income tax

TRANSCRIPT

Direct Tax BY CA BALA YADAV

TAX?

TAX

Latin-Word-TAXO-Means-RATEFinancial Charge/other levy

Imposed upon a tax payer (tax payer may a individual or legal entity)

By the state or the functional equivalent of a state That failure to pay or evasion of or resistance Is punishable by law.

Our tax system is based on our "ability to pay." The more money we earn, the more taxes we pay. And the opposite is also true. If we earn a small income, we pay less taxes.

A means by which governments finance their expenditure by imposing charges on citizens and corporate entities.

Governments use taxation to encourage or discourage certain economic decisions.

For example, reduction in taxable personal (or household) income by the amount paid as interest on home mortgage loans results in greater construction activity, and generates more jobs.

TYPE OF TAXES

DIRECT TAXES• A tax that is paid directly

by an individual or organization to the imposing entity.

• e.g income tax, wealth tax etc. Burden of tax borne by the person himself.

INDIRECT TAXES• A tax that increases the price

of a good so that consumers are actually paying the tax by paying more for the products.

• e.g excise duty, vat, sales tax, Service tax etc. Burden of tax shifted to another person

Income Tax Law

The Income Tax Act,

1961

The Income

Tax Rules, 1962

Circulars, Clarifications from CBDT

Time to time

Judicial Decision

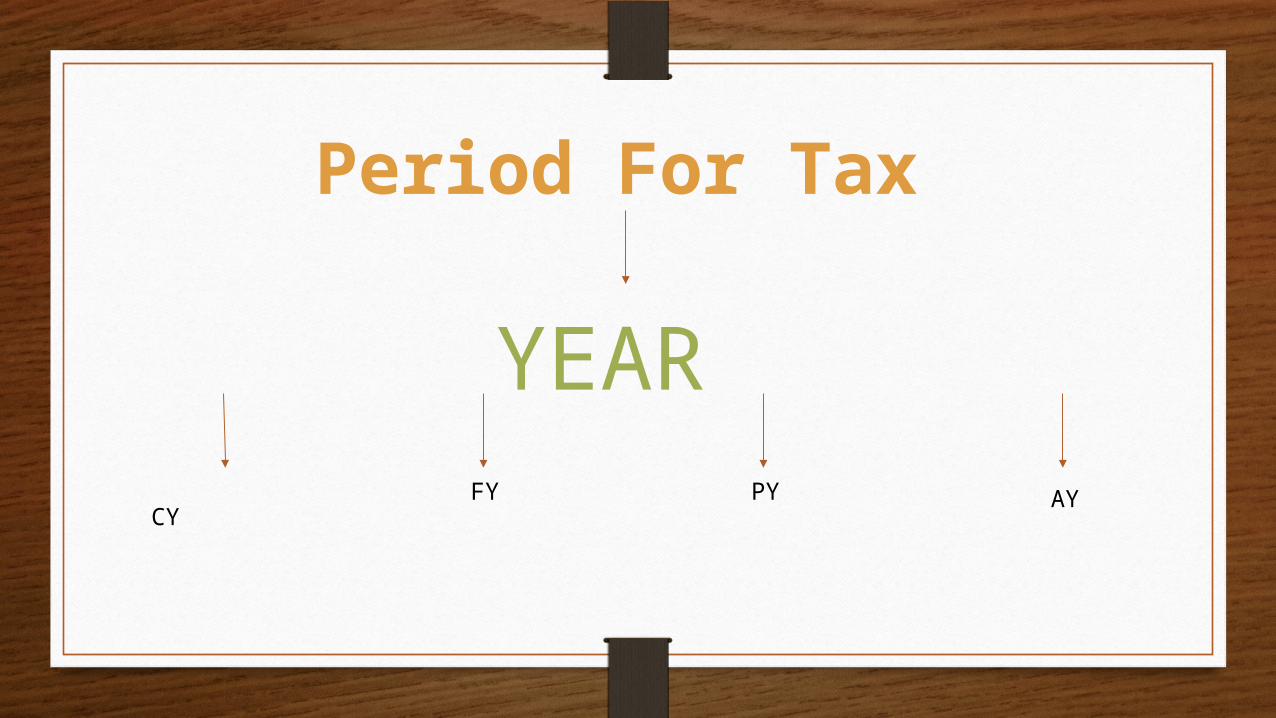

YEAR CY FY AY

Period For Tax

PY

AY-Assessment Year- Section 2 (9) of Income Tax Act, 1961A year in which income of an assessee of the previous year/last year needed to be assessed.It is called as “tax year” in some of the countries. Assessment Year (AY) is a period of twelve months starting from April 1st and ending on March 31st.

PY-Previous Year- Section 3 of Income Tax Act, 1961 A year in which income is earned to be taxed exactly in the immediately next/following assessment year.

It is also known as “income year” in some of the countries.

For Example – The income accrued in FY 2013-2014 its Assessment Year (AY) is 2014-2015. So, Financial Year (FY) is the Previous Year (PY) while Assessment Year (AY) is the Current Year (CY) in which the income is being assessed earned in Previous Year (PY). In the Assessment Year (AY) your total tax liability for the income earned in the previous financial year is evaluated and computed. Therefore, tax for the income earned in the Previous Year (PY) is paid in the Current Year (CY).

Previous Year in case of Newly Setup Business/ProfessionFirst Previous Year Second & Subsequent Previous Year

Starting Point It Commences on the date of setting date up of the B/P or on the date when the new source of income comes into existence.

April 1

Ending point Immediately following march 31

March 31st of the following year

Duration of Previous Year

12 months or less 12 months

Income of the Previous Year is not Taxable in the immediate

Assessment yeari.e. Exceptions

There are 5 cases in which income of previous year is not taxable in immediate assessment

year. Means Income is Taxable in the Previous Year in which such Income is earned.

Section 172

Shipping Business Of

Non-Residents

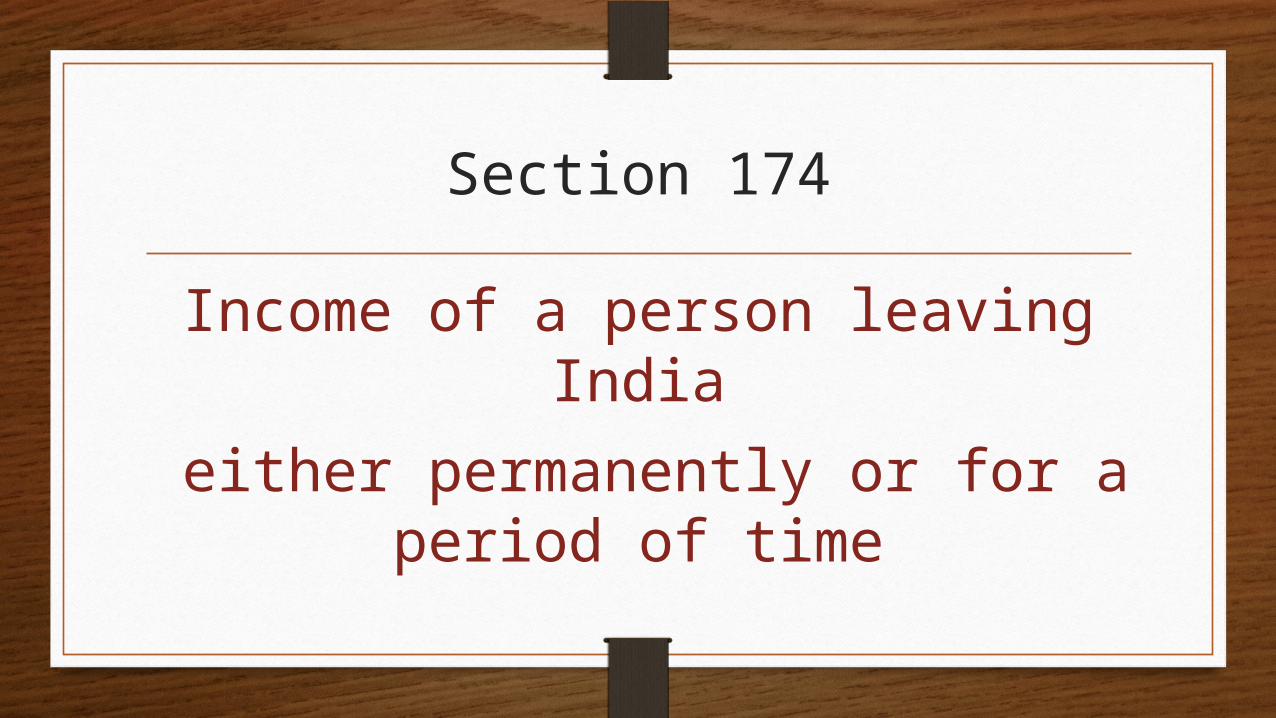

Section 174

Income of a person leaving India

either permanently or for a period of time

Section 174A

Association of person or body of individual,

formed or established for a particular event and purpose

and likely to be dissolved in the same year

in which the same was established.

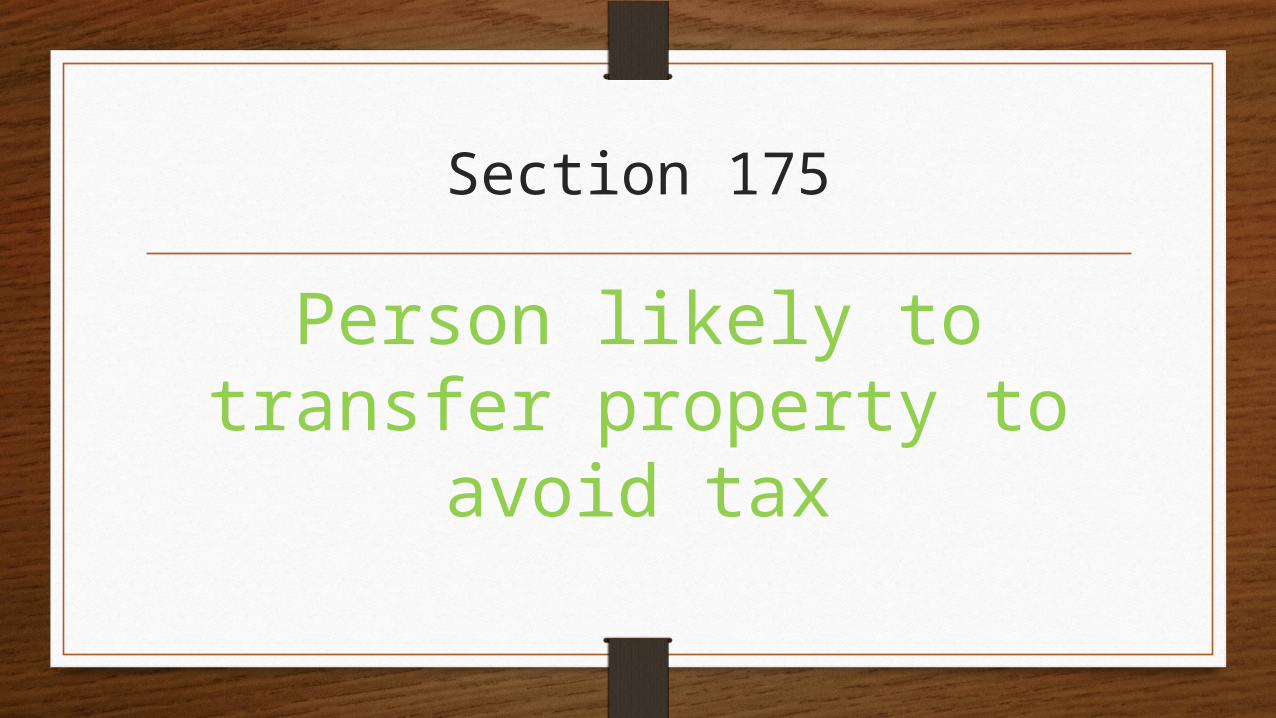

Section 175

Person likely to transfer property to avoid tax

Section176

Discontinued Business

Some Important Terms & Definitions Under INCOME TAX ACT, 1961

• Section 2(7) Section 2(8)

• Section 2(22) Section 2 (24)

• Section 2(25A) Section 2(26A)

• Section 2(26B) Section 2(29BA)

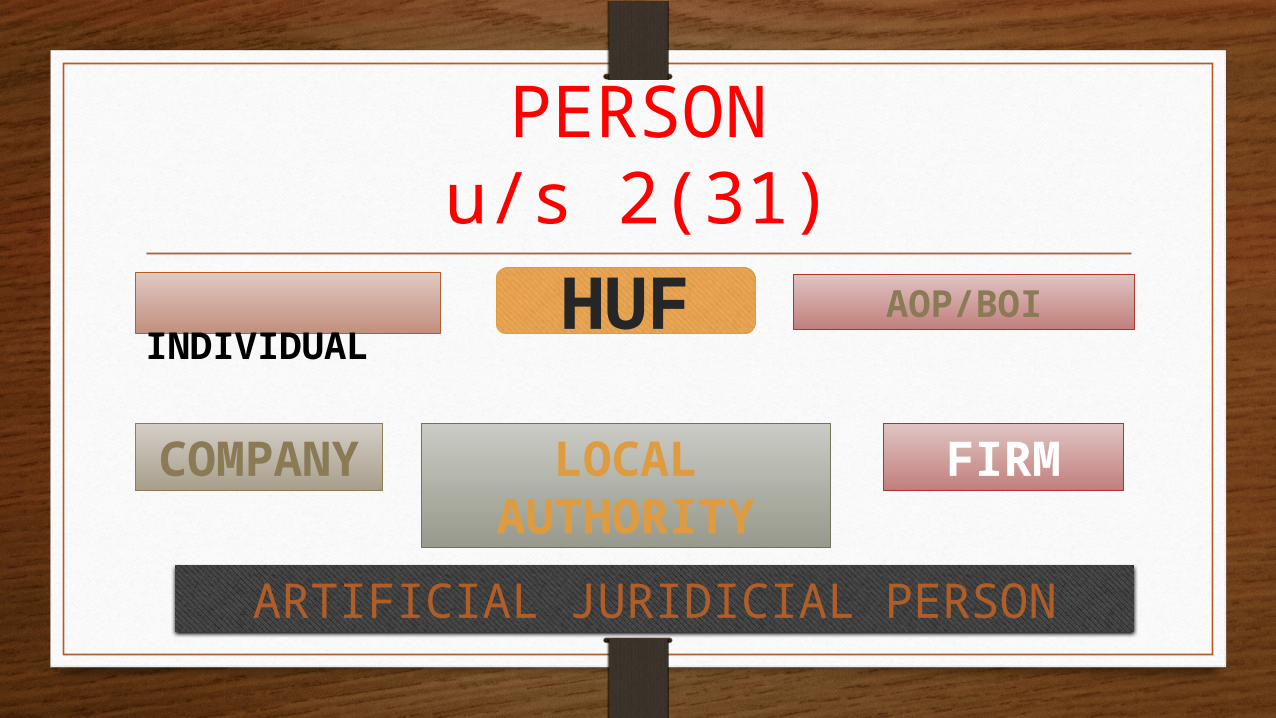

Section 2(31)

PERSONu/s 2(31)

INDIVIDUAL

HUF

COMPANY

AOP/BOI

FIRMLOCAL AUTHORITY

ARTIFICIAL JURIDICIAL PERSON

A natural human being

i.e. male, female, person of sound and unsound mind

It also includes minor child. However income of minor child included in the

income of a parent.

AN INDIVIDUAL

“

”

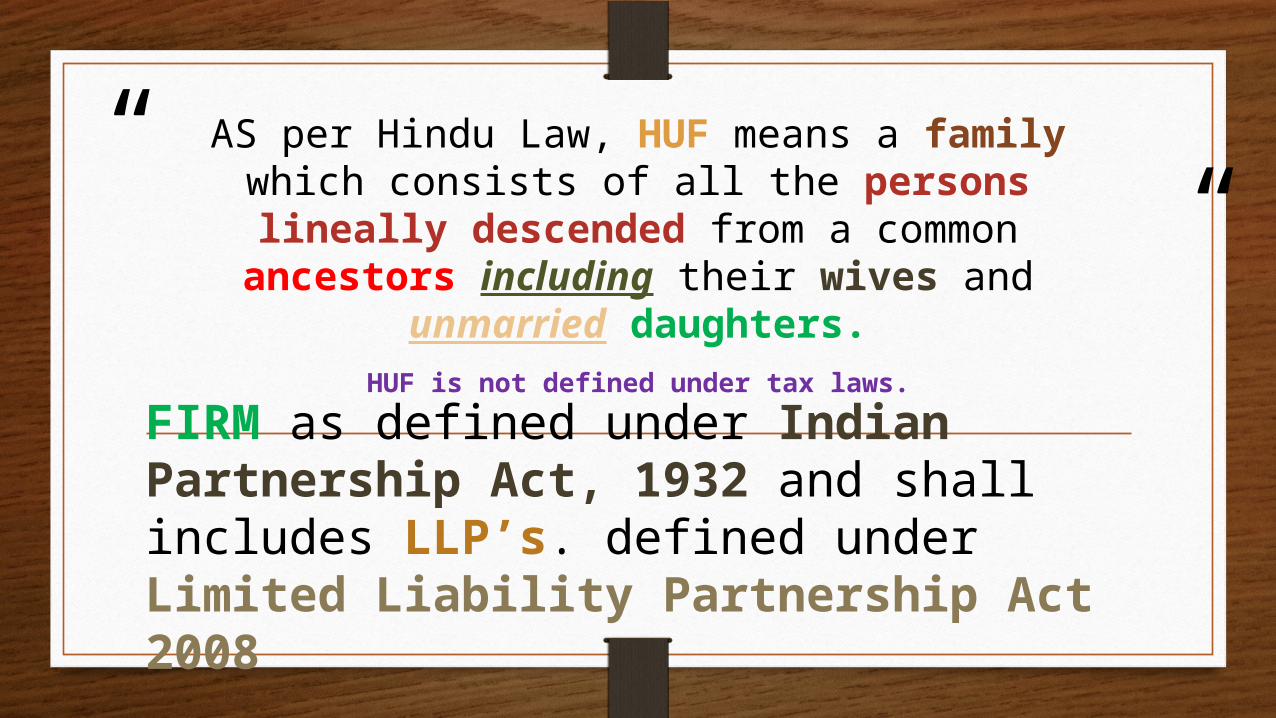

AS per Hindu Law, HUF means a family which consists of all the persons lineally

descended from a common ancestors including their wives and unmarried

daughters.HUF is not defined under tax laws.

FIRM as defined under Indian Partnership Act, 1932 and shall includes LLP’s. defined under Limited Liability Partnership Act 2008

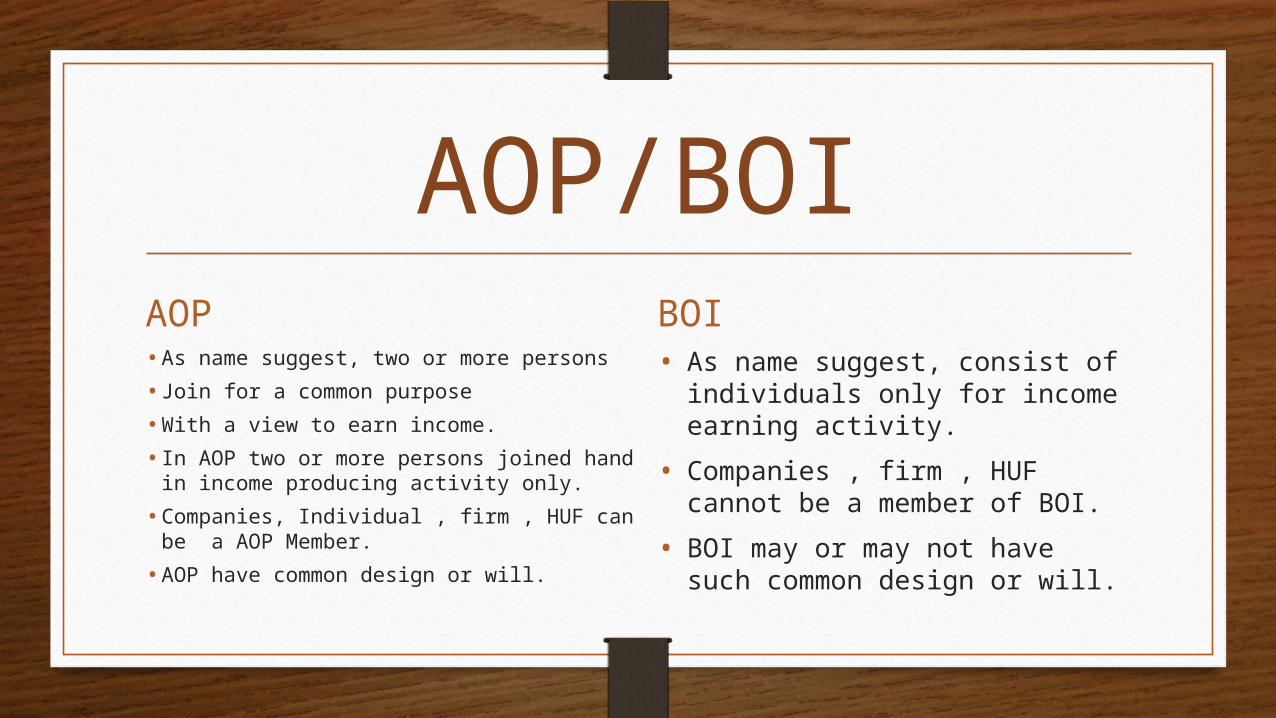

AOP/BOIAOP• As name suggest, two or more persons

• Join for a common purpose

• With a view to earn income.

• In AOP two or more persons joined hand in income producing activity only.

• Companies, Individual , firm , HUF can be a AOP Member.

• AOP have common design or will.

BOI• As name suggest, consist of

individuals only for income earning activity.

• Companies , firm , HUF cannot be a member of BOI.

• BOI may or may not have such common design or will.

LOCAL AUTHORITY

Artificial Judicial Persons

• It is the rest category for the purpose of income tax act.

• It includes entities which are not natural person and act as separate entity in the eyes of law.

• Artificial person with a juristic personality fall under this category.

Panchayat

Municipality

Municipal Committee

District Board

Cantonment Board

Thank You