in order to reverse the trend of falling stock prices and waning investor confidence, how can dell...

TRANSCRIPT

In order to reverse the trend of falling stock prices and waning

investor confidence, how can Dell find strong growth again in a

computer market dominated by a few key players selling a product

that is becoming increasingly commoditized?

• What is the nature of the competitive landscape in the PC market, who are the key players, and is Dell competing with all of them or do they need to focus only on specific threats?

• What is the current value proposition in today’s market and where can Dell focus their efforts to increase revenue and market footprint?

• How does Dell regain investor and internal confidence in their company, which is key to obtaining the necessary capital to move forward with corporate growth?

What is the nature of the competitive landscape in the PC market, who are the key players, and is Dell competing with all of them or do they need to focus only on specific threats?

Gateway Acer Apple DellStarted similar to Dell with direct sales. However, focus was on individual consumer vs. large business

Switched from ODM to OBM computer maker in 1990s and almost killed company

Spent late 1990s – early 2000s at around 3% global market share.

Used Direct Model from company’s beginning

Briefly surpassed Dell’s US sales in 1994 – but started going the wrong direction around 1997

Purchased Gateway, then Packard Bell, and grew internally to become fastest growing PC provider

Series of innovative products, new operating system, and introduction of Intel processors renewed customer interest

Focused largely on business segment. 70% of revenue from large customers ($1M+) in 1998

2000s led to series of moves to try and save market position and turn company around

Uses 100% Indirect strategy via retailers and distributors

Uses mainly contractors to produce their products.

Focused on high-performance PCs at relatively low prices.

- One year tried focusing on large accounts

- Opened non-stock show rooms

Individual consumer is primary market

Use a variety of distribution channels evenly and even have their own stores.

Focused sales/marketing on Transaction buyers & Relationship buyers.

- “Beyond the Box” strategy with post sales support

- “Back to Basics” strategy to refocus on PCs

Focus is low cost units – particularly Netbooks (smaller systems with limited functionality but good internet capabilities).

Did not want to focus attention on “educating the inexperienced customer”

2007 sold out to Acer Passed Dell in 2009 as second largest PC provider(by units).

Departed from direct model only rarely – 1990 & again presently

Acer & Apple are after a different segment than Dell. They can’t be ignored entirely, but the real threat to Dell’s dominance is the next guy………

Competitive Landscape – are they all direct competitors?

Compaq HP1995 – production based on channel member forecasts

Pre-merger HP shuns any mention of the term “Direct” till ’99

1997 ODM builds PCs after order (standardized & custom PCs)

1999 institutes direct purchase but with “hard deck” for customer size

1997 Direct Sales – but same price as retail

PC sales overall positive but razor thin

1998 reduced direct prices - resellers shunned Compaq PCs1999 – Direct sales & referred sales 29% of business w/ $337M profit. Indirect sales 71% of business and $190M loss.

After years of struggle HP seems to have found a formula that works for them.

- For personal consumers – making the computer a personalized accessory vs. a consumer product.

- For businesses, keeping the relationship and using sales to drive demand – but allowing the customer to be “in control” of the buying process and fulfillment channel.

A closer look at Compaq/HP – the global leaderCompaq/HP

Synergies not immediately realized

PCs for the consumer branded as “personal accessories” and not the consumer products they were becoming perceived as.

For business HP abandoned “hard deck” for direct sales, but still had internal sales personnel or resellers working with customers.

Surpassed IBM as worlds largest IT company in 2006

Modified sales/demand model to have field personnel drive demand – let the consumer decide how best to fill that demand (direct/indirect)

Acer Apple Compaq/HP IBM/Lenovo Dell

Direct vs. Indirect

95% Indirect1% Direct

69% Indirect27% Direct

80% Indirect17% Direct

84% Indirect14% Direct

25% Indirect74% Direct

Branding Strategy

Focus is low-cost Netbooks

Ease of use & integrated experience

“The Computer is Personal Again” campaign

???High Performance at Low Prices

Market Share (units) change 1994-2008

389% Increase 58.8% decrease 575% increase 12.6% decrease 425% increase

Success?? 2nd largest PC provider (units) in 2009

Only recently - Laptop sales growing 35% & PCs 6% 2005-2009

Current global leader in PC sales

PCs still loosing money. 2004 - supply chain looks like spaghetti

Unparalleled until mid 2000s – now 75% stock drop since 2004.

Acer is a competitor in low-cost. But the real comparison is between HP and Dell who focus on both business and individual consumers.

As the only company focusing primarily on direct sales – Dell has to create demand and deliver value both pre and post sale to drive customers to their product.

Comparing Apples or Oranges?

Does the Strategy Work?

Vendor Ratings By Consumers (2003)

Category Dell IBM HP

Price & Performance 1st 2nd 3rd

Vendor Reputation 1st 2nd 3rd

Product Reliability/Quality 1st 2nd 3rd

Desired Feature Set 1st 2nd 3rd

Web-Site Ordering & Support 1st 2nd 3rd

Customer Service 1st 2nd 3rd

Product Innovation 1st 3rd 2nd

Ergonomics 1st T-2nd T-2nd

Collaboration 1st T-2nd T-2nd

Brand Ratings 2009

Apple 84

Dell 75

HP 74

Others 74

We don’t have specific category rankings for 2009. But customer ratings still say that Dell is the best in its market (considering Apple’s customer segment is quite different).

It’s safe to say that Dell’s problem doesn’t lie in the product or customer perceptions.

Low Cost High Cost

High Customization/ Differentiation

Low Customization/ Differentiation

It would appear that Dell has one of the most customized systems, at one of the lower prices points – but somehow this isn’t enough to make them a global #1.

HPs success may indicate that customization isn’t the selling point that it used to be when computers seem a commodity in today’s market (vs. a luxury a decade ago).

Does the Strategy Work?

What is the current value proposition in today’s market and where can Dell focus their efforts to increase revenue and market footprint?

Hardware Software ResultCommodity Hardware

Micro-processors

Operating Systems

Application Software

End Products

Housings Intel (80%) Windows (90%)

MS Office (90%)

Desktop PC

Keyboards AMD (lower price and similar)

Apple Other (10%) Laptops

Motherboard Linux Work-stationsMemory Chips ServersDisk drives Netbooks

With this combination, and market dominance by a few key players – product differentiation will be very difficult to achieve, and still produce a product compatible with other systems (for networking, work file collaboration, etc).

Dell and other makers need to find a way to differentiate themselves on something other than just “system configuration”.

How’s it made – and what are my options?

Channels Example Short Desc. Pro’s & Con’sBrick & Mortar Retailer

Best Buy, Wal-Mart, Radio Shack

Sell a selection of pre-made computers to customers directly. Minimal on-going support (Geek Squad)

Manufacture

r subject to

buyback

s (up to 2.5

% of revenue lost)

18% increase 96-08. Stores run sales staff vs. mfg. At mercy of store sales staff to sell your product

Distributors Ingram Micro ($34B), Tech Data ($24B)

Sells to resellers (typically small owner-managed firms that sell computers and sometimes services/support) (41% sales decline between

distributors & resellers 96-08) Distributor & resellers run sales staff vs. mfg. Minimal post-sale support from manufacturer needed.

Integrated Resellers

Large resellers with extensive sales & support. Occasionally manage company networks, along with the computer sales.

Manufacturer Direct

Dell Accept orders via phone, internet, or sales personnel. Ship via mail/UPS.

(65.5% sales increase 96-08)Eliminates “middle man”. Likely more post-sale support. Sales is manufacturer’s responsibility

Distribution Channels – getting it into the customers’ hands.

The market is going away from middle-men and mainly to Distributor Direct models. Dell needs to leverage this by analyzing what they can do to maximize their strength in this area and compete effectively with the new entrants to this model (HP particularly).

1990 2008 Dell 2008 HP LenovoUS Market (units) 9.5 65.6 38% 25% 13%World Market (units) 23.8 287.6 62% 75% 86%Multiple (World vs. US) 2.5x 4.4x 1.6x 3x 6.6x

While worldwide unit sales has grown to 4.4 times the US market, Dell is still stuck at only 1.6 times worldwide sales vs. US sales.

Dell appears to be missing a huge market by not aggressively attacking the growth outside the US.

Where is the market today for computers?

* Acer & Apple considered different products/market segments

Is the Value in the Actual Product?

Average Product Price CAGR 1996-2008

Company Desktop PC Laptop PCAcer -9.7% -11.7%Apple 2.4% 7.0%Dell -8.5% -7.8%HP -6.0% -4.7%IBM/Lenovo -11.8% -3.3%

Apple has changed its product and generic strategy. For all other players the average sale price of the end product continues to decline. Revenue can only keep positive by increasing units sold for a finite period of time. It’s time for Dell to find the next growth stream in the market.

The Dell Manufacturing ProcessCustomer Places Order Peripherals &

Accessories (i.e. Monitor)

High-Speed Software Upload

High- Tech Hardware (microprocessors)

Commodity Hardware (box)

Burn-In Testing

Commodity Hardware (keyboard)

Commodity Hardware (hard drive) Peripherals &

Accessories (i.e. Printer)

Received by Customer

Packaging & Shipping

Post Sales Service & Support

By all assessments Dell already has a very optimized manufacturing and delivery system. Perhaps the growth avenue is here

Dell’s Post-Sale Support

Thousands of Pages of Customer Support Information

Third Party (Unisys) On-Site Technical Support

Phone-In Technical Support Staff

Five Control Centers Worldwide for Customer Support

400 Caches of Spare Parts Worldwide

While “sufficient” - with large customers spending an estimated $5,500 per computer for IT support and maintenance, this would appear the place for Dell to focus on growing their revenues with post-sale support and warranties.

With customers leaving the distributors & resellers, Dell should be able to find ample growth in providing IT services – especially to small/medium sized businesses, and possibly smaller educational institutions as well.

6313

159

Computers Enterprise Products

Peripherals & Software IT Type Services (design, deploy, support & maintain networks)

Managing Overhead - PC Providers 2008

Acer Apple Dell HP Lenovo

SG&A 7.8% 11.6% 11.6% 11.1% 10.5%

R&D 0.1% 3.4% 1.1% 3.0% 1.5%

Advertising N/A 1.5% 1.3% 0.8% N/A

Dell has the highest SG&A – how can we help control some of this overhead?

R&D is last among all but Acer. Is there a reason they are being outspent three fold by their biggest competitor, HP?

R&D isn’t for the PC maker any more – so perhaps they should save money on SG&A and put it towards R&D on their enterprise products or post-sale customer support improvements.

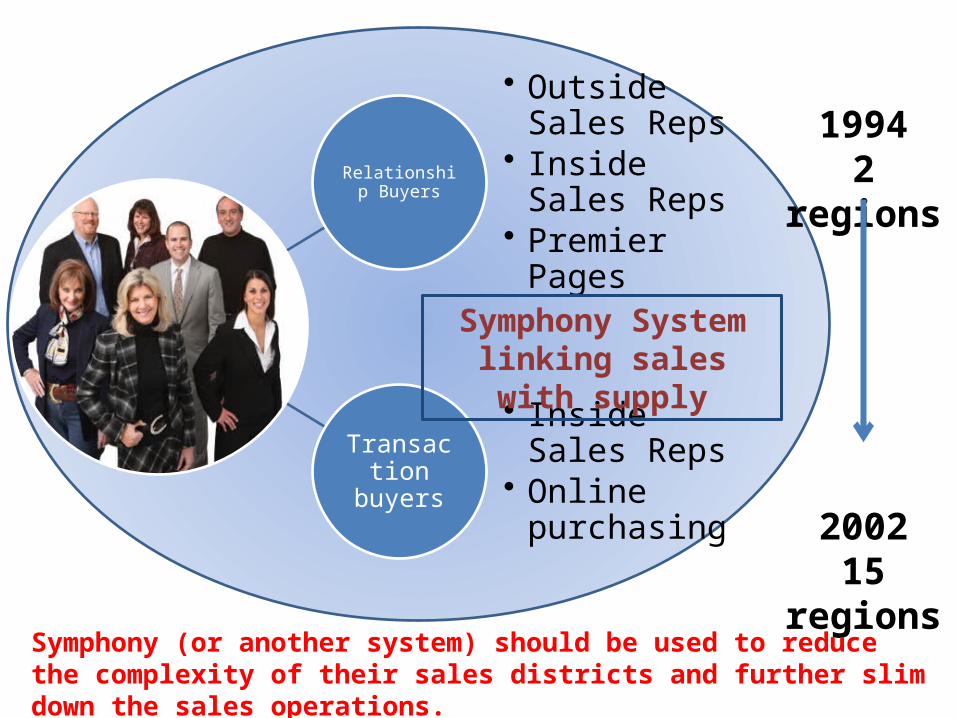

Relationship Buyers

• Outside Sales Reps

• Inside Sales Reps• Premier Pages

Transaction buyers

• Inside Sales Reps• Online

purchasing

19942 regions

200215 regions

Symphony System linking sales with supply

Symphony (or another system) should be used to reduce the complexity of their sales districts and further slim down the sales operations.

How does Dell regain investor confidence in their company to obtain the necessary capital to move forward with corporate growth?

1996 2008 ChangeLarge Business 28.9 20.2 31%Small &Mid Business 38.1 22.9 40%

Home Consumer 26.9 45.9 71%

Education 6.6 11.0 67%

Are We Moving In The Right Direction?

Dell’s focus has traditionally been selling to businesses – but share has declined.

Dell must find a way back into the business market where they were strongest.

Core Customer

% US Sales (by USD)

Key Feature Key Factors Dell Value Proposition

Large Business & Government 20.2 Reliable & Stable

systems

Large MIS staff. $1400 on computer, $5,500 lifetime cost of maintenance. Often a motley collection of system brands & age

Can offer the company a consistent product linecomplement to MIS staff with support and service

Small Business 22.9Productivity PCs for common applications

Low/No MIS staff. Performance, reliability, support, service & channel recommendations.

Supplement to MIS staff w/ support & service

Individual Consumer 45.9

High-end PCs (likely enhanced graphics & processing speed)

Rely highly on outside sources (sales people, reviews, publications) for information to make choice

Consistent performance w/ commercial tested products for the consumer.

Educational Institutions 11.0

Power workstations (likely enhanced RAM and/or processor speeds)

No Info Supplement to MIS staff w/ support & service

The ability of Dell to compliment MIS departments for larger customers ties in well with the purchase of EDS and Perot Systems.

What Can Dell Offer to Each Customer Segment??

Factor Issue How To Address

Customer Service

Poor Support, especially for individual consumers

Improve post sale customer support via both website and call-in support (already moved call centers back to the United States)

Products Battery recall effects image Refocus marketing on the “better product at a lower price” message

Corporate Practices

Gov’t investigation revealing questionable accounting practices

Reassure investors via outside audits published and more thorough SEC filings

Pricing Problems

Cut prices for business but didn’t gain market share

Find proper price points for both business and individual consumers (can price cuts be “undone”?)

Component Choices

Criticism of slow choice to use AMD chips (faster & cheaper over Intel)

Expand selection of components in configuration and use alternatives to drive supplier price competition. High tech components is 60% of PC cost so this is the place for the most price savings

Leadership Issues

Company insiders loosing confidence in leadership

Already shook up leadership with bringing on outside executives. Now they have to prove that it will work to have so many outsiders.

Why the precipitous drop in performance & stock price??

Investor confidence is key to any public company. Dell will need to address all of these issues – while also addressing their future in the computer market at large.

Hyper-Efficient ProcessesEstablished Direct Sales Business ModelIndustry Experience with Large BusinessesIndustry Experience Personalizing Products to Match Customer Needs

Waning Investor ConfidenceLow Market Presence Overseas - Late Entry

to Emerging MarketsPoor Customer Support (or at Least the

Perception of Poor CS)

Newer Executive Leadership Can Shake Old Paradigms and Steer a New CourseAcquisitions of EDS and Perot Systems opens new market/revenue opportunitiesMinimal Collection of Direct Competitors Means Company Can Narrow Focus and not Try to Compete Against “Everyone”.

Established Competitors Already

In the Emerging Markets

HP a Huge Rival In the Business to

Business Field With Both Computers and

IT SupportLack of Investor Confidence Will

Make Working Capital Scarce and

Difficult to Raise Additional Funds

STRENGTHS

OPPORTUNITIES THREATS

WEAKNESSES

What Does Dell Bring to the Future?

RECOMMENDATIONS

Large Business Small & Medium Business

Individual Consumer

Educational Institutions

Product Positioning

Same high-performance & low prices

Custom machines for your custom needs

Personalized computers for a personalized experience

High-Performance, Low Prices, Preparing Students for the Real World

Value Proposition

Order in Bulk – reduce “motley” collection of systems. Rely on our MIS staff to complement yours.

Expand MIS & Post-Sale support to companies.

The same computer the big guys use – along with the same support when you need without going back to the store.

Expand MIS & Post-Sale support to companies.

How to Implement

Re-Focus on large customers. Aim to sell “bundles” of PCs and work to include servers and other IT architecture products as well.

Showcase expanded MIS capabilities. Offer economy of scale to customers by employing Dell IT staff vs. own dedicated staff.

Continue to upgrade options to individual consumer and expand focus on high-end gaming and multi-media products to engage high-end consumer market.

Showcase expanded MIS capabilities. Offer economy of scale to customers by employing Dell IT staff vs. own dedicated staff.

Recommendations – Customer Segments

The recurring theme is to tap the $5,500 per computer post-sales IT support market in the business segment.

Operations Products MarketsInternal Focus

Continue to shore-up internal accounting and accountability. Show that leadership can carry them into new markets and expanded opportunities

Continue to find ways to drive down prices. But also focus on high-end configurations where margins are the company can leverage custom expertise.

Focus on each market individually, but insure capabilities continue to complement the company as a whole. Realize the disparity between US and global market share and work to gain ground outside of the United States.

External Focus

Allow more access to audit results for share-holders and market analysts. Create more accountability measures that are visible to outsiders.

Focus on post-sale value added activities where additional revenue opportunities exist. Showcase expanded MIS capabilities to answer the needs of businesses with limited resources to staff their own IT departments.

Realize expanding markets pose great opportunities for bulk sales to business and also a complementary MIS team to sell in the process. As emerging markets modernize their data sharing systems Dell should be poised to become the market leader overseas, as well as domestically.

Recommendations – Corporate Focus

The primary focus of Dell moving forward should be selling its entire product line of computers, enterprise systems, peripherals, and post sale IT/MIS support.

Dell must also push into expanding markets to reduce the gap between US and global sales.

As a complement to this strategy Dell should push bulk sales of products to reduce complexity of business IT systems caused by multiple different computers vs. a standardized approach.