india corporate health tracker - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

16 February 2017 Asia Pacific/India Equity Research

Banks

India Corporate Health Tracker Research Analysts

Ashish Gupta

91 22 6777 3895

Kush Shah

91 22 6777 3862

Prashant Kumar

91 22 6777 3942

SECTOR REVIEW

Stress rising, resolutions stalled

Figure 1: Share of debt with IC<1 at 41%

Source: Prowess, Company data, Credit Suisse

■ NPL formation likely to remain elevated. Our 3Q corporate health tracker

highlights that share of debt with companies with IC<1 stays high at 41%,

and 35% of debt is with chronically stressed corporates. Moreover,

companies with IC<1 are still witnessing a contraction in their profitability

(EBITDA -10% YoY). Even as operating profitability of some steel

companies improved, 65% still have IC<1. Additionally, 67% of power

companies' debt in our sample and 45% of telecom now has IC<1. In

addition to the 9.5% Gross NPAs, Indian banks have 4-8% of loans parked

in various stress classifications (restructured/SDR but standard) and as

most of these forbearances expire over next 12-18 months, it will keep

corporate NPA addition elevated.

■ Wall of provisioning ahead, without a Bad Bank. We estimate that

Indian banks need Rs860 bn of provisions on existing NPAs over the next

12 months as regulatory provisions are based on NPL vintage. As the NPA

spike from the RBI's AQR a year ago now migrates to next buckets,

provisioning needs will rise. Resolutions on most of the large NPLs have

not progressed even in sectors like steel that witnessed a cyclical upswing,

given the need for large haircuts and multiplicity of lenders. Therefore,

unless a government-sponsored bad bank is created to house a significant

share of the US$108 bn NPAs, provision costs will be high.

■ Raising provision estimates, cutting earnings; Cut Axis to NEUTRAL.

We are therefore cutting our earnings estimates for corporate lenders by 5-

10%, as we raise corporate impairment & provisioning estimates. We also

factor potential gains from stake sales in subs (general insurance) for ICICI

and SBI, resulting in lower earnings cuts. While, for Axis we still estimate

FY18 provisioning will be lower than FY17 we cut earnings and TP by ~7-

10%. Continue to prefer retail private banks (HDFCB, IIB)

10%

15%

20%

25%

30%

35%

40%

45%

10%

15%

20%

25%

30%

35%

40%

45%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

% of sample debt with companies with IC <1 % not covering interest in at least 4 quarters

16 February 2017

India Corporate Health Tracker 2

Focus charts

Figure 2: 37% of loans with IC<1 in the past 12 qtrs Figure 3: Overall EBITDA declined 2% QoQ

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 4: IC<1 firms' EBITDA declined 10% YoY Figure 5: 52% of steel debt has debt/EBITDA > 12x

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 6: 67% of power debt with IC<1 companies Figure 7: 45% of telecom debt with IC<1 companies

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 8: Ageing provs to result in 100bp credit cost Figure 9: Earnings cut 5-10% on higher credit cost

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 2 3 4 5 6 7 8 9 10 11 12

% of debt with companies corresponding to quarters when they had IC<1

-10

-5

0

5

10

15

20

25

0.0

1.0

2.0

3.0

4.0

5.0

4Q11

2Q12

4Q12

2Q13

4Q13

2Q14

4Q14

2Q15

4Q15

2Q16

4Q16

2Q17

EBITDA growth (% qoq) (RHS) IC coverage

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Sales EBITDA

All companies Co's with IC<1 in 2Q17

<6x, 1,325 , 32%

6x-12x, 649 , 16%

>12x, 2,117 , 52%

3Q17 Total Loans - Rs 4.1 tn

Down from 62% in 2Q

40%

45%

50%

55%

60%

65%

70%

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Power sector debt with IC<1 (Rs bn) Share of debt with IC<1 (%) (RHS)

15%

20%

25%

30%

35%

40%

45%

50%

-

500

1,000

1,500

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Telecom sector debt with IC<1 (Rs bn) Share of debt with IC<1 (%) (RHS)

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

IDBI

UCO

Unite

d

IOB

BoI

PNB

ALBK

BOM

CBoI

OBC

Andh

ra

Corp

BoB

Cana

ra

Union

India

n

PSB

SBI

ICIC

I

Synd

i…

Vijay

a

Axis

Ageing Credit Cost (%) - FY18E

-8% -8% -8%

-6%

-10%

-3%

-5%-5%

-6%

-8%

-12%

-8%

-4%

0%

SBI PNB BOI ICICI Axis

Change in earnings (%) FY18E FY19E

16 February 2017

India Corporate Health Tracker 3

3Q17: Stress rising, resolutions stalled

NPL formation likely to remain elevated

Our 3Q corporate health tracker highlights that share of debt with companies with IC<1 is

still high at 42%, and 35% of debt is with chronically stressed corporates. Moreover,

companies with IC<1 are still witnessing a contraction in their profitability (EBITDA -10%

YoY). Even as the operating profitability of some steel companies improved, 65% still have

IC<1. Additionally, 67% of our power companies' debt in our sample and 45% of telecom

debt now has IC<1. In addition to the 9.5% gross NPAs, Indian banks have 4-8% of loans

parked in various stress classifications (standard but restructured/SDR). As many of these

forbearances expire over the next 12-18 months it will keep corporate NPA addition

elevated, in our view.

Wall of provisioning ahead, without a Bad Bank

Over the past two quarters, the use of the strategic debt restructuring (SDR) structure has

been increasing by the banks. This is surprising given the lack of resolutions that have

been achieved through this structure. In addition, of the 30 cases that it was implemented

in, it has been successfully completed in none of the companies, with partial success only

in one company. The primary incentive appears to be the 18-month standstill on asset

classification that is available under this. Given the limited success in identifying buyers for

these assets, we expect that as the 18-month period expires, a large portion of these

loans will move from standard SDR to NPL classification.

We estimate that Indian banks need Rs860 bn of provisions on existing NPAs over the

next 12 months as regulatory provisions are based on NPL vintage. As the spike in NPAs

from RBI's AQR a year ago now migrates from sub-standard to doubtful, provisioning

needs will rise. Resolutions on most of the large NPLs have not progressed even in

sectors like steel that witnessed a cyclical upswing, given the need for large haircuts and

multiplicity of lenders. Therefore, unless a government sponsored bad bank is created to

house a significant share of the $108 bn NPAs, provision costs will be high.

Raising provision estimates, cutting earnings

Provisioning needs for the banks are likely to stay high on account of slippages from the

existing pool of recognized problem loans (SDR / Restructured / watch list) and ageing

related provisions post one year of the RBI's AQR exercise. As a result, we increase our

credit cost estimates for coverage banks to 1.5-1.9% with ageing-related provisions at 60-

160bp and as a result, our EPS goes down by 5-10% for corporate lenders. We also factor

potential gains from stake sales in subs (general insurance) for ICICI and SBI, resulting in

lower earnings cuts, while Axis sees larger FY18 cuts, as we increase NPL slippage

estimates as well.

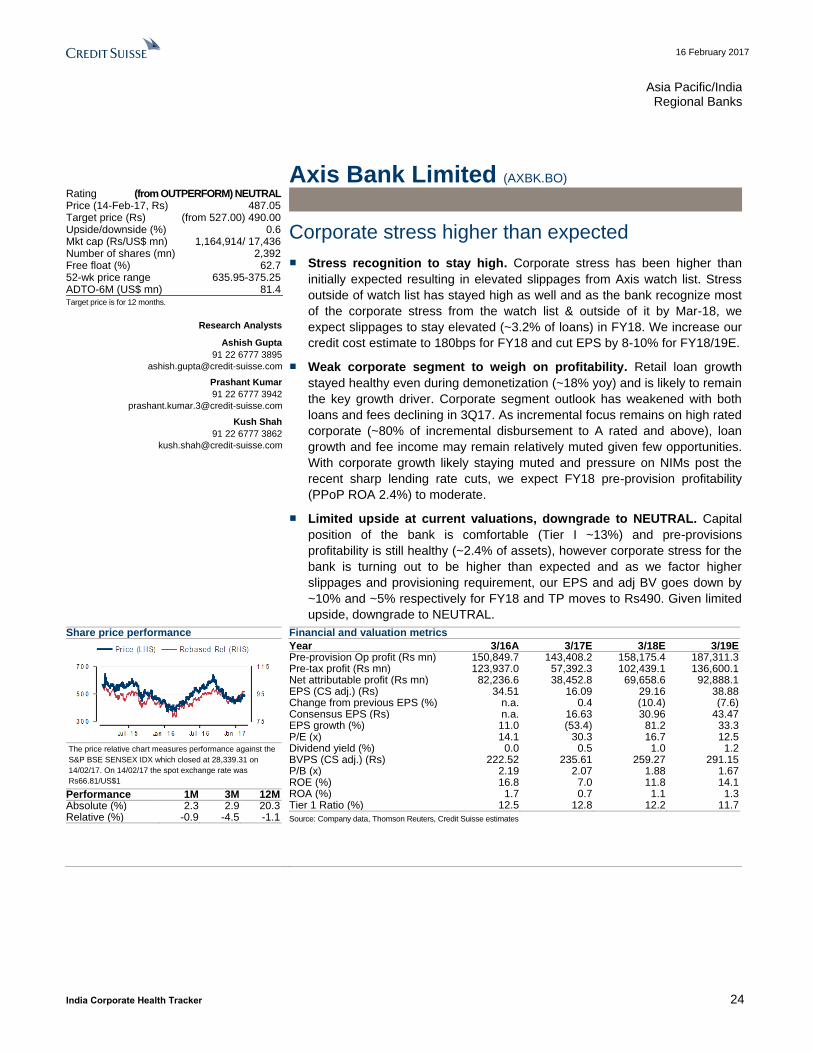

Downgrade Axis to Neutral

Corporate stress has been higher than initially expected resulting in elevated slippages

from Axis watch list. Stress outside of watch list has stayed high as well and as the bank

recognize most of the corporate stress from the watch list & outside of it by Mar-18, we

expect slippages to stay elevated (~3.2% of loans) in FY18. We increase our credit cost

estimate to 180bps for FY18 and cut EPS by 8-10% for FY18/19E. Our TP moves down to

Rs490 and at 1.8x FY18 book, given limited upside, we downgrade the stock to

NEUTRAL.

35% of debt is with chronically

stressed corporates

Ageing provision of Rs860bn in FY18E

1

6 F

eb

rua

ry 2

01

7

Ind

ia C

orp

ora

te H

ea

lth T

rac

ker

4

Valuation summary

Figure 10: Valuation summary

CS

Rating

CMP

(Rs)

Target

(Rs)

+/-

(%)

Mkt cap

($ bn)

P/B (x) P/Adj B (x) EPS (Rs) EPS growth (%) P/E (x) ROE (%) P/PPoP (x)

FY18E FY19E FY18E FY19E FY18E FY19E FY18E FY19E FY18E FY19E FY18E FY19E FY18E FY18E

Private Sector

HDFC Bank O 1,322 1,470 11% 50.6 3.5 3.0 3.5 3.0 68 83 22 22 20 16 19 20 12 9

ICICI O 281 316 13% 24.4 1.6 1.5 1.8 1.6 19 23 7 19 15 12 11 13 9 7

Kotak Mahindra N 784 827 5% 21.6 3.3 2.8 3.3 2.8 32 39 20 23 24 20 14 15 15 12

Axis N 488 490 0% 17.5 1.9 1.7 2.0 1.7 29 39 81 33 17 13 12 14 8 6

IndusInd O 1,316 1,400 6% 11.8 3.4 2.9 3.5 3.0 62 77 25 25 21 17 17 19 12 10

Yes Bank N 1,431 1,273 -11% 9.1 2.5 2.2 2.6 2.2 91 116 15 27 16 12 20 19 9 7

IDFC Bank N 62 68 10% 3.1 1.3 1.2 1.4 1.3 4 5 16 17 16 14 9 10 15 11

J&K Bank N 68 68 -1% 0.5 0.5 0.5 0.8 0.7 9 14 nm 63 8 5 7 10 2 2

Public Sector

SBI N 269 247 -8% 32.0 1.1 1.0 1.4 1.3 22 28 60 25 12 10 9 11 6 5

Bank of Baroda N 163 162 -1% 5.6 0.9 0.9 1.1 1.0 15 20 99 35 11 8 9 11 4 4

PNB U 140 94 -33% 4.5 0.7 0.7 1.2 1.1 14 19 52 35 10 7 7 9 3 3

Bank of India U 124 92 -26% 1.9 0.4 0.4 0.7 0.6 11 19 nm 68 11 6 4 6 2 2

Union Bank U 142 124 -12% 1.5 0.4 0.4 0.7 0.6 22 28 49 31 7 5 7 9 2 1

IOB U 26 19 -26% 0.9 0.5 0.5 1.1 0.8 1 2 nm 334 50 12 1 4 3 3

Non-bank fin

HDFC Ltd O 1,398 1,548 11% 33.2 5.4 4.9 5.4 4.9 54 62 10 16 26 23 22 23 18 15

Bajaj Finance U 1,040 670 -36% 8.5 4.7 3.8 4.8 3.9 39 47 12 18 26 22 20 19

Indiabulls O 813 885 9% 5.2 2.5 2.1 2.6 2.3 79 104 25 31 10 8 26 29

LIC Housing Fin O 550 635 16% 4.1 2.1 1.8 2.2 1.8 53 63 31 20 10 9 22 22

Shriram Transport O 934 1,070 15% 3.2 1.6 1.4 1.9 1.6 97 112 56 16 10 8 18 18 4 4

M&M Finance O 287 325 13% 2.4 2.1 1.8 3.8 3.1 18 29 66 62 16 10 14 20

Cholamandalam O 992 1,200 21% 2.3 3.1 2.5 3.9 3.2 59 83 32 40 17 12 19.9 23.2 8 6

SCUF O 1,894 2,210 17% 1.9 2.1 1.8 2.6 2.2 134 209 24 57 14 9 16 21

Bharat Financial N 820 720 -12% 1.7 3.2 2.6 3.3 2.7 55.9 56.8 26 2 15 14 25 20

Core Business

ICICI O 201 236 17.5 1.3 1.2 1.4 1.3 16 19 8 22 13 10 11 12 6 5

HDFC O 665 814 15.8 3.2 2.8 3.2 2.8 43 51 18 18 15 13 23 23 7 6

Source: Company data, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 5

NPL formation likely to remain elevated Corporate health continues to remain stressed, as our corporate health tracker does not

show any signs of recovery. With 3Q17 share of debt with interest cover (IC) < 1 having

increased to 41% (flat QoQ at 39% excluding the slip of Tata Motors in 3Q). Our sample of

3,700 companies has aggregate debt of ~US$520 bn.

The share of chronically stressed debt (having IC<1 for four or more of the past eight

quarters) increased further to 35%, despite the increase in share of debt with companies

that entered the list for the first time in the past two years (Tata Motors, JSW Energy), as

existing stressed companies continue to remain on the list as performance remains weak.

Share of debt with loss making companies remains stable at 32%.

Figure 11: Share of chronically stressed debt increased to ~35%

Source: Prowess, Company data, Credit Suisse

While share of debt with IC<1 was largely stable at ~30%, the share of chronic stress has

increased and is now at ~27%.

Figure 12: Share of chronic debt with IC<1 based on EBITDA also increased

Source: Prowess, Company data, Credit Suisse

The share of debt with companies not covering interest for the past 12 consecutive

quarters remains high at 37%. The quantum of debt with companies having an IC<1 for

the past eight consecutive quarters increased from Rs5.7 tn in 2Q to Rs7.1 tn in 3Q.

10%

15%

20%

25%

30%

35%

40%

45%

10%

15%

20%

25%

30%

35%

40%

45%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

% of sample debt with companies with IC <1 % not covering interest in at least 4 quarters

0%

5%

10%

15%

20%

25%

30%

35%

0%

5%

10%

15%

20%

25%

30%

35%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

% of sample debt with companies with IC <1 % not covering interest in at least 4 quarters

41% of debt with companies having

IC<1 in 3Q17

30% of debt with IC<1 based on EBITDA

16 February 2017

India Corporate Health Tracker 6

Figure 13: Rs7.1 tn of debt with companies having IC<1 for 12 consecutive qtrs

Source: Company data, Credit Suisse estimates

Metals, Power & construction remain major contributors

While stress is spread across sectors, metals, utilities and infra & construction continue to

contribute ~50% of the total stress of Rs15 tn. The share of industrials has increased on

account of Tata Motors' addition to the list.

Some of the other companies to be added are: JSW Energy, JBF Ind, Indiabulls Real

Estate and BGR Energy. Some of the companies that exited the list were Adani

Enterprises, IL&FS transport, Shipping Corp, Zuari Agro and Indian Hotels.

Figure 14: Stress remains concentrated in .. Figure 15: … infra and const and metal sectors

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 2 3 4 5 6 7 8 9 10 11 12

% of debt with companies corresponding to quarters when they had IC<1

Infra & construction

22%

Services4%

Airlines1%

Industrials12%

Diversified5%IT/ Telecom

10%

Metals17%

Textiles5%

Energy0%

Agri3%

Utilities14%

Pharma1%

CRE3%

Consumer3%

Total debt of Rs 15.1 tn

3Q17

Infra & construction

24%

Services7%

Airlines2%

Industrials8%Diversified

5%IT/ Telecom10%

Metals18%

Textiles4%

Energy0%

Agri3%

Utilities13%

Pharma1%

CRE2%

Consumer3%

Total debt of Rs 14.5 tn

2Q17

37% of IC<1 had IC<1 for 12 consecutive

quarters

Metals, Power and construction contribute

to ~50% of stress

16 February 2017

India Corporate Health Tracker 7

Figure 16: Larger stressed companies are yet to be recognised as NPAs

FY14 gross

borrowings

(Rs mn)

FY15 gross

borrowings

(Rs mn)

FY16 gross

borrowings

(Rs mn)

3Q EBIT 3Q Interest 3Q interest

cover

No. of quarters with

IC<1 0←→12*

Jaiprakash Associates Ltd. 729,792 761,804 691,366 -2,428 9,047 -0.3 ████████████

Tata Motors Ltd. 608,919 751,490 690,374 5,861 8,707 0.7 █

Adani Power Ltd. 443,969 448,993 532,002 10,413 14,302 0.7 ██████████

G M R Infrastructure Ltd. 437,787 479,766 498,014 1,127 1,964 0.6 ████████████

Idea Cellular Ltd. 206,519 268,770 482,806 2,002 9,669 0.2 ██

Videocon Industries Ltd. 407,681 454,055 476,795 361 6,342 0.1 ████████████

Reliance Communications Ltd. 408,910 395,000 473,320 -590 9,580 -0.1 ██████

Jindal Steel & Power Ltd. 365,321 457,184 470,250 2,493 8,353 0.3 ████████

Lanco Infratech Ltd. 375,370 399,024 454,362 -1,720 7,315 -0.2 ███████████

Bhushan Steel Ltd. 334,655 395,293 448,858 5,348 13,774 0.4 ████████████

Tata Power Co. Ltd. 403,092 421,473 416,446 6,518 7,010 0.9 ███

Steel Authority Of India Ltd. 253,067 298,980 344,312 -7,127 6,108 -1.2 ████████

G V K Power & Infrastructure Ltd. 226,268 251,988 271,709 31 112 0.3 ████████████

Jaiprakash Power Ventures Ltd. 275,029 321,951 257,264 1,047 4,472 0.2 █████████

Reliance Infrastructure Ltd. 242,891 257,660 254,729 -855 11,474 -0.1 █████████

Alok Industries Ltd. 200,217 182,092 229,192 -2,999 8,561 -0.4 ███████

K S K Energy Ventures Ltd. 143,453 191,874 203,468 114 5,405 0.0 ███████████

Mahanagar Telephone Nigam 144,344 167,004 179,424 -5,835 3,823 -1.5 ████████████

J S W Energy Ltd. 101,065 92,941 155,231 4,131 4,229 1.0 █

Amtek Auto Ltd. 152,269 176,630 147,043 -462 3,662 -0.1 ████████

Aban Offshore Ltd. 132,555 140,671 146,458 641 2,746 0.2 █████

Rattanindia Power Ltd. 102,164 109,837 137,948 1,429 2,491 0.6 ███████████

Monnet Ispat & Energy Ltd. 107,621 125,074 127,371 -1,142 2,771 -0.4 ███████████

Hindustan Construction Co. Ltd. 111,500 121,708 114,466 1,304 1,947 0.7 ██████████

Jet Airways (India) Ltd. 105,851 122,509 108,904 2,030 2,208 0.9 ██████████

Electrosteel Steels Ltd. 97,620 102,933 113,040 -1,552 2,827 -0.5 ████████████

I V R C L Ltd. 81,984 91,681 108,626 -820 1,754 -0.5 ████████████

J B F Industries Ltd. 63,952 86,962 106,112 336 388 0.9 █████

Tata Teleservices 64,145 71,568 104,267 -698 3,510 -0.2 ████████████

Jindal Stainless Ltd. 117,258 113,260 102,916 2,632 2,677 1.0 ████████████

Era Infra Engg. Ltd. 84,469 94,869 65,091 -949 2,326 -0.4 ████████████

Jaypee Infratech Ltd. 83,962 91,018 101,064 1,242 1,888 0.7 ██████

Unitech Ltd. 77,536 91,031 100,929 487 578 0.8 █████████

Shree Renuka Sugars Ltd. 98,087 93,238 90,049 161 891 0.2 ██████████

Bharati Defence & Infrastructure 13,858 65,023 89,384 -293 287 -1.0 ████████████

Ballarpur Industries Ltd. 68,902 73,883 85,557 -2,417 2,408 -1.0 █████████

Sadbhav Infrastructure Project 50,205 64,483 82,107 1,814 2,623 0.7 ████████

Reliance Defence & Engg. Ltd. 53,356 72,394 80,164 -461 1,425 -0.3 ███████████

Punj Lloyd Ltd. 53,324 71,622 80,581 -217 2,245 -0.1 ████████████

Sterling Biotech Ltd. 58,678 45,985 79,197 -608 969 -0.6 ████████████

Bajaj Hindusthan Sugar Ltd. 62,747 77,585 70,766 1,243 2,009 0.6 ██████████

Binani Industries Ltd. 51,217 58,769 64,481 -57 137 -0.4 ███████████

Moser Baer India Ltd. 45,063 48,085 61,962 -380 535 -0.7 ████████████

Indiabulls Real Estate Ltd. 35,538 60,720 61,809 109 1,402 0.1 ██

Castex Technologies Ltd. 45,617 57,462 57,033 -724 2,082 -0.3 ███████

S E L Manufacturing Co. Ltd. 45,377 58,503 59,191 -1,710 158 -10.8 ████████████

Essar Shipping Ltd. 53,581 53,383 56,423 64 940 0.1 ████████████

Ruchi Soya Inds. Ltd. 38,635 37,480 55,446 185 2,587 0.1 ████████

Kesoram Industries Ltd. 46,248 46,248 50,425 -248 688 -0.4 ████████████

* Column length indicates no. of qtrs for which IC is <1 ranging from 1 to 12; companies marked in red have turned NPA, while in orange are restructured accounts, blue are accounts that have been partially recognised as NPA and the ones in green have had strategic debt restructuring undertaken by the banks Source: Prowess, Company data, Credit Suisse Estimates

16 February 2017

India Corporate Health Tracker 8

Overall profitability remains weak

Overall EBITDA growth was stable at 9% YoY (on a low base) but remained weak,

declining 2% QoQ. EBIT declined 4% QoQ, while interest costs increased 4% QoQ

resulting in interest cover falling to 2.2x versus 2.4x in 2Q17. Net profit was also down

12% QoQ.

Figure 17: EBITDA growth remained negative QoQ, as aggregate IC eased to

2.2x

Source: Prowess, Company data, Credit Suisse

No improvement in performance of stressed firms

While overall corporate sector EBITDA grew ~9% YoY, the performance of stressed

companies (with an IC<1 in 2Q17) remained weak declining 10% YoY with sales falling

15% YoY. Profitability remained weak, as the net loss for the companies with IC<1 in

2Q17 remained large at ~Rs170 bn in 3Q17 and these companies have reported losses

for 14 of the past 15 quarters.

Figure 18: Performance of IC<1 firms still weak ... Figure 19: … as losses continue to remain large

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

-10

-5

0

5

10

15

20

25

0.0

1.0

2.0

3.0

4.0

5.0EBITDA growth (% qoq) (RHS) IC coverage

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Sales EBITDA

All companies Co's with IC<1 in 2Q17

-200,000

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

Net profit (Rs mn)

Aggregate Interest cover declined to 2.2x

Ebitda for co's with IC<1 in 2Q declined 10% yoy, net loss at

Rs170bn

16 February 2017

India Corporate Health Tracker 9

'House of debt' still to see a turnaround

Performance of our "house of debt" companies continues to remain weak. Overall

profitability has declined further, with EBITDA down 4% QoQ and net profits declined 41%

YoY. Aggregate interest cover remained weak at 0.9x with debt to EBITDA at 7.8x. Eleven

of the 19 companies reported losses this quarter, with 13 companies having an IC<1.

Figure 20: Performance of house of debt companies remains weak, with aggregate interest cover < 1x

3Q17 2Q17 3Q16

EBITDA Net profit Debt/

EBITDA (x)

Int. cover

(x)

EBITDA Net profit Debt/

EBITDA (x)

Int. cover

(x)

EBITDA Net profit Debt/

EBITDA(x)

Int. cover

(x)

Adani Power 16,490 (3,236) 8.1 0.7 18,211 (1,134) 7.4 0.9 20,077 1,018 6.5 1.1

Adani Ports & SEZ 13,707 8,482 4.1 3.6 14,515 10,959 3.9 3.9 10,531 6,373 4.7 2.9

Adani Enterprises 5,573 2,755 8.6 1.0 3,874 363 12.3 0.7 4,383 1,754 11.4 1.0

Adani Transmission 4,714 993 5.0 1.6 4,731 995 5.0 1.3 4,743 799 4.1 1.4

Essar Shipping 407 (836) 19.4 0.1 517 (620) 15.3 0.2 676 (1,096) 19.8 (0.4)

G M R Infra * 1,167 (3,814) 106.7 0.6 2,532 (7,003) 49.2 1.4 13,566 (3,480) 8.9 0.7

G V K Power & Infra * 31 (7) 2,163.3 0.3 (88) (134) (771.0) (0.7) 3,962 (3,747) 16.5 0.3

Jaiprakash Ass (234) (10,950) (309.9) (0.3) (859) (7,812) (84.2) (0.3) 2,419 (8,306) 31.9 0.0

Jaiprakash Power 2,325 (1,730) 27.5 0.2 2,791 (1,617) 22.9 0.3 3,732 (1,403) 16.1 0.5

Jaypee Infra 1,354 (414) 16.9 0.7 110 (1,318) 208.9 0.0 2,077 (207) 11.6 0.8

JSW Steel 28,669 7,157 3.8 2.1 29,469 6,469 3.7 2.1 8,892 (9,844) 11.5 0.1

JSW Energy 6,575 180 5.6 1.0 9,627 2,149 3.8 1.6 11,913 3,219 3.3 2.1

Lanco Infra 501 (8,842) 226.1 (0.2) 4,443 (2,931) 25.5 0.3 4,275 1,512 22.4 0.3

Reliance Infra 4,328 3,659 17.3 (0.1) 9,906 5,598 7.5 0.6 6,541 4,442 10.2 0.7

Reliance Power 11,546 2,757 7.3 1.2 11,443 2,721 7.3 1.4 12,297 3,518 6.9 1.6

Reliance Comm 11,060 (4,880) 10.7 (0.1) 15,000 620 7.9 0.8 17,820 1,980 6.0 1.3

Reliance Defence 41 (1,327) 525.5 (0.3) 115 (1,163) 185.2 (0.3) (1,270) (2,936) (15.5) (1.5)

Vedanta 58,775 29,851 3.4 2.9 46,632 22,782 4.3 2.2 31,141 4,997 6.3 1.0

Videocon Ind 1,830 (5,098) 65.1 0.1 2,227 (3,819) 53.5 0.1 4,088 (844) 27.8 0.4

Total 168,859 14,700 8.9 0.9 175,192 25,106 8.5 1.0 161,863 (2,251) 8.9 0.8

Total (ex. GMR & GVK) 167,661 18,521 7.8 0.9 172,749 32,243 7.5 1.0 144,335 4,976 8.7 0.8

*1Q & 2Q results for GMR & GVK are standalone and hence yoy numbers are not comparable Source: Prowess, Company data, Credit Suisse

16 February 2017

India Corporate Health Tracker 10

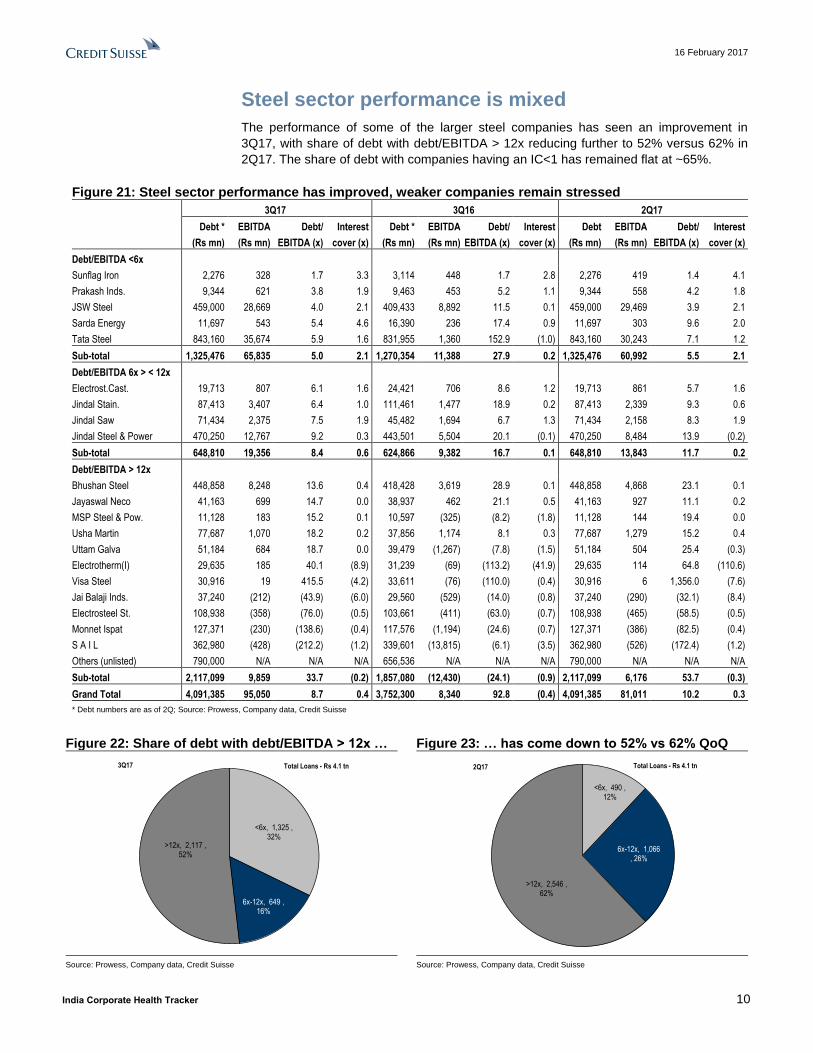

Steel sector performance is mixed

The performance of some of the larger steel companies has seen an improvement in

3Q17, with share of debt with debt/EBITDA > 12x reducing further to 52% versus 62% in

2Q17. The share of debt with companies having an IC<1 has remained flat at ~65%.

Figure 21: Steel sector performance has improved, weaker companies remain stressed

3Q17 3Q16 2Q17

Debt *

(Rs mn)

EBITDA

(Rs mn)

Debt/

EBITDA (x)

Interest

cover (x)

Debt *

(Rs mn)

EBITDA

(Rs mn)

Debt/

EBITDA (x)

Interest

cover (x)

Debt

(Rs mn)

EBITDA

(Rs mn)

Debt/

EBITDA (x)

Interest

cover (x)

Debt/EBITDA <6x

Sunflag Iron 2,276 328 1.7 3.3 3,114 448 1.7 2.8 2,276 419 1.4 4.1

Prakash Inds. 9,344 621 3.8 1.9 9,463 453 5.2 1.1 9,344 558 4.2 1.8

JSW Steel 459,000 28,669 4.0 2.1 409,433 8,892 11.5 0.1 459,000 29,469 3.9 2.1

Sarda Energy 11,697 543 5.4 4.6 16,390 236 17.4 0.9 11,697 303 9.6 2.0

Tata Steel 843,160 35,674 5.9 1.6 831,955 1,360 152.9 (1.0) 843,160 30,243 7.1 1.2

Sub-total 1,325,476 65,835 5.0 2.1 1,270,354 11,388 27.9 0.2 1,325,476 60,992 5.5 2.1

Debt/EBITDA 6x > < 12x

Electrost.Cast. 19,713 807 6.1 1.6 24,421 706 8.6 1.2 19,713 861 5.7 1.6

Jindal Stain. 87,413 3,407 6.4 1.0 111,461 1,477 18.9 0.2 87,413 2,339 9.3 0.6

Jindal Saw 71,434 2,375 7.5 1.9 45,482 1,694 6.7 1.3 71,434 2,158 8.3 1.9

Jindal Steel & Power 470,250 12,767 9.2 0.3 443,501 5,504 20.1 (0.1) 470,250 8,484 13.9 (0.2)

Sub-total 648,810 19,356 8.4 0.6 624,866 9,382 16.7 0.1 648,810 13,843 11.7 0.2

Debt/EBITDA > 12x

Bhushan Steel 448,858 8,248 13.6 0.4 418,428 3,619 28.9 0.1 448,858 4,868 23.1 0.1

Jayaswal Neco 41,163 699 14.7 0.0 38,937 462 21.1 0.5 41,163 927 11.1 0.2

MSP Steel & Pow. 11,128 183 15.2 0.1 10,597 (325) (8.2) (1.8) 11,128 144 19.4 0.0

Usha Martin 77,687 1,070 18.2 0.2 37,856 1,174 8.1 0.3 77,687 1,279 15.2 0.4

Uttam Galva 51,184 684 18.7 0.0 39,479 (1,267) (7.8) (1.5) 51,184 504 25.4 (0.3)

Electrotherm(I) 29,635 185 40.1 (8.9) 31,239 (69) (113.2) (41.9) 29,635 114 64.8 (110.6)

Visa Steel 30,916 19 415.5 (4.2) 33,611 (76) (110.0) (0.4) 30,916 6 1,356.0 (7.6)

Jai Balaji Inds. 37,240 (212) (43.9) (6.0) 29,560 (529) (14.0) (0.8) 37,240 (290) (32.1) (8.4)

Electrosteel St. 108,938 (358) (76.0) (0.5) 103,661 (411) (63.0) (0.7) 108,938 (465) (58.5) (0.5)

Monnet Ispat 127,371 (230) (138.6) (0.4) 117,576 (1,194) (24.6) (0.7) 127,371 (386) (82.5) (0.4)

S A I L 362,980 (428) (212.2) (1.2) 339,601 (13,815) (6.1) (3.5) 362,980 (526) (172.4) (1.2)

Others (unlisted) 790,000 N/A N/A N/A 656,536 N/A N/A N/A 790,000 N/A N/A N/A

Sub-total 2,117,099 9,859 33.7 (0.2) 1,857,080 (12,430) (24.1) (0.9) 2,117,099 6,176 53.7 (0.3)

Grand Total 4,091,385 95,050 8.7 0.4 3,752,300 8,340 92.8 (0.4) 4,091,385 81,011 10.2 0.3

* Debt numbers are as of 2Q; Source: Prowess, Company data, Credit Suisse

Figure 22: Share of debt with debt/EBITDA > 12x … Figure 23: … has come down to 52% vs 62% QoQ

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

<6x, 1,325 , 32%

6x-12x, 649 , 16%

>12x, 2,117 , 52%

3Q17 Total Loans - Rs 4.1 tn

<6x, 490 , 12%

6x-12x, 1,066 , 26%

>12x, 2,546 , 62%

Total Loans - Rs 4.1 tn2Q17

16 February 2017

India Corporate Health Tracker 11

While the recognition of steel sector stress has been higher at banks compared to other

sectors, with NPA recognition at ~30-50% for the larger banks, stress within the steel

sector remains high, with ~52% of debt having debt/EBITDA > 12x and 60% of debt with

companies having IC<1.

Figure 24: Share of debt with companies having

debt / EBITDA > 12x has come down to 52% …

Figure 25: … while share of debt with IC<1

companies has remained at ~60%

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

Stressed steel companies continue to report losses

While some of the larger companies (Tata Steel and JSW Steel) reported a profit this

quarter, the stressed steel companies continue to report losses, with companies like SAIL,

Bhushan Steel, Monnet Ispat and Electrosteel continued to report large losses. The

aggregate net loss for the steel sector for 3Q17 was ~Rs26 bn.

Figure 26: Interest costs rosed YoY, resulting in … Figure 27: … stressed firms still making losses

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

48%

86% 86% 88%

53%

62%

52%

0

100

200

300

400

500

600

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Share of debt with Debt / Ebitda > 12x Avg Steel Price US$/t (RHS)

15%

25%

35%

45%

55%

65%

75%

85%

95%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Steel sector debt with IC<1 (Rs bn) Share of debt with IC<1 (%) (RHS)

-

2

4

6

8

10

12

14

16

Bhushan Steel JSPL SAIL ElectrosteelSteel

Monnet Ispat

3Q16 3Q17Interest expense (Rs bn)

(18)

(16)

(14)

(12)

(10)

(8)

(6)

(4)

(2)

-

JSPL ElectrosteelSteel

Monnet Ispat Bhushan Steel SAIL

3Q16 2Q17 3Q17Net profit (Rs bn)

60% of steel debt has IC<1 in 3Q, 52% had

Debt/Ebitda > 12x

16 February 2017

India Corporate Health Tracker 12

Power sector stress rising

Stress within the power sector continues to rise, as most of the larger companies saw

EBITDA decline in 3Q, with EBITDA for the sector declining 13% YoY and 18% QoQ and

net profit falling 7% YoY and 34% QoQ. Private sector plant load factors (PLF) increased

QoQ, but were lower YoY and remain weak at ~56%, with merchant tariffs remaining low

at <Rs2.5/kWh. There have been no PPAs signed during the quarter either and stress is

likely to continue rising.

Figure 28: PLF and merchant tariffs remain low Figure 29: EBITDA has fallen for most companies

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

As profitability remains muted, the share of debt with interest cover < 1 increased to 67%

in 3Q versus 63% in 2Q, with Rs3.8 tn of debt now with companies having IC<1. Most of

the larger companies have seen interest cover decline this quarter, with IC<1 for

companies such as Reliance Infra, JP Power, Rattan India, Adani Power (despite

compensatory tariff's) Tata Power and JSW Energy.

Figure 30: Share of power sector debt with IC<1

increased further to 67%

Figure 31: As most of the larger companies saw

interest cover fall this quarter

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

57.4%

64.5%63.7%

58.9%

53.5%

56.2%

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Private Sector PLF (%) Merchat Price (Rs/Mw) (RHS)

-

5

10

15

20

25

Adani Power R Power Tata Power JSW Energy R Infra JP Power Rattan India

3Q16 2Q17 3Q17EBITDA (Rs bn)

40%

45%

50%

55%

60%

65%

70%

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Power sector debt with IC<1 (Rs bn) Share of debt with IC<1 (%) (RHS)

(0.5)

-

0.5

1.0

1.5

2.0

2.5

R Power JSWEnergy

TataPower

AdaniPower

RattanIndia

JP Power R Infra

3Q16 2Q17 3Q17Interest Cover (x)

Private power sector PLF remains low

at ~56%

67% of power sector debt has IC<1

in 3Q vs 63% in 2Q

16 February 2017

India Corporate Health Tracker 13

Telecom sector performance deteriorates

The performance of telecom companies has continued to worsen, with sector interest

cover turning negative in the 3Q. Losses for the stressed telecom companies widened

further. Sector EBITDA declined 16% YoY and 14% QoQ, and the sector posted a net loss

of Rs11 bn this quarter. Share of debt within the telecom sector with IC<1 companies

remained high at 45%. With recent spectrum auctions, debt levels for the sector would

increase further also resulting in increase in interest costs, impacting debt servicing.

Figure 32: Sector EBITDA has fallen 14% QoQ Figure 33: Share of debt with IC<1 firms high at 45%

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

The performance of stressed companies weakened further, with EBITDA declining 24%

QoQ and EBIT turning negative in 3Q, while interest costs were up 63% YoY. Losses

widened for most of the stressed companies, as they reported an aggregate loss of

Rs21 bn.

Figure 34: Stressed telcos saw negative EBIT in 3Q Figure 35: With losses widening for most firms

Source: Prowess, Company data, Credit Suisse Source: Prowess, Company data, Credit Suisse

0.0

0.5

1.0

1.5

2.0

2.5

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

EBITDA (Rs bn) Interest expenses IC coverageTelecom sector

Rs bn

15%

20%

25%

30%

35%

40%

45%

50%

-

200

400

600

800

1,000

1,200

1,400

1,600

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Telecom sector debt with IC<1 (Rs bn) Share of debt with IC<1 (%) (RHS)

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0

10

20

30

40

50

60

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

EBITDA Interest expenses IC coverageStressed telecom co's

Rs bn

(10)

(8)

(6)

(4)

(2)

-

2

4

6

8

10

Tata Comm Idea Tata Tele R Comm MTNL

3Q16 2Q17 3Q17Net profit (Rs bn)

45% of telecom sector debt had IC<1 in 3Q.

Losses for the weaker telecom companies widened

16 February 2017

India Corporate Health Tracker 14

Wall of provisioning ahead, without a Bad Bank

Forbearances to expire in 12-18 months

Currently, 4-8% of stressed loans are sitting as standard under various classifications. As

many of these forbearances expire in the next 12-18 months, we expect corporate NPL

slippages to remain elevated.

Figure 36: Reported standard restructured & SDR loans at 4-8% for PSU banks

Source: Company data, Credit Suisse estimates

As highlighted, the power sector remains stressed, with 67% of debt with companies

having IC<1, and as per our bottom-up analysis, ~Rs1.2 tn of debt is with stressed power

projects.

Figure 37: Infrastructure constitutes ~40% of

system restructured loans Figure 38: Infra restructured is ~34-57% of total

Source: RBI, Credit Suisse * Only power for SBI & IOB; Source: Company data, Credit Suisse estimates;

On a bottom-up basis, we have identified some of the larger stressed power projects,

which have seen large cost overruns or where PLFs are low. We have also included the

gas-based plants which continue to operate at low PLFs given the lack of gas availability.

This list of projects has debt amounting to ~Rs1.3 tn and while some are classified as

restructured and very few as NPLs at some banks, a majority continue to be classified as

standard.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Standard Restrd Standard SDR Standard Watch list(%) of loans

Power 21%

Steel10%

Other Infra 17%

Textile 3%

Others49%

Total Restructured Loans of Rs2,000bn57%

46%

37%36%

34%

29%

0%

10%

20%

30%

40%

50%

60%

PNB BOI Canara Union IOB* SBI*

Infra/power as % of restructured

4-8% of loans are classified as standard

and in various classifications

16 February 2017

India Corporate Health Tracker 15

Figure 39: Power projects with total debt of ~Rs1,200 bn being stressed

Company Project Capacity Operational /

CoD

Recognitio

n

Debt (Rs bn)

Coal Based

Projects

GMR Chattisgarh - Raikheda 1,370 Operational SDR 94

GVK Alaknanda 330 Operational 35

GVK Goindwal Sahib 540 Operational 34

Jaypee Bara I 1,980 Operational 110

Lanco Amarkantak III & IV 1,320 FY18 80

Lanco Vidarbha 1,320 FY19 55

Lanco Babandh 1,320 FY18 55

Essar Mahan 1,200 Operational 77

Essar Tori 1,200 FY18 65

JP Power Bara 1,980 Operational 110

KSK Mahanadi 3,600 Operational 124

ACPL Athena Chhattisgarh 1,200 Operational 60

East Coast Energy Kakarapalli 1,320 FY18 40

DB Power Limited 582 Operational 30

Meenakshi Energy 1,000 Operational 40

Total 1,009

Gas Based

Projects

GMR Kakinada 220 Operational 10

GMR Vemagiri I 370 Operational 8

GMR Rajahmundry 768 Operational SDR 35

GVK Jegurupadu - Phase I 455 Operational 13

GVK Gautami Power 469 Operational 13

Lanco Kondapalli I 368 Operational 23

Lanco Kondapalli II 366 Operational 8

Lanco Kondapalli III 742 Operational 23

Reliance Power Samalkot expansion 2,400 Operational 50

Essar Vadinar 890 Operational 18

Essar Hazira 270 Operational 7

Reliance Samalkot 2,620 50

Total 258

Source: Company data, Credit Suisse estimates

Figure 40: Power sector recognised

impaired loans at ~17%

Figure 41: Recognition of NPA

remains low in the power sector

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

NPLs, 355, 7%

Restructured , 519, 10%

Stressed -unrecognised ,

716, 14%

Standard, 3,710, 70%

Total Power sector loans - Rs 5,300bn

17%

4%

23%

8% 6%3% 5% 3%

17%

26%

2%

0%

10%

20%

30%

40%

ICICI Axis PNB Union BOB SBI OBC BOI

Power sector NPLs Watchlist (%)

Rs1.2tn of debt with stressed

power projects

16 February 2017

India Corporate Health Tracker 16

Increasing use of SDR

Over the past two quarters, the use of the strategic debt restructuring (SDR) structure has

been increasing by the banks. This is surprising given the lack of resolutions that have

been achieved through this structure. In addition, of the 30 cases that it was implemented

in, it has been successfully completed in none of the companies, with partial success only

in one company. The primary incentive appears to be the 18-month standstill on asset

classification that is available under this. Given the limited success in identifying buyers for

these assets, we expect that as the 18-month period expires, a large portion of these

loans will move from standard SDR to NPL classification.

While the declared SDR of banks adds up to ~Rs700 bn as of 31st Dec'16, based on the

list of companies where SDR has been announced, it amounts to Rs2.4tn, of which ~50%

are standard.

Figure 42: List of standard accounts is growing rapidly

Companies under SDR

Total debt (Rs bn) Debt to mkt cap (x)

Bhushan Power 373

Jaiprakash Associates 300 11.1

Alok Industries 260 56.0

Jaiprakash Power 250 16.1

Monnet Ispat 118 49.6

Gammon India 113 24.4

Electrosteel Steel 106 10.6

GMR Chhattisgarh 94 5.8

IVRCL 93 21.6

Ballarpur Industries 72 6.6

ABG Shipyard 70 46.4

Patel Engg 54 4.3

Transtroy 43

Coastal Projects 40

GMR Rajahmundry 40 5.8

Essar Projects 38

Shiv-Vani Oil 36 29.0

Adhunik Power and Natural Resources 31

Visa Steel 31 13.9

Educomp Solutions 31 21.8

Jyoti structures 30 29.5

Surana Industries 28 173.2

Diamond Power 23 2.1

Rohit Ferrotech 23 27.3

Lanco Teesta 22 44.5

GOL Offshore 20 11.4

AMW 14

Usher Agro 9 9.8

Tilaknagar Industries 8 4.4

Total 2,369

Of which now NPA 1,253

% already NPA 53%

Source: Company data, Credit Suisse estimates

Declared SDR by banks is ~Rs700bn, while

based on list of co's with SDR announced

amounts to Rs2.4tn

16 February 2017

India Corporate Health Tracker 17

ARC sales have dropped off

The private ARCs' role in the resolution of the stress loans has also not expanded despite

the government relaxing foreign ownership for ARCs (100% FDI in ARCs was allowed in

May-16). The sale of NPAs to ARCs declined 50% in FY16 and has likely fallen further in

FY17.

The change in regulations regarding the sale of NPA's to ARC's in Sep-16, caps the

maximum holding of SR's by the seller bank to 50% from Apr-17 and 10% from Apr-18 will

result in sale of assets to ARC's slowing down even further. If the bank hold more than

50% or 10% respectively, provisioning would need to be made treating the SR's as NPAs.

Figure 43: Sales to ARCs slowed in FY16

Figure 44: SRs outstanding are <1% of loans for

most banks

Source: EnY, Company data, Credit Suisse estimates Source: Company data, Credit Suisse

0

50

100

150

200

250

300

350

400

450

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Book value of assets acquired by ARC's

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

CB

oI

Indi

an

UC

O

ALB

K

BoI

ICIC

I

Den

a

Can

ara

Syn

dica

te

IDB

I

Axi

s

Uni

ted

Uni

on

Kot

ak SB

I

PN

B

IOB

Vija

ya

Yes

Indu

sInd

BoB

BO

M

SR's o/s as a % of advances

ARC sales have slowed and likely to

slow further

16 February 2017

India Corporate Health Tracker 18

RBI tools have not worked as planned

While the RBI has announced several schemes for dealing with stressed assets, these

have not been successful in dealing with the stressed loan problem.

Figure 45: RBI dispensations have not worked as expected

Scheme Quantum Step Pros Cons Failure

Sale to Asset

Reconstruction

Companies

Only ~Rs200

bn of the Rs7.3

tn of NPAs

were sold in

FY16

Increase in share of cash

component in ARC sale

from 5% to 15%.

(1) Increase in cash

component to 15%

resulted in more realistic

valuations

(1) Depreciation in value of

investment will only be realised after

a year

(1) Asset sales have happened largely in the

form of Security receipts, with cash component

remaining small

Allowing banks to write off

losses on ARC sales over

8 quarters.

(2) Allowing loss to be

spread over 8 quarters

resulted in wider

adoption

(2) Higher cash component has

resulted in banks requiring to take

larger losses, as ARC's are willing

to pay less

(2) Quantum of assets sold has also been small

and less than 1% of loans

Cap on holding of SRs by

seller banks.

(3) To result in better

pricing of sales

(3) With quantum of SRs that can be held to be

reduced to 50% and further to 10% by selling

banks, sales to ARCs are likely to slow further.

Strategic Debt

Restructuring

(SDR)

~50% of SDR

cases have

already turned

NPA

SDR allows banks to take

over 51% equity of

stressed companies by

conversion of interest or

principal, and gives them

18 months to find a new

buyer or management

(1) Lenders can force

management change in

stressed companies

(1) Banks misuse SDR to delay

NPA recognition, as asset

classification remains stand-still for

18 months

(1) Majority of the companies on which SDR

has been implemented have been failed cases

of corporate debt restructuring (CDR)

(2) Lenders can acquire

majority shareholding in

the company

(2) Banks end up with equity

ownership of bad companies

(2) Banks have been unable to find new buyers

for these assets, with the government now

looking to force PSUs to acquire stakes.

(3) % of debt converted to acquire

51% equity would be extremely

small as a % of total debt, leaving

debt levels unsustainably high

(3) With debt being significantly higher than

market cap, share of debt to be converted has

also been smaller.

5:25 refinancing Allows refinancing of large

(> Rs 500 crore) long-

gestation operational

projects in infrastructure

and core industries, with

periodic re-financing every

5-7 years.

(1) Allows refinancing for

operating infrastructure

projects that have a

longer gestation period

(1) Delaying recognition of problem,

even for projects which are clearly

stressed

(1) 5:25 has been used in a large no. of cases

where the asset was stressed and despite

pushing back of principal repayments, the firms

were unable to meet interest obligations.

(2) Does not bifurcate unsustainable

debt of over-leveraged companies,

resulting in refinancing of

unserviceable debt

(2) Has resulted in additional loans being given

to stressed companies and the required haircut

has not been taken.

Scheme for

Sustainable

Structuring of

Stressed Assets

(S4A)

Only one case

has been

completed

successfully till

date

Scheme for large (> Rs

500 crore) projects that

have commenced

operations and where

sustainable debt through

independent techno

economic viability study is

not < 50% of total debt.

Part A as sustainable

portion and Part B as

unsustainable.

(1) Right sizes deb, by

splitting it into

sustainable and

unsustainable portion

(1) Unsustainable portion of debt

(Part B) is converted to equity /

convertible preference shares

(1) Banks have yet to implement S4A, with only

a couple of companies undertaking this

scheme.

(2) Requires outside

agencies to arrive at the

serviceable levels of

debt

(2) No fresh moratorium or

extension of interest / principal

repayments on Part A.

(3) Allows lenders to

take over the project

(3) If there is a change in

management, there is no change in

asset classification as per SDR

rules; if no change in promoters,

asset classification stays same for

90 days, pushing back recognition

by banks.

Source: Company data, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 19

Ageing to result in >100bp of credit cost

We estimate that Indian banks need Rs860 bn of provisions on existing NPAs over the

next 12 months, as regulatory provisions are based on NPL vintage. As the spike in NPAs

from the RBI's AQR a year ago now migrates from sub-standard to doubtful, provisioning

needs will rise. Resolutions on most of the large NPLs have not progressed even in

sectors such as steel that witnessed a cyclical upswing, given the need for large haircuts

and multiplicity of lenders. Therefore, unless a government-sponsored bad bank is created

to house a significant share of the US$108 bn of NPAs, provision costs will be high.

Figure 46: Large share of sub-standard assets will move to doubtful category

Source: Company data, Credit Suisse estimates

RBI conducted its AQR in 2H16, which resulted in banks recognising ~Rs2.8 tn of loans as NPLs. As a year has now passed, the loans would move into the next bucket, which would result in significant provisions only on account of ageing. We estimate that banks would need to provide ~Rs860 bn in FY18 and another Rs720 bn in FY19 only on account of ageing.

Figure 47: Ageing to keep credit costs in FY18 and FY19 at > 100bp for PSUs

Source: Company data, Credit Suisse estimates

Figure 48: Regulatory provisioning requirements on NPAs

Sub Standard Doubtful 1 Doubtful 2 Doubtful 3

Provisioning requirement 15% 25% 40% 100%

Ageing of NPA 0-1 year 1-2 years 2-4 years > 4 years

Source: RBI, Credit Suisse

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sub Standard Doutbful 1 Doubtful 2 Doubtful 3 Loss

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

FY18E FY19EAgeing Credit Cost (%)

Ageing to result in ~Rs860bn of provisions

for FY18E

16 February 2017

India Corporate Health Tracker 20

Bad Banks: Decisive measures needed to tackle

problem loans

The resolution process has slowed primarily due to reluctance by bank's management to

take decisions on large haircuts. Given the quantum of problem loans and complexity

involved in resolving these problem loans, the creation of bad banks can significantly

simplify the process with consolidation of loans and final decision making in the hands of

one entity. Only a bad bank/bailout can help meet the provisioning need for the banks.

Figure 49: Pros and Cons of bad banks

Pros for bad banks

Decision making – Usually decision making around an account stands still once an account is classified NPA

Multiplicity of lenders – Single point of decision making

Haircut need on the problem loans – One of the biggest contentious points currently with the lenders. Under a bad bank

structure, decisions on haircuts can be taken at the time of transfer or post transfer in a transparent way

Funding requirement – Bad banks can provide last-mile funding to projects stuck in the last phase

Sectoral complexities – Focused management with clear specific skills needed to resolve these problem loans

Clarity on progress – Structured approach towards resolution

Improved transparency to regain markets trust

Cons for bad banks

Capital infusion to the bad bank or the banking system – Depending on who takes the haircut, the government would need

to put in additional capital and will have to raise resources for it.

Funding requirement – Bad banks may need to raise debt at competitive rates to provide funding to stuck projects.

Skillset required – Bad banks need skilled professionals specialising in the stressed sectors for effective resolution.

Management acceptance – This would require management to accept that the magnitude of the problem is large.

Political challenges – Creation of bad banks may create a backlash.

Source: Company data, Credit Suisse estimates

Bankruptcy code: Long-term structural positive

The Insolvency and Bankruptcy code became functional from December 2016 with most of

the key regulations in place and a large number of Investment Professionals (IPs) having

already registered. The first large case filed with the board was Innoventive Industries by

ICICI Bank, which was challenged in the court as the company claimed to have protection

under state labour laws. The bank's lawyers expect a favorable judgment from the

Supreme Court and this would set the precedent for Bankruptcy law preceding all the state

laws. In the near term, most of the laws are likely to be challenged, however as more

precedents are set and law stabilizes over a period of time, it can act as a potent tool for

recovery and resolution of stressed loans.

Without a bad bank, capital needs for PSU

banks would be significantly higher

Bankruptcy code could help resolve some

of the stress

16 February 2017

India Corporate Health Tracker 21

Raising provision estimates, earnings cut Provisioning needs for the banks are likely to stay high on account of slippages from the

existing pool of recognized problem loans (SDR/Restructured/watchlist) and ageing

related provisions post one year of the RBI's AQR exercise. As a result, we increase our

credit cost estimates for coverage banks to ~1.5-1.9% with ageing-related provisions at

60-160bp and as a result, our EPS goes down by by 5-10% for corporate lenders. We also

factor potential gains from stake sales in subs (general insurance) for ICICI and SBI,

resulting in lower earnings cuts, while Axis sees larger FY18 cuts, as we increase NPL

slippage estimates on larger stress outside of watchlist.

Figure 50: Increasing credit cost estimates to 150-

190bp for FY18E on ageing-related provisions

Figure 51: Cutting EPS by 5-10% on an increase in

NPL provisions

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 52: Summary change in estimates and target price

EPS

Financials Rating Old TP New TP % upside

(downside) FY17E % change FY18E % change

Pvt Banks

Axis Bank N 527 490 0% 29 -10% 39 -8%

ICICI Bank O 316 316 13% 19 -6% 23 -6%

PSU Banks

SBI N 247 246 -8% 18 -8% 24 -3%

PNB U 94 93 -33% 14 -8% 19 -5%

Bank of Baroda N 162 148 -9% 15 0% 20 0%

Bank of India U 92 92 -26% 11 -8% 19 -5%

Union Bank U 124 123 -13% 20 0% 26 0%

Source: Company data, Credit Suisse estimates

Downgrading Axis to NEUTRAL

The slower-than-expected pace of recovery and resolution for the banking system has

meant that slippages from the Axis watchlist have been higher than initially expected.

Stress outside of the watchlist has stayed high as well and as the bank is expected to

recognise most of the problem loans from inside and outside of the watchlist by March

2018, we expect slippages to stay elevated (~3.2% of loans) in FY18. We increase our

credit cost estimate to 180bp for FY18 and cut EPS by 8-10% for FY18/19E. Our TP

moves down to Rs490 and at 1.8x FY18 book, given limited upside, we downgrade the

stock to a NEUTRAL.

2.6

3.3

2.8

2.6

2.2 2.2 2.1

1.9 1.8 1.8 1.7

1.6 1.5 1.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

PNB Axis ICICI BOI Union SBI BOB

Credit cost (%) FY17E FY18E

-8% -8% -8%

-6%

-10%

-3%

-5%-5%

-6%

-8%

-12%

-8%

-4%

0%

SBI PNB BOI ICICI Axis

Change in earnings (%) FY18E FY19E

16 February 2017

India Corporate Health Tracker 22

Figure 53: Price to adj book Figure 54: Price to earnings

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

3.0 3.02.8

2.2

1.71.6

1.3 1.3

1.0 1.1

0.7 0.7 0.6

0

1

2

3

4P / Adj BV FY18E FY19E 21

20

1617

16

13 1211

9 10

78

1716

1413 12

10 108 7

65 5

0

5

10

15

20

25

P / E (x)FY18E FY19E

16 February 2017

India Corporate Health Tracker 23

Asia Pacific/India Regional Banks

ICICI Bank (ICBK.BO / ICICIBC IN) Rating OUTPERFORM Price (14-Feb-17, Rs) 284.90 Target price (Rs) 316.00 Upside/downside (%) 10.9 Mkt cap (Rs/US$ mn) 1,658,514/ 24,824 Number of shares (mn) 5,821 Free float (%) 57.0 52-wk price range 292.55-183.35 ADTO-6M (US$ mn) 73.3 Target price is for 12 months.

Research Analysts

Ashish Gupta

91 22 6777 3895

Prashant Kumar

91 22 6777 3942

Kush Shah

91 22 6777 3862

Support from subsidiaries

■ Stress recognition to stay elevated. NPL slippages have stayed high as

the bank continue to recognize problem assets from the watchlist at an

accelerated pace. While slippages from and outside of watchlist are likely to

remain on the higher side in FY18 as well (~4.2% of loans), with resolution of

some of the large known stress accounts nearing completion, it should lead

to meaningful contraction in watchlist (residual exposure of ~4% of loans).

■ Operating performance stabilizing. Domestic loan growth picked-up in 3Q

with retail loan growth healthy (+18%) and corporate loan growth (ex-stress

segments) in mid-teens as well. NIMs stabilized even with elevated slippages

(~3.1%) and fee income picked-up on strong retail fee income growth

(+18%). With growth being driven by retail segment and steady margins

supported by strong CASA inflows, we expect pre-provisions profit growth to

return to double-digit growth in FY18 (14% yoy).

■ Gains from subs stake sale may help offset provisioning requirements.

The bank is exploring options to sell stake in subs and non-core assets,

which could partially offset our increase in provisioning estimate for FY18. We

increase our credit cost estimate on ageing related provisions, while also

factor gains from stake sale in non-life subs, resulting in net earnings cut of

~5-6% for FY18/19E. As the legacy stress is recognized (& provided) and

with loan mix shift to retail, the stock can trade at better multiples. At 1.2x

FY19 core book, maintain OUTPERFORM.

Share price performance

The price relative chart measures performance against the

S&P BSE SENSEX IDX which closed at 28,339.31 on

14/02/17. On 14/02/17 the spot exchange rate was

Rs66.81/US$1

Performance 1M 3M 12M Absolute (%) 4.3 4.8 42.6 Relative (%) 1.1 -2.5 21.2

Financial and valuation metrics

Year 3/16A 3/17E 3/18E 3/19E Pre-provision Op profit (Rs mn) 236,043.3 270,058.8 246,960.7 263,669.1 Pre-tax profit (Rs mn) 119,365.1 123,812.4 152,850.2 187,737.8 Net attributable profit (Rs mn) 94,670.8 102,764.3 110,052.1 131,416.5 EPS (CS adj.) (Rs) 16.28 17.67 18.92 22.60 Change from previous EPS (%) n.a. 1.5 (5.5) (5.7) Consensus EPS (Rs) n.a. 17.43 19.50 23.67 EPS growth (%) (15.2) 8.5 7.1 19.4 P/E (x) 17.5 16.1 15.1 12.6 Dividend yield (%) 1.9 2.1 2.5 2.6 BVPS (CS adj.) (Rs) 149.44 161.01 172.93 188.03 P/B (x) 1.91 1.77 1.65 1.52 ROE (%) 11.3 11.4 11.3 12.5 ROA (%) 1.4 1.4 1.3 1.4 Tier 1 Ratio (%) 13.1 13.3 12.4 11.6

Source: Company data, Thomson Reuters, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 24

Asia Pacific/India Regional Banks

Axis Bank Limited (AXBK.BO) Rating (from OUTPERFORM) NEUTRAL Price (14-Feb-17, Rs) 487.05 Target price (Rs) (from 527.00) 490.00 Upside/downside (%) 0.6 Mkt cap (Rs/US$ mn) 1,164,914/ 17,436 Number of shares (mn) 2,392 Free float (%) 62.7 52-wk price range 635.95-375.25 ADTO-6M (US$ mn) 81.4 Target price is for 12 months.

Research Analysts

Ashish Gupta

91 22 6777 3895

Prashant Kumar

91 22 6777 3942

Kush Shah

91 22 6777 3862

Corporate stress higher than expected

■ Stress recognition to stay high. Corporate stress has been higher than

initially expected resulting in elevated slippages from Axis watch list. Stress

outside of watch list has stayed high as well and as the bank recognize most

of the corporate stress from the watch list & outside of it by Mar-18, we

expect slippages to stay elevated (~3.2% of loans) in FY18. We increase our

credit cost estimate to 180bps for FY18 and cut EPS by 8-10% for FY18/19E.

■ Weak corporate segment to weigh on profitability. Retail loan growth

stayed healthy even during demonetization (~18% yoy) and is likely to remain

the key growth driver. Corporate segment outlook has weakened with both

loans and fees declining in 3Q17. As incremental focus remains on high rated

corporate (~80% of incremental disbursement to A rated and above), loan

growth and fee income may remain relatively muted given few opportunities.

With corporate growth likely staying muted and pressure on NIMs post the

recent sharp lending rate cuts, we expect FY18 pre-provision profitability

(PPoP ROA 2.4%) to moderate.

■ Limited upside at current valuations, downgrade to NEUTRAL. Capital

position of the bank is comfortable (Tier I ~13%) and pre-provisions

profitability is still healthy (~2.4% of assets), however corporate stress for the

bank is turning out to be higher than expected and as we factor higher

slippages and provisioning requirement, our EPS and adj BV goes down by

~10% and ~5% respectively for FY18 and TP moves to Rs490. Given limited

upside, downgrade to NEUTRAL.

Share price performance

The price relative chart measures performance against the

S&P BSE SENSEX IDX which closed at 28,339.31 on

14/02/17. On 14/02/17 the spot exchange rate was

Rs66.81/US$1

Performance 1M 3M 12M Absolute (%) 2.3 2.9 20.3 Relative (%) -0.9 -4.5 -1.1

Financial and valuation metrics

Year 3/16A 3/17E 3/18E 3/19E Pre-provision Op profit (Rs mn) 150,849.7 143,408.2 158,175.4 187,311.3 Pre-tax profit (Rs mn) 123,937.0 57,392.3 102,439.1 136,600.1 Net attributable profit (Rs mn) 82,236.6 38,452.8 69,658.6 92,888.1 EPS (CS adj.) (Rs) 34.51 16.09 29.16 38.88 Change from previous EPS (%) n.a. 0.4 (10.4) (7.6) Consensus EPS (Rs) n.a. 16.63 30.96 43.47 EPS growth (%) 11.0 (53.4) 81.2 33.3 P/E (x) 14.1 30.3 16.7 12.5 Dividend yield (%) 0.0 0.5 1.0 1.2 BVPS (CS adj.) (Rs) 222.52 235.61 259.27 291.15 P/B (x) 2.19 2.07 1.88 1.67 ROE (%) 16.8 7.0 11.8 14.1 ROA (%) 1.7 0.7 1.1 1.3 Tier 1 Ratio (%) 12.5 12.8 12.2 11.7

Source: Company data, Thomson Reuters, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 25

Asia Pacific/India Regional Banks

State Bank Of India (SBI.BO / SBIN IN) Rating NEUTRAL Price (14-Feb-17, Rs) 270.50 Target price (Rs) 247.00 Upside/downside (%) -8.7 Mkt cap (Rs/US$ mn) 2,156,833/ 32,283 Number of shares (mn) 7,974 Free float (%) 40.6 52-wk price range 281.60-151.90 ADTO-6M (US$ mn) 68.6 Target price is for 12 months.

Research Analysts

Ashish Gupta

91 22 6777 3895

Prashant Kumar

91 22 6777 3942

Kush Shah

91 22 6777 3862

Core profitability outlook remains muted

■ Muted growth, NIM pressure to weigh on pre-provisions profitability.

Loan growth for the bank is likely to remain muted (6% for FY17 & ~11% in

FY18), as corporate loan growth remains weak even as retail growth picks up

(~18%). CASA inflows were strong during 3Q (CASA ratio at ~46.6%),

however given sharp lending rate cuts (MCLR cut of 90bps in jan'17), NIM is

likely to moderate 10-15bps in FY18. Strong treasury gains have been

supporting overall profitability, however as the bank step up pension

provisioning post actuarial valuations in 4Q, pre-prov profitability could come

under further pressure (~1.5% in FY18).

■ Provisioning requirement to stay high. NPL slippages were high (~3.0%)

in 3Q17 even as the bank deferred recognition for small ticket accounts

(~Rs20 bn) under RBI dispensation. Addition to SDR and S4A account were

high (~Rs70 bn during the quarter) and total SDR+S4A now at at ~1.1% of

loans. Consolidated NPLs for the bank stabilized after a period of sharp rise

at ~8.6%. Given continued pressure on corporate segment and total stressed

watchlist (Restrd+SDR/S4A+watchist) at ~4% of loans, NPL slippages are

unlikely to moderate quickly. Further the bank would need to step up ageing

related provisions and we expect total credit cost to remain high at ~150bps.

■ Recovery in profitability to be gradual. Merger related disruptions with

associate banks may take few quarters to stabilize and may impact FY18

profitability. With pre-prov profitability (PPoP ROA at just ~1.5%) under

pressure, even after building in a moderation in credit cost, ROAs remain at

55 bp & ROEs at ~9% (though more equity dilution likely in FY18). We

increase our credit cost estimate (to ~1.5%) as we factor higher ageing

related provisions. We also factor potential gains from stake sale in general

insurance sub resulting in net EPS cut of 3-6% for FY18/19. At 1.3x FY18 adj

book, maintain NEUTRAL.

Share price performance

The price relative chart measures performance against the

S&P BSE SENSEX IDX which closed at 28,339.31 on

14/02/17. On 14/02/17 the spot exchange rate was

Rs66.81/US$1

Performance 1M 3M 12M Absolute (%) 5.0 -3.2 71.8 Relative (%) 1.9 -10.6 50.4

Financial and valuation metrics

Year 3/16A 3/17E 3/18E 3/19E Pre-provision Op profit (Rs mn) 377,648.6 371,308.0 383,439.0 458,314.3 Pre-tax profit (Rs mn) 139,257.3 149,893.4 217,437.6 284,166.2 Net attributable profit (Rs mn) 101,023.3 106,424.3 147,857.6 191,812.2 EPS (CS adj.) (Rs) 13.27 13.71 18.71 23.86 Change from previous EPS (%) n.a. 0.0 (6.4) (3.2) Consensus EPS (Rs) n.a. 14.58 20.17 26.40 EPS growth (%) (24.4) 3.3 36.5 27.5 P/E (x) 20.4 19.7 14.5 11.3 Dividend yield (%) 1.0 1.2 1.7 1.9 BVPS (CS adj.) (Rs) 185.85 195.94 211.78 229.79 P/B (x) 1.46 1.38 1.28 1.18 ROE (%) 7.4 7.2 9.2 10.8 ROA (%) 0.5 0.4 0.6 0.7 Tier 1 Ratio (%) 9.9 10.6 11.0 10.5

Source: Company data, Thomson Reuters, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 26

Asia Pacific/India Regional Banks

Punjab National Bank Ltd (PNBK.BO) Rating UNDERPERFORM [V] Price (14-Feb-17, Rs) 144.10 Target price (Rs) 94.00 Upside/downside (%) -34.8 Mkt cap (Rs/US$ mn) 306,640/ 4,590 Number of shares (mn) 2,128 Free float (%) 37.2 52-wk price range 159.35-71.30 ADTO-6M (US$ mn) 26.6 Target price is for 12 months.

[V] = Stock Considered Volatile (see Disclosure Appendix)

Research Analysts

Ashish Gupta

91 22 6777 3895

Prashant Kumar

91 22 6777 3942

Kush Shah

91 22 6777 3862

Under-provisioning remains large

■ Operating performance remains weak. Operating performance has

remained weak in 3Q, as top line growth was muted, with loan book

contracting (-ve 2% yoy) and NII declining 9% yoy. PPoP to assets continues

to fall, at 1.5% in 3Q vs 1.7% yoy. NPL slippages remained elevated, with net

slippage at 1.85% in 3Q vs 1.55%, even as the management used RBI

dispensation to defer recognition of Rs12-15bn of retail small ticket loans.

With total stress watchlist (restructured +SDR/S4A+ SMA2) staying high at

~9% of loans, NPL slippages would stay elevated.

■ Under-provisioning remains high. Despite 8% dilution earlier this year,

CET-1 remains weak at 8.5% and problem asset cover is weak at < 30% on

its stressed book and pre-provision profit has weakened (PPoP RoA 1.6%).

Even assuming credit costs revert to FY09-11 levels of 75 bp, RoAs would

remain muted, at 0.8% and ROEs. Increase our credit cost estimate and cut

EPS by 5-8% for FY18/19. Maintain UNDERPERFORM.

Share price performance

The price relative chart measures performance against the

S&P BSE SENSEX IDX which closed at 28,339.31 on

14/02/17. On 14/02/17 the spot exchange rate was

Rs66.81/US$1

Performance 1M 3M 12M Absolute (%) 8.9 -5.3 92.8 Relative (%) 5.7 -12.7 71.4

Financial and valuation metrics

Year 3/16A 3/17E 3/18E 3/19E Pre-provision Op profit (Rs mn) 122,163.5 137,286.6 124,097.4 125,454.0 Pre-tax profit (Rs mn) (57,378.8) 26,945.1 42,413.2 57,109.8 Net attributable profit (Rs mn) (39,743.9) 18,592.1 29,265.1 39,405.7 EPS (CS adj.) (Rs) (20.24) 8.83 13.91 18.73 Change from previous EPS (%) n.a. (2.0) (8.0) (4.5) Consensus EPS (Rs) n.a. 8.10 13.89 18.28 EPS growth (%) 57.4 34.7 P/E (x) (7.1) 16.3 10.4 7.7 Dividend yield (%) 0.0 1.3 1.6 2.0 BVPS (CS adj.) (Rs) 180.61 185.29 196.63 212.19 P/B (x) 0.80 0.78 0.73 0.68 ROE (%) (10.9) 5.0 7.3 9.2 ROA (%) (0.6) 0.3 0.4 0.5 Tier 1 Ratio (%) 8.4 8.6 9.0 8.9

Source: Company data, Thomson Reuters, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 27

Asia Pacific/India Regional Banks

Bank of India (BOI.BO / BOI IN) Rating UNDERPERFORM Price (14-Feb-17, Rs) 128.75 Target price (Rs) 92.00 Upside/downside (%) -28.5 Mkt cap (Rs/US$ mn) 135,792/ 2,033 Number of shares (mn) 1,055 Free float (%) 25.0 52-wk price range 136.75-80.35 ADTO-6M (US$ mn) 8.3 Target price is for 12 months.

Research Analysts

Ashish Gupta

91 22 6777 3895

Prashant Kumar

91 22 6777 3942

Kush Shah

91 22 6777 3862

Capital position remains weak despite infusion

■ Weak core performance. The bank's core profitability remains one of the

weakest among banks (PPoP ROA Of ~95bps) given low margins (~2.2%)

and high opex ratio (~58%). Loan book continue to contract (-5% yoy) as the

bank goes through a period of consolidation and recovery in growth is likely

to be gradual. Given weak core profitability and high level of under-

provisioning, the bank would need significant external capital support for

profitability to recover.

■ Asset quality remains a concern. Even post the capital infusion of ~Rs26.4

bn since March 2016, the bank's CET-1 declined to ~7.7% despite negative

loan growth as the bank continues to report losses. Even with the

improvement in 3Q, PPoP ROA remained at 95 bp and is one of the lowest

among PSU banks. Further, given large under-provisioning (~180% of NW)

and low CET-1 (~7.7%), frequent dilutions are likely. Maintain Underperform.

Cut FY18/19 EPS further by 5-8% as increase credit cost estimate.

Share price performance

The price relative chart measures performance against the

S&P BSE SENSEX IDX which closed at 28,339.31 on

14/02/17. On 14/02/17 the spot exchange rate was

Rs66.81/US$1

Performance 1M 3M 12M Absolute (%) 6.9 3.1 44.2 Relative (%) 3.7 -4.3 22.8

Financial and valuation metrics

Year 3/16A 3/17E 3/18E 3/19E Pre-provision Op profit (Rs mn) 54,067.5 56,367.7 68,095.8 79,917.7 Pre-tax profit (Rs mn) (76,526.6) (8,481.6) 14,864.9 25,125.5 Net attributable profit (Rs mn) (59,511.0) (6,021.9) 10,702.7 17,964.8 EPS (CS adj.) (Rs) (80.26) (6.87) 11.45 19.22 Change from previous EPS (%) n.a. - (8.2) (5.2) Consensus EPS (Rs) n.a. (3.93) 10.33 16.63 EPS growth (%) 67.9 P/E (x) (1.6) (18.7) 11.2 6.7 Dividend yield (%) 0.0 0.0 2.0 2.7 BVPS (CS adj.) (Rs) 321.92 288.97 297.42 312.64 P/B (x) 0.40 0.45 0.43 0.41 ROE (%) (22.0) (2.3) 3.9 6.3 ROA (%) (1.0) (0.1) 0.2 0.3 Tier 1 Ratio (%) 9.4 9.3 8.8 8.3

Source: Company data, Thomson Reuters, Credit Suisse estimates

16 February 2017

India Corporate Health Tracker 28

Companies Mentioned (Price as of 15-Feb-2017) 3i Infotech (TIIN.NS, Rs5.25) ABG Shipyard (ABGS.BO, Rs26.85) ARSS (ARSS.BO, Rs62.8) Adani Enterprises Ltd. (ADEL.BO, Rs92.3) Adani Ports & SEZ (APSE.BO, Rs300.5) Adani Power Ltd (ADAN.BO, Rs34.7) Adhunik Metaliks (ADME.BO, Rs7.34) Allahabad Bank (ALBK.BO, Rs70.35) Alok Indus (ALOK.BO, Rs3.32) Amtek Auto (AMTK.BO, Rs34.45) Andhra Bank (ADBK.BO, Rs53.55) ArcelorMitta (ISPA.AS, €8.75) Arshiya (ARSH.BO, Rs47.65) Axis Bank Limited (AXBK.BO, Rs487.95, OUTPERFORM, TP Rs527.0) BGR Energy (BGRE.BO, Rs137.75) Bajaj Finance Ltd (BJFN.BO, Rs1040.05) Bajaj Hindusthan Limited (BJHN.BO, Rs14.44) Ballarpur Indu (BILT.BO, Rs16.0) Bank of Baroda (BOB.BO, Rs163.2) Bank of India (BOI.BO, Rs123.55, UNDERPERFORM, TP Rs92.0) Bharat Financial Inclusion Ltd. (BHAF.BO, Rs819.65) Bharati Defence (BHAR.BO, Rs15.35) Bhushan Steel (BSSL.NS, Rs52.45) Bhushan Steel (BSSL.BO, Rs52.85) Bk Maharashtra (BMBK.BO, Rs32.65) Bombay Rayon (BRFL.BO, Rs155.6) C & C Constr (CCCL.BO, Rs21.65) Cairn India Ltd (CAIL.BO, Rs274.55) Canara Bank (CNBK.BO, Rs292.5) Central Bank IN (CBI.BO, Rs85.75) Century Textiles (CNTY.BO, Rs890.0) Chennai Petro (CHPC.BO, Rs357.8) Cholamandalam Finance (CHLA.BO, Rs991.75) Corporation Bank (CRBK.BO, Rs46.65) Cox & Kings (COKI.BO, Rs192.6) Dena Bank (DENA.BO, Rs37.25) Diamond Power (DIAC.BO, Rs39.55) EID Parry (EIDP.BO, Rs282.15) Educomp Solutions Ltd (EDSO.BO, Rs11.03) Electrosteel (ELST.BO, Rs27.7) Electrosteel Stl (ELES.NS, Rs4.6) Electrotherm (ELTH.BO, Rs186.0) Entegra (ENTI.NS, Rs2.8) Era Infra (ERCI.BO, Rs1.43) Essar Shipping (ESPL.BO, Rs26.65) GAIL (India) Ltd (GAIL.BO, Rs494.3) GIPL (GAIN.BO, Rs3.65) GIPL (GAIN.NS, Rs3.65) GMR Infrastructure Ltd (GMRI.BO, Rs13.76) GOL Offshore (GOFS.BO, Rs21.25) GTL (GTL.BO, Rs16.3) GTL Infrastructr (GTLI.BO, Rs4.1) GVK Power & Infrastructure (GVKP.BO, Rs6.87) Gammon India Ltd (GAMM.BO, Rs12.19) Gerdau (GGBR4.SA, R$13.36) Gitanjali Gems (GTGM.BO, Rs66.3) Gujarat NRE Coke (GJNC.BO, Rs2.83) HDFC Bank (HDBK.BO, Rs1322.45) HTTL (HATT.BO, Rs4.92) Hindustan Constr (HCNS.BO, Rs38.75) Hindustan Zinc Limited (HZNC.BO, Rs293.15) Hotel Leela (HTLE.BO, Rs16.55) Housing Development Finance Corp (HDFC.BO, Rs1398.2) ICICI Bank (ICBK.BO, Rs280.65, OUTPERFORM, TP Rs316.0) IDBI Bank (IDBI.BO, Rs81.0) IDFC Bank (IDFB.BO, Rs61.65) IDFC Ltd (IDFC.BO, Rs52.45) ITNL (ILFT.BO, Rs102.45) IVRCL Ltd (IVRC.BO, Rs5.34) Idea Cellular Ltd (IDEA.BO, Rs107.15) Indiabulls Housing Finance Ltd (INBF.BO, Rs813.4) Indiabulls Real Estate Limited (INRL.BO, Rs75.4) Indian Bank (INBA.BO, Rs279.1) Indian Hotel (IHTL.BO, Rs118.8) Indian Overseas Bank (IOBK.BO, Rs25.6) IndusInd Bank (INBK.BO, Rs1315.55) JBF Industries (JBFI.BO, Rs240.0) JSW Energy (JSWE.BO, Rs60.0) JSW Steel Ltd (JSTL.BO, Rs183.55) Jai Balaji (JAIB.BO, Rs13.5) Jain Irrigation (JAIR.BO, Rs94.6) Jaiprakash Associates Ltd. (JAIA.BO, Rs12.08) Jaiprakash Power Ventures Ltd (JAPR.BO, Rs5.0) Jammu and Kashmir Bank (JKBK.BO, Rs68.45) Jayaswal Neco (JAYN.BO, Rs8.39) Jaypee Infra (JYPE.BO, Rs8.82)

16 February 2017

India Corporate Health Tracker 29