indian capital markets – equity fund raising options capital... · 2011-04-19 · indian capital...

TRANSCRIPT

Indian Capital Markets – Equity Fund Raising Options

Keyur ShahMBA (Finance), ACS, LLM

Practicing Company Secretary

Indian Capital Market - Background

• Liberalisation in 1992 by Dr. Manmohan Singh, the then Finance Minister

• Radical changes in law – from strict government to open economy

• Establishment of SEBI – strong legal framework

• Increased Foreign Direct Investment

• Corporate Governance and Reporting Requirements

General Understanding

• Sensex / Nifty: How determined

• Interest Rates: High/Low?

• Liquidity in the system

• Inflation

• Exchange rates: INR Vs. USD

• FEMA Guidelines: Foreign Investments in India (Sectoral

Caps): Automatic Route and Approval Route

• Investments by Indian Company abroad: Automatic

Route: up to 400% of net worth

Legal environment for companies seeking issuance of equity

Issuer

• Policy Decisions of Central Government

• Reserve Bank of India Guidelines

• Overseas Regulations

• Companies Act, 1956

Securities Contract

(Regulation) Act, 1956

Foreign Exchange

Management Act, 1999

Stock Exchanges

SEBI Guidelines for

ICDR

Issuer

Pricing Strategy

–Quality of demand (Retail, HNI, Institutions)

–Price sensitivity

–Account by account feedback

–Current market conditions

–Views of leading investors

–Price relative to comparable companies

– Likely aftermarket activity

Pricing

• Valuation based on Average EPS of Company –PE Multiple

• Compared with companies in similar sector with similar turnover

• Discounted Cash Flow Method

• Book Value Method

Size of IPO and Dilution

• Key Parameters:– Maximum issue size: 5 times of net worth

– Minimum Public Shareholding: 25%

– Dilution of 10%: Rule 19(2)(b): Rs. 100 Cr Public Issue, 20 Lacs shares, Book Building

– Minimum/Maximum Dilution: Minimum 25%/10% and Maximum upto the comfort level of promoters (generally below 50%)

– Minimum capital for listing at BSE/NSE: Rs. 10 Cr

– Feasibility of Project

Case Study

• Net Worth : Rs. 20 Cr

• Promoters Holding: 100%

• Turnover: Rs. 70 Cr

• Net Profit: Rs 7 Cr

• PE Multiple: 10

• Maximum size: ?

• Maximum Price: ?

• How Many Shares to be issued: ?

Solution

• Maximum size: Rs. 100 Cr

• Maximum Price: Rs. 100 (Rs. 10 EPS * 10)

• How Many Shares to be issued: 1 Cr

Allocation Considerations

– Tiering of Investors

– Target key accounts that can build core positions and support after market trading

– Focus on investors with long-term investment horizon and track record

– Target selective under-allocation to ensure after market performance

Media Strategy

Issues to be kept in mind

Cost to be incurred using various mediumsLong term corporate strategy and advantages of building brandSetting the league of the company and Investor perceptionCloser to market environment analysis

Advantages of Corporate Advertising

Corporate Ads are important as restrictions that can be carried out for corporate ads are less onerous than issue related advertisements and therefore better brand buildingServes to give advance notice of public offer though no specific mention is madeReinforces the Issuers name in the minds of investors

Television

SMS

Newspaper

Radio

Hoardings

Media Strategy has to be driven by long term corporate strategy.

Other Fund Raising Options - Debt

• Short Term: Working Capital

• Long Term: Term Loans, Project Finance Loans

• External Commercial Borrowings: Cheaper Rates, RBI norms, maximum $500 Million in a year, all in cost ceiling 300 basis points above LIBOR

• Benefits of Trade on Equity

• Lower Cost of Capital

Debt Considerations

• Viable Project

• Promoters Margin: Around 60% to 70%

• Security: Primary and Collateral

• Track Record of Promoters

• Sector concerns

Fund Raising Options: Equity

• Initial Public Offerings (IPO)

• Further Public Offerings (FPO)

• Rights Issue: to existing shareholders

• Preferential Allotment: Pricing guidelines, lock in requirements, Share Warrants (25%, conversion in 18 months)

• QIP: Allotment to institutional investors: Pricing Guidelines, warrants: conversion in 60 months)

Fund Raising Options

• FCCB: Foreign Currency Convertible Bonds

– Issued as debt first

– Option to convert into equity after 3 years or more

– Coupon rate till the time of non conversion

– If not converted, to be repaid with interest

– If converted, listed with the stock exchange in India/abroad

ADR/GDR

• Equity fund raising in foreign markets

• ADR: American Markets

• GDR: European Markets

• Equity shares in bundle are deposited with Indian Custodian Bank which allows issuance of ADR/GDR by foreign custodian banks to investors

• They have option to convert to shares and list in India

Equity Financing Options – Comparison

Criteria IPO

Follow on

Public

Offering Rights Offer GDR FCCB

Qualified

Institutions

Placement

Preferential

Allotment

Pricing • Free –

Issue

determine

d

• Free- Issuer

determined

• Usually Soft

• Free- Issuer

determined

• Usually Soft

• Book

Building

subject to

MoF floor

• Book

Building

subject to

MoF floor

• Same as

GDR

• Relevant

stock

exchange

prescribed

• SEBI

Formula

• Higher of 6

months or 2

week

average of

weekly high

and low

prices

Lock-in for

investors

• None • None • None • None • None • None • 1 Year

Shareholder

approval

• Not

required if

pure equity

instrument

Investors

covenant/

shareholder

agreement/

due

diligence

X X X X X X X

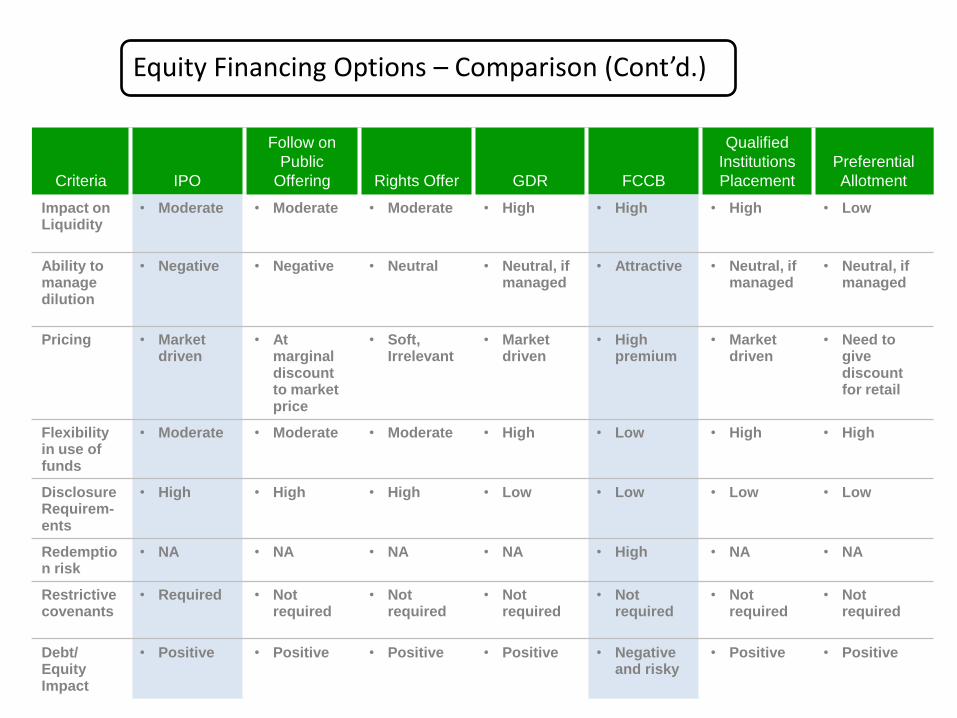

Equity Financing Options – Comparison (Cont’d.)

Criteria IPO

Follow on

Public Offering Rights Offer GDR FCCB

Qualified

Institutions

Placement

Preferential

Allotment

Target

Investors

• QIB defined

by SEBI

which

includes FII

• Non

institutional

• Retail

• QIB defined

by SEBI

which

includes FII

• Non

institutional

• Retail

• Shareholder

s

• Renounces

in all

categories

including

institutions

• FIIs • FIIs, Usually

Hedge and

Speculative

• QIB defined

by SEBI

which

includes FII

• FII, MFs

Completion

period

• 16-18 weeks • 16 – 18

weeks

• 20-22 weeks

to offer

closure

• 8-10 weeks • 8-10 weeks • 6-8 weeks • 10-12 weeks

Accounts • Indian

GAAP

• Indian GAAP • Indian

GAAP

• Indian

GAAP

• Indian

GAAP

• Indian

GAAP

• Indian GAAP

Allocation • Proportionat

e

• Proportionat

e

• Proportionat

e

• Discretionar

y

• Discretionar

y

• Discretionar

y

• Discretionary

Induction of

Quality

investors

• Neutral

• Retail

shareholder

s are

followers

• Neutral

• Retail

shareholder

s are

followers

• Low

• Substantiall

y restricted

to existing

investor

base

• High

• High quality

focused FIIs

participatio

n

• Low

• Attracts

speculative

investors /

hedge funds

• Very High

• High quality

focused QIB

participatio

n

• High

Diversifying

share-

holder base

• High • High • Limited

since caters

to existing

shareholder

base

• Moderate • Moderate • High • Low

Equity Financing Options – Comparison (Cont’d.)

Criteria IPO

Follow on

Public

Offering Rights Offer GDR FCCB

Qualified

Institutions

Placement

Preferential

Allotment

Impact on Liquidity

• Moderate • Moderate • Moderate • High • High • High • Low

Ability to manage dilution

• Negative • Negative • Neutral • Neutral, if managed

• Attractive • Neutral, if managed

• Neutral, if managed

Pricing • Market driven

• At marginal discount to market price

• Soft, Irrelevant

• Market driven

• High premium

• Market driven

• Need to give discount for retail

Flexibility in use of funds

• Moderate • Moderate • Moderate • High • Low • High • High

Disclosure Requirem-ents

• High • High • High • Low • Low • Low • Low

Redemption risk

• NA • NA • NA • NA • High • NA • NA

Restrictive covenants

• Required • Not required

• Not required

• Not required

• Not required

• Not required

• Not required

Debt/ Equity Impact

• Positive • Positive • Positive • Positive • Negative and risky

• Positive • Positive