in the supreme court of belize, a · 3 bbl was a minority shareholder in bcbl, the cbb by letter to...

TRANSCRIPT

1

IN THE SUPREME COURT OF BELIZE, A.D. 2013

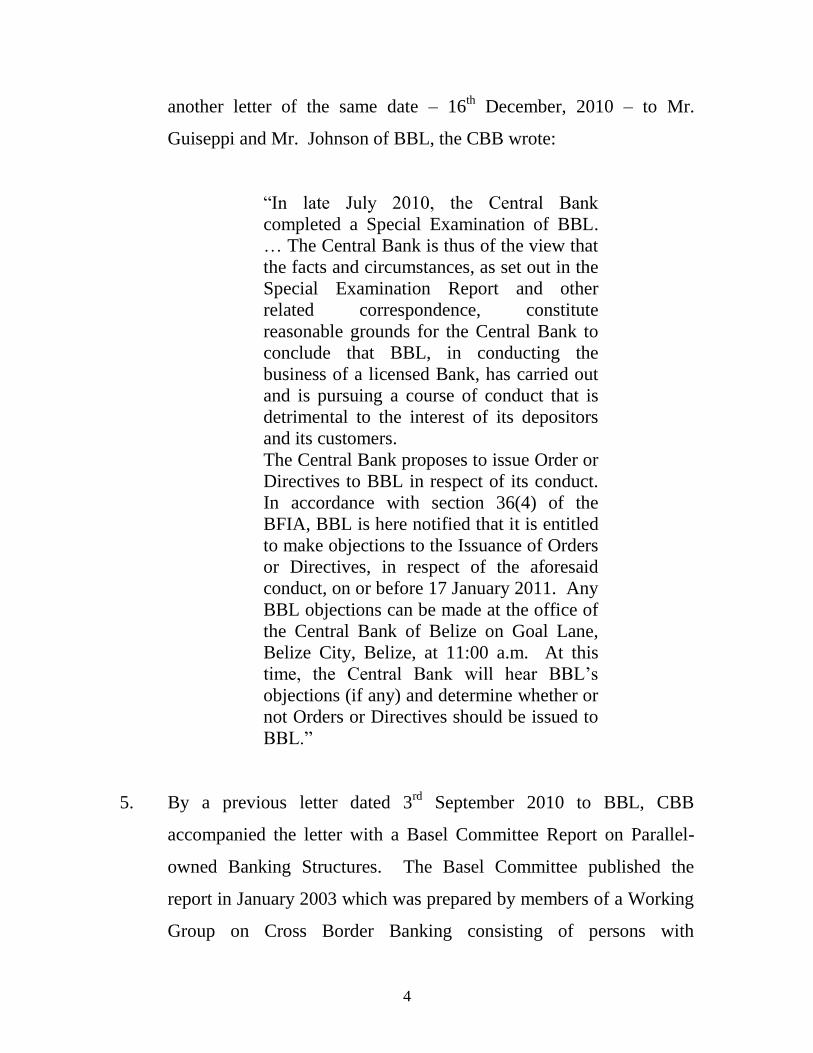

CLAIM NO. 80 of 2011

THE BELIZE BANK LIMITED CLAIMANTS

BCB HOLDINGS LIMITED

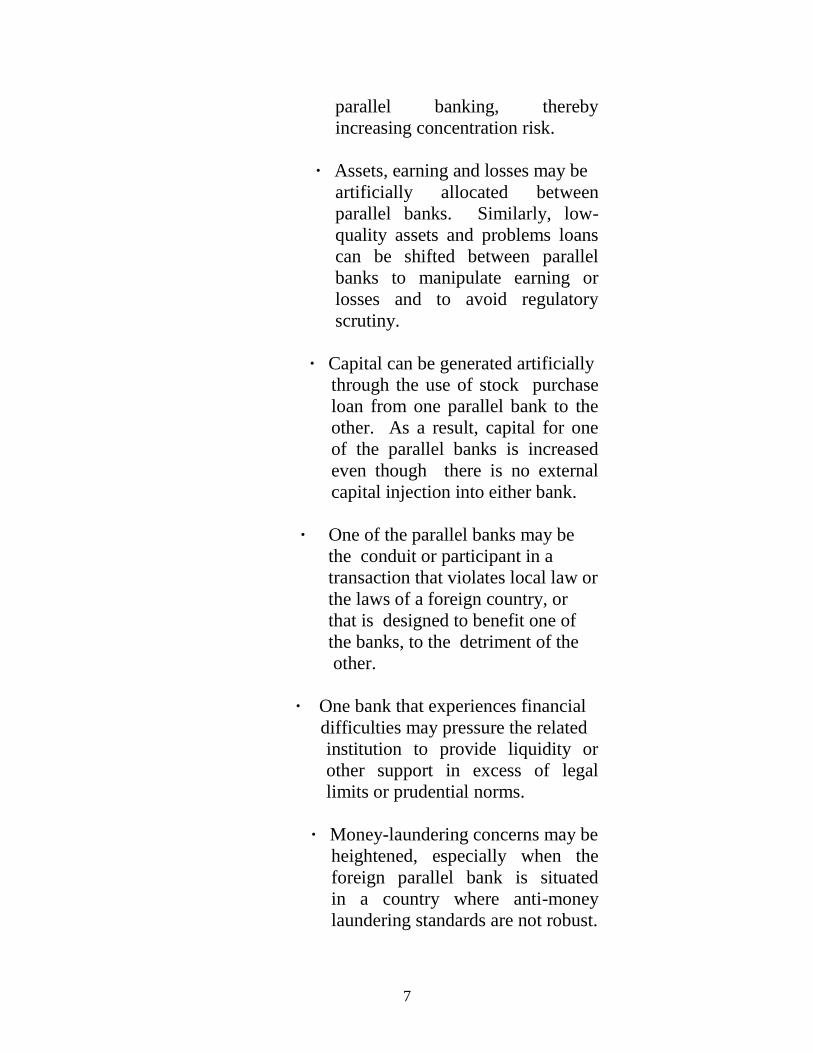

BRITISH CARIBBEAN BANK INTERNATIONAL LTD.

AND

THE CENTRAL BANK OF BELIZE DEFENDANT

Hearings

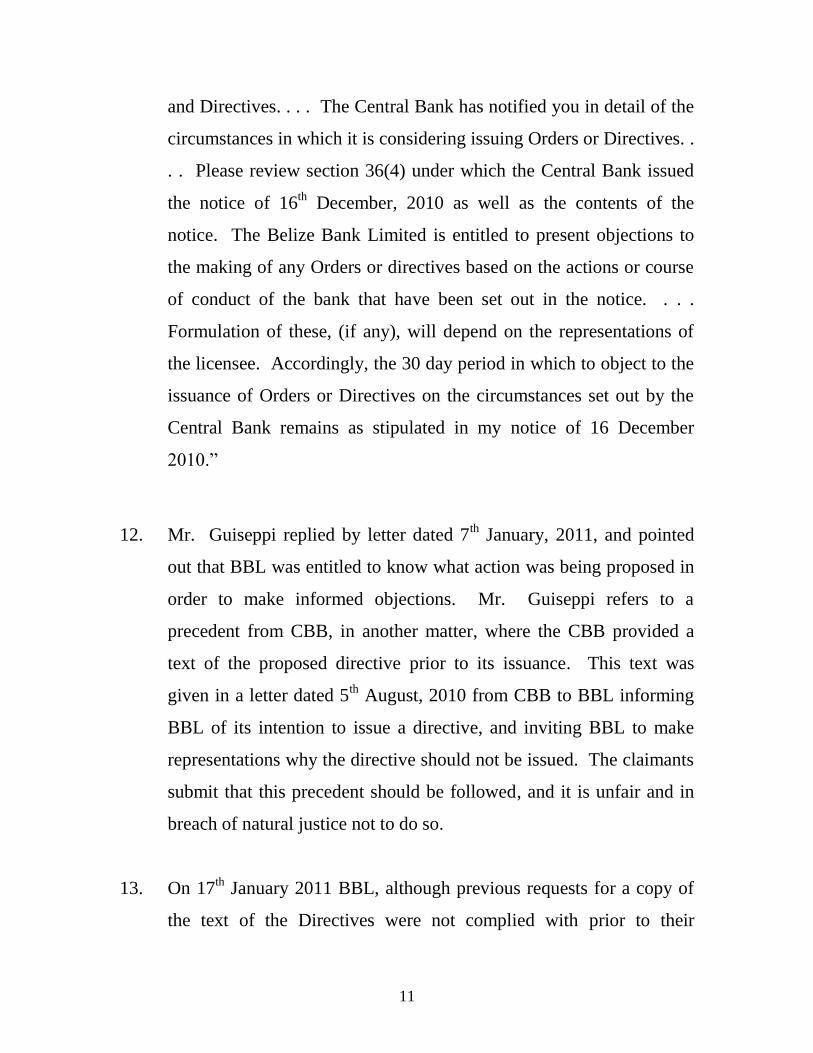

2012

1st November

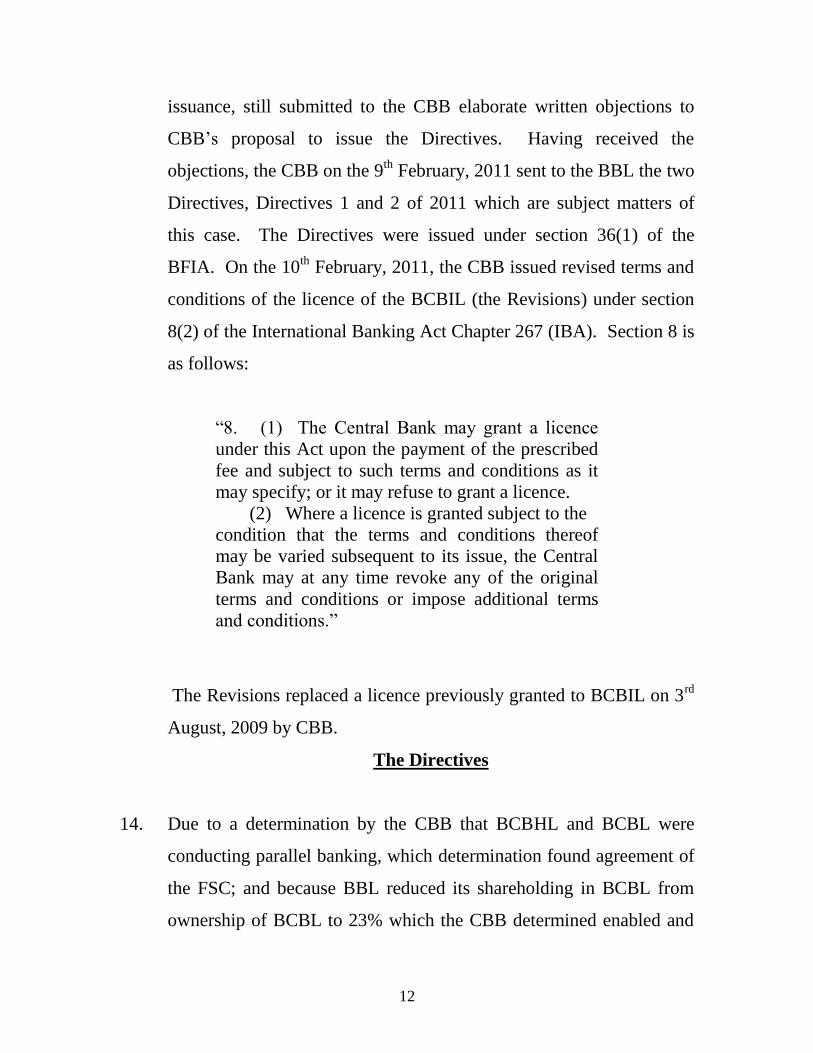

2013

4th

February

Mr. Eamon Courtenay SC and Ms. Pricilla Banner for the claimants.

Mr. Denys Barrow SC and Ms. Naima Barrow for the defendant.

LEGALL J.

JUDGMENT

Background

1. The claimants are all incorporated companies carrying on business in

the banking sector with offices in Belize City. The No. 2 claimant

(BCBHL) is the parent company of the No. 1 claimant (BBL); and

the No. 3 claimant (BCBIL) is a subsidiary of BBL. The defendant

2

(CBB) is a body corporate established by section 4(1) of the Central

Bank of Belize Act, Chapter 262. There is another bank incorporated

and located in the Turks and Caicos Islands, named British Caribbean

Bank Limited (BCBL) in which BBL is a shareholder.

2. BCBL was in 1998 solely owned by BBL and there was, in place at

that time, an agreed Memorandum of Understanding (MOU) and later

a 2004 Multi Lateral Memorandum of Understanding (MMOU) for

the exercise of consolidated supervision of the banks, and the sharing

of information, by the Financial Services Commission of the Turks

and Caicos Islands (FSC) and the CBB. In spite of the MOU and

MMOU the FSC, without informing the CBB, permitted, by the

process of the issuing of shares, BCBHL to be the new owner of

BCBL in place of BBL which had previously held 100% shares in

BCBL, but reduced to 23% of the shares in BCBL, which was later

increased to 25%, thereby removing BCBL from the regulatory

control by CBB through the control of BBL. The CBB in a letter

dated 21st February, 2011 therefore informed the FSC, in critical

language that, among other matters, because of the above reduction of

shares, CBB will “continue to act unilaterally as it sees fit in the

interest of Belize, the MMOU not-withstanding.” The CBB submitted

that this new ownership structure brought into place a parallel banking

system between BBL, BCBHL, BCBL and BCBIL.

3. Correspondence between parties to the claim would assist in

following the emergence of the alleged parallel banking system. On

receiving a letter from Mr. Phillip Johnson, President of BBL, that

3

BBL was a minority shareholder in BCBL, the CBB by letter to BBL

dated 6th

July, 2009 wrote that it was “concerned that this may be a

case of parallel banking and requested BBL to submit to CBB by 30th

July, 2009 an updated group structure chart, and “a list of all

shareholders (5% and over) and directors of BBL, BCBL and BCBIL

along with the number of shares held by those shareholders.” It is not

clear whether the requested information was submitted to the CBB.

But it seems that the next letter on the issue of parallel banking was

not sent by CBB to BBL until between September and December,

2010, more than one year after the letter of July 2009. The governor

of CBB in a letter dated 16th

December, 2010 on parallel banking

wrote to the chairman Mr. Guiseppi of BBL as follows:

“The fact that BBL and British Caribbean

Bank International Limited (BCBIL) are

owned and controlled by the same holding

company as BCBL and do not come under

consolidated supervision, is sufficient

evidence that a parallel owned banking

structure exists. The fact that you, Micheal

Coye, Dr. Uric Bobb, Phillip Johnson,

Phillip Osborne and Peter Gaze are directors

and/or officers of all three banks or their

parent companies is further evidence.”

4. The letter concludes that there is reason for CBB to proceed under

section 36 of the Banks and Financial Institution Act, Chapter 263

(BFIA), and that BBL would be afforded the opportunity to address

all its concerns in relation to the allegation of parallel banking. In

4

another letter of the same date – 16th December, 2010 – to Mr.

Guiseppi and Mr. Johnson of BBL, the CBB wrote:

“In late July 2010, the Central Bank

completed a Special Examination of BBL.

… The Central Bank is thus of the view that

the facts and circumstances, as set out in the

Special Examination Report and other

related correspondence, constitute

reasonable grounds for the Central Bank to

conclude that BBL, in conducting the

business of a licensed Bank, has carried out

and is pursuing a course of conduct that is

detrimental to the interest of its depositors

and its customers.

The Central Bank proposes to issue Order or

Directives to BBL in respect of its conduct.

In accordance with section 36(4) of the

BFIA, BBL is here notified that it is entitled

to make objections to the Issuance of Orders

or Directives, in respect of the aforesaid

conduct, on or before 17 January 2011. Any

BBL objections can be made at the office of

the Central Bank of Belize on Goal Lane,

Belize City, Belize, at 11:00 a.m. At this

time, the Central Bank will hear BBL’s

objections (if any) and determine whether or

not Orders or Directives should be issued to

BBL.”

5. By a previous letter dated 3rd

September 2010 to BBL, CBB

accompanied the letter with a Basel Committee Report on Parallel-

owned Banking Structures. The Basel Committee published the

report in January 2003 which was prepared by members of a Working

Group on Cross Border Banking consisting of persons with

5

experience in monetary policy, and banking supervisors from several

countries, including the UK, France, Germany, Japan, Singapore and

the USA and the Caribbean. The claimants do not object to the

admissibility of the Basel Report in evidence; but object to the Report

on the ground that it is not part of the law of Belize. But at the same

time, the claimants rely on aspects of the Report in support of their

written submissions. We will consider this Report below.

6. In another letter dated 21st December, 2010 to the second claimant,

the CBB wrote: “That the change in the shareholding structure of

British Caribbean Bank Limited (BCBL) that took place on 1

December 2008 effectively made BCB Holdings the owner of a

parallel banking structure. This resulted from the reduction of the

Belize Bank Limited’s (BBL) shareholdings in BCBL, to 23.1%

which changed BCBL’s status from an affiliate as defined by section

2(1) of the Banks and Financial Institutions Act (BFIA). For purposes

of consolidated supervision, this effectively excludes BCBL from the

BBL group.” In the said letter, The CBB states that a parallel banking

structure exists because:

(a) BCBL has the same holding company

as Belize Bank Limited (BBL) and

British Caribbean Bank

International Limited (BCBIL);

(b) All three banks share common

directors and officers;

(c) BCBL and BCBIL share similar

names;

(d) All three banks conduct interlinked

banking business and are known to act

6

in consert;

(e) All three banks are indirectly

controlled by the same person; and

(f) BCBL is not subject to consolidated

supervision by the Central Bank.

7. Parallel banks are defined as “banks licensed in different

jurisdictions that, while not being part of the same financial

group for regulatory consolidated purposes, have the same

beneficial owners and consequently often share common

management and interlinked business: see first affidavit of

Glenford Ysaguirre at paragraph 4. Mr. Ysaguirre in his

affidavit highlighted problems associated with parallel banking

as follows:

“Parallel banking is undesirable in and of

itself. The particular risks associated with

parallel-owned banking structures stem

primarily from the possibility that officers or

directors of one of the parallel banks will

expose the bank, either intentionally or

unintentionally, to higher risks through

transactions with related parallel banks.

There is a risk that transactions may not be

conducted at arms-length, or that the

relationship may be used to fabricate the

financial position of one or more of the

institutions. For instance, the following may

result:

“∙ One parallel bank may seek to

evade legal and other regulatory

lending limits by carrying out

transactions through its related

7

parallel banking, thereby

increasing concentration risk.

∙ Assets, earning and losses may be

artificially allocated between

parallel banks. Similarly, low-

quality assets and problems loans

can be shifted between parallel

banks to manipulate earning or

losses and to avoid regulatory

scrutiny.

∙ Capital can be generated artificially

through the use of stock purchase

loan from one parallel bank to the

other. As a result, capital for one

of the parallel banks is increased

even though there is no external

capital injection into either bank.

∙ One of the parallel banks may be

the conduit or participant in a

transaction that violates local law or

the laws of a foreign country, or

that is designed to benefit one of

the banks, to the detriment of the

other.

∙ One bank that experiences financial

difficulties may pressure the related

institution to provide liquidity or

other support in excess of legal

limits or prudential norms.

∙ Money-laundering concerns may be

heightened, especially when the

foreign parallel bank is situated

in a country where anti-money

laundering standards are not robust.

8

The parallel banking structure also

facilitates decision by boards of directors

and or officers common to both banks that

are not necessarily in the best interests of the

supervised bank but not subject to Central

Bank control because made by a bank which

is not subject to the Central Bank’s

consolidated supervision.”

8. The said letter of 21st December, 2010 concluded that the CBB had

recommended voluntary acceptance through BBL of consolidated

supervision, inclusive of BCBHL and BCBL, but this offer was

rejected.

9. The evidence shows that before the directives, considered below, were

issued several meetings between the CBB and the first and second

claimants were held, during which the CBB informed the claimants

that a system that permits parallel banking to occur must be subject to

consolidated supervision or be dismantled. Where a parallel banking

structure is not remedied, one solution, according to the CBB, is to

“ring fence” the BBL who is under the CBB’s control, under the

BFIA. The term “ring fence” means limiting the exposure of the

domestic bank, to its related parallel banks and other members of the

corporate group. The purpose of the Directives, according to the

CBB, is to ring fence the first claimant. The Governor testified that

the claimants were told by him that the Directives were likely to be

issued if the situation of parallel banking continued without

consolidated supervision. The CBB also informed the claimants that

9

it would take regulatory action under section 36(1) of the BFIA,

which states:

“36.-(1) Where the Central Bank has

reasonable grounds to believe that a

licensee, a holding company, an

affiliate or an official of such a

licensee (hereinafter the “subject

person”), in conducting the business

of the licensee, holding company or

affiliate, is committing or pursuing or

is about to commit or pursue any act

or course of conduct that is

detrimental to the interests of its

depositors or customers or a violation

of this Act, or any regulation, circular,

order, directive, notice or condition

imposed in writing by the Central

Bank, the Central Bank may direct the

subject person to do any or all of the

following-

(a) cease or refrain from doing

the act or pursuing the course

of conduct, or

(b) perform such acts as, in the

opinion of the Central Bank,

are necessary to rectify the

situation. In particular, but

without limiting the

generality of the foregoing,

the Central Bank may-

(i) require the subject person to refrain

from adopting or perusing a

particular course of action or to

restrict the scope of its business in a

particular way;

10

(ii) impose any limitation on the

subject person’s acceptance of

deposits, the granting of credit or

the making of investments;

(iii) prohibit the subject person from

soliciting deposits either generally

or from persons who are not

already depositors;

(iv) require the revision of any contract

to which the subject is a party, or

order the subject person to make

restitution or recompense to any

person aggrieved by its actions; or

(v) require the suspension or removal

from office of any director, officer,

official or other subject person.”

10. In the letter above dated 16th December, 2010 from CBB giving a time

period to BBL to object to the issuance of the Directives, Mr.

Guiseppi replied by letter dated 23rd

December, 2010 that: “BBL is

not able to prepare objections to any proposed Orders or Directives in

circumstances where the Central Bank has not yet provided the terms

of those Orders or Directives. Understandably, BBL will need details

of the Orders and Directives that the Central Bank proposes to make

in order to consider them and formulate any objections that it may

have.”.

11. The CBB replied on 4th

January, 2011 to Mr. Guiseppi letter that: “In

your letter you say that The Belize Bank Limited is not able to prepare

objections to any proposed Orders or Directives in circumstances

where the Central Bank has not yet provided the terms of those Orders

11

and Directives. . . . The Central Bank has notified you in detail of the

circumstances in which it is considering issuing Orders or Directives. .

. . Please review section 36(4) under which the Central Bank issued

the notice of 16th

December, 2010 as well as the contents of the

notice. The Belize Bank Limited is entitled to present objections to

the making of any Orders or directives based on the actions or course

of conduct of the bank that have been set out in the notice. . . .

Formulation of these, (if any), will depend on the representations of

the licensee. Accordingly, the 30 day period in which to object to the

issuance of Orders or Directives on the circumstances set out by the

Central Bank remains as stipulated in my notice of 16 December

2010.”

12. Mr. Guiseppi replied by letter dated 7th January, 2011, and pointed

out that BBL was entitled to know what action was being proposed in

order to make informed objections. Mr. Guiseppi refers to a

precedent from CBB, in another matter, where the CBB provided a

text of the proposed directive prior to its issuance. This text was

given in a letter dated 5th August, 2010 from CBB to BBL informing

BBL of its intention to issue a directive, and inviting BBL to make

representations why the directive should not be issued. The claimants

submit that this precedent should be followed, and it is unfair and in

breach of natural justice not to do so.

13. On 17th January 2011 BBL, although previous requests for a copy of

the text of the Directives were not complied with prior to their

12

issuance, still submitted to the CBB elaborate written objections to

CBB’s proposal to issue the Directives. Having received the

objections, the CBB on the 9th

February, 2011 sent to the BBL the two

Directives, Directives 1 and 2 of 2011 which are subject matters of

this case. The Directives were issued under section 36(1) of the

BFIA. On the 10th February, 2011, the CBB issued revised terms and

conditions of the licence of the BCBIL (the Revisions) under section

8(2) of the International Banking Act Chapter 267 (IBA). Section 8 is

as follows:

“8. (1) The Central Bank may grant a licence

under this Act upon the payment of the prescribed

fee and subject to such terms and conditions as it

may specify; or it may refuse to grant a licence.

(2) Where a licence is granted subject to the

condition that the terms and conditions thereof

may be varied subsequent to its issue, the Central

Bank may at any time revoke any of the original

terms and conditions or impose additional terms

and conditions.”

The Revisions replaced a licence previously granted to BCBIL on 3rd

August, 2009 by CBB.

The Directives

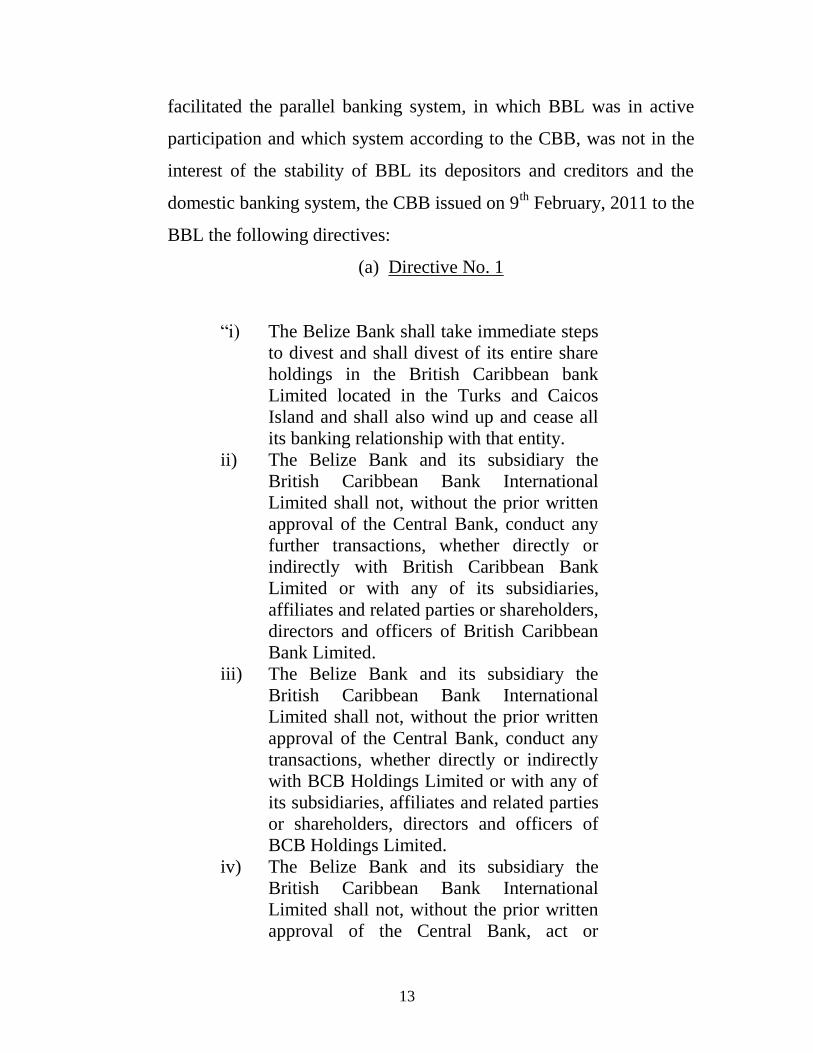

14. Due to a determination by the CBB that BCBHL and BCBL were

conducting parallel banking, which determination found agreement of

the FSC; and because BBL reduced its shareholding in BCBL from

ownership of BCBL to 23% which the CBB determined enabled and

13

facilitated the parallel banking system, in which BBL was in active

participation and which system according to the CBB, was not in the

interest of the stability of BBL its depositors and creditors and the

domestic banking system, the CBB issued on 9th

February, 2011 to the

BBL the following directives:

(a) Directive No. 1

“i) The Belize Bank shall take immediate steps

to divest and shall divest of its entire share

holdings in the British Caribbean bank

Limited located in the Turks and Caicos

Island and shall also wind up and cease all

its banking relationship with that entity.

ii) The Belize Bank and its subsidiary the

British Caribbean Bank International

Limited shall not, without the prior written

approval of the Central Bank, conduct any

further transactions, whether directly or

indirectly with British Caribbean Bank

Limited or with any of its subsidiaries,

affiliates and related parties or shareholders,

directors and officers of British Caribbean

Bank Limited.

iii) The Belize Bank and its subsidiary the

British Caribbean Bank International

Limited shall not, without the prior written

approval of the Central Bank, conduct any

transactions, whether directly or indirectly

with BCB Holdings Limited or with any of

its subsidiaries, affiliates and related parties

or shareholders, directors and officers of

BCB Holdings Limited.

iv) The Belize Bank and its subsidiary the

British Caribbean Bank International

Limited shall not, without the prior written

approval of the Central Bank, act or

14

continue to act as collecting agent for

deposits or loan payments on behalf of the

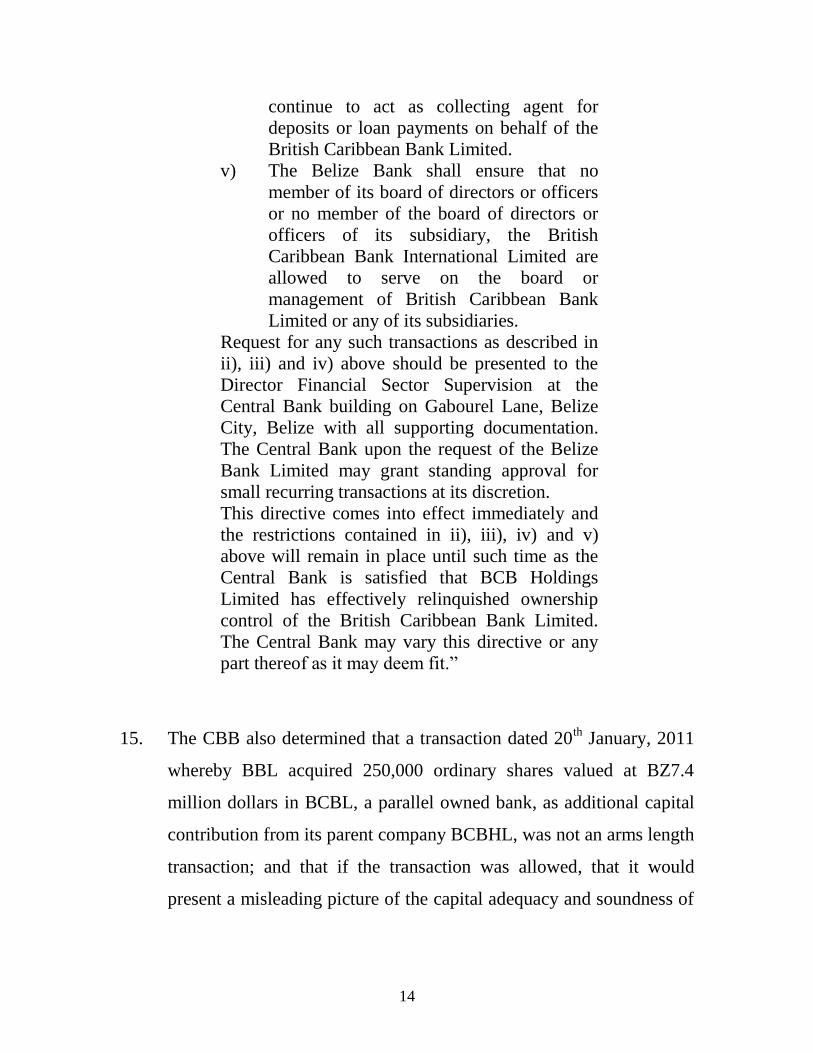

British Caribbean Bank Limited.

v) The Belize Bank shall ensure that no

member of its board of directors or officers

or no member of the board of directors or

officers of its subsidiary, the British

Caribbean Bank International Limited are

allowed to serve on the board or

management of British Caribbean Bank

Limited or any of its subsidiaries.

Request for any such transactions as described in

ii), iii) and iv) above should be presented to the

Director Financial Sector Supervision at the

Central Bank building on Gabourel Lane, Belize

City, Belize with all supporting documentation.

The Central Bank upon the request of the Belize

Bank Limited may grant standing approval for

small recurring transactions at its discretion.

This directive comes into effect immediately and

the restrictions contained in ii), iii), iv) and v)

above will remain in place until such time as the

Central Bank is satisfied that BCB Holdings

Limited has effectively relinquished ownership

control of the British Caribbean Bank Limited.

The Central Bank may vary this directive or any

part thereof as it may deem fit.”

15. The CBB also determined that a transaction dated 20th

January, 2011

whereby BBL acquired 250,000 ordinary shares valued at BZ7.4

million dollars in BCBL, a parallel owned bank, as additional capital

contribution from its parent company BCBHL, was not an arms length

transaction; and that if the transaction was allowed, that it would

present a misleading picture of the capital adequacy and soundness of

15

BBL, the CBB issued another Directive on the said 9th February, 2011

as follows:

(b) Directive No. 2

“i) The Belize Bank Limited take immediate

steps to reverse the transaction of 20

January 2011 whereby it acquired 250,000

ordinary shares of British Caribbean Bank

Limited valued at BZ$7.4 million by way of

further capital contribution from its parent

company.

ii) The Belize Bank shall provide the Central

Bank with proof of the reversal of the said

transaction by 15th

February, 2011.

This directive is to be complied with forthwith.”

Revision and Variation Orders

16. In relation to the revision of the licence of BCBIL, the CBB had

issued the licence with terms and conditions under the BCBIL in June

2009. Since the CBB came to the determination that because of the

creation and participation in a parallel banking scheme by BBL, and

by extension BCBIL, as a subsidiary of BBL, and in the interest of

BBL and BCBIL, their customers and depositors, the CBB on 10th

February, 2011 issued revised terms and conditions of the licence to

restrict actions by BCBIL supportive of a parallel banking structure.

17. The CBB also issued, as mentioned above, two variation orders,

Variation orders No. 1 and No. 2 dated 23rd

June, 2011 and 22nd

December, 2011 respectively for the purpose of varying the terms of

16

Directive No. 2 of 2011. The factual circumstances under which the

variation orders were made were not disputed. The claimants, on 15th

February, 2011, on an exparte application, applied for an interim

injunction restraining the defendant from enforcing the Directives and

the Revision, which injunction was granted on the said date. The

claimants, about a week later, filed an application to continue the

injunction until the hearing and determination of the claim which was

previously filed. On 22nd

February, 2011 the defendant filed an

application to discharge the injunction. The Supreme Court heard the

applications, and on 25th May, 2011, the court, in a written decision of

the said date, discharged the injunctions. Since the injunction was

discharged on 25th

May 2011, the Directives made on 9th

February,

2011, according to the defendant, became effective, not from 25th

May, 2011, but from 9th

February, 2011 when they were made.

Therefore the financial statements and reports of BBL for the financial

year ending 31st March, 2011, according to the defendant, must

comply with the Directive as at 9th

February, 2011, and not as at 25th

May, 2011 as was done by BBL which should have in its financial

statements for the year ending 31st March, 2011 reversed the

transaction of 20th January, 2011.

18. BBL disagreed and argued that the financial statements were correct,

and in accordance with generally accepted accounting principles.

BBL says, if I understand it correctly, that the Directives take effect

on the discharge of the injunction on 25th day of May, 2011, that is

after the end of BBL’s accounting year – 31st March 2011 – and

therefore the transaction would be reflected in the financial statements

17

of the coming financial year – 31st March, 2012. According to BBL

its financial statements and reports for the financial year ending 31st

March, 2011 were approved by its auditors, accountants and its Board

of Directors on 23rd

and 24th May, 2011 before the discharge of the

injunction on 25th

May, 2011. BBL says that since the interim

injunction was in effect up to the 24th May, 2011, the directives did

not take effect until after the discharge of the injunction on 25th May,

2011 when the financial year had already ended and the financial

report had already been approved and audited, and therefore the

financial statements cannot now be properly amended. The decision

discharging the injunction is not retrospective but prospective and

from 25th May, 2011. The factual position, according to BBL, is that

the financial statements had already been approved and audited for a

transaction that factually occurred during the financial year ending

31st March, 2011 and that fact cannot be changed and it is against

accounting principles to change it. The claimants state that the

transaction could be accounted for in the financial statements of BBL

for the financial year ending 31st March, 2012.

19. The defendant did not agree, and on 23rd

June 2011, the CBB, more

than three months after the date of the Directives, issued without

express notice to the claimants, an order, Variation Order No. 1,

under section 36(3) of the BFIA varying Directive No. 2 of 2011 as

follows:

18

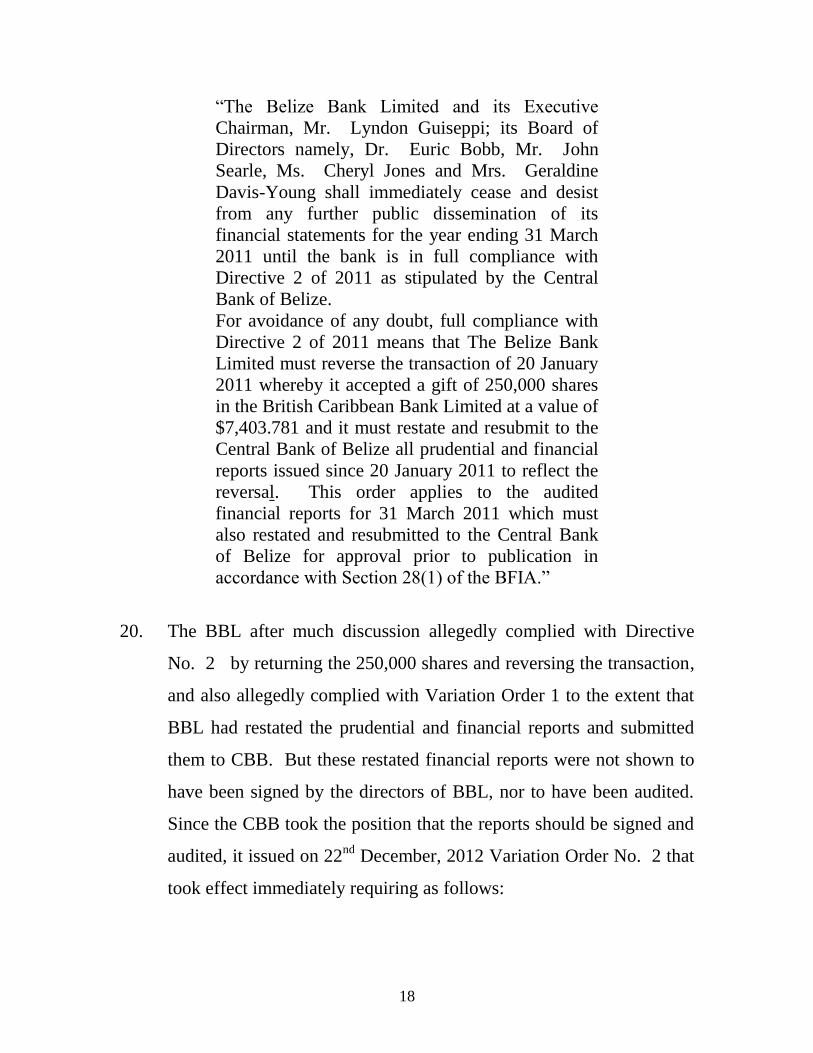

“The Belize Bank Limited and its Executive

Chairman, Mr. Lyndon Guiseppi; its Board of

Directors namely, Dr. Euric Bobb, Mr. John

Searle, Ms. Cheryl Jones and Mrs. Geraldine

Davis-Young shall immediately cease and desist

from any further public dissemination of its

financial statements for the year ending 31 March

2011 until the bank is in full compliance with

Directive 2 of 2011 as stipulated by the Central

Bank of Belize.

For avoidance of any doubt, full compliance with

Directive 2 of 2011 means that The Belize Bank

Limited must reverse the transaction of 20 January

2011 whereby it accepted a gift of 250,000 shares

in the British Caribbean Bank Limited at a value of

$7,403.781 and it must restate and resubmit to the

Central Bank of Belize all prudential and financial

reports issued since 20 January 2011 to reflect the

reversal. This order applies to the audited

financial reports for 31 March 2011 which must

also restated and resubmitted to the Central Bank

of Belize for approval prior to publication in

accordance with Section 28(1) of the BFIA.”

20. The BBL after much discussion allegedly complied with Directive

No. 2 by returning the 250,000 shares and reversing the transaction,

and also allegedly complied with Variation Order 1 to the extent that

BBL had restated the prudential and financial reports and submitted

them to CBB. But these restated financial reports were not shown to

have been signed by the directors of BBL, nor to have been audited.

Since the CBB took the position that the reports should be signed and

audited, it issued on 22nd

December, 2012 Variation Order No. 2 that

took effect immediately requiring as follows:

19

“Now therefore pursuant to section 36 of the BFIA

the CBB hereby issues the following variation

order in support of Bank Directive No 2 of 2011

and Variation Order No 1

1. BBL shall have the restated prudential and

financial reports audited by an approved

external auditor in the same way as if the said

reports were the reports required to be audited

by section 28 and in accordance with section

30 of the BFIA.

2. BBL shall have the said reports signed in the

usual manner by an on behalf of its board of

directors,

3. BBL shall submit the said reports, audited and

signed as specified above (the completed

reports), to the Central Bank not later than 16th

January 2012 and

4. BBL shall thereafter, and not alter than 31st

January 2012, publish, exhibit and otherwise

deal with the completed reports in the manner

specified by section 28 of the BFIA.”

The Claims

21. The claimants urge that the Directives 1 and 2, and Variation Orders 1

and 2 are ultra vires the provisions of the BFIA and unlawful, null and

void. They further claim that the revision is also contrary to the IBA,

unlawful null and void. On 24th February, 2012 the claimants filed an

amended fixed claim form, amending a previous claim form filed on

21st February, 2011, claiming the following reliefs:

“1.1 Declarations that Directives 1 and 2 issued

by the Central Bank of Belize on 9th

February, 2011, Variation Orders 1 and 2

20

issued 23rd

June, 2011 and 22nd

December,

2011 and the Revisions to BCBIL’s License

(each as defined below) are: ultra vires the

Central Bank’s statutory powers; and/or

(a) are disproportionate; and/or

(b) were made following an unfair

procedure; and/or

(c) were made on the basis of an erroneous

view of the law; and/or

(d) were made on the basis of an erroneous

view of the facts; and/or

(e) were made one the basis of irrelevant

considerations; and/or

(f) were made following a failure to

consider relevant considerations; and/or

(g) are arbitrary and/or made with an

improper motive;

and as a consequence are unlawful, void and

of no effect.

1.2 the defendant shall be restrained, by way of

an injunction, whether by itself, its servants

or agents or howsoever, from acting upon, in

consequence of or seeking to enforce the

Directives, the Variation Orders, and the

Revisions to BCBIL’s Licence;

1.3 such other reliefs as the court deems just and

equitable; and

1.4 costs.”

The Ultra Vires Points

(i) Notice

22. It is submitted by the claimants that CBB failed to comply with

section 36(4) of BFIA which requires, prior to the issuance of the

directives, a notice containing “a statement of the actual or purposed

action or course of conduct” giving rise to the directives, and also

21

containing the time and place, not less than 30 days when the CBB

will hear objections; and therefore the Directives, according to the

claimants, are unlawful, null and void and ultra vires the section under

which the Directives were made. Section 36(4) of BFIA states:

“(4) Prior to the issuance of any order or

directive under subsection (1) or (2), the

Central Bank shall cause to be served on or

delivered to the licensee or subject person a

notice containing a statement of the actual or

proposed action or course of conduct

referred to in subsection (1), or of the failure

to satisfy the requirements referred to in

subsection (2), and specifying a time and

place (not less than thirty days after the

service or delivery of the notice) at which

the Central Bank shall hear objections and

determine why an order or directive should

not be issued, and if the Central Bank so

decides a copy of every such order or

directive shall promptly be served on the

subject person.”

23. The CBB, say the claimants, “failed either to give adequate notice or

to give any notice at all” and therefore the Directives are void.

Moreover, say the claimants, the letter from the CBB dated 16th

December, 2010, a purported notice, “made no mention of alleged

parallel bank activities which were plainly the object of the

Directive;” and in any event, provisions of the letter did not amount to

a “statement of the actual or proposed action or course of conduct”

required under section 36(4) above.

22

24. As shown at paragraphs 3 and 4 of this judgment, the CBB wrote two

letters to the BBL dated 16th

December, 2010, prior to the issuing of

the Directives. One letter stated that there was “sufficient evidence

that a parallel owned banking structure exists” and that there was

reason to proceed under section 36 of the BFIA, and BBL would be

afforded the prescribed time to address concerns. In the other letter

given above of the same date, the CBB states that it purposes to issue

the Directives, and tells BBL that it is entitled to make objections to

the Directives on or before 17th January, 2011 giving BBL the thirty

days opportunity stated in section 36(4). In another letter above dated

21st February, 2010, the CBB wrote that BCBHL became the owner of

a parallel banking structure, and stated reasons, as we saw above, why

a parallel banking structure existed. This letter concludes, that “the

Central Bank is now informing you that it will take regulatory action

under section 36(1) of the BFIA”… Moreover, the letter above dated

4th January, 2011 reminded the claimant of the period given for their

objections. And in another letter dated 5th

January, 2011, BBL

accepted that it received a previous letter regarding CBB’s notice of

intention to issue Directives and Orders.

25. In my view the above letters amount to evidence that shows that the

claimants, although not supplied with the actual Directives prior to

their issuance, knew that Directives would be issued and the subject

matter of their contents and proposed action and the reasons for their

issuance prior to them being issued. The doctrine of ultra vires ought

to be reasonably and not unreasonably understood and applied and

whatever may fairly be regarded as incidental to or consequential

23

upon those things which the legislature has authorized ought not

(unless expressly prohibited) to be held by judicial construction to be

ultra vires: see AG v. Great Easter Ry Co. 1880 5AC 473 at p 478.

In my view, the evidence above satisfies the notice required by section

36(4). The notice, as we saw above, was given in December 2010 and

the Directives were not issued until 9th February, 2011 thereby giving

adequate opportunities to the claimants to object to the issuance of the

Directives, the subject matter of which, and the reasons for which, the

claimants knew.

26. After insisting on having prior notice of issuance of the actual terms

of the Directives, the claimants on 17th November, 2010 did give in

writing to the CBB their objections to the issuance of the Directives.

The written objections to the Directives were given in an eight page

document containing thirty-three paragraphs containing their

objections to the Directives at great length. In my view, this clearly

shows that the claimants were heard on the Directives prior to their

issuance and shows that the claimants knew the Directives were

coming and had knowledge of the subject of their contents and the

proposed action.

27. (ii) Requirements

The submission is that Directive No. 1 “purported to make

requirements” which section 36(1)(b)(i), under which it was made, did

not authorize; and therefore the Directive is unlawful and void. The

“requirements” objected to by the claimants are contained at

paragraphs (i) and (v) of the Directive 1 given above. The submission

24

is that paragraph (i) does not fall within the words of the above

section 36(1)(b)(i), namely to “refrain from adopting or perusing (sic)

a particular course of action.” Therefore paragraph (i) of the Directive

is void. As I see it, on a careful consideration of section 36 it would

be seen that paragraph (i) of the Directive, falls within the said

section, especially section 36(1)(a) and (b) of the Act which gives the

CBB power to “direct” or “to perform such acts,” to rectify a

situation. Section 36(1)(b)(i) gives the CBB a discretion “to restrict

the scope” of a licensee’s business” in a particular way.” Paragraph

(i) of the Directive in effect restricts the business of BBL in a

particular way. This answer is also applicable to the claimants

objection to paragraph (v) of Directive 1.

28. (iii) Reversal

In relation to Directive 2, it is said that the requirements of this

Directive requiring BBL to reverse the transaction of 20th January,

2011 concerning the 250,000 ordinary shares of BCBL, do not fall

within section 36(1)(b)(iv) of the Act under which it is made, because

the Directive does not require the revision of any contract, as

mentioned in the section, and therefore the Directive is unlawful and

void. Section 36(1)(b) clearly authorities the CBB to direct BBL “to

perform such acts as in the opinion of the Central Bank are necessary

to rectify the situation.” The situation the CBB wanted to rectify was

the transaction (the Transaction) whereby BBL increased its

shareholding on 20th January, 2011 in BCBL by 250,000 ordinary

shares valued at $7,403,781 which CBB considered to be not an arms

25

length transaction and misleading. Surely this situation falls within

those general words above of section 36(1)(b) of the BFIA.

29. (iv) Insufficient Evidence

The claimants urge that CBB acted without sufficient evidence and

misdirected itself when it issued the Directives 1 and 2 under section

36(1). This section, authorizes the CBB where it has reasonable

grounds to believe that a licensee in conducting its business “is

committing or pursuing or is about to commit or pursue any act or

course of conduct that is detrimental to the interest of its depositors or

customers. …” The claimants say that on the facts, reasonable

grounds to believe the quoted portion above, did not exist, as there is

no evidence that the claimants committed or about to commit or

pursue such act or conduct. The evidence in the various letters above

between CBB and BBL, shows that a parallel banking structure in

existence, involving the claimants and BCBL; and there is also the

Transaction which the evidence shows presents a misleading picture

of the capital adequacy of BBL. The evidence is that there existed a

parallel banking system and it has been shown above the problems of

such a system. This evidence, it seems to me, constitutes reasonable

grounds under section 36(1) of BFIA to make the Directives. It is true

that the drafters of the Directives, instead of including the relevant

words of section 36(1) in drafting them, which in my view ought to

have been done, used only words in relation to the conduct of BBL

such as “facilitation of and participation in parallel banking scheme

not in the best interest of the domestic banking system and in

consequence its depositors and creditors:” whereas section 36(1)

26

speaks of licensee “committing or pursuing or is about to commit or

pursue any act or course of conduct that is detrimental to the interests

of its depositors or customers.” But the evidence is that participation

in a parallel banking scheme is conduct that is detrimental to the

interest of BBL’s customers or depositors. It seems to me though that

there may not be a meaningful difference between “facilitation and

participation in a parallel banking scheme” and “committing or

pursuing” such parallel banking scheme.

30. It is true that on the face of the Directive 1 there is no statement that

actions by BBL are detrimental to its depositors and customers as

submitted by the claimants. Section 36(1) under which the Directive

was issued does not require such a specific statement on the face of

the Directive, and I have not found any provision in the Act which

requires it. The letter of 16th December, 2010 to BBL is evidence that

the actions being pursued by BBL are detrimental to BBL’s depositors

and customers. The Directive No. 1 itself states that participation in

parallel banking scheme is not in the best interest of the domestic

banking system its depositors and creditors of BBL, who knew of the

allegation against it of parallel banking. And there is evidence in the

second affidavit of Glenford Ysaguirre highlighting problems

associated with parallel banking which could result in detriment to the

banks, depositors and customers.

31. (v) Misleading

27

Directive 2 at the fourth paragraph states that the CBB has determined

that if the Transaction is allowed it will present a misleading picture

of the capital adequacy and soundness of BBL. The claimants say

there is no evidence to support what is stated above in the fourth

paragraph of the Directive, or that the Transaction is detrimental to the

interest of BBL’s depositors and customers. Therefore the Directive 2

is void and unlawful and contrary to section 36(1) of the Act. But

there is, in fact, evidence from Mr. Ysaguirre in his fourth affidavit

which is supported to some extent by Mr. Guiseppi in his fifth

affidavit where a share transfer form dated 31st May, 2011 is

exhibited, to the effect that BBL transferred 3,249,999 shares at $1.00

US or ($2.00 BZ) each in BCBL to a company named BB (TCl)

Holdings Limited, the parent company of BCBL, for the sum of

US$6,701.890.38. The above amount of shares transferred included

the said 250,000 shares referred to above in the Transaction which

were valued, as we saw above, at $7,403,781, which when divided by

250,000 would result at $29.16 BZ per share, greatly higher than the

$2.00 per share above. In relation to the above difference in the price

of the shares, Mr. Ysaguirre in his fourth affidavit at paragraph 14

swore as follows:

“This implies that the other 2,999,999 shares of the

exact same class were divested by the BBL for a

disproportionately lower price of BZ$2.00 per

share i.e. at par value (See Exh. L.G. 36 to fifth

affidavit of Lyndon Guiseppi). This is a marked

variation in pricing for identical assets of the same

class and underscores the Central Bank’s concern

as to the integrity of the value assigned to the

28

250,000 shares when they were acquired on 20th

January 2011. The huge discrepancy in pricing

treatment for these identical shares also

underscores the Central bank’s concerns about

financial statements that could mislead the public

and hence the need to expunge the entire

transaction of 20th

January 2011 from the books of

BBL.”

32. The transfer form giving particulars of the transfer of the 3,249,999

shares at US$1.00 each was given in evidence by Mr. Guiseppi in

paragraph 12 of his fifth affidavit. On the basis of the above, it is a

misconception, in my view, to submit that there is no evidence to

support what is stated in the fourth paragraph of Directive 2.

33. It is further said that there has been no breach by BBL of the BFlA or

any regulation, circular, order, directive, notice or condition imposed

in writing by the CBB. Once again the evidence is that there was non

compliance by BBL of e-mails from CBB not to increase its

shareholding in BCBL, – not to engage in the Transaction; and in a

letter dated 31st January, 2011 to BBL CBB said it cannot support the

Transaction for several reasons, including the valuation of the 250,000

shares at a value of BZ7.4 million or BZ29,16 per share on the ground

that it was not derived from an objective arms length assessment, and

because CBB did not agree that an investment in BCBL, an entity that

is weaker than BBL, can strengthen BBL’s capital. BBL by letter

dated 1st February, 2011, in spite of the correspondence above from

CBB requesting BBL not to complete the Transaction, BBL in the

29

letter to CBB said that the “transaction had been completed and all

steps have been taken including the lodgment and filing of the share

transfer in TC1”: see e-mail and letters at G.Y. 32 to 37 of the fourth

affidavit of Glenford Ysaguirre. The above is clearly evidence of

violation of requirements in writing given by CBB to BBL.

34. (vi) Necessary to rectify the situation

It is said by the claimants that section 36(1)(b) only permits the CBB

to issue directives where what is required is necessary to rectify the

situation – parallel banking. The claimants state that the only action

which could be said to be necessary to rectify the situation was

dialogue between CBB and FSC. The section states inter alia, that

the CBB may direct the licensee to “perform such acts as, in the

opinion of the Central Bank, are necessary to rectify the situation.”

The evidence above shows that parallel banking is a course of conduct

that is detrimental to the interest of depositors and customers. CBB

therefore had the authority under the general words above of section

36(1)(b) to direct a reversal of the transaction to rectify the situation.

Moreover, the relationship between FSC and CBB, as we saw above,

was not amendable to dialogue at the date of the Directive, because

the relationship had been terminated about one month before because

of mistrust and alleged misconduct of FSC in relation to BBL

reduction of shares in BCBL without prior information to CBB by

FSC. It seems to me, in that environment of distrust, it would have

been an unreasonable exercise to engage FSC in productive dialogue,

30

especially considering the contents of the letters exchanged between

the parties.

35. (v) Restrictions

The claimants further state that section 36(1)(b)(i) above authorizes

the imposition of restrictions on the subject person, in this case the

BBL; but Directive 1, made under the section, requires at paragraph

(i) BBL “to do something positive” which requires BBL “to take

immediate steps to divest and shall divest of its entire shareholdings in

BCBL and shall also wind up and cease all its banking relationship

with that entity.” The above paragraph (i) of Directive No. 1 does

not, according to the claimants, impose restrictions as the section

requires, but does something positive, and therefore the paragraph is

contrary to section 36(1)(b)(i) of the Act. Once again paragraph (i) is

not only consistent with the general power given by section 36(1)(b),

but is in conformity with section 36(1)(b)(i) when it required BBL to

wind up and cease all its banking relationship with BCBL. This

seems to fall within the power of CBB under the section 36(1)(b)(i) to

restrict the scope of a licensee business in a particular way.

36. Paragraph (v) of Directive 1 which restricts members of BBL Board

of Directors and officers from serving on the board or management of

BCBL is also said to be inconsistent with section 36(i)(b)(i) of the

BFIA and void. Once again section 36(1)(b)(i) states that the CBB

may restrict the scope of a licensee business in a particular way.

Paragraph (v) of Directive 1 restricts directors and officers from

31

serving on the board of BCBL and therefore restricts the business of

BBL in a particular way.

37. (vi) Contract

Under section 36(1)(b)(iv) of the BFIA, the CBB is authorized to

“require the revision of any contract to which the subject is a party, or

order the subject person to make restitution or recompense to any

person aggrieved by its actions.” The CBB acted under the said

section in making Directive 2 which orders BBL to take immediate

steps to reverse the Transaction. It is submitted by the claimants that

Directive 2 does not cause a revision of any contract, as is required by

the section, but orders a reversal of the said Transaction which is

different from the requirements of the section and therefore the

Directive is ultra vires the section. A careful reading of section

36(1)(b) ought to show that the general power given in that section to

the CBB is not limited by subsection (iv) of the said section 36(1)(b).

In other words, the Directive 2 clearly falls within the general words

above of section 36(1)(b) authorizing CBB to perform such acts as are

necessary to rectify the situation, which in this case meant the

Transaction. The general purpose of section 36 of the Act would be to

prevent a licensee such as BBL from committing or pursuing a course

of conduct that is detrimental to the interest of its depositors or

customers. Parallel banking, is conduct, as we saw above, that is

detrimental to depositors or customers of BBL.

(vii) Opportunity to be heard

32

38. It is also urged by the claimants that the Revision above of BCBL’s

licence by CBB was unlawful because it was done without giving

BCBL an opportunity to be heard, and because it was done without

any evidence to support the purpose for which the Revision was done,

which purpose was, as stated in CBB letter of 10th February, 2011

above, “in the best interest of the national banking system, the

stability of BBL and BCBL and in consequence, their depositors and

customers.” In a letter to Mr. Johnson, President of BCBL from the

Governor of CBB, it is stated that “The need to revise BCBIL terms

and conditions of licence has arisen as a result of the creation of and

participation in a parallel banking scheme by BBL and by extension

BCBIL as a wholly owned subsidiary.” There is evidence, as we saw

above, that there existed a parallel banking structure and in which

BCBIL was a part; and, we have also seen above the effects that a

parallel banking structure can have on the national banking system

and depositors and customers of a bank.

39. Though BCBIL was not given actual notice of the Revision of the

licence prior to the revision, the letter of 10th February, 2011 gave

BCBIL “a twenty-one day period in which to make representations as

to why the revisions of the conditions of the licence should be varied

or removed.” BCBIL was afforded an opportunity to be heard with

respect to removing or varying the revision, though after it was made.

The revised licence itself states that it may be revoked or varied at any

time. In the light of the above opportunities, the court in its

discretionary powers, as we shall see below, ought to be reluctant to

strike down the revision on this ground.

33

(viii) No power to make variation orders

40. The variations orders are unlawful, say the claimants, because, firstly,

the Directive 2 which they seek to vary is itself ultra vires the BFIA.

It is further submitted by the claimants that CBB exceeded its

jurisdiction when it purported to make the variation orders under

section 36(3) of the BFIA when that section did not authorize the

CBB to make the orders. The section provides that any order or

directive shall be given by notice in writing to the licensee and the

order or directive “may be varied by further written orders or

directives.” According to the claimants, the variation orders did not

vary the Directive, but imposed new and different requirements from

those stated in the Directive. In other words, the CBB made “new

Directives under the guise of Variation Orders” and therefore acted

contrary to section 36(3) of BFIA. In addition, the CBB, say the

claimants, imposed the variation orders without notice as required by

section 36(4) of BFIA.

41. The words of section 36(3) of BFIA are clear: A Directive may be

varied by further written orders or Directives. There is no

modification or limitation on the varying power conferred on CBB by

the section. Moreover, the Oxford Dictionary defines the word “vary”

as “change from one form or state to another;” and the word “varied”

is defined as “involving a number of different types or elements.”

Based on the absence of any limitation on the word “varied” in the

section, and also considering the definition of the words, the

imposition of new and different conditions in the variation orders, in

my judgment, fall within the said section. Moreover, for the reasons

34

in this judgment I do not find myself agreeing that the Directives are

ultra vires the BFIA. In relation to the question of notice, section

36(4) states:

“(4) Prior to the issuance of any order or

directive under subsection (1) or (2), the

Central Bank shall cause to be served on or

delivered to the licensee or subject person a

notice containing a statement of the actual or

proposed action or course of conduct

referred to in subsection (1), or of the failure

to satisfy the requirements referred to in

subsection (2), and specifying a time and

place (not less than thirty days after the

service or delivery of the notice) at which

the Central Bank shall hear objections and

determine why an order or directive should

not be issued, and if the Central Bank so

decides a copy of every such order or

directive shall promptly be served on the

subject person.”

42. The variation orders are orders under the section but they were not

issued under subsection (1) or (2) of section 36, but under section

36(3): see variation order 1, but see variation order 2 which states it

was made under section 36. Section 36(3) states:

(3) Any order or directive given under

subsection (1) or (2) shall be given by notice

in writing to the subject person. Such order

or directive may be varied by further written

orders or directives; and any order or

directive may be revoked by the Central

35

Bank by notice in writing to the subject

person.”

It does not seem that a notice in writing is required by the subsection

prior to the varying of a directive. Moreover, Directive 2 required, as

we saw above, the reversal of the Transaction and required BBL to

provide CBB with proof of the reversal by 15th February, 2011. From

that Directive it is implied, it seems to me, that such a reversal would

involve adjusting the financial statements of BBL, signed and audited,

to reflect the reversal, and not to publish such statements until these

things are done. These are generally the matters required by the

variation orders. The terms of the Directive would imply the matters

stated the variation orders, requiring the restatement of financial

statements, audited and signed reflecting the reversal stated in the

Transaction. Consequently, the BBL knew or must have known the

nature of the orders before they were issued. Moreover, by letter

dated 31st May, 2011, before the variation orders were made, the CBB

in the letter to BBL wrote that: The financial statements as presented

are unsigned by any director or manager of BBL and are thus invalid.

The BBL then re-submitted signed Financial Statements to CBB on 1st

June, 2011 for which the CBB expressed thanks by letter of 3rd

June,

2011. In another letter dated 9th

June, 2011 to BBL, CBB wrote that

full compliance with Directive 2 “requires that BBL now amend all its

financial and prudential reports since 20th January, 2011 (the original

date of the transaction) including its year end financials to reflect the

complete removal of the offending transaction from the records.” The

36

letter states that if BBL fails to comply it will take enforcement

action. From the above it seems that BBL had advance knowledge of

the contents and nature of the variation orders.

43. The remedy of certiorari is discretionary and therefore the court may

refuse this relief even though there has been a clear violation of

natural justice: see Chief Constable v. Evans 1982 3 AER 141;

Hoffmann LA Roche v. Secretary of State 1975 AC 295 and

Gladden v. AG Supreme Court Claim No. 692 of 2010. In the

exercise of that discretion the court may consider the conduct of the

claimant. In White v. Kuzyel 1951 AC 585, the privy Council

refused a remedy to the claimant on the basis of his conduct. The

court found that the applicant’s right to natural justice was violated,

but refused a remedy because of the claimant’s conduct in breach of

his contract when he failed to comply with terms of the contract with

his union, to which he was bound. In the claim before me the BBL

reduced its status as owner of BCBIL without informing CBB, and

although it reversed the transaction it refused to reflect the reversal in

it financial statements from the dates of the Directive on grounds

which we saw above. Moreover, section 36(5) of BFIA makes

provision for the summary issue of an order or directive. For the

above reasons, the court declines to strike down the variation orders

on the ground of no notice of actual or proposed action under section

36(4) of BFIA.

(ix) Restatement of financial statements

37

44. It is further said that section 36 of BFIA does not empower the CBB

to make Directives or Orders, including the variation orders, that

impose mandatory requirements on a licensee with respect to the

circulation, restatement, audit, signature and publication of its

financial statements as the Directives and variation orders seek to do.

The BFIA does not authorize CBB, according to the claimants, to

order or direct these matters, which are matters for the licensee, such

as BBL, and its auditors and accountants. And even assuming that

these matters can be done by CBB under the section, it does not

authorize CBB according to the claimants, to make orders and

directives which would have a retrospective effect, as the Directives

and Orders in this case seek to do. It is further submitted by the

claimants that section 36 of BFIA does not empower the CBB to

require a licensee, such as BBL to behave “in the same way as if”

section 28 of BFIA applied to the amended and restated financial

statements, as paragraph (1) of the Variation Order 2 directed. It was

submitted that section 28 did not apply, because the licensee had

already complied with section 28 by publication of its financial

statements in accordance with section 28. Moreover, section 28 of

the BFIA, according to the claimants, sets out the scope and extent of

a licensee’s duties, such as BBL, in respect of audits. Paragraph (1) of

Variation Order 2 imposes, say the claimants, additional audit duties

and requirements not specified in the section 36 or in the BFIA and

therefore the Variation Order is unlawful and void. Section 36, say

the claimants does not, on a proper construction, authorize CBB to

direct the way in which audits are or should be carried out. In

38

addition it was submitted that section 36 did not authorize a particular

accounting treatment as the Directives and Orders seek to do.

45. I have to apologize for my repetition of this point, but I think the

above submissions fail to consider the general words of section 36(1)

(b). The section says that “the Central Bank may direct the subject

person to perform such acts as, in the opinion of Central Bank are

necessary to rectify the situation, in particular, but without limiting the

generality of the foregoing;” and the section goes in to list particular

acts the CBB may perform. I think the submissions fail to appreciate

that the particular acts mentioned in section 36(1)(b)(i) to (v) do not

limit what is stated in 36(1)(b): that the CBB may direct the licensee

to “perform such acts as, in the opinion of the Central Bank are

necessary to rectify the situation.” Directing the circulation,

accounting treatment, restatement, audit, signatories and the

publication of the financial statement falls within the general words of

the quoted phrase above which words are wide enough to include the

making of the Directives and Orders to apply to a transaction that

occurred before the making of the Directive or Orders. In relation to

the submission on section 28, the evidence is that the restated

financial statements submitted by BBL to CBB were not, at the date

of the Variation Order 2 signed and audited; and therefore could not

be properly said to have complied with section 28 of BFIA.

(x) Unreasonable and disproportionate

39

46. The claimants further submit that although section 36(1)(b) gives the

CBB the power to perform such acts as are necessary to rectify the

situation, the section does not confer on the CBB arbitrary or absolute

power to rectify the situation. The CBB under the section is bound to

act reasonably. The Directives and the Revision, according to the

claimants, are disproportionate and unreasonable and therefore do not

fall within the provision of section 36(1)(b) of the BFIA. The

Directive and Revision are disproportionate and unreasonable because

(i) the CBB could have achieved the purposes or objectives of the

Directives and Revision through consolidated supervision or

cooperation with FSC, rather than the draconian and unworkable

restrictions contained in the Directives and Revisions; (ii) because

BCBL was an affiliate of BBL under section 2(1) of the BFIA, the

CBB therefore had all the power necessary to retain adequate

regulatory supervision over BCBL and could have used those powers

to achieve its regulatory objective rather than issuing the Directives

and the Revision; and (iii) that there was no need for the Directives

and the Revisions to take effect immediately as is stated therein

because CBB was aware since 2009 that BCBL was no longer a

wholly owned subsidiary of BBL; and that BBL gave an undertaking

that there would be no inter company dealings between BBL and

BCBL and there was agreement that this would not change and that

would “be sufficient to meet any concern.”

47. In relation to (i) above on consolidated supervision with FSC, the

relationship between CBB and FSC had been terminated, and prior to

this the CBB had offered consolidated supervision but this offer,

40

according to the evidence, was not accepted. The MOU was a

mechanism for consolidated supervision of BCBL as a subsidiary of

BBL. But the MOU came to an end because of alleged behaviour of

FSC. The CBB made these points in a letter dated 6th

January, 2011

to FSC and copied to BBL as follows:

“Prior to the establishment of a subsidiary in the

Turks & Caicos Islands (TCI) by Belize Bank

Limited (BBL), the Central Bank of Belize (the

Central Bank) signed a Memorandum of

Understanding (MOU) with the TCI’s Financial

Service Commission (FSC), conforming that the

Central Bank will be responsible for conducting

consolidated supervision of BBL and its

subsidiary in TCI. The FSC without consultation

with the Central Bank approved a change in

ownership of British Caribbean Bank Limited

(BCBL) which resulted in BBL owning only

23% of BCBL.

Since the MOU was signed on the principle that

the bank in TCI was a wholly owned subsidiary

of BBL, the Central Bank can no longer conduct

consolidated supervision of BCBL since it is now

a minority interest of BBL. On 3 September

2010, the Central Bank attempted to resolve this

issue by requesting through BBL that the holding

company, BCB Holdings Limited and BCBL

voluntarily agree to consolidated supervision.

This offer has not been accepted by any of the

parties and BBL officially informed the Central

Bank that it is not in a position to compel BCBL

to accept. Consequently, and given your non-

response to our letter of 12 November 2009, by

this medium the Central Bank now confirms

effective termination of the MOU as per Section

11.1 with retroactive effect from that same date.”

41

Moreover, according to the Examination Report above dated 31st

March, 2010, BBL rejected consolidated supervision.

48. In relation to (ii) above, even assuming that CBB could have, under

the IBA, used those powers to regulate BCBL, this does not prevent

the CBB from exercising its wide and general discretionary power

under section 36(1) of the BFIA. In relation to (iii) above, there is,

once again no restriction under the BFIA preventing the CBB from

directing that the Directives and Revisions to take effect immediately,

and therefore it could not be unlawful that they should take effect

immediately, bearing in mind that they were issued to prevent parallel

banking, the problems of which have already been alluded to above.

The numerous letters between the CBB and BBL, some of which have

been considered above, show that there is distrust of, and a lack of

confidence on the part of both parties; and it is not unreasonable that

CBB did not rely on the alleged undertaking and agreement.

49. Mr. Guiseppi in his first affidavit at paragraph 20 (A) to (G) has

stated elaborately why the Directives are draconian and unworkable.

Briefly, the claimants say that the Directives and Revisions make no

financial sense and impossible for BBL to divest its shareholding in

BCBL, and this cannot be done immediately. As shown above, there

is evidence of the disadvantages of parallel banking which involve

risks to the financial position of the banks and risks to customers and

depositors of the banks involved. The evidence is that the Directives

were issued to avoid these disadvantages and risks. Moreover, the

Directives do not state that BBL to divest itself immediately of its

42

interest in BCBL, though the Directive comes into effect immediately.

The Directive states that BBL to “take immediate steps” to divest and

to reverse the transaction. In his seventh affidavit, Mr. Guiseppi

accepted that Directive 2 required steps for the reversal of the

“transaction” and did not therefore require the reversal to take place

immediately on the 9th

February, 2011, the date of the Directive, but

to be done on the 15th February, 2011 which Mr. Guiseppi submitted

was an impossible task. The Governor swore, on the other hand, that

the reversal could have been done in about three days between the 9th

February, 2011, the date the Directives were made, and 15th February,

2011 the date the exparte injunction was granted. I am therefore not

satisfied, on a balance of probabilities, that the reversal was an

“impossible task.”

50. The claimants say that the Directive 1 prohibits dealings with

shareholders of BCBHL and “that this is impossible to observe

because BCBHL is listed in several national stock exchanges in which

stocks are traded daily and consequently shareholders can also

changed daily.” Moreover, say the claimants, a large number of

shareholders in BCBHL hold accounts in BBL. It is to be noted that

Directive 1 at paragraph (iii) states that BBL and its subsidiary

BCBIL shall not, without written prior approval, conduct any

transactions with BCBHL. BCBIL’s licence at paragraph 4 makes a

similar prohibition. So the Directive and the licence leave the

possibility of approval from the CBB for some matters, and the

Directive states that the CBB on request may approve “small recurring

transactions at its discretion” and that CBB may “vary” the Directive.

43

So the Directive is not a blanket prohibition but does allow for

variation and the approval of some matters which BBL, if it requires,

may request, if it thinks terms of the Directive are impossible to

observe. Taking account of this, I am not satisfied that the Directive

is unreasonable.

51. The claimants then make the further submission that it is not viable

for BBL to have to make such a request, because it is “likely to create

a significant administrative burden.” The option of applying to vary

the Directive is available to the claimants, who should put systems in

place to ease the alleged administrative burdens. The assumption by

the claimants that it would have to wait a long time for a response

from CBB of any request is an assumption for which adequate reasons

have not been advanced. A request to the CBB for the payment of a

utility bill for instance, would, as was submitted, involve long

waiting; but I see no reason on the evidence why such a request

cannot be immediately responded to by CBB bearing in mind modern

communication facilities.

52. Paragraph (v) of the Directive 2 according to the claimants, are

unworkable and unreasonable because it would result in BBL and

BCBIL having to perform without their management personnel and

structure. The paragraph states that no member or officer of the

boards of Directors of the two banks is allowed to serve on the board

or management of BCBL. The Directive at paragraph (v) does not say

that no person being a director or officer of BBL and BCBIL is

allowed to serve on the board of BCBL. BCBL can obtain the

44

services of any person, other than the directors or officers of BBL or

BCBIL, aptly qualified to serve on its board or management. Though

the Directive comes into effect immediately it does not state that the

requirements of paragraph (v) thereof must be implemented

immediately. In addition, the Directive states, as we saw above, that

the CBB may vary any part of the Directive. If there is need for a

period of time to implement paragraph (v) a request by any of the

claimants to that effect can under the varying power above be

considered by the CBB who is required to respond on reasonable

grounds. I have found no evidence of such a request. There is

though, as was submitted, ambiguity in the phrase “related parties” as

appears paragraph (iii) in Directive 1. There is merit in this

submission; but this phrase, on request by BBL, could be explained by

a variation or amendment under provisions of the Directive.

(xi) Error of Law

53. It is further submitted by the claimants that the CBB erred in law and

exceeded its jurisdiction by relying on the Basel Committee on

Banking Supervision Guidelines (the Basel Guidelines) for purposes

of justifying the Directives and Revision, because the Basel

Guidelines have no force of law in Belize; and because their

provisions are not part of any statute or subsidiary legislation in

Belize. The claimants do not object to the admissibility of the Basel

Guidelines. In fact, they submitted, as we saw above, that the

document can be used as guidance. I do not see that the document

must be grounded on legislation before it can be considered by CBB

45

in the exercise of its discretion under section 36(1) of the BFIA. Even

if, say the claimants, the CBB could properly rely on the Basel

Guidelines, the guidelines provide for close cooperation between

regulators; and the CBB erred in not seeking to resolve this matter

through close cooperation with the FSC. The claimants accept that a

public body can consider relevant policy and guidance, but they

submit that CBB in this case considered that it was required by the

Basel Guidelines to issue the Directives. The first affidavit of

Glenford Ysaguirre at paragraph 12 says as follows:

“The Central Bank carefully considered the

representations made by the claimants at the

meeting on 17th

January 2011. The rejection by

the BCB Holdings Limited (BCBHL) group, in

particular BCBL, of the Central Bank’s proposed

solution of consolidated supervision effectively

eliminated any chance of establishing a

satisfactory supervisory regime for the group.

Under these circumstances, and in the best interest

of the domestic banking system, the stability of

BBL, and in consequence its depositors and

creditors, the Central Bank felt that international

standards as laid out by the Basel Committee on

Banking Supervision required that the Central

Bank direct BBL to immediately divest from

BCBL and ring-fence both BBL and its subsidiary

British Caribbean Bank International Limited

(BCBlL) from activated with BCBL. These

considerations contributed to the decision to

formulate Directive 1.”

46

54. By considering that the Basel Guidelines required CBB to direct BBL

“to immediately divest from BCBL …” CBB, according to the

claimants, unlawfully exercised its power under section 36(1) of BFIA

since the Basel Guidelines made no such requirement. An

examination of the Basel Guidelines shows that it “sets out

supervisory guidance for dealing with parallel banks”: see page 1 of

the document. The claimants therefore submitted that “guidance”

should not be treated as automatically determining the outcome of a

particular case: it should not be interpreted as meaning required, as

Mr. Ysaguirre felt it did.

55. The claimants in support of this submission relied on Laker Airways

Limited v. Department of Trade 1977 QBD 643 where the court had

to consider a White Paper headed “Future Civic Aviation Policy

CCMND 6400” which got parliamentary approval under section 3(2)

& (3) of the Civil Aviation Authority Act 1971 (UK), and was

presented by the Secretary of State to the UK Parliament. The White

Paper had two parts, one of which was headed “Guidance.”

Paragraph 7 of the “Guidance” constituted in effect an instruction to

the Civil Aviation Authority established by the 1971 Act to eliminate

competition with the State owned airlines; which in effect was a

reversal of previous policy under which competition was allowed; and

to revoke a licence previously granted to the claimant under that

previous policy to operate an air passenger service known as Skytrain

between London and New York for which the claimant had incurred

huge capital expenditure. The claimant brought an action for

declarations that the “Guidance” was ultra vires the Act; and that the

47

licence ought not to have been revoked. The court held that though

the Secretary of State was entitled to reverse the previous policy by

legislation amending the Civil Aviation Act 1971, he had acted

beyond his powers in formulating the “Guidance” because any

guidance under section 3(2) of the Act had to be consistent with the

Act or be done by an amendment to the Act;, and as there was no

amendment, and the guidance was inconsistent with the objectives of

the Act, the claimant was entitled to the declaration. Lord Denning

gives the reasons for the decision: “ … the White Paper cannot be

regarded as giving “guidance” at all. In marching terms, it does not

say “right incline” or “left incline.” It says “right about turn.” That is

not guidance, but the reverse of it … . I am afraid that he (the

Secretary of State) went about it the wrong way. Seeing that the old

policy had been laid down in an Act of Parliament then, in order to

reverse it, he should have introduced an amending Bill and got

Parliament to sanction it. He was advised apparently, that it was not

necessary and that it could be done by “guidance.” That I think was a

mistake. . . . It was in this respect ultra vires …” The principles

concerning guidance in the White Paper were ultra vires the Act

because for the guidance to be effective, it had to be done by an

amending Act, and not a White Paper.

56. In this case before me, the “Guidance” of the Basel Guidelines has not

been shown to be ultra vires the BFIA or any Act and therefore the

CBB is entitled to consider it in the exercise of its discretion under

section 36(1) of the BFIA. It may be considered as unfortunate that