in collective bargaining harry c. fischer, c.p.a

TRANSCRIPT

tnqtv

SHEW

'¶HE USES OF ACCOUNTING

IN COllECTIVE BARGAINING

by Harry C. Fischer, C.P.A.

INSTITUTE 5c

THE USES OF ACCOUNTINGIN COLLECTIVE BARGAINING

The Uses ofAccounting in

CollectiveBargaining

By HARRY C. FISCHER, C.P.A.

Edited by Irving BernsteinDrawings by Bill Tara

INSTITUTE OF INDUSTRIAL RELATIONS

University of California * Los Angeles

COPYIGHT, 1969, BYTHE REGENTS OF THE uNiVERSrrY OF CALIFORNIA

POPULAR PAMPHLETS OF THE INSTrrUTE OF INDUSTRIAL RELATIONS

Southern Division:Collective Bargaining, by Edgar L. Warren and Irving Bernstein. 50cMaking Grievance Procedures Work, by Abbott Kaplan. 50cEmploying the Seriously Impaired, by Robert D. Meicher. 50cWages: An Introduction, by H. M. Douty. 50c.Union Security, by Orme W. Phelps. 50cWage Structures and Administration, by H. M. Douty. SOcHealth Insurance: Group Coverage in Industry, by Richard N. Bais-den and John Hutchinson. 50c

Personnel Management in Small Companies, by Frances Torbert. 50cStandards of Wage Determination, by Paul Bullock. 75cAbsenteeism, by Marjorie Brookshire. 75cMerit Employment, by Paul Bullock. 75cWomen & Work, by Marjorie B. Turner. 75cEqual Opportunity in Employment, by Paul Bullock. 75cThe Uses of Accounting in CoUective Bargaining, by Harry C.

Fischer. 75cNorthern Division:

Pensions under Collective Bargaining, by William Goldner. 50cStrikes, by William Goldner, 50cHours of Work, by William Goldner. 50cProductivity, by Peter 0. Steiner and William Goldner. 50cGuaranteed Wages, by J. W. Garbarino. 50cThe Business Agent and His Urnon, by Wilma Rule Krauss and VanDusen Kennedy. 50c

Local Employers' Associations, by William H. Smith. 50cUnemployment Insurance, by Margaret S. Gordon and Ralph W.Amerson. 50c

Automation, by Jack Rogers. 50cThe Old Worker, by B. V. H. Schneider, 75cWage Incentive Systems, by Garth L. Mangum. 75cThe Business Agent and His Union, by Van Dusen Kennedy andWilma Rule Krauss, Revised Edition. 75c

Quantity discounts are available.Order from the

INSTITUTE OF INDUSTRIAL RELATIONSSouthern Division: Northern Division:Bunche Hall 2521 Channing WayUniversity of California University of CaliforniaLos Angeles, California 90024 Berkeley, California 94720

Foreword

IH INSTITUTE OF INDusTmIAL RELATIONS ofthe University of California was created for the purpose,among others, of conducting research in industrial rela-tions. A basic problem is to reach as large an audience aspossible. Hence, through this series of popular pam-phlets the Institute seeks to disseminate research beyondthe professional academic group. Pamphlets like this oneare designed for the use of management, labor organi-zations, government officials, schools and universities,and the general public. Those pamphlets already pub-lished (a list appears on the preceding page) haveachieved a wide distribution among these groups. TheInstitute research program includes, as well, a substan-tial number of books, monographs, and journal articles,a list of which is available to interested persons uponrequest.A collective bargain is in substantial part a money

"package," an assemblage of wage rates and fringe bene-fits that the employer offers his employees over a pros-pective period of time. Its negotiation involves a subtleprocess of balancing equities. The union and the workers

[v]

vi * FOREWORD

must satisfy themselves that the bargain is fair accordingto the standards they apply to their particular situation.The employer must be persuaded that he can afford topay the costs of the bargain. In the conduct of the bar-gaining each side must be aware of and give considera-tion to the other's equity. Thus, both the employer andthe union must weigh the former's ability to pay. Thelanguage in which this is expressed is accounting. Thispamphlet is intended to serve as an introduction to thatlanguage.The author of The Uses of Accounting in Collective

Bargaining is well fitted to write such a pamphlet. HarryC. Fischer holds the B.B.A. from the Baruch School ofBusiness of the City College of the University of the Cityof New York. Both the states of New York and Californiahave certified him to practice as a Certified Public Ac-countant. He has, in fact, practiced for many years inCalifornia in the firm of Sunderman, Miller, Fischer &Co., specializing in health, welfare, and pension funds.He is a member of the American Institute of CertifiedPublic Accountants and of its Committee on Health,Welfare, and Pension Funds. He is also a member of theAccountants Advisory Committee of the National Foun-dation of Health, Welfare, and Pension Plans, Inc. He isthe author of Accounting and Office Manual for LaborUnions, published by the Bureau of National Affairs, aswell as of many articles on accounting and tax problems.The Institute wishes to express its gratitude to the

following persons from the University of California, LosAngeles, who reviewed the manuscript: Paul Prasow,

FOREWORD vii

Ted Ellsworth, and John W. Buckley. Bill Tara designedthe cover and drew the illustrations. Mrs. Felicitas Hin-man assisted with the editing.The viewpoint is that of the author and is not neces-

sarily that of the Institute of Industrial Relations or ofthe University of California.

BENJAMIN AARON, DirectorSouthern Division

LLOYD ULMAN, DirectorNorthern Division

Preface

HE INTRODUCTION TO The Uses of Account-ing in Collective Bargaining points out the need for anunderstanding of accounting terminology and the in-terpretation of items in financial statements for thoseengaged in collective bargaining.Members of negotiating teams may have had little

formal education in accounting. Therefore, the presen-tation of certain material must of necessity be on anelementary level. This booklet is not an accounting text.It emphasizes comprehension of accounting procedures,the way accountants differ in their treatment of them,and the effect of such procedures on reported profits. Itis the reported profits figure that features in a discussionof ability to pay, and an understanding of the account-ing procedures followed will also afford a basis for com-parison of operating results with other companies.The chapter on suggestions for further reading should

prove helpful for continued study. For those desiringproficiency in accounting, a more formal course of studyis recommended.

HmARY C. FISCHER, C.P.A.

Lix ]

ContentsI. INTRODUCTION 1

II. THE MFANMNG OF ACCOUNTING. 41. Definition of Accounting. 42. Accounting Principles .63. Financial Statements. 9

III. FiNANciAL STATEMENTS ILLUSTRATED . . 111. Principal Financial Statements-the Bal-

ance Sheet and the Statement of Incomeand Expense . .12

2. Statement of Retained Earnings . . . 133. Statement of Source and Application ofFunds . .13

4. Supporting Schedules.. 15IV. THE BALANCE SHEET . .22

1. Assets . .232. Liabilities . .343. Stockholders' Equity ..38

V. THE STATEMENT OF INCOME AND EXPENSE . 421. Income .442. Cost of Goods Sold. 453. Depreciation Charges . 46

[xi]

xii * CONTENTS

4. Depletion Charges .495. Selling: General and Administrative Ex-

penses . .506. Research and Development Expenses 517. Net Income for the Year ..52

VI. EFFECT OF INCOME TAX PROVISIONS ON RE-PORTED EAmRINGS .531. Individual Income Taxes .552. Partnerships .563. Corporations .574. Net Operating Loss-Carryback and Car-

ryover .615. Investment Credit .62

VII. ANALYSIS OF FINANcLAL STATEMENTS . . . 641. Financial Statement Ratios-Measure of

Earnings and Productivity .662. Financial Statement Ratios-Measure of

Financial Management .713. Ratios of Special Importance to Investors . 77

VIII. ACCOUNT[NG REcoEDs DESCIBMED: THEiR USEIN CLAIMS OF INABnrrY TO PAY. .821. Accounting Records Described . . . 822. Employer's Claim of Inability to Pay In-

creased Wages . .86IX. COMPLIANCE WITH TERMs OF THE COT .1 IVE

BARGAINING AGREEMENT AS TO WAGES AND

FRINGE BENEFITS . .911. The Need for Compliance. .912. Responsibility for Employee Records . . 95

CONTENTS * xiii

3. Responsibility for Assignment of Auditorsin Connection with Fringe Benefits . . . 96

4. Responsibility for Assignment of Auditorsin Connection with Both Wages and FringeBenefits . ..... . ........... . . 97

5. Performing the Audit . . . . 98X. SOURCES OF FINANcLAL INFORMATION . . . 101

1. General and Background Information . . 1012. Financial Reporting Services. . 1043. Corporation Financial Reports. . 105

XI. SUMMARY AND CONCLUSION. 107XII. SUGGESnONS FOR FURTHER READING . . . . 109

1. Accounting. . 1092. Security Analysis .1113. Financial Management .1124. Income Taxes .1135. General .1146. Guide to Sources of Financial Information. 116

I. Introduction

COLLECTIVE BARGAINING has been estab-lished as the accepted means by which representativesof organized labor and of management reach agreementas to wages, fringe benefits, hours of work, and workingconditions. Labor's immediate objective is an adequatereturn for its work and thereby improvement of theworker's standard of living. To management it is vitalthat the terms concluded permit the continued profit-ability of the enterprise and a return on the investmentof stockholders.Union representatives in a bargaining role are familiar

with the desires of their members and have acquiredsome working knowledge of the industry. The assump-tion of this booklet, however, is that they also need tomake use of available and pertinent financial informa-tion as an additional tool in collective bargaining.Sources of financial information discussed later in thisbook make such data available.

Such financial information will not only be of interestas an indication of the employers' ability to pay, but itmay also show the rate of growth of the enterprise andits standing as compared to other firms in its field.

[ 1]

2 * ACCOUNTING IN COLLECTIVE BARGAINING

Recent emphasis by labor unions on participation oftheir members in the results of increased productivityrequires the assembling and analysis of financial data.From time to time, the government has suggested"guidelines" or "guideposts" of percentage wage in-creases that would not upset the stability of the economyas a whole, another need for unions to use financial datain their attempt to equate such "guideposts" with theresults to the industry of labor's increased productivity.

It may be argued that because labor negotiators maybe assisted by professional advisers, they need not beproficient in understanding of financial statements andaccounting terminology. However, since accountingdeals with financial transactions, it is in effect the lan-guage of business, and the representatives of laborshould have a knowledge of accounting terminology inorder to properly communicate with managementshould such references be brought up during the courseof the negotiations.

Negotiations with smaller enterprises may not entailthe use of professional advisers, and here the individualnegotiator should indeed be conversant with accountingterminology. Furthermore, the decision-making processand the requirement to report to the union membersplaces the burden on the negotiating committee for aclear understanding of all financial matters involved.From management's viewpoint one would think that

it would expedite negotiations and simplify communica-tion if both sides in the negotiating process understoodthe meaning of any financial terms that may arise.

In subsequent chapters of this booklet the reader will

ACCOUNTING IN COLLECTIVE BARGAINING * 3

note that accountants differ in their treatment of finan-cial data which is reflected on the "bottom line" or profitfigure of the operating statement. An understanding ofthe makeup of the items in that statement is therefore ofimportance. Certain financial ratios will provide ameasure of the earnings and productivity of the enter-prise. Of significance too is the effect of income tax pro-visions on the results shown in the operating statement.

Analysis of the Balance Sheet or Statement of Finan-cial Condition will provide significant ratios, thoseshowing the utilization of plant and equipment and theliquidity of the organization among them.

It will be of some help to the negotiator if he has ageneral understanding of the structure of the businessorganization with which he is dealing and its accountingprocesses and records. This may be particularly usefulshould management offer to "open its books" on a claimof inability to pay. True, the union negotiating com-mittee may call upon an accountant for this purpose, butagain the committee will have a clearer understandingof what is done when it reports back to the members.

In matters of contract enforcement of wage, pension,and health benefit provisions, the collective bargainingagreement often provides for inspection of records. Suchuse of the accounting records will be reviewed in somedetail.To summarize, the entire focus of this booklet is to

provide a general understanding of the uses of account-ing in collective bargaining for whatever help it mayoffer to those directly concerned with the main task ofnegotiations.

II.The Meaning ofAccounting

IN THIS AGE OF scientffic achievement it maybe popularly assumed that accounting too has developedto become an exact science. However, it will be seen thatby its very nature accounting is unfortunately not anexact science. In fact, it is not a science at all, but an artthat requires judgment in its practice. Therefore, it isnecessary to know what to expect from its applicationin industry. The task is not too difficult and its under-standing will be rewarding for those who are confrontedwith its use in a collective bargaining situation.

1. DEFINITION OF ACCOUNTING

An accounting bulletin of the American Insti-tute of Certified Public Accountants sets forth thefollowing definition of accounting developed by its com-mittee on terminology:Accounting is the art of recording, classifying, and summa-rizing in a significant manner and in terms of money, transac-

4

ACCOUNTING IN COLLECTIVE BARGAINING I

tions and events which are, in part at least, of a financialcharacter, and interpreting the results thereof.(Acounting Terminology Bulletins, No. 1, Review and Re-sume (New York: The American Institute of Certified PublicAccountants, 1953) p. 9.)

Accounting may be called the language of businessand it is used to control operations and to arrive at a re-port of the financial accomplishments of the businessorganization. Trained persons make use of record sys-tems and procedures to maintain internal control anddevelop the financial data required for reporting. Re-ports are required for management, stockholders, taxingauthorities, and for many public and private agencies,dependent upon the nature of the enterprise. Suchagencies may include the Securities and Exchange Com-mission, Utility Commissions, the Interstate CommerceCommission, and credit agencies. Dun & Bradstreet,Inc. is an example of a private agency requiring financialinformation.For further clarification and in the light of continuing

business development, the preceding definition of ac-counting has been expanded in a later accounting re-search study to read as follows:Accounting is the body of knowledge and functions con-cerned with systematic originating, authenticating, re-cording, classifying, processing, summrizing, analyzing,interpreting, and supplying of dependable and significantinformation covering transactions and events which are, inpart at least, of a financial character, required for the man-agement and operation of an entity and for the reports that

5

6 * ACCOUNTING IN COLLECTIVE BARGAINING

have to be submitted thereon to meet fiduciary and otherresponsibilities.

(Paul Grady, Accounting Research Study No. 7, "Inventoryof Generally Accepted Accounting Principles for BusinessEnterprises" (New York: The American Institute of CertifiedPublic Accountants, Inc., 1965) p. 4.)

2. ACCOUNTING PRINCIPLES

Accounting principles refer to the develop-ment of a body of applicable rules derived through usageand practice, but subject to the judgment of the skilledaccountant in their application in each instance. It is thevariation in treatment of accounting procedures under

ACCOUNTING IN COLLECTIVE BARGAINING 0 7

these rules to which the reader of a financial statementmust be alerted.Differences in treatment of certain items by account-

ants will markedly affect reported earnings. For ex-ample, research and development costs may be chargedoff to expense during the current year or spread overseveral years. Methods and rates of depreciating plantand equipment, and methods of computing the inven-tories of merchandise may differ between companies inthe same industry.

It is an accounting principle that a provision for de-preciation of plant and equipment should be set up inthe accounts of the enterprise by a charge to expense inorder to provide for its decline in value through use.However, someone must exercise judgment as towhether, for example, a 5-year or 10-year useful lifeshould be assigned to a piece of equipment. If the orig-inal cost is $55,000 and assuming a salvage value of$5,000, then the amount to be depreciated is $50,000.Use of a 5-year life results in an annual expense of$10,000 (1/5 of $50,000). Use of a 10-year life results inan annual expense of $5,000 (1/10 of $50,000).Here we see that the exercise of judgment to use a

5-year life rather than a 10-year life has increased re-ported expense by $5,000 with a consequent decrease inreported earnings by a like amount. Tax considerationsmay influence judgment on how depreciation, inven-tories, research and development costs, and certain otheritems are to be treated. These will be touched uponlater on.

8 * ACCOUNTING IN COLLECTIVE BARGAINING

When the independent public accountant retained forthe annual audit examines the financial statements, herenders an "accountants opinion" with the report. Thefirst part of his letter states the nature of the examina-tion made "in accordance with generally accepted audit-ing standards." The opinion portion of the letter reads"In our opinion, the accompanying balance sheet andstatement of income and earnings retained for use in thebusiness present fairly the consolidated financial posi-tion of the ..... Company and its subsidiaries at ..(date), and the consolidated results of their operationsfor the year then ended, in conformity with generallyaccepted accounting principles applied on a basis con-sistent with that of the preceding year."The significant phraseology is that the statements

were prepared in conformity with generally acceptedaccounting principles, and that such principles are con-sistently applied each year for that company. The ap-plicable body of accounting rules is not only generallyaccepted by the accounting profession, but its usage hasbeen generally accepted by the business and the finan-cial world.Where conflicts in accounting treatment have arisen,

Accounting Research Bulletins have been issued by theCommittee on Accounting Procedure of the AmericanInstitute of Certified Public Accountants for purposes ofclarification of procedures to be followed. More recently,an Accounting Principles Board has been establishedby the American Institute of Certified Public Account-ants to review the need for uniformity in accounting

ACCOUNTING IN COLLECTIVE BARGAINING

treatment. The American Accounting Association isanother organization that has spoken out on accountingprmciples.The Securities and Exchange Commission has issued

rules and regulations regarding financial statements thathave had an effect on accounting practice and financialreporting.

Variation in accounting treatment will affect only alimited number of items in the operating statement, butit may have great impact on the net earnings reported.This is covered in Chapter V on the Statement of Incomeand Expense.

3. FINANCIAL STATEMENTS

The accounting process includes preparationof the two principal financial statements: the BalanceSheet or Statement of Financial Condition, and theOperating Statement or Statement of Income and Ex-pense.

Basically the Balance Sheet lists the resources of theorganization as of the statement date. By inspection ofthe statement we can observe such matters as ability topay outstanding obligations, working capital, and in-vestment in plant and equipment.The Operating Statement relates in summary form

the financial results of the past period. It will show thevolume of business, costs and expenses, and the earningsremaining for shareholders. Comparison can be madewith past periods for trends in sales volume, labor costsin relation to sales, net income, and other data.

0 9

10 * ACCOUNTING IN COLLECTIVE BARGAINING

III. Financial StatementsIllustrated

IINANCIAL STATEMENTS are prepared by theaccounting department of the business organization atregular intervals in order to provide information as to itsresources and profitability. These statements reflect insummary form financial transactions, which have takenplace during the accounting period. Statements of oneaccounting period may be compared with those of aprevious one in order to determine what changes havetaken place in financial resources and in operating activ-ity and net profits.A corporation may own the capital stock of other

companies or "subsidiary corporations." These compa-nies may be in allied enterprises, or they may be incompletely unrelated businesses. An example of theformer is a parts supplier owned by an automobile man-ufacturer, and an example of the latter is an appliancemanufacturing subsidiary owned by the same automo-bile manufacturer. At the end of the fiscal year, thefinancial statements of the subsidiary corporations are

11

12 * ACCOUNTING IN COLLECTIVE BARGAINING

combined with the statements of the parent corporationto form "consolidated" financial statements.

Financial reports are prepared at least annually, butthey may be supplemented by monthly, quarterly, orsemiannual statements. An organization may preparethese reports at the end of each calendar year, or it mayadopt a natural business year as its fiscal year. In thelatter event, the annual financial statements will covera complete seasonal cycle of its business activity, endingwhen its inventories are at their lowest point of the year.For example, many department stores adopt a fiscalyear which ends on January 31. This offers them anopportunity to complete the Christmas season and toclear out additional merchandise in January pre-inven-tory sales. By the end of its natural business year onJanuary 31, more merchandise has been converted intosales, the work entailed in taking stock is reduced, andnet profits can be more accurately determined.

1. PRINCIPAL FINANCIAL STATEMENTS

Chapters IV and V explain in detail the itemsmaking up the two principal financial statements,namely the Balance Sheet and the Statement of Incomeand Expense. Figures 1 and la provide an illustration ofthe fonner and Figure 2 illustrates the latter statement.Most annual financial reports also include a Statement

of Retained Earnings (Figure 3) and a Statement ofApplication of Funds (Figure 4). Additional financialinformation for management's use may include sched-

ACCOUNTING IN COLLECTIVE BARGAINING * 13

ules furnishing a detailed breakdown of items summa-rized in the principal financial statements. Examples area Schedule of Cost of Products Sold (Figure 5) and aSchedule of Cost of Goods Manufactured (Figure 6).

2. STATEMENT OF RETAINED EARNINGS

It is normal for the business enterprise toretain part of its profits for its continued growth and inorder to cover possible future losses. Therefore, only aportion of the annual earnings are paid to stockholdersas dividends.The Statement of Earnings retained for use in the

business (Figure 3) sets forth the balance of retainedearnings at the beginning of the year, is increased by theaddition of the net income for the year, and is reducedby the amount of dividends declared. The balance atthe end of the accounting period is part of the stock-holders' equity (Figure la).

Extraordinary gains and losses, not derived from nor-mal operations of the business, are also shown in thisstatement. For example, an award by a court as theresult of a patent infringement suit would be shownhere rather than in the Statement of Income andExpense.

3. STATEMENT OF SOURCE ANDAPPLICATION OF FUNDS

In recent years it has become customary forcompanies to include as part of the annual report a

14 * ACCOUNTING IN COLLECTIVE BARGAINING

Statement of Application of Funds (Figure 4). This state-ment summarizes the source of all cash funds receivedduring the fiscal year and indicates how the funds soobtained were applied. It sets forth the changes occur-ring in financial resources between reporting periods.Amounts shown in the illustration were derived from

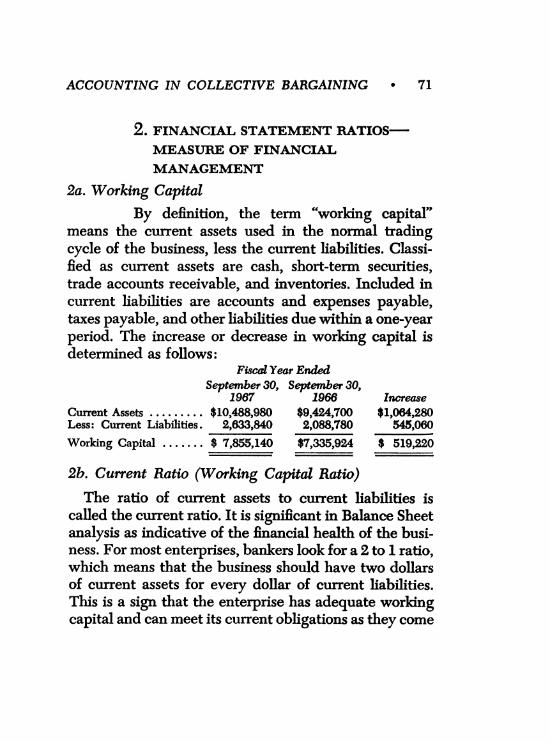

a comparison of the Balance Sheet amounts at the be-ginning of the fiscal year with those of the end of thefiscal year (Figures 1, la). The year's increases or de-creases in assets, liabilities, and capital are the itemssummarized in the Statement of Application of Funds.From this statement can be obtained the "Cash Flow"

for the year (net income plus charges that did not in-volve an actual cash outlay). It can be observed whetheradditional funds were obtained from the sale of secur-ities and what use was made of funds derived fromprofits and from other sources. For example, the state-ment illustrated in Figure 4 shows total expendituresfor new plant and equipment of $640,320, and an in-crease in working capital of $519,220. Comparison of thecurrent assets and current liabilities between the begin-ning and end of the periods furnishes the increase ordecrease in "working capital."A working capital increase may represent a net in-

crease in cash, accounts receivable, and inventories.Comparison of amounts in the fiscal year's beginningand ending Balance Sheets will indicate changes thatmay be a key to future developments. For example, alarge increase in the finished goods inventory withoutan accompanying increase in volume of business for the

ACCOUNTING IN COLLECTIVE BARGAINING

year may point towards a forthcoming slack in produc-tion until an inventory reduction is achieved.

4. SUPPORTING SCHEDULES

The Schedule of Cost of Products Sold (Fig-ure 5) provides the detail relating to the amount shownin the Statement of Income and Expense (Figure 2).The provision for depreciation is often shown separatelyfor statement purposes because it does not entail theexpenditure of cash.The Schedule of Cost of Goods Manufactured (Fig-

ure 6) provides a further breakdown of the total shown

* 15

16 * ACCOUNTING IN COLLECTIVE BARGAINING

under this caption in the Schedule of Products Sold(Figure 5). In a wholesale or retail business the Scheduleof Cost of Products Sold would show the total cost ofmerchandise acquired by purchase, eliminating the needfor a supporting Schedule of Manufacturing Costs.

FIGURE 1MANUFACrURIG COMPANY OF AMERCA

CONSOLiDATED BALANCE SHEETASsETS

Years EndedSeptember 30,

Current Assets 1967 1966Cash .......................... $ 1,135,580 $ 957,490Short-Term Securities-At Cost 841,120 596,450

(Approximates Market)Trade Accounts Receivable, Less Allow-

ances of $61,400 (1966-$51,000) . 2,977,280 2,625,890Inventories-At Lower of Cost or MarketRaw Materials and Work in Process 2,465,830 2,305,240Finished Products ........ ...... 3,069,170 2,939,630

Total Current Assets ........ $10,488,980 $ 9,424,700

Property, Plant, and EquipmentBuildings and Equipment-At Cost.. $10,642,590 $10,002,270

Less: Accumulated Depreciation .. 5,270,130 4,596,540

$ 5,372,460 $ 5,405,730Land-At Cost .........5......... 60,100 560,100

Total Property, Plant andEquipment-Net ........ $ 5,932,560 $ 5,965,830

Other AssetsPrepaid Expenses and Deferred

Charges ............. ......... $ 370,170 $ 365,780Investments-At Cost ...... ...... 137,830 132,810

Total Other Assets ..... .... $ 508,000 $ 498,590$16,929,540 $15,889,120

ACCOUNTING IN COLLECTIVE BARGAINING * 17

FIGURE 1AMANUFACTURING COMPANY OF AMERICA

CONSOLIDATED BALANCE SHEETLIABILMIES AND STOCKHOLDERS' EQuITY

YeaSept

Current Liabilities 1967Accounts Payable ........ ........ $ 1,296,290Accrued Taxes, Interest and

Other Expenses ........ ........ 264,310Loans Payable to Banks ..... ..... 142,270Dividends Payable ....... ........ 117,430Income Taxes Payable ... ....... 63,540Long-Term Debt Due WithinOne Year ........... ......... 150,000

Total Current Liabilities .... $ 2,633,840Long-Term Liabilities

5% Sinldng Fund DebenturesPayable $150,000 Annually 1967-1968, Less Amount Called ForRedemption November 1, 1967 .... $2,850,000

Deferred Federal Income Taxes .... 335,500Total Long-Term Liabilities.. $ 3,185,500

Stockholders' Equity6% Cumulative Preferred Stock

Authorized 50,000 Shares at $100.00Par Value

Outstanding 8,010 Shares(1966-7,170) ......... $ 801,000

Common StockAuthorized 350,000 Shares at $10.00

Par ValueOutstanding 234,757 Shares

(1966-233,248) ......... 2,347,570Capital Surplus

Additional Capital Paid In ...... 969,500Earned Surplus

Earnings Retained For Use in theBusiness ... ...... 6,992,130

Total Stockholders' Equity .... $11,110,200$16,929,540

rs Endedtemrber 30,

1986$ 1,085,320

224,900134,300116,620527,640

-0-

$ 2,088,780

$ 3,000,000261,300

$ 3,261,300

$ 717,000

2,332,480

887,580

$ 6,601.980$10,539,040$15,889,120

18 * ACCOUNTING IN COLLECTIVE BARGAINING

FIGuRm 2MANUFACTURIG CoMPANY OF AUMECA

CONSOLIDATED STATEMENT OF INCOME AND EXPENSEYears EndedSeptember 30,

Income 1967 1966Net Sales ........................ $25,766,050 $24,095,480Other Earnings .123,83 . 123,830 115,630

Total .$25,889,880.. $25,889,880 $24,211,110Costs and Expenses

Cost of Products Sold, Exclusive ofDepreciation .$17,404,840.. $17,404,840 $16,450,960

Depreciation .673,59 673,590 675,040Selling, General and AdministrativeExpenses .5,223,23 ..223,230 4,893,490

Taxes-Exclusive of Taxes on Income 644,150 602,390Interest Expense .142,50 142,500 142,500

Total .$24,088,310.. $24,088,310 $22,764,380Earnings Before Income Taxes.$ 1,801,570 $ 1,446,730

Provision For Income TaxesCurrent Year . $ 820,900 $ 557,700Deferred .74,20 74,200 139,600

Total . $ 895,100 $ 697,300Net Income For the Year . ............$ 906,470 $ 749,430

FiGuRE 3STATEMENT OF EARNINGS RETAINED FOR USE IN THE BusINEss

Balance At Beginning of Year . $ 6,601,980 $ 6,360,840Net Income for the Year .906,47 906,470 749,430

Total .$ 7,508,450 $ 7,110,270Cash Dividends Declared

Preferred Stock-$6.00 A Share $ 48,070 $ 42,000Common Stock-$2.00 A Share ..... 468,250 466,290

Total . $ 516,320 $ 508,290Balance At End of Year .$ 6,992,130 $ 6,601,980

ACCOUNTING IN COLLECTIVE BARGAINING * 19

FiGuRE 4

MANUFACTURING COMPANY OF AMERICACONSOLIDATED STATEMENT OF SOURCE AND APPLICATION OF FuNDs

YEAR ENDED SEPTEMBER 30, 1967Source of FundsFrom Operations:Net Income .............. .................... $ 906,470Charges Which Did Not Involve Current

ExpendituresProvision for Depreciation and Depletion.673,590Provision for Deferred Income Taxes ..... ...... 74,200

Total From Operations ("Cash Flow") ..... ... $1,654,260Sale of Preferred Stock ......... ................. 84,000Sale of Common Stock Under Option Plans-

1,509 SharesCredit to Common Stock ..... ...... 15,090Credit to Capital Surplus ..... ...... 81,920

Total ................ ................... $1,835,270

Application of FundsDividends Declared

Preferred Stock ........... .................... $ 48,070Common Stock ........... .................... 468,250

Expenditures for Property, Plant and Equipment ...... 640,320Sinking Fund Debentures Called for Redemption 150,000Deferred Charges ........... .................... 4,390Investments ................. ................... 5,020Increase in Working Capital ........ ............... 519,220

Total ................ ................... $1,835,270

20 * ACCOUNTING IN COLLECTIVE BARGAINING

FIGUiM 5MANUFACTURING COMPANY OF AMERICASCHEULE OF COST OF PRODUCTS SOLDYEAR ENDED SEPTEMBER 30, 1967

1967 1966Finished Goods Inventory, October 1 .. $ 2,939,630 $ 2,762,500Add: Cost of Goods Manufactured .... 18,207,970 17,303,130

Merchandise Available for Sale ....... $21,147,600 $20,065,630Less: Finished Goods Inventory,

September 30 ................... 3,069,170 2,939,630Cost of Products Sold .........

Cost of Products Sold, ExcludingDepreciation ..............

Depreciation ................Total ....................

$18,078,430

$17,404,840673,590

$18,078,430

FiGumR 6MANUFACTURING COMPANY OF AMERICA

SCHEDULE OF COST OF GooDS MANUFACTUREDYEAR ENDED SEPTEmBER 30, 1967

Raw MaterialsInventory, October 1, 1966. $ 1,845,100Purchases ......... ...... 11,500,220Freight in ......... ...... 828,150

Total ........ ..... $14,173,470Less: Inventory,

September 30, 1967 1,975,630Raw Materials Used.

Direct Labor CostsFactory Wages ....... .... $ 3,760,000Fringe Benefits ....... .... 376,000Payroll Taxes ........ .... 253,700Compensation Insurance ... 18,800

Total DirectLabor Costs .....

$17,126,000

$16,450,960675,040

$17,126,000

Percentageof

Total Cost

$12,197,840 67.0%

4,408,500 24.2%

ACCOUNTING IN COLLECTIVE BARGAINING

Manufacturing OverheadFactory Superintendents $ 36,000Indirect Labor ........... 162,000Fringe Benefits,

Taxes and OtherIndirect Labor Costs .... 46,900

Light, Heat and Power ..... 230,000Factory Supplies Used ..... 175,000Repairs ana Maintenance 240,000Depreciation-Buildingsand Equipment ......... 673,590

Other Factory Overhead ... 68,200Total ManufacturingOverhead.

Total Materials, Laborand Overhead Costs.

Deduct: Increase in Costs Allo-cated to Work in Process

Inventory, September30, 1967 ........ $ 490,200

Inventory, October1, 1966 ......... 460,140

1,631,690 9.0%

$18,238,030 100.2%

30,060 0.2%$18,207,970 100.0%

* 21

Cost of Goods Manufactured..

IV. The Balance Sheet

l7HE FIRST STATEMENT to be examined is theBalance Sheet, sometimes called the Statement of Finan-cial Condition. Listed in summary form are the Assets,Liabilities, and Net Worth or Capital of an organizationas of a given date.An asset is a thing of value, such as cash or merchan-

dise. On the other hand, a liability is an amount ofmoney owed or due to others, such as for merchandisepurchased or for money borrowed.

Net Worth or Capital may be determined from thefundamental equation, viz:

Assets minus Liabilities equal Net Worth. Stated an-other way, this equation may read:

Assets equal Liabilities plus Net Worth.As an example, assume total assets of $30,000 and

total liabilities of $20,000, and insert the figures for theequation as follows:

Assets $30,000 minus Liabilities $20,000 equal NetWorth $10,000

Assets $30,000 equal Liabilities $20,000 plus NetWorth $10,000

22

ACCOUNTING IN COLLECTIVE BARGAINING * 23

Presenting this information in outline Balance Sheetform results in the following financial statement:

Assets $30,000 Liabilities $20,000Net Worth(Capital) 10,000

$30,000 $30,000

The Balance Sheet may list separately such assets ascash on hand, cash in checking account, and cash insavings accounts, or these items may be classified underthe one heading of "Cash." Business financial statementsavoid an excess of detail and combine items of assetsunder standardized headings such as Cash, AccountsReceivable, and Merchandise Inventory.

Assets are further classified on the Balance Sheetunder group headings in accordance with their liquidity(the rate at which they may be converted to cash) andtheir nature. Liabilities are usually classified in the orderthat payment will be due, viz: those due currently withinone year and those due after one year. A classified Bal-ance Sheet is illustrated in Chapter III, Figures 1, la.

1. ASSETSla. Current Assets

Items classified as Current Assets are in thefirst grouping of Assets on the Balance Sheet becausethey are the most liquid. Current Assets include, cash,short-term securities, trade accounts receivable, notesreceivable, and merchandise inventories. The accepted

24 * ACCOUNTING IN COLLECTIVE BARGAINING

S2

6

ACCOUNTING IN COLLECTIVE BARGAINING * 25

usage of the classification refers to cash or assets that willbe converted into cash within a period of one year.The cycle of business activity is one in which raw

material inventory is converted into work in process andthen into finished goods. The sale of finished goods re-sults in charge accounts to customers. Collection ofthese charge accounts (accounts receivable) results inthe receipt of checks deposited to cash accounts.These current assets are in constant use and turn over

in operating the business. For this reason, after deduc-tion of the current liabilities of the business, these assetsare called the working capital.

Cash: Included are cash on hand for deposit, cashin checking accounts, and cash in savings and savingsand loan accounts.

Short-Term Securities: Treasury Bills and listed stocksand bonds used for temporary investment of excess cashare shown under this category. However, long-term in-vestments are shown under a separate classification, notas current assets.Accounts Receivable: This represents the total on the

statement date of amounts due from customers arisingfrom the sales of goods or services. It is usual in mostbusinesses, under the terms of sale, to allow the customera certain number of days before payment is due. Forexample, the manufacturer may sell to the wholesalerunder terms of 2/10, net 30. This means that he maydeduct a discount of 2 percent if he pays the bill withinten days, and he must pay the full amount if he pays in30 days when the bill is finally due.

26 * ACCOUNTING IN COLLECTIVE BARGAINING

Notes Receivable: Arrangements may be made withcertain customers, permitting them to extend the periodof payment by converting their open account receivableinto a longer term written promissory note receivable,payable on a certain date for the amount due and includ-ing a rate of interest. The amount due will no longerappear under the heading of accounts receivable, butwill be shown under the notes receivable headinginstead.

This is a usual practice in certain industries, and inothers it is done only as a special accommodation. In anyevent, receipt of a note permits the seller to "discount"it or borrow money from his own bank with the note ascollateral. When due it is presented by the bank to thecustomer for payment. If not paid, or "dishonored," theseller must make good and then proceed against thecustomer for payment.A note receivable may also arise out of a cash loan

to customers or to others. If the due date is more thanone year from the date of the Balance Sheet, such notesare not shown under the heading of Current Assets, butare classified separately or as Other Assets.Allowance for Doubtful Accounts: Despite the careful

extension of credit, most businesses cannot avoid somebad debts arising from nonpayment of accounts receiv-able. To provide for this contingency, an estimatedpercentage of credit sales is recorded in an account onthe books as a reserve to allow for possible doubtfulaccounts. When the Balance Sheet is prepared, thisallowance, or reserve, is deducted from the totals of

ACCOUNTING IN COLLECTIVE BARGAINING * 27

Accounts Receivable and Notes Receivable, leaving thenet estimated collectible amount as the Balance SheetAsset.

Should a bad debt occur at a subsequent date, theamount is charged against the Reserve Account, reduc-ing both the Accounts Receivable and the ReserveAccount, and having no effect on profit or loss at thattime. Profits are reduced in the year when the reserve isoriginally provided for in the accounts.

Inventories

Inventories are quantities of merchandise on hand atthe statement date to which a dollar value has beenassigned, usually the lower of cost or market. Quantitiesare determined by physical count or listed from per-petual inventory records, and checked against the actualstock. Inventory totals are usually listed under the sub-headings of raw materials, goods in process, finishedgoods, and factory supplies.Raw Materials on hand refer to materials entering

directly into the manufacture of the finished productand include the cost of freight, import duties, and otherincidental costs required to bring such materials intothe factory.Goods in Process (or work in process) include the cost

of raw materials, direct labor, and factory overhead upto the unfinished stage of manufacture of such items onthe inventory date. Factory overhead includes fixedcharges such as depreciation and property taxes, andvariable charges such as supervisory and indirect labor.

28 * ACCOUNTING IN COLLECTIVE BARGAINING

Factory overhead may be allocated on some unit basissuch as a percentage of raw materials, or of direct labor,or of both.A "standard cost" method of pricing goods may be

used for the various stages of production. Such standardunit costs are derived from raw material cost studies,labor time and motion studies, and unit overhead costallocations.

Finished Goods refer to merchandise in stock, readyfor shipment to customers.

Factory Supplies refer to unused items on hand notdirectly becoming a part of the finished product, butrequired in the factory during the course of its manu-facture, such as machine oil for the equipment or clean-ing supplies for the plant.

Valuation of InventoriesInventories are generally valued at purchase price or

cost of manufacturing, not at selling price to customers.If the purchase price of raw materials has dropped sincethe acquisition of the raw materials on hand, the govern-ment permits the use of the lower market price for in-come tax purposes. However, a problem appears whencosts are constantly rising. At what prices should itemsremaining in the inventory on the statement date bevalued: Costs of the first lot? Cost of the last lot? Theaverage cost?

Using a First-In-First-Out Valuation (FIFO), costsare assigned in order of acquisition of the merchandiseso that in a market of rising costs the lower priced mer-

ACCOUNTING IN COLLECTIVE BARGAINING * 29

chandise is assumed to have been used first, and thehigher priced merchandise (the current market price) isassumed to remain in the inventory. This method has afavorable effect on profits.

Using a Last-In-First-Out Valuation (LIFO) assumesthat the most recently acquired merchandise is used upfirst, with the oldest merchandise acquired still remain-ing in inventory at the lower acquisition price. In aperiod of rising prices, this results in the most recentlyacquired merchandise being charged to current costs atthe highest cost .Use of this method of inventory valuation may result

in an understatement of the value of the inventorycarried in the Balance Sheet and an understatement ofnet worth. Assigning the most recent cost to the mer-chandise sold results in a lower net profit than wouldbe the case if the earlier cost had been charged.The Weighted Average Valuation is another method

of pricing the inventory to determine the cost of theitems remaining on hand. It consists of totalling thenumber of units purchased during the period and thetotal dollar cost of all these units. Dividing the totaldollar cost by the total number of units purchased givesthe average cost per unit purchased. The quantitiesremaining in the inventory are then priced at this aver-age cost.

Retail stores may use the retail inventory method,which provides for listing the inventory at retail sellingprices and then reducing the total to cost by applicationof an average gross profit percentage.

30 * ACCOUNTING IN COLLECTIVE BARGAINING

Construction companies engaged in long-term uncom-pleted contracts may value construction in progress atcost and add a percentage of profit based on the Degreeof Completion.Knowledge of the method of inventorying used is of

the utmost importance to the reader of the financialstatements. The government permits any of the abovemethods, provided they are consistently followed.When comparing the financial statements of severalcompanies in the same industry, the method of inven-tory pricing should be noted for its effect on profits ofeach company.

lb. Property, Plant and EquipmentThis classification, sometimes called "fixed assets,"

represents the total of assets that are long lasting andnecessary in the operation of the business. Included areoffice and warehouse buildings, factory buildings, ma-chinery and equipment, trucks and automobiles, andoffice furniture. Land is shown separately under thisclassification.

These assets are carried at their original cost of acqui-sition, which includes freight and installation costsnecessary to put machinery in place. Interest and prop-erty taxes incurred during the course of construction ofnew buildings may be included in building costs or maybe charged off as an expense of operations in the yearincurred. If charged to expense before the plant is pro-ductive, such interest and taxes may have a markedeffect on current year's profits.

ACCOUNTING IN COLLECTIVE BARGAINING * 31

U I

Accumulated DepreciationBuildings, machinery and equipment, trucks and

automobiles, and office furniture are all subject to agradual wearing out through use and action of theelements. Machinery and equipment may also becomeobsolescent (out of date) because of the invention of newmachines or a new process which makes the old onesuneconomic to use and noncompetitive with the newones.

I

32 * ACCOUNTING IN COLLECTIVE BARGAINING

By annual charges to a depreciation expense which inturn is charged against profit, an attempt is made towrite off the cost of these assets over a period of timethey are estimated to be of use in the business. Theseannual depreciation charges to expense are accumulatedin a separate account for the purpose of "evaluating" orreducing to "book value" the cost of the plant and equip-ment accounts on the Balance Sheet. Cost less accumu-lated depreciation represents the estimated undepreci-ated cost and salvage value of these assets.

LandLand is shown separately in the Balance Sheet be-

cause it is not subject to depreciation. However, landcontaining timber, oil, coal, iron ore, or other naturalresources is subject to depletion, or a using up of itsresources, and provision may be made in the BalanceSheet for a gradual reduction in value of such assets,offset by a charge against current year's profits.

Tools, Patterns and DiesThese assets may be included in the totals of plant

and equipment shown in annual reports. At other timesthey may be grouped as a separate asset under the gen-eral classification of property, plant and equipment.Tools, patterns and dies have only short useful lives,sometimes for merely one model year. For that reasonat the end of the accounting period the remaining usefulitems are inventoried at cost less depreciation. The ex-

ACCOUNTING IN COLLECTIVE BARGAINING * 33

cess over this amount is charged to manufacturingexpense. Any salvage value realized is offset againstsuch expense.A policy of too fast "amortization" (write-off to ex-

pense) of these assets may result in both an understate-ment of assets and of profits for the year.

lc. Intangible Assets

Buildings and equipment are "tangible" items whichcan be physically seen. "Intangible assets," on the otherhand, exist only on paper. Examples are patents andcopyrights, costs of leases, etc. Where these items repre-sent actual costs incurred, they may be amortized(charged off to expense) over the time remaining beforetheir expiration.

Goodwill may represent the cost of acquisition of theassets of a business over their market value and is a pricepaid for acquiring access to customers or earning powerof a business. Financial analysts will ignore this item ifit appears on the Balance Sheet. It may be eliminatedby a charge against capital and surplus, but not againstcurrent year's profits.

ld. Prepaid Expenses and Deferred ChargesThis classification of assets refers to expenses incurred

during one accounting period that are chargeable tooperating expense of subsequent accounting periods.Examples are prepaid insurance premiums, prepaid in-terest, and prepaid rent. The cost of a three-year insur-

34 * ACCOUNTING IN COLLECTIVE BARGAINING

ance premium will be allocated over the period covered;prepaid interest will be charged to expense over the lifeof the loan, etc.

Current accounting practice permits prepaid accountsto be shown under the Current Asset classification orthat of other assets. Either method results in no reduc-tion of profits until the prepaid item is charged off toexpense of the appropriate period.Research and Development Expenue is another ex-

ample of an account that may be carried as a deferredcharge asset on the Balance Sheet when incurred, andsubsequently charged to operating expense over theaccounting periods directly benefiting from the research.Income tax laws permit the company an alternativemethod of charging research and development expenseto operating expense as such charges are incurred. Thismay have a depressing effect on profits one year, whilesubsequent years will reap the benefit of higher profitsshould the research result in new products at lowercosts.

2. LIABILITIES

2a. Current LiabilitiesMost business activity is carried on by credit,

evidenced by bills submitted for merchandise purchasedon open account or notes given to cover open accounts ormoney borrowed from banks and other agencies. In thenormal operating cycle of business activity, materials arepurchased and labor is applied to convert the raw mate-

ACCOUNTING IN COLLECTIVE BARGAINING * 35

rials into finished goods. These finished goods are sold onopen account; later collections are received in cash andthe cash is used to pay liabilities due.

Liabilities for merchandise, payrolls, taxes, loans, etc.,arising out of the operating cycle are classified as currentliabilities. The portion of long-term debt due within oneyear is also classified this way.

Accounts Payable: Amounts due to trade suppliers forsuch items as raw materials and factory supplies aresummarized under this heading on the Balance Sheet.Accrued Taxes, Interest and Other Expenses: As of

the close of the accounting period, amounts may beunpaid for such items as manufacturer's excise taxes,employees' payroll taxes, or for interest on loans.

Similarly, employees may have earned all or part of aweek's pay with payment not due until a date followingthe end of the fiscal year. These items are added toliabilities or "accrued" as due in the Balance Sheet. Theyare also reflected as expenses in the operating accountsfor the accounting period in which they were incurred.

Loans Payable to Banks: This classification representsshort-term (less than one year) loans from banks madeto supplement cash need.

Dividends Payable: The Board of Directors meets and"declares a dividend" to stockholders of record on a cer-tain date, payment to be made at a subsequent date.Thus, Dividends Payable represents the liability fordividends already declared but unpaid. It is offset by acharge against the retained earnings account and doesnot affect the income statement.

36 * ACCOUNTING IN COLLECTIVE BARGAINING

Income Taxes Payable: Federal and state income taxesunpaid on prior year's profits and estimated due on cur-rent profits to date are included under this heading.Long-Term Debt Due Within One Year: Debt install-

ments due within a one-year period are classified ascurrent liabilities on the Balance Sheet, and the balanceis shown below under Long-Term Liabilities.

2b. Long-Term LiabilitiesAmounts due on corporation bonds, mortgages, and

other long-term loans are classified as long-term liabil-ities. From such total is deducted the amount due withinone year for inclusion under the heading of currentliabilities.Debentures or Bonds are represented by certificates

issued in amounts of $1,000 or more by the corporationand represent the written promise of the corporation topay the principal amount on or before a specified datewith interest at a fixed rate payable semiannually. Thebonds may be "registered" to a named individual, orthey may be "coupon" bonds, payable to bearer. Bondsare covered by a group contract or "trust indenture" heldby a trustee and may be secured by property of thecorporation or unsecured.A "sinking fund" provision requires the corporation

to deposit an amount annually with the trustee in orderto establish a fund to retire the bonds. Each year a num-ber of bonds may be "callable" by the trustee and thecash in the sinking fund is used to pay those bond-holders presenting their bond certificates for payment.

ACCOUNTING IN COLLECTIVE BARGAINING * 37

Certain series of bond numbers may be payable atstated intervals and are called "serial bonds." Otherbonds may be "convertible" (exchangeable) into a statednumber of common shares of stock of the corporation inlieu of payment in cash.Cash obtained from issuance of bonds will have an

indirect effect on profits by providing working capitalor machinery and equipment to expand the business andhopefully increase revenue. The direct effect on theoperating statement will be an annual fixed charge forinterest, which is a deduction from profits.

2c. Contingent LiabilitiesNormally liabilities represent amounts determined as

of the statement date to be obligations of the organiza-tion.

However, sometimes there is an element of doubt asto whether an obligation exists. An example is a pendinglawsuit against the corporation for damages. In suchcase a contingent liability may be shown on the BalanceSheet to cover the amount payable if the lawsuit is lost.This provision would be offset by an appropriation ortentative reduction of retained earnings or surplus. Taxlaws do not permit deduction of contingent liabilities asa charge against current profits.

2d. Deferred Federal Income Taxes

In order to reduce the current liability for corporationincome taxes, certain adjustments may be made whichwill have the effect of postponing income taxes to a later

38 * ACCOUNTING IN COLLECTIVE BARGAINING

period. For example, a greater charge for depreciationmay be taken on the tax return than that shown on theStatement of Income and Expense. The deferred federalincome tax account accumulates the temporary savingsin income tax which theoretically will be paid at somelater date.

It should be noted that an increase in the deferredfederal income tax account has been offset by a chargeagainst the current year's profits. (This so-called "con-servative accounting" concept may be difficult for thelayman to grasp. The net effect is to charge currentyear's profits with the greater income tax that wouldhave been paid if the depreciation reported in the in-come statement had been reported on the corporationtax return. The day of reckoning is supposed to comewhen the greater depreciation charges taken on the taxreturn have been exhausted and there is no furtherdepreciation on the equipment in question necessitatingpayment of a larger tax at that time. But with constantlyincreasing investment in plant and use of group or classaccounts to record acquisitions, the variation in corpora-tion income tax may be deferred for a long time. In themeantime profits have been understated by the excesstax charge and the cash is retained in the business. Notall accountants agree with this concept of deferred in-come taxes.)

3. STOCKHOLDERS EQUITY

The capital required to operate a business ismade up of two parts: investment of the stockholders

ACCOUNTING IN COLLECTIVE BARGAINING * 39

or owners in the business, increased by accumulatedearnings retained in the business, and borrowed capitalor long-term debt. (Short-term borrowings are part ofthe trading cycle and are constantly being paid off ascollections are made on sales.)When a business is operated on a great proportion of

long-term debt as compared to the stockholders' invest-ment, it is said that the business has good "leverage,"meaning that it is earning profits with money other thanthat of its owners. However, at the same time net profitsare being reduced by the amount of the interest charge,which is also deductible from corporation income taxes.Payment of dividends to stockholders is made after thenet profit figure has been determined and is not a deduc-tion for tax purposes.Given two competing companies making an equal

profit on sales (before deduction for interest), the com-pany operating with the greater long-term debt willusually show a greater percentage return on stockhold-ers' equity. Preferred stock, common stock, capital sur-plus, and earnings retained in the business make up thestockholders' equity or ownership.

3a. Preferred StockThe preferred stockholders have a prior claim against

dividends and assets than do the common stockholders.The stock is "senior" to the common stock. The preferredstock is said to be "cumulative" when dividends are pay-able in later years if unpaid and skipped in any year. Thepreferred stock may also be "participating" if the stock-

40 * ACCOUNTING IN COLLECTIVE BARGAINING

holders share in dividends paid to common stockholdersin addition to their preferred dividends. The shares maybe "convertible" or exchangeable into a predeterminednumber of common shares.

3b. Common StockThe common stockholders bear the greatest risk, but

are entitled to share in all of the remaining profits aftersatisfying the prior claim of the preferred stockholders.Common stock may have a stated face value or "parvalue" or may be of "no par value" shares with no valuestated. However, this is only an arbitrary matter for thepurpose of complying with state corporation laws, andsuch values have no relation to the actual asset valueper share of stock or to the values at which stocks aretraded on the Stock Exchanges.When the stock is originally issued by the corpora-

tion, amounts received over the par value of the stockare credited to Capital Surplus.

Treasury stock represents stock repurchased by thecorporation after it has been issued. Corporations withexcess cash may later reacquire some of their stockwhen the price is favorable. This has the effect of reduc-ing the capital, but it also increases the per share eam-ings since fewer shares are now outstanding.

Stock splits have no effect on the dollar capitalizationexcept that the number of shares in the hands of thestockholders has been increased, thus usually making iteasier for the shareholder to dispose of part of his stock.

Stock dividends, representing shares of stock given to

ACCOUNTING IN COLLECTIVE BARGAINING * 41

stockholders as opposed to cash dividends, increase thenumber of shares in the hands of stockholders. A booktransfer is made from retained earnings to the morepermanent common stock and/or capital surplus ac-counts.

Stock options grant officers and others the right topurchase stock at a present or later date at a prede-termined price. Thus, if the market price rises, theofficer "exercises his option" and pays the corporationthe option price per share and can later sell his stockand realize a gain.3c. Capital SurplusThe amount paid in by common stockholders over the

par value or stated price of the stock is credited to capi-tal surplus. Transfers are sometimes made to this ac-count from retained earnings in order to restrict theamount of earnings available for cash dividends.3d. Earned Surplus or Retained EarningsAnnual profits are credited to this account and ac-

cumulated in the business from year to year as addi-tional stockholders' equity. Dividends paid to stock-holders are charged against retained earnings (Figure 3).Extraordinary gains and losses (other than from currentoperations) are also added to or deducted from this total.For example, a large sum obtained through a court suitagainst another company for patent infringements wouldbe credited directly to retained earnings, as the amountwas not obtained from the normal revenue of the busi-ness.

V. The Statement ofIncome and Expense

]7HE STATEMENT OF Income and Expensesummarizes items of revenue, cost, and expenses to arriveat the net profit or loss for the accounting period. Sinceit shows the results of operations for the period, thereport is also called the Statement of Operations. Othercommonly used descriptions for this report are State-ment of Earnings or Statement of Profit and Loss, ormerely Statement of Income.

This report should be distinguished from a Statementof Cash Receipts and Disbursements, which summarizesall cash received and all cash disbursed during theperiod. However, cash receipts will include collectionof the prior year's sales, and cash disbursements will in-clude payment of the prior year's bills but will excludebills of the current year not yet paid. Furthermore a cashstatement will include such items as money borrowedor loans repaid which are not income from sales. There-fore, a Statement of Cash Receipts and Disbursementsis inadequate for purposes of stating the results of opera-tions.

42

ACCOUNTING IN COLLECTIVE BARGAINING * 43

The Statement of Income and Expense is prepared onthe "accrual basis." Sales of the accounting period areincluded as income, whether collected or not. Unpaidmerchandise or expense bills are accrued or included incosts and expenses as they are incurred, regardless of thetime of payment. Merchandise remaining in inventory isdeducted from cost of goods sold during the period.The interrelationship of the Balance Sheet and the

Statement of Income and Expense may be better under-stood by noting how accrued items affect each. Forexample, uncollected income from sales is shown on theBalance Sheet as accounts receivable and included in

44 * ACCOUNTING IN COLLECTIVE BARGAINING

income from sales on the Statement of Income and Ex-pense. Unpaid expense bills are included in accountspayable on the Balance Sheet and added to Selling,General and Administrative Expenses on the Statementof Income and Expense.The year-end merchandise inventory deducted from

the cost of products sold in the Income Statement isshown as an asset on the Balance Sheet. The net incomefor the year is included in the accumulated retainedearnings shown in the Balance Sheet.By means of a consolidated Statement of Income and

Expense, the parent corporation and solely owned sub-sidiary corporations combine their individual operatingstatements into one summary statement for the fiscalyear. For comparative purposes, the current year andprior year's figures are usually listed. (See Chapter III,Figure 2.)

1. INCOME

Net Sales refer to total billings for the fiscalyear, less sales returned, allowances made, and sales dis-counts deducted by customers in accordance with theterms. Sales taxes and excise taxes where applicable areexcluded from sales and shown as a liability to the taxingagency. Freight charges are excluded and offset againstthe expense. A separate schedule showing the break-down of dollar sales and number of units sold by productis of interest for comparative purposes and is includedin some published annual reports.

ACCOUNTING IN COLLECTIVE BARGAINING * 45

Other Earnings include such items as interest anddividends received on cash temporarily invested. Salesof supplies and used equipment (not part of the productnormally sold) would be included in other earnings.

2. COST OF GOODS SOLD

Included in cost of goods sold are all costs allo-cated to the merchandise that was sold. (See ChapterIII, Figures 5 and 6.) The cost of raw materials, laborand fringe benefit costs, and overhead costs, adjusted forthe beginning and ending inventories of raw materialsand work in process, make up the cost of goods manu-factured. Adding the inventory of finished goods at thebeginning of the accounting period and deducting theinventory of finished goods at the end of the accountingperiod gives us the cost of goods sold.Overhead costs entering into the cost of goods manu-

factured refer only to factory expenses such as indirectlabor, heat and power, factory supplies, etc. (SeeChapter III, Figure 6.)

In a wholesale or retail business, where no manufac-turing is done, the cost of goods sold is the cost of ac-quiring the merchandise for sale, adjusted for the varia-tion in beginning and ending inventories.

In accounting usage, the term "costs" generally refersto items entering into the cost of goods sold. The term"expenses" generally refers to such items as selling andadministrative expenses. However, the terms are some-times used interchangeably.

46 * ACCOUNTING IN COLLECTIVE BARGAINING

3. DEPRECIATION CHARGES

Depreciation is the estimated amount addedto costs and expenses during the accounting periodrepresenting the wearing out, or increasing inadequacythrough obsolescence, of the buildings and equipment.Equipment declines in value due to age and use. An in-vention of a new machine or process may make the oldequipment obsolete.

Depreciation is often shown as a separate item in theStatement of Income and Expense. However, deprecia-tion of plant and equipment used in a manufacturingbusiness is properly chargeable to factory overhead.

It is expected by means of these annual depreciationcharges to ultimately write off to costs and expenses theentire cost of buildings and equipment, less an estimatedsalvage value. (See discussion of accumulated deprecia-tion in the Balance Sheet in Chapter IV.)One should note carefully that these annual charges

for depreciation are only estimates of additions to costsand expenses made on the books and in the financialstatements. But the effect is to reduce reported profitsby the amount of the depreciation. Charges for deprecia-tion do not as such represent cash outlays. Cash is ex-pended only when the equipment is acquired.

Therefore, the charge against profit for depreciationhas the effect of retaiIning cash in the business until ex-pended for replacement equipment. In fact, unless aseparate fund is set up for the purchase of new equip-

ACCOUNTING IN COLLECTIVE BARGAINING * 47

ment when the old is worn out, the cash so retained mayin the meantime be used for other purposes.The term "cash flow" is used to designate net profits

plus depreciation. Cash flow per share is often indicatedin annual financial reports, as well as the reported earn-ings per share.

3a. Methods of Computing DepreciationVariation in the method of computing depreciation

and the estimated useful life of the asset will affect thecharge for depreciation and stated net profits.The most commonly used method of computing de-

preciation is the Straight Line Method which allocatesthe depreciation equally over the estimated life. Assumea machine costs $12,000, the estimated salvage value is$2,000, and the cost to be depreciated is $10,000. Esti-mating a useful life of ten years, one-tenth of $10,000,or $1,000, is charged to depreciation each year. How-ever, note that if the estimated useful life is five years,the annual charge to depreciation would be $2,000. Inthe first example the resulting net profit would be morethan in that of the second.

In manufacturing plants, a Service Life method maybe used by estimating useful life on the basis of machinehours used, or on the basis of units of production.Tax laws may permit "accelerated" methods of de-

preciation such as the "declining-balance method" andthe "sum of years' digits" method.Under the Declining-Balance Method the amount to

48 * ACCOUNTING IN COLLECTIVE BARGAINING

be depreciated each year is based on cost reduced byeach year's depreciation. Under the Double Declining-Balance Method, taking as an example an amount to bedepreciated of $10,000 and a 10-year life, twice 10 per-cent or 20 percent may be deducted or $2,000 the firstyear. In the second year the deduction is 20 percent of$8,000 ($10,000 less the first year's depreciation) or$1,600. Under this accelerated method greater amountsof depreciation are charged in the early years of themachine's acquisition. As a result of a greater deprecia-tion charge in the early years, the stated profit is reducedin the early years of the life of the equipment.The Sum of Years' Digits method is also an accelerated

depreciation method whereby the annual depreciationdeduction is figured by applying a changing fraction tothe cost of the property. The result is also higher de-preciation charged in the early years. For example, as-sume the cost less salvage value of the equipment is$10,000 and the useful life is five years. The first year'sdepreciation is 5/15 or 1/3 of $10,000 or $3,333. (Thedenominator 15 is arrived at by adding the sum of theremaining years-5 plus 4 plus 3 plus 2 plus 1.)An accelerated method of depreciation may be used

for purposes of preparing the corporation income taxreturns, while the financial statement may show a lowerstraight line depreciation deduction. To properly under-stand the net operating income of a company and to beable to compare the results with companies in similarlines of business, the reader of the financial statements

ACCOUNTING IN COLLECTIVE BARGAINING * 49

should know the depreciation method used. In fact,management often contends that the depreciationcharge should be on the basis of replacement cost andnot original cost. In periods of rising costs for equip-ment, such a practice would increase the charge fordepreciation and reduce stated profits. At this timeneither government tax laws nor conservative account-ing practice permits depreciation based on replacementcost.

4. DEPLETION CHARGES

Depletion Charges is the term used for thegradual using up of what is called a wasting asset, repre-senting a natural resource such as gas, oil, coal, iron ore,timber, etc. Just as for depreciation of equipment, acharge is made against profits for the estimated usingup of this resource. The charge may be made on thebasis of an estimated unit cost of the resource to be ob-tained from the land. Each year the charge for depletionis made on the number of units (or volume) produced.

Current tax laws permit a continuous depletion rateof 273i percent of gross receipts from oil sales, regardlessof the actual unit cost, with a limitation that the deple-tion charge cannot exceed 50 percent of the taxable in-come realized each year from the oil property, calcu-lated without regard for the charge for depletion. Otherrates for minerals are set forth in the tax laws.Where a provision for depletion is deducted from net

profits, the "cash flow" is arrived at by adding the deple-tion and depreciation charges back to net profits.

50 * ACCOUNTING IN COLLECTIVE BARGAINING

5. SELLING, GENERAL ANDADMINISTRATIVE EXPENSES

The expenses included in this grouping are allof the operating expenses, except those included in fac-tory overhead as part of the cost of goods manufactured.There may be a further breakdown, with supportingschedules showing a detailed listing of categories ofselling expenses, shipping expenses, and office and ad-ministrative expenses. Other operating expense itemssuch as taxes and interest expense may be shown sepa-rately in order to emphasize what is being paid to taxingagencies and to lenders for the use of borrowed funds.

Selling expenses include such items as advertisingexpenses, salesmen's salaries, commissions, traveling ex-

>0 oAtD la op -6 .2 %P 0

ACCOUNTING IN COLLECTIVE BARGAINING * 51

penses, and entertaining and sales promotion expenses.Office expenses include office salaries and fringe benefits,telephone, stationery, postage, office occupancy ex-penses. Administrative expenses include officers' salaries,bonuses and fringe benefits, and officers' traveling andentertaining expenses.

Financial statements prepared for management andcredit agency reports will usually fumish a greaterbreakdown of detailed expenses than will the annualpublished reports to stockholders. Stockholders usuallyreceive, with the notice for the annual meeting, a listof the directors of the corporation and their stockhold-ings and a list of the principal officers and their annualsalaries, bonuses, and retirement benefit information.Indirectly then, this will furnish some breakdown of thecharges to administrative expenses for officers' accounts.

6. RESEARCH AND DEVELOPMENTEXPENSES

With federal and state corporation incometaxes taking in excess of 50 cents of each dollar earned,and in view of the highly competitive nature of industry,many corporations are expending increasing amountsfor research and development in their search for newproducts.

Such expenses may not be shown separately in thefinancial report, but may be included in costs charged tothe cost of goods manufactured. It is important to de-termine whether such charges have been abnonnally

52 * ACCOUNTING IN COLLECTIVE BARGAINING

high in the current fiscal year, with a depressing effecton current profits. The full benefits of new products andnew processes discovered through research often maynot increase profits until put to use in subsequent years.

7. NET INCOME FOR THE YEAR

Deducting costs and expenses from gross re-ceipts will show the company's earnings before incometaxes. After deducting estimated federal and state in-come taxes, the remainder is the net income for the year.This net income is added to earnings retained in thebusiness from which stockholders' dividends are paid(Figure 3). (See also the note in Chapter IV relative tocharges for deferred income taxes.)

VI. Effect of Income Taxrovisions on

Reported Earnings

B EFORE EXAMINING how income tax provi-sions affect reported income in financial statements, it iswell to understand how taxes on wage and fringe bene-fits affect employees and employers.The employee's "take home pay" is reduced by deduc-

tions for social security taxes and withholding taxes, forwhich the employer acts as a collecting agent for thefederal government. In California, employees' take homepay is further reduced by the 1 percent tax for disabilitybenefits administered by the Department of Employ-ment. Deductions for contributory pension plans andvacation benefits would further reduce take home pay.The employee pays no income taxes on employer pen-

sion and health insurance contributions made to ap-proved plans for his benefit. The employee is subject toincome taxes when he retires and receives his pension,but at that time if he has little other income his tax willbe negligible.

53

54 * ACCOUNTING IN COLLECTIVE BARGAINING

The employer must match the social security tax de-duction from wages with an equal payment to the In-ternal Revenue Service. He must make quarterly pay-ments of unemployment taxes on wages to states wherehe has employees, and a small annual payment for fed-eral unemployment tax. Wages, payroll taxes, and fringebenefits such as pension and health contributions are alldeductible by the employer from his gross income indetermining his taxable income.

If the employer's effective federal and state incometax rate is 50 percent, then for every dollar paid in wagecosts he is out of pocket 50 cents. (This is true becauseevery dollar of deduction from gross income reduces theincome to be taxed at the 50 percent rate, if that happensto be his effective rate.) The rates will vary betweenemployers operating as sole proprietors and betweencorporations operating in different states, but the prin-ciple remains the same.

Taxable income and rates for corporations and forindividuals are determined in accordance with the In-ternal Revenue Code of 1954 and subsequent amend-ments by Acts of Congress. Regulations and rulings areissued by the Commissioner of Internal Revenue withinthe Treasury Department of the United States.Most states and some cities also have income tax laws.

These laws usually follow closely the provisions of theInternal Revenue Code for the determination of taxableincome. However, tax rates are much lower than federalrates and vary from one state to the other.

ACCOUNTING IN COLLECTIVE BARGAINING * 55

1. INDIVIDUAL INCOME TAXES

Income from business enterprises operated assingle proprietorships is reported on Form 1040, Sched-ule C, of the owner's individual income tax return. Netprofits from the business are added to his other incomeor offset against losses from other sources in arriving athis taxable income subject to individual income tax rates.

Individual income tax rates are subject to periodicchanges by act of Congress. However, 1967 is illustrativewith rates ranging on a graduated basis from 14 percentof the first $500 to 70 percent on taxable income over$200,000. According to the tax table, the tax on the first$200,000 of taxable income on a joint return amounts to$110,980, or an effective rate of 55 percent ($110,980divided by $200,000 = 55 percent).

Self-employed individuals are also subject to a self-employment tax to cover social security and Medicareprovisions of the law, comparable to the tax paid byemployees. For 1968 the maximum self-employment taxis $499.20 (self-employment income of $7,800 at a rateof 6.4 percent).

For a comprehension of how certain corporate trans-actions will affect individual income taxes, it is well tounderstand how dividends received and capital gainsfrom sales of securities are taxed to individuals.

Individuals exclude the first $100 of dividends re-ceived in cash, and include the balance in their incomesubject to individual income tax rates. On a joint return,

56 * ACCOUNTING IN COLLECTIVE BARGAINING

$200 may be excluded. Distribution by a corporation ofshares of its own stock as a stock dividend results in notax to the shareholder until the stock is sold.