ind-as - practical issues - northern india regional … -intro consolidation...disclosure of...

TRANSCRIPT

Ind-AS - Practical Issues

♣presented by

PARVEEN KUMAR ASA & Associates LLP www.asa.in

NIRCJune, 2015

1

Why IFRS

3

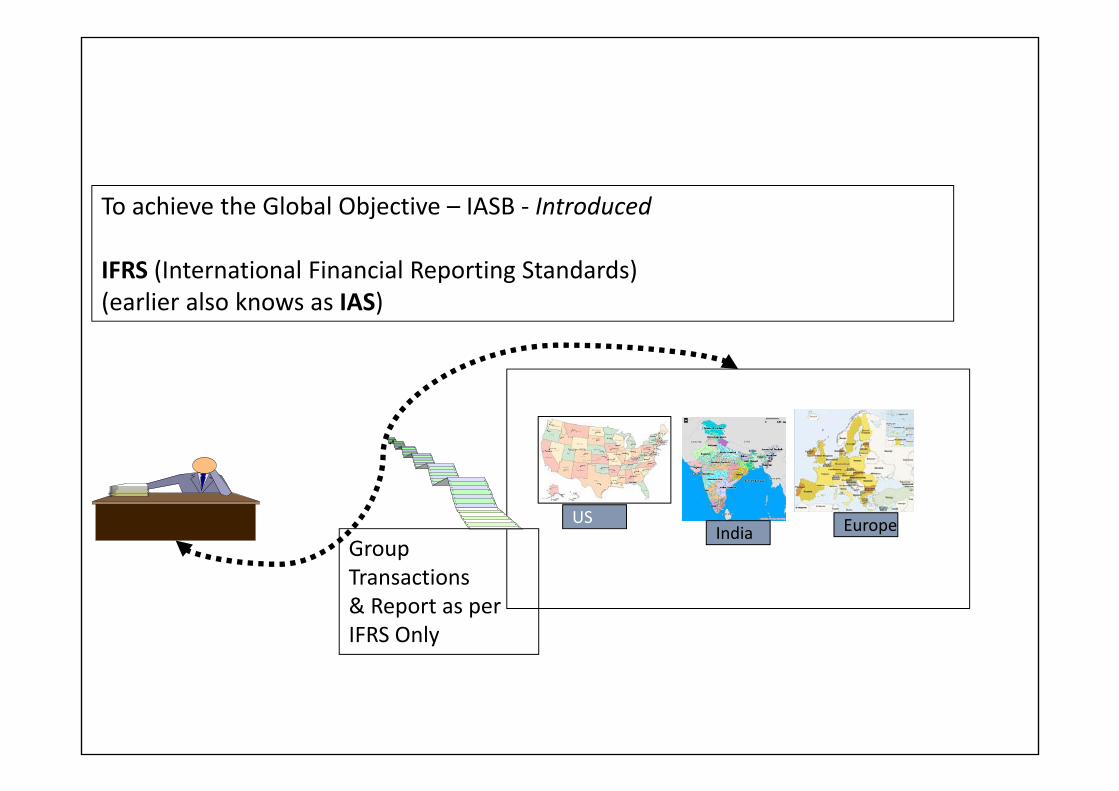

Example:‐A Listed Indian Companies having listed subsidiaries in US, Europe etc

Regroup Transactions& Report as per USGAAPFor SEC.

Regroup Transactions& Report as per Indian GAAPFor ROC and SEBI.

Regroup Transactions& Report as per IFRSFor Europe.

Major Challenges:‐a) Huge Cost and Resource Requirmentb) Comparability

4

To achieve the Global Objective – IASB ‐ Introduced

IFRS (International Financial Reporting Standards) (earlier also knows as IAS)

Group Transactions& Report as per IFRS Only

USIndia Europe

Why Ind-AS

Adoption..?

Carve Outs..?

Implications..? IFRS15

IFRS 9

Framework

8

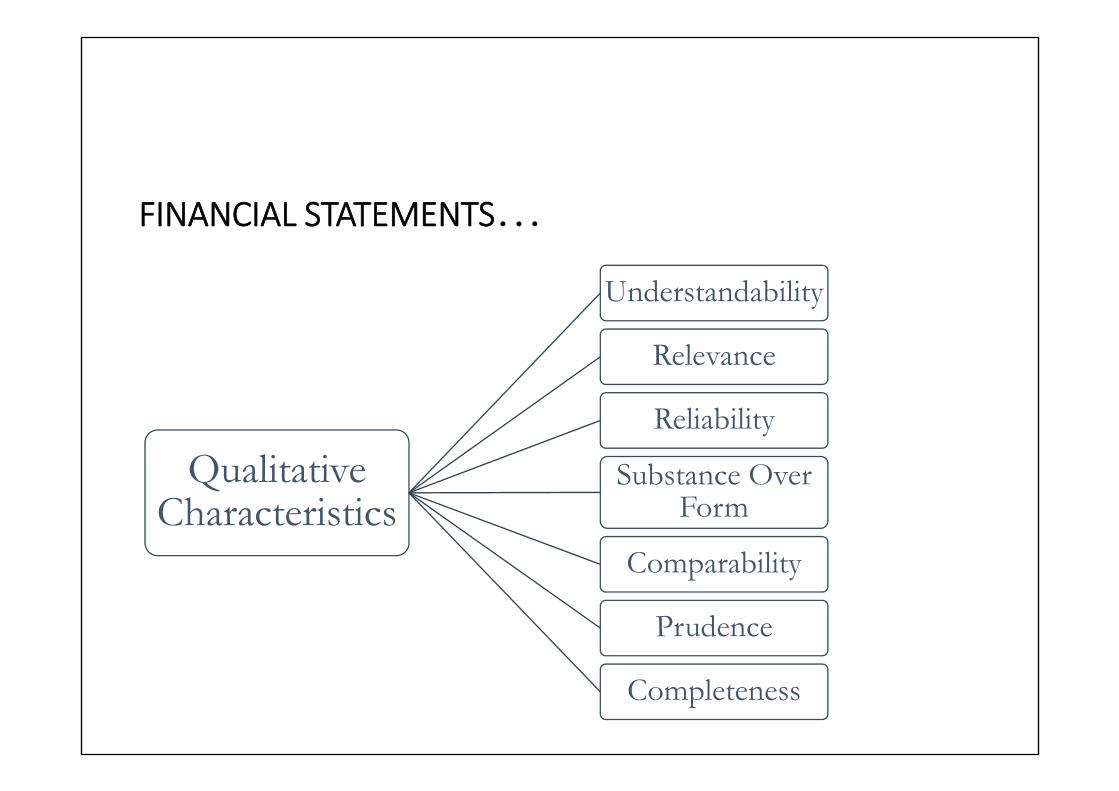

FINANCIAL STATEMENTS…

OBJECTIVES

Financial Position

Performance

Changes in Financial Position

FINANCIAL STATEMENTS…

Qualitative Characteristics

Understandability

Relevance

Reliability

Substance Over Form

Comparability

Prudence

Completeness

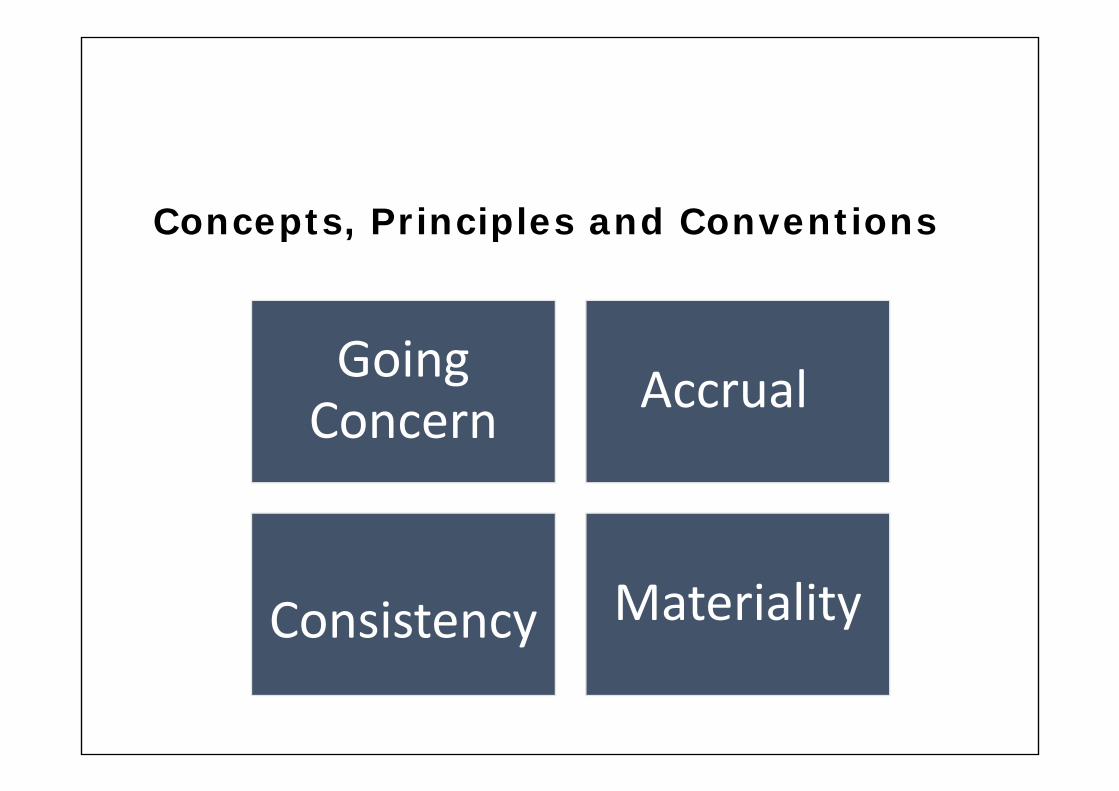

Concepts, Principles and Conventions

Going Concern Accrual

Consistency Materiality

India works on a multi-regulator model

Reserve Bank (RBI)

NBFCs

…FC AAA.C XXX

LC..C

MCA State RegistrarOf Chit Funds

RBI regulates deposittaking activity

XXXNidhi

ZZZZChit Fund C.

NationalHousing

BankIRDA SEBI

CCCCHFC SBC MF

XX co.YY

Infrastructure

General Insurance ABC

Financial Statements

IndAS

IFRSAS

Company Law

Regulators –RBI, SEBI, IRDA….

To Help User Take Decisions

ICDS Cost Standards

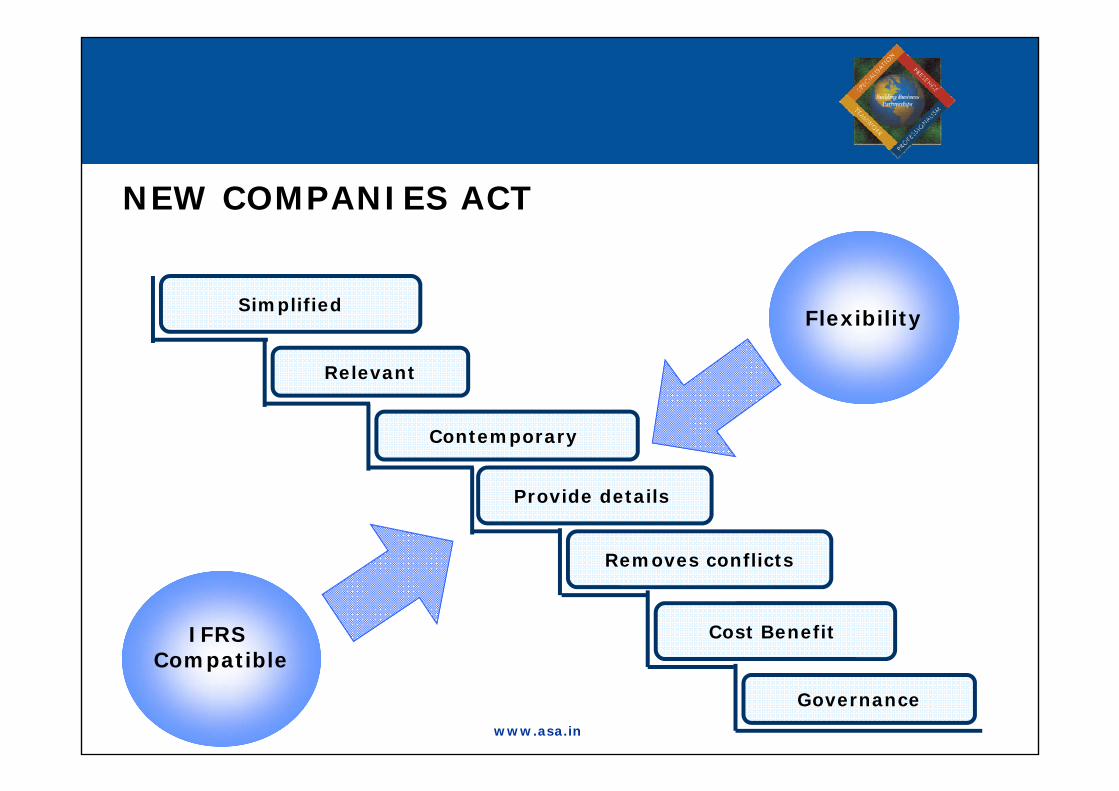

NEW COMPANIES ACT

Flexibility

IFRS Compatible

Governance

Simplified

Relevant

Contemporary

Provide details

Removes conflicts

Cost Benefit

www.asa.in

CONSOLIDATION

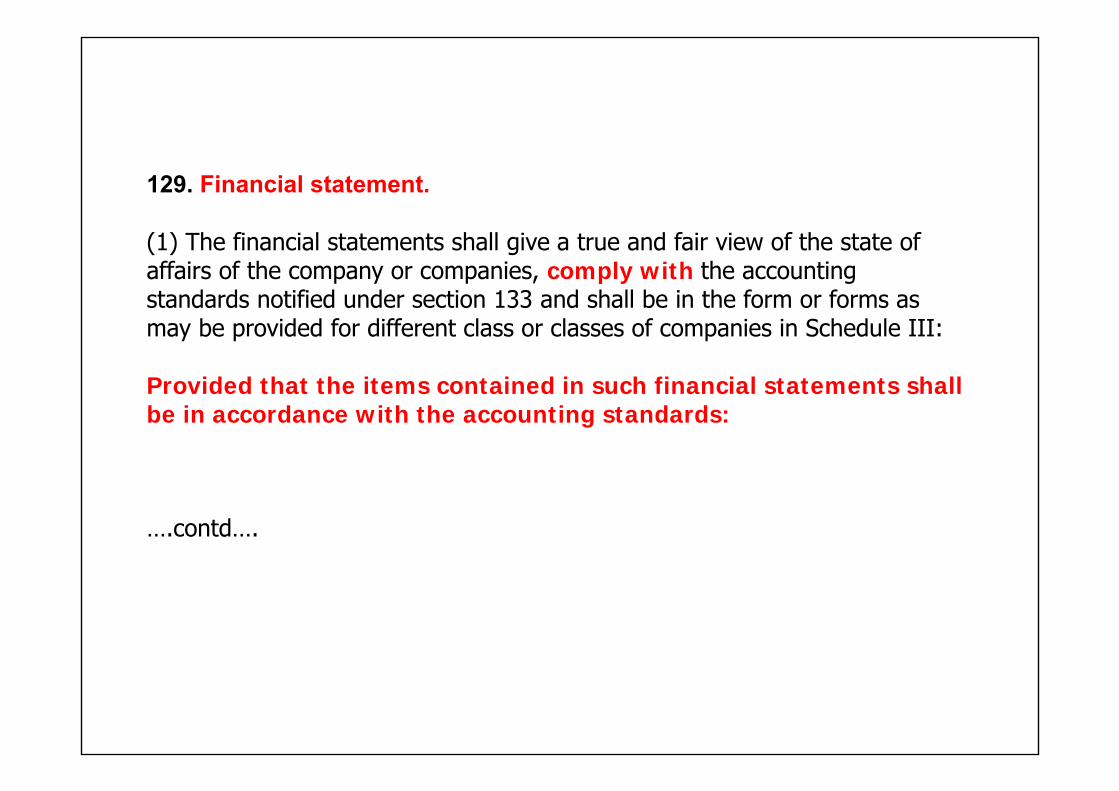

129. Financial statement.

(1) The financial statements shall give a true and fair view of the state of affairs of the company or companies, comply with the accounting standards notified under section 133 and shall be in the form or forms as may be provided for different class or classes of companies in Schedule III:

Provided that the items contained in such financial statements shall be in accordance with the accounting standards:

….contd….

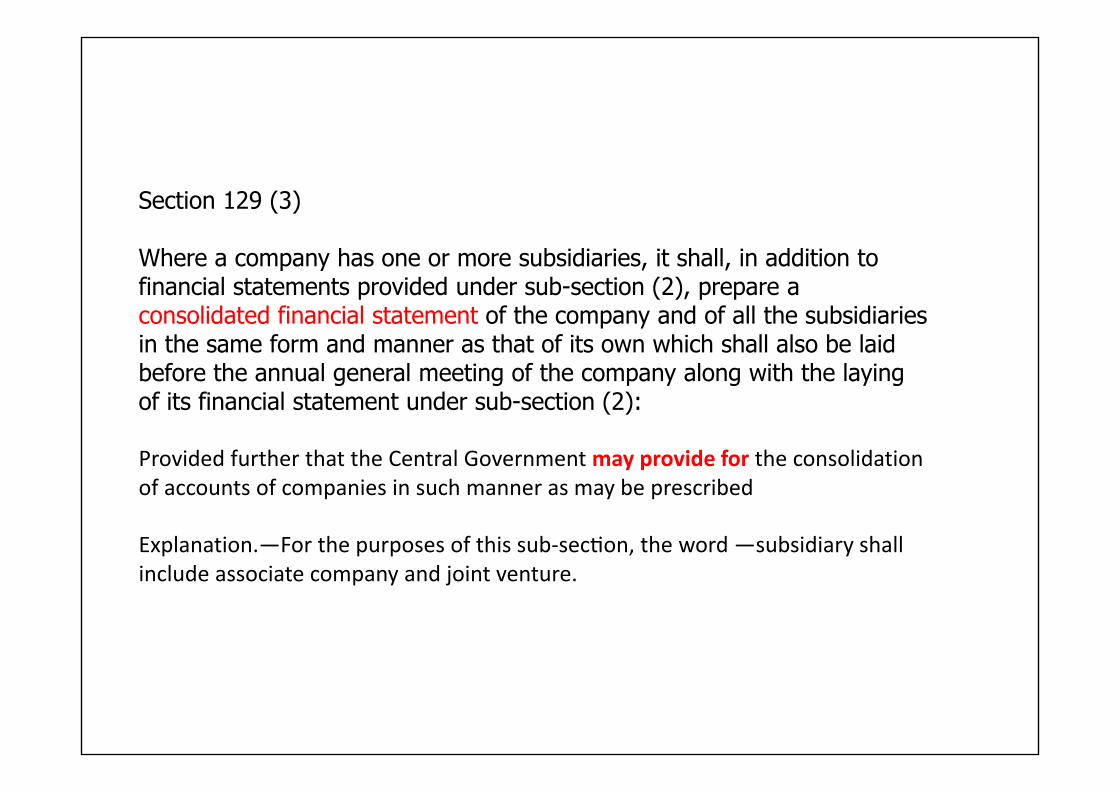

Section 129 (3)

Where a company has one or more subsidiaries, it shall, in addition to financial statements provided under sub-section (2), prepare a consolidated financial statement of the company and of all the subsidiaries in the same form and manner as that of its own which shall also be laid before the annual general meeting of the company along with the layingof its financial statement under sub-section (2):

Provided further that the Central Government may provide for the consolidation of accounts of companies in such manner as may be prescribed

Explanation.—For the purposes of this sub‐sec on, the word ―subsidiary shall include associate company and joint venture.

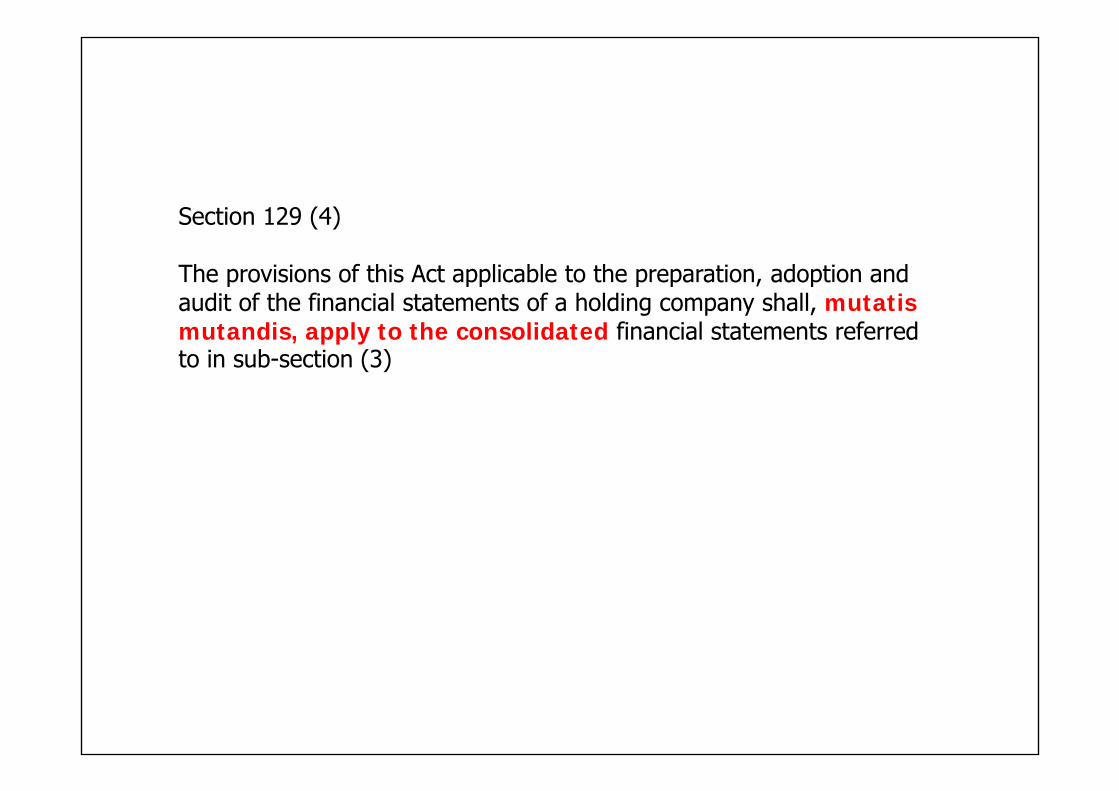

Section 129 (4)

The provisions of this Act applicable to the preparation, adoption and audit of the financial statements of a holding company shall, mutatis mutandis, apply to the consolidated financial statements referred to in sub-section (3)

Rules for Chapter IXCompanies (Accounts) Rules, 2014

Clause 6.

Manner of consolidation of accounts.- The consolidation of financial statements of the company shall be made in accordance with the provisions of Schedule III of the Act and the applicable accounting standards:

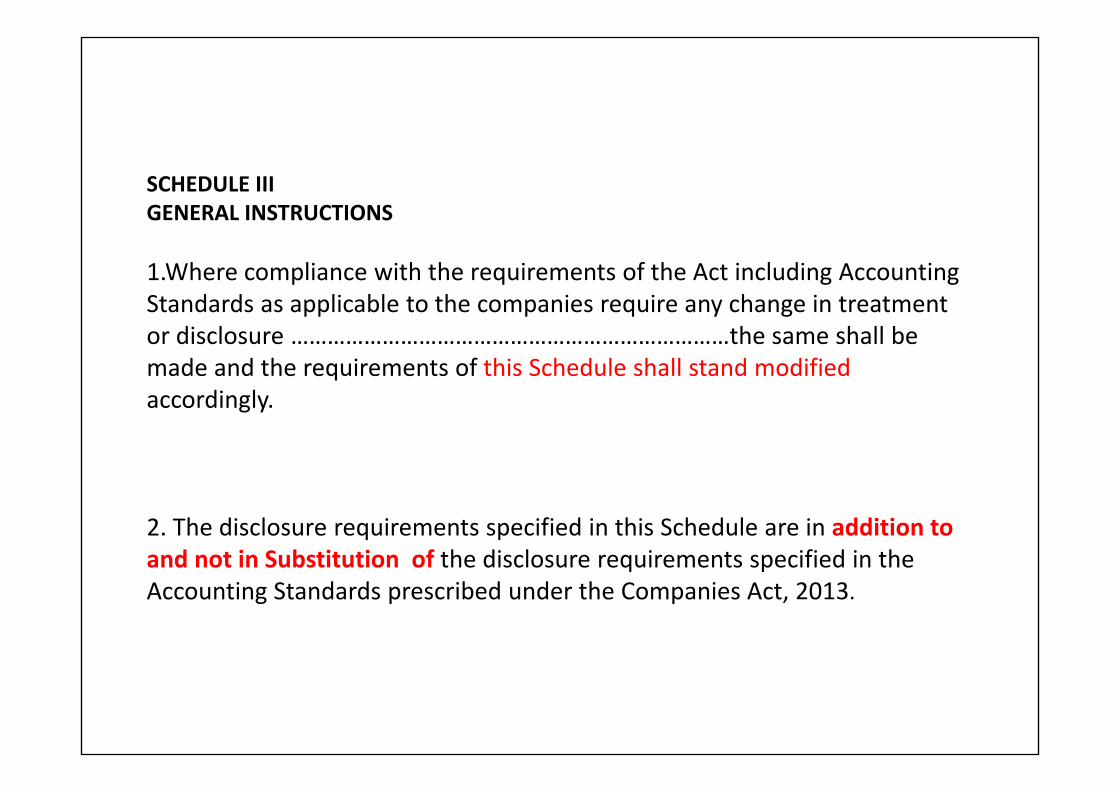

SCHEDULE IIIGENERAL INSTRUCTIONS

1.Where compliance with the requirements of the Act including Accounting Standards as applicable to the companies require any change in treatment or disclosure ………………………………………………………………the same shall be made and the requirements of this Schedule shall stand modified accordingly.

2. The disclosure requirements specified in this Schedule are in addition to and not in Substitution of the disclosure requirements specified in the Accounting Standards prescribed under the Companies Act, 2013.

Schedule III

GENERAL INSTRUCTIONS FOR THE PREPARATION OF CONSOLIDATED FINANCIAL STATEMENTS

Where a company is required to prepare Consolidated Financial Statements, i.e., consolidated balance sheet and consolidated statement of profit and loss, the company shall mutatis mutandis follow the requirements of this Schedule as applicable to a company in the preparation of balance sheet and statement of profit and loss………

Accounting Standard (AS) 21Consolidated Financial Statements

The objective of this Standard is to lay down principles and procedures for preparation and presentation of consolidated financial statements.

Accounting Standard (AS) 21Consolidated Financial Statements1

5.1 Control:

(a) the ownership, directly or indirectly through subsidiary(ies), of more than one half of the voting power of an enterprise; or

(b) control of the composition of the board of directors in the case of a company or of the composition of the corresponding governing body in case of any other enterprise so as to obtain economic benefits from its activities.

5.2 A subsidiary is an enterprise that is controlled by another enterprise (known as the parent).

Section 2 (27) ―control - shall include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner;

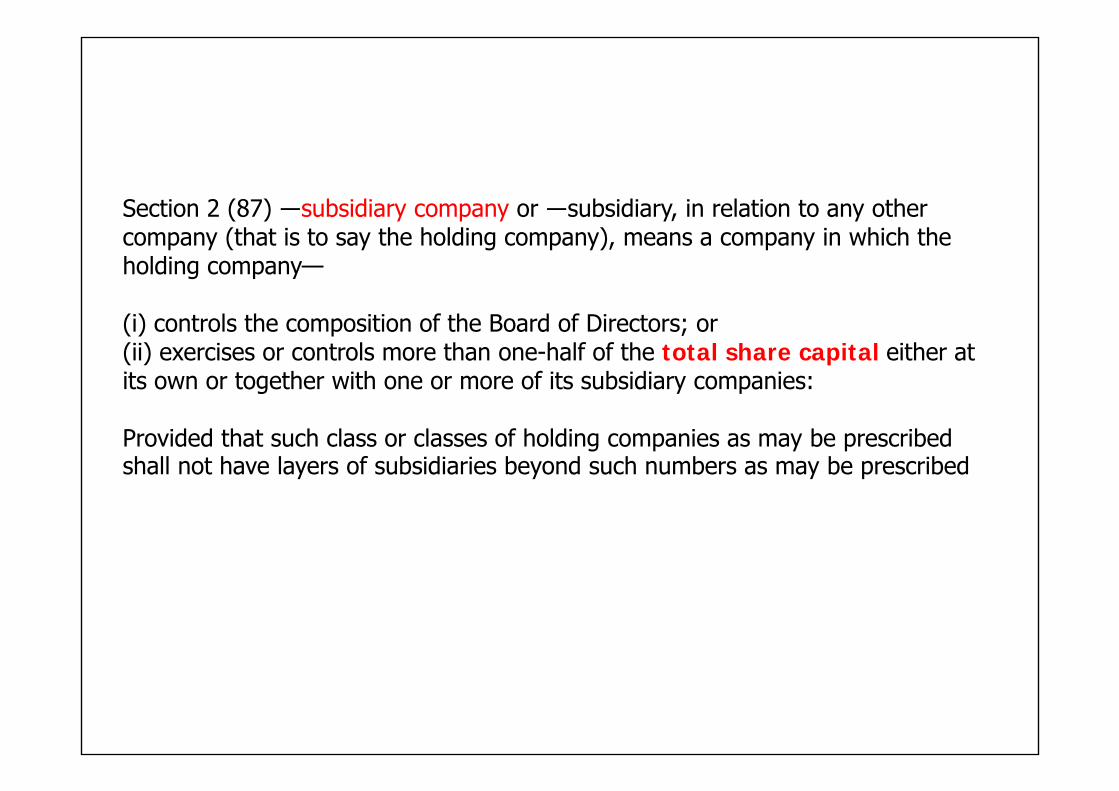

Section 2 (87) ―subsidiary company or ―subsidiary, in relation to any other company (that is to say the holding company), means a company in which the holding company—

(i) controls the composition of the Board of Directors; or(ii) exercises or controls more than one-half of the total share capital either at its own or together with one or more of its subsidiary companies:

Provided that such class or classes of holding companies as may be prescribed shall not have layers of subsidiaries beyond such numbers as may be prescribed

Section 2 (6) ―associate company, in relation to another company, means a company in which that other company has a significant influence, but which is not a subsidiary company of the company having such influence and includes a joint venture company.

Explanation.—For the purposes of this clause, ―significant influenceǁ means control of at least twenty per cent. of total share capital, or of business decisions under an agreement;

Consolidation in Ind‐AS

Consolidated Financial Statements ‐ IFRS 10 / Ind AS 110Joint Arrangements – IFRS 11 / Ind AS 111

Disclosure of Interest in other entities – IFRS 12 / Ind AS 112Investment in Associates – IAS 28 / Ind‐AS 28

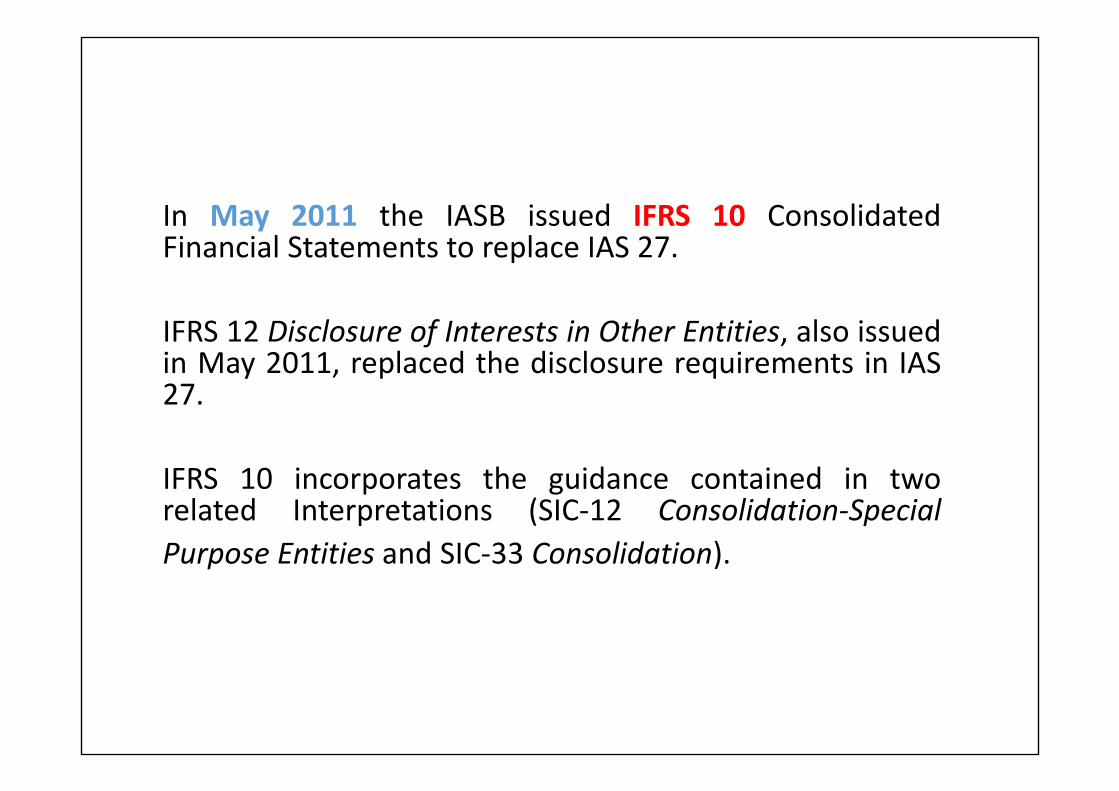

In May 2011 the IASB issued IFRS 10 ConsolidatedFinancial Statements to replace IAS 27.

IFRS 12 Disclosure of Interests in Other Entities, also issuedin May 2011, replaced the disclosure requirements in IAS27.

IFRS 10 incorporates the guidance contained in tworelated Interpretations (SIC‐12 Consolidation‐SpecialPurpose Entities and SIC‐33 Consolidation).

0% 20% 50% 100%

ControlPassive Significant Influence

40%

10% controlling interest in a financial asset

controlling interest in anassociate or a jointlycontrolled entity

About IFRS – 10 / Ind AS 110

• 33 Clauses• Application Guidance • Basis for Conclusion

Touch Base with IAS 1, IFRS 3 and IFRS 5

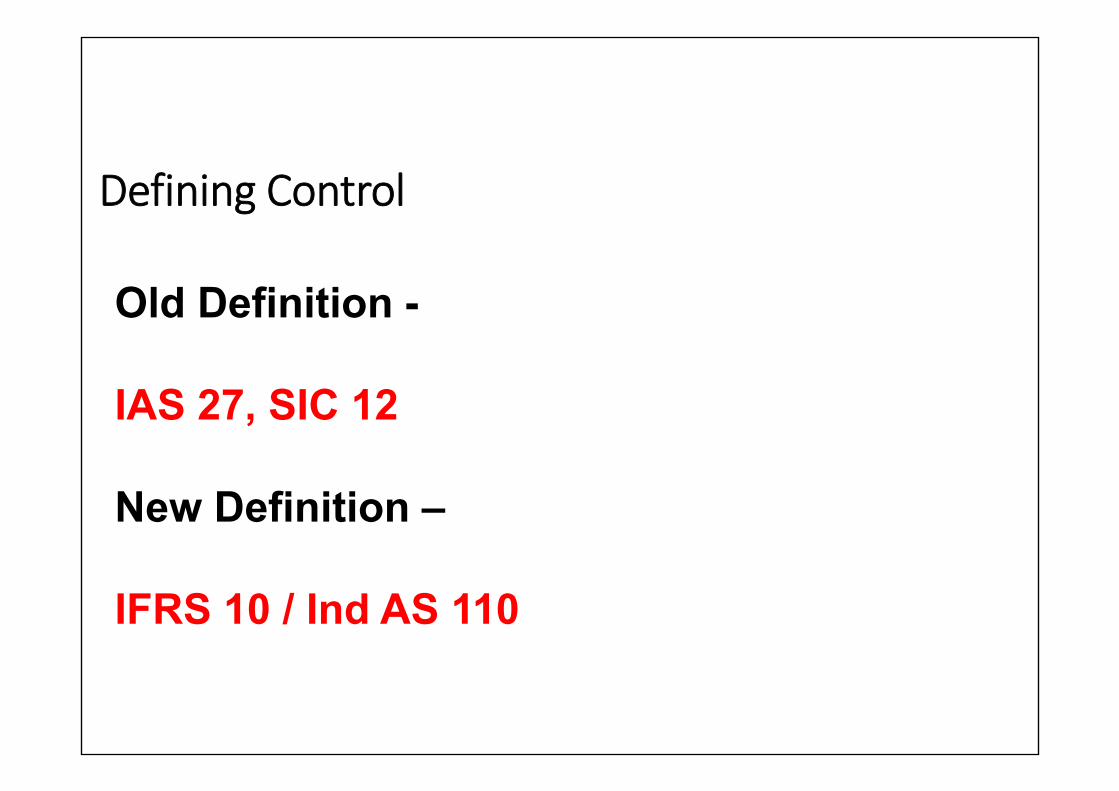

Defining Control

Old Definition -

IAS 27, SIC 12

New Definition –

IFRS 10 / Ind AS 110

Defining Control

Old Definition -

Power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

More than half of voting power

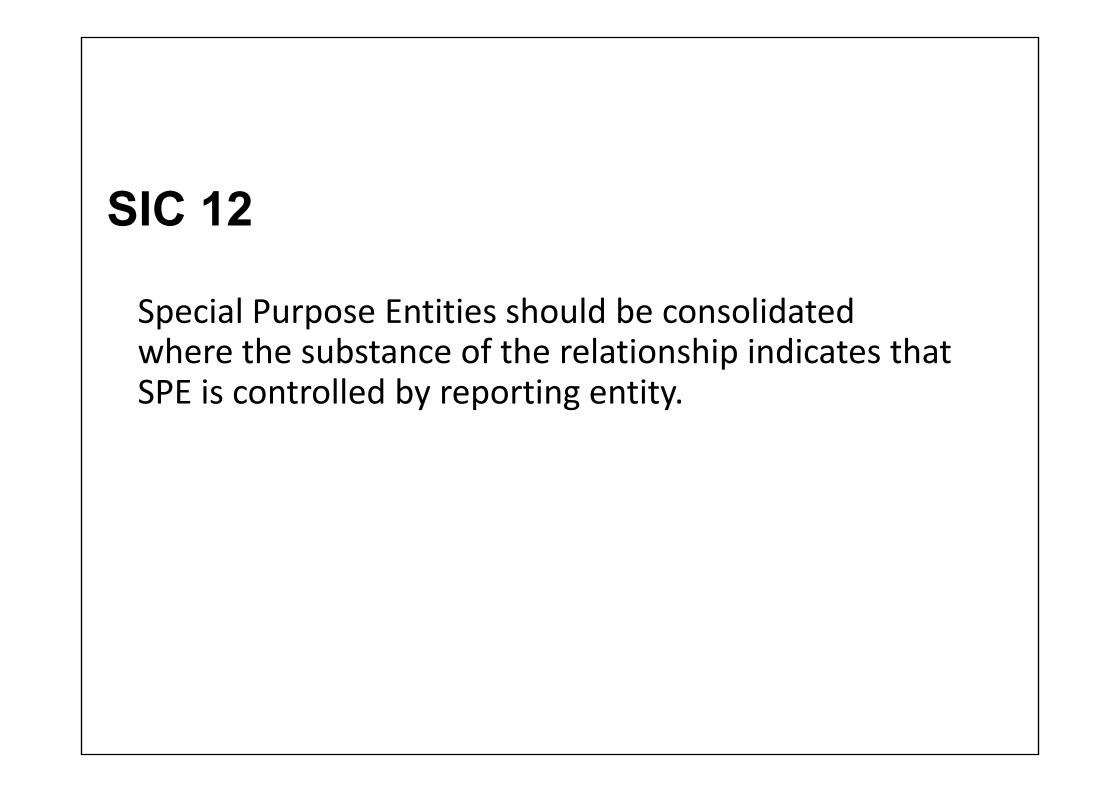

SIC 12

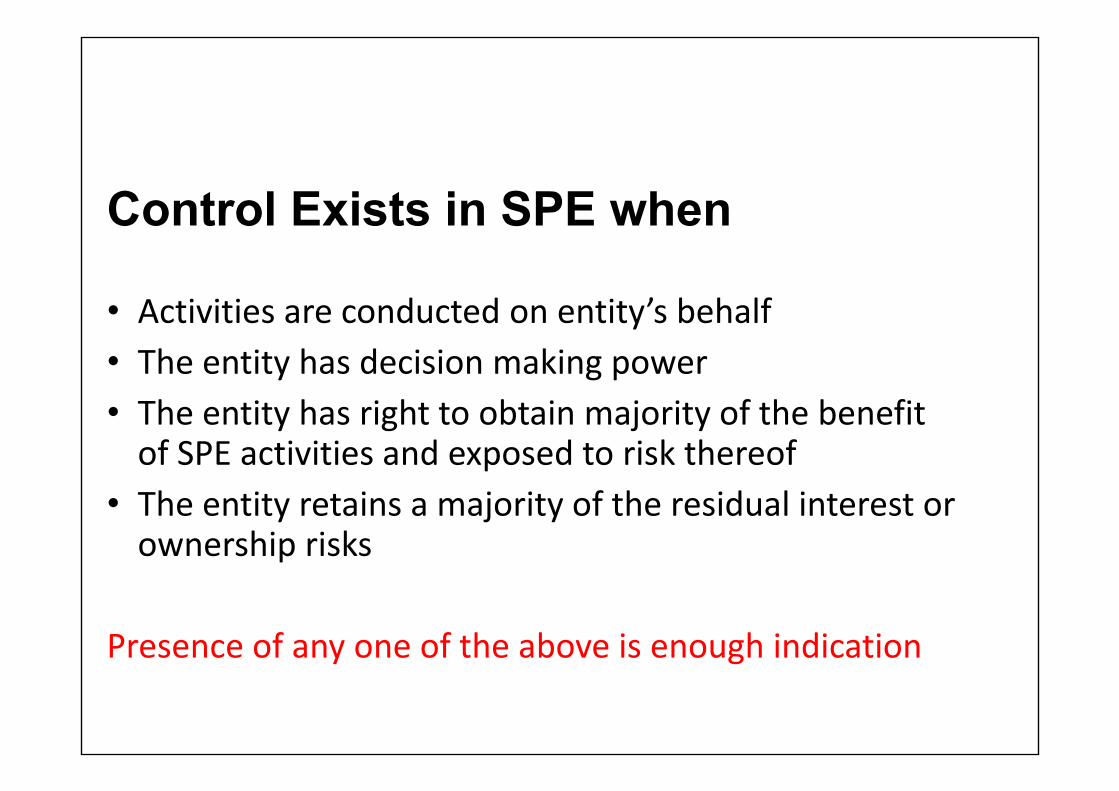

Special Purpose Entities should be consolidated where the substance of the relationship indicates that SPE is controlled by reporting entity.

Control Exists in SPE when

• Activities are conducted on entity’s behalf• The entity has decision making power • The entity has right to obtain majority of the benefit of SPE activities and exposed to risk thereof

• The entity retains a majority of the residual interest or ownership risks

Presence of any one of the above is enough indication

An investor controls an investee when it is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee.

IFRS 10 / Ind AS 110 – clause 6

New Definition ‐

An investor controls an investee if and only if the investor has all the following:

‐ power over the investee

‐ exposure, or rights, to variable returns from its

involvement with the investee

‐ the ability to use its power over the investee to affect the

amount of the investor's returns

Clause 7 of IFRS 10 / Ind AS 110

New Definition ‐

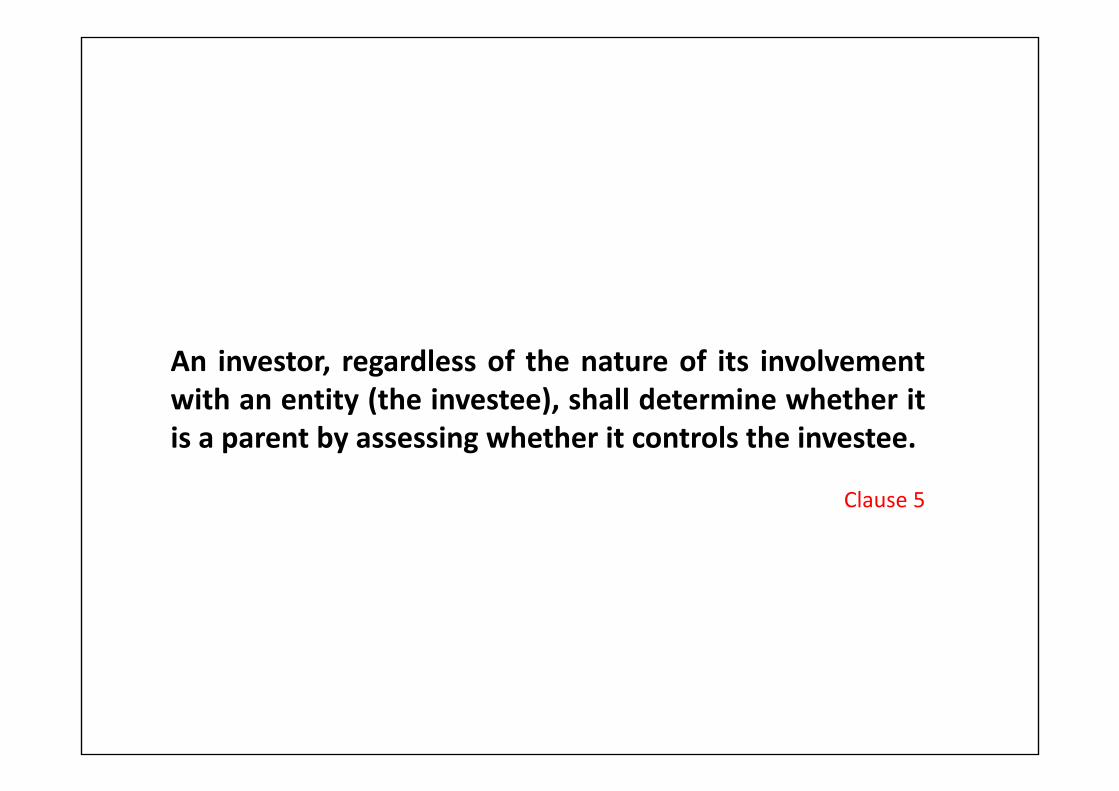

An investor, regardless of the nature of its involvementwith an entity (the investee), shall determine whether itis a parent by assessing whether it controls the investee.

Clause 5

CASE STUDY