in re life partners holdings, inc., et. al., case no. 15 ... · why is this case so complicated?...

TRANSCRIPT

In re Life Partners Holdings, Inc., et. al., Case No. 15-40289-RFN-11

Third Amended Joint Plan of Reorganization

H. Thomas Moran II, Trustee

Welcome

Presentation Overview

• Meeting Overview

• Purpose/Disclaimer

• Presentation Overview

• LPHI Bankruptcy – General Overview

• The Plan and Disclosure Statement

• Options Available to Investors

• Ballot and Election Forms

• Life Insurance Policy Information

• Closing

• Questions

Why Is This Case So Complicated?Extremely Complex Case• 3,400 life insurance policies (face amount of approx. $2.4 billion)

• 22,000 investors with over 100,000 outstanding Fractional Positions

• Years of mismanagement and problems to resolve

Competing Needs• Competing investor needs (viaticals vs life settlements, cash vs IRA accounts)

• Collaboration with many investors, attorneys, etc.

Complicated Legal Issues• Securities Issue

• Tax and ERISA Issues

• Active lawsuits

• Class Action settlement

• Ownership Issue

Next Steps

July 15, 2016

Solicitation Mailing Deadline

Aug 15, 2016

Voting, Election and Objection Deadline

(Forms must be received by Epiq)

Aug 29, 2016

Confirmation Hearing Date

Effective Date

*Dates are subject to change.

The Plan

The Plan: Designed by the Investors – for The Investors

• Developed in consultation with investors

• Addresses numerous issues, including resolution of Ownership issue

• Offers options from which you can choose to meet differing needs

Strategic Partnership – Vida Capital, Inc.

1. Industry Recognized Expert• SEC expert witness in case against Life Partners and Brian Pardo• Registered Investment Adviser (RIA) Barron’s Top 100 Funds – 2016• Board member of multiple Life Settlement industry groups

2. Service large life settlement portfolios of policies for high net worth individuals and institutions• $1.2 billion in equity value• $2.1 billion of face value of policies• Over 1150 policies• Over 1,500 investors

3. Provide capital so funds can be distributed to fractional holders as soon as possible• $10 million “DIP loan” to get the estate through the bankruptcy process• $55 million loan to the policy trust (pooled option 2)• $25 million revolving loan facility in case capital is needed in the future

New Entities

• A five-member board will provide ongoing oversight

• 3 investor members

• Jose Montemayor (industry professional)

• TBD

• Position Holder Trust

• Own and administer Policy Holder Trust assets including the policies

• Trustee: Eduardo Espinosa

• IRA Partnership

• Hold IRA Partnership interests

• Creditors’ Trust

• Own and Administer Creditors Trust Assets, including Causes of Action….

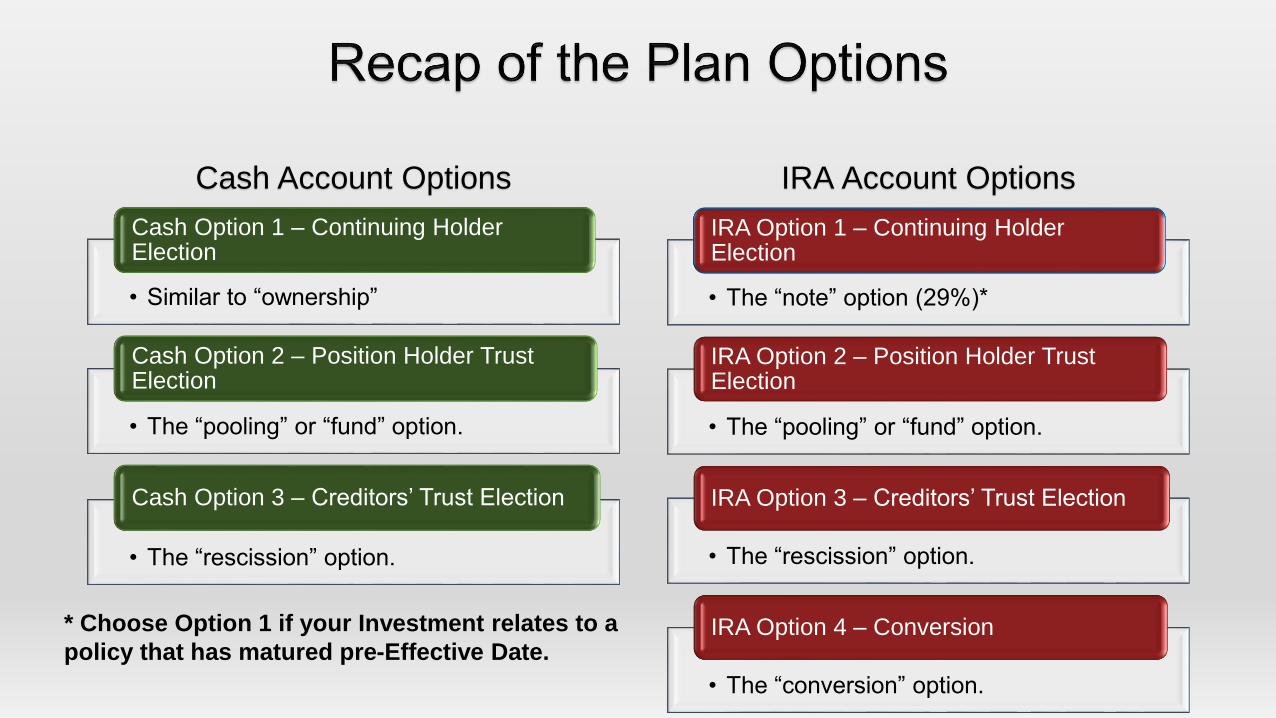

Plan Options

• Similar to “ownership”

Cash Option 1 – Continuing Holder Election

• The “pooling” or “fund” option.

Cash Option 2 – Position Holder Trust Election

• The “rescission” option.

Cash Option 3 – Creditors’ Trust Election

• The “note” option (29%)*

IRA Option 1 – Continuing Holder Election

• The “pooling” or “fund” option.

IRA Option 2 – Position Holder Trust Election

• The “rescission” option.

IRA Option 3 – Creditors’ Trust Election

• The “conversion” option.

IRA Option 4 – Conversion

Cash Account Options IRA Account Options

Overview of Plan Options

* Choose IRA Option 1 if your investment relates to

a policy that has matured pre-Effective Date.

Cash Option 1: Continuing Holder Elections

• Similar to “ownership” • Pay all future premiums and costs

• 95% of face amount (“ownership” certificate)

• 5% beneficial interest in pool

Must pay all past-due premium amounts to be eligible to make this election

If you are unable to pay premiums and fees in the future and default to the “pool”, there will be a penalty.

For Cash Accounts

Cash Option 2: Position Holder Trust Election

• The “pooling” or “fund” option• Exchange interest in a policy for interest in Position Holder

Trust (“pool”)• No longer pay premiums and service fees• No longer tied to any one policy• Distributions from Trust (from pooled maturities) will be made

periodically

Must pay all pre-petition premium amounts owed (any other unpaid pre-petition platform service fees will be withheld from future distributions).

For Cash Accounts

Cash Option 3: Creditor’s Trust Election

• The “rescission” option

• Rescind, or undo, the original investment agreement

• Distributions from Creditor’s Trust (from litigation recoveries) will be made periodically

Rescission Settlement Subclass Members only.

For Cash Accounts

IRA Option 1: Continuing Holder Election

Receive a New IRA Note • Approximately 29% (of expected payout)

• Bears interest at approximately 3% per annum

• Pays out by the 15th anniversary of the Plan Effective Date

• Pay no premiums or servicing fees

• Secured by liens linked to beneficial ownership and maturity proceeds of fractional positions of investors electing this option

Must pay all past due premium amounts and servicing fees to be eligible to make this election

Qualified Plan Holders can make this election.

*Please consult a tax professional

For IRA Accountholders

IRA Option 2: Position Holder Trust Election

• The “pooling” or “fund” option

• No longer pay premiums and service fees

• Exchange current IRA Note for new note/interest in the IRA

Partnership (which has a beneficial interest in the Position

Holder Trust – the “pool”)

• Distributions from Position Holder Trust (from pooled

maturities) will be made periodically Must pay all pre-petition premium amounts owed, to be eligible to make this election

(any unpaid pre-petition platform service fees will be withheld from future

distributions)

*Please consult a tax professional

For IRA Accountholders

IRA Option 3: Creditor’s Trust Election

• The “rescission” option

• Rescind, or undo, the original investment agreement

• Distributions from Creditor’s Trust (of litigation recoveries) will be made periodically

Not an option for Qualified Plan Holder (employee benefit plan) Rescission Settlement Subclass Members only

*Please consult a tax professional

For IRA Accountholders

IRA Option 4: Conversion Election

Process for an IRA Holder to distribute the note to the individual and exchange it for a fractional interest so they may elect “ownership”

*Please consult a tax professional

For IRA Accountholders

Tax Consequences: IRA

“No part of the trust funds will be invested in life insurance contracts.” 26 U.S.C. § 408(a)(3)

Violation of 26 U.S.C. § 408(a)(3) results in the disqualification of the IRA. Treas. Reg. § 1.408-1(c)(2)

*Please consult a tax professional

For IRA Accountholders

Tax Consequences

• Please read the appropriate sections in the Plan and Disclosure Statement.

• There are 25 pages of tax disclosure• Tax Risks – Disclosure Statement section 25.04 (pg 177)

• Tax Consequences – Disclosure Statement Art. 26 (pgs 183-219)

• Please seek advice from a tax professional.

• The Trustee, LPI and the Trustee’s professionals cannot provide tax or legal advice.

Financial Information

• Must be analyzed on a policy-by-policy basis

Cash Option 1 – Continuing Holder

• Projected to be as high as 85% of amount invested

Cash Option 2 – Position Holder Trust Election

• Undeterminable at this time

Cash Option 3 – Creditors’ Trust Election

• Note: 29% of expected payout

• Plus 3% interest – paid annually

IRA Option 1 – Continuing Holder

• Projected to be as high as 85% of amount invested

IRA Option 2 – Position Holder Trust

• Undeterminable at this time

IRA Option 3 – Creditors’ Trust

• See cash option 1

IRA Option 4 – Conversion

Cash Account Options IRA Account Options

* Choose Option 1 if your Investment relates to a policy that has matured pre-Effective Date.

Exhibit D toJoint DS

Total Recoveries Distributed

$1,140,264,000

Past Policy Maturities

Plan Section 4.04 / Disclosure Statement 6.03• You will receive a Statement of Maturity Account• Tax withholding and any owed premiums/platform fees will be deducted• 5% contribution in exchange for interest in pool• Will receive10% interest on borrowed funds• Vida Financing• 2.8% servicing fee not applicable

Elect Option 1 – Cash or IRA

Plan Package

The Plan Package

Epiq, the noticing agent, will send each investor a personalized

Plan package It includes:

1. A letter from the Trustee2. Instructions with option summaries3. A CD with a copy of the Disclosure Statement, Plan and exhibits 4. A Ballot – to vote for the Plan5. An Election Form – to elect options for your positions (Reconciliation

payment invoice is attached)

Each completed Ballot and Election form must be received by Epiq by the voting deadline August 15, 2016 at 5:00 pm CT

The Ballot – To Vote for the Plan

The Ballot (page 2)

To vote on the Plan, please ensure that one of the boxes is checked.

The Election Form

• To make your election for each position/policy

• Should be completed whether you vote for or against the Plan

The Election Form – Section 1(Cash Example)

SECTION 1. Complete this section to elect the same option for ALL positions.

If you choose to Elect the same Option for all of your Class B2 Fractional Interest Holder Claims, please check one box below:

I Elect Option 1 (Continuing Holder Election) for all of my Class B2 Fractional Interest Holder

Claims and agree to pay all future premiums and expenses as defined in the Plan.

I Elect Option 2 (Position Holder Trust Election) for all of my Class B2 Fractional Interest

Holder Claims and understand that I will no longer have to pay premiums and expenses, but

participate in contributions, as defined in the Plan.

I Elect Option 3 (Creditors’ Trust Election) for all of my Class B2 Fractional Interest Holder

Claims

The Election Form – Section 2(Cash Example)

SECTION 2. Complete this section to elect different options for EACH OF YOUR

POSITIONS.

What Happens if I Don’t Make Elections?

• You will be deemed to have chosen the “ownership” option –Option 1

• For interests with no past due balances

• Option 1 requires that you pay all future premiums

If you are a Fractional Interest Holder and do not want to pay premiums and fees in the future, elect option 2.

For Cash Accountholders

What Happens if I Don’t Make Elections?

• You will be deemed to have chosen the Position Holder Trust Election (Option 2).

• Assumes you have no past due balance for premiums or fees

IMPORTANT: If you currently have matured funds you must elect IRA Option 1 so that your funds will be distributed on or after the effective date!

For IRA Accountholders

What Information Should I Consider if I plan to keep

some policies?

Decision Making Considerations

• Can I afford to pay premiums?

• Can I afford to wait before receiving funds?

• What policy information should I consider?• UL

• WL

• Term

• Group

• What is the age and LE for the insured of each policy?

Where Can I Find Information About My Policies?

www.LPI-policies.com

• Policy Detail Summary Report• Policy Information

• Insured and LE Information

• Premium Information

• Basic Overview of Life Insurance – Relative to the LPI Portfolio of Policies

• Life Expectancy Estimates – What You Need to Know

Policy Detail Summary Report Example

Life Expectancies

• Life Expectancy Estimate – (LE for short)

• As an estimate, it means that the lifespan of half of the people will be shorter and the other half longer….

• An educated guess

Universal Life Insurance - Points to Consider

• Unexpected cost of insurance increases

• Premiums are optimized and will increase every year.

Please see the “Basic Overview of Life Insurance” white paper available at www.lpi-policies.com.

Whole Life Insurance – Points to Consider

• Premiums and death benefit remain level = easy planning

Please see the “Basic Overview of Life Insurance” white paper available at www.lpi-policies.com.

Term Life Insurance – Points to Consider

• Policy coverage may terminate (only for a certain “term”)

• Inability to predict future premiums on most policies

• Significant premium increases are possible

• Conversions to permanent Insurance – some conversions are becoming increasingly difficult as some carriers are requiring insured cooperation

Please see the “Basic Overview of Life Insurance” white paper available at www.lpi-policies.com.

Group Life Insurance – Points to Consider

Group policies carry the most risk and uncertainty!

• Coverage is linked to insureds continued employment

• If insured leaves employment coverage may be lost

• Amount of coverage can fluctuate due to issues such as a salary change

• Future premiums are typically unknown

Please see the “Basic Overview of Life Insurance” white paper available at www.lpi-policies.com.

Recap and Closing

• Similar to “ownership”

Cash Option 1 – Continuing Holder Election

• The “pooling” or “fund” option.

Cash Option 2 – Position Holder Trust Election

• The “rescission” option.

Cash Option 3 – Creditors’ Trust Election

• The “note” option (29%)*

IRA Option 1 – Continuing Holder Election

• The “pooling” or “fund” option.

IRA Option 2 – Position Holder Trust Election

• The “rescission” option.

IRA Option 3 – Creditors’ Trust Election

• The “conversion” option.

IRA Option 4 – Conversion

Cash Account Options IRA Account Options

* Choose Option 1 if your Investment relates to a

policy that has matured pre-Effective Date.

1. Created with the Investors – for the Investors

2. Creates necessary structure for maximum financial recovery

3. Creates options so you can select the one that best meets your

individual needs.

4. Creates oversight board that includes not only industry

professionals, but also individual investors like yourself.

Why Should I Vote for This Plan?

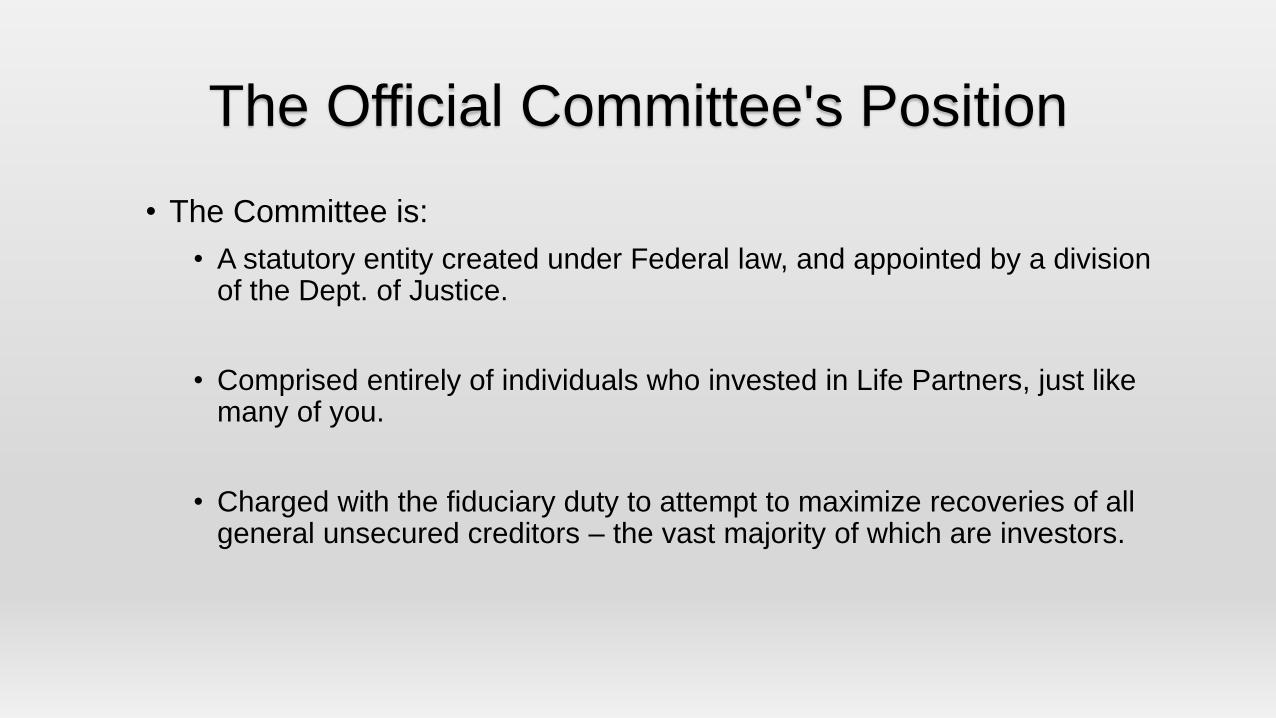

The Official Committee's Position

• The Committee is:

• A statutory entity created under Federal law, and appointed by a division of the Dept. of Justice.

• Comprised entirely of individuals who invested in Life Partners, just like many of you.

• Charged with the fiduciary duty to attempt to maximize recoveries of all general unsecured creditors – the vast majority of which are investors.

The Committee Supports the Trustee / Committee Plan

• The Committee DOES NOT support the TA Plan.

• The Committee's members, all investors, are voting to Accept the Trustee / Committee Plan and to Reject the TA Plan.

Why…?

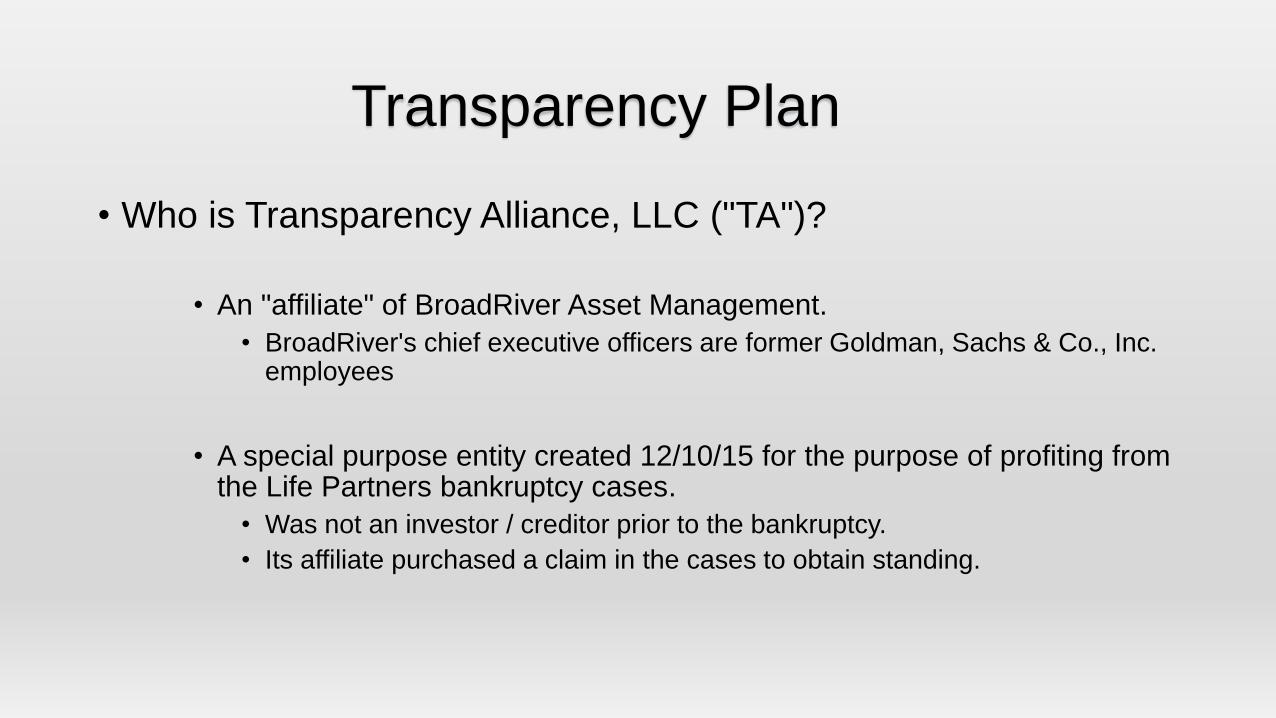

Transparency Plan

• Who is Transparency Alliance, LLC ("TA")?

• An "affiliate" of BroadRiver Asset Management.

• BroadRiver's chief executive officers are former Goldman, Sachs & Co., Inc. employees

• A special purpose entity created 12/10/15 for the purpose of profiting from the Life Partners bankruptcy cases.

• Was not an investor / creditor prior to the bankruptcy.

• Its affiliate purchased a claim in the cases to obtain standing.

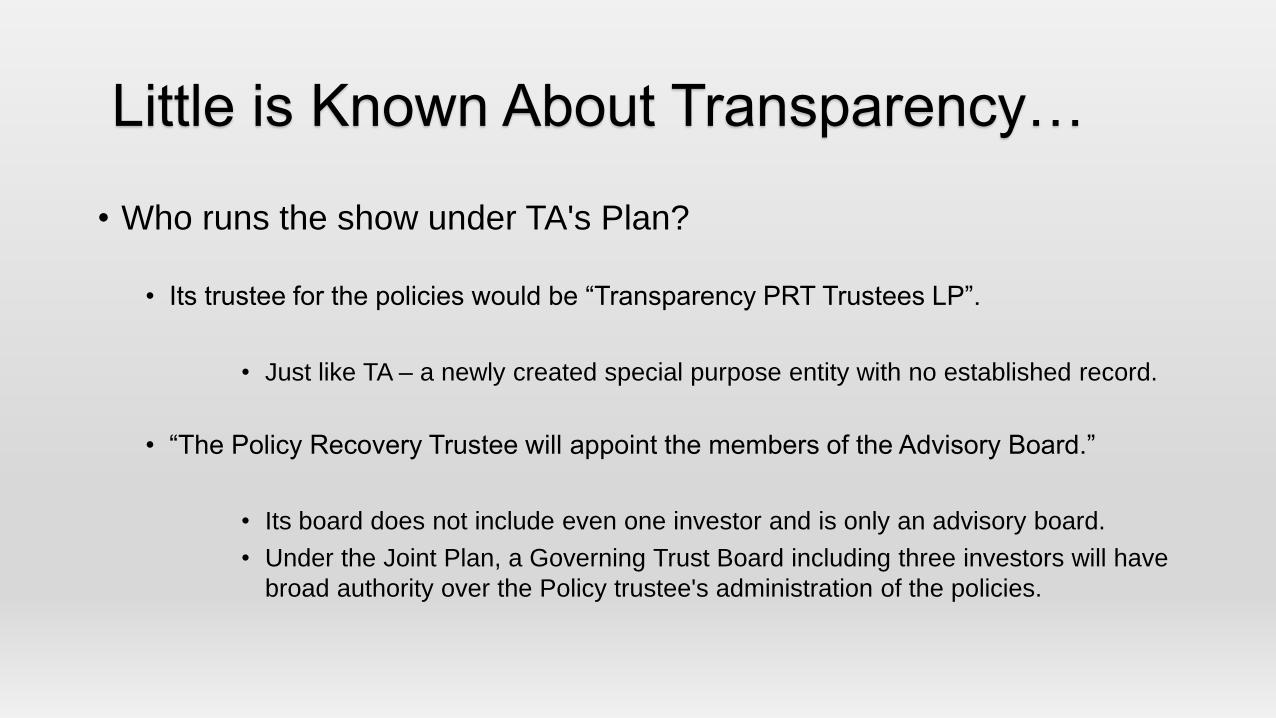

Little is Known About Transparency…

• Who runs the show under TA's Plan?

• Its trustee for the policies would be “Transparency PRT Trustees LP”.

• Just like TA – a newly created special purpose entity with no established record.

• “The Policy Recovery Trustee will appoint the members of the Advisory Board.”

• Its board does not include even one investor and is only an advisory board.

• Under the Joint Plan, a Governing Trust Board including three investors will have

broad authority over the Policy trustee's administration of the policies.

Why is TA Proposing a Plan?

• What does TA get out of this?

• A $2.3 billion portfolio to manage since TA's affiliate, BroadRiver, sold its prior portfolio to Vida.

• $41 million in exit financing fees (at least) to an affiliate for putting up $62 million in exit financing.

• No evidence of who exactly will lend the money, or that the money is currently available.

• Projected $43 million in servicing and management fees for ten years.

• TA will outsource most of this work.

• Ability to select an affiliate of TA to derive significant fees to sell what it projects will be a $1.1 billion portfolio ten years from now.

• TA's affiliate did this in 2015, and paid its broker a 7 figure commission. Investors could

bear these charges.

Committee Concern – Up-Front Fees

• TA Costs to Continuing Holders (TA Disclosure Statement, Exh. 4)• $100,000.00 Position Example

• 3.1% Up-front payment for bankruptcy (could be higher, if opt-in % is lower).

• .2% Paid each year for TA management (1.4% in 7 years, 2.0% in 10 years).

• .12% Paid each year for servicing (0.84% in 7 years, 1.2% in 10 years), plus part of onboarding fee.

• Projected 5.9% paid each year for premiums (41.4% in 7 years, 59.0% in 10 years).

• Result – 47% of face amount paid in costs by Continuing Holders by year 7 (65% by year 10)

• TA predicts more than 60% of policies projected to run past year 7.

Transparency Ex 4, page 8

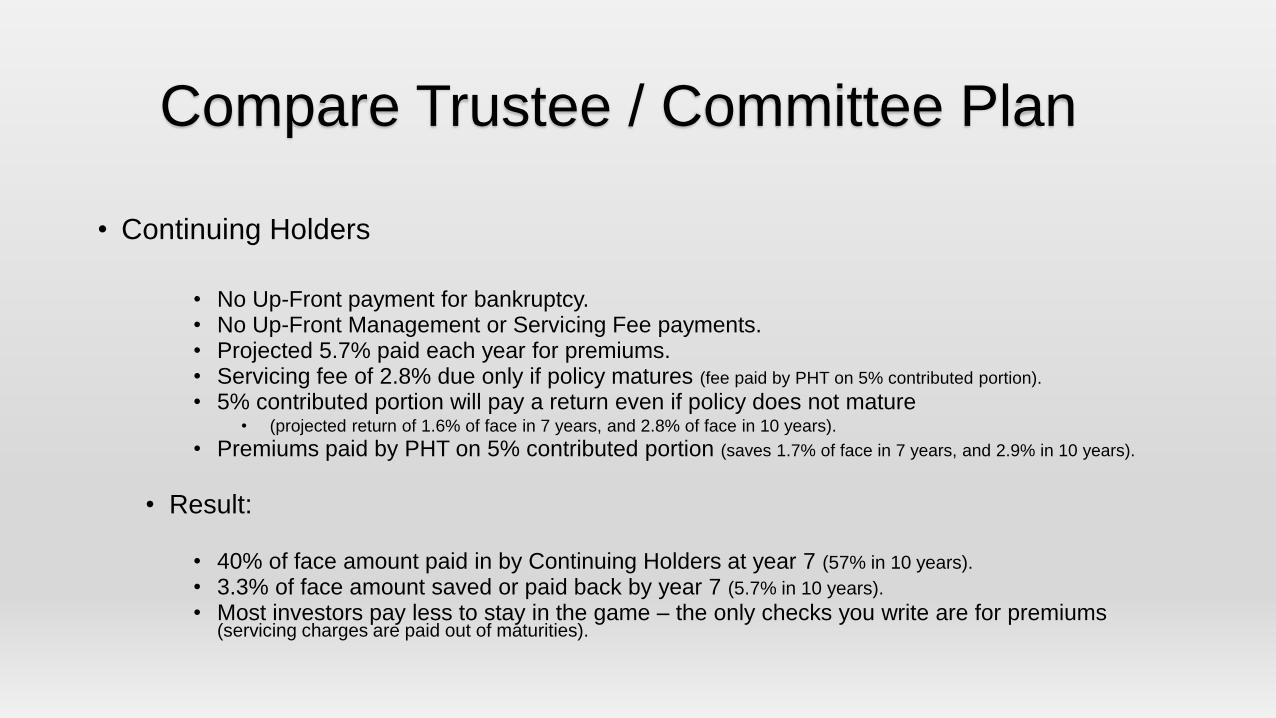

Compare Trustee / Committee Plan

• Continuing Holders

• No Up-Front payment for bankruptcy.• No Up-Front Management or Servicing Fee payments.• Projected 5.7% paid each year for premiums.• Servicing fee of 2.8% due only if policy matures (fee paid by PHT on 5% contributed portion).

• 5% contributed portion will pay a return even if policy does not mature• (projected return of 1.6% of face in 7 years, and 2.8% of face in 10 years).

• Premiums paid by PHT on 5% contributed portion (saves 1.7% of face in 7 years, and 2.9% in 10 years).

• Result:

• 40% of face amount paid in by Continuing Holders at year 7 (57% in 10 years).

• 3.3% of face amount saved or paid back by year 7 (5.7% in 10 years).

• Most investors pay less to stay in the game – the only checks you write are for premiums (servicing charges are paid out of maturities).

Committee Concern – Pool Return

• TA Projection for Pool (TA Disclosure Statement, Exh. 4)

• $1.5 billion into pool

• $298 million distributed from pool

• 20% of the original face amount

• Pool payout is 34% of invested amount

• Compared to approximately 86% pool payout under Trustee / Committee Plan

Committee Concern – Exit Financing

• TA Exit Financing - $62 million.• Costs investors at least $41 million.

• Using more realistic projected maturities, and assumptions about future abandonments into the PHT, costs investors more than $62 million.

• Trustee / Committee Plan Exit Financing - $55 million term facility.

• Costs investors $4 million.

• Plus, $25 million standby line of credit.

Committee Concern – IRA Issues

• TA says New IRA Note unnecessary• But, TA admits in the fine print: "…despite their form, there is significant risk

that the Class B3 Notes likely would be treated as equity for federal tax purposes and the Class B3 Note Holders likely would be viewed as investing in life insurance by virtue of holding Class B3 Notes, resulting in disqualification of the Class B3 Note Holder’s IRA."

• TA's Old Life Partners "Note" is too good to be true.• TA's note structure could ultimately invalidate the holders' IRA.

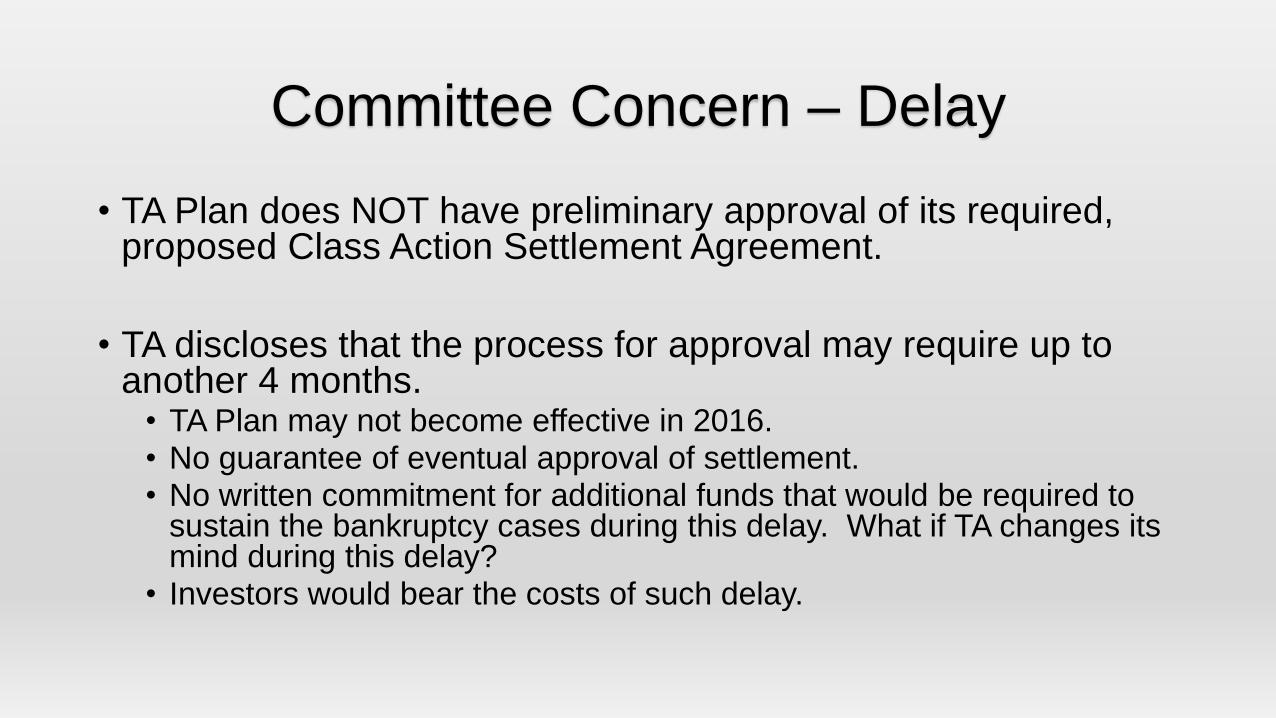

Committee Concern – Delay

• TA Plan does NOT have preliminary approval of its required, proposed Class Action Settlement Agreement.

• TA discloses that the process for approval may require up to another 4 months.

• TA Plan may not become effective in 2016.• No guarantee of eventual approval of settlement.• No written commitment for additional funds that would be required to

sustain the bankruptcy cases during this delay. What if TA changes its mind during this delay?

• Investors would bear the costs of such delay.