important points regarding submission of ...000 units and units sold 8,000 units at cost plus 12%...

TRANSCRIPT

IMPORTANT POINTS REGARDING SUBMISSION OF INTERNAL

PROJECTS.

1. DATE AND TIME OF SUBMISSION OF INTERNAL PROJECTS

AND VIVA – VOCE 22ND OF JULY 2017 AT 11 AM.

2. STUDENTS HAVE TO SUBMIT THE PROJECTS ON A4 SIZE

FULLSCAPE PAPER IN HANDWRITTEN FORM ONLY.

3. THEY HAVE TO REMAIN PRESENT IN PERSON.

4. THEY HAVE TO CARRY THEIR HALL TICKET OR FEE

RECEIPT (IF HALL TICKET NOT COLLECTED OR RECEIVED)

FOR THE VIVA- VOCE.

5. THEY HAVE TO WEAR FORMAL DRESS.

6. THEY HAVE TO ASSEMBLE IN THE RESPECTIVE CLASS

ROOM (AS MENTIONED ON THE WEBSITE).

7. THEY HAVE TO MAINTAIN DISCIPLINE DURING THE

PRESENTATION. ANY STUDENT FOUND MISBEHAVING MAY

BE SUSPENDED AND NECESSARY ACTION WILL BE TAKEN.

8. DISCRETION OF SUBJECT TEACHER IS FINAL AND NO CLAIM

WHATSOEVER WILL BE ENTERTAINED.

9. STUDENTS FAILING TO SUBMIT THE PROJECTS AND

APPEARING FOR VIVA-VOCE WILL BE DECLARED AS FAIL

IN THAT SUBJECT.

INTERNAL QUESTIONS

SEM I

SUBJECT: PRINCIPLES OF MANAGEMENT

Roll No. 31

Q.1 Explain the principles of Henry Fayol.

Q.2 Explain the process of planning.

Q.3 What are the factors affecting decentralization.

Q. 4 Write down the qualities of a good leader.

Q.5 Need for CSR.

Sem II

Subject: Introduction to Costing

Roll No. : 114

1. The accounts of A Manufacturing Ltd. For the year ended 31st December 2013 shows the

following:

PARTICULARS AMOUNT

Stock of Materials

1.1.2013

31.12.2014

Materials purchased

Drawing office salaries

General office salaries

Bad debts written off

Traveller’s salaries and commission

Depreciation written-off Office furniture

Plant, machinery and tools

Rent, rates, taxes and insurance:

Factory

Office

Productive wages

General expenses

Gas and Water:

Factory

Office

Travelling expenses

Sales

Manager’s salary

Cash discount allowed

Carriage outwards

Repairs on plant, machinery and tools

Direct expenses

67,200

87,920

2,59,000

9,100

17000

9,100

10,780

420

9,100

11,900

2,800

1,76,400

4,760

1,680

560

2,940

6,45,540

15,000

4.060

6,020

6,230

10,010

2. The profit as per cost accounts is Rs. 1,50,000. The following details are ascertained on comparison

of cost and financial accounts:

PARTICULARS COST A/C FINANCIAL A/C

Opening stocks:

Materials

Finished goods

Closing stock:

Materials

Finished goods

Interest charged but not paid

Write-off: preliminary expense Rs. 500, Goodwill Rs..

1,500

Dividend received from Unit Trust of India

Indirect expenses charged in financial accounts Rs.

80,000 but 75,500 recovered in cost accounts.

10,000

18,000

12,000

20,000

15,000

16,000

13,000

17,000

10,000

Find out the profit as per financial accounts by drawing up a reconciliation statement.

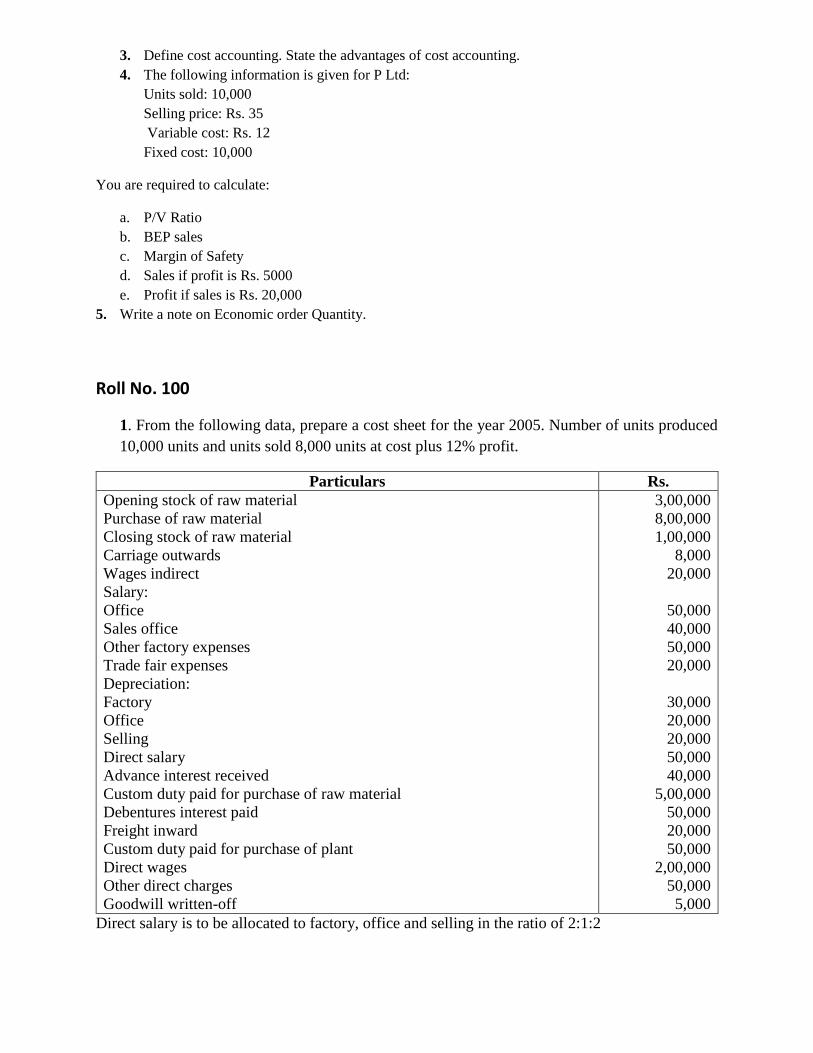

3. Define cost accounting. State the advantages of cost accounting.

4. The following information is given for P Ltd:

Units sold: 10,000

Selling price: Rs. 35

Variable cost: Rs. 12

Fixed cost: 10,000

You are required to calculate:

a. P/V Ratio

b. BEP sales

c. Margin of Safety

d. Sales if profit is Rs. 5000

e. Profit if sales is Rs. 20,000

5. Write a note on Economic order Quantity.

Roll No. 100

1. From the following data, prepare a cost sheet for the year 2005. Number of units produced

10,000 units and units sold 8,000 units at cost plus 12% profit.

Particulars Rs.

Opening stock of raw material

Purchase of raw material

Closing stock of raw material

Carriage outwards

Wages indirect

Salary:

Office

Sales office

Other factory expenses

Trade fair expenses

Depreciation:

Factory

Office

Selling

Direct salary

Advance interest received

Custom duty paid for purchase of raw material

Debentures interest paid

Freight inward

Custom duty paid for purchase of plant

Direct wages

Other direct charges

Goodwill written-off

3,00,000

8,00,000

1,00,000

8,000

20,000

50,000

40,000

50,000

20,000

30,000

20,000

20,000

50,000

40,000

5,00,000

50,000

20,000

50,000

2,00,000

50,000

5,000

Direct salary is to be allocated to factory, office and selling in the ratio of 2:1:2

2.The following information is presented to you from the costing and financial departments of

a manufacturing company:

PARTICULARS COST

RECORDS

FINANCIAL

RECORDS

Stores consumed

Works on cost

Works expenses

Office on cost

Office expenses

Net profit

2,00,000

75,000

42,700

97,500

2,02,000

80,500

37,000

95,700

You are to prepare a statement reconciling profit as per cost records with profit as per financial

records.

3.Define cost accounting. State the advantages of cost accounting.

4. Explain various types of cost.

5. Calculate Economic Order Quantity for the following:

a. Quantity – 10,000 units Ordering cost – Rs. 1,200 per order

Carrying cost – 20% Price per unit – Rs. 2,000

b. Annual requirement – 1,600 units Ordering cost – Rs. 50

Cost of material per unit Rs. 40 carrying cost – 10%

Roll No. 113

1. From the following information work out the production hour rate of recovery of overheads

in dept. A, B and C using repeated distribution method:

PARTICULARS TOTAL PRODUCTION DEPT. SERVICE DEPT.

A B C D E

Rent

Electricity

Fire insurance

Plant depreciation

Transport

Estimated working

hours

2,000

400

800

4,000

400

-

400

100

160

1000

50

-

800

160

320

1,500

50

1,000

300

60

120

1,000

50

2,500

300

40

120

300

100

1,800

200

40

80

200

150

-

Expenses of service department D and E are apportioned as under:

A B C D E

D 30% 40% 20% - 10%

E 10% 20% 50% 20% -

2. The following information is given for QR Ltd:

Units sold: 20,000

Selling price: Rs. 50

Variable cost: Rs. 20

Fixed cost: 30,000

You are required to calculate:

a. P/V Ratio

b. BEP sales

c. Margin of Safety

d. Sales if profit is Rs. 7,000

e. Profit if sales is Rs. 10,000

3. The following information is given for QR Ltd:

Units sold: 15,000

Selling price: Rs. 30

Variable cost: Rs. 13

Fixed cost: 30,000

You are required to calculate:

a. P/V Ratio

b. BEP sales

c. Margin of Safety

d. Sales if profit is Rs. 13,000

e. Profit if sales is Rs. 25,000

4. Write a note on Material.

5. Explain Labour.

SEM II

Subject: Environmental Management

Roll No. : 60

Write a note on following;

1. Components of environment

2. Biogeo chemicle cycle

3. Eco system 4. Food chain 5. pyramid

SEM III

SUBJECT: Accounting for Managerial Decision

Roll No. 2156

Q1) M/s. Radha Ltd carrying on business, furnished their position as on 31st March 2012,2013 & 2014.

Balance Sheet as on 31st March

Particulars 2012 2013 2014

Assets

Fixed Assets 30000 25500 43800

Investment 13000 13000 18400

Current Assets 27000 33200 18900

70000 71700 81100

Liabilities

Share Capital 33000 31350 41000

Debentures 27000 28350 9500

Liabilities for expenses 10000 12000 30600

70000 71700 81100

Prepare Trend Balance Sheet in vertical form.

Q2) Compute the Balance Sheet of Titanic Ltd.

Balance Sheet

Liability Amt Asset Amt

Share Capital 2000000 Fixed Assets ??

Reserves & Surplus ??? Current Assets

Loans 200000 Stock ??

Current Liabilities ?? Debtors ??

Cash ??

Total ?? Total ??

Ratios of the company are :

a) Reserves & Surplus to share capital ratio is 1:1.

b) Sales to Net worth Ratio is 1.5:1.

c) Sales to debtors ratio is 6:1.

d) G.P. Ratio 20% on sales.

e) Net working capital Rs 12lakhs.

f) Stock Turnover ratio 6times.

g) Current Ratio 2.5:1.

h) Acid Test ratio 1.5:1.

Q3) Explain in brief the main provisions of AS3.

Q4) Write a short note on Gross Working Capital & Net Working Capital.

Q5) Explain in brief Contingent Liabilities.

Roll No. 2076

Q1) M/s. Radha Ltd carrying on business, furnished their position as on 31st March 2014.

Balance Sheet as on 31/3/2014.

Particulars Amt Particulars Amt

Land & Building 600000 Misc. Current Assets 5000

Plant & Machinery 500000 P/L A/c. (Cr Bal) 200000

Equity Capital 500000 General Reserve 100000

Preference Capital 200000 Creditors 80000

Stock 240000 Bills Payable 60000

Debtors 200000 Misc. Current Liabilities 60000

Cash & Bank 55000 Debentures 400000

Prepare Common size from the above information.

Q2) Compute the Balance Sheet of Titanic Ltd.

Balance Sheet

Liability Amt Asset Amt

Share Capital 3000000 Plant & Machinery ??

Reserves & Surplus 4500000 Current Assets

Loans ?? Stock ??

Current Liabilities 1000000 Debtors ??

Cash ??

Total ?? Total ??

Ratios of the company are :

Debt Equity ratio is 1:2,Total Asset Turnover is 2/5,Inventory Turnover is 9times,Acid Test Ratio is 1,ACP

45days,Gross Profit Margin is 10%.Assume 360days/yr, 100%credit sales.

Q3) Explain in brief Importance & Classification of Cash Flow Statements.

Q4) Write a short note on Factors determining Working Capital.

Q5) Explain in brief Receivable Management.

SUBJECT: Organization Behavior and HRM

Roll No. 2144

Q.1 Explain the cross cultural dynamics in short.

Q.2 Explain retrenchment, downsizing, & layoffs in short

Q.3 What are the functions of HRD?

Q.4 Explain various methods of Performance Appraisal in detail.

Q.5 Explain the Career Planning Stages in detail

SUBJECT: Basics of Financial services

Roll No. 2098

1) Features of financial services

2) Money market.

3)Secondary functions of commercial banks.

4) Role & functions of RBI.

5) Functions of reinsurance.

SEM IV

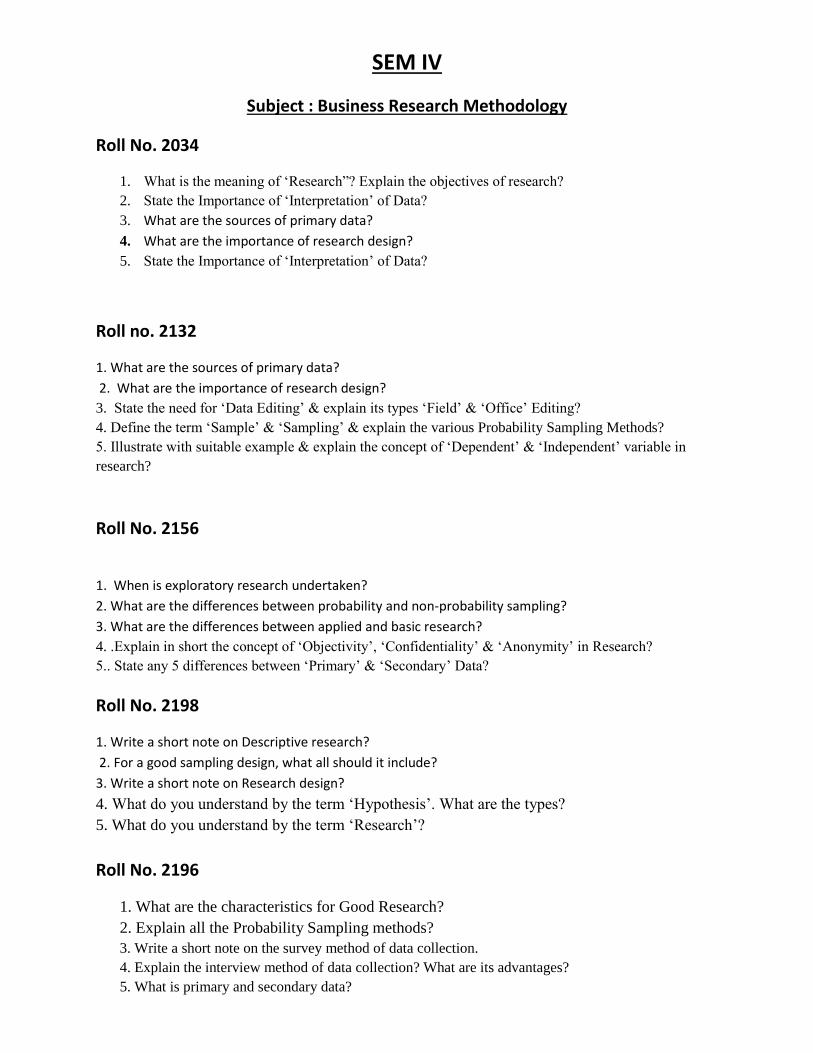

Subject : Business Research Methodology

Roll No. 2034

1. What is the meaning of ‘Research”? Explain the objectives of research?

2. State the Importance of ‘Interpretation’ of Data?

3. What are the sources of primary data?

4. What are the importance of research design?

5. State the Importance of ‘Interpretation’ of Data?

Roll no. 2132

1. What are the sources of primary data?

2. What are the importance of research design?

3. State the need for ‘Data Editing’ & explain its types ‘Field’ & ‘Office’ Editing?

4. Define the term ‘Sample’ & ‘Sampling’ & explain the various Probability Sampling Methods?

5. Illustrate with suitable example & explain the concept of ‘Dependent’ & ‘Independent’ variable in

research?

Roll No. 2156

1. When is exploratory research undertaken?

2. What are the differences between probability and non-probability sampling?

3. What are the differences between applied and basic research?

4. .Explain in short the concept of ‘Objectivity’, ‘Confidentiality’ & ‘Anonymity’ in Research?

5.. State any 5 differences between ‘Primary’ & ‘Secondary’ Data?

Roll No. 2198

1. Write a short note on Descriptive research?

2. For a good sampling design, what all should it include?

3. Write a short note on Research design?

4. What do you understand by the term ‘Hypothesis’. What are the types?

5. What do you understand by the term ‘Research’?

Roll No. 2196

1. What are the characteristics for Good Research?

2. Explain all the Probability Sampling methods?

3. Write a short note on the survey method of data collection.

4. Explain the interview method of data collection? What are its advantages?

5. What is primary and secondary data?

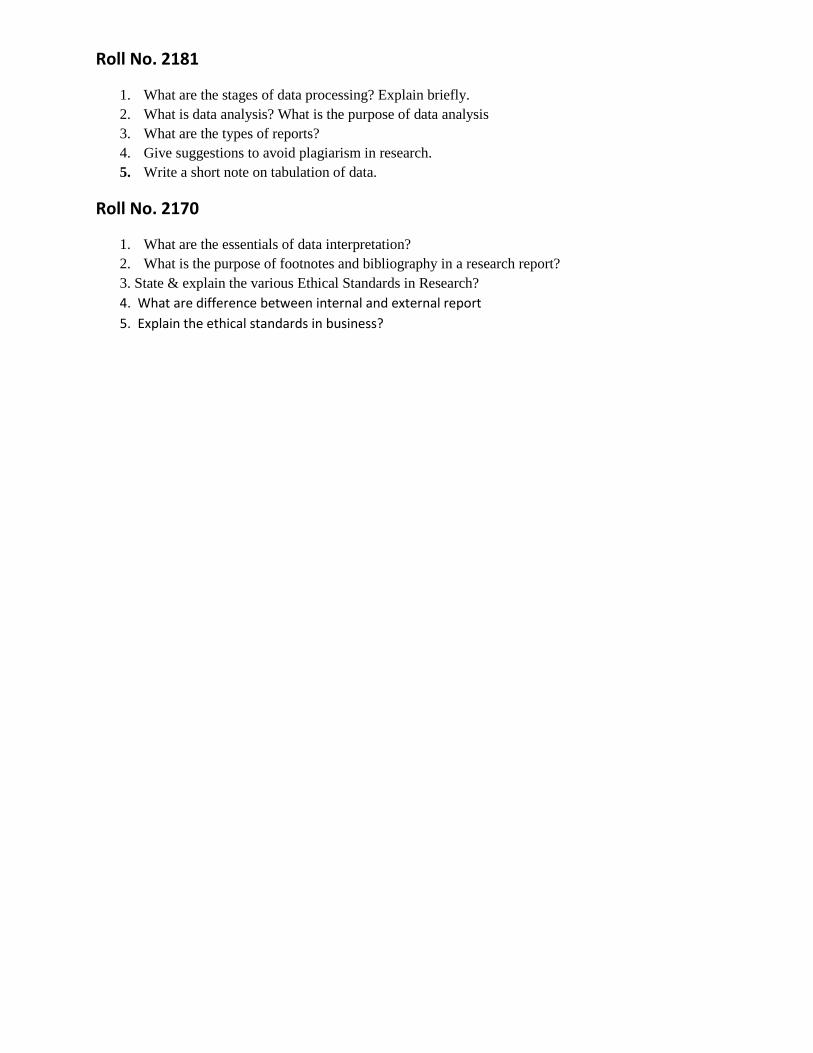

Roll No. 2181

1. What are the stages of data processing? Explain briefly.

2. What is data analysis? What is the purpose of data analysis

3. What are the types of reports?

4. Give suggestions to avoid plagiarism in research.

5. Write a short note on tabulation of data.

Roll No. 2170

1. What are the essentials of data interpretation?

2. What is the purpose of footnotes and bibliography in a research report?

3. State & explain the various Ethical Standards in Research?

4. What are difference between internal and external report

5. Explain the ethical standards in business?

SUB: ADVANCE COSTING

Roll No. 2042

1. Prepare necessary accounts from the following information:

Particulars Total Process P Process Q Process R

Material

Direct wages

Production overheads

1,50,840

1,80,000

1,80,000

82,000

40,000

39,600

60,000

59,240

80,000

10,000 units @ Rs. 6 per unit were introduced in process P.

Production overheads to be distributed as 100% of direct wages

Particulars Actual output Normal loss Scrap value

Process P

Process Q

Process R

9500

8400

7500

5%

10%

15%

4

8

10

2. Prepare contract account for the year ended 31st December, 2015 from the following information:

N ltd undertook a contract for Rs. 25,00,000 for construction ofa building.

Particulars Rs. Particulars Rs.

Material sent to contract

Labour

Plant installed

Direct expenses

Other charges

Materials returned to stores

Work certified

Value of plant at site on 31.12.15

8,47,860

7,41,520

1,50,000

32,010

48,780

5,520

19,50,000

1,10,000

Work uncertified

Material at site on 31.12.15

Wages accrued

Direct expenses accrued

Cash received

45,000

18,800

24,000

2,400

18,00,000

3. Calculate material variances from the following information:

For Standard output of 10kgs we need 50 units of material @ Rs. 5

Actual production = 1000kgs, material used 6000 @ Rs. 4.

4. Calculate labour variances from the following information:

Particulars Hours Rate

Standard output = 50 kgs

Actual output = 70 kgs

10

15

6

10

Also Calculate material variances from the following information:

Particulars Output Quantity Rate

Standard

Actual

25

75

50

55

10

20

5. Define audit. Explain the objectives of audit.

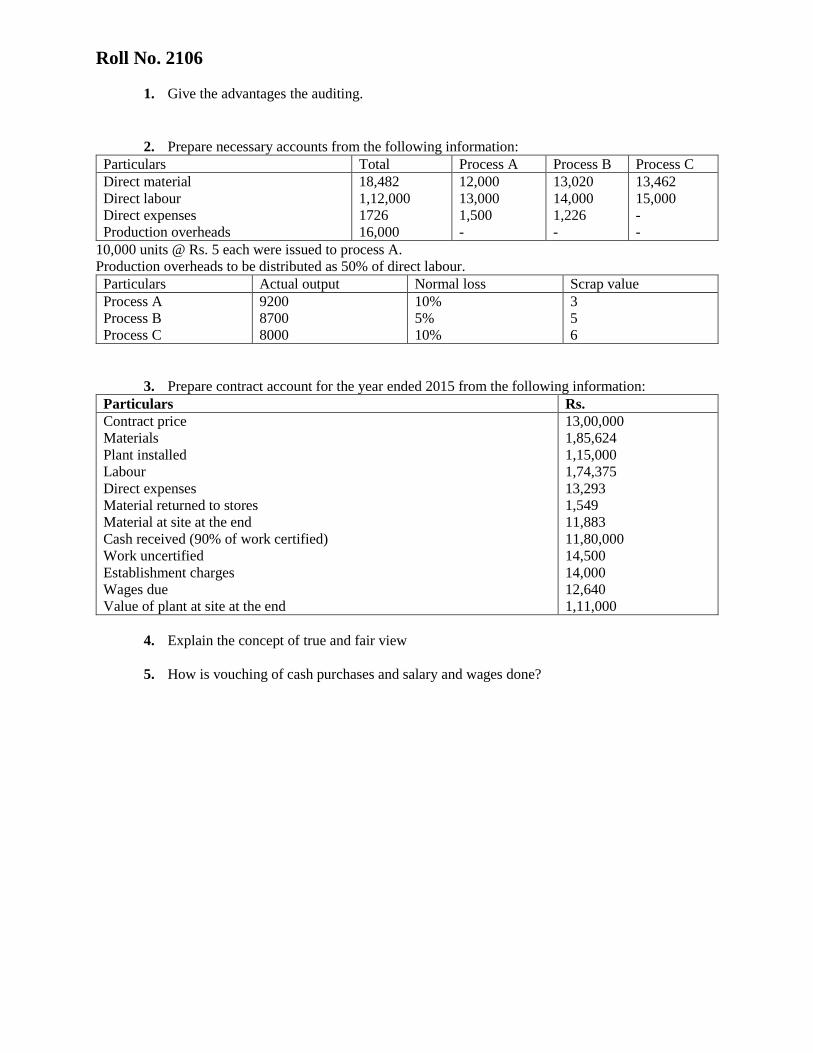

Roll No. 2106

1. Give the advantages the auditing.

2. Prepare necessary accounts from the following information:

Particulars Total Process A Process B Process C

Direct material

Direct labour

Direct expenses

Production overheads

18,482

1,12,000

1726

16,000

12,000

13,000

1,500

-

13,020

14,000

1,226

-

13,462

15,000

-

-

10,000 units @ Rs. 5 each were issued to process A.

Production overheads to be distributed as 50% of direct labour.

Particulars Actual output Normal loss Scrap value

Process A

Process B

Process C

9200

8700

8000

10%

5%

10%

3

5

6

3. Prepare contract account for the year ended 2015 from the following information:

Particulars Rs.

Contract price

Materials

Plant installed

Labour

Direct expenses

Material returned to stores

Material at site at the end

Cash received (90% of work certified)

Work uncertified

Establishment charges

Wages due

Value of plant at site at the end

13,00,000

1,85,624

1,15,000

1,74,375

13,293

1,549

11,883

11,80,000

14,500

14,000

12,640

1,11,000

4. Explain the concept of true and fair view

5. How is vouching of cash purchases and salary and wages done?

SUBJECT: PRODUCTION AND TOTAL QUALITY MANAGEMENT

ROLL NO. 2196

1. Distinguish between Intermittent and Continuous Production System.

2. What are the characteristics of Process Production?

3. Explain the different types of material handling systems.

4. Explain the most common equipments used in material handling.

5. Explain the GOLF analysis.

ROLL NO. 2139

1. Explain the factors affecting quality.

2. Explain the benefits of total quality management.

3. Explain the benefits of ISO 9000.

4. Explain the goals of SIX SIGMA.

5. Write short note on VED.

Subject: Equity and Debt Market

Roll no. 2042

Q. 1 Regulatory framework in the Indian Debt market.

Q.2 Divorce between ownership and management in companies.

Q.3 Red herring prospectus - unique features.

Q. 4 Stock exchanges in India

Q.5 Primary dealers in Govt. securities.

ROLL NO. 2033

Q.1 Which are the various participants involved in equity market?

Q.2. Explain benefits and importance of Listing.

Q. 3 Write a short note on STCI.

Q.4 Write a note on Zero Coupon Bonds.

Q.5 Who is Merchant banker? What is his role?

SUBJECT: INTEGRATED MARKETING COMMUNICATION AND ADVERTISING

ROLL NO. 2141

1. Explain features of integrated marketing.

2. Explain the merits of DAGMAR.

3. Explain the communication process.

4. Explain the types of sales promotion.

5. Explain the 5M’s of Advertising

ROLL NO. 2134

1. Explain the demerits of DAGMAR.

2. Explain the common types of trade promotion tools.

3. Explain the importance of public relations.

4. What is direct mail marketing?

5. Explain the advantages of direct marketing

ROLL NO. 2128

1. Explain the promotional tools for IMC.

2. Explain the types of publicity

3. What are the advertising strategies that are commonly used?

4. Explain the 5 key features of IMC.

5. What are the advantages of branding?

ROLL NO. 2198

1. What are the characteristics of outdoor advertising?

2. Explain the forms of out of home advertising.

3. Explain the evolution of an advertising agency.

4. What are the marketing functions of an advertising agency?

ROLL NO. 2157

1. Explain the formula of AIDA advertising.

2. What are the characteristics of good brand name?

3. Explain the guidelines for advertising directed to children.

4. Explain ethical pitfalls in advertising with regards to promotional

content.

5. Write short note on media research.

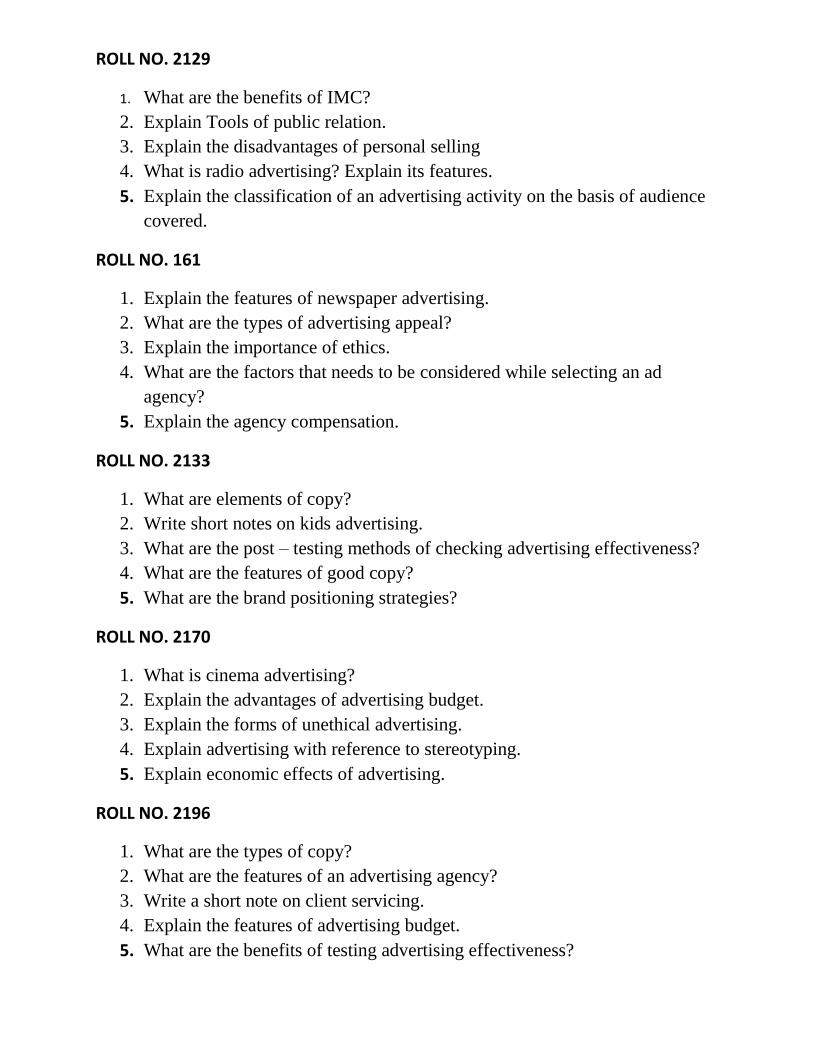

ROLL NO. 2129

1. What are the benefits of IMC?

2. Explain Tools of public relation.

3. Explain the disadvantages of personal selling

4. What is radio advertising? Explain its features.

5. Explain the classification of an advertising activity on the basis of audience

covered.

ROLL NO. 161

1. Explain the features of newspaper advertising.

2. What are the types of advertising appeal?

3. Explain the importance of ethics.

4. What are the factors that needs to be considered while selecting an ad

agency?

5. Explain the agency compensation.

ROLL NO. 2133

1. What are elements of copy?

2. Write short notes on kids advertising.

3. What are the post – testing methods of checking advertising effectiveness?

4. What are the features of good copy?

5. What are the brand positioning strategies?

ROLL NO. 2170

1. What is cinema advertising?

2. Explain the advantages of advertising budget.

3. Explain the forms of unethical advertising.

4. Explain advertising with reference to stereotyping.

5. Explain economic effects of advertising.

ROLL NO. 2196

1. What are the types of copy?

2. What are the features of an advertising agency?

3. Write a short note on client servicing.

4. Explain the features of advertising budget.

5. What are the benefits of testing advertising effectiveness?

SUBJECT : RURAL MARKETING

ROLL NO. : 2157

1. What are the efforts for Rural Development by Government?

2. Bring out the emerging profile of Rural Market in India.

3. Explain the Social factors which are affecting Consumer Behaviour

4. Explain PDS & Cooperative Societies in Rural Market

5. Case Study :After setting a firm foot in the urban market, Colgate was looking at tapping the

potential of the rural market. One of the reasons being the increase in literacy rate and continuously

growing awareness among village folks. Colgate’s life line has always been its high quality

products that have never failed to win customer’s trust. Now it needed to cater to the unattended

rural market. So with the motto of ‘Think global act local’ in mind, in 1998, it reached out to 6

million people in 20,000 villages of which 15,000 villages had not experienced the availability of

toothpaste or tooth powder. Mass media had worked well in the urban areas but the problem faced

in the rural compass was that very few people had access to television and radio. The need of the

hour was a scheme that would penetrate deep into the rural network and spread its roots throughout

this network. This challenge was encountered by Sampark’s Door to door selling program. The

program involved hiring people from various localities who could converse comfortably as well

as effectively in the local language and also make use of the local idioms and jargons. This ensured

effectual communication between the company and the consumers, thus reducing the

communication gap tremendously. So, even though the audience was scattered and had varied

languages, cultures and lifestyles it was insured that everyone got the right message from the

company. The local people were trained to go about the village informing the people about the

pros of advanced oral hygiene and throw light on the cons of traditional oral care system,

convincing them to use the free samples made available by Colgate. Again another ordeal came in

the form of the mindset of people who preferred natural over synthetic.

a) Bring out the importance of Mass Media in promoting the product in Rural Market?

b) Explain various Promotional Strategies in Rural Market?

SUBJECT : DIRECT TAX

ROLL No. : 2001

1. Mrs. Chang, a Japanese citizen had left India on 1st June, 2013 after a 10 years stay.

During the financial year 20114-15 she visited India and stayed for 56 days only. Later

she returned to India 14th May, 2015 and stayed until 10th September, 2015. She left for

Japan on 11th September, 2015. On 9th February, 2016 she visited India again and was

staying here until 31st March, 2016. Determine her residential status for the AY 2016-17.

2. Mr. Tanish has provided you with the details of his income as follows.

Particulars Amount in ₹

a. Profits from a business set up in Japan, controlled from India.

40,000

b. Income from property in Mumbai, received in UK 70,000

c. Income from a USA based company received in India. 2,00,000

d. Income from shop given on rent in Japan. 50,000

e. Income from providing services Paris and deposited in Paris

80,000

f. Interest from investments held in Dubai, received in Dubai 12,000

g. Dividend received from an Australian Company 23,000

h. Dividend received from an Indian Company 17,000

i. Profits from Singapore business, wholly managed in Singapore

1,00,000

From the above information, you are required to calculate Gross Total Income for Mr.

Tanish for the AY 2016-17 if he is a –

a. Resident and Ordinarily Resident. b. Resident and Not Ordinarily Resident. c. Non-Resident.

3. Mr. Hemant, an Indian citizen staying in Canada came to India for the first time on 1st

May, 2008 and stayed in India for 3 years without any break. On 1st June 2011, he left

for Thailand. He came back to India on 1st April 2012 and went back to Canada on 1st

December, 2012. He was posted back to India on 20th January 2016 and he has been in

India since then. Determine her residential status for the AY 2016-17.

4. Define the following concepts under the Income Tax Act, 1961:

a. Assessment

b. Assessee

c. Assessment Year

d. Previous Year

e. Person

f. Exception rules for assessment year.

5. Differentiate between:

a. Assessment Year and Previous Year.

b. Person and Assessee

ROLL NO. : 2064

1. Mr. Pujari has provided you with the details of his income as follows.

Particulars Amount in ₹

Profits from a business set up in Peru, controlled from India. 80,000

Income from property in Mumbai, received in Colombia. 1,40,000

Income from a Venezuela based agriculture received in India. 4,00,000

Income from shop given on rent in Brazil. 1,00,000

Income from providing services in Chile and deposited in Chile. 1,60,000

Interest from investments held in Uruguay, received in Uruguay. 24,000

Dividend received from an Argentina Company. 46,000

Dividend received from an Indian Company. 34,000

Profits from Brazil business, wholly managed in Brazil. 2,00,000

From the above information, you are required to calculate Gross Total Income for Mr.

Pujari for the AY 2016-17 if he is a –

a. Resident and Ordinarily Resident. b. Resident and Not Ordinarily Resident. c. Non-Resident.

2. Mr. Aacharya is a lecturer in a college at Mumbai. The details of his salaries and other expenses for the PY 2015-16 are as follows.

Particulars Amount in ₹

a. Basic Salary 40,000

b. Dearness Allowance (Shall be forming a part of salary) 7,000

c. City Compensatory Allowance 3,000

d. Education Allowance For his son (Exempt under the Rules @ 100 per month for 2 Children)

4,000

e. House Rent Allowance Exemption u/s 10 (13A)

6200 2400

f. Remuneration from Mumbai University for acting as an examiner

3,000

g. Remuneration from Chennai University for acting as a paper setter

500

h. Allowance per month for looking after the evening shift of the college

500

i. He incurred an expenditure for attending a seminar at Jaipur. This expenditure was reimbursed by college.

1,000

j. During the year he spent on books for teaching purposes 3,000

k. Professional Tax 1,600

Determine the taxable salary of Mr. Aacharya for the AY 2016-17.

3. Mr. Tanmay Dabholkar owns 4 houses, House I and II are self-occupied and House III and IV are let out on rent. Compute his income from house property with the help of the following information.

Particulars HOUSE I

S.O.P

HOUSE II

S.O.P

HOUSE III

L.O.P

House IV

L.O.P

Standard Rent 15,000 20,000 45,000 NA

Fair Rent 20,000 18,000 25,000 30,000

Actual Rent - - 40,000 32,000

Municipal Rateable Value 14,000 21,000 30,000 21,000

Municipal Taxes Paid by Mr. Guha 2,000 3,000 3,500 3,500

Fire Insurance Premium 400 500 500 800

Expenditure on repairs 10,000 - 4,000 200

Year of completion of construction 1988 1996 1993 1994

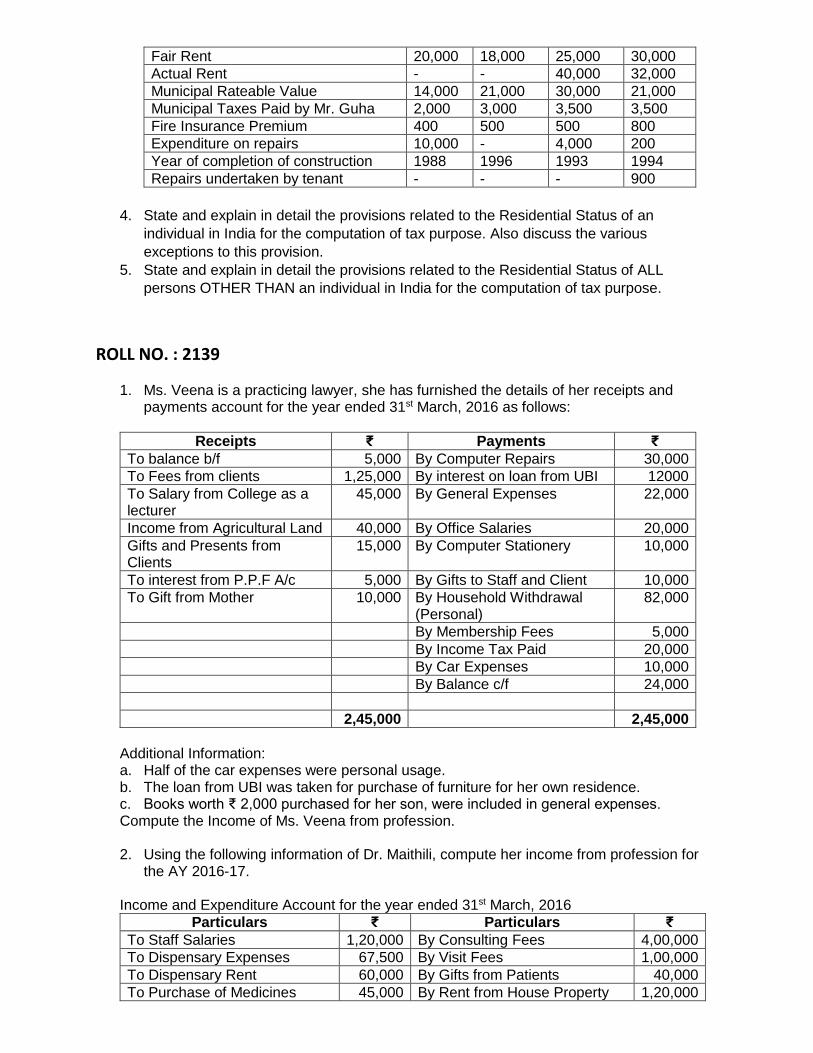

Repairs undertaken by tenant - - - 900

4. State and explain in detail the provisions related to the Residential Status of an

individual in India for the computation of tax purpose. Also discuss the various

exceptions to this provision.

5. State and explain in detail the provisions related to the Residential Status of ALL

persons OTHER THAN an individual in India for the computation of tax purpose.

ROLL NO. : 2139

1. Ms. Veena is a practicing lawyer, she has furnished the details of her receipts and payments account for the year ended 31st March, 2016 as follows:

Receipts ₹ Payments ₹

To balance b/f 5,000 By Computer Repairs 30,000

To Fees from clients 1,25,000 By interest on loan from UBI 12000

To Salary from College as a lecturer

45,000 By General Expenses 22,000

Income from Agricultural Land 40,000 By Office Salaries 20,000

Gifts and Presents from Clients

15,000 By Computer Stationery 10,000

To interest from P.P.F A/c 5,000 By Gifts to Staff and Client 10,000

To Gift from Mother 10,000 By Household Withdrawal (Personal)

82,000

By Membership Fees 5,000

By Income Tax Paid 20,000

By Car Expenses 10,000

By Balance c/f 24,000

2,45,000 2,45,000

Additional Information: a. Half of the car expenses were personal usage. b. The loan from UBI was taken for purchase of furniture for her own residence. c. Books worth ₹ 2,000 purchased for her son, were included in general expenses. Compute the Income of Ms. Veena from profession. 2. Using the following information of Dr. Maithili, compute her income from profession for

the AY 2016-17. Income and Expenditure Account for the year ended 31st March, 2016

Particulars ₹ Particulars ₹

To Staff Salaries 1,20,000 By Consulting Fees 4,00,000

To Dispensary Expenses 67,500 By Visit Fees 1,00,000

To Dispensary Rent 60,000 By Gifts from Patients 40,000

To Purchase of Medicines 45,000 By Rent from House Property 1,20,000

To Income Tax 35,000 By Sale of medicines at dispensary

80,000

To Professional Fees to Doctors

22,000

To Car Expenses 36,400

To Membership Fees 2,000

To Municipal Taxes for Rented House

12,000

To Interest on Housing Loan for Rented House

18,000

To Printing Charges 4,000

To Depreciation 48,000

To Charity 1,500

To Surplus for the Year 268,600

7,40,000 7,40,000

Additional Information: a. Gifts from patients include ₹ 1,000 from her father in personal capacity. b. Depreciation as per income tax rules is ₹ 45,000.

3. Mr. Mihir inherited a house in Jaipur under will of his father in May 2003. The house was

purchased by his father in January, 1981 for ₹ 2,50,000. He invested an amount of ₹7,00,000 in construction of one more floor in June, 2005. The house was sold by him on November, 2015 for ₹47,25,000. Brokerage charged by Mr. Sanjay was ₹ 37,500. The fair Market Value of the house as on 01st April, 1981 was ₹ 2,70,000. You are required to find out the amount of Capital Gains chargeable to tax for the AY 2016-17 for Mr. Mihir with the help of the given information. Given-

Financial Year

CII

2015-16 1081

2005-06 497

2003-04 463

4. What are the various cases when the matter is deemed to accrue or arise in India.

5. What does salary include?

ROLL NO. : 2141

1. From the following information, compute the income under the heading ‘Income from Other Sources’ for Mr Bhavesh.

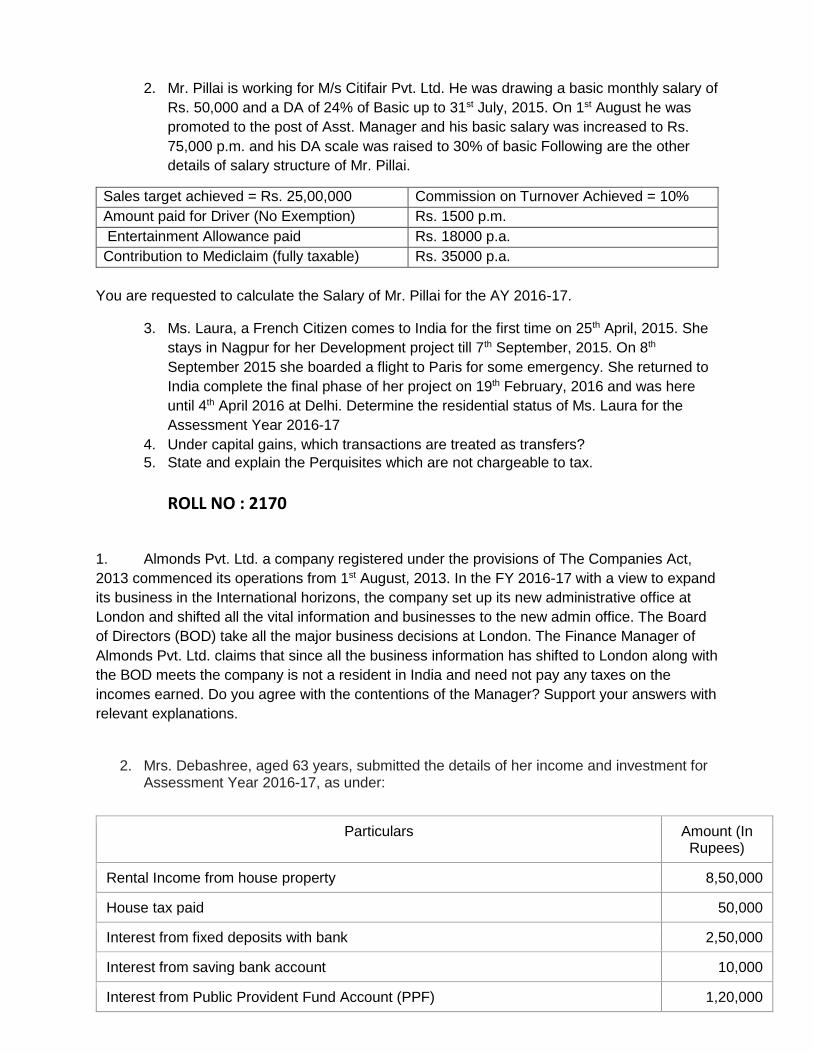

Income from Agricultural Land in India- ₹ 24,000 Income from Agricultural Land in India- ₹ 20,000 Mr. Bhavesh is a tenant of Ms. Mahesh in respect of a bungalow in Lonavala. Mr. Bhavesh has in turn rented the bungalow to Mr.Haresh. Following are the details of rent. i) Rent charged from Ms. Haresh per month ₹ 2,000 ii) Rent paid to Ms. Mahesh per month ₹ 1,000 Interest earned i) Interest on Deposit with the banks. ₹ 1,000 ii) Interest on P.P.F ₹ 2,000 iii) Interest on Government Securities (Net after charging TDS of ₹ 2,400) ₹ 24,000 Lottery Prize (Net after charging TDS of ₹ 40,000) ₹ 1,00,000 Received refund from Income Tax Department pertaining to AY 2008-09. Excess income tax amount received was ₹ 2000 and interest was ₹ 500 ₹5,000

2. Mr. Pillai is working for M/s Citifair Pvt. Ltd. He was drawing a basic monthly salary of

Rs. 50,000 and a DA of 24% of Basic up to 31st July, 2015. On 1st August he was

promoted to the post of Asst. Manager and his basic salary was increased to Rs.

75,000 p.m. and his DA scale was raised to 30% of basic Following are the other

details of salary structure of Mr. Pillai.

Sales target achieved = Rs. 25,00,000 Commission on Turnover Achieved = 10%

Amount paid for Driver (No Exemption) Rs. 1500 p.m.

Entertainment Allowance paid Rs. 18000 p.a.

Contribution to Mediclaim (fully taxable) Rs. 35000 p.a.

You are requested to calculate the Salary of Mr. Pillai for the AY 2016-17.

3. Ms. Laura, a French Citizen comes to India for the first time on 25th April, 2015. She

stays in Nagpur for her Development project till 7th September, 2015. On 8th

September 2015 she boarded a flight to Paris for some emergency. She returned to

India complete the final phase of her project on 19th February, 2016 and was here

until 4th April 2016 at Delhi. Determine the residential status of Ms. Laura for the

Assessment Year 2016-17

4. Under capital gains, which transactions are treated as transfers?

5. State and explain the Perquisites which are not chargeable to tax.

ROLL NO : 2170

1. Almonds Pvt. Ltd. a company registered under the provisions of The Companies Act,

2013 commenced its operations from 1st August, 2013. In the FY 2016-17 with a view to expand

its business in the International horizons, the company set up its new administrative office at

London and shifted all the vital information and businesses to the new admin office. The Board

of Directors (BOD) take all the major business decisions at London. The Finance Manager of

Almonds Pvt. Ltd. claims that since all the business information has shifted to London along with

the BOD meets the company is not a resident in India and need not pay any taxes on the

incomes earned. Do you agree with the contentions of the Manager? Support your answers with

relevant explanations.

2. Mrs. Debashree, aged 63 years, submitted the details of her income and investment for Assessment Year 2016-17, as under:

Particulars Amount (In Rupees)

Rental Income from house property 8,50,000

House tax paid 50,000

Interest from fixed deposits with bank 2,50,000

Interest from saving bank account 10,000

Interest from Public Provident Fund Account (PPF) 1,20,000

Deposit in Public Provident Fund Account (PPF) 60,000

Life Insurance Premium Paid 20,000

Medical Insurance Premium paid 10,000

Calculate her Total Income for Assessment Year 2016-17.

3. Mr. Vinayak is working as Chief Personnel officer in a bank. The following are the particulars of his income for the year March 31, 2016.

a. Basic Salary Rs. 5,500 per month. b. DA Rs. 1,000 p.m. c. Special Executive allowance Rs. 500 p.m. d. Taxable Conveyance, allowance Rs. 5,200 e. He received 2 months’ basic salary as bonus. f. He receives Rs. 750 p.m. as entertainment allowance of which he spends Rs.

500 p.m. On an average for office purposes only. g. During the year he received Rs. 4,800 as leave travel allowance to go to Mysore

with his family. He incurred Rs. 4200 expenses on his tour. h. He spent Rs. 2000 on purchase of Law books which are necessary for his Job. i. Employer deducted Profession Tax Rs. 600 for the year.

You are required to compute taxable income from salaries of Mr. Vinayak for AY 2016-17.

4. What is meant by Profit in Lieu of salary?

5. Explain the provision related to gratuity u/s 10(10).

ROLL NO.:2106

1) Mr. Raman owns 2 houses constructed in March 2004, One, whose Municipal valuation is Rs. 2,50,000 is occupied by him for his own residence and the other, whose municipal valuation is 2,70,000 is let out of Rs. 27500 p.m. The expenses in respect of both the houses are:

Particulars SOP LOP

Municipal Taxes 30,000 35,000

Land Revenue 15,000 20,000

Interest on loan for construction of the houses 35,000 42,500

Fire insurance premium 20,000 20,000

Rent Collection Charges - 20,000

Interest on Mortage (loan Taken for Daughter’s Marriage)

- 75,000

Compute his oncome from House property for the AY 2016-17

2) Mrs. Jaya a practicing CA, furnishes the following particulars of her Receipts and Payments for the year ending 31st March, 2016

Receipts Rs Payment Rs.

Balance b/f 28900 Salary and bonus (including to son Rs. 24000)

80000

Professional fees from client 140000 Printing and stationery 5500

Gift from father 15000 Books and periodicals 2400

Present from client for winning the case

15000 Conveyance expenses 9000

Salary from a college as a lecturer (Net after deducting income tax Rs. 10000)

20600 Interest on loan for higher education of son

10000

Loan from bank for purchase of a car

50000 Purchase of a car 120000

Prize received from the rotary club as the best member of the year.

4500 Motor car expenses 20000

Medical Insurance premium 6500

Interest on bank loan for car 5000

Income tax 8500

Professional tax 800

Balance c/f 6300

Other Information:

a. Depreciation allowable on the motor car as per income tax rule is 20%.

b. Motor car is used for office as well as for personal use, and in the past 25% of the

expenses were treated as for personal use.

Compute the taxable professional income of Mrs Jaya for the AY 2016-17.

3) Mr. Rajan acquired a Residential House in January 1979 for Rs. 2,00,000. It’s market value

on 1st April, 1981 is Rs. 1,80,000. He constructed its first floor in September 1987 by

incurring Rs. 3,00,000. He Constructed second floor in October 2001 by incurring Rs.

4,00,000. He constructed its third floor in February 2012 by incurring Rs. 5,00,000. He sold

the house on 1st January, 2016 for Rs. 1,00,00,000 and paid brokerage of Rs. 1,00,000.

Compute his capital gains for the AY 2016-17.

4) Explain the provision related to pension u/s 10(10A).

5) What Provisions are mentioned in the Income Tax Act, 1961 for Deemed Let Out Property?

ROLL NO.:2144

1. Mr. Gagan purchased one house on 1st October 1978 for Rs. 5,00,000 and paid brokerage

Rs. 25,000. The fair value of this house on 1st April, 1981 was Rs. 5,10,000. He constructed its

1st floor on 1st January 2003 by incurring Rs. 4,00,000 and subsequently this house was sold on

1st January 2016 for Rs. 1,60,00,000 and selling expenses were Rs. 85,000. Compute the

capital gains for Mr. Gagan AY 2016-17.

2. Mr. Abhinav purchased a house property for Rs. 36,000 on 10th May, 1963. He gets the

first floor of the house constructed in 1967-68 by spending Rs. 80,000. He dies on 12th

September, 1983. The property is transferred to Mrs. Ekta by his will. Mrs. Ekta spends

Rs. 40,000 during 1984-85 for renewals/reconstruction of the property. Mrs. Ekta sells

the house property for Rs. 54,50,000 on 15th March, 2016 (brokerage paid by Mrs. Ekta

is Rs. 14,500). The fair Market Value of the house on 1st April, 1981 is Rs. 1,10,000.

Find out the amount of Capital gain chargeable to tax for the AY 2016-17.

3. Shri Surendra furnishes the following particulars of his incomes for the financial year

ending 31st March 2016.

a. Dividends received in May 2015 from UTI Rs 1,552

b. Dividends received in May 2015 from Tata Ltd. Rs. 3,680.

c. Amount received on 1st December 2015 in connection with winning from Horse race Rs.

7,100.

d. Amount received on 1st December 2015 in connection with winning from Lottery Rs.

39,500. Cost of Lottery tickets purchased Rs. 2,000

e. Director’s fees received in Aug. 2015 Rs 20,000

f. He has rented a residence for Rs. 250 p.m. Half portion of this house was sub-let on a

monthly rent Rs. 250 p.m.

Compute his taxable income for the AY 2016-17

4. What Provisions are mentioned in the Income Tax Act, 1961 for Self-Occupied Property?

5. What is Unabsorbed Depreciation? Discuss the provisions for Unabsorbed Depreciation

under the Act.

ROLL NO.:2163

1. Kajal a resident individual submits the following particulars for her income for the year ended

31-03-2016.

a. Royalty from a Coal Mine Rs. 20,000

b. Agricultural Income in Brazil Rs. 15000

c. Salary from Parliament Rs. 36000

d. Daily allowance as a MP Rs. 5000

e. Her residential house has been taken on a rent of Rs. 10000 p.a half of which

she has sublet at Rs. 1200 p.m.

f. Dividend received from a co-operative society Rs. 5,000

g. She has incurred the following expenses:

Paid collection charges for collecting dividend Rs. 100

Rs. 3000 paid for earning for earning and collecting royalty income.

Compute Kajal’s income from other sources for the AY 2016-17

2. From the following incomes earned by Mr. Amit during the financial year 2015-16,

determine his total income for the AY 2016-17 if he is (i) Resident, (ii) Not ordinarily

Resident, (iii) Non-Resident.

Particulars Rs.

Profits from a business in Delhi managed from Oman 30,000

Pension for services rendered in India. 15,000

Interest on Hungary Government Bonds, half of which is received in India

4,000

Income from property situated in Mauritius received there. 20,000

Past foreign untaxed income brought to India during the RPY 7,000

Income from agricultural land in Jakarta received there and then brought to India.

30,000

Income from profession in Nairobi which was set up in India, received there

12,000

3. Ms. Mudra had the following income during the year ended 31st March 2016.

Particulars Rs.

Salary received in India for 3 months 9000

Income from House property in India 13470

Interest from saving bank account in SBI 1000

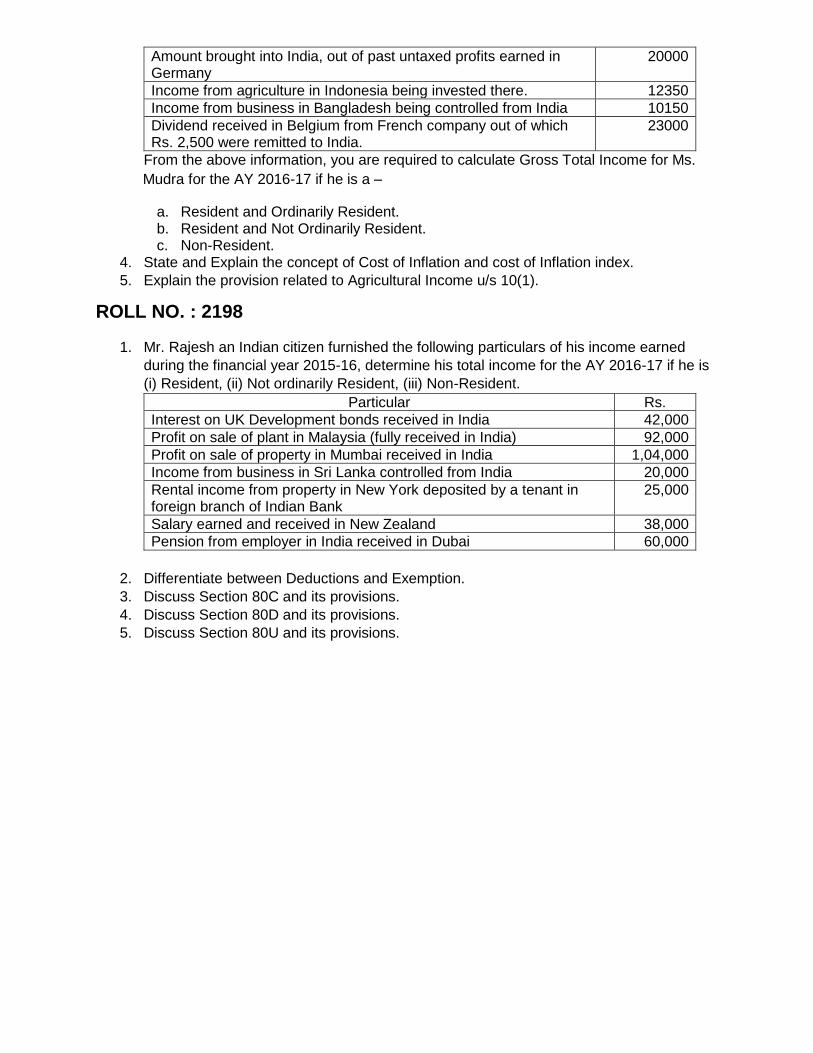

Amount brought into India, out of past untaxed profits earned in Germany

20000

Income from agriculture in Indonesia being invested there. 12350

Income from business in Bangladesh being controlled from India 10150

Dividend received in Belgium from French company out of which Rs. 2,500 were remitted to India.

23000

From the above information, you are required to calculate Gross Total Income for Ms.

Mudra for the AY 2016-17 if he is a –

a. Resident and Ordinarily Resident. b. Resident and Not Ordinarily Resident. c. Non-Resident.

4. State and Explain the concept of Cost of Inflation and cost of Inflation index.

5. Explain the provision related to Agricultural Income u/s 10(1).

ROLL NO. : 2198

1. Mr. Rajesh an Indian citizen furnished the following particulars of his income earned

during the financial year 2015-16, determine his total income for the AY 2016-17 if he is

(i) Resident, (ii) Not ordinarily Resident, (iii) Non-Resident.

Particular Rs.

Interest on UK Development bonds received in India 42,000

Profit on sale of plant in Malaysia (fully received in India) 92,000

Profit on sale of property in Mumbai received in India 1,04,000

Income from business in Sri Lanka controlled from India 20,000

Rental income from property in New York deposited by a tenant in foreign branch of Indian Bank

25,000

Salary earned and received in New Zealand 38,000

Pension from employer in India received in Dubai 60,000

2. Differentiate between Deductions and Exemption.

3. Discuss Section 80C and its provisions.

4. Discuss Section 80D and its provisions.

5. Discuss Section 80U and its provisions.