audit function” and “external audit process” were each classified as governance activities by 32% of respondents, each was also frequently classified as control activities (23% and 21% respectively). Including internal audit under controls would be consistent with COSO’s internal control model, which includes internal audit as a component of the control environment.

Though the activities are worded in a way that provides room for respondent interpretation, the responses raise additional questions related to how members of the profession consider various activities that are a part of GRC and ERM.

For example, analysis of the rankings as well as percentages indicates that respondents identify two activities (“code of conduct, code of ethics, or corporate policy,” and “conf lict of interest process”) highly within both Governance and Compliance classifications in their organizations. It would have been expected that respondents would have chosen one or the other but not both. This provides addi-tional evidence of an absence of consistency in classification within components of the GRC structure.

ConclusionAlthough the majority of respondents (60%) indicated that ERM is a component of GRC, a

significant percentage (40%) of respondents had an alternative view. Additional questions about the components of GRC and ERM revealed further differences in perspective.

With consideration of the differences in respondent perceptions, in the next chapter we discuss the respondents’ perception of their organizations’ maturity related to GRC and ERM.

Perceived Meanings of GRC and ERM

www.theiia.org/research 36

Chapter 8

grC And erm mAturity

how do internal auditors perceive the maturity of GrC and erM in their organizations?

This section provides a summary of questions related to the maturity of organizational GRC activities and ERM processes. The responses show that:

Approximately four out of 10 respondents described ERM (39%) or GRC (44%) in their organizations as ad hoc or preliminary.

Respondents gave almost identical maturity ratings for GRC and ERM, which suggests a lack of differentiation between the two concepts.

Respondents indicated that more of their internal audit charters included governance (73%) than ERM (43%).

Respondents also indicated that more of their audit committee charters included governance (77%) than ERM (62%).

ERM was included in 19% more audit committee charters than internal audit charters.

Following is a detailed description of the results for questions on this topic.

MaturIty leVels of GrC and erM ProCesses

Respondents were asked to rate the maturity of their organization’s current GRC structure and ERM processes using the following scale.

Ad hoc—Undocumented; state of dynamic change; individual experiences.

Preliminary—Risk defined in different ways, in silos.

Defined—Common risk framework. Organizationwide view of risk. Action plans imple-mented in response to high priority risks.

Integrated—ERM activities coordinated. Common tools and processes, with enter-prisewide risk monitoring, measurement, and reporting. Scenario planning and process metrics in place.

The IIA Research Foundation 37

Optimized—Risk discussion embedded in strategic planning, capital allocation, and permeates into daily decision-making. Early warning system to notify board and management to risks above established thresholds.

Respondents consistently rated GRC and ERM at approximately the same maturity level (see exhibit 8.1).

Exhibit 8.1. Based on the [following] five maturity model classifications, rate your organization’s maturity of current ERM and GRC processes. (question 4)

ERM Maturity

GRC Maturity

13%16%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

26%28%

39%

36%

19%

17%

4% 4%

Ad hoc DefinedPreliminary Integrated Optimized

N = 850 respondents for ERM maturity and 895 responses for GRC maturity

Note: As a result of rounding, totals may exceed 100%.

Given that GRC and ERM are different, although related, the expectation would be that maturity levels would be independent of each other; however, they were highly correlated.1 It is unlikely that GRC and ERM are at the same level of maturity for so many respondents. One possible explanation is that respondents did not differentiate between the two concepts. In other words, respondents considered GRC and ERM to be the same or similar.

Additional analysis showed that the maturity levels of both GRC and ERM were positively correlated with the size of the internal audit function. This was especially true at the optimized level. Notably, the correlation was stronger for the size of the internal audit function than for revenue. This suggests the possibility that larger internal audit staff size has a positive impact on the maturity of GRC and ERM.

GRC and ERM Maturity

www.theiia.org/research 38

Contrasting GRC and ERM

Perspective from Active Internal Audit LeadersLet’s consider possible reasons why many respondents indicated that GRC or ERM maturity in

their organizations was ad hoc or preliminary. Regarding low GRC maturity, José Luis Rojas, partner at Grant Thornton (Mexico), suggested that

many respondents have not yet recognized that strong GRC adds value to the business:

There has been a great push driven by regulators, bankers and shareholders toward adopting better governance structures that integrate risk management and compliance, but companies still have to realize that it is not a cost but a business driver and that trans-parency and good governance add value to their investments.

Regarding low ERM maturity, Rojas commented that, similar to GRC perceptions, many organiza-tions do not recognize that strong ERM adds value beyond regulatory compliance:

Most organizations still have an internal control process based on models such as COSO and CoCo [criteria of control] and are more concerned with complying with regula-tions rather than adopting best practices because they do not see the value added from a comprehensive ERM approach. It is important for governing institutions and collegiate bodies to spread such culture.

Similarly, Barry Leithhead, a consultant for governance, risk management, and internal auditing in Australia, stated that organizations are not embracing ERM because “they haven’t realized that it’s a profit-maker, not an overhead cost.”

Regarding the relatively low percentage of respondents who indicated maturity levels as integrated or optimized for GRC (21%) or ERM (23%), Steven Casazza, vice president and controller of Nestlé PetCare, confirmed:

[I have] not really seen any organization that has a highly integrated GRC model. [When] networking at conferences, I have yet to find anyone who has embedded GRC into the core DNA of the organization.

Internal audIt Charters

Another way to assess the maturity of GRC or ERM in an organization is to see whether these concepts are referenced in the internal audit charter and/or the audit committee charter. First, we’ll look at what respondents said about internal audit charters.

Internal audit responsibilities, as defined within their charter or the audit committee charter, generally focus more on controls and risk than on governance. This was consistent with the results about the internal audit charter (see exhibit 8.2).

The IIA Research Foundation 39

Exhibit 8.2. Are the following areas identified or referenced in your internal audit charter? (question 34)

yes no

governance 73% 27%

Control environment 88% 12%

risk 88% 12%

erm 43% 57%

specific internal controls 57% 43%

Compliance 87% 13%

Assurance services 61% 39%

extent of advisory services 56% 44%

mandatory audits 36% 64%

N = 266 respondents

Note: See appendix D for more detailed analysis by demographic groupings.

The elements that were most frequently included in the internal audit charter were:

Risk (88%)

Control environment (88%)

Compliance (87%)

Approximately seven out of 10 internal audit charters also included governance, but ERM was included in less than half:

Governance (73%)

ERM (43%)

Note that there was a gap of 30% between internal audit charters that included governance (73%) and internal audit charters that included ERM (43%). The lower percentage for ERM is probably due to organizations in the study that did not have an ERM process. The responses for the audit committee charters had a similar gap but not as extensive (see comments regarding exhibit 8.3).

audIt CoMMIttee Charters

Now that we’ve seen responses regarding the internal audit charter, let’s look at the audit committee charter. Historically, audit committees have been relied upon to provide oversight of the financial reporting process and results. This oversight responsibility for publicly traded companies creates a significant relationship between audit committees and external auditors. At the same time, the audit

GRC and ERM Maturity

www.theiia.org/research 40

Contrasting GRC and ERM

committee maintains oversight of the internal audit function—in many cases through a direct reporting relationship. As a result of these roles and the increased need for oversight of risk management, ERM processes also have frequently fallen under the purview of the audit committee.

Please see exhibit 8.3 for an overview of the governance and risk elements that respondents said were included in their organizations’ audit committee charters.

Exhibit 8.3. Are the following roles identified in your audit committee charter? (question 2)

roles formal Informal no unknown

governance 57% 20% 15% 9%

Control environment 59% 22% 11% 9%

risk 63% 19% 10% 8%

erm 36% 26% 28% 10%

Controls 70% 16% 7% 8%

Compliance 63% 19% 10% 8%

Assurance oversight 69% 13% 9% 9%

N = 914 respondents Note: As a result of rounding, totals may exceed 100%.

As indicated in exhibit 8.3, the elements that were most frequently included in the audit committee charter (formally and informally) were:

Controls (86%)

Risk, compliance, assurance oversight (82% for each)

Control environment (81%)

Governance (77%)

ERM (62%)

Note that there was a gap of 15% between inclusion of governance (77%) and inclusion of ERM (62%) in the audit committee charter. Possible reasons are that governance has been in place much longer than ERM. Also, governance is a more general term and therefore is more likely to be included to some extent in charters, whereas ERM, especially in the COSO context, is much more specific. Additionally, many organizations have not implemented ERM, and the ones that have may have assigned oversight to the entire board or a board committee other than the audit committee (for example, a risk committee).

Additional analysis showed that organizations with higher revenue and/or larger internal audit staff size were more likely to have governance and ERM roles identified within the audit committee charter.

The IIA Research Foundation 41

Comparing Internal Audit Charters and Audit Committee ChartersThere were some similarities and differences between the internal audit charters and the audit

committee charters worth noting:

Governance was included in audit committee charters (77%) and internal audit charters (73%) at about the same rate.

Audit committee charters are more likely to include ERM (62%) than internal audit charters (43%).

These differences exist even though the perceived maturity levels for GRC and ERM were almost identical (see exhibit 8.1).

Best practices charters are a factor as a criteria in a quality assessment review. The charter should ref lect the activities and role of the internal audit function. It is critical to reference governance, risk (ERM), and control in the audit committee and internal audit charters.

GRC and ERM Maturity

www.theiia.org/research 42

Chapter 9

vAlue PerCePtion oF grC And erm

how do internal auditors define the value of GrC and erM?

Value perception is an important component of the relationship between internal audit, management and the audit committee. The survey included several questions about value and areas of effective-

ness for GRC and ERM from internal audit’s perspective. Key findings include:

Internal auditors say that internal stakeholders’ top expectations for GRC and ERM are to reduce operational risk, organizational risk, financial reporting risk, and strategic risk, while enhancing the organization’s reputation.

Internal auditors perceive ERM as most effective at addressing financial risk and least effective at addressing governance risk.

In reference to the components in the definition of internal auditing, internal auditors rated their effectiveness at adding value in the following order (from highest to lowest): 1) controls, 2) compliance, 3) risk, 4) governance.

Internal stakeholder exPeCtatIons of BenefIts froM GrC and erM aCtIVItIes

The nature of a GRC or ERM program in an organization will be shaped by the expectations of internal stakeholders. Survey respondents were asked to indicate their stakeholders’ expectations regarding the benefits they expected from GRC or ERM activities. Exhibit 9.1 lists the benefits that were presented in the question, plus the responses for both GRC and ERM.

The IIA Research Foundation 43

Exhibit 9.1. Indicate your level of agreement. Internal stakeholders expect the following benefits associated with GRC activities (question 9)/ERM activities (question 16).

Benefits expectedGrC erM

sd* d* n* a* sa* sd* d* n* a* sa*

enhanced business strategy

3% 5% 29% 49% 14% 2% 6% 25% 54% 11%

enhanced reputation* 2% 3% 14% 50% 30% 1% 2% 20% 56% 20%

improved benchmarking 3% 8% 40% 38% 10% 2% 9% 44% 40% 6%

improved financial performance

4% 11% 29% 45% 13% 2% 11% 29% 47% 10%

improved market performance

3% 15% 46% 28% 7% 3% 13% 48% 29% 7%

lower financial reporting risk*

2% 3% 18% 53% 24% 2% 5% 21% 57% 15%

lower financial volatility 3% 10% 33% 44% 10% 2% 10% 34% 45% 8%

lower market volatility 5% 18% 47% 25% 4% 3% 15% 51% 27% 4%

lower operational risk* 2% 2% 12% 59% 25% 1% 2% 6% 62% 29%

lower organizational risk* 1% 1% 14% 59% 24% 1% 2% 10% 61% 26%

lower strategic risk* 2% 4% 21% 52% 22% 1% 1% 15% 60% 23%

reduced cost of capital 3% 15% 40% 34% 8% 2% 13% 44% 33% 8%

other 2% 2% 73% 14% 10% 5% 2% 60% 23% 10%

*SD = Strongly Disagree, D = Disagree, N = Neutral, A = Agree, SA = Strongly Agree

The respondents had few differences in their responses between GRC and ERM, even though the questions regarding GRC benefits and ERM benefits were separated by several questions within the survey (questions 9 and 16). While this may indicate a lack of differentiation between GRC and ERM, it also shows that internal auditors have a strong sense of what is most valuable to their stakeholders. See exhibit 9.2 for a summary of the top benefits internal stakeholders expect from GRC and ERM.

Exhibit 9.2. Internal Stakeholders’ Top Expectations for GRC and ERM (question 16 summary)

Benefits expected GrC erM

lower operational risk 84% 91%

lower organizational risk 83% 87%

enhanced reputation 80% 83%

lower financial reporting risk 77% 76%

lower strategic risk 74% 72%

Note: This table shows the percentage of internal auditors who agreed or strongly agreed that internal stakeholders expected the benefits. These are the top five percentages for GRC and ERM.

Value Perception of GRC and ERM

www.theiia.org/research 44

Contrasting GRC and ERM

effeCtIVeness of erM at addressInG dIfferent tyPes of rIsk

Because ERM is emerging as a new component in many organizations, it is interesting to see how the internal audit respondents assessed the effectiveness of ERM for addressing various risks. Respondents were asked to evaluate the effectiveness of their organization’s ERM process to identify, assess, and manage 18 types of risk. Their responses indicate that financial risk is considered a top area of effectiveness, while governance was considered one of the lowest areas of effectiveness. See exhibits 9.3 and 9.4 for details.

Risks That Are Most Effectively Addressed Through ERMThe four risk types that respondents ranked as most effectively addressed within their ERM

processes were financial, regulatory, compliance, and operating. These rankings were fairly consistent across identification, assessment, and management (see exhibit 9.3).

Exhibit 9.3. Risks That Internal Auditors Perceive to Be Most Effectively Identified, Assessed, and Managed Through ERM (question 26)

Identified assessed Managed

Financial risk Financial risk Financial risk

regulatory risk regulatory risk regulatory risk

Compliance risk operating risk operating risk

operating risk Compliance risk Compliance risk

economic risk Credit risk reputational risk

it risk it risk Credit risk

legal risk reputational risk legal risk

Note: This table is based on question 26: How effective do you believe your current ERM process is at adequately identifying, assessing, and managing the following types of risk? The survey question asked respondents to rate effectiveness on a scale of low (1), medium (2), high (3). A weighted score was calculated based on the number of responses within each category times the rating. The risks with the highest weighted scores are included in this table.

Risks That Are Least Effectively Addressed Through ERMExhibit 9.2 shows the risks respondents ranked as least effectively addressed within their ERM

processes. Respondents consistently gave lower ratings for governance, cultural, vendor, human capital, and environmental risks.

The IIA Research Foundation 45

Exhibit 9.4. Risks That Internal Auditors Perceive to Be Least Effectively Identified, Assessed, and Managed Through ERM (question 26)

Identified assessed Managed

governance risk governance risk external risk

environmental risk vendor risk environmental risk

human capital risk environmental risk human capital risk

vendor risk human capital risk vendor risk

Cultural risk Cultural risk Cultural risk

Note: This table is based on question 26: How effective do you believe your current ERM process is at adequately identifying, assessing, and managing the following types of risk? The survey question asked respondents to rate effectiveness on a scale of low (1), medium (2), high (3). A weighted score was calculated based on the number of responses within each category times the rating. The risks with the lowest weighted scores are included in this table.

how well does Internal audIt add Value, alIGnInG wIth the defInItIon of Internal audItInG

The IIA’s definition of internal auditing states that internal audit will add value through the assess-ment of four key areas: governance, risk, controls, and compliance. Respondents were asked to identify how strongly they agree that the internal audit activity in their organization is bringing value in these four areas (see exhibit 9.5).

Exhibit 9.5. To what extent do you agree that internal audit activities within your organization are aligned with The IIA’s Definition of Internal

Auditing to add value through the assessment of: (question 35)

assessment of:strongly disagree

disagree neutral agreestrongly

agree

governance 4% 5% 15% 44% 32%

risk 3% 4% 11% 44% 38%

Controls 3% 1% 4% 41% 51%

Compliance 4% 4% 6% 49% 37%

N = 268 respondents

Value Perception of GRC and ERM

www.theiia.org/research 46

Contrasting GRC and ERM

The responses in exhibit 9.5 are remarkably parallel with the evolution of internal auditing described in chapter 3 (see exhibit 3.1). Historically, internal audit has progressed from assessing controls to risk to governance. Ref lecting that pattern, respondents scored themselves highest in controls and lowest in governance (see exhibit 9.6)

Exhibit 9.6. The Effectiveness of Internal Audit at Adding Value (question 36 - summary results)

assessment of:Percentage of respondents who agreed

or strongly agreed that internal audit adds value through the assessment of:

Controls 92%

Compliance 86%

risk 82%

governance 76%

Note: This table is based on responses to question 35: To what extent do you agree that internal audit activities within your orga-nization are aligned with The IIA’s Definition of Internal Auditing to add value through the assessment of:

Exhibit 9.6 indicates an opportunity to enhance the value-added proposition of internal audit by increasing the emphasis on governance.

Richard Anderson, Clinical Professor of Strategic Risk Management at DePaul University, commented that for internal audit to add more value in assessing governance, its role should be clearer:

There is a lack of clarity on exactly what governance encompasses on the part of both internal auditors and their organizations. As a result, it is not clear to stakeholders or audi-tors which governance processes and risks should be part of the scope of internal auditing.

Adding value to the organization will always be an area where internal audit will work to improve and expand. The next chapter highlights the survey respondents’ suggestions for improving GRC and ERM in an organization.

The IIA Research Foundation 47

Chapter 10

imProving grC And erm

how do internal auditors think GrC structures and erM processes can be improved?

This chapter reports the survey responses related to improving GRC and ERM in an organization. Key themes include:

Respondents were most positive regarding the impact of auditing ERM but most negative regarding the impact of leading the ERM process (see exhibit 10.1).