india infoline - iifl securities pte....

TRANSCRIPT

Company Registration No. 200816119H

IIFL Securities Pte. Ltd.

Annual Financial Statements31 March 2016

building a betterworking world

IIFL Securities Pte. Ltd.

General information

Directors

Prabodh Kumar AgrawalAmit Nitin ShahChopra Arun Vijay

Company Secretary

Lim Ka BeeLynn Wan Tiew Leng

Registered Office

6 Shenton Way#18-08B, OUE Downtown 2Singapore 068809

Auditor

Ernst &Young LLP

Index

(Appointed on 9 April 2015)

(Resigned on 3 August 2015)(Appointed on 3 August 2015)

Directors' statement

Page

1

Independent auditor's report 4

Statement of comprehensive income 6

Balance sheet 7

Statement of changes in equity 8

Cash flow statement 9

Notes to the financial statements 10

IIFL Securities Pte. Ltd.

Directors' statement

The directors are pleased to present their statement to the member together with the auditedfinancial statements of IIFL Securities Pte. Ltd. (the "Company") for the financial year ended31 March 2016.

Opinion of the directors

In the opinion of the directors,

(a) the accompanying statement of comprehensive income, balance sheet, statement ofchanges in equity and cash flow statement together with notes thereto are drawn up so asto give a true and fair view of the financial position of the Company as at 31 March 2016and the financial performance, changes in equity and cash flows of the Company for thefinancial year ended on that date; and

(b) at the date of this statement, there are reasonable grounds to believe that the Company willbe able to pay its debts as and when they fall due.

Directors

The directors of the Company in office at the date of this statement are:

Prabodh Kumar AgrawalAmit Nitin ShahChopra Arun Vijay

Arrangements to enable directors to acquire shares or debentures

Neither at the end of nor at any time during the financial year was the Company a party to anyarrangement whose objects are, or one of whose object is, to enable the directors of the Companyto acquire benefits by means of the acquisition of shares or debentures of the Company or anyother body corporate.

-1-

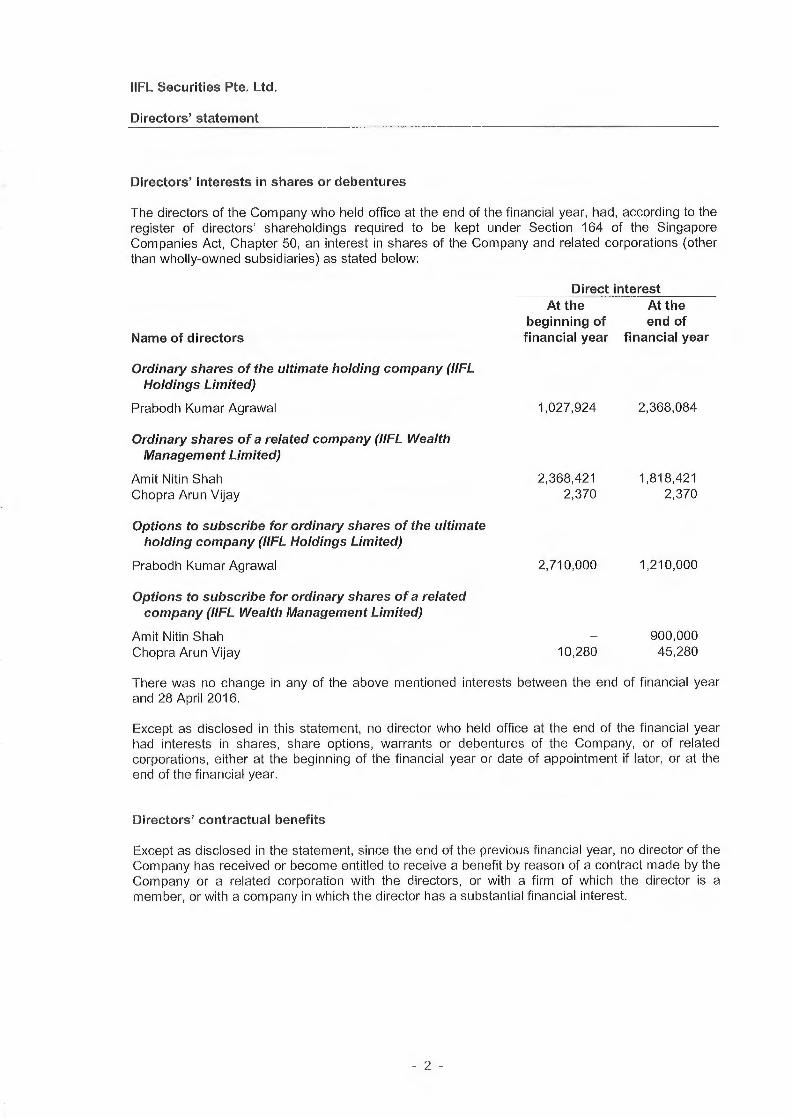

IIFL Securities Pte. Ltd.

Directors' statement

Directors' interests in shares or debentures

The directors of the Company who held office at the end of the financial year, had, according to theregister of directors' shareholdings required to be kept under Section 164 of the SingaporeCompanies Act, Chapter 50, an interest in shares of the Company and related corporations (otherthan wholly-owned subsidiaries) as stated below:

Direct interestAt the At the

beginning of end ofName of directors financial year financial year

Ordinary shares of the ultimate holding company (IIFLHoldings Limited)

Prabodh Kumar Agrawal 1,027,924 2,368,084

Ordinary shares of a related company (IIFL WealthManagement Limited)

Amit Nitin Shah 2,368,421 1,818,421Chopra Arun Vijay 2,370 2,370

Options to subscribe for ordinary shares of the ultimateholding company (IIFL Holdings Limited)

Prabodh KumarAgrawal 2,710,000 1,210,000

Options to subscribe for ordinary shares of a relatedcompany (IIFL Wealth Management Limited)

Amit Nitin Shah — 900,000Chopra Arun Vijay 10,280 45,280

There was no change in any of the above mentioned interests between the end of financial yearand 28 April 2016.

Except as disclosed in this statement, no director who held office at the end of the financial yearhad interests in shares, share options, warrants or debentures of the Company, or of relatedcorporations, either at the beginning of the financial year or date of appointment if later, or at theend of the financial year.

Directors' contractual benefits

Except as disclosed in the statement, since the end of the previous financial year, no director of theCompany has received or become entitled to receive a benefit by reason of a contract made by theCompany or a related corporation with the directors, or with a firm of which the director is amember, or with a company in which the director has a substantial financial interest.

- 2 -

IIFL Securities Pte. Ltd.

Directors' statement

Share options

During the financial year, there was:

(a) no option granted by the Company to any person to take up unissued shares of theCompany; and

(b) no share issued by virtue of the exercise of options to take up unissued shares of theCompany.

At the end of the financial year, there was no unissued share of the Company under option.

Auditor

Ernst &Young LLP have expressed their willingness to accept reappointment as auditor.

On behalf of the Board of Directors:

J~. ~.5~,~A~Fnit Nitin ShahDirector

~~1'

1~ .

Chopra Arun VijayDirector

Singapore28 April 2016

-3-

IIFL Securities Pte. Ltd.

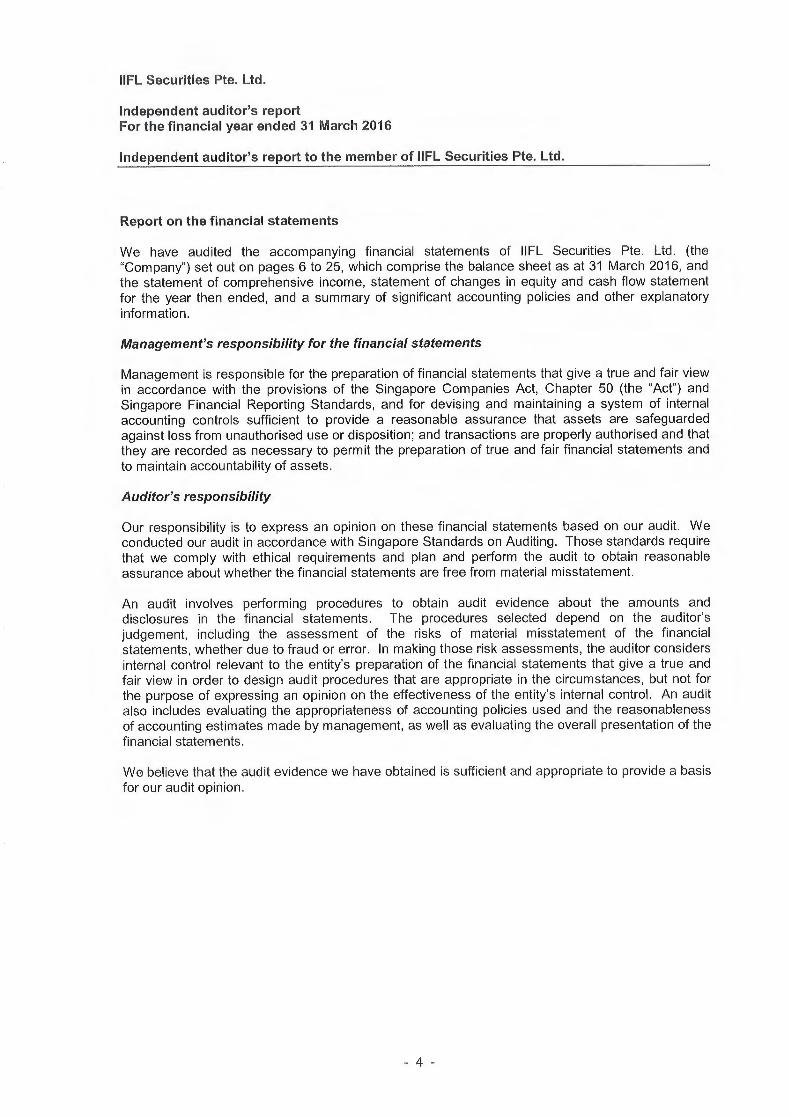

Independent auditor's reportFor the financial year ended 31 March 2016

Independent auditor's report to the member of IIFL Securities Pte. Ltd.

Report on the financial statements

We have audited the accompanying financial statements of IIFL Securities Pte. Ltd. (the"Company") set out on pages 6 to 25, which comprise the balance sheet as at 31 March 2016, andthe statement of comprehensive income, statement of changes in equity and cash flow statementfor the year then ended, and a summary of significant accounting policies and other explanatoryinformation.

Management's responsibility for the financial statements

Management is responsible for the preparation of financial statements that give a true and fair viewin accordance with the provisions of the Singapore Companies Act, Chapter 50 (the "AcY') andSingapore Financial Reporting Standards, and for devising and maintaining a system of internalaccounting controls sufficient to provide a reasonable assurance that assets are safeguardedagainst loss from unauthorised use or disposition; and transactions are properly authorised and thatthey are recorded as necessary to permit the preparation of true and fair financial statements andto maintain accountability of assets.

Auditor's responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with Singapore Standards on Auditing. Those standards requirethat we comply with ethical requirements and plan and perform the audit to obtain reasonableassurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor'sjudgement, including the assessment of the risks of material misstatement of the financialstatements, whether due to fraud or error. In making those risk assessments, the auditor considersinternal control relevant to the entity's preparation of the financial statements that give a true andfair view in order to design audit procedures that are appropriate in the circumstances, but not forthe purpose of expressing an opinion on the effectiveness of the entity's internal control. An auditalso includes evaluating the appropriateness of accounting policies used and the reasonablenessof accounting estimates made by management, as well as evaluating the overall presentation of thefinancial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basisfor our audit opinion.

-4-

IIFL Securities Pte. Ltd.

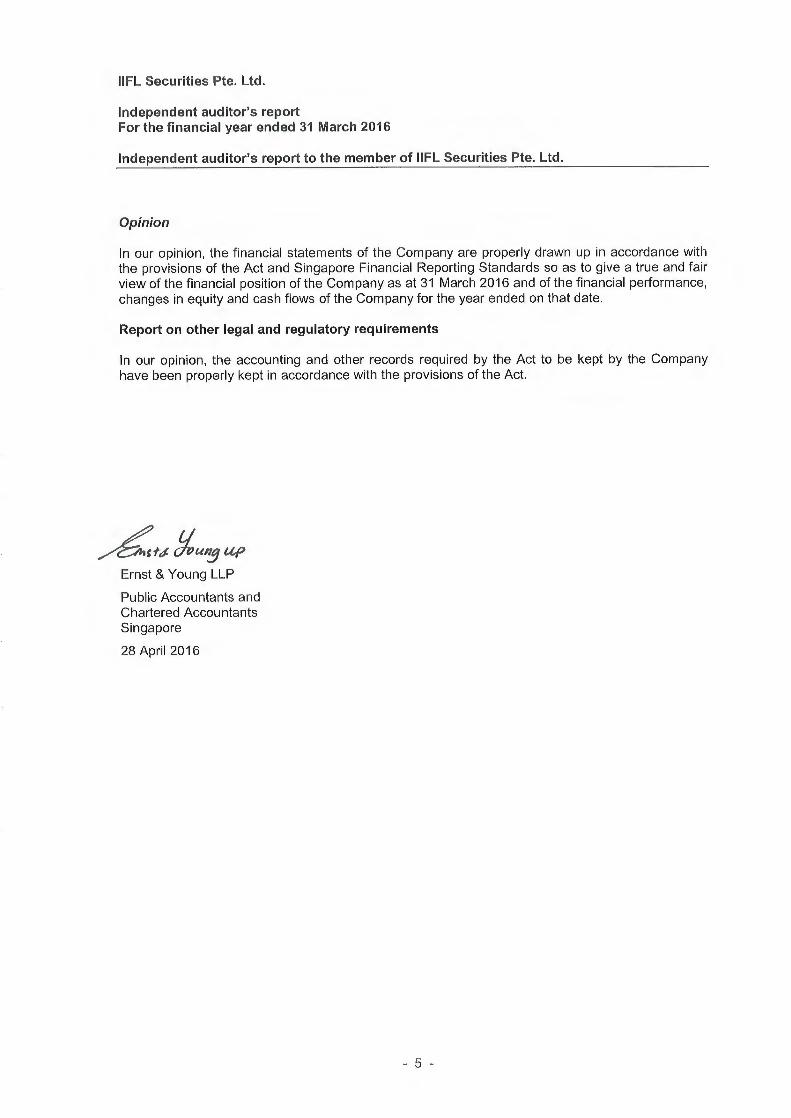

Independent auditor's reportFor the financial year ended 31 March 2016

Independent auditor's report to the member of IIFL Securities Pte. Ltd.

Opinion

In our opinion, the financial statements of the Company are properly drawn up in accordance withthe provisions of the Act and Singapore Financial Reporting Standards so as to give a true and fairview of the financial position of the Company as at 31 March 2016 and of the financial performance,changes in equity and cash flows of the Company for the year ended on that date.

Report on other legal and regulatory requirements

In our opinion, the accounting and other records required by the Act to be kept by the Companyhave been properly kept in accordance with the provisions of the Act.

.~ ~=.i'~sfi~ Uvun~ ~Ernst &Young LLP

Public Accountants andChartered AccountantsSingapore

28 April 2016

-5-

IIFL Securities Pte. Ltd.

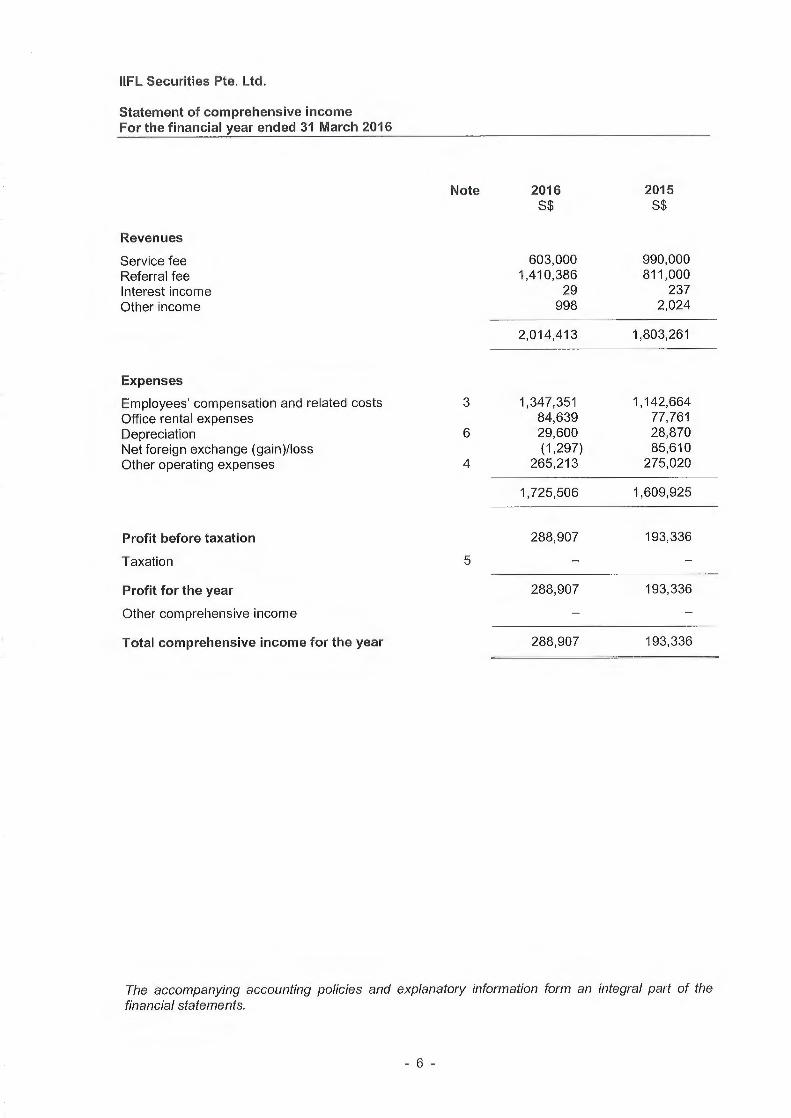

Statement of comprehensive incomeFor the financial year ended 31 March 2016

Revenues

Service feeReferral feeInterest incomeOther income

Expenses

Employees' compensation and related costsOffice rental expensesDepreciationNet foreign exchange (gain)/lossOther operating expenses

Profit before taxation

Taxation

Profit for the year

Other comprehensive income

Total comprehensive income for the year

Note 2016 2015S$ S$

603,000 990,0001,410,386 811,000

29 237998 2, 024

2,014,413 1,803,261

3 1,347,351 1,142,66484,639 77,761

6 29,600 28,870(1,297) 85,610

4 265,213 275,020

1,725,506 1,609,925

288,907 193,336

5 — —

288,907 193,336

288,907 193,336

The accompanying accounting policies and explanatory information form an integral part of thefinancial statements.

Z:~

IIFL Securities Pte. Ltd.

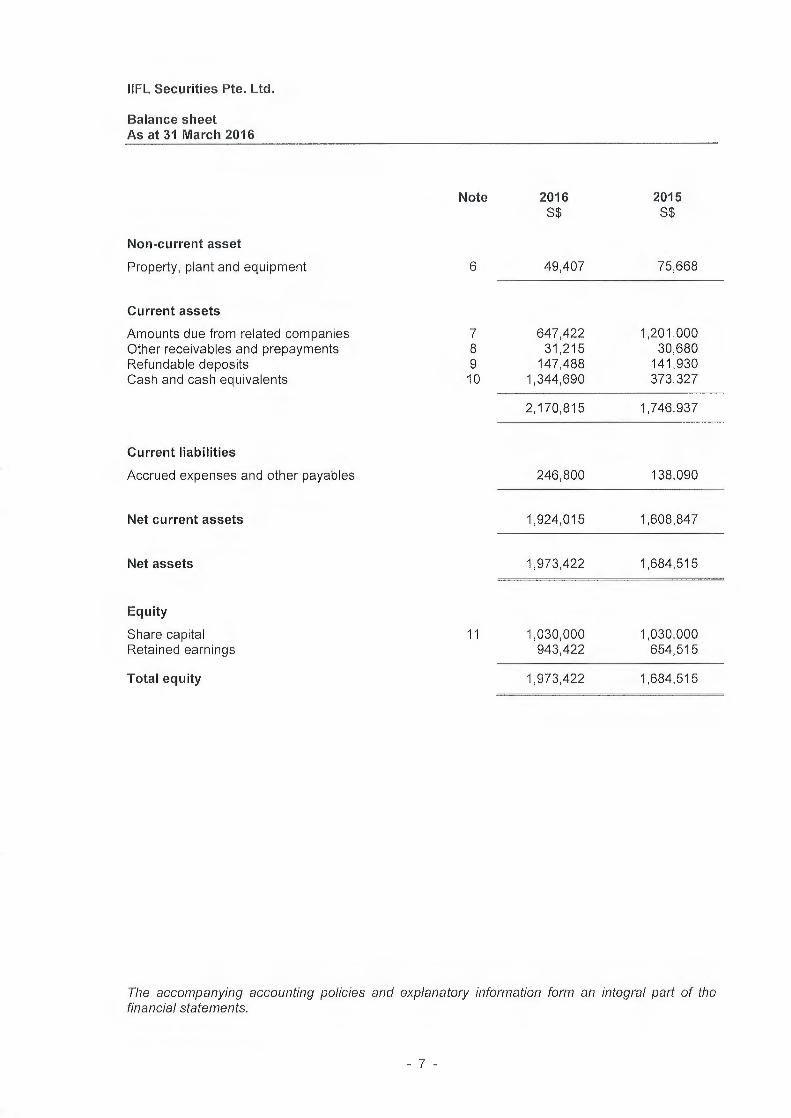

Balance sheetAs at 31 March 2016

Non-current asset

Property, plant and equipment

Current assets

Amounts due from related companiesOther receivables and prepaymentsRefundable depositsCash and cash equivalents

Current liabilities

Accrued expenses and other payables

Net current assets

Net assets

Equity

Share capitalRetained earnings

Total equity

Note 2016 2015S$ S$

6 49,407 75,668

7 647,422 1,201,0008 31,215 30,6809 147,488 141,93010 1,344,690 373,327

11

2,170,815 1,746,937

246,800 138,090

1,924,015 1,608,847

1,973,422 1,684,515

1,030,000 1,030,000943,422 654,515

1,973,422 1,684,515

The accompanying accounting policies and explanatory information form an integral part of thefinancial statements.

-7-

IIFL Securities Pte. Ltd.

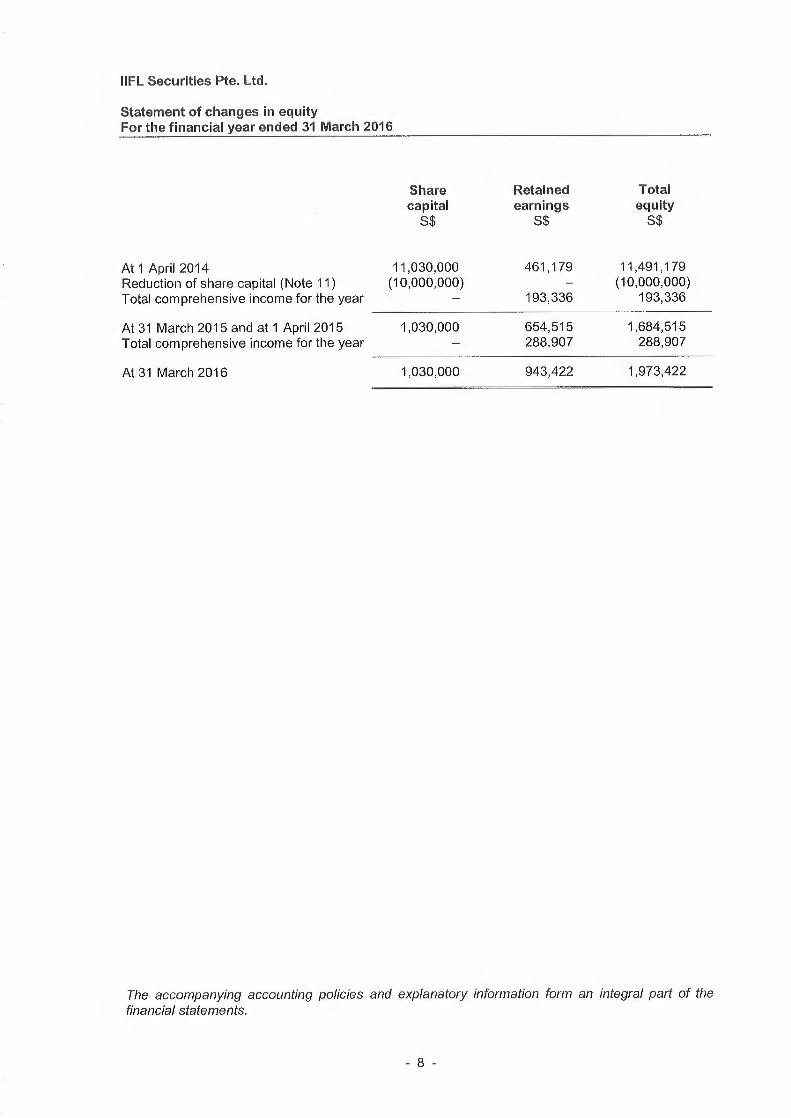

Statement of changes in equityFor the financial year ended 31 March 2016

Share Retained Totalcapital earnings equityS$ S$ S$

At 1 April 2014 11,030,000 461,179 11,491,179Reduction of share capital (Note 11) (10,000,000) — (10,000,000)Total comprehensive income for the year — 193,336 193,336

At 31 March 2015 and at 1 April 2015 1,030,000 654,515 1,684,515Total comprehensive income for the year — 288,907 288,907

At 31 March 2016 1,030,000 943,422 1,973,422

The accompanying accounting policies and explanatory information form an integral part of thefinancial statements.

'~

IIFL Securities Pte. Ltd.

Cash flow statementFor the financial year ended 31 March 2016

2016 2015S$ S$

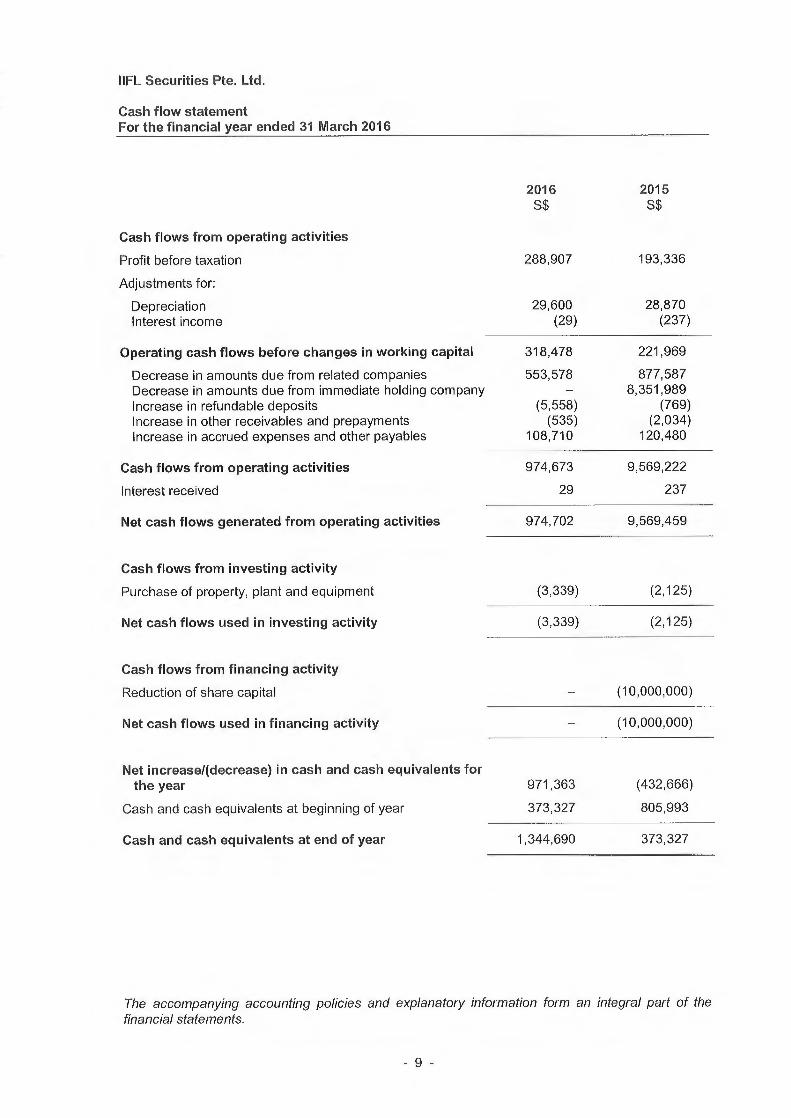

Cash flows from operating activities

Profit before taxation 288,907 193,336

Adjustments for:

Depreciation 29,600 28,870Interest income (29) (237)

Operating cash flows before changes in working capital 318,478 221,969

Decrease in amounts due from related companies 553,578 877,587Decrease in amounts due from immediate holding company — 8,351,989Increase in refundable deposits (5,558) (769)Increase in other receivables and prepayments (535) (2,034)Increase in accrued expenses and other payables 108,710 120,480

Cash flows from operating activities 974,673 9,569,222

Interest received 29 237

Net cash flows generated from operating activities 974,702 9,569,459

Cash flows from investing activity

Purchase of property, plant and equipment (3,339) (2,125)

Net cash flows used in investing activity (3,339) (2,125)

Cash flows from financing activity

Reduction of share capital — (10,000,000)

Net cash flows used in financing activity — (10,000,000)

Net increase/(decrease) in cash and cash equivalents forthe year 971,363 (432,666)

Cash and cash equivalents at beginning of year 373,327 805,993

Cash and cash equivalents at end of year 1,344,690 373,327

The accompanying accounting policies and explanatory information form an integral part of thefinancial statements.

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

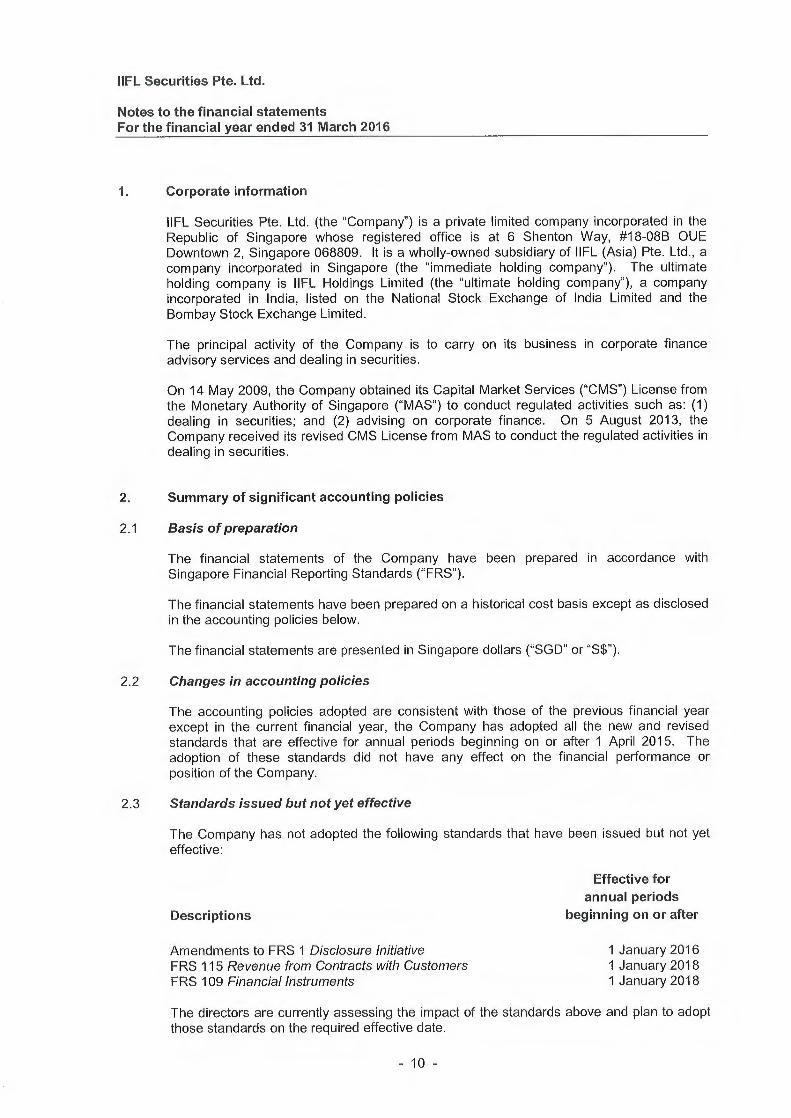

1. Corporate information

IIFL Securities Pte. Ltd. (the "Company") is a private limited company incorporated in theRepublic of Singapore whose registered office is at 6 Shenton Way, #18-08B OUEDowntown 2, Singapore 068809. It is a wholly-owned subsidiary of IIFL (Asia) Pte. Ltd., acompany incorporated in Singapore (the "immediate holding company"). The ultimateholding company is IIFL Holdings Limited (the "ultimate holding company"), a companyincorporated in India, listed on the National Stock Exchange of India Limited and theBombay Stock Exchange Limited.

The principal activity of the Company is to carry on its business in corporate financeadvisory services and dealing in securities.

On 14 May 2009, the Company obtained its Capital Market Services ("CMS") License fromthe Monetary Authority of Singapore ("MAS") to conduct regulated activities such as: (1)dealing in securities; and (2) advising on corporate finance. On 5 August 2013, theCompany received its revised CMS License from MAS to conduct the regulated activities indealing in securities.

Summary of significant accounting policies

2.1 Basis of preparation

The financial statements of the Company have been prepared in accordance withSingapore Financial Reporting Standards ("FRS").

The financial statements have been prepared on a historical cost basis except as disclosedin the accounting policies below.

The financial statements are presented in Singapore dollars ("SGD" or "S$").

2.2 Changes in accounting policies

The accounting policies adopted are consistent with those of the previous financial yearexcept in the current financial year, the Company has adopted all the new and revisedstandards that are effective for annual periods beginning on or after 1 April 2015. Theadoption of these standards did not have any effect on the financial performance orposition of the Company.

2.3 Standards issued but not yet effective

The Company has not adopted the following standards that have been issued but not yeteffective:

Effective forannual periods

Descriptions beginning on or after

Amendments to FRS 1 Disclosure Initiative 1 January 2016FRS 115 Revenue from Contracts with Customers 1 January 2018FRS 109 Financial Instruments 1 January 2018

The directors are currently assessing the impact of the standards above and plan to adoptthose standards on the required effective date.

- 10 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (cont'd)

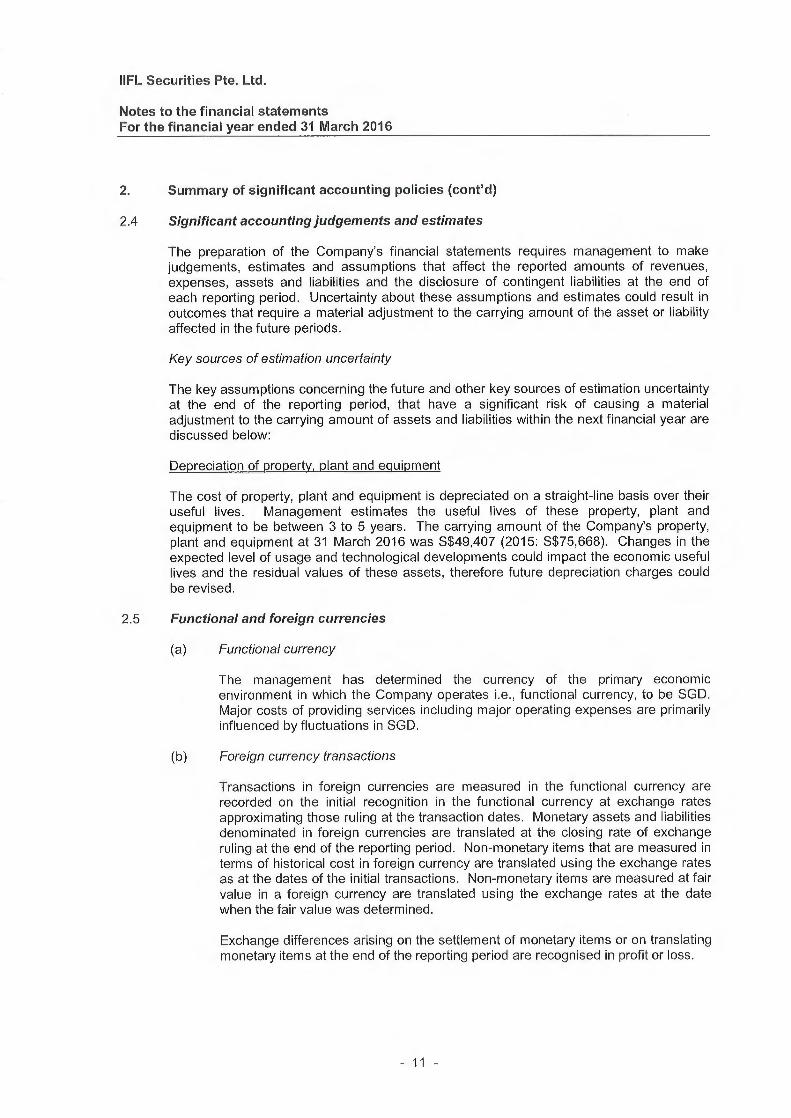

2.4 Significant accounting judgements and estimates

The preparation of the Company's financial statements requires management to makejudgements, estimates and assumptions that affect the reported amounts of revenues,expenses, assets and liabilities and the disclosure of contingent liabilities at the end ofeach reporting period. Uncertainty about these assumptions and estimates could result inoutcomes that require a material adjustment to the carrying amount of the asset or liabilityaffected in the future periods.

Key sources of estimation uncertainty

The key assumptions concerning the future and other key sources of estimation uncertaintyat the end of the reporting period, that have a significant risk of causing a materialadjustment to the carrying amount of assets and liabilities within the next financial year arediscussed below:

Depreciation of proaerty. plant and equipment

The cost of property, plant and equipment is depreciated on a straight-line basis over theiruseful lives. Management estimates the useful lives of these property, plant andequipment to be between 3 to 5 years. The carrying amount of the Company's property,plant and equipment at 31 March 2016 was S$49,407 (2015: S$75,668). Changes in theexpected level of usage and technological developments could impact the economic usefullives and the residual values of these assets, therefore future depreciation charges couldbe revised.

2.5 Functional and foreign currencies

(a) Functional currency

The management has determined the currency of the primary economicenvironment in which the Company operates i.e., functional currency, to be SGD.Major costs of providing services including major operating expenses are primarilyinfluenced by fluctuations in SGD.

(b) Foreign currency transactions

Transactions in foreign currencies are measured in the functional currency arerecorded on the initial recognition in the functional currency at exchange ratesapproximating those ruling at the transaction dates. Monetary assets and liabilitiesdenominated in foreign currencies are translated at the closing rate of exchangeruling at the end of the reporting period. Non-monetary items that are measured interms of historical cost in foreign currency are translated using the exchange ratesas at the dates of the initial transactions. Non-monetary items are measured at fairvalue in a foreign currency are translated using the exchange rates at the datewhen the fair value was determined.

Exchange differences arising on the settlement of monetary items or on translatingmonetary items at the end of the reporting period are recognised in profit or loss.

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (cont'd)

2.6 Property, plant and equipment

All items of property, plant and equipment are initially recorded at cost. The cost of an itemof property, plant and equipment is recognised as an asset if, and only if, it is probable thatfuture economic benefits associated with the item will flow to the Company and the cost ofthe item can be measured reliably. Subsequent to recognition, property, plant andequipment are measured at cost less accumulated depreciation and accumulatedimpairment losses.

Depreciation is calculated on a straight-line basis over the estimated useful lives of theassets as follows:

Computers - 3 yearsFurniture and fittings - 5 yearsOffice equipment - 5 years

The carrying values of property, plant and equipment are reviewed for impairment whenevents or changes in circumstances indicate that the carrying values may not berecoverable.

The residual value, useful life and depreciation method are reviewed at each financial yearend, and adjusted prospectively, if appropriate.

An item of property, plant and equipment is derecognised upon disposal or when no futureeconomic benefits are expected from its use or disposal. Any gains or losses onderecognition of the asset is included in profit or loss in the financial year the asset isderecognised.

2.7 Impairment ofnon-financial assets

The Company assesses at the end of each reporting period whether there is an indicationthat an asset may be impaired. If any such indication exists, or when annual impairmentassessment for an asset is required, the Company makes an estimate of the assetsrecoverable amount.

An asset's recoverable amount is the higher of an assets or cash-generating units fairvalue less costs to sell and its value in use and is determined for an individual asset, unlessthe asset does not generate cash inflows that are largely independent of those from otherassets. In assessing value in use, the estimated future cash flows expected to begenerated by the asset are discounted to their present values. Where the carrying amountof an asset exceeds its recoverable amount, the asset is written-down to its recoverableamount.

An assessment is made at the end of each reporting period as to whether there is anyindication that previously recognised impairment losses may no longer exist or may havedecreased. A previously recognised impairment loss is reversed only if there has been achange in the estimates used to determine the assets recoverable amount since the lastimpairment loss was recognised. If that is the case, the carrying amount of the asset isincreased to its recoverable amount. That increase cannot exceed the carrying amountthat would have been determined, net of depreciation, had no impairment loss berecognised previously. Such reversal is recognised in profit or loss unless the asset ismeasured at revalued amount, in which case the reversal is treated as revaluationincrease.

- 12 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (cont'd)

2.8 Financial assets

Financial assets are recognised when, and only when, the Company becomes a party tothe contractual provisions of the financial instruments. When financial assets arerecognised initially, they are measured at fair value, plus, in the case of financial assets notat fair value through profit or loss, directly attributable transaction costs.

A financial asset is derecognised where the contractual right to receive cash flows from theasset has expired. On derecognition of a financial asset in its entirety, the differencesbetween the carrying amount and the sum of the consideration received and anycumulative gains or losses that have been recognised in other comprehensive income isrecognised in profit or loss.

All regular way purchases and sales of financial assets are recognised or derecognised onthe trade date i.e., the date that the Company commits to purchase or sell the asset.Regular way purchases or sales are purchases or sales of financial assets that requiredelivery of assets within the period generally established by regulation or convention in themarketplace concerned.

Loans and receivables

Non-derivative financial assets with fixed or determinable payments that are not quoted inan active market are classified as loans and receivables. Subsequent to initial recognition,loans and receivables are measured at amortised cost using the effective interest method.Gains or losses are recognised in profit or loss when the loans and receivables arederecognised or impaired and through the amortisation process. The Company classifiescash and cash equivalents, amounts due from ultimate holding company, amounts duefrom related companies, refundable deposits and other receivables as loans andreceivables.

2.9 Impairment of financial assets

The Company assesses at the end of each reporting period whether there is any objectiveevidence that a financial asset is impaired:

Financial assets carried at amortised cost

If there is objective evidence that an impairment loss on financial assets carried atamortised cost has been incurred, the amount of the loss is measured as the differencesbetween the assets carrying amount and the present value of estimated future cash flowsdiscounted at the financial asset's original effective interest rate. The carrying amount ofthe asset is reduced through the use of an allowance account. The impairment loss isrecognised in profit or loss.

When the asset becomes uncollectible, the carrying amount of impaired financial assets isreduced directly or if an amount was charged to the allowance account, the amountscharged to the allowance account are written-off against the carrying values of the financialassets.

To determine whether there is objective evidence that an impairment loss on financialassets had been incurred, the Company considers factors such as the probability ofinsolvency or significant financial difficulties of the debtor and default or significant delay inpayments.

If in a subsequent period, the amount of the impairment loss decreases and the decreasecan be related objectively to an event occurring after the impairment was recognised, thepreviously recognised impairment loss is reversed to the extent that the carrying amount ofthe asset does not exceed its amortised cost at the reversal date. The amount of reversalis recognised in profit or loss.

- 13 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (conYd)

2.10 Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and cash at bank.

2.11 Provisions

Provisions are recognised when the Company has a present obligation as a result of a pastevent, it is probable that an outflow of economic resources will be required to settle theobligation and the amount of the obligation can be estimated reliably.

Provisions are reviewed at the end of each reporting period and adjusted to reflect thecurrent best estimate. If it is no longer probable that an outflow of economic resources willbe required to settle the obligation, the provisions are reversed. If the effect of the timevalue of money is material, provisions are discounted using a current pre tax rate thatreflects, where appropriate, the risks specific to the liability. When discounting is used, theincreases in the provisions due to the passage of time are recognised as a finance cost.

2.12 Financial liabilities

Financial liabilities include accrued expenses. Financial liabilities are recognised when,and only when, the Company becomes a party to the contractual provisions of the financialinstruments. The Company determines the classification of its financial liabilities at initialrecognition. All financial liabilities are recognised initially at fair value, and in the case ofother financial liabilities, plus directly attributable transaction costs.

Subsequent to initial recognition, all financial liabilities are measured at amortised costusing the effective interest method. For financial liabilities, gains or losses are recognisedin profit or loss when the liabilities are derecognised and through the amortisation process.The liabilities are derecognised when the obligation under the liability is discharged orcancelled or expired.

2.13 Employee benefits

As required by law, the Company makes contributions to the Central Provident Fund("CPF") scheme in Singapore, a defined contribution pension scheme. Contributions tonational pension schemes are recognised as an expense in the financial period in whichthe related service is performed.

2.14 Operating leases

Leases where the lessor effectively retains substantially all the risks and benefits ofownership of the leased item are classified as operating leases. Operating lease paymentsare recognised as an expense in profit or loss on a straight-line basis over the lease term.

- 14 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (cont'd)

2.15 Taxes

(a) Current income tax

Current income tax assets and liabilities for the current and prior periods aremeasured at the amount expected to be recovered from or paid to the taxationauthorities. The tax rates and tax laws used to compute the amount are those thatare enacted or substantively enacted by the end of the reporting period, in thecountry where the Company operates and generates taxable income.

Current income taxes are recognised in profit or loss except to the extent that thetax relates to items recognised outside profit or loss, either in other comprehensiveincome directly in equity.

(b) Deferred tax

Deferred tax is provided using the liability method on temporary differences at theend of the reporting period between the tax bases of assets and liabilities and theircarrying amounts for financial reporting purposes.

Deferred tax assets and liabilities are recognised for all temporary differences,except:

Where the deferred tax arises from the initial recognition of an asset orliability in a transaction that is not a business combination and, at the timeof the transaction affects neither the accounting profit nor taxable profit orloss; and

In respect of deductible temporary differences and carry-forward of unusedtax credits and unused tax losses, if it is not probable that taxable profit willbe available against which the deductible temporary differences and carry-forward of unused tax credits and unused tax losses can be utilised.

The carrying amount of deferred tax asset is reviewed at the end of each reportingperiod and reduced to the extent that it is no longer probable that sufficient taxableprofit will be available to allow all or part of the deferred tax asset to be utilised.Unrecognised deferred tax assets are reassessed at the end of each reportingperiod and are recognised to the extent that it has become probable that futuretaxable profit will allow the deferred tax asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expectedto apply to the financial year when the asset is realised or the liability is settled,based on tax rates and tax laws that have been enacted or substantively enactedat the end of the reporting period.

- 15 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (cont'd)

2.15 Taxes (cont'd)

(c) Goods and services tax ("GST')

Revenues, expenses and assets are recognised net of the amount of GST except:

(i) Where the GST incurred on a purchase of assets or services is notrecoverable from the taxation authority, in which case the GST isrecognised as part of the cost of acquisition of the asset or as part of theexpense item as applicable; and

(ii) Receivables and payables that are stated with the amount of GSTincluded.

The net amount of GST recoverable from, or payable to, the taxation authority isincluded as part of receivables or payables in the balance sheet.

2.16 Share capital and share issue expenses

Proceeds from issuance of ordinary shares are recognised as share capital in equity.Incremental costs directly attributable to the issuance of ordinary shares are deductedagainst share capital.

2.17 Revenue recognition

Revenue is recognised to the extent that it is probable that the economic benefits will flowto the Company and the revenue can be reliably measured. Revenue is measured at thefair value of consideration received or receivable.

Referral fee is recognised on an accrual basis based on rates determined between theCompany and its related parties when service is rendered.

Service income is recognised on an accrual basis between the Company and a relatedparty when service is rendered.

Interest income is recognised using the effective interest method.

- 16 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

2. Summary of significant accounting policies (cont'd)

2.18 Related parties

A related party is defined as follows:

(a) A person or a close member of that person's family is related to the Company ifthat person:

(i) Has control or joint control over the Company;(ii) Has significant influence over the Company; or(iii) Is a member of the key management personnel of the Company or of a

parent of the Company.

(b) An entity is related to the Company if any of the following conditions applies:

(i) The entity and the Company are members of the same group (whichmeans that each parent, subsidiary and fellow subsidiary is related to theothers);

(ii) One entity is an associate or joint venture of the other entity (or anassociate or joint venture of a member of a group of which the other entityis a member);

(iii) Both entities are joint ventures of the same third party;(iv) One entity is a joint venture of a third entity and the other entity is an

associate of the third entity;(v) The entity is apost-employment benefit plan for the benefit of employees

of either the Company or an entity related to the Company. If theCompany is itself such a plan, the sponsoring employers are also relatedto the Company;

(vi) The entity is controlled or jointly controlled by a person identified in (a); or(vii) A person identified in (a)(i) has significant influence over the entity or is a

member of the key management personnel of the entity (or of a parent ofthe entity).

3. Employees' compensation and related costs

2016 2015S$ S$

Salaries and bonuses 1,296,927 1,096,743CPF contributions 32,738 27,890Other short-term benefits 17,686 18,031

1,347,351 1,142,664

- 17 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

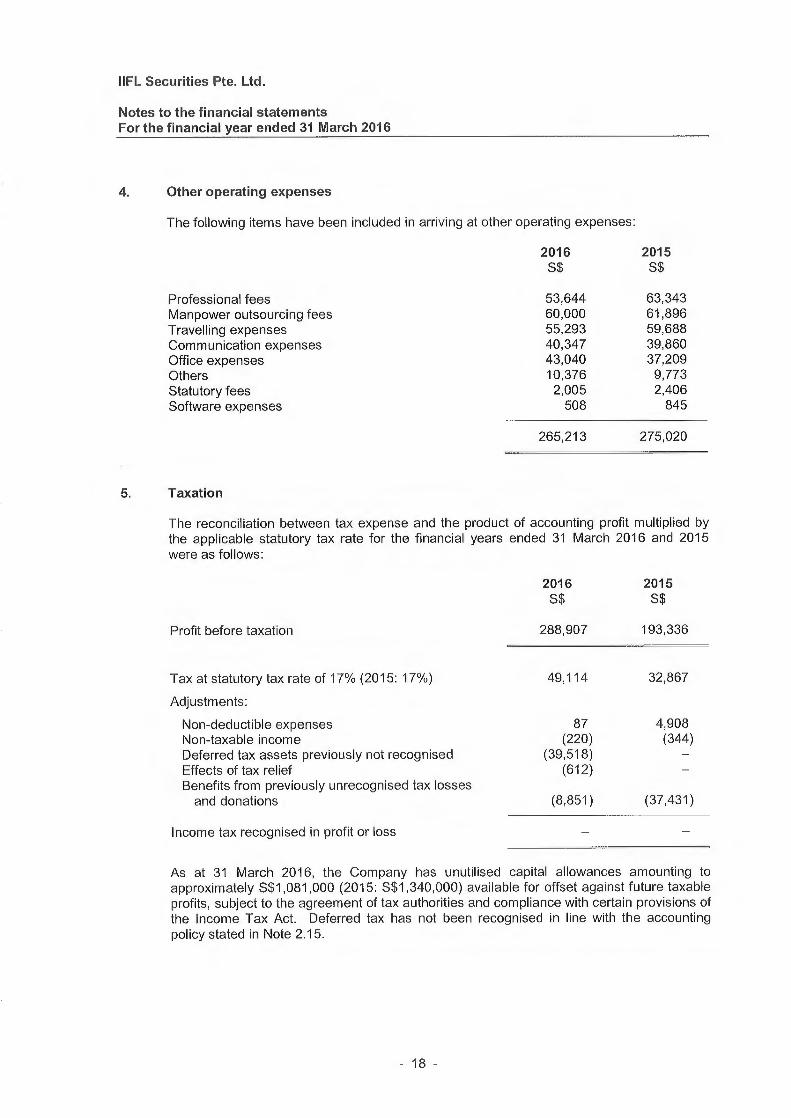

4. Other operating expenses

The following items have been included in arriving at other operating expenses:

2016 2015S$ S$

Professional fees 53,644 63,343Manpower outsourcing fees 60,000 61,896Travelling expenses 55,293 59,688Communication expenses 40,347 39,860Office expenses 43,040 37,209Others 10,376 9,773Statutory fees 2,005 2,406Software expenses 508 845

265,213 275,020

5. Taxation

The reconciliation between tax expense and the product of accounting profit multiplied bythe applicable statutory tax rate for the financial years ended 31 March 2016 and 2015were as follows:

Profit before taxation

Tax at statutory tax rate of 17% (2015: 17%)

Adjustments:

Non-deductible expensesNon-taxable incomeDeferred tax assets previously not recognisedEffects of tax reliefBenefits from previously unrecognised tax lossesand donations

2016 2015S$ S$

288,907 193,336

49,114 32,867

87 4,908(220) (344)

(39,518) —(612) —

(8,851) (37,431)

Income tax recognised in profit or loss — —

As at 31 March 2016, the Company has unutilised capital allowances amounting toapproximately S$1,081,000 (2015: S$1,340,000) available for offset against future taxableprofits, subject to the agreement of tax authorities and compliance with certain provisions ofthe Income Tax Act. Deferred tax has not been recognised in line with the accountingpolicy stated in Note 2.15.

- 18 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

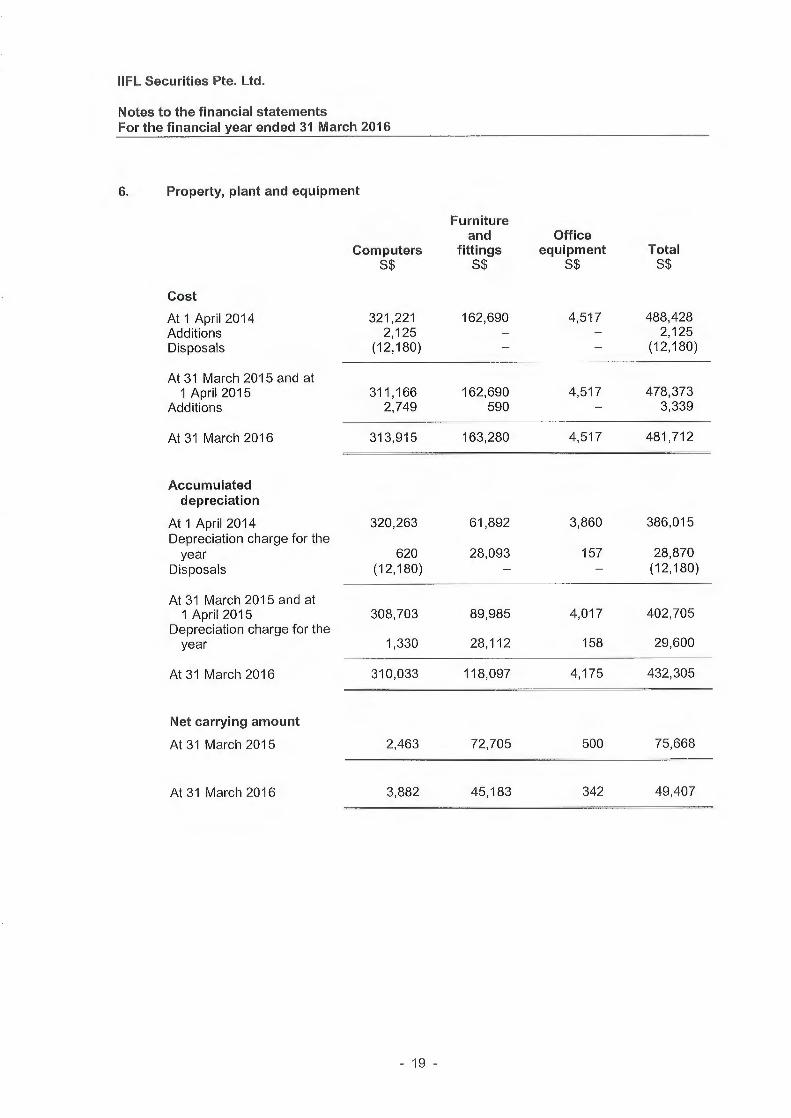

6. Property, plant and equipment

Furnitureand Office

Computers fittings equipment TotalS$ S$ S$ S$

Cost

At 1 April 2014 321,221 162,690 4,517 488,428Additions 2,125 - - 2,125Disposals (12,180) - - (12,180)

At 31 March 2015 and at1 April 2015 311,166 162,690 4,517 478,373

Additions 2,749 590 - 3,339

At 31 March 2016 313,915 163,280 4,517 481,712

Accumulateddepreciation

At 1 April 2014 320,263 61,892 3,860 386,015Depreciation charge for theyear 620 28,093 157 28,870

Disposals (12,180) - - (12,180)

At 31 March 2015 and at1 April 2015 308,703 89,985 4,017 402,705

Depreciation charge for theyear 1,330 28,112 158 29,600

At 31 March 2016 310,033 118,097 4,175 432,305

Net carrying amount

At 31 March 2015 2,463 72,705 500 75,668

At 31 March 2016 3,882 45,183 342 49,407

- 19 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

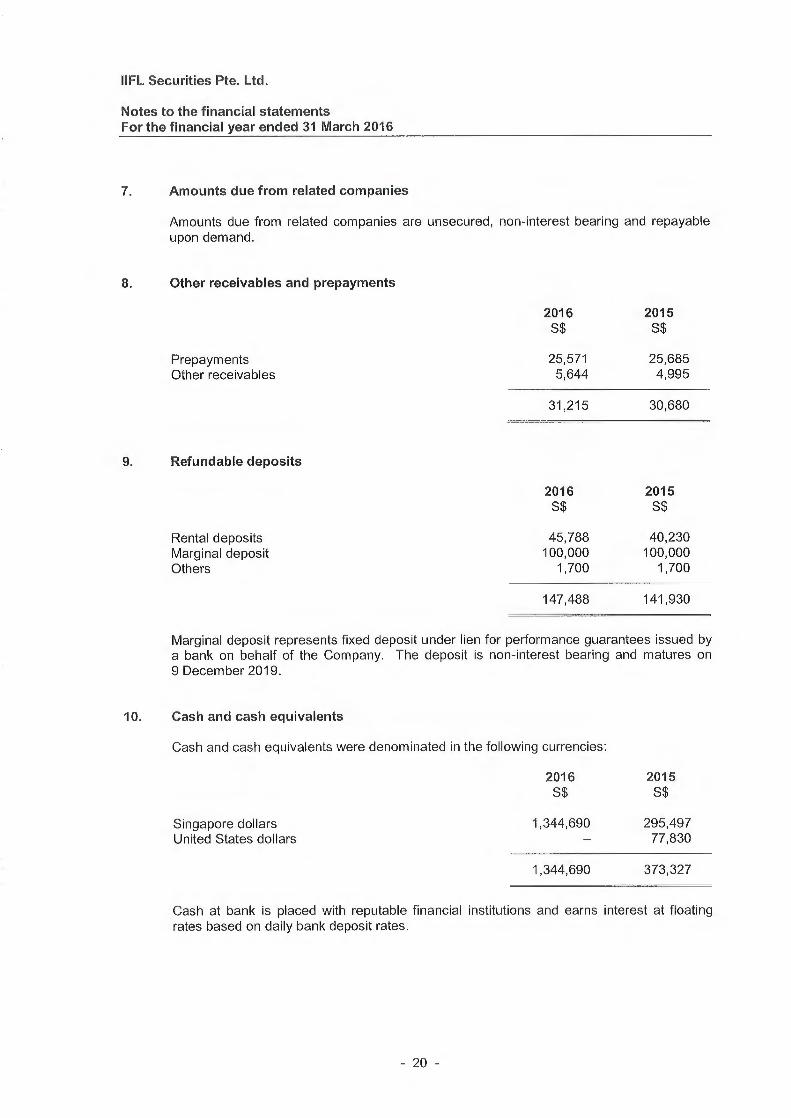

7. Amounts due from related companies

Amounts due from related companies are unsecured, non-interest bearing and repayableupon demand.

8. Other receivables and prepayments

2016 2015S$ S$

Prepayments 25,571 25,685Other receivables 5,644 4,995

31,215 30,680

9. Refundable deposits

2016 2015S$ S$

Rental deposits 45,788 40,230Marginal deposit 100,000 100,000Others 1,700 1,700

147,488 141,930

Marginal deposit represents fixed deposit under lien for performance guarantees issued bya bank on behalf of the Company. The deposit is non-interest bearing and matures on9 December 2019.

10. Cash and cash equivalents

Cash and cash equivalents were denominated in the following currencies:

2016 2015S$ S$

Singapore dollars 1,344,690 295,497United States dollars — 77,830

1,344,690 373,327

Cash at bank is placed with reputable financial institutions and earns interest at floatingrates based on daily bank deposit rates.

-20-

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

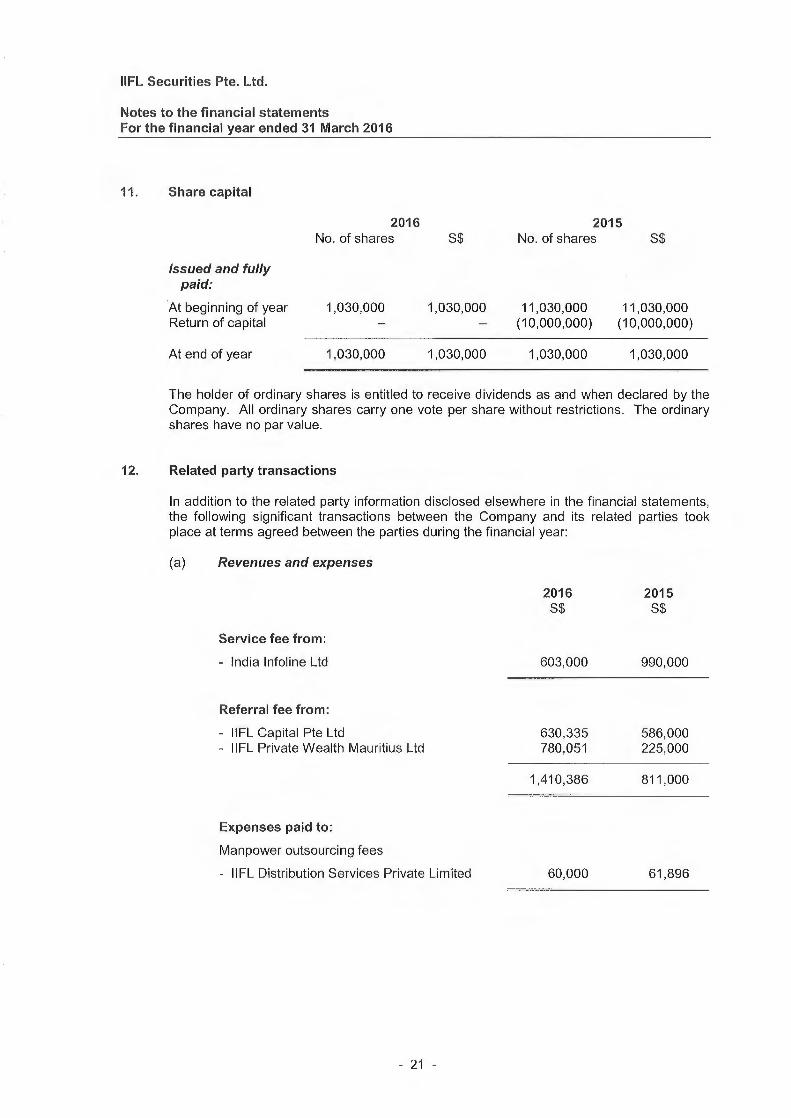

11. Share capital

2016 2015No. of shares S$ No. of shares S$

Issued and fullypaid:

At beginning of year 1,030,000 1,030,000 11,030,000 11,030,000Return of capital — — (10,000,000) (10,000,000)

At end of year 1,030,000 1,030,000 1,030,000 1,030,000

The holder of ordinary shares is entitled to receive dividends as and when declared by theCompany. All ordinary shares carry one vote per share without restrictions. The ordinaryshares have no par value.

12. Related party transactions

In addition to the related party information disclosed elsewhere in the financial statements,the following significant transactions between the Company and its related parties tookplace at terms agreed between the parties during the financial year:

(a) Revenues and expenses

2016 2015S$ S$

Service fee from:

- India Infoline Ltd 603,000 990,000

Referral fee from:

- IIFL Capital Pte Ltd 630,335 586,000-

IIFL Private Wealth Mauritius Ltd 780,051 225,000

1,410,386 811,000

Expenses paid to:

Manpower outsourcing fees

- IIFL Distribution Services Private Limited 60,000 61,896

- 21 -

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

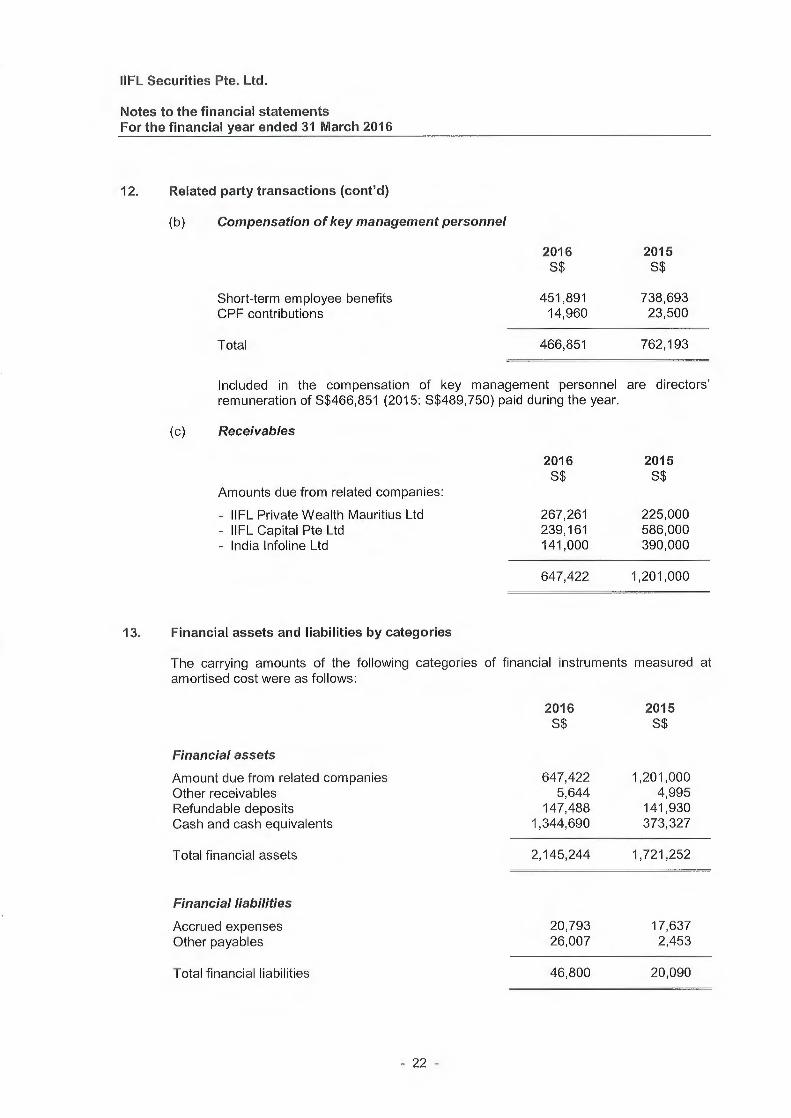

12. Related party transactions (cont'd)

(b) Compensation of key management personnel

2016 2015S$ S$

Short-term employee benefits 451,891 738,693CPF contributions 14,960 23,500

Total 466, 851 762,193

Included in the compensation of key management personnel are directors'remuneration of S$466,851 (2015: S$489,750)paid during the year.

(c) Receivables

2016 2015S$ S$

Amounts due from related companies:

- IIFL Private Wealth Mauritius Ltd 267,261 225,000- IIFL Capital Pte Ltd 239,161 586,000- India Infoline Ltd 141,000 390,000

647,422 1,201,000

13. Financial assets and liabilities by categories

The carrying amounts of the following categories of financial instruments measured atamortised cost were as follows:

Financial assets

Amount due from related companiesOther receivablesRefundable depositsCash and cash equivalents

Total financial assets

Financial liabilities

Accrued expensesOther payables

Total financial liabilities

-22-

2016 2015S$ S$

647,422 1,201,0005,644 4,995

147,488 141,9301,344,690 373,327

2,145,244 1,721,252

20,793 17,63726,007 2,453

46,800 20,090

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

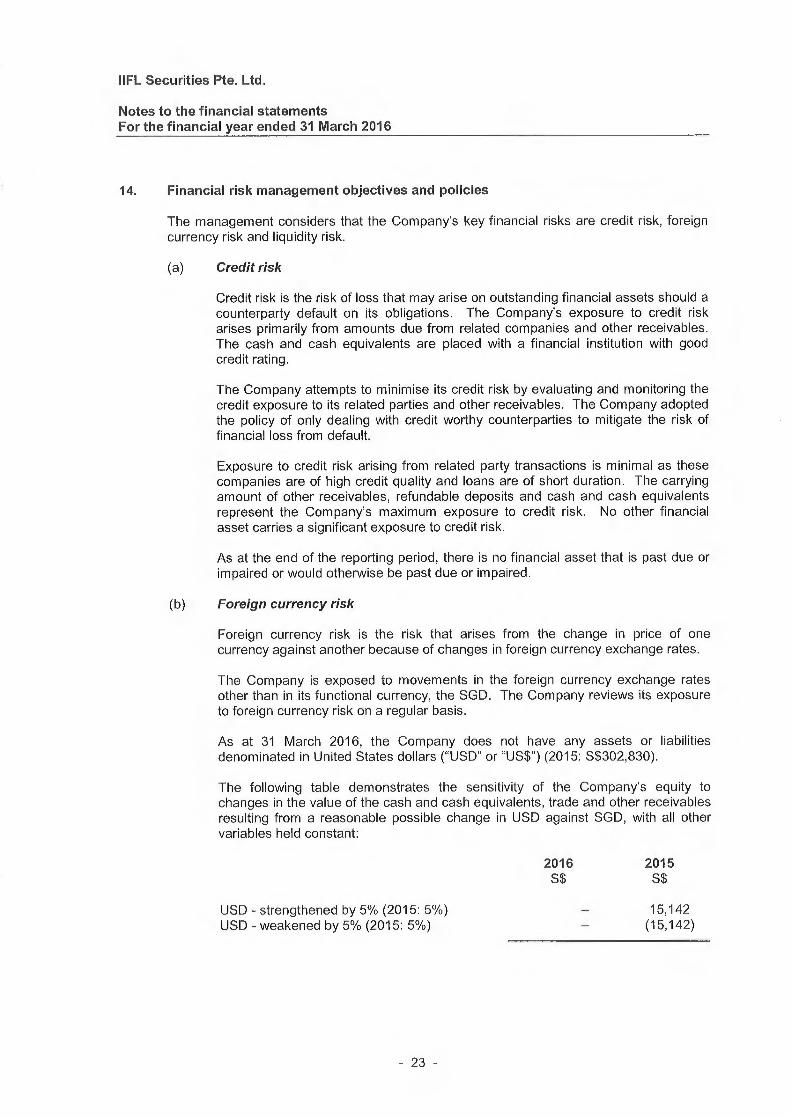

14. Financial risk management objectives and policies

The management considers that the Company's key financial risks are credit risk, foreigncurrency risk and liquidity risk.

(a) Credit risk

Credit risk is the risk of loss that may arise on outstanding financial assets should acounterparty default on its obligations. The Company's exposure to credit riskarises primarily from amounts due from related companies and other receivables.The cash and cash equivalents are placed with a financial institution with goodcredit rating.

The Company attempts to minimise its credit risk by evaluating and monitoring thecredit exposure to its related parties and other receivables. The Company adoptedthe policy of only dealing with credit worthy counterparties to mitigate the risk offinancial loss from default.

Exposure to credit risk arising from related party transactions is minimal as thesecompanies are of high credit quality and loans are of short duration. The carryingamount of other receivables, refundable deposits and cash and cash equivalentsrepresent the Company's maximum exposure to credit risk. No other financialasset carries a significant exposure to credit risk.

As at the end of the reporting period, there is no financial asset that is past due orimpaired or would otherwise be past due or impaired.

(b) Foreign currency risk

Foreign currency risk is the risk that arises from the change in price of onecurrency against another because of changes in foreign currency exchange rates.

The Company is exposed to movements in the foreign currency exchange ratesother than in its functional currency, the SGD. The Company reviews its exposureto foreign currency risk on a regular basis.

As at 31 March 2016, the Company does not have any assets or liabilitiesdenominated in United States dollars ("USD" or "US$") (2015: S$302,830).

The following table demonstrates the sensitivity of the Company's equity tochanges in the value of the cash and cash equivalents, trade and other receivablesresulting from a reasonable possible change in USD against SGD, with all othervariables held constant:

USD - strengthened by 5% (2015: 5%)USD - weakened by 5% (2015: 5%)

-23-

2016 2015S$ S$

— 15,142— (15,142)

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

14. Financial risk management objectives and policies (cont'd)

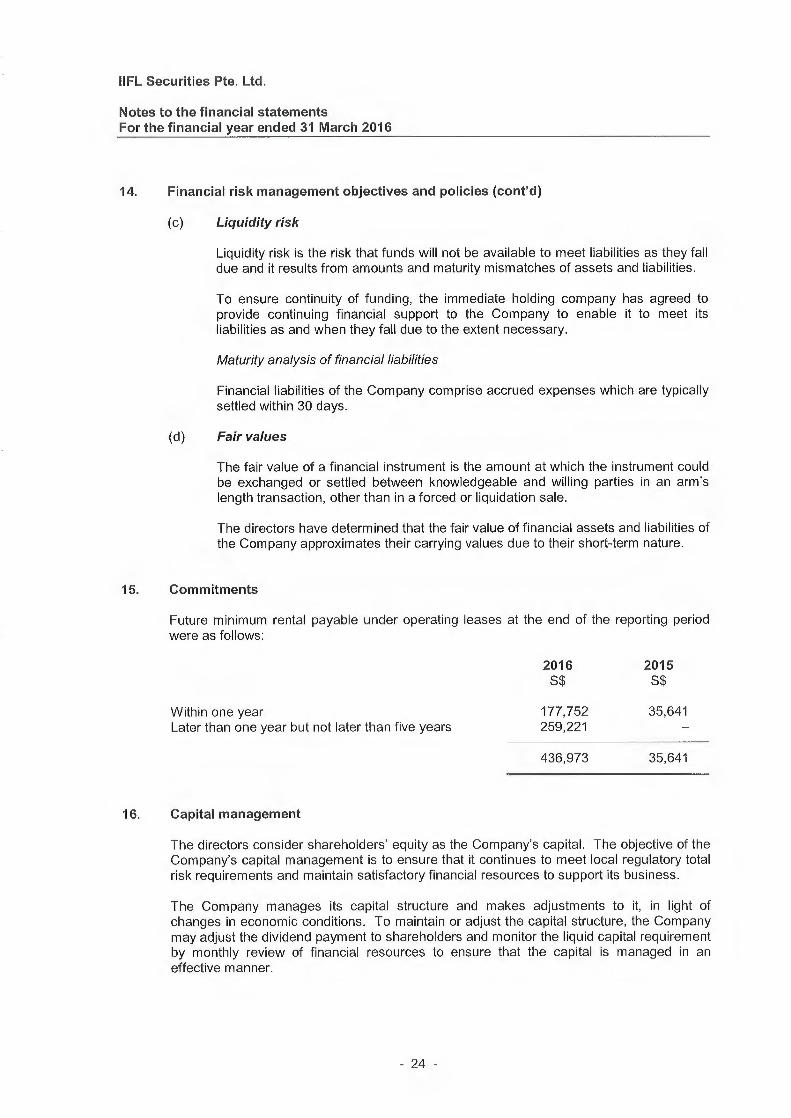

(c) Liquidity risk

Liquidity risk is the risk that funds will not be available to meet liabilities as they falldue and it results from amounts and maturity mismatches of assets and liabilities.

To ensure continuity of funding, the immediate holding company has agreed toprovide continuing financial support to the Company to enable it to meet itsliabilities as and when they fall due to the extent necessary.

Maturity analysis of financial liabilities

Financial liabilities of the Company comprise accrued expenses which are typicallysettled within 30 days.

(d) Fair values

The fair value of a financial instrument is the amount at which the instrument couldbe exchanged or settled between knowledgeable and willing parties in an arm'slength transaction, other than in a forced or liquidation sale.

The directors have determined that the fair value of financial assets and liabilities ofthe Company approximates their carrying values due to their short-term nature.

15. Commitments

Future minimum rental payable under operating leases at the end of the reporting periodwere as follows:

Within one yearLater than one year but not later than five years

16. Capital management

2016 2015S$ S$

177,752 35,641259,221 —

436,973 35,641

The directors consider shareholders' equity as the Company's capital. The objective of theCompany's capital management is to ensure that it continues to meet local regulatory totalrisk requirements and maintain satisfactory financial resources to support its business.

The Company manages its capital structure and makes adjustments to it, in light ofchanges in economic conditions. To maintain or adjust the capital structure, the Companymay adjust the dividend payment to shareholders and monitor the liquid capital requirementby monthly review of financial resources to ensure that the capital is managed in aneffective manner.

-24-

IIFL Securities Pte. Ltd.

Notes to the financial statementsFor the financial year ended 31 March 2016

17. Authorisation of financial statements

The financial statements of the Company for the financial year ended 31 March 2016 wereauthorised for issue in accordance with a resolution of the directors on 28 April 2016.

-25-