india pesticides ipo everything you need to know! about

TRANSCRIPT

www.jstinvestments.com

India Pesticides IPO – Everything you need to know!

About India Pesticides

Incorporated in 1984, India Pesticides Limited (IPL) is one of the leading agrochemicals manufacturers in India. The company operates in two business verticals; 1 Technicals and 2. Formulations. It manufactures herbicide, fungicide Technicals, and Active Pharmaceuticals Ingredients (APIs). It is the sole Indian manufacturer of several Technicals i.e. Folpet, Thiocarbamate, and Herbicide. The company also manufactures 30+ formulations of insecticides, fungicides, and herbicides. Its Technicals are majorly exported to 20+ countries including Australia, Asia, Africa, and European countries, contributed 62% of technical segment revenues in Fiscal 2020. However, agrochemical formulations are primarily sold to domestic crop protection manufacturers i.e. Syngentia Asia Pte Ltd, UPL Ltd, ASCENZA AGRO, S.A., Conquest Crop Protection Pty Ltd, Sharda Cropchem Limited, and Stotras Pty Ltd. Currently, the firm has two manufacturing plants UPSIDC Industrial Area at Dewa Road, Lucknow and Sandila, Hardoi in Uttar Pradesh, India with an installed capacity of 19,500 MT for agrochemicals and 6500 MT for formulations. As of March 31, 2021 - Its insurance cover as a percentage of gross block of property, plant and equipment, and inventory, was 122%. Network of over 20 sales depots consisting of branches, carrying and forwarding agents, and warehouses spread across 15 states in India.

www.jstinvestments.com

About the Offer

Dates – June 23 to 25, 2021

Pricing – Rs 290 to Rs 296

Size – 800 Cr (100 Cr Fresh Issue + 700 Cr Offer for sale)

Market Cap Post Listing – Rs 3407 Cr (11,17,85,130 existing + 0.34 cr new shares * 296 )

Objects of Issue

To finance the working capital requirements of the company.

To meet general corporate purposes.

www.jstinvestments.com

Strengths

www.jstinvestments.com

www.jstinvestments.com

Strategies

www.jstinvestments.com

Quick Numbers

Shareholding

On RHP Date, Promoters and members of Promoter Group hold an aggregate of 92,424,517 Equity Shares, aggregating to 82.68% of the pre-Offer issued, subscribed and paid-up Equity Share capital of the Company.

www.jstinvestments.com

Capital Structure

A recent deal in January happened at Rs 34 per share. The management clarified that it was for an

old consideration and hence the price was low compared to IPO price.

Risks

- Engaged in the manufacture of Technicals and Formulations and their products are required to obtain regulatory pre-approval. As of the date of this Red Herring Prospectus, the following applications for registration from the CIBRC made by the Company were pending:

- The final approval from CIBRC may take from two months to one year depending on the category of the requested registration (Source: F&S Reports).

- They are subject to strict technical specifications, quality requirements, regular inspections and audits by customers including various multinational corporations.

www.jstinvestments.com

- The quality of pesticides manufactured in India, including the pesticides they manufacture, are open to independent verification by Government agencies including the respective governments of the countries where they export products.

- Certain of the raw materials that they use as well as finished goods are corrosive and flammable and require specialized handling and storage, failing which they may be exposed to fires or other industrial accidents. (For instance, on August 18, 2020, they received a notice from the UPPCB in relation to the alleged disposal of industry generated pesticides waste from their facilities at Dewa road, affecting the soil and groundwater quality of the surrounding areas, and directing their Company to conduct a detailed survey of certain sites and to further submit a time-bound program for remediation of the polluted soil and groundwater in the affected area, based on a detailed project report to be approved by the Central 35 Pollution Control Board and the UPPCB within a specified time period and to deposit the annual cost for such remediation in a separate escrow account.) – Update - Report was generated by 3rd party saying everything is fine now.

- Manufacturing facilities, Registered Office and Corporate Office are concentrated in a single region (Uttar Pradesh)

- Business is working capital intensive. If they experience insufficient cash flows from operations or are unable to borrow to meet working capital requirements, it may materially and adversely affect business and results of operations.

- Agro-chemicals business is subject to climatic conditions, the overall area under cultivation and the cropping pattern adopted by the farming community. Seasonal variations and unfavorable local and global weather patterns may have an adverse effect on business, results of operations and financial condition.

- There is a growing consumption of bio-pesticides globally and in India. The use and adoption of bio pesticides by customers may affect competitive position and thereby have an adverse effect on business, results of operations, and financial condition. However, the industry is at a quite nascent stage right now. (Note - Their core focus is on quality and sustainability and none of their key Technicals are classified as ‘red triangle’ or highly toxic products.)

- Majority of revenue is from outside, the management explains their forex strategy in the webinar.

- The Indian agro-chemicals industry is fragmented in nature with presence of more than 150 active ingredient manufacturers, over 1,000 formulators and over 200,000 companies engaged in distribution (Source: F&S Report). They face competition from both domestic and multinational corporations. (They mentioned for this that they are price competitive and experts in chemistries, Technicals and price competitive as well)

- They typically do not enter into long-term agreements with majority of customers (But there are many companies that are with the company from 10-15 years+)

www.jstinvestments.com

Financials

Balance Sheet:

- Business with the requirement of high working capital, however very high asset turnover.

- Borrowings are minimal & all extra WC requirements will be paid by IPO proceeds.

www.jstinvestments.com

Profit & Loss:

Revenue growth has been strong at over 38%.

Management has maintained over 50% gross margins consistently

EBITDA margin jumped to 29% in the latest year: sustainability must be tracked.

www.jstinvestments.com

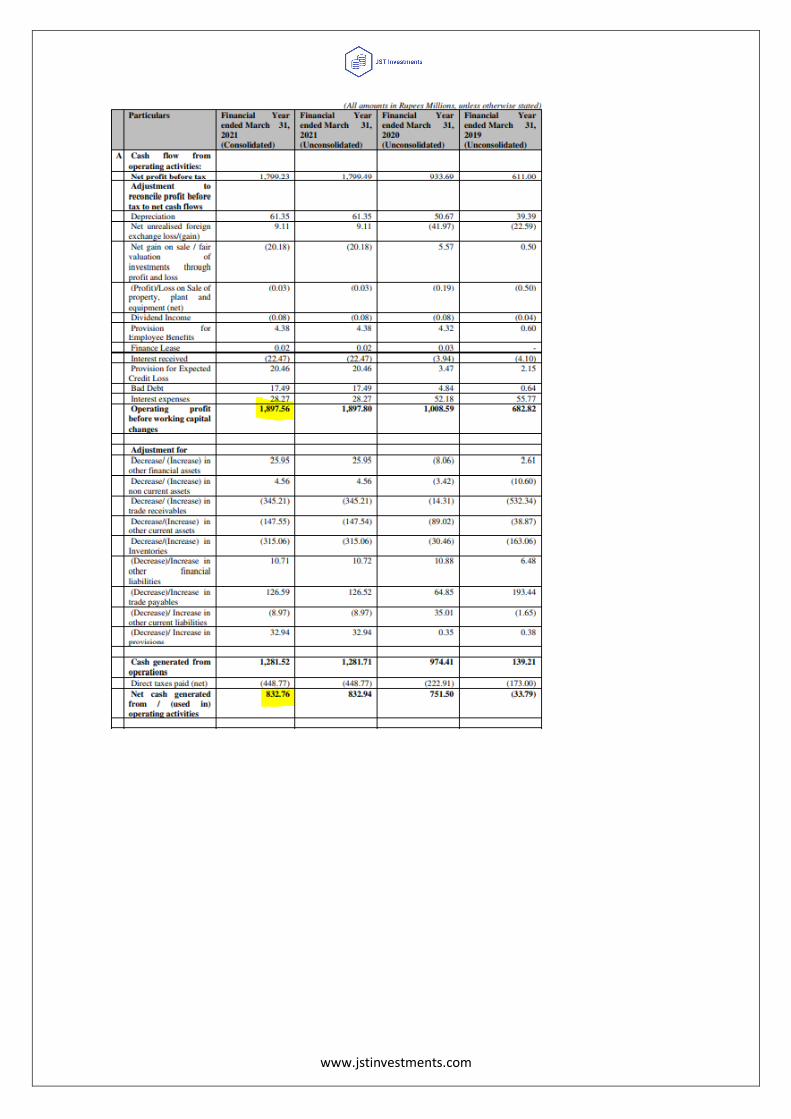

Cash flow Statements:

Working capital investments are aggressive (Note: lack of any bad debt risks)

Any huge capex requirements would have to be debt/ equity funded due to the inherent

volatility in OCF.

In the past, the capex requirements have been controlled.

www.jstinvestments.com

www.jstinvestments.com

Working capital days is nearly 90.

www.jstinvestments.com

IPO Meet Answers -

- Spike in ebitda margins is driven by improvement in yield which is a permanent feature. R&D

spending has resulted in 600 bps improvement in yield, also they are globally cost competitive

(even to China). They are confident that yield margin will be sustainable.

- Lifecycle - They select molecules – regular discussions with customers, they visit us, they attend

conferences, exhibitions, during discussions, we try to zero out some products and after this we

try to evaluate from capability, synergy and availability of RM, process of producing.

Communication always stays open with customers.

- From discovery of molecule to applying for product registration – timeline is 2.5 to 3 years,

during this time parallel they generate registration data which is very big work, CIB registration is

one part, export registration, customer has to register in each one of the region where he has to

sell the product, once customers are with them, they are associated with them for quite some

time as they also spend a lot of money to register IPL as a source, long partnership continues for

5-10-15 years.

- APIs expansion – absolutely , close to 10% rev from APIs, want to increase it further

Our Interaction with Management (Our Head of Research Anish Moonka and our COO Aditya

Kondawar had candid chat with Mr. Anand Agarwal Sir (Chairman) and Rahul Bagaria Sir

(Nonexecutive director) )

- Their focus in always on something complex, meaning creating a differentiated product.

- Don’t just focus on N-1 products but on the ground up: how they can make the molecules using

the basic product.

- Inspiring story of Anand sir (Chairman): Created this business from ground up; from 10K rupees

in 1984 in his courtyard.

- State of the Art plants is the key.

- Most of the customers are there since 10-15 years: They make the products ready & customer

helps with the registrations in different countries: API is a distant story as of now as they are just

having land at the time.

- Geographical concentration risk? Yes, looking for some coastal regions to set up additional

plants.

- Not looking at Products who have more than 50% of RM cost

- Making more molecules is the only remedy to ward off risks and competition

- R&D Future – last 20-30 years, they continuously made products, synergies they have which

others don’t. Like chlorine, 1000-1500 tonne per month they use, people pay you to take it from

their factories, handling of chlorine is very complex, developed expertise in handling carbon

disulphate, and this is synergy for future products.

- R&D API Side - working on APIs, big plans to go APIs, more vigorously

- Speciality chemicals also coming out very soon at their plants, arrangement with customers,

cracked chemistry for those

- Capacity expansion – 20k to 30k, facilities are fungible, same mode of chemistry, so easy to shift

from one to new,

www.jstinvestments.com

- 3rd site – API requires different registration as per USFDA, API plant. Approvals and plant set up

ready to go – final stages of allotment. Capex, permission will go hand in hand post basic

permissions. In talk with global innovator and Indian pharma companies

- Close to 4 bn $ of technical going off patent - they are targeting some big opportunities here,

huge demand there when they go off patent

- API – no number, once they install a capacity, they only do when they have the demand in mind,

capex won’t go dry.

Valuations & Conclusion

Indian Pesticides Limited had a diluted EPS of Rs 12.07 and Book Value of Rs 34.94 as of March 31,

2021. Our talk with the management also helped us understand the fact that they know their

‘Dhanda’ (business) very well.

At upper price band of Rs 296, it is priced at 24.5x P/E and 8.5x P/BV. The valuations seems

reasonable given the complex chemistries (chlorination, etc.) that the company deals with; however

we would like to see the show on the key deliverables in the quarters to come before taking up any

decision.

--------------------------------------------------------------------------------------------------------------------------

Thanks for reading till the end!

If you would like to add anything or give any feedback or would like to appreciate the article, reach

out to me on twitter – aditya_kondawar or email me at [email protected]!

--------------------------------------------------------------------------------------------------------------------------