improper payment oversight in the federal government beryl “berri” davis director, financial...

TRANSCRIPT

Improper Payment Oversight in the Federal Government

Beryl “Berri” DavisDirector, Financial Management and Assurance, GAO

Gloria JarmonDeputy Inspector General for Audit, U.S. Department of Health & Human Services Office of Inspector General

Mike WetklowBranch Chief, Office of Management and Budget, Office of Federal Financial Management

Jenny RoneActing Executive Director, U.S. Department of Treasury, Do Not Pay Business Center

2

IMPROPER PAYMENTS:

WHAT CAN BE DONE TO PREVENT THEM?

SEPTEMBER 16, 2015

BERYL H. “BERRI” DAVISCGFM, CPA, CIA, CGAP, CGMA, CCSADIRECTOR, FINANCIAL MANAGEMENT AND [email protected]

4

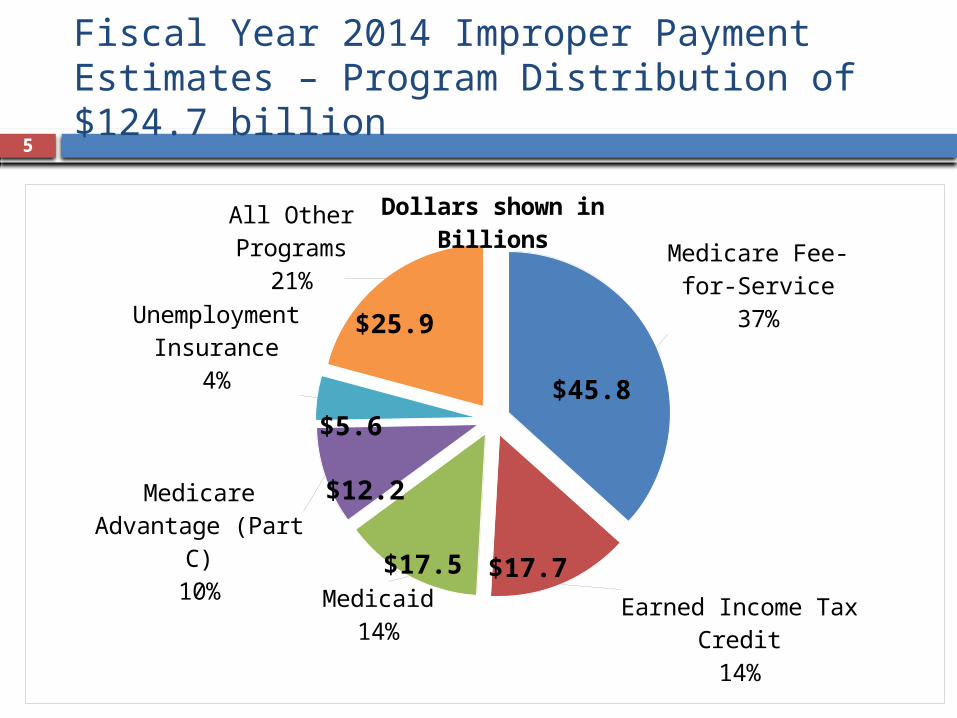

Fiscal Year 2014 Improper Payment Estimates

OMB and federal agencies reported improper payment estimates totaling $124.7 billion in fiscal year 2014, an increase of approximately $19 billion from the prior year revised estimate of $105.8 billion. $16 billion of the estimated $19 billion increase in

fiscal year 2014 is attributed primarily to increased error rates in three major programs: HHS’s Medicare Fee-for-Service (10.1% to 12.7%) HHS’s Medicaid (5.8% to 6.7%) Treasury’s Earned Income Tax Credit (24.0% to 27.2%)

5

Fiscal Year 2014 Improper Payment Estimates – Program Distribution of $124.7 billion

Medicare Fee-for-Service

37%

Earned Income Tax Credit14%

Medicaid14%

Medicare Advan-tage (Part C)

10%

Unemployment Insurance

4%

All Other Programs

21%

Dollars shown in Billions

$45.8

$17.7$17.5

$12.2

$5.6

$25.9

6

Medicare

Fee-fo

r-Servi

ce

Earned In

come T

ax Cre

dit

Medicaid

Medicare

Adva

ntage (Part C

)

Unemployment In

sura

nce

Supplemental Secu

rity In

sura

nce

Old Age, S

urvivo

rs, and D

isabilit

y Insu

rance

Supplemental Nutrit

ion Ass

istance

Pro

gram

Medicare

Pre

scrip

tion D

rug

School L

unch

Direct

Loan

Public H

ousing/R

ental Ass

istance

$0

$10

$20

$30

$40

$50$45.8

$17.7$17.5$12.2

$5.6 $5.1 $3.0 $2.4 $1.9 $1.7 $1.5 $1.0

Dollars (in billions)

Programs with Improper Payment Estimates Exceeding $1 Billion in Fiscal Year 2014

7

Earn

ed In

com

e Tax

Cre

dit

Schoo

l Bre

akfas

t

Farm

Sec

urity &

Rura

l Inve

stmen

t

Loan

Defi

ciency

Paym

ents

Schoo

l Lunch

Disaste

r Reli

ef - A

CF Soc

ial S

ervic

es B

lock G

rant

Medica

re Fe

e-for

-Ser

vice

Disaste

r Reli

ef - S

AMHSA

Disaste

r Ass

istan

ce Lo

ans

Unemploy

men

t Insu

rance

0%

5%

10%

15%

20%

25%

30% 27% 26%23%

19%15% 14% 13% 13% 12% 12%

Error Rate (percentage of outlays)

Programs with Error Rates Greater than 10% in Fiscal Year 2014

8

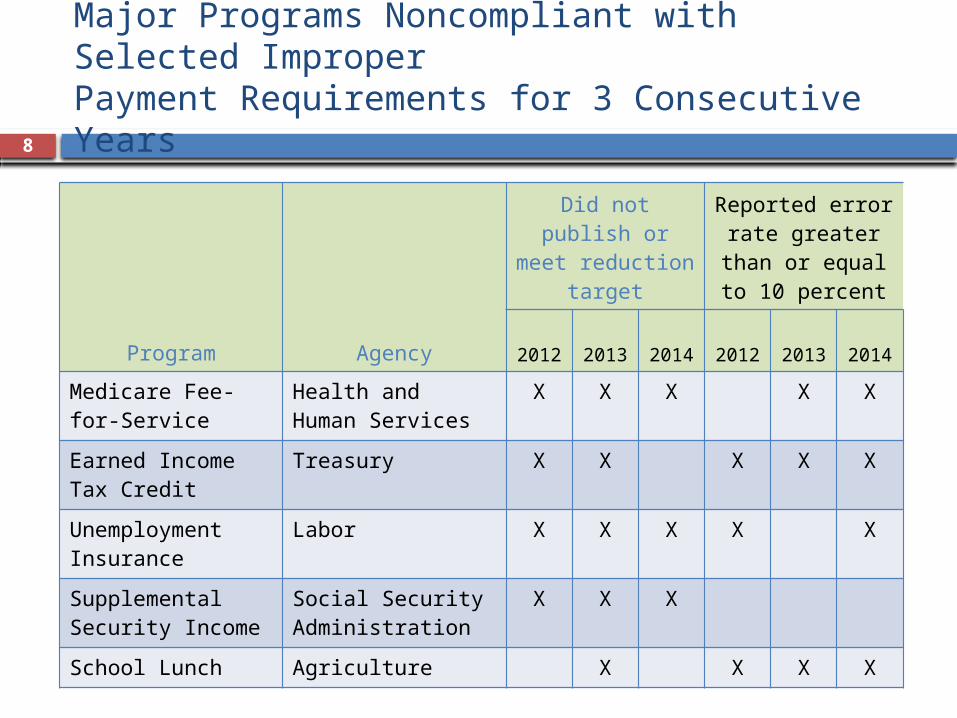

Major Programs Noncompliant with Selected Improper Payment Requirements for 3 Consecutive Years

Program Agency

Did not publish or meet

reduction target

Reported error rate greater

than or equal to 10 percent

2012

2013

2014

2012

2013

2014

Medicare Fee-for-Service

Health and Human Services

X X X X X

Earned Income Tax Credit

Treasury X X X X X

Unemployment Insurance

Labor X X X X X

Supplemental Security Income

Social Security Administration

X X X

School Lunch Agriculture X X X X

9

Key GAO Recommendations

Medicare examples: improving use of automated edits and removing Social Security numbers from Medicare cards

Medicaid examples: improving third-party liability efforts and increasing oversight of managed care

Earned Income Tax Credit examples: regulating paid tax preparers and accelerating W-2 filing deadlines

10

Reviewing medical necessity of TRICARE payments

Key GAO Recommendations (continued)

11

DOE Recommendations GAO found that the Department of Energy’s (DOE) fiscal year 2011 risk assessments: did not always include a clear

basis for the risk determination; and

did not always fully evaluate other relevant risk factors.

GAO recommended that DOE take steps to improve its risk assessments including: revising guidance on how

programs are to address risk factors; and

providing examples of other risk factors likely to contribute to improper payments and directing programs to consider those factors.

26

23

6

DOE Programs

Did Not Prepare Risk AssessmentPrepared Risk AssessmentPrepared Risk Assessment, but did not take into account the 8 qualitative risk factors

Key GAO Recommendations (continued)

Improper Payment Oversight in the Federal Government

Gloria Jarmon

Deputy Inspector General for Audit ServicesU.S. Department of Health & Human Services

12

In FY 2014, HHS reported $78.4 billion in improper payments

13

Programs Susceptible to Significant Improper Payments

Program FY2014 Improper Payment Estimate Dollars (in millions)

Medicare FFS $45,754

Medicare Advantage $12,229

Medicare Prescription Drug Benefit

$1,931

Medicaid $17,492

Children’s Health Insurance Program (CHIP)

$612

Temporary Assistance for Needy Families (TANF)

N/A

Foster Care $66.2

Child Care and Development Fund (CCDF)

$299

Disaster Relief Appropriation Act Programs (DRAA)

$9

14

OIG Objectives

1) Determine whether HHS complied with the IPIA for FY 2014 in accordance with OMB guidance

2) Evaluate HHS’ assessment of the level of risk and the quality of the improper payment estimates and methodology for high-priority programs

3) Assess HHS’ performance in reducing and recapturing improper payments

15

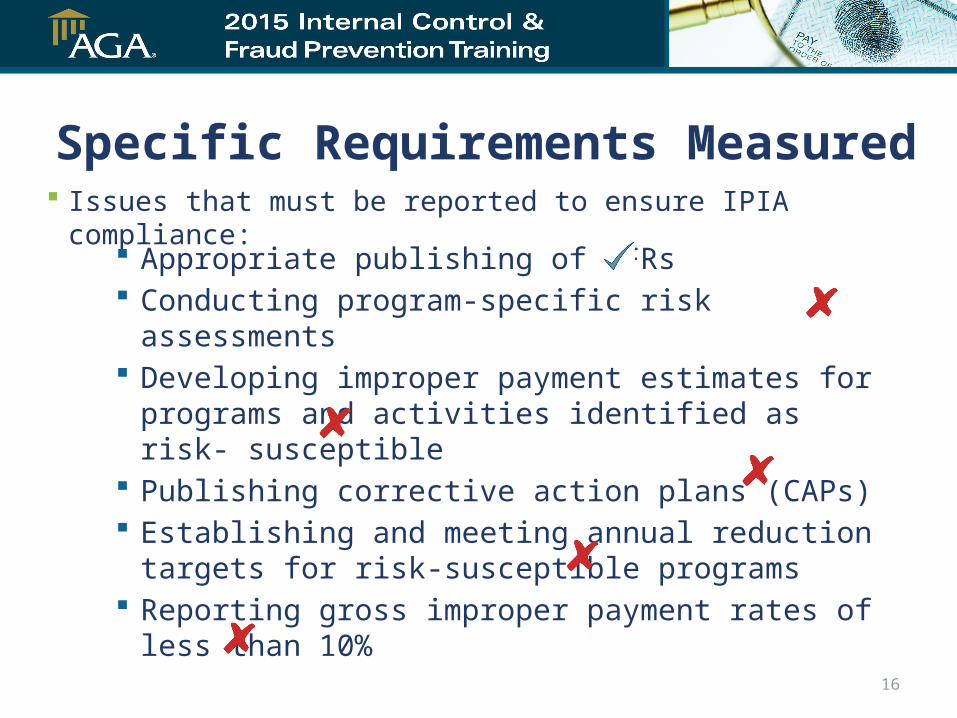

Specific Requirements Measured Issues that must be reported to ensure IPIA compliance:

Appropriate publishing of AFRs Conducting program-specific risk assessments Developing improper payment estimates for

programs and activities identified as risk- susceptible Publishing corrective action plans (CAPs) Establishing and meeting annual reduction targets for

risk-susceptible programs Reporting gross improper payment rates of less than

10%

16

In FY 2014, HHS Failed To:

1) Perform risk assessments of payments to employees and charge card payments

2) Publish an improper payment estimate for TANF that OMB determined to be susceptible to improper payments

3) Publish a CAP for TANF

4) Meet reduction targets for four of the six programs for which HHS reported reduction targets in the FY 2013 AFR

5) Report an improper payment rate of less than 10 percent for Medicare FFS and two DRAA programs

17

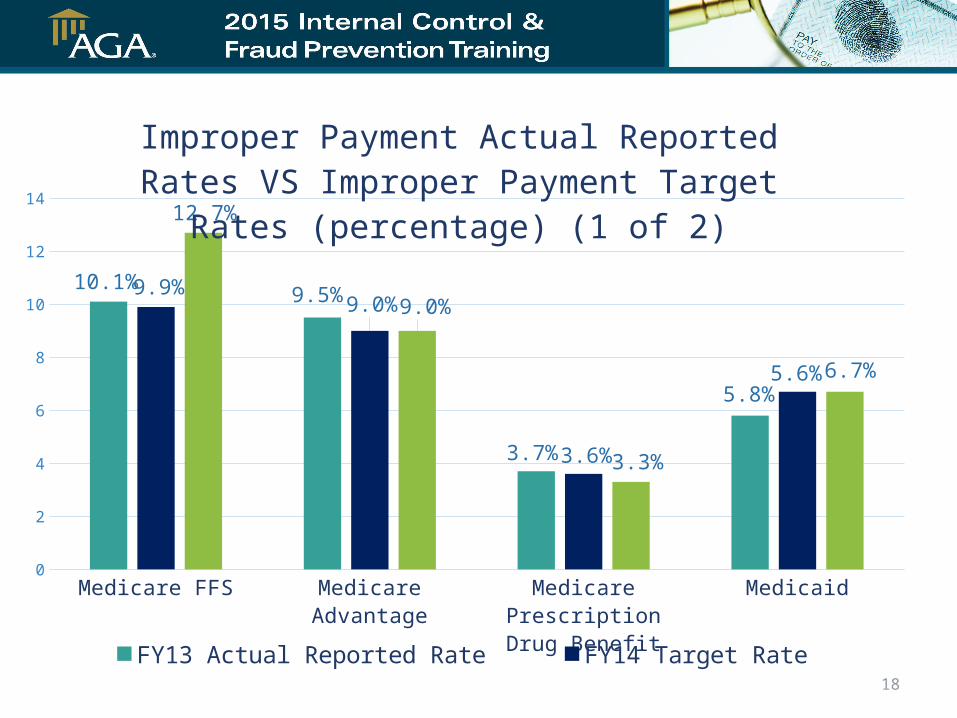

Medicare FFS Medicare Advantage Medicare Prescription Drug Benefit

Medicaid0

2

4

6

8

10

12

14

10.1%9.5%

3.7%

5.8%

9.9%9.0%

3.6%

5.6%

12.7%

9.0%

3.3%

6.7%

Improper Payment Actual Reported Rates VS Im-proper Payment Target Rates (percentage) (1 of 2)

FY13 Actual Reported Rate FY14 Target Rate FY14 Actual Reported Rate18

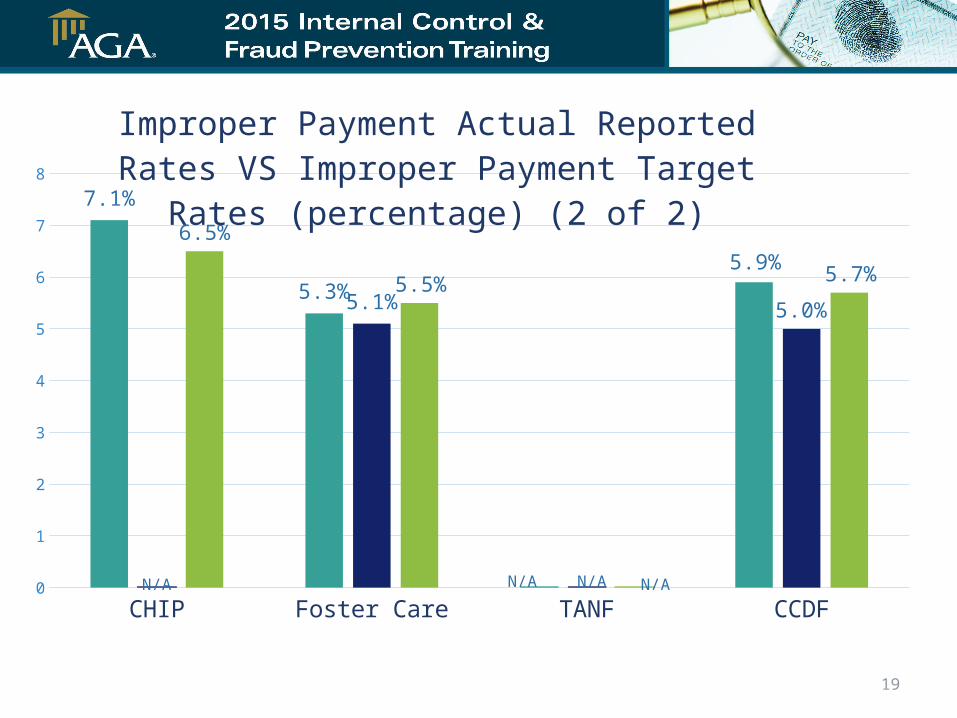

CHIP Foster Care TANF CCDF0

1

2

3

4

5

6

7

8

7.1%

5.3%

N/A

5.9%

N/A

5.1%

N/A

5.0%

6.5%

5.5%

N/A

5.7%

Improper Payment Actual Reported Rates VS Im-proper Payment Target Rates (percentage) (2 of 2)

FY13 Actual Reported FY14 Target Rate FY14 Actual Reported19

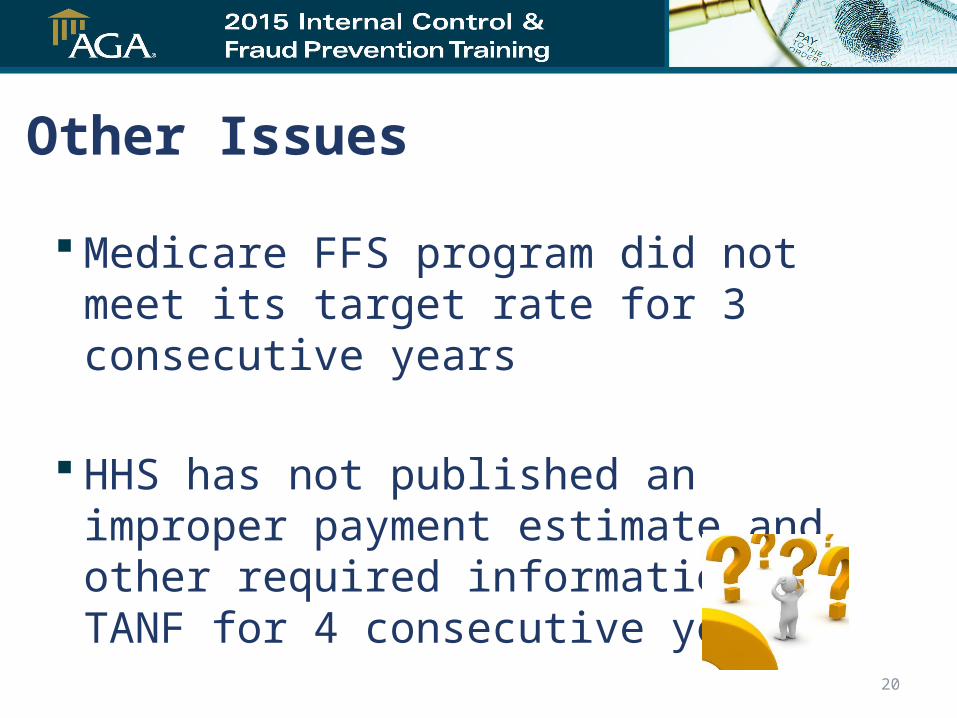

Other Issues

Medicare FFS program did not meet its target rate for 3 consecutive years

HHS has not published an improper payment estimate and other required information for TANF for 4 consecutive years

20

OIG Recommendations

1) Take actions to ensure Medicare FFS program meets its established target rates

2) Develop and establish an improper payment estimate for TANF

3) Reduce improper payment rates to below 10 percent and achieve established improper payment target rates

4) Conduct risk assessments of payments to employees and charge card payments 21

OMB Update

22

AGA Internal Control and Fraud

Prevention Training September 16, 2015

Mike WetklowBranch Chief, Office of Management and BudgetOffice of Federal Financial Management

23

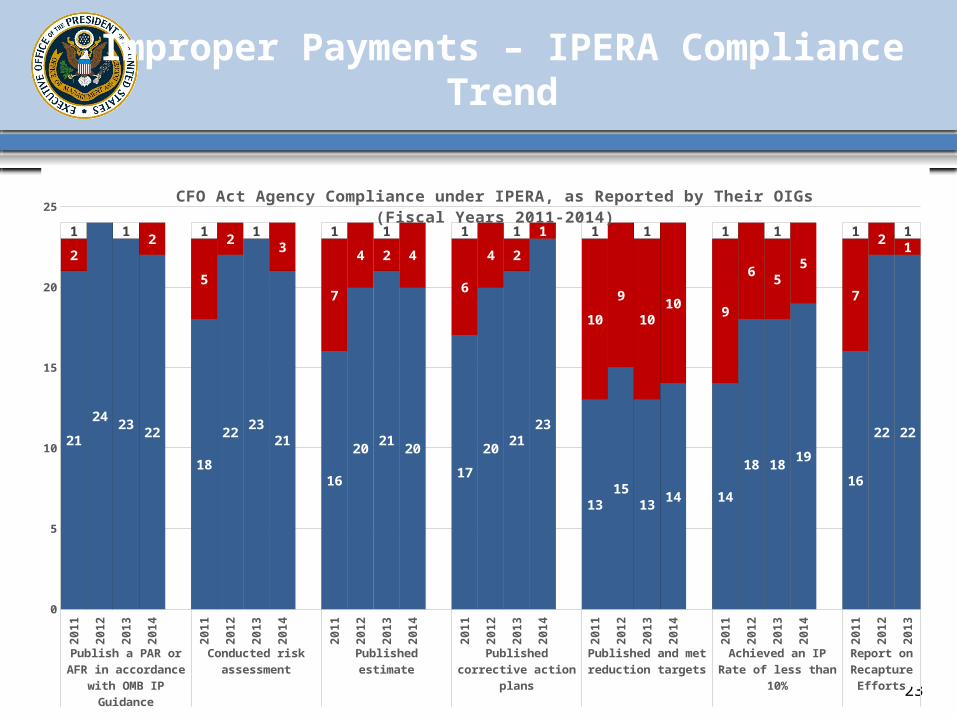

Improper Payments – IPERA Compliance Trend20

11

2012

2013

2014

2011

2012

2013

2014

2011

2012

2013

2014

2011

2012

2013

2014

2011

2012

2013

2014

2011

2012

2013

2014

2011

2012

2013

Publish a PAR or AFR in accordance with OMB IP

Guidance

Conducted risk as-sessment

Published estimate Published corrective ac-tion plans

Published and met reduction targets

Achieved an IP Rate of less than 10%

Report on Re-capture Efforts

0

5

10

15

20

25

21

24 23 22

18

22 2321

16

20 21 20

17

20 2123

1315

13 14 14

18 18 19

16

22 22

22

5

2 3

7

4 2 4

6

4 2

1

10

9

1010 9

6 55

7

2 11 1 1 1 1 1 1 1 1 1 1 1 1 1

CFO Act Agency Compliance under IPERA, as Reported by Their OIGs (Fiscal Years 2011-2014)

Yes: OIG reported compliance No: OIG reported noncompliance Not Applicable: NSF did not report.

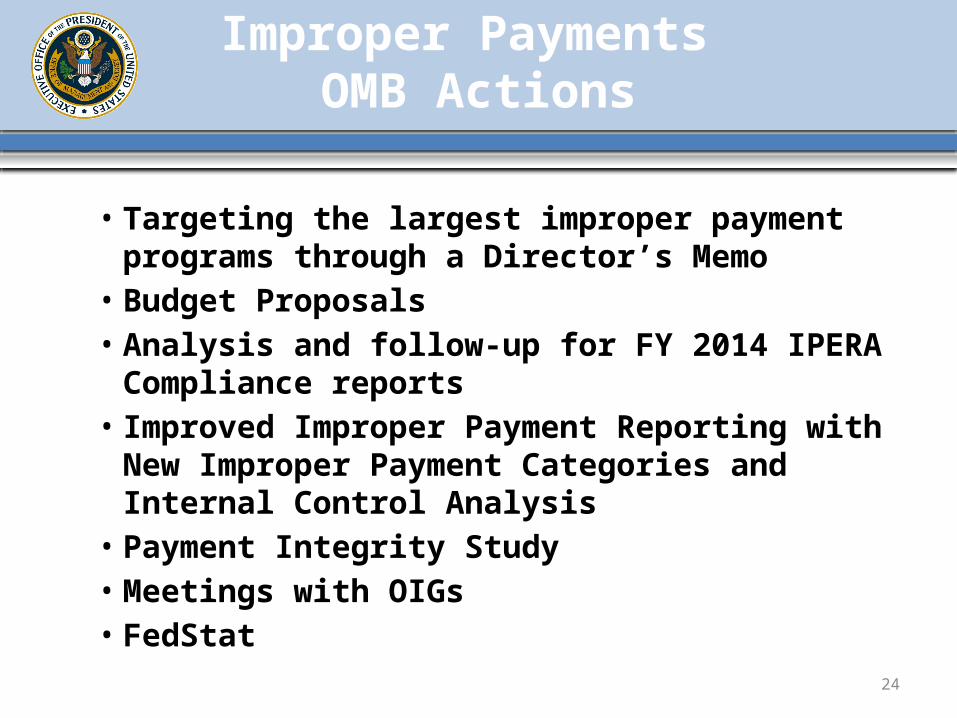

Improper Payments OMB Actions

24

• Targeting the largest improper payment programs through a Director’s Memo

• Budget Proposals• Analysis and follow-up for FY 2014 IPERA Compliance

reports• Improved Improper Payment Reporting with New

Improper Payment Categories and Internal Control Analysis

• Payment Integrity Study• Meetings with OIGs• FedStat

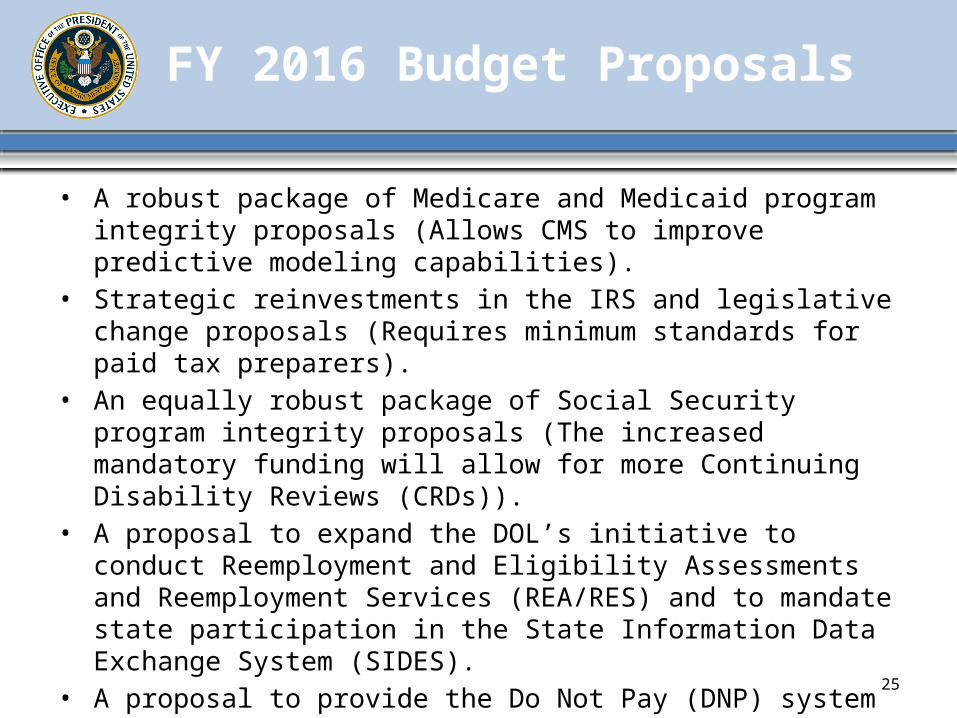

• A robust package of Medicare and Medicaid program integrity proposals (Allows CMS to improve predictive modeling capabilities).

• Strategic reinvestments in the IRS and legislative change proposals (Requires minimum standards for paid tax preparers).

• An equally robust package of Social Security program integrity proposals (The increased mandatory funding will allow for more Continuing Disability Reviews (CRDs)).

• A proposal to expand the DOL’s initiative to conduct Reemployment and Eligibility Assessments and Reemployment Services (REA/RES) and to mandate state participation in the State Information Data Exchange System (SIDES).

• A proposal to provide the Do Not Pay (DNP) system at Treasury access to the SSA’s full death data

25

FY 2016 Budget Proposals

Program Integrity Funding

26

• The Consolidated and Further Continuing Appropriations Act, 2015 fully funded the adjustment to the discretionary spending limit for HCFAC for the first time and SSA for the second time since the cap adjustment was available in 2012.

– In June 2015 - FBI arrested 46 doctors and nurses across the country for allegedly billing Medicare for $712 million worth of patient care that was never given or unnecessary.

• The Department of Labor Established a UI Integrity Center of Excellence in 2012. The center has been able to use Internet Protocol (IP) address blocking to prevent claimants from certifying for benefits while outside the country. Claimants that attempt to initiate a claim or certify from a disallowed IP address are advised they may not do so until they return to the United States, a U.S. Territory, or Canada. In New York, this solution discourages and prevents an estimated $15.6 million in improper payments each year and is being implemented in multiple states.

Do Not Pay Business CenterJenny Rone

Acting Executive Director

September 16, 2015

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 28

Do Not Pay - Part of the Solution

Providing information for informed decisions about eligibility

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 29

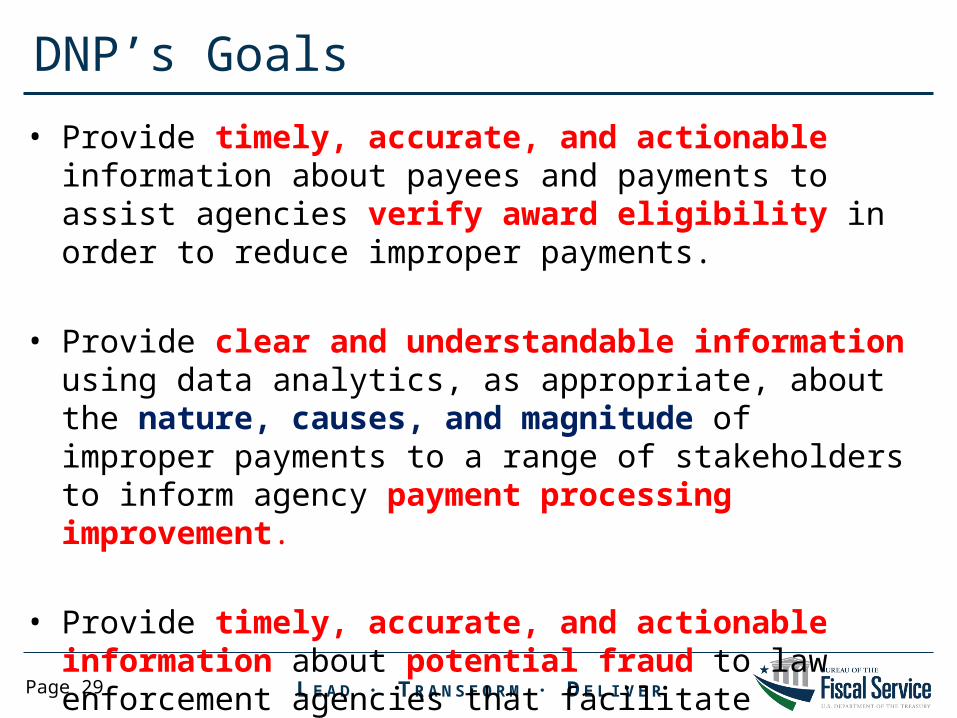

DNP’s Goals

• Provide timely, accurate, and actionable information about payees and payments to assist agencies verify award eligibility in order to reduce improper payments.

• Provide clear and understandable information using data analytics, as appropriate, about the nature, causes, and magnitude of improper payments to a range of stakeholders to inform agency payment processing improvement.

• Provide timely, accurate, and actionable information about potential fraud to law enforcement agencies that facilitate investigations and prosecutions.

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 30

Through use of the DNP Portal ~

• Pre-Award / Pre-Payment Eligibility Verification– 50 agencies; 175 programs/groups

• At time of payment (payment integration)– For FY 15 (October – June)

• 207.5M payments screened equaling $941.4B • $5.7M identified as improper by the issuing agency

Detecting & Preventing Improper Payments

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 31

Bureau of Fiscal Service – Payment Integrity

Ensuring the integrity of Federal payments by providing services to detect and prevent improper payments and combat fraud, waste and abuse

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 32

Payment Integrity Program

Fiscal Service operations assists efforts to ~

reduce improper payments, fraud, waste, and abuse in Federal spending.

Fiscal Service provides valuable data and insight to support Federal Agency efforts, as well as law enforcement entities and the oversight community, to ensure the integrity of Federal payments and combat improper payments, fraud, waste and abuse.

Treasury disburses 85% of Federal government payments, equaling $3 Trillion • Treasury’s broad authorities (31 U.S.C. 3325, IPERIA, 31 CFR Parts 210 and 240, etc.) offer

broader techniques to manage and analyze payment data to support efforts to improve data quality, prevent improper payments, and detect fraud, waste and abuse.

• Fiscal Service has access to multiple Federal and public data sources which can be used to detect fraud and systemic improper payments. Additionally, Fiscal Service is authorized to utilize OMB-approved commercial databases in its operations.

• As the owner of government wide payment data, Treasury supports inter- and intra-agency analysis.

• Preventing improper payments through Fiscal Service entitles users to specialized computer matching authorities under the Improper Payments Elimination and Recovery Act of 2012 (IPERIA) and OMB Implementing Guidance, M-13-20, Protecting Privacy while Reducing Improper Payments with the Do Not Pay Initiative.

• Treasury utilizes a robust set of analytical tools, techniques, data and expertise to support a wide variety of prevention, detection and recovery efforts for all payment integrity stakeholders.

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 33

Cross-Cutting Government Analytics

Z

• Unique ability to look across payments and program areas to observe government spending as a whole

• Fiscal Service can assist agencies to address potential overlap in payments or any other cross-government issue

• Positioned at a “top looking down” location to see them entire picture of payments

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 34

• provide information to agencies on intra-agency payments to help assess likelihood of a payment being duplicative

• provide information on individuals who have been paid by multiple agencies to provide leads for further research

• done using strict matching or sensitivity analysis on the identification number, payment amount, payment type, payment date

Duplicate Payment Analytics Support

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 35

Audit Investigations

• Access to the Do Not Pay data sources and data matching functionalities/services for the purposes of detection and prevention of improper payments

• Analytics to support improper payment detection & prevention and strengthening internal controls

• Reactive data analysis or data sharing based upon a law enforcement entity request in support of a criminal investigation

• Proactive development of criminal investigation packages and/or leads based upon identified trends, patterns and anomalies which are subsequently provided to the appropriate law enforcement entity

Supporting Fraud & Internal Control Efforts

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 36

Payment Integrity Tools & Services

Prevailing Practices, Capabilities and Services

Central repository of data sources managed by knowledgeable and skilled staff.

Flexible, scalable, and rapid technology solutions that can adopt to environment changes.

Tailor information to the needs of the end users and integrate in to the paying agencies business processes.

Support for Inspector General criminal investigation and other law enforcement agencies by providing information for current investigations or information to substantiate a new investigation

Support for Inspector General audits to prevent improper payments, fraud, waste, and abuse by strengthening internal controls.

Support for Agencies and programs to prevent and detect improper payments, recover funds, and support improvements to payment operations/processes in order to prevent fraud, waste and abuse.

Perform analysis and statistical analytics on Federal payment data.

Ability to conduct payment data analysis and statistical analytics across government agencies and programs as well as across programs within an agency.

Authority to execute a one to many data source analytics matching via one Computer Matching Agreement (per M-13-20).

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 37

Specialized Services for Law Enforcement

• Forensic analysis of the various physical components of U.S. Treasury checks including: signature, magnetic ink character recognition, multiple endorsement, altered and counterfeit, etc. and applicable certification therein

• Address inbound data requests for investigative entities, to aid in prosecution in active cases

• Detect and send actionable referrals for investigative entities, where fraud is highly suspected

• Analyze U.S. Treasury checks and ACH payments for Fraud patterns including: stolen blocks of checks, many to one address/zip code/account, signature commonalities, altered/counterfeit commonalities, etc.

• Provide expert/fact witness testimony as to the authenticity of U.S. Treasury check and ACH payments, and the processes comprised within the U.S. Treasury Payment Lifecycle

L E A D ∙ T R A N S F O R M ∙ D E L I V E RPage 38

Contact InformationActing Executive Director, Do Not Pay Business CenterJenny [email protected]

Regional Deputy Director, Philadelphia Financial CenterWesley [email protected]

Questions?