ind as 16 property, plant & equipment - ctconline.org · property plant & equipment – ind...

TRANSCRIPT

Page 1

Ind AS 16Property, Plant & Equipment

CA Hemal D Shah

Page 2 PPE and other related standards

1. Property Plant & Equipment - Ind AS 162. Government Grant – Ind AS 20

Contents

Page 3 PPE and other related standards

Property Plant & Equipment – Ind AS 16

► Measurement

► Depreciation

► Component Accounting

► Site Restoration & Decommissioning Obligations

► Non Current Assets Held for Sale – Ind AS 105

► Indian GAAP vs. Ind AS

► Ind AS vs. IFRS

► Related Exemptions under Ind AS 101

► Issues discussed by Ind AS Facilitation Transition Group

Page 4 PPE and other related standards

Measurement – At Recognition

► An item of property, plant and equipment that qualifies for recognition as an asset shallbe measured at its cost.

The cost of an item of property, plant and equipment comprises:

► Net purchase price.

► directly attributable costs for bringing the asset to the location and condition

► Site Restoration obligation

Page 5 PPE and other related standards

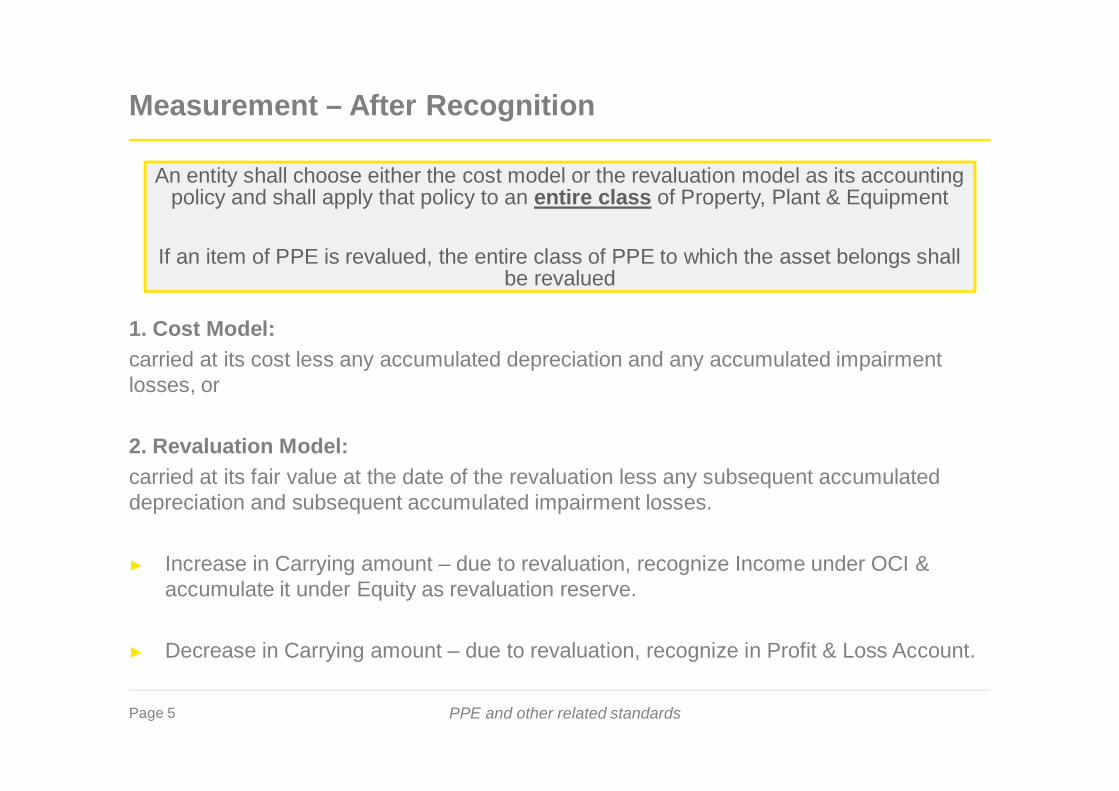

Measurement – After Recognition

1. Cost Model:carried at its cost less any accumulated depreciation and any accumulated impairmentlosses, or

2. Revaluation Model:carried at its fair value at the date of the revaluation less any subsequent accumulateddepreciation and subsequent accumulated impairment losses.

► Increase in Carrying amount – due to revaluation, recognize Income under OCI &accumulate it under Equity as revaluation reserve.

► Decrease in Carrying amount – due to revaluation, recognize in Profit & Loss Account.

An entity shall choose either the cost model or the revaluation model as its accountingpolicy and shall apply that policy to an entire class of Property, Plant & Equipment

If an item of PPE is revalued, the entire class of PPE to which the asset belongs shallbe revalued

Page 6 PPE and other related standards

► Spare parts and servicing equipment are usually carried as inventory and recognisedin profit or loss as consumed except:

§ Major spare parts and stand-by equipment with expected use during more thanone period

§ Spare parts and servicing equipment which can only be used in connection withan item of PPE

► Replacements which leads a capital asset to its full productive capacity or acontribution after damage, accident, or prolonged use, without increase in itspreviously estimated service life or productive capacity.§ Should be charged to profit & loss as and when incurred.

► Improvements or betterments leading to increase in estimated service life orproductive capacity.§ Should be capitalized

► Cost of new component purchased for replacement will be capitalized anddepreciated over the period not exceeding the useful life of the principal asset.

MeasurementSpare parts and Replacement costs

Page 7 PPE and other related standards

Depreciation

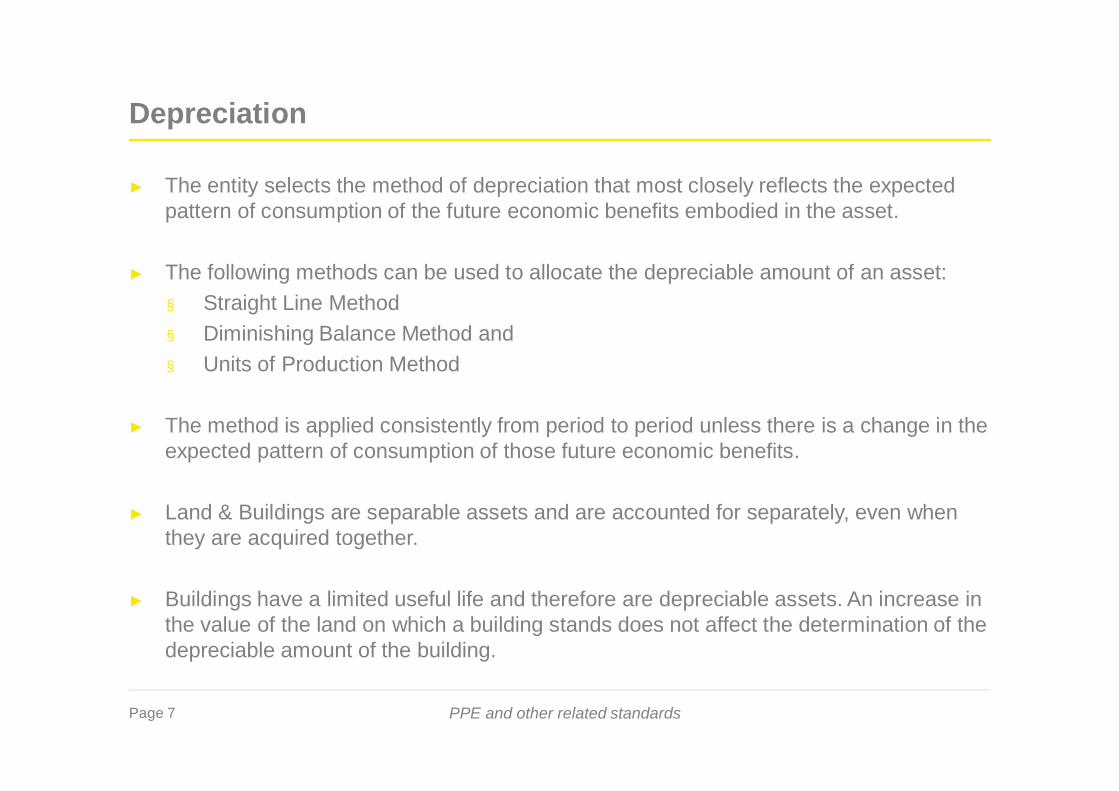

► The entity selects the method of depreciation that most closely reflects the expectedpattern of consumption of the future economic benefits embodied in the asset.

► The following methods can be used to allocate the depreciable amount of an asset:§ Straight Line Method§ Diminishing Balance Method and§ Units of Production Method

► The method is applied consistently from period to period unless there is a change in theexpected pattern of consumption of those future economic benefits.

► Land & Buildings are separable assets and are accounted for separately, even whenthey are acquired together.

► Buildings have a limited useful life and therefore are depreciable assets. An increase inthe value of the land on which a building stands does not affect the determination of thedepreciable amount of the building.

Page 8 PPE and other related standards

► Cost of each significant item of PPE to be recognised separately which havingdifferent useful life

► Item of PPE means parts having a cost that is significant to total cost

► Identification of such parts required to recognise replacement cost, if required

Ship costs 150, useful life 10 years,Estimated docking cost 15, planned after 3 years

Component 1Cost: 135

Life: 10 years

Component 2Cost: 15

Life: 3 yearsCapitalise as

incurred

Total ShipCost150

Example :

Component accounting

Page 9 PPE and other related standards

Componentization- key considerations

Componentization

Materiality/Significant

components

Useful life ofcomponents

Replacementcosts

Major inspection/Overhaul

Page 10 PPE and other related standards

Componentization- key considerationsMateriality/Significant components

► Identification of material/ significant components separately may involve complexjudgement. Item may not be material in a particular year become so in later years.

► Materiality is a matter of management and needs to be decided on the facts of eachcase.

► Consider impact on

§ retained earnings

§ current year profit or loss

§ future profit or loss

to decide materiality. Component with material impact will require separateidentification.

Page 11 PPE and other related standards

► Each significant component of the asset having useful life, which is different from theuseful life of the remaining asset, is depreciated separately.

*higher useful life for a component can be used only when management intends to usethe component even after expiry of useful life for the principal asset.

Componentization- key considerationsUseful life of components

► Useful life of component < Useful life of principalasset

= Consider lower life

► Management’s estimateof useful life

< Statute = Consider lower life

► Useful life of thecomponent

> Useful life of the principalasset

= Option to use either thehigher or lower useful life*

Page 12 PPE and other related standards

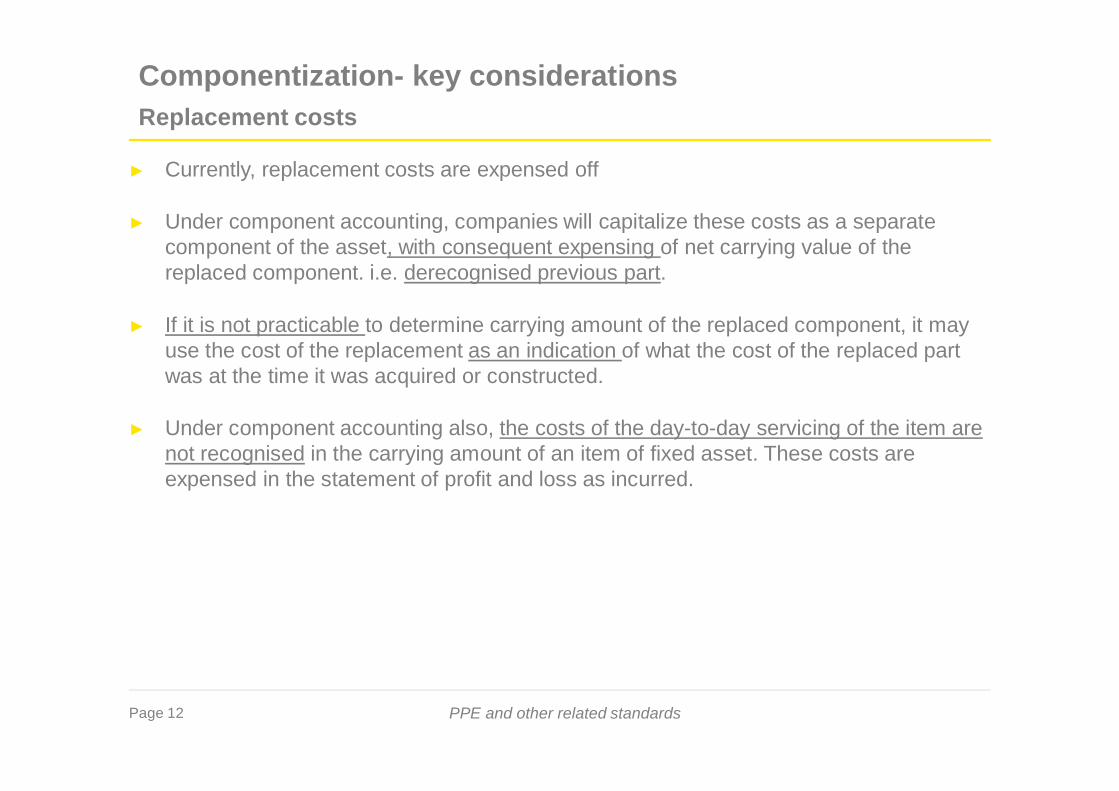

► Currently, replacement costs are expensed off

► Under component accounting, companies will capitalize these costs as a separatecomponent of the asset, with consequent expensing of net carrying value of thereplaced component. i.e. derecognised previous part.

► If it is not practicable to determine carrying amount of the replaced component, it mayuse the cost of the replacement as an indication of what the cost of the replaced partwas at the time it was acquired or constructed.

► Under component accounting also, the costs of the day-to-day servicing of the item arenot recognised in the carrying amount of an item of fixed asset. These costs areexpensed in the statement of profit and loss as incurred.

Componentization- key considerationsReplacement costs

Page 13 PPE and other related standards

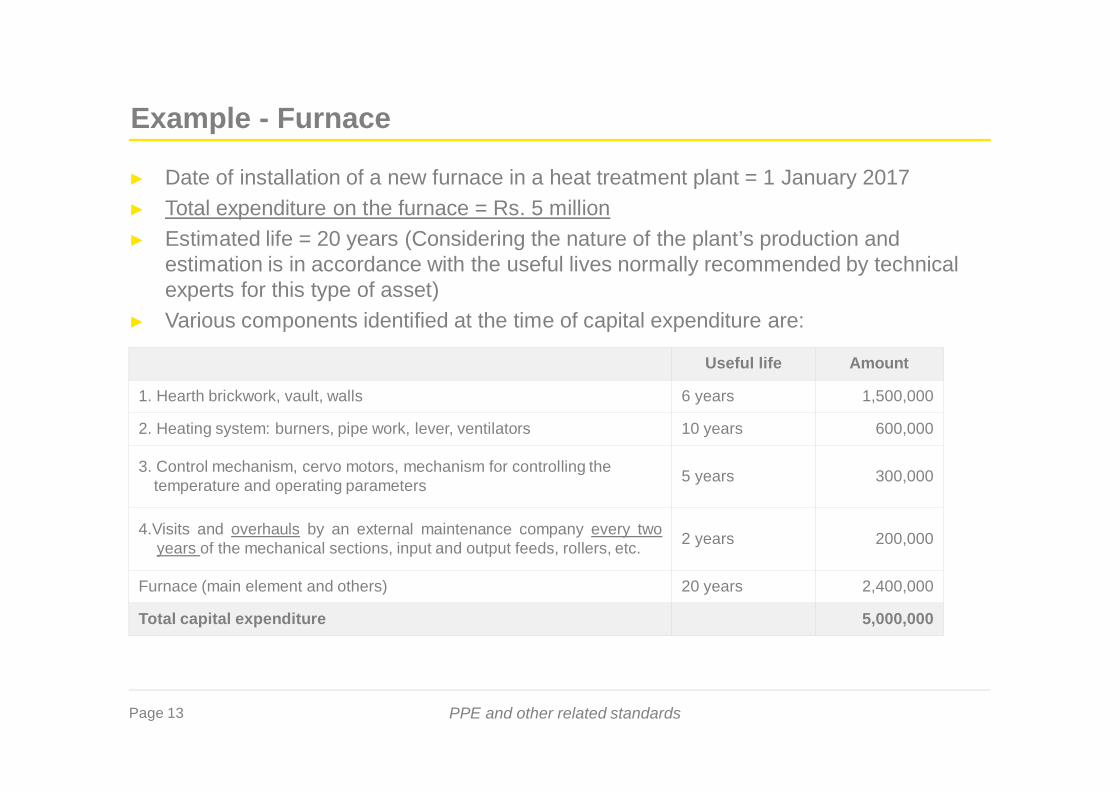

Example - Furnace

► Date of installation of a new furnace in a heat treatment plant = 1 January 2017► Total expenditure on the furnace = Rs. 5 million► Estimated life = 20 years (Considering the nature of the plant’s production and

estimation is in accordance with the useful lives normally recommended by technicalexperts for this type of asset)

► Various components identified at the time of capital expenditure are:

Useful life Amount

1. Hearth brickwork, vault, walls 6 years 1,500,000

2. Heating system: burners, pipe work, lever, ventilators 10 years 600,000

3. Control mechanism, cervo motors, mechanism for controlling thetemperature and operating parameters 5 years 300,000

4.Visits and overhauls by an external maintenance company every twoyears of the mechanical sections, input and output feeds, rollers, etc. 2 years 200,000

Furnace (main element and others) 20 years 2,400,000

Total capital expenditure 5,000,000

Page 14 PPE and other related standards

Site restoration and decommissioning obligations

Ø Where the effect of the time value ofmoney is material, the amount of a provisionshall be at discounted value.

Ø The periodic unwinding of the discount shall berecognized in profit or loss as a finance cost as itoccurs. The same cannot be capitalized under IndAS 23.

Ø The associated decommissioning costsshould also be capitalized

Ø It should form part of the cost of the assetsacquired or constructed

Ø It may also be necessary to recognise afurther decommissioning provision duringthe production phase

Recognised at the time of initial recognition of PPE Requires significant judgment due to:Ø Dependency on scale of operations,Ø Environmental damage caused,Ø Uncertainty regarding timing of

decommissioning,Ø Costs which may be directly attributable to

decommissioning etc.

MeasurementRecognition

SiteRestoration and

DecommissioningObligations

Discounting Accounting

Page 15 PPE and other related standards

► The facts relevant to well are summarized below:

► Cost

► Decommissioning costs = INR 14000

► Discount rate = 10%

► Net present value = INR 800

► Period = 30

► Show accounting treatment of site restoration and decommissioning obligation.

Response:

► Management should include INR 800 in the carrying amount of the asset at the time of installationand corresponding provision with equivalent amount.

► Each year an adjustment is made for the amount of borrowing cost; calculated as the currentbalance of provision multiplied by the discount rate

§ Year 1 - INR 800*10% = INR 80

§ Year 2 - INR (800 + 80)*10% = INR 88 and similarly for the rest of the years

Site restoration and decommissioning obligationsCase study

Page 16 PPE and other related standards

Response (Contd.):

► Entries:§ Recognition of decommissioning costs while recognising asset

PPE-Dr 800Provisions decommissioning-Cr 800

§ Year1 for interestInterest expense –Dr 80Provisions decommissioning-Cr 80

§ Year 30 for interestInterest expense – Dr 1273Provisions decommissioning-Cr 1273

Site restoration and decommissioning obligationsCase study (Contd.)

Year Opening balance-Provision Interest @10% Closing balance-Provision

1 800 80 880

2 880 88 968

…

30 12727 1273 14000

Page 17 PPE and other related standards

Non-current assets held for sale - Ind AS 105

► For an asset to be classified as held for sale:

► Recognition* : Lower of carrying amount and fair value less costs to sell.

► Although Interest and other expenses attributable to the liabilities of a disposal group classified asheld for sale should continue to be recognized, such assets should not be depreciated/ amortized.

► Impairment:

§ Requirement to measure a non-current asset at the lower of carrying amount and fair valueless costs to sell may give rise to a write down in value (impairment loss).

§ Any subsequent increase in fair value less costs to sell of an asset up to the cumulativeimpairment loss previously recognized should be recognized as a gain.

*When the sale is expected to occur beyond one year, the costs to sell should be measured at their present value. Andincrease in present value due to passage of time shall be charged to profit and loss.

Non-current assets held for sale are ‘those assets whose carrying amount will be recoveredprincipally through a sale transaction rather than through continuing use’.

Must be available for immediatesale in its present condition

Must genuinely be sold, notabandoned

Sale must be highly probable

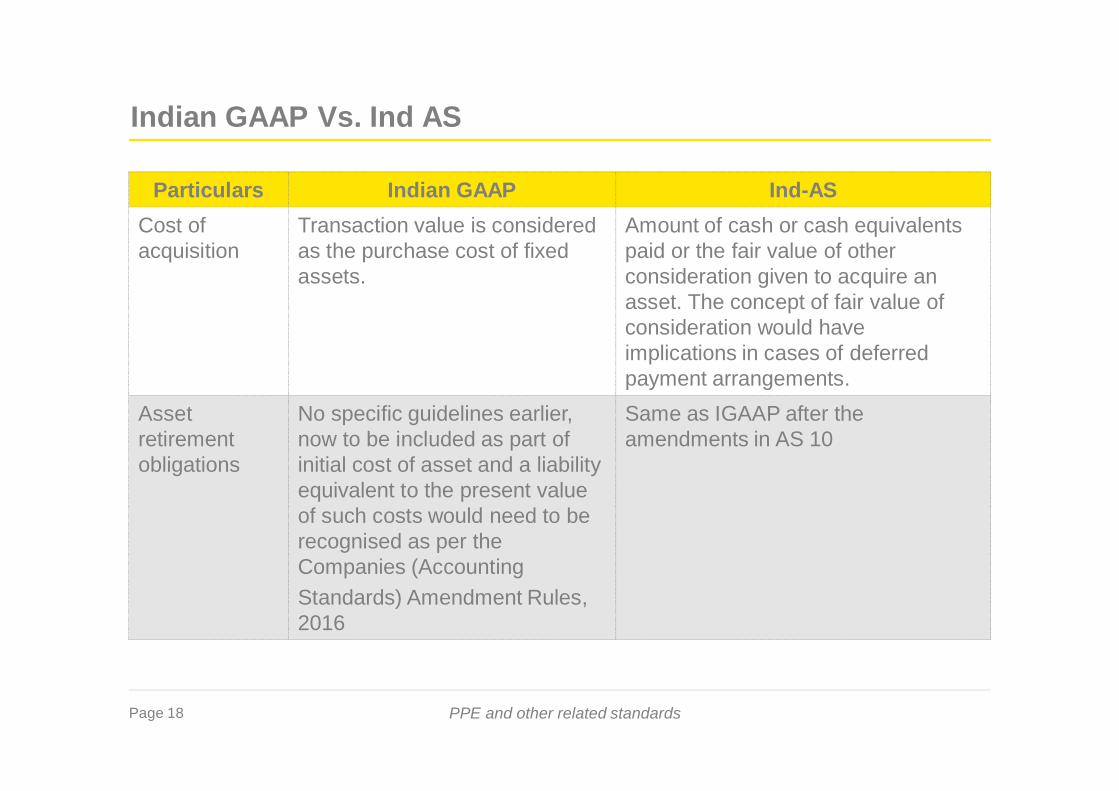

Page 18 PPE and other related standards

Indian GAAP Vs. Ind AS

Particulars Indian GAAP Ind-ASCost ofacquisition

Transaction value is consideredas the purchase cost of fixedassets.

Amount of cash or cash equivalentspaid or the fair value of otherconsideration given to acquire anasset. The concept of fair value ofconsideration would haveimplications in cases of deferredpayment arrangements.

Assetretirementobligations

No specific guidelines earlier,now to be included as part ofinitial cost of asset and a liabilityequivalent to the present valueof such costs would need to berecognised as per theCompanies (AccountingStandards) Amendment Rules,2016

Same as IGAAP after theamendments in AS 10

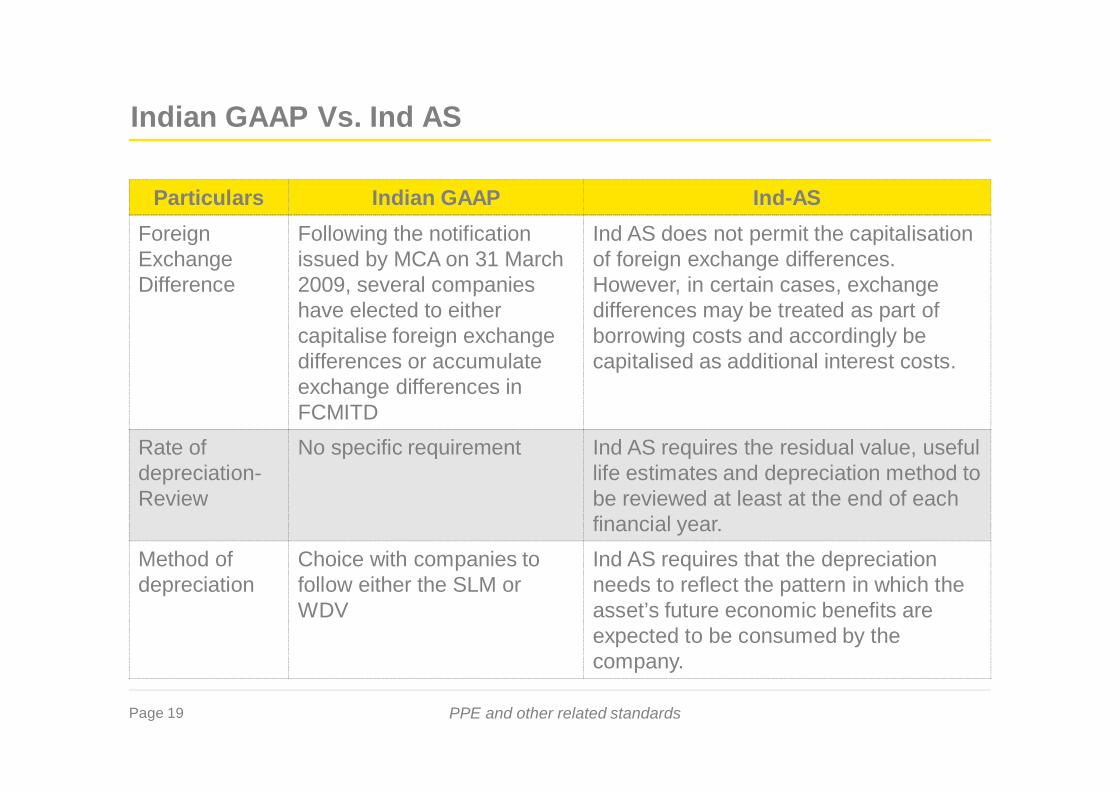

Page 19 PPE and other related standards

ForeignExchangeDifference

Following the notificationissued by MCA on 31 March2009, several companieshave elected to eithercapitalise foreign exchangedifferences or accumulateexchange differences inFCMITD

Ind AS does not permit the capitalisationof foreign exchange differences.However, in certain cases, exchangedifferences may be treated as part ofborrowing costs and accordingly becapitalised as additional interest costs.

Rate ofdepreciation-Review

No specific requirement Ind AS requires the residual value, usefullife estimates and depreciation method tobe reviewed at least at the end of eachfinancial year.

Method ofdepreciation

Choice with companies tofollow either the SLM orWDV

Ind AS requires that the depreciationneeds to reflect the pattern in which theasset’s future economic benefits areexpected to be consumed by thecompany.

Particulars Indian GAAP Ind-AS

Indian GAAP Vs. Ind AS

Page 20 PPE and other related standards

Particulars Indian GAAP Ind-ASSubstantialperiod oftimedefinition

A period of 12 months isordinarily considered as asubstantial period of time,unless a shorter or longerperiod can be justified.

No bright line rules for determining whatconstitutes ‘a substantial period of time’.

Interestexpenses

Contractual interest expense isconsidered as a part ofborrowing costs.

Under Ind AS, the amount of interestexpense to be included as borrowingcosts is based on the effective interestrate method.

Borrowingrate

Borrowing costs are capitalisedbased on company levelborrowings and no separateadjustments are made tocompute group borrowing rate.

Ind AS requires that the consolidatedgroup’s average borrowing rate needs tobe considered for capitalisation ofgeneral borrowing costs.

Indian GAAP Vs. Ind AS

Page 21 PPE and other related standards

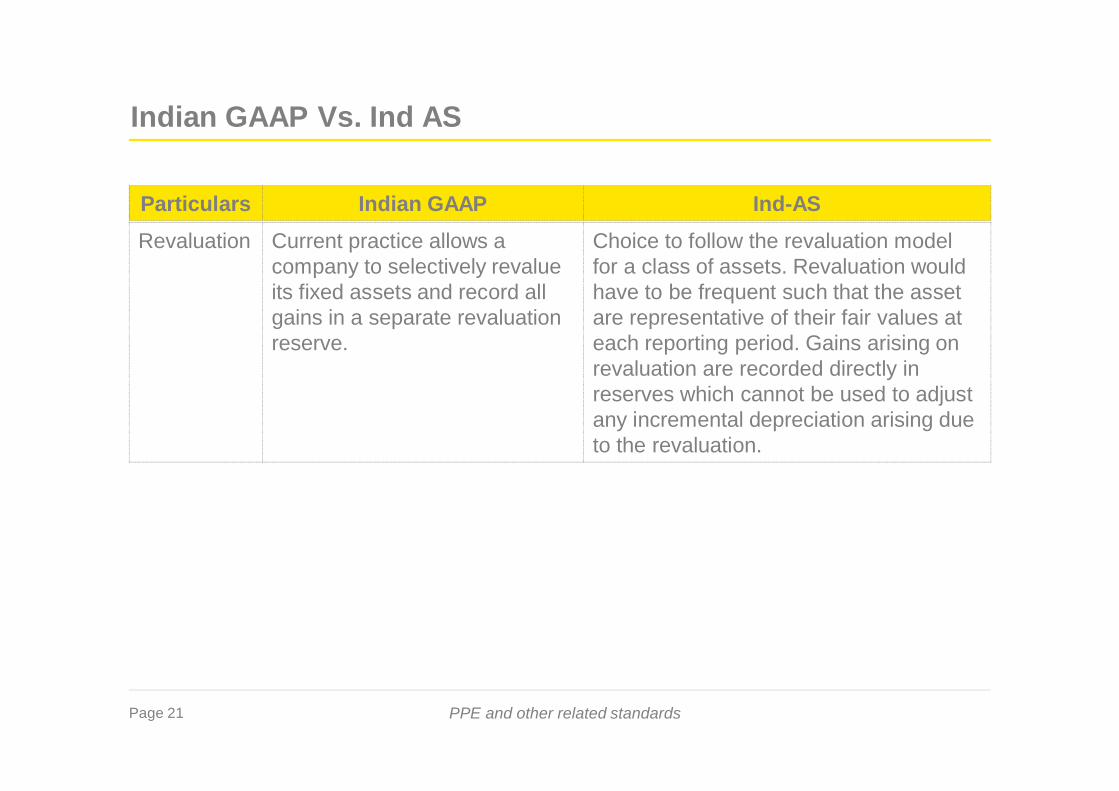

Revaluation Current practice allows acompany to selectively revalueits fixed assets and record allgains in a separate revaluationreserve.

Choice to follow the revaluation modelfor a class of assets. Revaluation wouldhave to be frequent such that the assetare representative of their fair values ateach reporting period. Gains arising onrevaluation are recorded directly inreserves which cannot be used to adjustany incremental depreciation arising dueto the revaluation.

Indian GAAP Vs. Ind AS

Particulars Indian GAAP Ind-AS

Page 22 PPE and other related standards

Issue Ind AS IFRSRates ofdepreciation

Ind AS 16 mentions the use of rates ofdepreciation as per the CompaniesAct, 2013

IFRS does not recognizethe depreciation ratesprescribed by the statute

Stand byequipment andserviceequipment

Capitalise when an entity expects touse them during more than one period

Capitalise when it can beused in connection with anitem of PPE and entityexpects to use them duringmore than one period

Ind AS vs. IFRS

Page 23 PPE and other related standards

Related Exemptions under Ind AS 101

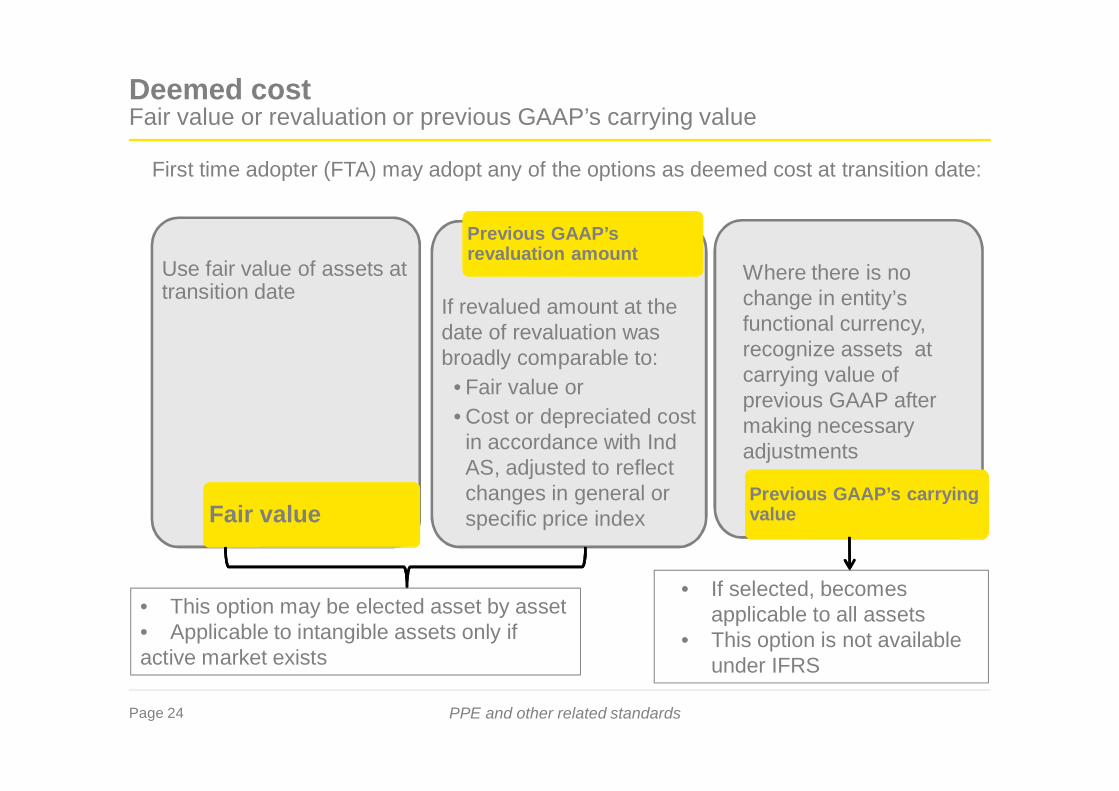

► Deemed cost - Fair Value or revaluation or Previous GAAP’s carrying Value

► Decommissioning, restoration and similar liabilities

Page 24 PPE and other related standards

Deemed costFair value or revaluation or previous GAAP’s carrying value

Use fair value of assets attransition date

Fair value

If revalued amount at thedate of revaluation wasbroadly comparable to:

• Fair value or• Cost or depreciated costin accordance with IndAS, adjusted to reflectchanges in general orspecific price index

Previous GAAP’srevaluation amount

Where there is nochange in entity’sfunctional currency,recognize assets atcarrying value ofprevious GAAP aftermaking necessaryadjustments

Previous GAAP’s carryingvalue

First time adopter (FTA) may adopt any of the options as deemed cost at transition date:

• This option may be elected asset by asset• Applicable to intangible assets only ifactive market exists

• If selected, becomesapplicable to all assets

• This option is not availableunder IFRS

Page 25 PPE and other related standards

Deemed costPrevious GAAP’s carrying value

If entity avails option of considering previous GAAP’s carrying value asdeemed cost, then:

► Necessary adjustments to be made for decommissioning liabilities

► No further transitional adjustment is required to determine deemed cost in the openingbalance sheet that other Ind ASs might require

► Applicable to PPE, investment property and intangible assets

Page 26 PPE and other related standards

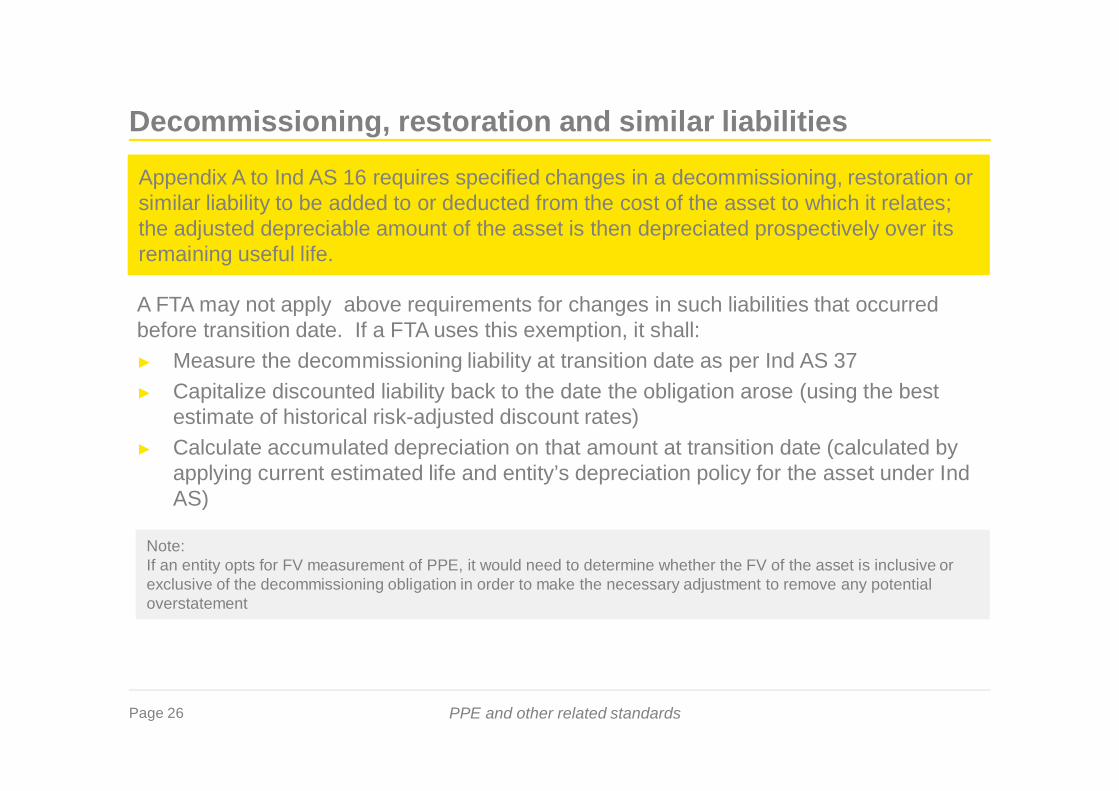

Decommissioning, restoration and similar liabilities

A FTA may not apply above requirements for changes in such liabilities that occurredbefore transition date. If a FTA uses this exemption, it shall:► Measure the decommissioning liability at transition date as per Ind AS 37► Capitalize discounted liability back to the date the obligation arose (using the best

estimate of historical risk-adjusted discount rates)► Calculate accumulated depreciation on that amount at transition date (calculated by

applying current estimated life and entity’s depreciation policy for the asset under IndAS)

Note:If an entity opts for FV measurement of PPE, it would need to determine whether the FV of the asset is inclusive orexclusive of the decommissioning obligation in order to make the necessary adjustment to remove any potentialoverstatement

Appendix A to Ind AS 16 requires specified changes in a decommissioning, restoration orsimilar liability to be added to or deducted from the cost of the asset to which it relates;the adjusted depreciable amount of the asset is then depreciated prospectively over itsremaining useful life.

Page 27 PPE and other related standards

On initial application of the Ind AS, preparers, users and other stakeholders have comeacross various issues on which clarification or explanations were/are required.

Hence the Accounting Standards Board (ASB) of the Institute of Chartered Accountantsof India has constituted ‘Ind AS Transition Facilitation Group’ (ITFG) on January 11,2016.

The objective behind formation of the group is to provide clarifications on various issuesrelated to the applicability and implementation of Ind AS under the Companies (IndianAccounting Standards) Rules, 2015.

The group has come out with 12 bulletins so far comprising of many clarifications. Theissues majorly pertain to clarifications required on application of Ind AS or issuespertaining to interpretation of the same.

Issues discussed by Ind AS Facilitation Transition Group

Page 28 PPE and other related standards

Deemed cost exemption vs. revaluation model

A Co is covered under phase 1 of Ind AS roadmap ( i.e. FY 2016-17 and transition date is 1April 2015). Co is evaluating various options related to PPE measurement at the transitiondate and revaluation model for its subsequent measurement. How these two aspectsinteract with each other?

Response:

Below are various options available for PPE valuation:► Historical cost determined by applying Ind AS 16 retrospectively► Fair value at the date of transition to Ind AS used as deemed cost► Revaluation in accordance with previous GAAP that meets criteria in Ind AS 101 as

deemed cost► Fair value at the date of an event such as a privatisation or initial public offering as

deemed cost► Previous GAAP carrying amount as deemed cost, provided that this option is used

for all items of PPE.

Page 29 PPE and other related standards

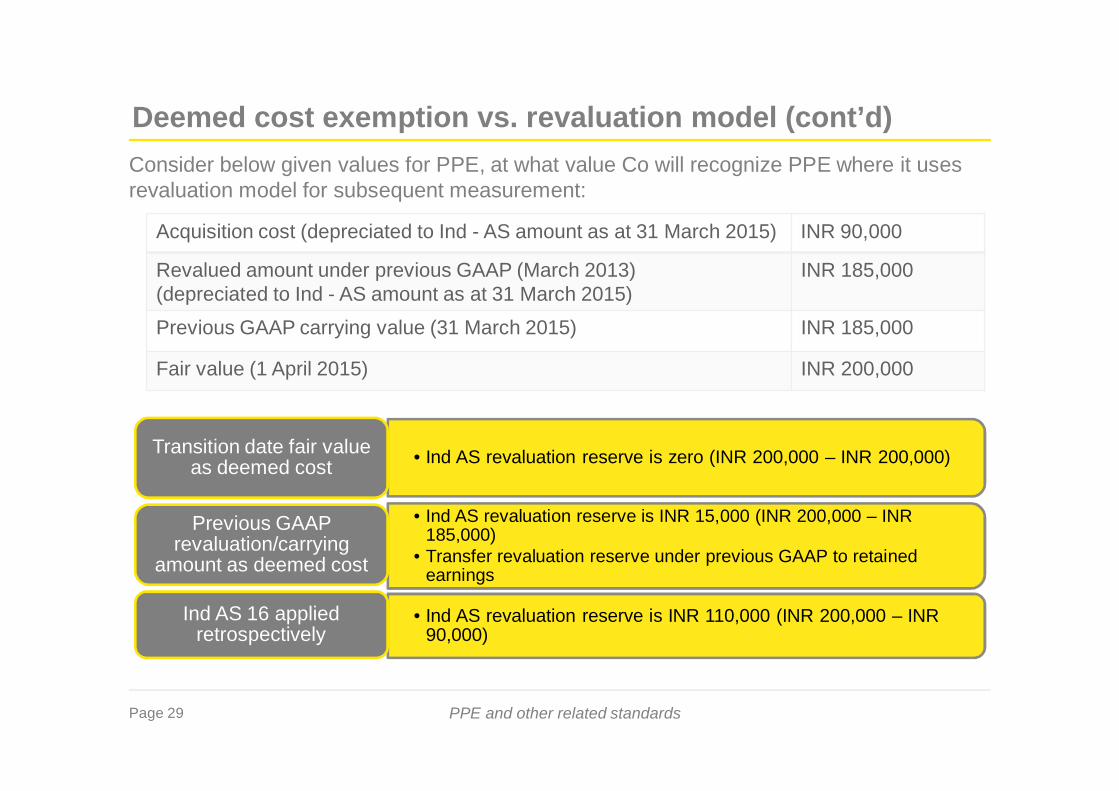

Deemed cost exemption vs. revaluation model (cont’d)Consider below given values for PPE, at what value Co will recognize PPE where it usesrevaluation model for subsequent measurement:

Acquisition cost (depreciated to Ind - AS amount as at 31 March 2015) INR 90,000

Revalued amount under previous GAAP (March 2013)(depreciated to Ind - AS amount as at 31 March 2015)

INR 185,000

Previous GAAP carrying value (31 March 2015) INR 185,000

Fair value (1 April 2015) INR 200,000

• Ind AS revaluation reserve is zero (INR 200,000 – INR 200,000)Transition date fair valueas deemed cost

• Ind AS revaluation reserve is INR 15,000 (INR 200,000 – INR185,000)

• Transfer revaluation reserve under previous GAAP to retainedearnings

Previous GAAPrevaluation/carrying

amount as deemed cost

• Ind AS revaluation reserve is INR 110,000 (INR 200,000 – INR90,000)

Ind AS 16 appliedretrospectively

Page 30 PPE and other related standards

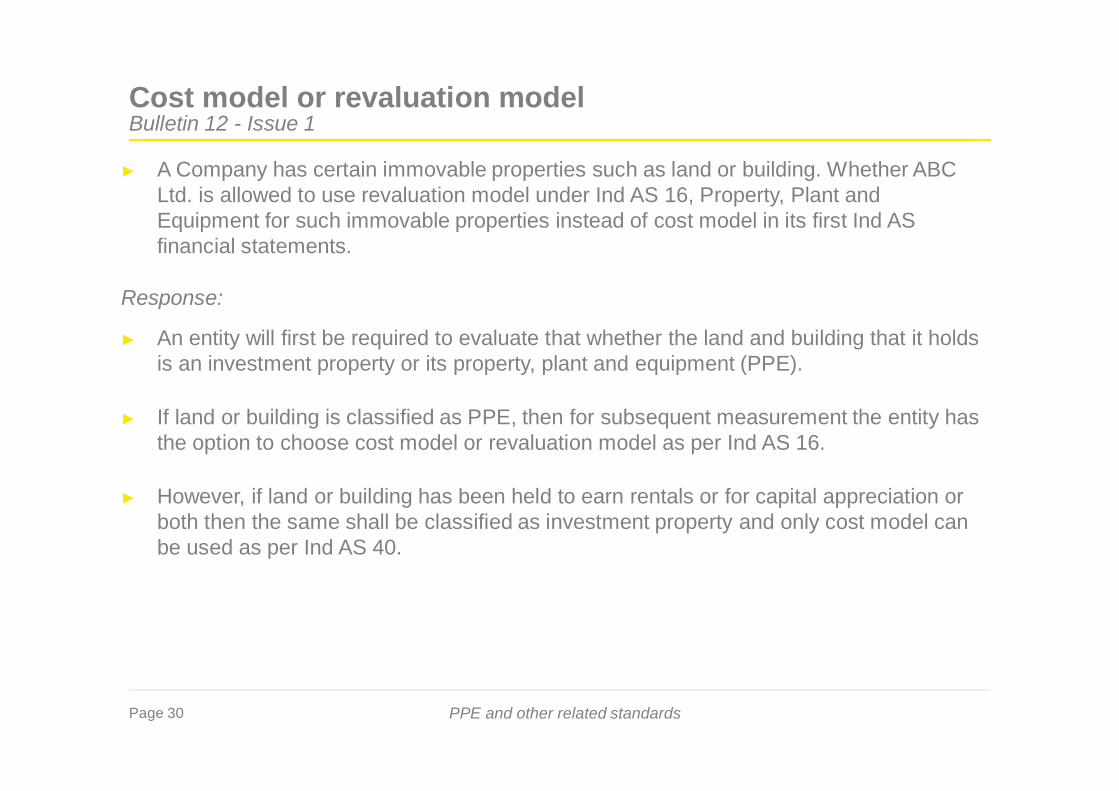

► A Company has certain immovable properties such as land or building. Whether ABCLtd. is allowed to use revaluation model under Ind AS 16, Property, Plant andEquipment for such immovable properties instead of cost model in its first Ind ASfinancial statements.

Response:

► An entity will first be required to evaluate that whether the land and building that it holdsis an investment property or its property, plant and equipment (PPE).

► If land or building is classified as PPE, then for subsequent measurement the entity hasthe option to choose cost model or revaluation model as per Ind AS 16.

► However, if land or building has been held to earn rentals or for capital appreciation orboth then the same shall be classified as investment property and only cost model canbe used as per Ind AS 40.

Cost model or revaluation modelBulletin 12 - Issue 1

Page 31 PPE and other related standards

Deemed cost of PPEFAQ by ASB

► If an entity avails deemed cost exemption under para D7AA, whether the entity shoulduse the original cost or the net book value as deemed cost? whether accumulateddepreciation and impairment loss is considered as nil? Whether impairment lossrecognized under previous GAAP can be reversed?

Response:

Deemed cost

• Entity should consider the net book value (NBV) attransition date as the deemed cost of PPE and not itsoriginal value. As the previous GAAP carrying value heremeans net book value.

• The future depreciation charge on PPE will be based onthe NBV and the remaining useful life on transition date toInd AS

Depreciationand

Impairmentloss

• Since NBV is deemed cost, previously recognizeddepreciation and impairment loss is considered to be Nil.Thus, reversal of previously recognized impairment loss isnot permitted.

Page 32 PPE and other related standards

Application of Deemed cost exemptionBulletin 10 - Issue 4 and Bulletin 3 - Issue 11

► An entity had recognised few assets as assets held for sale and disclosed the sameunder current assets instead of fixed assets under the previous GAAP. However, ontransition to Ind AS, the said asset could not fulfil the criteria of assets held for saleprescribed under Ind AS 105, hence the same needs to be classified as PPE.

► The issue under consideration is whether the deemed cost exemption can be applied tothese assets?

► Whether para D7AA can be applied for capital work in progress?

Response:

► As per Ind AS 101, the deemed cost exemption is applicable to PPE as defined underInd AS 16 and recognised as Fixed Assets in the financial statements at the transitionaldate irrespective of whether these were disclosed separately. Since the entity had onlydisclosed it separately and had not eliminated the same from the books, it can avail thedeemed cost exemption for such type of assets as well.

► Capital work in progress is in the nature of PPE under construction and accordingly,provisions of Ind AS 16 apply to it. Thus, exemption under para D7AA will be availablefor CWIP as well.

Page 33 PPE and other related standards

Retrospective application of Ind AS 16:Bulletin 3 - Issue 14

► A Ltd. measure its PPE by applying Ind AS 16 retrospectively in first Ind AS FS. Underprevious GAAP, it followed depreciation rates specified in Schedule XIV to theCompanies Act, 1956.

► Whether A Ltd need to re-compute depreciation based on useful lives from the date ofinitial capitalisation of PPE or it will have to apply depreciation rates applied underprevious GAAP till the date of opening balance sheet?

Response:

► When entity apply Ind AS 16 retrospectively, all requirements including componentaccounting and depreciation based on estimated useful life are applied retrospectively.If entity’s previous GAAP’s depreciation methods and rates are acceptable under IndAS, it accounts for any change in estimated useful life or depreciation patternprospectively from when it makes that change in estimate.

► If depreciation rates were adopted solely based on useful lives/ rates prescribed inSchedule XIV/ Schedule II and do not reflect a reasonable estimate of the asset’suseful life as per Ind AS, and If those differences have a material effect on the financialstatements, the entity adjusts accumulated depreciation in its opening Ind AS balancesheet retrospectively so that it complies with Ind AS.

Page 34 PPE and other related standards

Treatment of capital sparesBulletin 2 - Issue 4, Bulletin 3 – Issue 9 and Bulletin 5 - Issue 6

► A Company has certain spare parts that were recognized as inventory under previousGAAP but meets the definition of PPE under Ind AS. Company has applied D7AAexemption.

► At what amount spares can be recognized? Whether depreciation should be chargedfrom the date when it becomes available for use or date of actual use? How will usefullife determined?

Response:

reco

gniti

on

Ind AS should beapplied retrospectivelysince it meets thedefinition andrecognition criteria ofInd AS 16. Entity cannot apply D7AAdeemed costexemption in this caseas it is available onlyfor PPE which wasearlier recognized asinventory

depr

ecia

tion The depreciation

begins when asset isavailable for usewhich, in case of sparepart, may be from itsdate of purchase, asspare part is readilyavailable for use. us

eful

life In determination of the

useful life of sparepart, life of themachine in respect ofwhich it can be usedcan be one of thedetermining factors

Page 35 PPE and other related standards

Foreign exchange differences pertaining to fixed assets and borrowingsrelated to fixed assetsBulletin 1 - Issue 3

► Exchange gains or losses arisen for purchase of fixed assets is capitalised in cost ofProperty, plant and equipment or accumulated in a reserve named as Foreign CurrencyMonetary Item Translation Difference Account (FCMITDA) as per AS 11.

► Transitional exemptions under Ind AS 101 (paragraph D13AA) allows continuation ofrecognition of exchange differences in the same way it was accounted before thebeginning of the first Ind AS financial reporting period.

► Whether this option be availed for loans taken even after the Ind AS transition date.

Response:

► No. exchange differences arising from translation of long term foreign currencymonetary items recognised in the financial statements for the period endingimmediately before the beginning of the first Ind AS financial reporting period asper the previous GAAP”

► Considering this, this exemption can be availed only for loans which are taken up to thedate of Ind AS transition date

Page 36 PPE and other related standards

Foreign exchange differences pertaining to fixed assets and borrowingsrelated to fixed assetsBulletin 7 - Issue 3

► A further question was raised where the part of the loan (say 70% was drawn beforethe Ind AS transition date). However remaining sanctioned loan of 30% was drawn afterthe Ind AS transition date e.g after April 1, 2015 for a company adopting Ind AS for thefirst time in financial year 2016-17 with 2015-16 being comparative year.

► Whether the treatment allowed under Ind AS will continue to apply after the transitiondate for the undrawn part of the loan.

Response:

► No. Considering the same explanation above, this exemption can be availed only forloans which are taken up to the date of Ind AS transition date

► Therefore the exemption would not apply to any loan taken subsequent to the date ofadoption to Ind AS and also the undrawn part of the foreign currency loan for the loanssanctioned earlier and the foreign exchange differences arising on these cases wouldbe taken to statement of profit and loss.

► However for the purpose of Income Tax Act, companies will still be governed byprovisions of Section 43A of the Income Tax Act, 1961

Page 37 PPE and other related standards

► Loan borrowed prior to Ind AS transition date in case of companies who have opted forrecognising the differences in FCMITDA

► Whether the amortisation of balance in FCMITDA needs to be taken to Profit or loss orother comprehensive income.

Response:

► Since the amortisation of exchange differences under the existing policy (as per theprevious GAAP) would be recognised in the statement of profit and loss affecting theprofit or loss for the period, amortisation of balance of FCMITDA shall also be routedthrough profit or loss and not through Other Comprehensive Income (OCI).

Foreign exchange differences pertaining to fixed assets and borrowingsrelated to fixed assetsBulletin 2 - Issue 1

Page 38 PPE and other related standards

Capitalisation of asset not meeting the criteria of Ind AS 16Bulletin 8 - Issue 4

► ABC Ltd. is a FTA of Ind AS and has opted for deemed cost exemption. It hadcapitalised an item of property, plant and equipment under previous GAAP even thoughit did not meet the definition of an asset. Whether this asset cost can also be continuedto be capitalised under deemed cost exemption?

Response:

► The option of deemed cost exemption can be availed for property, plant and equipmentmeasured as per previous GAAP. The incorrect capitalisation of the item of PPE did notmeet the definition of asset as per previous GAAP and the definition of ‘PPE’ as per IndAS 16, accordingly the deemed cost exemption under paragraph D7AA of Ind AS 101cannot be availed for those assets.

► The incorrect capitalisation of asset which does not meet the definition of tangible assetwill be covered under Ind AS 101 being an error, and the disclosure of the same shouldbe done as per Ind AS 101.

Page 39 PPE and other related standards

Treatment of Revaluation Reserve & Deferred Tax on transitionBulletin 8 - Issue 7

► A company is a FTA of Ind AS. It has opted for exemption under paragraph D7AA of IndAS 101, First-time Adoption of Indian Accounting Standards and also elected the costmodel under Ind AS 16, Property, Plant and Equipment for subsequent measurement.

► On the date of transition to Ind AS, what will be the accounting treatment of the balanceoutstanding in the “Revaluation Reserve” created as per previous GAAP.

Response:

► In the given case balance outstanding in the revaluation reserve should be transferredto retained earnings or if appropriate, another category of equity. This is because aftertransition, the Company is no longer applying the revaluation model of Ind AS 16,instead it has elected to apply the cost model approach.

► It may be noted that the requirements of Companies Act, 2013 for declaration ofdividend will be required to be evaluated separately.

Page 40 PPE and other related standards

► On the date of transition to Ind AS, what will be the treatment of deferred tax on thistransition revaluation reserve?

Response:

► In accordance with Ind AS 12, Income Taxes, deferred tax would need to be recognisedon any difference between the carrying amount and tax base of assets and liabilities.No deferred tax is created on equity components.

► However, since the asset has been revalued, there will be difference for the amountbetween carrying value and tax base. Hence, deferred tax will have to be recognised onsuch asset.

Treatment of Revaluation Reserve & Deferred Tax on transitionBulletin 8 - Issue 7

Page 41 PPE and other related standards

► An entity is setting up a new refinery outside the city limits and hence an additionalexpenditure is incurred for construction of railway siding, road and bridge.

► Whether the cost of the support assets created should be capitalised with the main costof the asset

Response:

► In the given case, the railway siding, road and bridge are required to facilitate theconstruction of the refinery and for its operations and also expenditure on these itemswill help the entity to get future economic benefits, the aforesaid expenditure is directlyattributable to bringing the asset to the location and condition necessary for it to becapable of operating in the manner intended by management.

► In this case, even though the company may not be able to recognise expenditureincurred on these assets as an individual item of Property, plant and equipment as itmay not be able to restrict others from using it, entire expenditure incurred may becapitalised as a part of overall cost of the project

Capitalisation of cost incurred for the assets used as a support forbuilding/creation of main assetBulletin 11 - Issue 8

Page 42 PPE and other related standards

Government Grants – IND AS 20

► Scope and Definition

► Treatment of grants received against assets

► Indian GAAP vs. Ind AS

► Ind AS vs. IFRS

► Issues discussed by Ind AS Facilitation Transition Group

Page 43 PPE and other related standards

Grants related to assets are government grants whose primary condition is that an entity qualifying forthem should purchase, construct or otherwise acquire long-term assets. Subsidiary conditionsmay also be attached restricting the type or location of the assets or the periods during which they areto be acquired or held.

Notes:Ø Grants related to non depreciable assets-§ If related directly to incurring specific expenditures – on the same basis as the expenditures

§ If related to fulfillment of certain obligations and would then be recognized in the profit or loss overthe periods that bear the cost of meeting the obligations. Eg: a grant of land may be conditionalupon the erection of a building on the site and it may be appropriate to recognise the grant in profitor loss over the life of the building

Accounting:Present the grant as deferred income which is recognized in the profit or loss account on a systemand rational basis over the useful life of the asset.

Scope and Definition

Page 44 PPE and other related standards

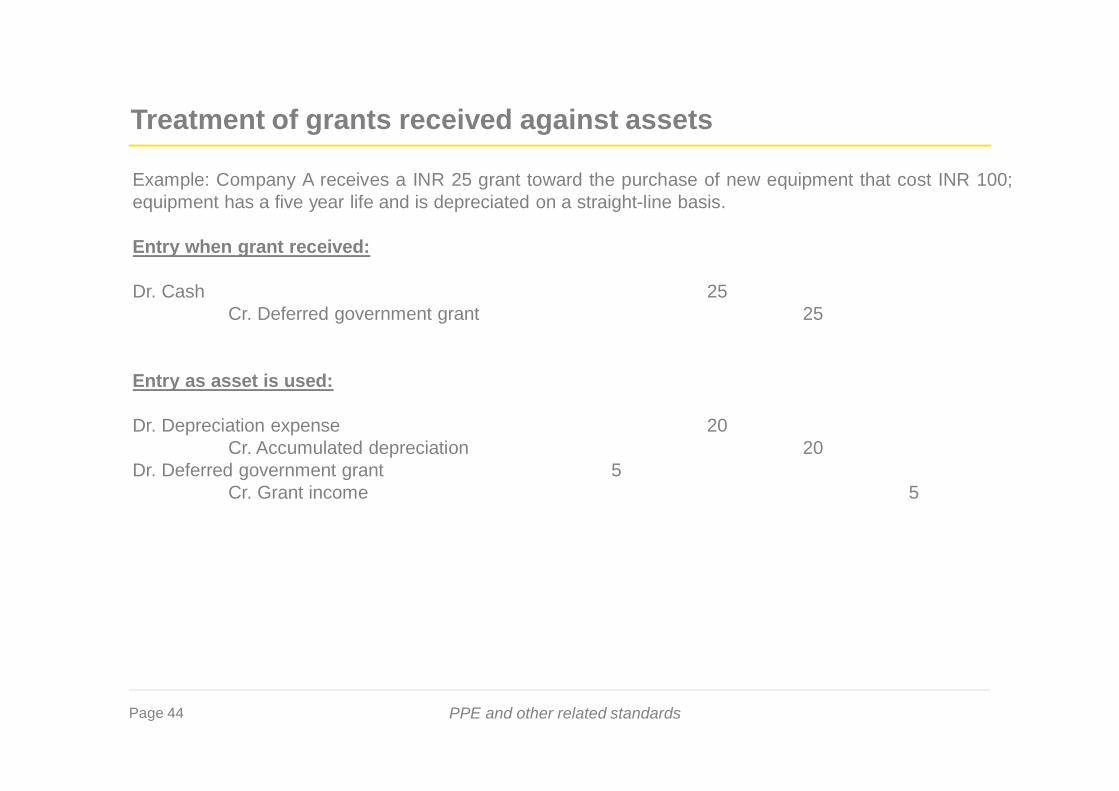

Example: Company A receives a INR 25 grant toward the purchase of new equipment that cost INR 100;equipment has a five year life and is depreciated on a straight-line basis.

Entry when grant received:

Dr. Cash 25Cr. Deferred government grant 25

Entry as asset is used:

Dr. Depreciation expense 20Cr. Accumulated depreciation 20

Dr. Deferred government grant 5Cr. Grant income 5

Treatment of grants received against assets

Page 45 PPE and other related standards

Indian GAAP Vs. Ind AS

Particulars Indian GAAP Ind-ASRecognition ofasset relatedgrants

Grants related to depreciableassets are either treated asdeferred income and transferredto the profit and loss account inproportion to the depreciation; ordeducted from the cost of theasset.

Government grants related to assetsare presented in the balance sheetonly by setting up the grant asdeferred income and not as areduction from PPE.

Grants of non-monetaryassets

Under current practice,companies are required toaccount for government grantsreceived in the form of non-monetary assets, at theiracquisition cost. If non-monetaryassets are given free of cost,they are recorded at a nominalvalue

Ind AS requires companies toaccount for government grants in theform of non-monetary assets, whichare given at concessional rates, atfair value (both the grant as well asthe asset).

Page 46 PPE and other related standards

Issue Ind AS IFRSGovernment grant Ind-AS 20 requires presentation of

such grants in the balance sheet onlyby setting up the grant as deferredincome. Thus, the option to presentsuch grants by deduction of the grantin arriving at the carrying amount ofthe asset is not available.

IAS 20 gives an option topresent the grants related toassets, including non-monetary grants at fairvalue, in the balance sheeteither by setting up thegrant as deferred income orby deducting the grant inarriving at the carryingamount of the asset.

Ind AS vs. IFRS

Page 47 PPE and other related standards

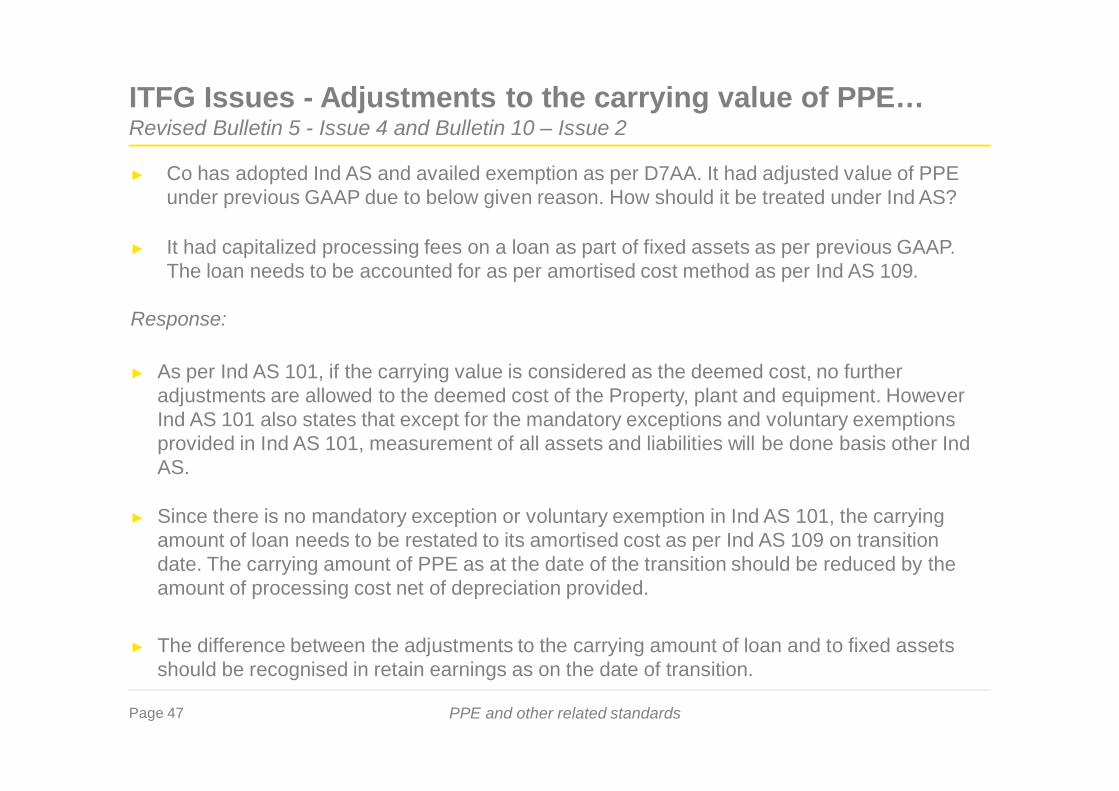

ITFG Issues - Adjustments to the carrying value of PPE…Revised Bulletin 5 - Issue 4 and Bulletin 10 – Issue 2

► Co has adopted Ind AS and availed exemption as per D7AA. It had adjusted value of PPEunder previous GAAP due to below given reason. How should it be treated under Ind AS?

► It had capitalized processing fees on a loan as part of fixed assets as per previous GAAP.The loan needs to be accounted for as per amortised cost method as per Ind AS 109.

Response:

► As per Ind AS 101, if the carrying value is considered as the deemed cost, no furtheradjustments are allowed to the deemed cost of the Property, plant and equipment. HoweverInd AS 101 also states that except for the mandatory exceptions and voluntary exemptionsprovided in Ind AS 101, measurement of all assets and liabilities will be done basis other IndAS.

► Since there is no mandatory exception or voluntary exemption in Ind AS 101, the carryingamount of loan needs to be restated to its amortised cost as per Ind AS 109 on transitiondate. The carrying amount of PPE as at the date of the transition should be reduced by theamount of processing cost net of depreciation provided.

► The difference between the adjustments to the carrying amount of loan and to fixed assetsshould be recognised in retain earnings as on the date of transition.

Page 48 PPE and other related standards

…ITFG Issues - Adjustments to the carrying value of PPERevised Bulletin 5 - Issue 5

► Co has adopted Ind AS and availed exemption as per D7AA. It has to adjust the value of PPEas prescribed by Ind AS 20 on account of Government grant received against purchase offixed asset while it was deducted from the carrying value of fixed asset as per AS 12. Whetherthe adjustment is allowed or not?

Response:

► No, applying the same principle as above, since there is no mandatory exception orvoluntary exemption in Ind AS 101, the cost of PPE will be increased to the extent ofgrant amount and the same will be shown as deferred income as per Ind AS 20.

► The grant will be recognised as unamortised deferred income as at the date of thetransition and the corresponding adjustment needs to be made to the carrying amountof PPE and retained earnings, respectively, as the grant is directly linked to the PPE.

► In both the cases, since the adjustment to the PPE is only consequential and arisingbecause of applying the transition requirements, it would not be construed as anadjustment to the deemed cost of PPE

Page 49 PPE and other related standards

Adjustments to the carrying value of PPEBulletin 12 - Issue 2

► Continuing the above example, however in this case, Co has chosen to measure the item ofPPE at its fair value and use that as its deemed cost on the date of transition to Ind AS.How should the value of Government grant received be treated under Ind AS consideringthe adjustment required by Ind AS 20.

Response:

► As per Ind AS 113, Fair Value Measurement, “Fair value is the price that would bereceived to sell an asset or paid to transfer a liability in an orderly transaction in theprincipal (or most advantageous) market at the measurement date under current marketconditions (i.e. an exit price) regardless of whether that price is directly observableor estimated using another valuation technique.”

► Accordingly, in the given case, fair value of the asset is independent of the governmentgrant received on the asset and no adjustment with regard to the government grantshould be made to the fair value of the property, plant and equipment taken as deemedcost on the date of transition to Ind AS.

Page 50 PPE and other related standards

Impact on Indian Corporates

Major impact due the following

Capitalization ofStores and spares

Major overhaulexpenses Change in

depreciation method

§ Mixed impact on net worth and net profit due to adoption of Ind AS 16 and related Ind AS

59 Companies

8

8

Impact on net worth Impact on profit

10 Companies

36

29

On thebasis of

standalonefinancial

statements as atMarch 31, 2016

Page 51

Questions?

QUESTIONS

Page 52

Thank You