income- tax amendments applicable for the assessment … · jagdish t punjabi june 25, 2014 income-...

TRANSCRIPT

Jagdish T Punjabi June 25, 2014

Income- tax amendments applicable for the

assessment year 2014-15 and

E-Filing of returns of Income.

2

Contents

Persons obliged to file return of income.

Due dates for filing return of income.

Rates of tax applicable for AY 2014-15.

Amendments to the Act, relating to filing of return of income, applicable with effect

from AY 2014-15.

Forms to be used by various assessees.

Persons required to file return electronically.

Cases where return is to be digitally signed.

Changes in the Forms.

Data required for filing return of income which may not be available from financial

statements to be taken in filing returns of income

Jagdish T Punjabi June 25, 2014

3

Persons obliged to file return of income

Jagdish T Punjabi June 25, 2014

Sr.

No.

Status of the Assessee Conditions

1 Firms (including LLP) Every Firm irrespective of earning income or incurring

loss

2 Company Every Company irrespective of earning income or

incurring loss

3 Person other than Company or Firm If his or its total income during the previous year

exceeds maximum amount not chargeable to tax,

without considering deduction u/ss. 10A, 10B, 10BA,

and Chapter VI-A

4 Charitable or religious trust If the total income in the previous year exceeds the

maximum amount not chargeable to tax without giving

effect to section 11 and section12

5 Every person To whom notice u/s 142(1) or 148 is issued

6 Any resident person other than not

ordinary resident

Who has any asset (including financial interest in any

entity) located outside India or signing authority in any

account located outside India

4

Persons obliged to file return of income…

Jagdish T Punjabi June 25, 2014

Sr.

No.

Status of the Assessee Conditions

7 • Research Association u/s 10(21)

• News Agency u/s 10(22B)

• Association / Institution referred u/ss.

10(23A) and 10(23B)

• Universities / Hospitals / Medical

institutions referred under various sub-

clauses of Section 10(23C) i.e. (iiiad) or

(iiiae) or (iv) or (v) or (vi) or (via)

• Trade Union referred u/ss. 10(24)(a)

and 10(24)(b)

• Board / Trust / Commission referred u/s

10(46)

• Infrastructure Debt Fund referred u/s

10(47)

If the income exceeds maximum amount not

chargeable to tax without considering

exemptions under respective provisions of

section 10

8 University, college or any other institution

referred u/s 35(1)(ii)/(iii)

Required to furnish return of income / loss even if

not required to furnish return of income under

any other provisions

9 Political Party Total income in the previous year without giving

effect to section 13A exceeds the maximum

amount not chargeable to income tax

5

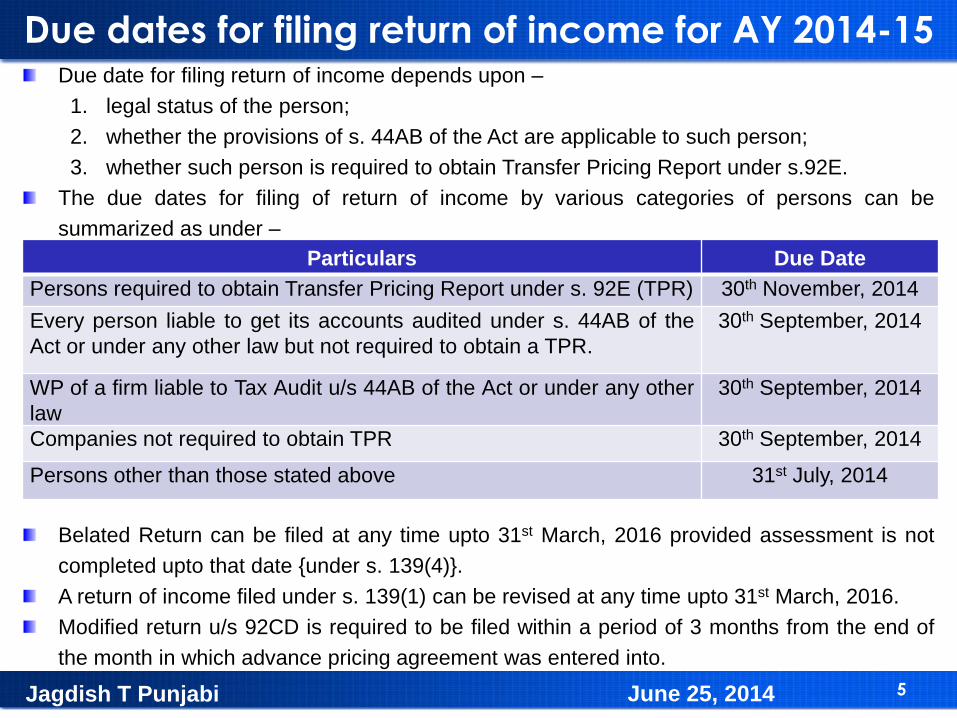

Due dates for filing return of income for AY 2014-15Due date for filing return of income depends upon –

1. legal status of the person;

2. whether the provisions of s. 44AB of the Act are applicable to such person;

3. whether such person is required to obtain Transfer Pricing Report under s.92E.

The due dates for filing of return of income by various categories of persons can be

summarized as under –

Belated Return can be filed at any time upto 31st March, 2016 provided assessment is not

completed upto that date {under s. 139(4)}.

A return of income filed under s. 139(1) can be revised at any time upto 31st March, 2016.

Modified return u/s 92CD is required to be filed within a period of 3 months from the end of

the month in which advance pricing agreement was entered into.

Jagdish T Punjabi June 25, 2014

Particulars Due Date

Persons required to obtain Transfer Pricing Report under s. 92E (TPR) 30th November, 2014

Every person liable to get its accounts audited under s. 44AB of the

Act or under any other law but not required to obtain a TPR.

30th September, 2014

WP of a firm liable to Tax Audit u/s 44AB of the Act or under any other

law

30th September, 2014

Companies not required to obtain TPR 30th September, 2014

Persons other than those stated above 31st July, 2014

6

Tax Rates for Assessment Year 2014-15

Individuals / HUF / AOP / BOI

Co-operative Society

Tax Rate Total Income Slabs

Individual who is Resident

Very Senior Citizen

(> 80 yrs)

Individual who is

Resident Senior Citizen

(60 - 80 yrs)

Other Individual /

HUF/AOP/BOI

Nil ≤ 5,00,000 ≤ 2,50,000 ≤ 2,00,000

10% - > 2,50,000 ≤ 5,00,000 > 2,00,000 ≤ 5,00,000

20% > 5,00,000 ≤ 10,00,000 > 5,00,000 ≤ 10,00,000 > 5,00,000 ≤ 10,00,000

30% > 10,00,000 > 10,00,000 > 10,00,000

Tax Rate Total Income Slabs (in Rs.)

10% ≤ 10,000

20% > 10,000 ≤ 20,000

30% > 20,000

Jagdish T Punjabi June 25, 2014

Note : In addition to tax at

above rates, EC & SHEC @

3% of income-tax is also

payable, in certain cases

surcharge is also leviable –

see separate slide

7

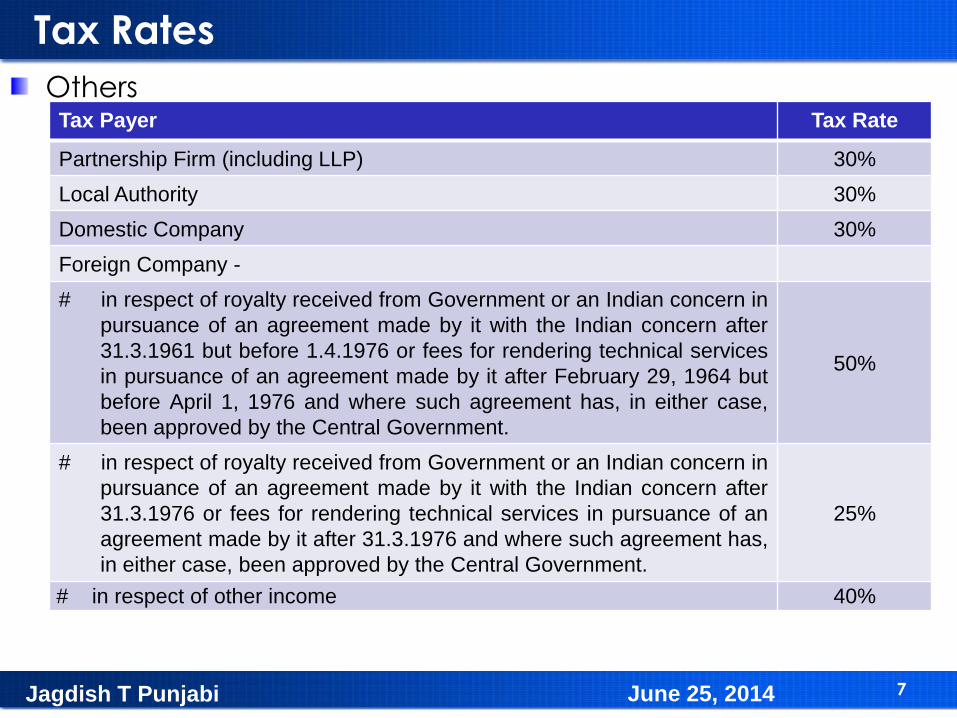

Tax Rates

Tax Payer Tax Rate

Partnership Firm (including LLP) 30%

Local Authority 30%

Domestic Company 30%

Foreign Company -

# in respect of royalty received from Government or an Indian concern in

pursuance of an agreement made by it with the Indian concern after

31.3.1961 but before 1.4.1976 or fees for rendering technical services

in pursuance of an agreement made by it after February 29, 1964 but

before April 1, 1976 and where such agreement has, in either case,

been approved by the Central Government.

50%

# in respect of royalty received from Government or an Indian concern in

pursuance of an agreement made by it with the Indian concern after

31.3.1976 or fees for rendering technical services in pursuance of an

agreement made by it after 31.3.1976 and where such agreement has,

in either case, been approved by the Central Government.

25%

# in respect of other income 40%

Others

Jagdish T Punjabi June 25, 2014

8

Tax Rates

Tax Payer Tax Rate

Minimum Alternate Tax (MAT) – As a percentage of Book Profit (payable by

Companies) (115JB)

18.50%

Alternate Minimum Tax (AMT) – As per rate given u/s 115JC on adjusted

total Income (payable by Other than Companies) (115JC)

18.50%

Tax on dividend declared, distributed or paid by a domestic company

(115O)

15.00%

Tax on ―distributed income‖ by domestic company on buy back of shares not

listed on a recognised stock exchange

20.00%

Tax on income distributed by Securitisation Trust 25.00%

Others

Jagdish T Punjabi June 25, 2014

9

Tax Rates - Trusts

Particulars Tax Rate

Public Religious / Charitable Trust / income Exempt u/s 11

Corpus Donations Exempt u/s 11

Private religious trust / religion specific charitable

trust

Taxable as AOP (rates applicable to

individuals)

Religious / Charitable Trust - for non exempt

income / loss of exemption u/s 13(1)(c) & 13(1)(d)Maximum Marginal Rate*

Any other taxable income of religious / charitable

trusts

Taxable as AOP (rates applicable to

individuals)

Anonymous Donations (‗AD‘) (section 115BBC)30% on AD in excess of 5% of total

donations or Rs. 1 lakh

Private trust – shares of beneficiaries known

(no business profits)

Trustee assessed as Representative

Assessee of each beneficiary (section

161)

Private trust – shares of beneficiaries unknown

(no business profits)

Maximum Marginal Rate*

(taxable as AOP in certain circumstances)

Private trust earning business profits Maximum Marginal Rate*

Oral Trust Maximum Marginal Rate*

* Maximum Marginal Rate for AY 2014-15 –33.99% including surcharge & cess

Jagdish T Punjabi June 25, 2014

10

Rates of Tax given in various sections of the Act.Tax rates specified in the Income-tax Act - The following incomes are taxable at the rates

specified by the Income-tax Act. (the list contains often used rates. It is not exhaustive list)

Jagdish T Punjabi June 25, 2014

Section Income Income-taxrates

111A Short-term capital gains 15

112 Long-term capital gains 20

115A(1)(a)(i) Dividend received by a foreign company or a non-resident non-

corporate assessee [*it is not applicable in the case of

dividends referred to in section 115-O]

20*

115A(1)(a)(ii) Interest received by a foreign company or a non-resident non-

corporate assessee from Government or an Indian concern on

moneys borrowed or debt incurred by Government or the

Indian concern in foreign currency

20

115A(1)(a)(iia) Interest received from an infrastructure debt fund referred to in

section 10(47)

5

115A(1)(a)(iiaa) Interest received from an Indian company specified in section

194LC

5

115A(1)(a)(iiab) Interest of the nature and extent referred to in section 194LD

(applicable from the assessment year 2014-15)

5

11

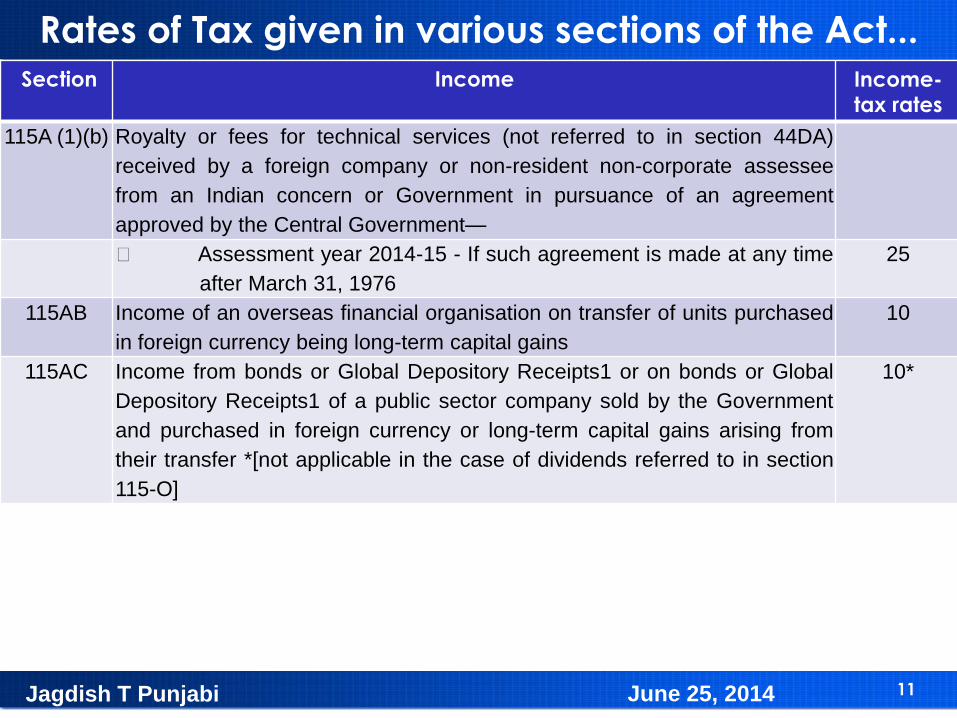

Rates of Tax given in various sections of the Act...

Jagdish T Punjabi June 25, 2014

Section Income Income-tax rates

115A (1)(b) Royalty or fees for technical services (not referred to in section 44DA)

received by a foreign company or non-resident non-corporate assessee

from an Indian concern or Government in pursuance of an agreement

approved by the Central Government—

Assessment year 2014-15 - If such agreement is made at any time

after March 31, 1976

25

115AB Income of an overseas financial organisation on transfer of units purchased

in foreign currency being long-term capital gains

10

115AC Income from bonds or Global Depository Receipts1 or on bonds or Global

Depository Receipts1 of a public sector company sold by the Government

and purchased in foreign currency or long-term capital gains arising from

their transfer *[not applicable in the case of dividends referred to in section

115-O]

10*

12

Rates of Tax given in various sections of the Act...

Jagdish T Punjabi June 25, 2014

Section Income Income-tax rates

115ACA Income from Global Depository Receipts held by a resident individual who is

an employee of an Indian company engaged in information technology

software/services

Dividend [other than dividend referred to in section 115-O] on global

Depository Receipts issued under employees stock option scheme

and purchased in foreign currency

10

Long-term capital gain on transfer of such receipts 10

115AD Income in respect of securities received by a Foreign Institutional Investor

as specified by the Government

Short-term capital gain covered by section 111A 15

Any other short-term capital gain 30

Long-term capital gain 10

Interest referred to in section 194LD (applicable from the assessment

year 2014-15)

5

Other income [*not applicable in the case of dividends referred to in

section 115-O]

20*

13

Rates of Tax given in various sections of the Act...

Jagdish T Punjabi June 25, 2014

Section IncomeIncome-tax rates

115B Profits and gains of life insurance business 12.5

115BB

Winnings from lotteries, crossword puzzles, or race including horse race

(not being income from the activity of owning and maintaining race horse)

or card game and other game of any sort or from gambling or betting of any

form or nature 30

115BBA(1)

(a)/(b)

Income of a non-resident foreign citizen sportsman for participation in any

game in India or received by way of advertisement or for contribution of

articles relating to any game or sport in India or income of a non-resident

sport association by way of guarantee money 20

115BBA(1)

(c)

Income of non-resident foreign citizen (being an entertainer) for

performance in India 20

115BBC Anonymous donation 30

115BBD

Income of an Indian company by way of dividends declared, distributed or

paid by a specified foreign company (in which the Indian company holds 26

per cent or more of equity share capital) 15

115BBE Income referred to in sections 68, 69, 69A, 69B, 69C and 69D 30

14

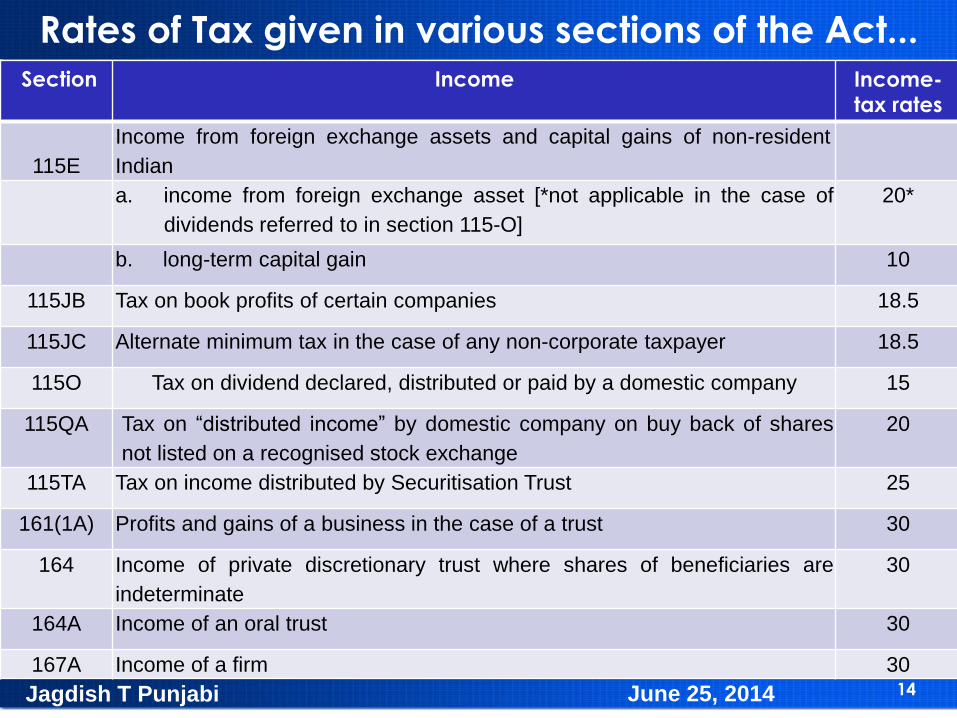

Rates of Tax given in various sections of the Act...

Jagdish T Punjabi June 25, 2014

Section Income Income-tax rates

115E

Income from foreign exchange assets and capital gains of non-resident

Indian

a. income from foreign exchange asset [*not applicable in the case of

dividends referred to in section 115-O]

20*

b. long-term capital gain 10

115JB Tax on book profits of certain companies 18.5

115JC Alternate minimum tax in the case of any non-corporate taxpayer 18.5

115O Tax on dividend declared, distributed or paid by a domestic company 15

115QA Tax on ―distributed income‖ by domestic company on buy back of shares

not listed on a recognised stock exchange

20

115TA Tax on income distributed by Securitisation Trust 25

161(1A) Profits and gains of a business in the case of a trust 30

164 Income of private discretionary trust where shares of beneficiaries are

indeterminate

30

164A Income of an oral trust 30

167A Income of a firm 30

15

Rates of Tax given in various sections of the Act...

Jagdish T Punjabi June 25, 2014

Section Income Income-tax rates

167B Income of an association of persons or body of individuals if shares of

members are unknown

30

167B(2) Income of an association of persons or body of individuals if total income of

any member (excluding share from the association or body) exceeds the

maximum amount not chargeable to tax [*if total income of any member of

the association or body is chargeable to tax at a rate higher than 33.99 per

cent for the assessment year 2014-15, then tax shall be charged on that

portion of the total income of the association/body which is relatable to the

share of such member at such higher rate and the balance of the total

income is taxable at a rate of 33.99 per cent for the assessment year 2014-

15]

30*

16

Rates of Tax given in various sections of the Act...Notes :

1. Surcharge - The above income-tax rates are subject to surcharge. Surcharge is calculated

as a percentage (given below) of income-tax –

† or book profit (for the purpose of section 115JB) or adjusted total income (for the purpose

of section 115JC).

2. Education cess - 2 per cent of income-tax and surcharge

3. Secondary and higher education cess : 1 per cent of income-tax and surcharge.

4. Marginal relief is available to individuals, HUF, AOP, BOI, every artificial juridical person, co-

operative society, firm, domestic company, foreign company. MR is also for MAT & AMT.

Jagdish T Punjabi June 25, 2014

If total income

If total income† is

up to Rs. 1 crore

If total income† is

> Rs.1 cr ≤ Rs 10 cr

If total income† is

> Rs. 10 crore

Individuals/HUF/AOP/BOI

/Artificial Juridical PersonNil 10% 10%

Firm Nil 10% 10%

Co-operative Society Nil 10% 10%

Local Authority Nil 10% 10%

Domestic Company Nil 5% 10%

Foreign Company Nil 2% 5%

Alternate Minimum Tax Nil 5% 10%

17

ITR Forms to be used

Jagdish T Punjabi June 25, 2014

Form

No.

Applicable To Not Applicable To

ITR-1

(Sahaj)

Individual having income

only from Salaries,

Pension, House Property

(HP), Income from Other

Sources (IOS)

Individual having:

i. More than one HP

ii. B/f losses under HP or loss under IFOS

iii. Winnings from Lottery or Income from Race

Horses

iv. R & OR having foreign assets/ signing

authority in foreign bank account

v. Claim for foreign tax credit/ relief under

section 90/90A/91

vi. Exempt income exceeding Rs.5,000

ITR-2 Individual/HUF Individual/HUF having business/professional

income

ITR-3 Individual/HUF who is

partner in a firm

Individual/HUF having any other business/

professional income

ITR-4 Individual/HUF having

business/ professional

income

-

18

Form

No.

Applicable To Not Applicable To

ITR-4S

(Sugam)

Individual/HUF having

presumptive business

income computed

under section

44AD/44AE

Individual/HUF :

i. Being R & OR having foreign assets/ signing

authority in foreign bank account

ii. Claiming foreign tax credit/ relief under

section 90/90A/ 91

iii. Having exempt income exceeding Rs.5,000

ITR-5 Person other than

Individual / HUF /

company

Persons required to file return

u/s.139(4A),(4B),(4C) or (4D) – They are required

to file ROI in Form ITR 7

ITR-6 Company Company required to file ITR 7

ITR-7 Person (including

company) required to

file return under

section 139(4A),(4B),

(4C) or (4D)

-

Jagdish T Punjabi June 25, 2014

ITR Forms to be used

19

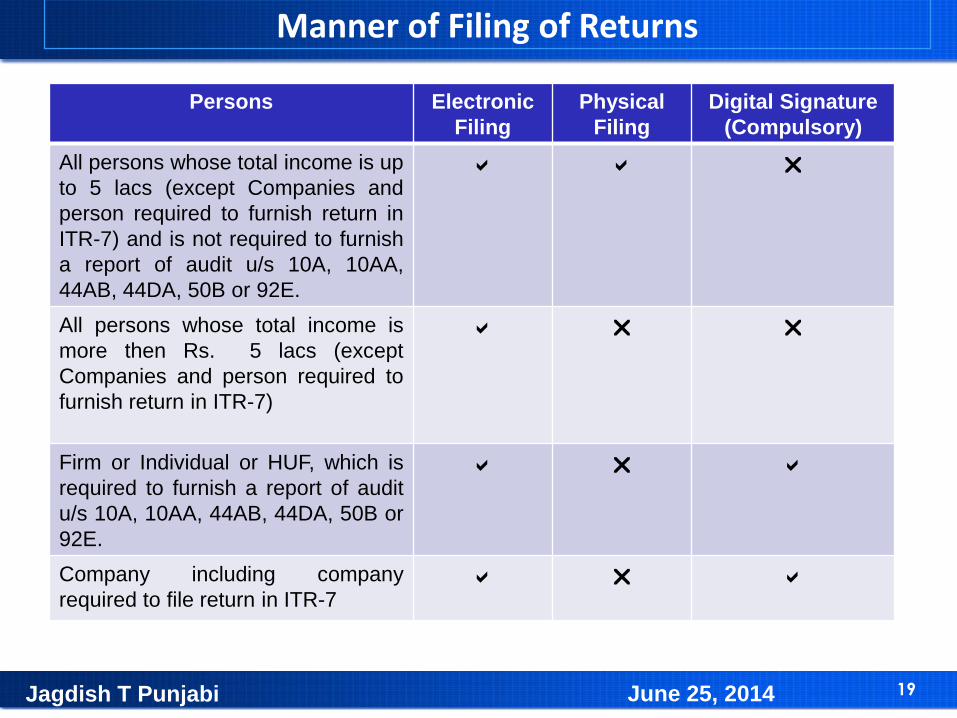

Manner of Filing of Returns

Persons Electronic

Filing

Physical

Filing

Digital Signature

(Compulsory)

All persons whose total income is up

to 5 lacs (except Companies and

person required to furnish return in

ITR-7) and is not required to furnish

a report of audit u/s 10A, 10AA,

44AB, 44DA, 50B or 92E.

a a r

All persons whose total income is

more then Rs. 5 lacs (except

Companies and person required to

furnish return in ITR-7)

a r r

Firm or Individual or HUF, which is

required to furnish a report of audit

u/s 10A, 10AA, 44AB, 44DA, 50B or

92E.

a r a

Company including company

required to file return in ITR-7a r a

Jagdish T Punjabi June 25, 2014

20

Changes in Online Filing of Returns

Persons Electronic

Filing

Physical

Filing

Digital

Signature

(Compulsory)

Person claiming benefit of Double Taxation

Avoidance Agreement (‗DTAA‘) (u/s 90 or 90A)

or unilateral relief (u/s 91)

a r r

Person required to furnish return in ITR-7 -

# and who is required to furnish a report of

audit under sections 10(23C)(iv),

10(23C)(v), 10(23C)(vi), 10(23C)(via), 10A,

10AA, 12A(10(b), 44AB, 44DA, 50B, 80IA,

80IB, 80IC, 80ID, 80JJA, 80LA, 92E,

115JB or 115VB

a r a

# others a a r

Individual or HUF being resident and ordinarily

resident having assets outside India or signing

authority in any account located outside India

a r r

Jagdish T Punjabi June 25, 2014

21

Amendments effective from

Assessment Year 2014-15

Jagdish T Punjabi June 25, 2014

22

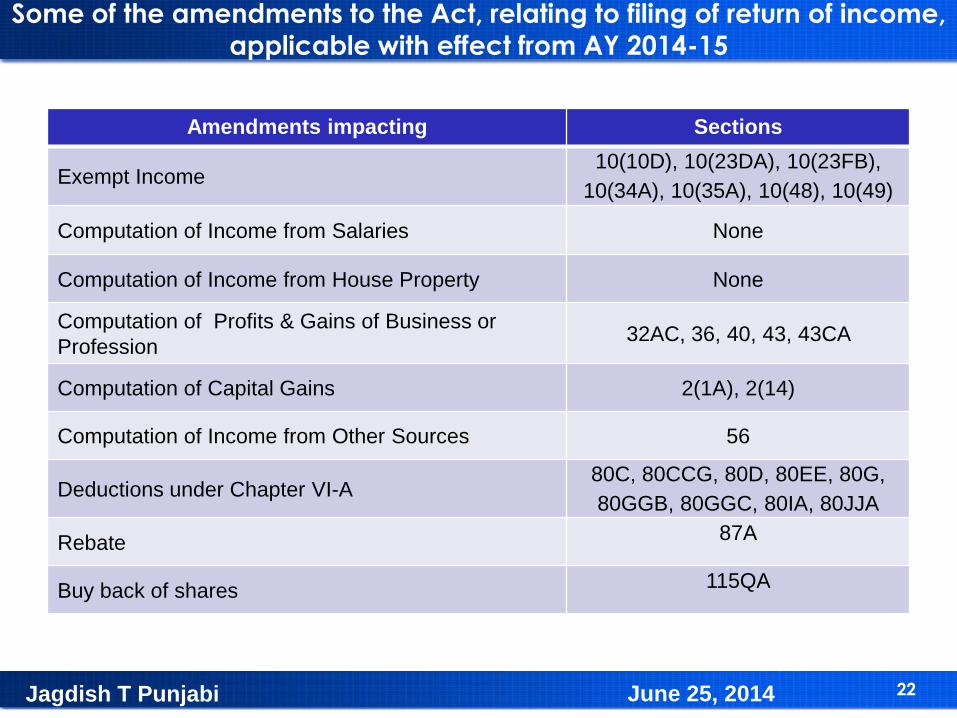

Some of the amendments to the Act, relating to filing of return of income,

applicable with effect from AY 2014-15

Jagdish T Punjabi June 25, 2014

Amendments impacting Sections

Exempt Income10(10D), 10(23DA), 10(23FB),

10(34A), 10(35A), 10(48), 10(49)

Computation of Income from Salaries None

Computation of Income from House Property None

Computation of Profits & Gains of Business or

Profession32AC, 36, 40, 43, 43CA

Computation of Capital Gains 2(1A), 2(14)

Computation of Income from Other Sources 56

Deductions under Chapter VI-A80C, 80CCG, 80D, 80EE, 80G,

80GGB, 80GGC, 80IA, 80JJA

Rebate 87A

Buy back of shares 115QA

23

Amendment to s. 2(1A) and s. 2(14)The definition of the terms `agricultural land‘ and `capital asset‘ have been amended. Prior

to the amendment land situated in an area notified by the Central Government was regarded

as non agricultural land. Also, income from such land was not regarded as agricultural

income. Central Government could notify land situated within a distance of not more 8 kms

from the local limits of a local authority or a cantonment board. While so notifying the areas,

the Government had to have regard to the extent of, scope for urbanization of that area and

other relevant considerations.

Post the amendment w.e.f. 1.4.2014, the land situated outside the local limits of local

authority or cantonment Board will be regarded as non agricultural land considering the

population of the local authority or a cantonment board.

If the population is more than 10,000 but upto 1,00,000 then land situated within 2 kms from

the local limits of the local authority or cantonment board will be non agricultural land.

If the population is more than 1,00,000 but upto 10,00,000 then land situated within 6 kms

from the local limits of the local authority or cantonment board will be non agricultural land.

If the population is more than 10,00,000 then land situated within 8 kms from the local limits

of the local authority or cantonment board will be non agricultural land.

For this purpose, population means the population according to the last preceding census of

which the relevant figures have been published before the first day of the previous year.

For AY 2014-15, the relevant figures will be the figures of the census which figures have

been published before 1.4.2013. The distance is to measured aerially.

Jagdish T Punjabi June 25, 2014

24

Amendment to s. 10(10D)

Under section 10(10D) any sum received under a life insurance policy, including the sum

allocated by way of bonus on such policy is exempt from tax. However, amounts received

under certain policies are not exempt. One such policy is an insurance policy issued on or

after 1.4.2012 in respect of which the premium payable for any of the years during the term

of the policy exceeds 10% of the actual capital sum assured. Effective 1.4.2014 a proviso is

added to this which provides that in case a policy is issued on or after 1.4.2013 and is for

insurance on life of a person who is

1. a person with disability; or

2. a person with severe disability as referred to in s. 80U; or

3. is a person suffering from disease or ailment specified in rules made under s. 80DDB

then for the words 10% the words 15% are substituted.

The term ―actual capital sum assured‖ in relation to a life insurance policy shall mean the

minimum amount assured under the policy on happening of the insured event at any time

during the term of the policy, not taking into account –

1. The value of any premium agreed to be returned; or

2. Any benefit by way of bonus or otherwise over and above the sum actually assured,

which is to be or may be received under the policy by any person.

Corresponding amendment has been made in s. 80C as well.

Jagdish T Punjabi June 25, 2014

25

Insertion of Section 10(34A)

S. 10(34A) provides that any income arising to an assessee, being a shareholder, on

account of buy back of shares (not being listed on a recognized stock exchange) by the

domestic company as referred to in s. 115QA will be exempt.

This section applies to any assessee irrespective of legal status and residential status. The

assessee should be a shareholder. Income should arise to the assessee on account of buy

back of shares which are not listed on a recognized stock exchange. Income should arise

from the domestic company referred to in s. 115QA. This section has been introduced since

the company buying back the shares is now required to pay tax under section 115QA /

Chapter XII-DA. A tax of 20% of the distributed income paid to shareholders is required to be

paid by the domestic Company.

Jagdish T Punjabi June 25, 2014

26

Insertion of Section 10(35A)

Amendments have been made to tax Securitisation Trust. Correspondingly, with a view to

avoid double taxation, s. 10(35A) has been introduced so as to provide that any income

received by an investor of a Securitisation Trust from such trust by way of distributed income

referred to in s. 115TA shall be exempt under s. 10(35A).

Jagdish T Punjabi June 25, 2014

27

Insertion of Section 32ACIncentive for Investment in new Plant or machinery: Deduction equal to 15% of the actual

cost of new assets acquired and installed after 31.3.2013 but before 1.4.2015.

Applicable to : A company. Residential status is not relevant.

Conditions required to be satisfied:

1. the Company is engaged in the business of manufacture or production of any article or

thing;

2. the Company acquires and installs new asset after 31.3.2013 but before 1.4.2015; (the

term `new asset‘ is defined in sub-section (4) of section 32AC)

3. actual cost of such new assets exceeds one hundred crore rupees.

Deduction to be allowed:

1. For assessment year 2014-15: 15% of the actual cost of new assets acquired and

installed after 31.3.2013 but before 1.4.2014 if the actual cost of new assets exceeds

one hundred crore rupees.

2. For assessment year 2015-16: 15% of the actual cost of new assets acquired and

installed after 31.3.2013 but before 1.4.2015 as reduced by the amount of deduction

allowed in assessment year 2014-15.

New asset is defined to mean any new plant or machinery (other than ship or aircraft) other

than items specifically excluded.

Jagdish T Punjabi June 25, 2014

28

Insertion of Section 32AC…Items specifically excluded from the definition of the term `new asset‘ –

1. any plant or machinery which before its installation by the assessee was used either

within or outside India by any other person; (this is any way evident from the term

`new‘);

2. any plant or machinery installed in any office premises or any residential

accommodation, including accommodation in the nature of a guest house;

3. any office appliances including computers or computer software;

4. any vehicle; or

5. any plant or machinery, the whole of the actual cost of which is allowed as a deduction

(whether by way of depreciation or otherwise) in computing the income chargeable

under the head `Profits and gains of business or profession‘ of any previous year.

If the actual cost of new assets acquired and installed after 31.3.2013 but before 1.4.2014 is

less than rupees one hundred crore then such company will not get a deduction under this

section in assessment year 2014-15.

Therefore, if in the current year, claim under section 32AC cannot be made since the actual

cost of new assets acquired and installed after 31.3.2013 but before 1.4.2014 is less than

one hundred crore rupees then the company may be able to claim deduction in assessment

year 2015-16 if the actual cost of new assets acquired and installed after 31.3.2013 but

before 1.4.2015 is more than one hundred crore rupees.

Jagdish T Punjabi June 25, 2014

29

Insertion of Section 32AC…This deduction is in addition to depreciation allowable under section 32 of the Act.

The claim for deduction under this section does not go to reduce the actual cost which needs

to be added to the block of assets for computing `written down value‘ on which depreciation

is allowable.

If the actual cost of the new assets acquired and installed after 31.3.2013 but before

1.4.2014 is more than one hundred crore rupees then irrespective of whether the result of

computation under the head `Profits and Gains of Business or Profession‘ is a profit or a loss

for assessment year 2014-15, the assessee company will be able to claim this deduction.

The incremental loss, if any, arising on account of such claim will be allowed to be carried

forward as a business loss but not as unabsorbed depreciation.

While the deduction under this section goes to reduce the total income chargeable under the

normal provisions of the Act, it does not reduce the `book profits‘ on which tax is payable

under section 115JB.

Deduction under this section will be allowable only while computing income under the head

`Profits and gains of business or profession‘ and not while computing income under the head

`Income from Other Sources‘.

The section requires that the new asset should be acquired and installed after 31.3.2013 but

before 1.4.2014. User of the asset does not seem to be necessary. Also, even if the new

asset is used for less than 180 days during the previous year still the amount of deduction

will be the same.

Jagdish T Punjabi June 25, 2014

30

Insertion of Section 32AC…

What is necessary is that the new asset should be acquired and installed within the dates

given in the section i.e. both acquisition and installation should happen in the specified

period. Orders placed earlier but delivery received in the period mentioned may still qualify.

Advance may have been paid earlier but delivery received in the period mentioned will also

qualify. However, if acquisition was in an earlier year and installation is in the period

specified then it could be a debatable question as to whether the deduction will be allowable.

Also, if asset is acquired but not installed then also the allowability of the claim for deduction

under this section may be doubtful.

In case the new asset acquired and installed is sold or otherwise transferred (otherwise than

in connection with an amalgamation or demerger) within a period of 5 years from the date of

its installation then the amount of deduction allowed under s. 32AC(1) in respect of such

asset shall be taxable as business income in the previous year in which such new asset is

sold or otherwise transferred.

In case the new asset acquired and installed is sold or otherwise transferred in connection

with an amalgamation or demerger within a period of 5 years from the date of its installation

then the amount of deduction allowed under s. 32AC(1) in respect of such asset shall be

taxable as business income of the amalgamated company or resulting company.

Jagdish T Punjabi June 25, 2014

31

Amendment to Section 36

S. 36(1)(vii) has been amended. An explanation has been inserted to provide that for the

purposes of the proviso to clause (vii) of sub-section (1) and clause (v) of sub-section (2), the

account referred to therein shall be only one account in respect of provision for bad and

doubtful debts under clause (viia) and such account shall relate to all types of advances,

including advances made by rural branches.

Jagdish T Punjabi June 25, 2014

32

Amendment to Section 40Sub-clause (iib) has been inserted to clause (a) of S. 40 to provide for disallowance of certain

payments made by State Government Undertaking to a State Government. The term `State

Government Undertaking‘ is defined in an Explanation to this sub-clause to include a corporation,

company, authority, a board or an institution which satisfies the conditions laid down in the

Explanation. The amounts paid which are to be disallowed are –

a. royalty, license fee, service fee, privilege fee, service charge or any other fee or charge,

by whatever name called, which is levied exclusively on; or

b. which is appropriated, directly or indirectly, from,

a State Government undertaking by the State Government.

The term `state government undertaking is defined to include –

i. a corporation established by or under any Act of the State Government;

ii. a company in which more than fifty per cent of the paid-up equity share capital is held by the

State Government;

iii. a company in which more than fifty per cent of the paid-up equity share capital is held by the

entity referred to in clause (i) or clause (ii) (whether singly or taken together);

iv. a company or corporation in which the State Government has the right to appoint the

majority of the directors or to control the management or policy decisions, directly or

indirectly, including by virtue of its shareholding or management rights or shareholders

agreements or voting agreements or in any other manner;

v. an authority, a board or an institution or a body established or constituted by or under any Act

of the State Government or owned or controlled by the State Government.

Jagdish T Punjabi June 25, 2014

33

Amendment to the definition of `speculative transaction’ – section 43

Clause (e) has been inserted in proviso to clause (5) of section 43 to provide that an eligible

transaction in respect of trading in commodity derivatives carried out in a recognized

association shall not be deemed to be a speculative transaction. Explanation 2 defines the

term `commodity derivative‘, `eligible transaction ‗ and `recognized association‘.

Commodity derivative means –

a contract for delivery of goods which is not a ready delivery contract; or

a contract for differences which derives its value from prices or indices of prices-

of such underlying goods; or

of related services and rights, such as warehousing and freight; or

with reference to weather and similar events and activities having bearing on the

commodity sector.

The definition of eligible transaction is on the same lines as definition of the said term for the

purpose of share derivatives.

Losses incurred in commodity derivatives in earlier years may have been c/fd as speculation

loss. Gains, subsequent to the amendment will be Non Speculative. Therefore, a question

will arise whether loss b/fd can set off against gains.

Gajendra Kumar Agarwal v. ITO (142 TTJ 612)(Mum)

Jagdish T Punjabi June 25, 2014

34

Insertion of Section 43CA This section has been introduced by the Finance Act, 2013 with effect from 1.4.2014. This

section applies to all assessees.

Conditions to be fulfilled:

1. The assessee transfers an asset (other than a capital asset)

2. The asset transferred is land or building or both;

3. Such transfer is for a consideration;

4. Consideration received or accruing as a result of such transfer is less than the value

adopted or assessed or assessable for the purpose of payment of stamp duty in respect

of such transfer.

Consequence if the above conditions are satisfied:

for the purposes of computing profits and gains from transfer of such asset, the value

adopted or assessed or assessable by any authority of a State Government shall be

deemed to be full value of consideration received or accruing as a result of such

transfer.

Exception:

1. There is an agreement fixing the value of consideration for transfer of the asset;

2. The date of such agreement and date of registration of such transfer of asset are not

the same;

3. On or before the date of the agreement, the consideration or part thereof has been

received by a mode other than cash.

Jagdish T Punjabi June 25, 2014

35

Insertion of Section 43CA… Then,

The value assessable by any authority of the State Government as on the date of agreement

shall be taken to be full value of consideration received or accruing as a result of the transfer

instead of the value on the date of registration.

Provisions of s. 50(2) and 50C(3) shall apply in relation to determination of value adopted or

assessed or assessable.

Issues:

1. Is letter of allotment an agreement?

2. If the initial amount is paid in cash but all subsequent amounts are paid by cheque then

will the benefit of sub-section (3) be denied?

3. In which year is the difference between the stamp duty value and the consideration

chargeable to tax?

4. Is this section applicable to sale of under construction flats by a builder / developer?

5. Is this section creating a charge or is laying down a computation provision or is merely a

rule of evidence?

6. In which year should the difference be offered for taxation in case of an assessee who

is following percentage completion method?

7. Are the provisions of this section applicable even to cases where income is offered for

taxation on presumptive basis.

Jagdish T Punjabi June 25, 2014

36

Amendment to section 56(2)(vii)(b)Item (ii) has been inserted in sub-clause (b) of clause (vii) of sub-section (2) of section 56 of

the Act. This clause provides that when an individual or a hindu undivided family receives an

immovable property (being land or building or both) for a consideration which is less than its

stamp duty value and the difference between the two is more than Rs. 50,000 then the

difference between the stamp duty value and the consideration will be charged to tax under

the head `Income from Other Sources‘ in the year of receipt. The immovable property so

received should be capital asset of the recipient. The charge is attracted in the year of

receipt of the immovable property. The proviso to this item provides that in case an

assessee has entered into an agreement which fixes the consideration of the immovable

property and the date of such agreement is different from the date of registration and the

assessee has on or before the date of agreement paid consideration or part thereof by a

mode other than cash then the stamp duty value on the date of agreement may be

considered instead of the stamp duty value on the date of registration.

Issues:

1. Is the provision retroactive?

2. Will the provision apply to booking of flats under construction?

3. Is the provision applicable to rural agricultural land?

4. Is letter of allotment an agreement?

Jagdish T Punjabi June 25, 2014

37

Amendment to section 80C

Section 80C provides for deduction for amounts invested / saved / deposited in the modes

specified in the section. This section interalia grants deduction for premia paid by the

assessee to insure life of the assessee or any member of his family. In respect of a policy

issued on or after 1.4.2012 premia paid qualifies for deduction only if the amount of premia

does not exceed 10% of the capital sum assured in any of the years during the term of the

policy. With effect from 1.4.2014 it is now provided that in respect of a policy issued on or

after 1.4.2013 for insurance on life of a person who is a person with disability or a person

with severe disability as referred to in s. 80U; or is a person suffering from disease or ailment

specified in rules made under s. 80DDB then the premia paid can be upto 15% of the capital

sum assured in any of the years during the term of the policy.

Jagdish T Punjabi June 25, 2014

38

Amendment to Section 80CCG

This section provides for deduction to a resident individual in respect of investment made

under equity savings scheme. The section provided that the assessee should acquire listed

equity shares in accordance with Rajiv Gandhi Equity Savings Scheme, 2013. Investment in

listed units of an equity oriented fund did not qualify for deduction under this section. The

section has been amended to provide that with effect from AY 2014-15 investment made

even in listed units of an equity oriented fund will also qualify for deduction. Further, the

section provided for deduction equivalent to 50% of the amount invested subject to a

maximum cap of Rs. 25,000. The deduction was allowed only for one assessment year.

With effect from AY 2014-15 the deduction is allowable for three consecutive assessment

years beginning with the assessment year relevant to the previous year in which the listed

equity shares or listed units of equity oriented fund were first acquired. One of the conditions

for claiming deduction under this section was that the gross total income of the resident

individual should not be in excess of Rs. 12 lakhs. This has now been changed to Rs.10

lakhs with effect from AY 2014-15.

Jagdish T Punjabi June 25, 2014

39

Amendment to Section 80DSection 80D provides a deduction of sum paid, by an assessee who is an individual or a

hindu undivided family, to insure the health of the assessee or his family. With effect from AY

2013-14 amount upto Rs. 5,000 paid for preventive health check-up is also allowable as a

deduction. The deduction under this section is subject to satisfaction of the conditions

mentioned in the section. One of the conditions was that the amounts qualifying for

deduction under this section should be paid by a mode other than cash. It has also been

provided that the any sum paid on account of preventive health check-up can be paid by any

mode including cash.

Another amendment is that what qualified for deduction under this section was premia paid

to insure health or contribution made to Central Government Health Scheme. It has now

been provided that amount paid to a scheme notified by Central Government will also qualify

for deduction. There are many schemes of Central and State Government which are similar

to CGHS but the contributions to these schemes did not qualify for deduction under this

section. The objective of the amendment is to bring such schemes at par with CGHS. The

following schemes have been notified for this purpose.

Contributory Health Scheme of Department of Space (Notification No. 06/2014 dated

15.01.2014)

Jagdish T Punjabi June 25, 2014

40

Insertion of Section 80EESection applies to: An assessee being an individual. Residential status is not relevant.

Conditions to be satisfied to claim deduction u/s 80EE:

a. The assessee is an individual.

b. The assessee has taken a loan.

c. Loan is taken from a financial institution. Financial institution is defined in sub-section

(5).

d. The loan is taken for the purpose of acquisition of a residential house property.

e. Loan has been sanctioned by the financial institution during the period beginning on

1.4.2013 and ending on 31.3.2014.

f. Amount of loan sanctioned for acquisition of the residential house property does not

exceed Rs. 25 lakhs.

g. The value of the residential house property does not exceed Rs. 40 lakhs.

h. The assessee does not own any residential house property on the date of sanction of

the loan.

Amount of deduction: Lower of the following –

a. Interest payable on loan taken from the financial institution for acquisition of residential

house property; OR

b. Rs. 1,00,000.

Jagdish T Punjabi June 25, 2014

41

Insertion of Section 80EE…Deduction of upto Rs. 1,00,000 is allowable only for AY 2014-15. However, in case the

amount of interest is lower than Rs. 1,00,000 then the balance amount i.e. Rs. 1,00,000

minus the amount of interest allowed in AY 2014-15 will be allowed as a deduction in AY

2015-16.

Consequence of claiming deduction under this section: Sub-section (4) provides that in

respect of interest for which deduction has been allowed under this section, deduction shall

not be allowed for such interest under any other provisions of the Act for the same or any

other assessment year.

Financial Institution is defined to mean –

a. a banking company to which the Banking Regulation Act, 1949 applies; and

b. including any bank or banking institution referred to in section 51 of that Act; or

c. a housing finance company

Housing Finance Company means a public company formed or registered in India with the

main object of carrying on the business of providing long-term finance for construction or

purchase of houses in India for residential purposes.

Jagdish T Punjabi June 25, 2014

42

Amendment to Sections 80G, 80GGB and 80GGC

Section 80G provides for deduction in respect of donations. Donations to persons listed in

sub-section (2) qualify for deduction. Of the persons listed in sub-section (2) donations to

certain persons can be without any upper limit and donations to others can be subject to a

maximum cap of 10% of adjusted gross total income i.e. gross total income minus

deductions under chapter VI-A (other than deduction under section 80G). Donation to

National Children‘s Fund qualified for deduction @ 50% of the amount donated. With effect

from AY 2014-15, section 80G has been amended to provide that donations to National

Children‘s Fund will now qualify for deduction @ 100%.

Section 80GGB provides for deduction to an Indian Company of amounts paid by it as

contribution to any political party or to an electoral trust. With effect from AY 2014-15 it is

now provided that deduction under this section shall not be allowed in cases where such

contribution is in cash.

Section 80GGC provides for deduction to an assessee other than local authority and every

artificial juridical person wholly or partly funded by the Government of amounts paid by it as

contribution to any political party or to an electoral trust. With effect from AY 2014-15 it is

now provided that deduction under this section shall not be allowed in cases where such

contribution is in cash.

Jagdish T Punjabi June 25, 2014

43

Amendment to Section 80IA

The sunset date for industrial undertakings claiming deduction under section 80IA and which

are engaged in generation of power or transmission or distribution of power by laying a

network of new transmission or distribution lines or undertaking substantial renovation and

modernization of existing network of transmission or distribution lines has been extended

from 31.3.2013 to 31.3.2014.

Jagdish T Punjabi June 25, 2014

44

Amendment to Section 80JJAA

Section 80JJAA provided deduction to an Indian Company whose gross total income

included profits and gains derived from an industrial undertaking engaged in manufacture or

production of an article or thing. Deduction was equivalent to an amount equal to 30% of

additional wages paid to new regular workmen employed by the assessee in the previous

year for 3 assessment years. This section is now amended to provide that the deduction will

be allowed to an Indian company whose gross total income includes any profits and gains

derived from the manufacture of goods in a factory. Therefore, earlier the qualifying

condition was that the gross total income should have included profits and gains derived

from an industrial undertaking engaged in manufacture or production of an article or

thing. Now, it is that the gross total income should included profits and gains derived from

manufacture of goods in a factory. For this purpose the term `factory‘ has been defined to

have the same meaning as is assigned to it in s. 2(m) of Factories Act, 1948.

Further, sub-section (2) provided that the deduction shall be denied if the industrial

undertaking is formed by splitting up or reconstruction of an existing undertaking or

amalgamation with another industrial undertaking. Now, w.e.f. AY 2014-15 it is provided that

the deduction shall be denied if the factory is hived off or transferred from another existing

entity or acquired by the assessee company as a result of amalgamation with another

company.

Jagdish T Punjabi June 25, 2014

45

Amendment to Section 80JJAA…

Earlier deduction was 30% of additional wages paid to new regular workemen employed by

the assessee in the previous year for three assessment years including the assessment year

relevant to the previous year in which such employment is provided. Now the deduction is

an amount equal to 30% of additional wages paid to the new regular workmen employed by

the assessee in such factory, in the previous year, for three assessment years including the

assessment year relevant to the previous year in which such employment is provided.

Jagdish T Punjabi June 25, 2014

46

Insertion of Section 87A

Rebate under section 87A : For Assessment Year 2014-15 a resident individual whose

total income does not exceed Rs. 5 lakhs is entitled to claim a rebate of 100% of the amount

of income-tax payable by him subject to a maximum of Rs. 2000.

Conditions:

The assessee is a resident individual

His total income does not exceed Rs. 5 lakhs.

Rebate: Lower of –

(a) 100% of amount of tax; or

(b) Rs. 2,000

Jagdish T Punjabi June 25, 2014

47

Levy of tax under section 115QA on Buy Back of Shares

A new Chapter XII-DA has been inserted in the Act with effect from 1.6.2013. This chapter

has sections 115QA to 115QC. The title of the chapter is `Special Provisions relating to Tax

on Distributed Income of Domestic Company for Buy-back of shares‘. When companies

distribute dividend they are liable to pay Dividend Distribution Tax. If the domestic company

buys back the shares which are not listed on a recognised stock exchange then tax has to be

paid u/s 115QA by the domestic company buying back such shares.

Conditions:

The assessee is a domestic company;

The company has bought back shares from a shareholder;

Such shares are not the shares listed on a recognized stock exchange;

Consequence: The company shall pay additional income-tax at the rate of twenty per cent

of distributed income. Distributed income is defined to mean the consideration paid by the

company on buy back of shares as reduced by the amount which was received by the

company for issue of shares.

Buy back has been defined to mean purchase by a company of its own shares in accordance

with the provisions of section 77A of the Companies Act, 1956.

Even if the company is not liable to pay any tax on its total income, yet it shall be required to

pay tax under section 115QA if it has bought back shares and other conditions are satisfied.

Jagdish T Punjabi June 25, 2014

48

Levy of tax under section 115QA on Buy Back of Shares…

Tax required to be paid under this section has to be paid within 14 days from the date of

payment of any consideration to the shareholder on buy-back of shares.

Credit shall not be claimed by the company or by any other person in respect of amount of

tax so paid on buy back of shares.

The income which has been charged to tax under sub-section (1) shall not be allowed as a

deduction under any other provision of the Act to the company or to the shareholder thereof.

Since amounts distributed by the domestic company on buy back of shares are liable to tax

under s. 115QA, exemption has been granted to a shareholder to whom income may arise

on buy back of shares. To provide for exemption income on s. 10(34A) has been inserted to

provide that any income arising to an assessee, being a shareholder, on account of buy back

of shares (not being listed on a recognized stock exchange) by the company referred to in s.

115QA shall be

S. 10(35A) provides that any income by way of distributed income referred to in s. 115TA

received from a securitization trust by any person being an investor of the said trust shall be

exempt from tax.

Jagdish T Punjabi June 25, 2014

49

Provisions dealing with Securitisation Trust

Chapter XII-EA captioned ―Special Provisions relating to Tax on Distributed Income by

Securitisation Trusts‖ has been introduced w.e.f. 1.6.2013. It contains sections 115TA to s.

115TC. Section 115TA levies tax on income distributed by securitization trust to its investors,

s. 115TB provides for interest payable on non-payment of tax and section 115TC deems

securitization trust to be an assessee in default in certain cases mentioned therein. The

Explanation after section 115TC defines the terms ―investor‖, ―securities‖, ―securitized debt

instrument‖ and ―securitization trust‖.

The provisions of s. 115TA(1) begin with a non-obstante clause and are notwithstanding

anything contained in any other provisions of the Act.

Conditions to be satisfied for levy of tax under s. 115TA(1)

1. There is a securitization trust;

2. It distributes any amount of income;

3. Distribution is to its investors

Consequence:

1. Income Distributed by the securitization trust shall be chargeable to tax

2. Such securitization trust shall be liable to pay additional income-tax on such distributed

income at the rates mentioned in s. 115TA(1);

Jagdish T Punjabi June 25, 2014

50

Provisions dealing with Securitisation Trust…

Rates of tax :

The rate of tax depends upon the legal status of the investor.

If the investor is an individual or a hindu undivided family the rate is 25%; and

In case the investor is any other person then the rate is 30%.

Exception: Tax under this section is not payable if the income is distributed by securitization

trust to any person in whose case income, irrespective of its nature and source, is not

chargeable to tax under the Act.

The responsibility for payment of tax is on the person responsible for making payment of

income distributed by the securitization trust. Tax has to be paid to the Central Government

within 14 days of the date of distribution or payment of such income, whichever is earlier.

On or before 15th of September a statement is required to be furnished to the prescribed

income-tax authority. The statement is required to be in the prescribed form and in the

prescribed manner and should give details of amount of income distributed to investors

during the previous year, the tax paid thereon and such other relevant details as may be

prescribed. This statement is to be furnished by the person responsible for making payment

of the income distributed by the securitization trust.

Jagdish T Punjabi June 25, 2014

51

Transactions with Cyprus, being a non co-operative tax jurisdiction.

Cyprus has been notified as a non-co-operative tax jurisdiction. Consequently, every

transaction entered into by the assessee with

a) a person who is resident of Cyprus; or

b) a person (not being an individual) is established in Cyprus; or

c) a permanent establishment of a person not falling in (a) or (b) is in Cyprus.

Shall be deemed to be an international transaction; and

all the parties to the transaction of the assessee with any of the above mentioned persons

will be deemed to be associated enterprises within the meaning of s. 92A; and

transfer pricing provisions shall apply.

Deduction in respect of any payment made by the assessee to any financial institution

located in Cyprus shall be allowed only if assessee furnishes an authorization from the said

financial institution authorizing the board or any other income-tax authority acting on its

behalf to seek relevant information from the said financial institution on behalf of the

assessee.

If any sum is received by the assessee from any person located in Cyprus then the onus

would be on the assessee to prove the source of such sum in the hands of such person or in

the hands of the beneficial owner. In case of failure to do so, the amount shall be deemed to

be income of the assessee.

Jagdish T Punjabi June 25, 2014

52

Transactions with Cyprus, being a non co-operative tax jurisdiction….

Any payment made to a person located in Cyprus which is liable to TDS shall be subjected to

TDS at the highest of the following rates –

a. at the rate or rates in force;

b. at the rate specified in the relevant provisions of this Act;

c. at the rate of thirty percent.

Information required to furnish return of income which may not be readily available in the

financial statements and computation of total income.

Jagdish T Punjabi June 25, 2014

53

Amendments to Forms of Return of

Income for Assessment Year

2014-15

Jagdish T Punjabi June 25, 2014

54

Changes in FormsCommon changes

Suitable changes have been made to incorporate the claim for deduction under section 80EE

and also rebate under section 87A.

If the return being filed is a Modified Return under section 92CD or a return in response to a

notice treating the return as defective then in filing status the relevant information has to be

given i.e. ―Modified Return – 92CD‖ or ―139(9) – Defective,‖

If the return is being filed in response to notice under s. 139(9), 142(1), 148, 153A or 153C –

the date of notice or date of advance pricing agreement is to be stated.

Mention is required to be made if assessee has made any transaction with a person located

in a jurisdiction notified u/s 94A of the Act. (ITR 3, 4, 5, 6, 7)

While section 32AC has been introduced for companies w.e.f. AY 2014-15 there is no

separate cell for filling in the amount of deduction claimed under this section. Therefore, this

will have to be reflected in Form 6 in the cell for ―Other Deductions‖.

In form ITR IV the Trade Name of proprietary concerns needs to be mentioned. Earlier this

was not required.

Schedule BBS : Details of tax on distributed income of a domestic company on buy back of

shares, not listed on stock exchange has been added.

Jagdish T Punjabi June 25, 2014

55

Changes in Forms...In Schedule of TDS break up has to be given deductor wise in respect of Unclaimed TDS

brought forward (this is to be financial year-wise i.e. two columns financial year in which

deducted and amount b/fd). This will mean, wherever there is TDS brought forward from

earlier years which is to be claimed in the current year or is to be carried forward to the

subsequent year, one will have to find out Unique TDS certificate number and also the

financial year in which TDS which has been brought forward was deducted. Corresponding

changes have also been made for TCS.

Throughout the forms where two separate cells were earlier required for Name and Address,

now a common cell has been provided for Name and Address. This change to a certain

extent will obviate the difficulty of form not getting validated if either of the two cells was not

filled in.

For LLP and Companies LLPIN and CIN have to be stated.

In respect of partners / directors their DPIN / DIN is required to be mentioned.

Amounts claimed u/s 10A or 10AA were earlier to be deducted in Schedule BP : Computation

of Income from business or profession. Now the same are to be deducted after Gross Total

Income in Part B – TI – Computation of Total Income.

Refund will now be granted only by credit to bank account.

In case of Companies if profit & loss account is not prepared in accordance with the

provisions of Part II of Schedule VI to the Companies Act, whether it is prepared in

accordance with the provisions of the Act governing such company?

.Jagdish T Punjabi June 25, 2014

56

Changes in Forms…

Assessees who are required to furnish report under section 92E and / or s. 115JC are

required to state date of furnishing of such reports.

In ITR -5 in status a new category viz. ―Private discretionary trust‘ has been added.

In respect of returns to be filed by Trusts in ITR-7

In addition to the name of the project / institution and nature of activity the form now requires

mention of registration number, registering authority and section under which it is claiming

exemption in respect of the project / institution being run by it.

Accumulation of income for future application has to be reported in the form.

Schedule VC : Voluntary contributions has been inserted for reporting various voluntary

donations received by a trust. Donations are now to be reported along with their nature and

quantum as under –

Local voluntary donations (corpus and non-corpus)

Foreign contributions (corpus and non-corpus)

Anonymous donations

Jagdish T Punjabi June 25, 2014

57

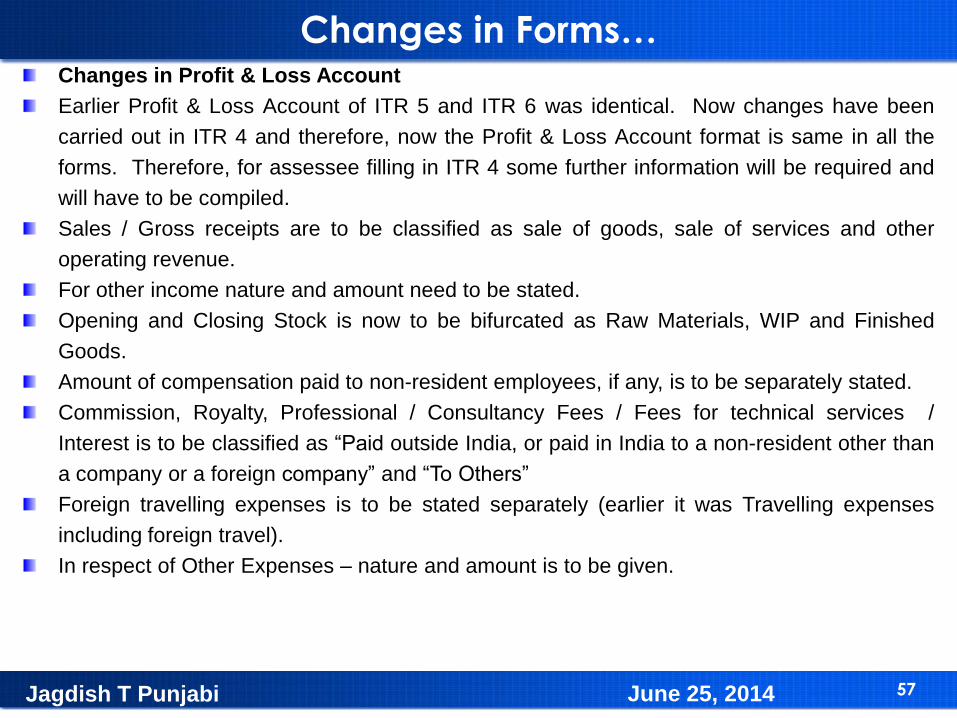

Changes in Forms…Changes in Profit & Loss Account

Earlier Profit & Loss Account of ITR 5 and ITR 6 was identical. Now changes have been

carried out in ITR 4 and therefore, now the Profit & Loss Account format is same in all the

forms. Therefore, for assessee filling in ITR 4 some further information will be required and

will have to be compiled.

Sales / Gross receipts are to be classified as sale of goods, sale of services and other

operating revenue.

For other income nature and amount need to be stated.

Opening and Closing Stock is now to be bifurcated as Raw Materials, WIP and Finished

Goods.

Amount of compensation paid to non-resident employees, if any, is to be separately stated.

Commission, Royalty, Professional / Consultancy Fees / Fees for technical services /

Interest is to be classified as ―Paid outside India, or paid in India to a non-resident other than

a company or a foreign company‖ and ―To Others‖

Foreign travelling expenses is to be stated separately (earlier it was Travelling expenses

including foreign travel).

In respect of Other Expenses – nature and amount is to be given.

Jagdish T Punjabi June 25, 2014

58

Changes in Forms…

Changes in Profit & Loss Account….

In respect of Bad Debts – in respect of each person for whom bad debt is Rs. 1 lakh or more

PAN is required to be stated. In respect of persons where amount is more than Rs 1lakh but

PAN is not available such cases are to be aggregated and aggregate amount is to be

mentioned. For bad debts of less than Rs 1 lakh aggregate is to be stated as Others

(amounts less than Rs. 1 lakh).

Jagdish T Punjabi June 25, 2014

59

Changes in Forms….

Changes in Other Information

The following are now required to be stated -

Amount of contribution to a pension scheme referred to in s. 80CCD.

Securities transaction tax paid in respect of transaction in securities if such income is

not included in business income.

Expenditure of capital nature not allowable u/s 37.

Expenditure laid out or expended wholly and exclusively NOT for the purpose of

business or profession not allowable u/s 37.

Amount paid by way of royalty, license fee, service fee, etc, as per s. 40(a)(iib).

Earlier disallowance u/s 40(a)(i), (ia) and (iii) a consolidated amount was required to be

stated – now separate amounts are to be stated clause wise i.e. 40(a)(i), 40(a)(ia), 40(a)(iii)

In case company has recognized provident fund – information needs to be given about total

number of employees – bifurcated into deployed in India and deployed outside India. (ITR 4,

5, 6, 7)

Jagdish T Punjabi June 25, 2014

60

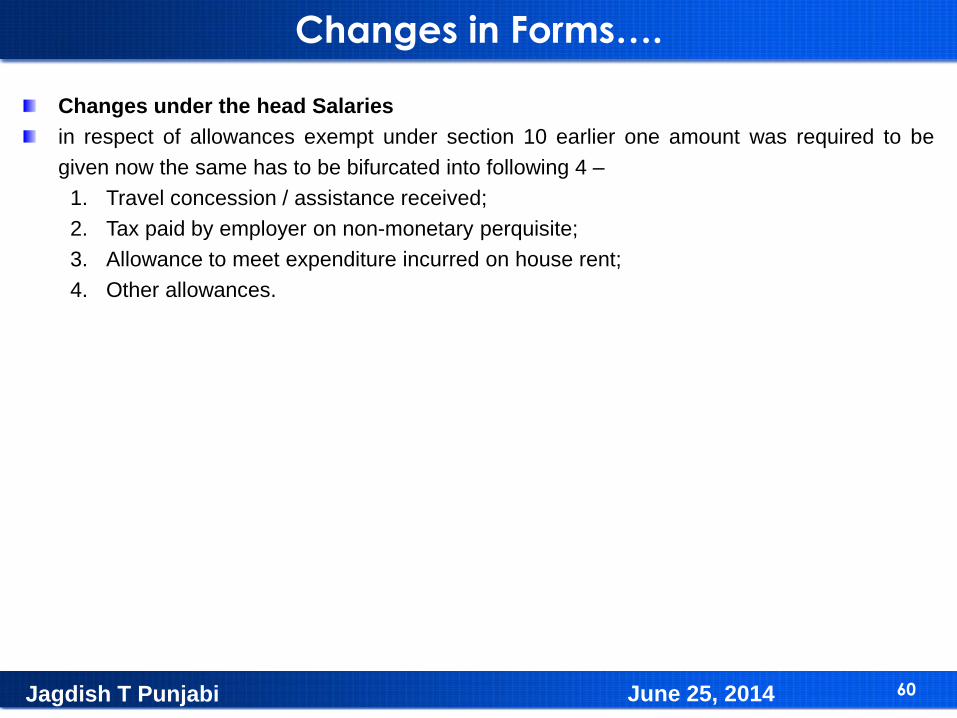

Changes in Forms….

Changes under the head Salaries

in respect of allowances exempt under section 10 earlier one amount was required to be

given now the same has to be bifurcated into following 4 –

1. Travel concession / assistance received;

2. Tax paid by employer on non-monetary perquisite;

3. Allowance to meet expenditure incurred on house rent;

4. Other allowances.

Jagdish T Punjabi June 25, 2014

61

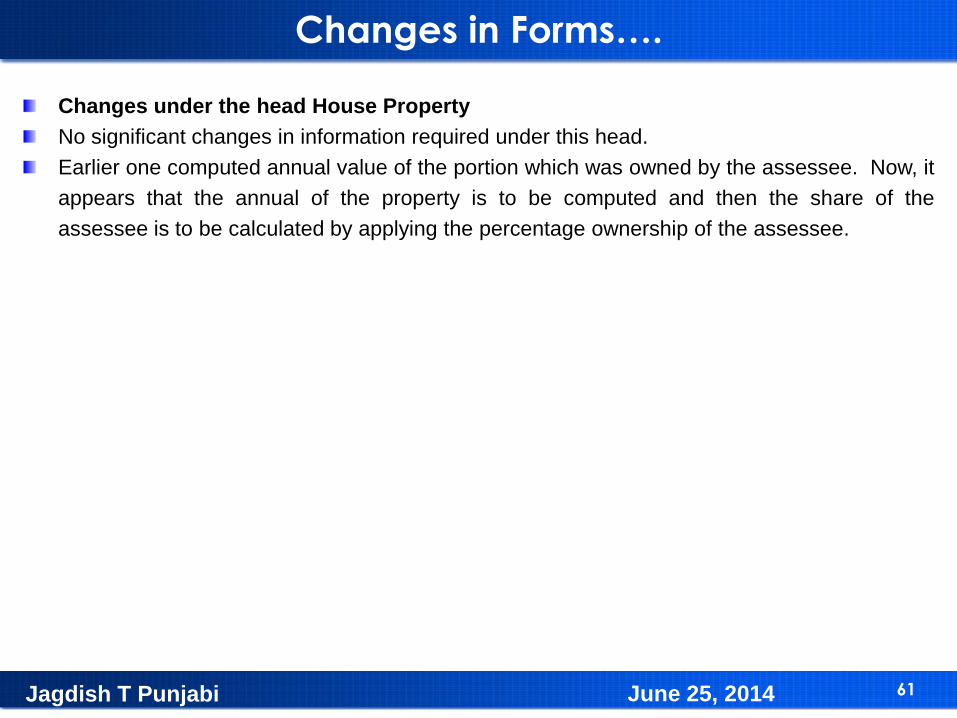

Changes in Forms….

Changes under the head House Property

No significant changes in information required under this head.

Earlier one computed annual value of the portion which was owned by the assessee. Now, it

appears that the annual of the property is to be computed and then the share of the

assessee is to be calculated by applying the percentage ownership of the assessee.

Jagdish T Punjabi June 25, 2014

62

Changes in Forms….

Changes under the head Business Income

Items of income credited to P & L but considered under other heads – here one has to now

mention the head under which the amount being deducted has been considered – Salaries,

House property, Capital gains, Other sources.

For each item of Exempt income credited to P & L – nature and amount need to be specified

Items of expenses debited to P & L but considered under other heads – here one has to now

mention the head under which the amount being deducted has been considered – Salaries,

House property, Capital gains, Other sources.

Intra head set off of business loss has to be stated – i.e. business loss set off against income

speculative business and Income from specified business.

Deemed income under section 43CA has to be stated.

Jagdish T Punjabi June 25, 2014

63

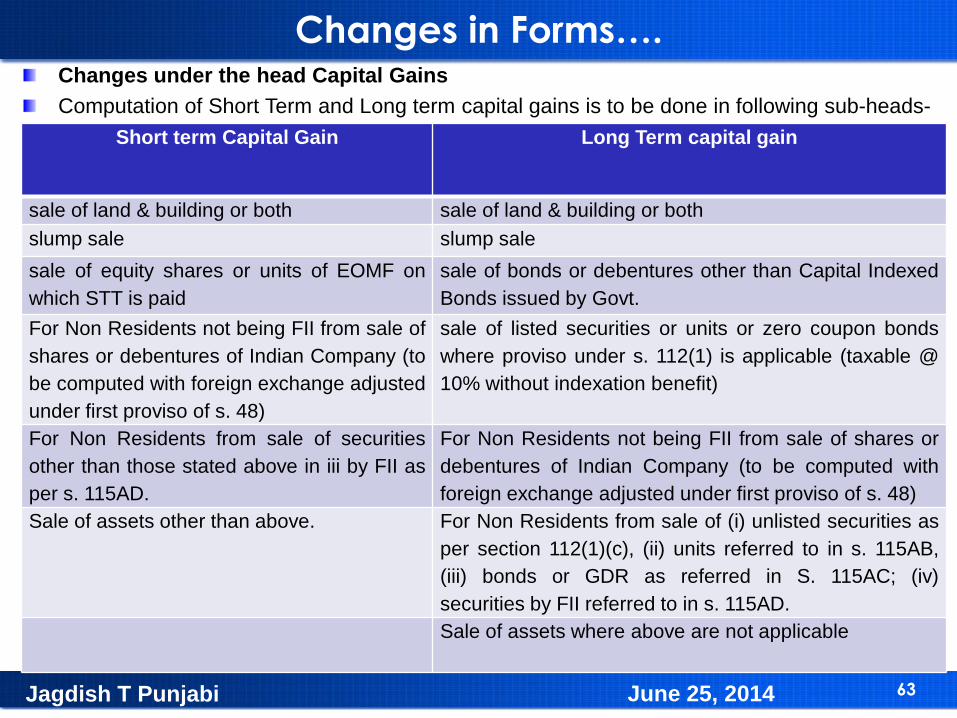

Changes in Forms….Changes under the head Capital Gains

Computation of Short Term and Long term capital gains is to be done in following sub-heads-

Jagdish T Punjabi June 25, 2014

Short term Capital Gain Long Term capital gain

sale of land & building or both sale of land & building or both

slump sale slump sale

sale of equity shares or units of EOMF on

which STT is paid

sale of bonds or debentures other than Capital Indexed

Bonds issued by Govt.

For Non Residents not being FII from sale of

shares or debentures of Indian Company (to

be computed with foreign exchange adjusted

under first proviso of s. 48)

sale of listed securities or units or zero coupon bonds

where proviso under s. 112(1) is applicable (taxable @

10% without indexation benefit)

For Non Residents from sale of securities

other than those stated above in iii by FII as

per s. 115AD.

For Non Residents not being FII from sale of shares or

debentures of Indian Company (to be computed with

foreign exchange adjusted under first proviso of s. 48)

Sale of assets other than above. For Non Residents from sale of (i) unlisted securities as

per section 112(1)(c), (ii) units referred to in s. 115AB,

(iii) bonds or GDR as referred in S. 115AC; (iv)

securities by FII referred to in s. 115AD.

Sale of assets where above are not applicable

64

Changes in Forms….

Changes under the head Capital Gains…

In respect of deduction claimed under Ss. 54B, 54D, 54EC, 54F, etc. for each section under

which deduction is claimed one has to state Cost of new asset, date of its acquisition,

amount deposited under capital gains account scheme before due date. Here one will have

to take a call on date of acquisition where a flat under construction has been booked.

In schedule for set off of current years capital losses against gains short term capital gain

has to be classified as 15%, 30%, applicable rate and LTCG as 10% and 20%.

Information about accrual/receipt of capital gain has to be given rate wise into 5 categories

i.e. STCG 15%, 30%, applicable rate and LTCG as 10% and 20%.

Jagdish T Punjabi June 25, 2014

65

Changes in Forms….

Changes under the head Other Sources

Total income from other sources has to be bifurcated as chargeable at special rates and

chargeable at normal rates. Within items chargeable at special rates the bifurcation is

between income by way of winning from lotteries, crossword puzzles, races, games,

gambling, betting, etc (u/s 115BB) and Any other income under Chapter XII/XII-A.

Jagdish T Punjabi June 25, 2014

66

Changes in Forms….

Other Changes:

In respect of allowance u/s 35(4) following information has to be provided in Schedule UD :

Unabsorbed depreciation and allowance under section 35(4).

1. Amount of brought forward unabsorbed allowance

2. Amount of brought forward unabsorbed allowance

3. Balance carried forward to next year.

In respect of deductions under s. 10A and 10AA for each undertaking one has to now

mention assessment year in which the unit began to manufacture / produce / provide service.

In respect of Deductions under section 80IA, 80IB, 80IC and 80IE the amount of deduction

claimed for each undertaking has to be separately stated as against a consolidated amount

which was required to be mentioned earlier.

In information regarding partnership firms in which the assessee is a partner now against the

name of each of the firms it is also required to be stated whether the firm is liable for audit?

(ITR 4 – Schedule IF)

Jagdish T Punjabi June 25, 2014

67

Information required to furnish return of income which may not be readily available

in the financial statements and computation of total income.

Date of birth of the assessee / date of formation.

Phone number

Email id

Date of furnishing of tax audit report

Name of auditor signing the report

Membership number of the auditor

PAN of the auditor

In case of LLP / company – LLPIN / CIN

DPIN / DIN of designated partners of LLP and directors of company

Details of bank account – account number, IFSC code, type of account i.e. savings / current /

cash credit

Name of employer, PAN of employer

Address of properties owned by the assessee

Assessee‘s percentage of share in the property

Name of co-owner, PAN of co-owner, Percentage share in property of each co-owner

Name of tenant, PAN of tenant (optional)

Brought forward losses if losses as assessed are different from losses as returned

Adjustments, if any, required to be made to WDV as a consequence of disallowance of

certain expenditure on the ground that it is capital in nature or otherwise.

Date of furnishing of report under Ss. 92E, 115JB, 115JC, wherever applicable

Stamp Duty Value of land or building transferredJagdish T Punjabi June 25, 2014

68

Information required to furnish return of income which may not be readily available

in the financial statements and computation of total income...

Assessment year in which each of the units located in SEZ began to manufacture / produce

(where deduction is being claimed u/s 10A / 10AA.

Name and address and PAN of each of the donees to whom donation has been given and

deduction under s. 80G is to be claimed.

TDS brought forward from earlier years with details of financial year in which it was

deducted, certificate number and the amount.

In case assessee is a partner in a firm / LLP – name of the firm where he is a partner, PAN of

the firm, his profit sharing ratio, his capital balance in the firm as on 31st March.

Particulars of persons who were beneficial owners of shares holding not less than 10% of the

voting power at any time during the previous year – Name and Address, percentage of

shares held, PAN.

In case the assessee is a settlor, beneficiary or a trustee in a trust created outside India

details required for Schedule FA: Foreign Assets viz. Country Name, country code, name

and address of the trust, name and address of trustees, name and address of settlor and

name and address of beneficiaries.

Details of foreign bank accounts along with peak balance during the year (in Rupees)

Following information is required in Balance Sheet / P & L / Other Information :

Foreign currency loans (classified into secured and unsecured)(in case of ITR-5)

Unsecured rupee loans from persons specified in s. 40(A)(2)(b).

Advances from persons specified in s. 40(A)(2)(b)

Jagdish T Punjabi June 25, 2014

69

Information required to furnish return of income which may not be readily available

in the financial statements and computation of total income...

Debtors outstanding for more than one year

Loans and advances for the purpose of business or profession

Loans and advances not for the purpose of business or profession

Creditors outstanding for more than one year

Interest accrued and due on borrowings

Interest accrued but not due on borrowings

Income received in advance

Compensation to employees classified as –

a. Salaries and wages b. Bonus

c. Reimbursement of medical expenses

d. Leave encashment

e. Leave travel benefits

f. Contribution to approved superannuation fund

g. Contribution to recognized provident fund

h. Contribution to recognized gratuity fund

i. Contribution to any other fund

j. Any other benefit to employees in respect of which an expenditure has been incurred

k. Total compensation to employees (total of a to j above)

l. Whether any compensation included above is paid to non-residents

m. If yes, amount paid to non-residents.

Jagdish T Punjabi June 25, 2014

70

Information required to furnish return of income which may not be readily available

in the financial statements and computation of total income...

Following payments made outside India or paid in India to a non-resident

Commission

Royalty

Professional / Consultancy fees

Interest

Insurance classified as –

a Medical Insurance

b Life Insurance

c Keyman‘s Insurance

d Other Insurance including factory, office, car, goods, etc.

PAN of debtors from whom amounts in excess of Rs. 1 lakh has been written off

Aggregate amount of debtors written off (each amount being in excess of Rs. 1 lakh) for

which PAN is not available

Aggregate amount of bad debts written off where each amount is less than Rs 1 lakh.

Guest House expenses

Conference

Sales promotion including publicity (including advertisement)

Advertisement

Foreign Travelling Expenses

Hotel, boarding and lodging

Jagdish T Punjabi June 25, 2014

71

Information required to furnish return of income which may not be readily available

in the financial statements and computation of total income...

Festival celebration expenses

Entertainment

Hospitality

Where an assessee is on inclusive method of recording purchases, etc following information

may not be readily available in financial statements –

Duties and taxes paid or payable in respect of goods and services purchased

i. Customs duty

ii. Counterveiling duty

iii. Special additional duty

iv. Union excise duty

v. Service tax

vi. VAT / Sales tax

vii. Any other tax paid or payable

Rates and taxes, paid or payable to Government or any local body (excluding taxes on

income)

i. Union excise duty

ii. Service tax

iii. VAT / Sales tax

iv. Cess

v. Any other rate, tax, duty or cess including STT and CTT

Jagdish T Punjabi June 25, 2014

72

e-Filing process for online filing of ITR Form

Jagdish T Punjabi June 25, 2014

73

Select appropriate type of Return Form .

Download Return Preparation Software for selected Return Form.

Fill your return offline and generate a XML file.

Register and create a user id/password .

Login and click on relevant form on left panel and select "Submit Return".

Browse to select XML file and click on "Upload" button .

On successful upload acknowledgement details would be displayed. Click on "Print" to

generate printout of acknowledgement/ITR-V Form.

Incase the return is digitally signed, on generation of "Acknowledgement" the Return

Filing process gets completed. Assessee may take a printout of the Acknowledgement for his

record.

Incase the return is not digitally signed, on successful uploading of e-Return, the ITR-V

Form would be generated which needs to be printed by the tax payers. This is an

acknowledgement cum verification form. The tax payer has to fill-up the verification part and

verify the same. A duly verified ITR-V form should be submitted with the Income Tax

Bangalore Office within 30 days of filing electronically. This completes the Return filing

process for non-digitally signed Returns.

Jagdish T Punjabi June 25, 2014

e-Filing process for offline filing of ITR Form

74

How to e-file?Steps to file form offline

Download the applicable ITR form from Downloads

Fill it offline

Generate XML

Register on e-filing website using your PAN.

LOGIN to the portal

Go to e-File link – Upload Return

OR

LOGIN to Prepare and Submit ITR Online

Jagdish T Punjabi June 25, 2014

75

Jagdish T Punjabi

B.Com., B.G.L., FCA.

June 25, 2014