in this issue pe investors see robust m&a activity ahead & interactive services . . . . . ....

TRANSCRIPT

The Jordan, Edmiston Group, Inc. (JEGI)offered a select group of private equity execu-tives that invest in the media, information,marketing services and technology sectors theopportunity to provide their keen insights onthe current state of their funds’ investmentactivities and their outlook on the market:

1. What key market forces will impact yourinvestment activities into 2013? How activedo you anticipate being in M&A over the next12-18 months?

2. In which market sectors within media,information, marketing services and technolo-gy are you looking to invest and why?

3. What is your view of the debt market todayand over the next 6-9 months? How is itaffecting transactions and multiples? For yourtransactions, what is your optimal mix of equi-ty, senior and mezzanine debt?

Here are their responses:

Andy Davis, Managing DirectorBV Investment [email protected]

We anticipate M&A activity to be quite robustover the next 12-18 months. This year, BV ison track to have 6-8 realizations, mostly tostrategic acquirers. We continue to find highgrowth, attractive companies in informationservices and communications, as these areasare growing much faster than the economy,due to long-term secular growth trends.

Over the past decade, the firm has primarilyinvested in high growth, mission critical,information services companies. BV takes athesis-driven approach to investing in higher-than-average growth segments of the economy,within the information sector.

Despite dramatic improvement since 2008,debt markets are still very discriminating; weexpect the debt markets to remain open tocredit worthy buyers. We focus on creatingvalue through growing earnings, so don’t typi-cally try to maximize the leverage on our deals.We keep the balance sheets of our portfoliocompanies relatively simple.

Walter Florence, Managing DirectorFrontenac [email protected]

In the past two years, Frontenac has bought sixnew platform companies and has sold sevenportfolio companies, and we see that momen-tum continuing into 2012. As a firm, we arestill focused on investing behind strong man-agement teams that see an opportunity tobuild a market leading company; we call it“CEO1st” investing. We have also beenuniquely focused on the family and founder-owned business market, with over 220 suchtransactions completed. If the economy con-tinues to slowly strengthen, or even holds, dealflow should continue to grow, with the help ofstrong debt markets.

(continued on page 6)

PE Investors See Robust M&A Activity Ahead

July 2012 Independent Investment Banking for Media, Information, Marketing Services & Technology

In This Issue...PE Investors See Robust M&A ActivityAhead . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Active M&A Market Continues, Led byMarketing & Interactive Services . . . . . . .1

Digital M&A at the Event Horizon . . . . . .4

SIIA Strategic & Financial InvestmentConference . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Exceptional Transaction Experience . . . .8

Mergers and acquisitions in the media, information, marketing services and tech-nology sectors continued at a fast clip in the first half of 2012, as the number ofdeals rose 52% over 2011 levels. Announced transaction value increased 49% tonearly $32 billion, primarily due to a few multi-billion dollar transactions, withthe balance of market activity centered around mid-sized transactions.

Overall, acquirers have been focusing on smaller, complementary acquisitions,with nearly 95% of transactions in 1H 2012 at values of less than $100 million.Only five deals exceeded $1 billion in value, including Alibaba Group’s pendingacquisition of 20% of its shares from Yahoo for $7.1 billion, and the $3.3 billionbuy-out of TransUnion by Advent International and Goldman Sachs.

(continued on page 2)

To subscribe to JEGI’s Client Briefing Newsletter: http://tiny.cc/JEGI_Client_Briefing

JEGI hosted its first Emerging Company Dinner of2012 on May 17th at the 21 Club in New York City.

Follow JEGI on Twitter:http://twitter.com/JordanEdmiston

Active M&A Market Continues, Led by Marketing& Interactive Services

$70

$60

$50

$40

$30

$20

$10

0

700

600

500

400

300

200

100

0

($ b

illio

ns)

1h 2005

1h 2006

1h 2007

1h 2008

1h 2009

1h 2011

1h 2012

1h 2010

First Half M&A Transactions and Value

value transactions

652

292

$5.3

source: jegi transaction database

$31.7

$27.9

280$42.7

355397

$65.8

426

$22.5 $20.3

471 430

$21.2

(From left) Lance Maerov, SVP, CorporateDevelopment, WPP; Wilma Jordan, CEO, JEGI;Tolman Geffs, Co-President, JEGI; Matthew Egol,Partner, Media & Entertainment, Booz & Co.; andRandall Rothenberg, President & CEO, IAB

(From left) Brian Keil, VP, Strategy & BusinessDevelopment, Arbitron; Henrique De Castro,President, Global Media, Mobile & Platforms,Google; and Kurt Abrahamson, CEO, ShareThis

2 JEGI Client Briefing – July 2012

The majority of the deal activity in the first halfof 2012 took place across the interactive, mar-keting services and technology markets. B2Band B2C Online Media & Technology,Marketing & Interactive Services, and MobileMedia & Technology accounted for 79% oftotal deals and 75% of deal value for the period.

Marketing & Interactive Services

There are clashing forces in the marketplace.On the one hand, there is the uncertainty cre-ated by such factors as historically high unem-ployment rates and low consumer confidence,the Eurozone challenges in Greece, Spain andelsewhere, as well as poorly performing bell-wether stocks and post-IPO hangover (e.g.,Zynga, Facebook, etc.). At the same time,unprecedented waves of change and innovationare creating new opportunities in the market.The explosive growth of social media – the“Socialization of Everything” – is transformingwhole industries, such as entertainment, news,e-commerce, and gaming. Large brands arequickly trying to adapt and are shifting dollarsto interactive media and below the line market-ing (i.e., customer-centric communications,typically with measurable results). As a result,Internet advertising spending for Q1 2012 seta new record at $8.4 billion, according to theInteractive Advertising Bureau (IAB). “Moreonline consumers than ever are taking to theInternet to inform and navigate their daily lives– by desktop, tablet or smartphone,” saidRandall Rothenberg, President and CEO, IAB.“Marketers and agencies are clearly – and wise-ly – investing dollars to reach digitally connect-ed consumers.”

At the same time, mobile is exploding.Smartphone sales have surpassed PC sales, and,according to StatCounter, mobile trafficaccounted for 10% of Internet traffic in May2012 vs. less than 1% in December 2009.According to eMarketer, mobile ad spend willreach $10.8 billion in 2016, up from $2.6 bil-

lion in 2012 and representing a CAGR of43%. There is a secular evolution at hand,and marketing dollars continue to rapidlyfollow consumers. Media consumptioncontinues to shift to the Internet, and nowto mobile, moving away from traditionalmedia. On average, consumers are spend-ing 26% of their media time online and10% of their media time with mobile,according to Kleiner Perkins partner MaryMeeker’s annual overview of Internettrends. Digital ad spending has started tocatch-up with time spent online, with22% of ad dollars flowing to the web.However, the gap is still significant withmobile, as it captures only 1% of ad dol-lars. According to Meeker, closing the gapbetween share of time spent online/onmobile and share of advertising dollarsspent online/on mobile represents a $20billion annual advertising opportunity inthe US and points to the continuing move-ment of ad dollars to digital media in the yearsahead.

As a result, companies are investing in market-ing services to better assist their customers andcapture more revenue. Advertising agenciesand marketing services companies are retoolingtheir business models by investing in integrat-ed and interactive marketing solutions, such asExperian’s acquisition of Conversen, a pioneerin developing interaction management tech-nologies, enabling cross-channel conversations(JEGI represented Conversen in this deal).According to Doug Bacon, Director, CorporateDevelopment, Experian, “We see Conversen asa bridge between our digital and traditionalofferings. The concept of consistent messagingto the consumer, regardless of channel, is criti-cal to marketing success. This acquisitionbecomes the glue that puts it all together andprovides us with a platform to tie together ourmarket leading products into a single point ofentry for our clients.”

Large technology companies, such as IBM,Oracle, Adobe and others, are also aggressivelyinvesting in marketing technology solutions tohelp marketers create value from their data andprovide customers with key business intelli-gence and analytics, to drive better customerexperiences and enhance customer engage-ment. Oracle’s $300 million acquisition ofVitrue, which enables companies to managetheir presence on social networks, clearly high-lights this point. These trends have madeMarketing & Interactive Services by far themost active sector for M&A, accounting for40% of all transactions and 27% of total valuein 1H 2012.

Areas of Focus for Marketing & InteractiveServices M&A In the first half of 2012, the adagency and digital agency sub-sectors were themost active within Marketing & InteractiveServices, accounting for a combined 34% ofdeal volume and 26% of deal value. Marketingtechnology and market research/consultingwere the next most active sub-sectors, eachaccounting for 16% and 15%, respectively, ofdeal volume for the half year. Other active sub-sectors for M&A included data & analytics (17deals), PR agency (12 deals), ad technology (13deals), and monitoring & intelligence (11 deals).

Drivers of M&A Value The Marketing &Interactive Services sector saw only one $1+billion transaction in the first half of 2012 –Microsoft’s acquisition of Yammer, a providerof social networking portals for enterprises, for$1.2 billion. However, there were two $500+million deals and seven more with values of$200 million and higher. The marketing tech-nology sub-sector accounted for 37% ofMarketing & Interactive Services deal value,led by Salesforce.com’s acquisition of BuddyMedia, which helps companies manage acrosssocial media platforms, for $745 million. Other

Active M&A Market Continues, Led by Marketing & Interactive Services (cont. from p. 1)

3JEGI Client Briefing – July 2012

Business-to-Business Media 8 23

2012 2011

Value ($MM)

% Change

B2B Online Media & Technology

Exhibitions & Conferences

Consumer Magazines

Database & Information Services

B2C Online Media & Technology

Education Information, Technology & Training

39

11

16

21

130

32

3,056

165

2,020

3,064

4,554

1,272

75% 266%

21%

164%

69%

71%

2%

(3%)

160%

165%

(94%)

103%

(7%)

(9%)

14 82

47

29

27

36

133

31

7,932

437

122

6,205

1,153

Media, Information, Marketing Services & Technology M&A Activity

No. of Deals Value ($MM) No. of Deals ValueJanuary -June January - June

Industry Sector

Total 430 $21,236 52% 49%652 $31,658

Marketing & Interactive Services 129 5,740 103% 51%262 8,677

No. of Deals

Mobile Media & Technology 44 1,345 66% 109%73 2,808

4,242

marketing technology deals making the top 10in 1H 2012 included the Intuit acquisition ofDemandforce, a SaaS application that auto-mates Internet marketing and communica-tions, for $424 million and Oracle’s acquisitionof Vitrue for $300 million.

Ad and digital agencies combined accountedfor $2.2 billion of deal value in 1H 2012, ledby WPP’s acquisition of digital agency AKQAfrom General Atlantic for $540 million.Market research and consulting was next,accounting for 12% of deal value, includingthe acquisition by Genstar Capital of eResearchTechnology, a provider of health outcomesresearch services, for $377 million. The chartbelow shows the top 10 Marketing &Interactive Services deals by value in the firsthalf of 2012.

The “New Normal” At the SIIA Strategic &Financial Investment Conference on June 21 inNYC, JEGI Co-Presidents, Tolman Geffs andScott Peters, provided the opening keynotepresentation for more than 200 M&A focusedstrategic executives and private equityinvestors. This insightful session described theconfluence of global uncertainty with theforces of rapid technological change as the“New Normal”, leading to interesting businesscombinations via M&A activity. Examplesinclude several deals highlighted above, includ-ing Experian/Conversen, Oracle/Vitrue andSalesforce.com/Buddy Media, as well as theAmazon acquisition of Kiva Systems, whichmakes robots used in shipping centers to simpli-fy operations and reduce costs, and the acquisi-tion by Facebook of Instagram, which providesFacebook users with a compelling experiencefor photo sharing, for $1 billion. Companies,possibly more than ever, are focusing on servic-ing their customers, and we expect to see moreinteresting combinations via M&A in the yearsto come. The complete presentation is availableat: http://tiny.cc/SIIA_Presentation.

M&A Highlights for 1H 2011• The b2b online media and technology sec-tor saw a 21% rise in the number of M&Atransactions announced in 1H 2012 vs. 1H2011 and a 160% increase in deal value to$7.9 billion, led by the pending AlibabaGroup/Yahoo deal. Other notable Q2 transac-tions included the IHS acquisition ofGlobalspec, a b2b lead gen provider connect-ing industrial marketers with their target audi-ences in engineering, technical and industrialmarkets; the acquisition by LinkedIn ofSlideShare, a professional content sharing plat-form, for $119 million; and Norwest VenturePartners’ acquisition of a 49% stake in Manta,a web site for business listings serving the localmarket, for $44 million.

• The b2c online media and technology sec-tor was the second most active in the first halfof 2012, with 133 transactions at a total valueof $4.2 billion – very similar results to the firsthalf of 2011. The largest deal of the half wasthe acquisition by Cerberus CapitalManagement of 53% of AT&T’s AdvertisingSolutions business, which comprises a combi-nation of print and online yellow page listings,for $950 million in April. Other notable Q2deals included Axel Springer’s acquisition ofTotaljobs, an online recruiting platform, fromReed Elsevier for $176 million; YbrantDigital’s acquisition of online shopping com-parison sites PriceGrabber, Classes USA andLowerMyBills from Experian for $175 mil-lion; and the acquisition by Cox Target Mediaof Savings.com, an online source for savings,personalized deals and money-savings experts,for $100 million.

•M&A activity for the business-to-businessmedia sector continues to be relatively quiet,with only 14 deals in the first half of 2012, fora total value of $82 million. In Q2, QuestexMedia sold its b2b industrial and specialty

publications to North Coast Media; and BobitBusiness Media acquired b2b media assets forthe trucking industry from Newport BusinessMedia.

• The consumer magazine sector has beenuneventful in the first half of 2012, with 27deals at a total value of $122 million, a sharpcontrast to the first half of 2011, which sawseveral multi-hundred million dollar deals,including the acquisition by HearstCorporation of Lagardère’s magazine portfoliofor $651 million.

• The database and information servicessector picked up considerably in the first halfof 2012, led by the PE buy-out of TransUnionin Q1; and two transactions in Q2 – VeritasCapital’s acquisition of Thomson Reuters’Healthcare business, a provider of healthcaredata and analytics, for $1.25 billion; andPiramal Healthcare’s acquisition of DecisionResources, a provider of healthcare data,research and consulting, from ProvidenceEquity Partners for $635 million. Othernotable Q2 deals included the R.R. Donnelleyacquisition of Edgar Online, a distributor offinancial data and public filings, for $67 mil-lion; and Markit’s acquisition of DataExplorers, a provider of global securities lend-ing data.

• The education information, technologyand training sector saw a similar number ofdeals and value in the first half of 2012, com-pared to the first half of 2011. The mostnotable deal of Q2 was the acquisition byPLATO Learning of Archipelago Learning, aSaaS provider of supplemental educationproducts, for $301 million. Pearson contin-ued to be very acquisitive in the education sec-tor, with two acquisitions in May –GlobalEnglish, which offers on-demand enter-prise solutions for advancing Enterprise

(continued on page 5)

4 JEGI Client Briefing – July 2012

Digital M&A at the Event Horizon

By David Clark, Managing Director, JEGI, [email protected] the backdrop of a challenged global economy, growth in digitalmedia spending continues uninterrupted. The rate of growth is impres-sive – 2006-2011 CAGR of 13% and expected CAGR of 15% for 2011-2016.No other sector of the economy has grown, or is expected to grow at thisrate, which is 5X the growth rate of US GDP.

The forces at work in the sector are powerful and continue to com-pound. Smart phone penetration of 50+% at home and in the work-place. Approximately 15% YoY growth in ecommerce. Rapid proliferationof tablet, app and emedia platforms. And accelerating growth in brandmarketer spending in online video and social media.These mutually reinforcing market drivers call to mind the concept of“event horizon”. In physics, an event horizon is the point at which anobject becomes so large – black holes are the best example – that nonearby matter can escape its gravitational field. The size of the digitalsector (media + services + infrastructure) has reached this level of scale.And the impact is so far-reaching that companies well outside of thecore “ad tech” sector are feeling the pull. To be sure, search marketing and online display advertising, the truework horses of ad tech, have already sailed past the event horizon. Everyconceivable publishing, lead gen, response marketing and ecommercemodel has been permanently re-shaped by search and online display.

M&A transactions have played a significant role in re-shaping the adtech landscape. In the past five years alone, JEGI has tracked approxi-mately $83 billion of online media and interactive marketing transac-tions. And ad tech M&A is not yet done. With well over $1 billion of ven-ture capital invested in the extremely crowded ad network, DSP andreal-time bidding category (and with the IPO market likely shut for awhile to come), consolidation needs to occur. True differentiation in theDSP category is low, marketing “noise” is high, and the large mediaagencies have created their own competing trading desks. As a result,some of the largest, best funded independent companies in the ad techsector will likely pursue M&A as an alternative, if not preferred exit. Itwill be interesting to see how sizable investments in the DSP/RTB cate-gory get realized.

Equally interesting to observe are the new “industry” participants fromoutside the ad tech sector that are getting pulled closer to the digitalevent horizon. In terms of M&A activity, what we’re seeing is ad techM&A giving way to “marketing technology” M&A. There is a notablecooling down of M&A in the ad tech categories of search and displayservices and tools, while M&A activity has heated up in marketing infra-structure, particularly for technology solutions that address the needsof global brand marketers and premium publishers (including ecom-merce brands that operate as marketer and publisher alike). In a recentForbes article, Randall Rothenberg stated that “Marketing for large com-panies is fundamentally an industrial process. They depend on scale.”No surprise, then, to see companies like IBM looking over the horizonand seeing the large opportunity in enterprise marketing systems, andthen rapidly assembling an enterprise marketing “technology stack” viavery aggressive M&A. From 2010 to 2012 alone, IBM invested over $3 bil-lion directly pointed at enterprise marketing management.

Here’s why. According to a new survey by the CMO Council, 80% of 200global marketing executives confirmed that “digital marketing” is astrategic agenda item with strong corporate support. Meanwhile, overa third of these executives admitted that their digital models were littlemore than a collection of poorly integrated, tactical point solutions.Along those lines, IBM’s “State of Marketing 2012” report revealed thatmore than seven out of 10 respondents to its survey said that theybelieve integration is important across owned, earned and paid chan-nels, while less than three out of 10 were effectively integrating thosedifferent channels.

SIIA Strategic & Financial Investment ConferenceThe 2012 SIIA Strategic & Financial Investment Conference was a bigsuccess. More than 20 presenting companies from across digital media,data/information, SaaS/software and marketing technology sharedtheir stories with nearly 250 strategic M&A-focused executives andfinancial sponsors. This sold out event, which was co-founded by spon-sors JEGI and Veronis Suhler Stevenson, was held at the Princeton Clubin NYC on June 21. The audience comprised executives from a strong mix of global compa-nies and private equity firms, including Aegis Media, American Express,Arvato, Bloomberg, BV Investment Partners, Catalyst Investors, CengageLearning, Cognizant, DMG Information, Dow Jones, Dun & Bradstreet,Equifax, Frontenac, Gartner, GE Capital, Interpublic Group of Companies,Leeds Equity, LexisNexis, McGraw-Hill, MidOcean Partners, News Corp,Nielsen, Oaktree Capital, Riverside Company, Spire Capital, SummitPartners, Thomson Reuters, Wicks Group, Wolters Kluwer, WPP, andmany others. JEGI Co-Presidents Tolman Geffs and Scott Peters keynote presentationtitled “The End of The World As We Know It: Innovation & Growth inDigital Services” provided an insightful view on the “New Normal”.While there is much uncertainty in the world, there are also excitingwaves of innovation, leading to interesting combinations via M&A. Thecomplete presentation is available at: http://tiny.cc/SIIA_Presentation. Speaking of M&A, while presenting companies varied in terms of sizeand lifecycle stage, they are each actively seeking a 'next stage' oppor-

tunity, which could include an add-on acquisition, a strategic partner-ship, a round of investment, or an exit. See the chart below for the com-plete set of presenting companies and be sure to hold June 13, 2013 onyour calendar for next year’s conference. ■

2012 Presenting Companies

saas

/sof

twar

e

data

mar

keti

ng

tech

nol

ogy

med

ia

ting Cesen2012 Pr ompaniesting C

are

s/so

ftw

ompaniesting C

aatd

s/so

ftw

aasy

ogogn

olte

chn

g ar

keti

dia

me

arke

tim

5JEGI Client Briefing – July 2012

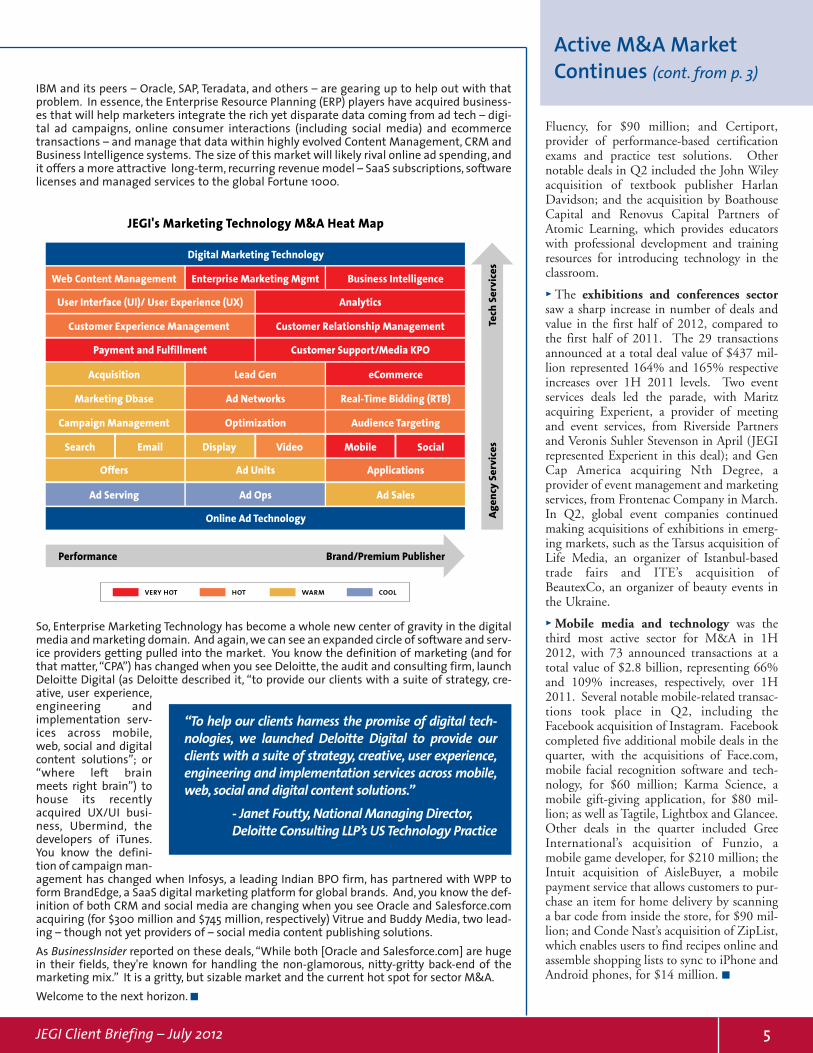

IBM and its peers – Oracle, SAP, Teradata, and others – are gearing up to help out with thatproblem. In essence, the Enterprise Resource Planning (ERP) players have acquired business-es that will help marketers integrate the rich yet disparate data coming from ad tech – digi-tal ad campaigns, online consumer interactions (including social media) and ecommercetransactions – and manage that data within highly evolved Content Management, CRM andBusiness Intelligence systems. The size of this market will likely rival online ad spending, andit offers a more attractive long-term, recurring revenue model – SaaS subscriptions, softwarelicenses and managed services to the global Fortune 1000.

So, Enterprise Marketing Technology has become a whole new center of gravity in the digitalmedia and marketing domain. And again, we can see an expanded circle of software and serv-ice providers getting pulled into the market. You know the definition of marketing (and forthat matter, “CPA”) has changed when you see Deloitte, the audit and consulting firm, launchDeloitte Digital (as Deloitte described it, “to provide our clients with a suite of strategy, cre-ative, user experience,engineering andimplementation serv-ices across mobile,web, social and digitalcontent solutions”; or“where left brainmeets right brain”) tohouse its recentlyacquired UX/UI busi-ness, Ubermind, thedevelopers of iTunes.You know the defini-tion of campaign man-agement has changed when Infosys, a leading Indian BPO firm, has partnered with WPP toform BrandEdge, a SaaS digital marketing platform for global brands. And, you know the def-inition of both CRM and social media are changing when you see Oracle and Salesforce.comacquiring (for $300 million and $745 million, respectively) Vitrue and Buddy Media, two lead-ing – though not yet providers of – social media content publishing solutions. As BusinessInsider reported on these deals, “While both [Oracle and Salesforce.com] are hugein their fields, they're known for handling the non-glamorous, nitty-gritty back-end of themarketing mix.” It is a gritty, but sizable market and the current hot spot for sector M&A.Welcome to the next horizon. ■

JEGI's Marketing Technology M&A Heat Map

Digital Marketing Technology

User Interface (UI)/ User Experience (UX)

Web Content Management Enterprise Marketing Mgmt Business Intelligence

Online Ad Technology

Customer Experience Management

Payment and Fulfillment

Analytics

Customer Relationship Management

Customer Support/Media KPO

Acquisition Lead Gen eCommerce

Marketing Dbase Ad Networks Real-Time Bidding (RTB)

Campaign Management Optimization Audience Targeting

Offers Ad Units Applications

Ad Serving

Performance

Ad Ops Ad Sales

Search Email Display Video Mobile Social

very hot hot warm cool

Brand/Premium Publisher

Tech

Ser

vice

sAg

ency

Ser

vice

s

Fluency, for $90 million; and Certiport,provider of performance-based certificationexams and practice test solutions. Othernotable deals in Q2 included the John Wileyacquisition of textbook publisher HarlanDavidson; and the acquisition by BoathouseCapital and Renovus Capital Partners ofAtomic Learning, which provides educatorswith professional development and trainingresources for introducing technology in theclassroom.

• The exhibitions and conferences sectorsaw a sharp increase in number of deals andvalue in the first half of 2012, compared tothe first half of 2011. The 29 transactionsannounced at a total deal value of $437 mil-lion represented 164% and 165% respectiveincreases over 1H 2011 levels. Two eventservices deals led the parade, with Maritzacquiring Experient, a provider of meetingand event services, from Riverside Partnersand Veronis Suhler Stevenson in April (JEGIrepresented Experient in this deal); and GenCap America acquiring Nth Degree, aprovider of event management and marketingservices, from Frontenac Company in March.In Q2, global event companies continuedmaking acquisitions of exhibitions in emerg-ing markets, such as the Tarsus acquisition ofLife Media, an organizer of Istanbul-basedtrade fairs and ITE’s acquisition ofBeautexCo, an organizer of beauty events inthe Ukraine.

•Mobile media and technology was thethird most active sector for M&A in 1H2012, with 73 announced transactions at atotal value of $2.8 billion, representing 66%and 109% increases, respectively, over 1H2011. Several notable mobile-related transac-tions took place in Q2, including theFacebook acquisition of Instagram. Facebookcompleted five additional mobile deals in thequarter, with the acquisitions of Face.com,mobile facial recognition software and tech-nology, for $60 million; Karma Science, amobile gift-giving application, for $80 mil-lion; as well as Tagtile, Lightbox and Glancee.Other deals in the quarter included GreeInternational’s acquisition of Funzio, amobile game developer, for $210 million; theIntuit acquisition of AisleBuyer, a mobilepayment service that allows customers to pur-chase an item for home delivery by scanninga bar code from inside the store, for $90 mil-lion; and Conde Nast’s acquisition of ZipList,which enables users to find recipes online andassemble shopping lists to sync to iPhone andAndroid phones, for $14 million. ■

Active M&A MarketContinues (cont. from p. 3)

“To help our clients harness the promise of digital tech-nologies, we launched Deloitte Digital to provide ourclients with a suite of strategy, creative, user experience,engineering and implementation services across mobile,web, social and digital content solutions.”

- Janet Foutty, National Managing Director, Deloitte Consulting LLP’s US Technology Practice

6 JEGI Client Briefing – July 2012

We have long focused on business services asan attractive area for investment. Meeting thecompetitive needs of enterprise customerstoday requires best-in-class, cost-effective solu-tions, often delivered by businesses specializingin a specific functional process or vertical mar-ket, or both. This is especially true in theinformation, marketing services and technolo-gy sectors.

The debt markets are strong, but not across allsectors. There is a clear thirst for yield intoday’s low interest rate environment. In myview, the rally in the credit markets stems fromthe search for higher yields, helped by a stabi-lizing and strengthening economy. Strongdebt markets drive the M&A markets andmultiples. Size of deals is another real consid-eration for multiples and optimal capital struc-tures. Bigger companies appeal to morelenders. At the lower end of the market, 2.5xto 3x is still the prevailing leverage range. Atthe higher end, there are deals above 6x. It alldepends on the strength of the credit.

Stewart Kohl, Co-CEORiverside [email protected]

We’re seeing a lot of activity in our deal pipeline,thanks to our global Origination team. A num-ber of factors are driving the uptick in activity,and multiples remain high for top-quality com-panies after the difficult period of 2009 and2010. Meanwhile, strategic and financial buyersare eager to put money to work in a low interestrate environment and in advance of a cyclical

recovery. Some private equity buyers are tryingto use funds before the expiration of their invest-ment periods. Many buyers sat on capital forthe past few years, and there is a need to investin quality businesses. Some sellers are motivat-ed to sell before potential tax law changes. Andfinally, despite macroeconomic uncertainty,some lenders also have strong incentives to lendmoney, and they’re hungry to get deals done.

Jeff Stevenson, Managing PartnerVeronis Suhler [email protected]

The increased availability of credit and theexpiring investment periods of many privateequity funds have been key drivers of the recentincrease in middle market M&A activity and

valuation multiples. A continued weakening ofthe European banking system and threats ofexit or insolvency from a variety of Euro coun-tries are the events most likely to impact USmiddle market investing.

VSS is primarily focused on Business andInformation Services, SaaS and Educationcompanies with a portion of recurring revenuefor new platform investments. We are activelylooking for add-ons for a majority of our plat-form companies.

The current debt market in the US is moreactive with senior debt multiples as high as5.5x-6x for businesses with more than $35 mil-lion of EBITDA and 4x-4.5x for less than $25million of EBITDA. We do not expect theEuro crisis to significantly impact the US bank-ing sector and believe leverage multiples willremain at current levels. Clearly, the moreaggressive approach by lenders has forced trans-action multiples higher and incentivized com-panies to seek a sale. We aim to keep a conser-vative capital structure with approximately 2x-4x senior leverage, 1x-2x mezzanine and 40-50% equity.

Dan Kortick, Managing PartnerWicks [email protected]

The economy continues under generallyimproving conditions. Different sectors andspecific niches within those sectors are reactingto this recovery in varying degrees. Many fastgrowing segments have already achieved and/orexceeded pre-recession benchmarks. Wicksintends to remain an active investor in nichesegments where recovery growth rates exceedthat of GDP.

Tax strategies and planning are also a marketforce that will drive M&A for the remainder of2012. With the prospect of changes to capitalgains and gift tax exemptions, entrepreneur-and family-owned businesses are prudentlyplanning and may take advantage of a liquidityevent this year.

The debt markets appear to be open, but notaggressively so, for platform companies in oursize range ($5-$15 million EBITDA). We areencouraged by seeing more traditional banks re-entering this part of the lower middle market,and they are focused on quality transactions. Inthe lower middle market, senior debt levels are

not typically greater than 50% of the capitalstructure, and senior leverage multiples are inthe 3.5x-4.5x range.

Peggy Koenig, Managing Partner & Co-CEOJohn Hunt, Partner/Head of Sr. Equity Funds ABRY [email protected], [email protected]

We closely monitor macroeconomic issues thatcould disrupt the US M&A market. Any oneof several factors could impact investmentactivity and the M&A market over the next 12-18 months.

We continue to be active in buying and sellingcompanies. On the private equity side, we havea number of sale processes underway, whilepursuing both new platform companies andfollow on acquisitions for existing platforms.On the senior equity side, we continue to enjoytailwinds in committing new capital to smallergrowth-oriented companies in the middle mar-ket. We expect this environment to continue,as the lending environment for such firms hasnot recovered in the way that the larger middlemarket has.

We remain very active investors in sub-sectorsbenefiting from broadband proliferation. Weare buying and selling data center companies, aswell as telecom related businesses that are real-izing the benefits of these trends. We also areactively investing in information businesses anda myriad of business processing outsourcingcompanies.

The debt markets are volatile and have been forquite a while. We opportunistically tap thedebt markets for existing portfolio companies.Debt capital is available to us from the lenderswith whom we have done business for manyyears. Interest rates are still low, and we canattract financing on relatively positive terms.The sub-sector we are investing in will dictatethe mix of equity, senior and mezzanine debt.

Sean White, PartnerSpire Capital [email protected] is a significant amount of equity capitalseeking good investments. This has created arobust seller slanted environment. Potential taxchanges will be impactful as well. We haverecently sold two businesses and will probablysell more. I would also anticipate several newinvestments over this time period as well.

PE Investors See Robust M&A Activity Ahead (cont. from p. 1)

“...we continue to enjoy tailwindsin committing new capital tosmaller growth-oriented compa-nies in the middle market.”

“The increased availability ofcredit and the expiring invest-ment periods of many privateequity funds have been keydrivers of the recent increase inmiddle market M&A activity.”

“...strategic and financial buyersare eager to put money to workin a low interest rate environ-ment and in advance of a cyclicalrecovery.”

Our focus is on the information and technologysectors, because we see a better relationshipbetween valuations and growth in these marketsegments. Said differently, valuations are morecompelling in these sectors for us. We are con-sidering both.

The debt markets are currently favorable from apricing and availability perspective. Valuationmultiples are a bit higher due to the currentavailability of debt financing. We prefer 60/40debt to equity.

Sam Levine, Managing DirectorEos Partners [email protected]

We view the economy with caution and arebeing conservative regarding capital structure.We will be aggressive, but avoid overleveragingthe balance sheets of companies. During thispast recession, we bought the debt of six com-panies overleveraged during good times. Weturned debt into equity by purchasing seniordebt at huge discounts and driving a restruc-turing process. Today, those companies areachieving strong growth.

Given the current uncertainty, we are makingprivate equity investments with modest lever-age and some type of preferred equity that ishigher up in the cap structure. Over the past13 months, we have made seven new platforminvestments, many with entrepreneurs whoare not ready to seek a full exit but still wantan equity partner to either provide partial liq-uidity and/or some growth capital. In caseswhere our target has limited organic growthprospects, we can make accretive acquisitionsof smaller tuck-ins. Both organic growth andacquisition scenarios can generate attractiveprivate equity returns without using full mar-ket leverage.

We continue to see some interesting opportu-nities with companies transitioning from printto digital and also in niche data driven tradeshow/conference driven business models.Having great data is a key foundation to driv-ing growth.

Within the B2B media space, we are lookingat companies that have depth within one (or alimited number) of verticals. Companies needto focus on deep vs. wide so they can capturethe mindshare of their customers. We are alsolooking at a number of events/trade showbusinesses with high market share. Tradeshows aren’t going away.

As for marketing/media services, digital mediagrowth has slowed but is still growing at a high-er rate than other channels. There is increasedcommoditization and competition within thedigital realm, and many digital agencies havehad a hard time scaling, given the labor intensi-ty relative to traditional mass media.

We generally don’t put max leverage on thebalance sheets of companies we invest in andusually avoid mezzanine debt. Instead, wefocus on companies led by entrepreneurs whodon’t want to fully lever their companies, fear-ing that max leverage will prevent them frompursuing an aggressive growth strategy.

Mark Colodny, Managing Director Warburg Pincus [email protected]

We expect deal activity to continue to bestrong for a variety of reasons:

For corporations:

• Corporations can be very conservativebuyers when the economy is poor and theyare going through cost cutting exercises;but when profits are stronger, as they arenow, corporations tend to get more confi-dent as buyers.

• They also have a lot of cash on their bal-ance sheets.

• In media, many traditional media compa-nies are still furiously working on themigration to digital and need acquisitionsto help them cross the Rubicon. That trendwill continue for many years.

For private equity:

• Many private equity firms are contem-plating fundraising and need to achieveexits to do that.

• The debt markets are very strong rightnow, after a tough second half of 2011. Weare routinely seeing debt multiples in the4x-7+x range, depending on the size andpredictability of the company. Meaningfuldebt is starting to be available for Internet-only companies.

The past six months have been very busy forus as both buyers and sellers, and we expect tocontinue to be active in the near future as well.We are still highly intent on growth andfocused on digital media, electronic informa-tion, software and tech-enabled services.

Although the valuations for digital media andSaaS software in particular have been stratos-pheric, we have continued to find interestingminority investments in private companies.

Neil Garfinkel, Partner Francisco [email protected]

The acceleration of media dollars into online(including social) and mobile channels willcontinue through the foreseeable future.While macro events (Europe and its dampen-ing effect on US) will impact growth, theunderlying trends are very positive. We antic-ipate being very active in M&A over the next18 months.

We constantly review the digital marketinglandscape. We are particularly interested innew investment platforms in (i) data-drivendigital marketing companies; and (ii) crosschannel analytics companies.

The current debt market is quite robust (3x-7xEBITDA, depending on the quality of theasset) which is helping deals get done.However, we are more focused on growth thanon leverage, and most of our digital marketingdeals have very little leverage in the capitalstructure.

Chris Langone, VP, Business DevelopmentSymphony Technology Group [email protected]

Market activity will be shaped by both politi-cal and economic trends, such as Europe, thePresidential election, the potential fiscal cliff, apotential double dip and changes to the taxcode. I believe our deal-making ability will behindered by a lessening of debt availability,offset by increasing middle market deal flowfrom owner-operated companies looking tosell before potential 2013 tax code changes.We are equally active, if not more so, in downmarkets.

For the middle market, I believe the debt mar-kets will see more robust activity for the rest ofthe year, at the normally lower leverage multi-ples. We are seeing debt to equity ratios of60/40 to 50/50 in the deals we are looking atand total leverage of 4x to 5x, with great vari-ability in leverage, depending on the profile ofthe business. ■

JEGI Client Briefing – July 2012 7

“The current debt market is quiterobust (3x-7x EBITDA, dependingon the quality of the asset) whichis helping deals get done.”

“There is a significant amount ofequity capital seeking goodinvestments.”

“...many traditional media com-panies are still furiously workingon the migration to digital andneed acquisitions to help them...”

Exceptional Transaction Experience

JEGI’s client is mentioned first in each of the above transactions.

has sold the assets ofFUTURE MUSIC US

including

to

a portfolio company of

has acquired

a global digital marketing services company

the No. 1 media brand in the motorcycle industry

to

has sold

a leading provider of banking information and analytics

has been sold

to

A

a leading European display ad exchange for premium unsold inventory

has been sold

to

a unit of

a leading distributor of company data and public filings for equities,

mutual funds and a variety of other publicly traded assets

has secured $12 million in growth capital

from

a leading provider ofintegrated event solutions

anda portfolio company of

The Riverside Companyand

VS&A Comm Partners Fund IIhas been sold

to

a leading provider of social media insights via search,

monitoring and measurement

has been sold to

a leading developer of onlineshopping solutions for local media

has been sold to

a consortium of eight leading media and publishing companies:

Advance Digital, A.H. BeloCorporation, Cox Media Group,

Gannett Co. Inc., HearstCorporation, MediaNews Group,

The McClatchy Co., and The Washington Post

150 East 52nd Street, 18th FloorNew York, NY 10022 (212) 754-0710

www.jegi.com

Bill HitzigCOO

Scott PetersCo-President

Richard MeadManaging [email protected]

Wilma JordanFounder & [email protected]

Tom PechtManaging Director

Tom CreaserEVP

Adam GrossCMO

Tolman GeffsCo-President

Contact Us to Discussthe Marketplace and Your Company’s

M&A Strategy. David ClarkManaging Director

Amir AkhavanDirector

a leading Australia-based online community for parents

has been sold

to

a leading global social media agencyF R O M C O N T E N T T O C O M M E R C E ™

has been sold to

a unit of

the leading provider of consumershopping predictive targeting data

a divison of

has been sold to

a SaaS marketing platform (CRM) for real-time, multi-stage, and

multi-channel marketing including social media, email, and mobile

has been sold

to

a leading B2B lead generation provider for IT vendors

has been sold to

®

®

a portfolio company of

a leading provider of ecommerce solutions

to publishers via

has been sold

to

Journalism Online

has sold Summers Press and select CCH

OSHA compliance andemployment guide publications

to

MEDIA

MARKETING SERVICES

INFORMATION

TECHNOLOGY

has sold

to

a division of DMGT plc

a leading producer of trade showsserving the U.S retail markets for gifts, home furnishings,action sports and antiques

for $180,000,000

a leading interactive marketing agencyand CRM solutions provider

a divison of

has been sold

to

has been soldto

a provider of content, data, advertising, and career services

for the oil and gas industry

for $39,000,000

the leading SaaS platform for retail transaction optimization solutions

has been sold

to