indian economy: a snapshotdnb.co.in/fesconftool/uploads\downloads\90\indian e… · ·...

TRANSCRIPT

Indian Economy: A Snapshot

“For its first 45 years, Indians had abundant political freedom, but limited economic freedom. (Wealthy Indians could have any car they wanted, so long as it was a white Ambassador).” –International Herald Tribune.

India always held great promise. Soon after independence, in 1947, its foreign reserves were among the worlds largest, at US $2.1 billion in 1950. It accounted for 2.4 percent of global trade. It was one of the prosperous countries in terms of growth in GDP and overall economic activity; certainly ahead of China. However, fallout of certain policy measures such as over-emphasis on agriculture, excessive government intervention and two oil-shocks moderated the pace of economic growth. Rupee started depreciating, fiscal deficit widened, expanding trade deficit depleted the foreign reserves and gradually country was left to pledge its gold with the foreign central bank to mobilise the resources. The rescue operation by IMF urged the government to liberalise the economy. Slowly and steadily economy was put on the path of liberalisation (Exhibit 1).

Exhibit 1. Moving towards new growth trajectory

9.0

5.84.7

3.7

5.6

4.1

0

2

4

6

8

10

1960s 1970s 1980s 1990s FY00-04 FY05-07

Real GDP, period avg. growth (percent) Source: GOI Traditionally agriculture has remained the backbone of India’s

economic growth. The weather related crisis such as drought, flood and cyclone has affected the agriculture production and ultimately the growth in overall economic activities. In 60s, the contribution of agriculture to GDP was around 50-55 percent. Over the period, the share of agriculture to GDP has declined drastically to around 20 percent. The share of industry has improved marginally. The share of services sector to GDP has increased significantly. However, it must be noted that agriculture still employs almost 60 percent of the

2

population. Besides, social problems such as poverty, inequality are widespread in rural areas. The benefits of ‘Green revolution’ have been limited to certain areas and there is an urgent need to innovate and implement the new techniques of farming in both existing and new areas (Exhibit 2).

Exhibit 2 : Services and industry driving the growth process

10

20

30

40

50

60

FY 60 FY 66 FY 72 FY 78 FY 84 FY 90 FY 96 FY 02

(Sha

re in

real

GD

P, p

erce

nt)

Industry Services Agriculture Source: GOI

"I put India on the top priority market among emerging markets."- Yuanquing Yang, Chairman, Lenovo

The gradual opening of the economy has definitely helped the Indian economy to mark its presence in the global growth map. In Asia, both India and China account for almost 60 percent of the growth. Since FY04 India has witnessed real growth above 8 percent, thus taking India to a new growth trajectory. During FY 07, India’s economy expanded by 9.4 percent. Globally, India is now the fastest growing economy after China. According to IMF estimates, India would clock a growth of 8.5 percent in 2007 far above the world growth of 5 percent. In fact, in terms of PPP (Purchasing Power Parity), India has overtaken Japan to become the third largest economy after China and US (Exhibit 3)

3

Exhibit 3: India- fastest growing country after China

0

2

4

6

8

10

12

World G-7 countries NewlyIndustrialised

Asia

China

(Rea

l GD

P gr

owth

, per

cent

)

2006 2007E 2008E Source: IMF

The New Economic Policy of 1991 included standard structural adjustment measures including the devaluation of the rupee, increase in interest rates, reduction in public investment and expenditure, reduction in public sector food and fertilizer subsidies, increase in imports and foreign investment in capital-intensive and high-tech activities, and abolition of the cash compensatory support for exports. Slowly but steadily India’s share in global merchandise trade has improved from meagre 0.5 percent (in early 1990s) to 1 percent (2005). The share of merchandise trade to GDP has increased substantially to almost 35 percent. In early 1990s, India had foreign reserves for hardly 3 months. The outward looking policy has accentuated the foreign reserves to US$ 170 bn in 2006 from US$ 5 bn in 1993. The huge pool of foreign reserves would help to manage not only rising imports but also external debt (Exhibit 4).

4

Exhibit 4: Rising foreign reserves

0

5

10

15

20

Dec

-92

Feb-

94

Apr

-95

Jun-

96

Aug

-97

Oct

-98

Dec

-99

Feb-

01

Apr

-02

Jun-

03

Aug

-04

Oct

-05

Dec

-06

0

55

110

165

220

Import cover of foreign reserves (# months) (LHS)

Foreign reserves (US $ bn) (RHS) Source: RBI

“23% of the Global workforce addition over the next five years will be from India” - Economist

Traditional emphasis on education, high skills and young population has given tremendous comparative advantage to make India powerhouse in IT and ITES. According to Science and Engineering Report 2006, 20,382 Indians received doctorate during 1983-2003 in United States. Annually, around 50,000 engineers are generated in India’s education system. Such a pool of talent, available both domestically as well as internationally, has been a source of both visibility and financial assets in terms of NRI deposits and private remittances. With increasing participation of working population, India would be one of the fastest growing young countries (Exhibit 5).

5

Exhibit 5: Fastest growing young country

10

25

40

55

70

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

(Sha

re o

f wor

king

pop

ulat

ion

to to

tal p

opul

atio

n, p

erce

nt)

Source: UN

China

US

India

“FDI will continue to be encouraged and actively sought, particularly in the areas of infrastructure, high technology and exports”- P. Chidambaram, Finance Minister

The development of infrastructure is critical to keep the Indian economy on new growth trajectory. This is one area where there is a need for private sector and foreign investment to come in. Because of the long gestation period, and many social implications, the infrastructure sector competes unfavourably with manufacturing and many other sectors. For this, specific policies in this area are needed to make infrastructure attractive. Clearly, there is a wide gap between the potential demand for infrastructure for high growth and the available supply. This is the challenge placed before the economy, i.e. before the public and private sector and foreign investors. This can also be seen as an opportunity for a widening market and enhanced production.

6

Exhibit 6: Investment avenues in infrastructure

Sectoral Investments (Rs.bn)

Power generation,

4,100

Urban Infrastructure,

1,974

Railways, 3,000

Energy, 2,120

Airports, 400

Ports, 500

Highways, 2,200

Source: Planning Commision

“Finance is, as it were, the stomach of the country, from which all the other organs take their tone.”- William Gladstone, Former British PM

A well-developed financial system should improve the efficiency of financing decisions, favouring a better allocation of resources and thereby economic growth. The financial system is also particularly important in reallocating capital and thus providing the basis for the continuous restructuring of the economy that is needed to support growth. In recognition of the critical role of the financial markets, the initiation of the structural reforms in the early 1990s in India also encompassed a process of phased and coordinated deregulation and liberalisation of financial markets. Financial markets in India in the period before the early 1990s were characterised by administered interest rates, quantitative ceilings, statutory pre-emptions, captive market for government securities, and excessive reliance on central bank financing, pegged exchange rate, and current and capital account restrictions. As a result of various reforms, the financial markets have transited to a regime characterised by market-determined interest and exchange rates, price-based instruments of monetary policy, current account convertibility, phased capital account liberalisation and an auction-based system in the government securities market. Furthermore, various measures are underway to bring efficiency in the various aspects of financial market such as capital account convertibility, IPO grading, risk management, market for credit default swap.

7

Key Indicators of Financial Market Development

Price Stability

4

8

12

16

20

FY 9

2FY

93

FY 9

4FY

95

FY 9

6FY

97

FY 9

8FY

99

FY 0

0FY

01

FY 0

2FY

03

FY 0

4FY

05

FY 0

6FY

07

(per

cent

)

0

4

8

12

16

Bank Rate PLR (Max) Inflation (RHS) Source: GOI

PLR

Bank Rate

Inflation

Interest rate mechanism supported by price stability management has created investment friendly environment

Sound banking system

0

2

4

6

8

FY 00 FY 01 FY 02 FY 03 FY 04 FY 05 FY 06Non-performing assets (% to total assets) Source: RBI

India has one of the lowest NPAs among BRIC countries

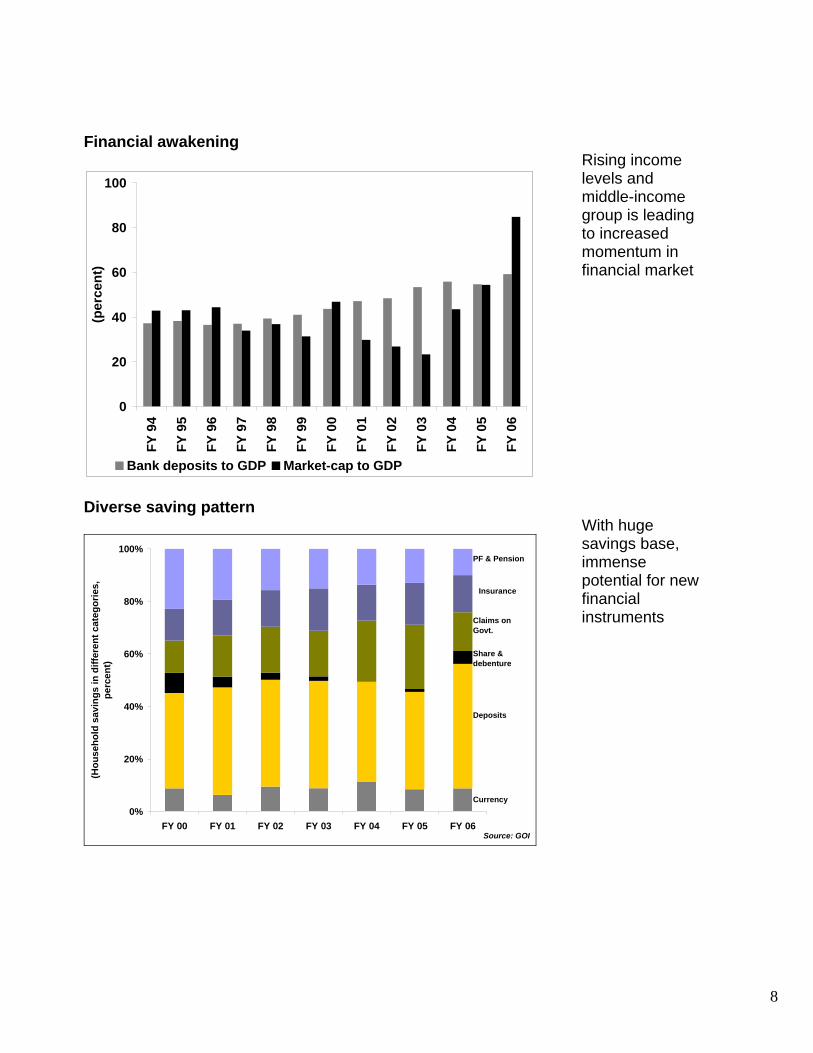

8

Financial awakening

0

20

40

60

80

100

FY 9

4

FY 9

5

FY 9

6

FY 9

7

FY 9

8

FY 9

9

FY 0

0

FY 0

1

FY 0

2

FY 0

3

FY 0

4

FY 0

5

FY 0

6

(per

cent

)

Bank deposits to GDP Market-cap to GDP

Rising income levels and middle-income group is leading to increased momentum in financial market

Diverse saving pattern

0%

20%

40%

60%

80%

100%

FY 00 FY 01 FY 02 FY 03 FY 04 FY 05 FY 06

(Hou

seho

ld s

avin

gs in

diff

eren

t cat

egor

ies,

pe

rcen

t)

Source: GOI

Currency

Deposits

Share & debenture

Claims on Govt.

Insurance

PF & Pension

With huge savings base, immense potential for new financial instruments

9

Growing penetration of MF industry The mutual fund industry’s contribution to the nation’s GDP (in terms of AUM) is on the rise. In 2006, Rs. 1 lakh crore was added to the total asset base. The current figure stands at Rs. 4.85 lakh crore or thereabouts. However, the asset under management for India is a mere 0.36% of the total world assets as on 31st march 2007.

Gross resource mobilisation by MFs

0%

20%

40%

60%

80%

100%

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Pvt Public UTISource: NSE

Public

Pvt

UTI

There is huge potential to enhance equity ownership

Growing middle class

14,958

16,130

17,258

18,742

19,512

21,357

22,487

25,046

0 5,000 10,000 15,000 20,000 25,000

FY 01

FY 00

FY 01

FY 02

FY 03

FY 04

FY 05

FY 06

Per capital personal disposable income (Rs) Source: GOI

Surveys indicate sharp increase in the rise of middle-high income group population

10

Foreign investors are bullish on Indian equity market

50

70

90

110

130

150

170

190

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

0

4

8

12

16

20

24

28

Average market turnover, Rs.billion (LHS)Share of FII activity in market turnover, percent (RHS) Source: SEBI

Underlying fundamentals of Indian economy makes India a preferred investment destination

Bond market yet to develop

0

1

2

3

4

5

6

Apr

-01

Dec

-01

Aug

-02

Apr

-03

Dec

-03

Aug

-04

Apr

-05

Dec

-05

Aug

-06

Apr

-07

4

5

6

7

8

9

10

Turnover in G-sec mkt (Rs.trn)-LHS 10 Yr yield - RHS Source: RBI

G-sec still remains under RBI’s control thus leading to task management at interest rate level

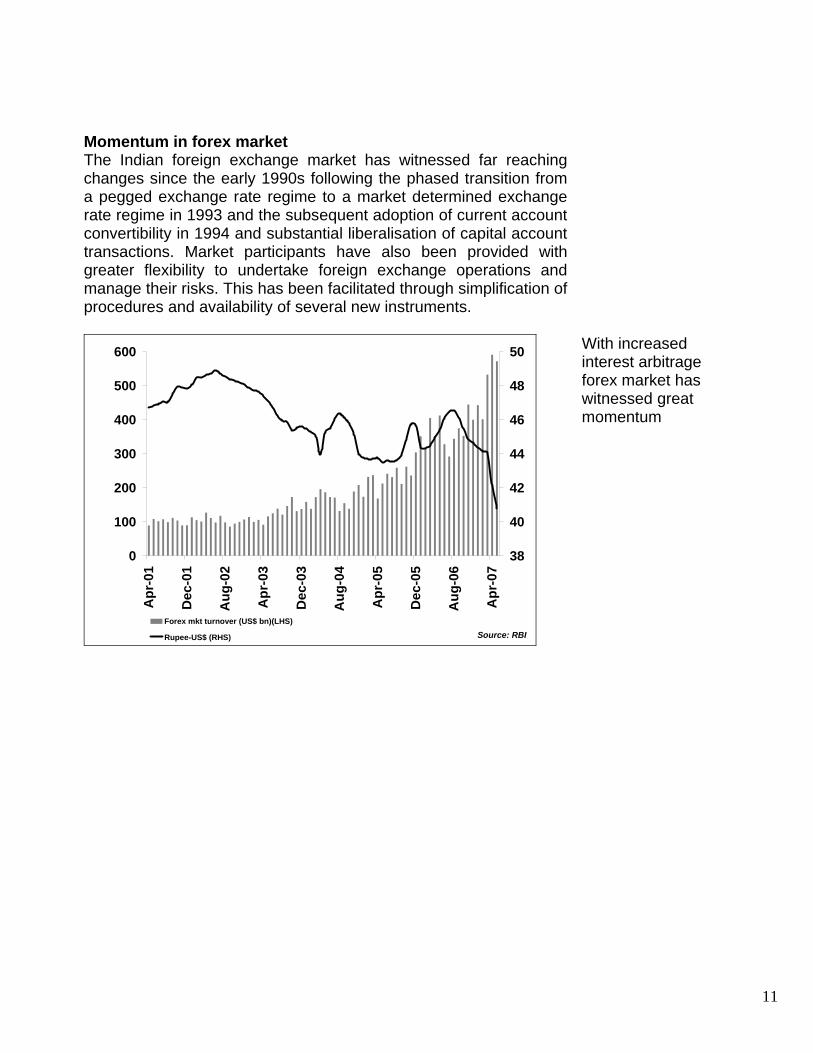

11

Momentum in forex market The Indian foreign exchange market has witnessed far reaching changes since the early 1990s following the phased transition from a pegged exchange rate regime to a market determined exchange rate regime in 1993 and the subsequent adoption of current account convertibility in 1994 and substantial liberalisation of capital account transactions. Market participants have also been provided with greater flexibility to undertake foreign exchange operations and manage their risks. This has been facilitated through simplification of procedures and availability of several new instruments.

0

100

200

300

400

500

600

Apr

-01

Dec

-01

Aug

-02

Apr

-03

Dec

-03

Aug

-04

Apr

-05

Dec

-05

Aug

-06

Apr

-07

38

40

42

44

46

48

50

Forex mkt turnover (US$ bn)(LHS)

Rupee-US$ (RHS) Source: RBI

With increased interest arbitrage forex market has witnessed great momentum

12

New areas of investment

0

100

200

300

400

500

Apr

-04

Aug

-04

Dec

-04

Apr

-05

Aug

-05

Dec

-05

Apr

-06

Aug

-06

Dec

-06

Apr

-07

Average daily turnover in derivative market (Rs.bn) Source: NSE

• One of the highest returns in derivatives market globally.

• Trading in

commodities is also picking up substantially.The MCX volumes grew 123% in 2006.

Corporate on roll

2

4

6

8

10

12

Mar

-01

Nov

-01

Jul-0

2

Mar

-03

Nov

-03

Jul-0

4

Mar

-05

Nov

-05

Jul-0

6

Mar

-07

Profit Margins (%) (a sample of ~ 4000 cos.)

Better corporate governance, best management practices are helping India Inc to improve the margins

13

Increased M & A activities

100

600

1100

1600

FY 04 FY 05 FY 06 FY 070

800

1600

2400

Mergers & acquisitions (number) (LHS) Acquisition (Rs. Bn) (RHS) Source: CMIE

Backed by better financial performance, Indian companies are not only acquiring domestic companies but overseas companies too. This necessitates strong banking system

Significant rise in FDI inflows

0

5

10

15

20

FY 9

1FY

92

FY 9

3FY

94

FY 9

5FY

96

FY 9

7FY

98

FY 9

9FY

00

FY 0

1FY

02

FY 0

3FY

04

FY 0

5FY

06

FY 0

7

FDI inflows, gross (US $ bn) Source: GOI

Strong economic fundamentals and better corporate performance is attracting huge foreign investments

14

Financial market integration Financial market reforms in India have enabled a greater integration of various segments of the financial market, reducing arbitrage opportunities, achieving higher level of efficiency in market operation of intermediaries and increasing efficacy of monetary policy in the economy. Growing integration of financial markets beginning 2000 could be gauged from cross correlation among various market interest rates. The correlation structure of interest rates reveals several notable features of integration of specific market segments.

15

Competing for future!

• Globally, India’s FDI attractiveness is the highest across the sectors

• Innovation-another factor, where India has advantage over its peers

• However, socio-political structure blocks Ease of Doing Business in India

16

India: In juxtapose

Gross Domestic Savings (as % of GDP)

43.0

32.4

31.7

28.7

18.3

17.0

13.7

47.3China

Malaysia

India

South Korea

Indonesia

Philippines

Sri Lanka

Pakistan

44.9

33.8

29.8

28.4

24.6

21.8

20.7

14.3

0 10 20 30 40 50

China

India

South Korea

Sri Lanka

Indonesia

Pakistan

Malaysia

Philippines

Capital formation (as % of GDP)

Merchandise Exports (FOB) (% growth) 2006

24.7

17.5

15.4

14.4

13.9

12.3

10.3

27.2China

India

Indonesia

Pakistan

South Korea

Philippines

Sri Lanka

Malaysia

5.9

8.6

10.8

18.4

19.7

19.9

31.5

39.4

0 10 20 30 40

Indonesia

Philippines

Malaysia

South Korea

Sri Lanka

China

India

Pakistan

Merchandise Imports CIF (growth %)-2006

17

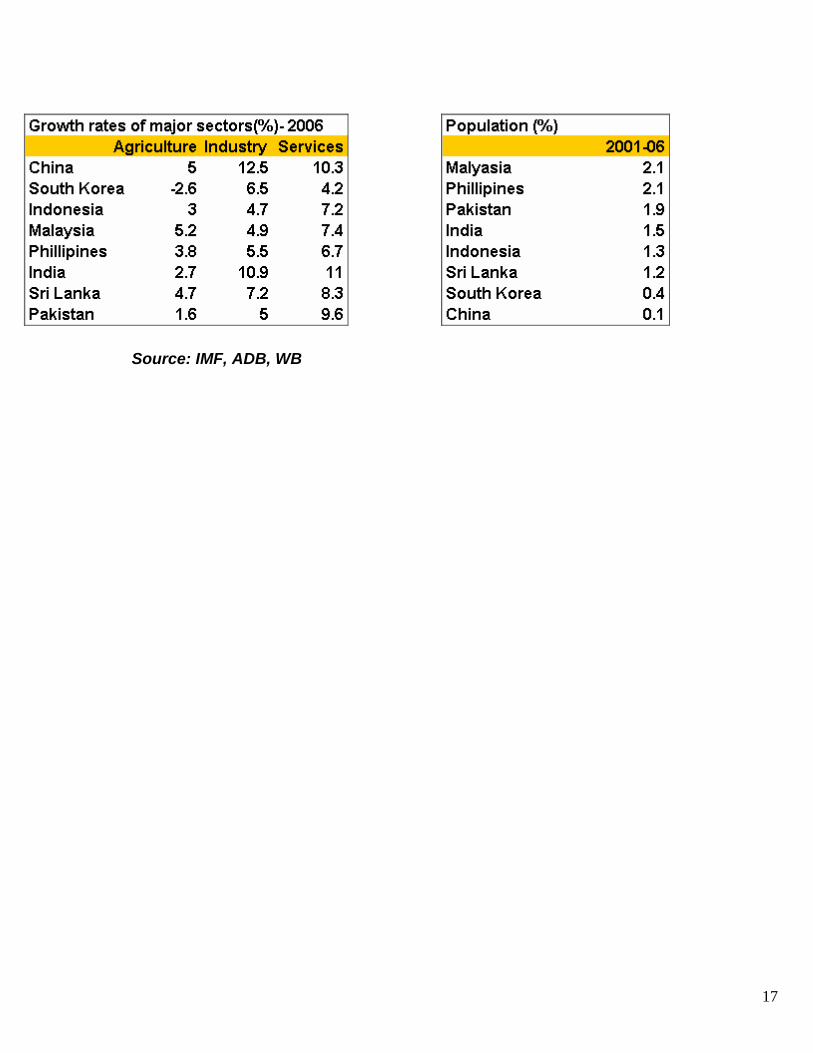

Source: IMF, ADB, WB

18

Major Economic Indicators

1990 2000 2001 2002 2003 2004 2005 2006 2007E 2008E Real GDP Growth-(%) Brazil -4.20 4.30 1.30 2.70 1.10 5.70 2.90 3.70 4.40 4.20 China 3.80 8.40 8.30 9.10 10.00 10.10 10.40 10.70 10.00 9.50 India 6.00 5.30 4.10 4.30 7.30 7.80 9.20 9.20 8.40 7.80 Indonesia 7.20 5.40 3.60 4.50 4.80 5.00 5.70 5.50 6.00 6.30 Japan 5.20 2.90 0.20 0.30 1.40 2.70 1.90 2.20 2.30 1.90 Korea 9.20 8.50 3.80 7.00 3.10 4.70 4.20 5.00 4.40 4.40 Pakistan 4.50 4.30 2.00 3.20 4.90 7.40 8.00 6.20 6.50 6.50 Phillipines 3.00 6.00 1.80 4.40 4.90 6.20 5.00 5.40 5.80 5.80 Russia n/a 10.00 5.10 4.70 7.30 7.20 6.40 6.70 6.40 5.90 Singapore 9.20 10.10 -2.40 4.20 3.10 8.80 6.60 7.90 5.50 5.70 South Africa

-0.30 4.20 2.70 3.70 3.10 4.80 5.10 5.00 4.70 4.50

Sri Lanka 6.20 6.00 -1.50 4.00 6.00 5.40 6.00 7.50 7.00 7.00 Turkey 9.30 7.40 -7.50 7.90 5.80 8.90 7.40 5.50 5.00 6.00 United Kingdom

0.70 3.80 2.40 2.10 2.70 3.30 1.90 2.70 2.90 2.70

United States

1.90 3.70 0.80 1.60 2.50 3.90 3.20 3.30 2.20 2.80

GDP Per capita –Current prices(US $) Brazil 3,464 3,762 3,190 2,867 3,085 3,654 4,789 5,717 6,220 6,523 China 339 946 1,038 1,132 1,270 1,486 1,716 2,001 2,310 2,574 India 378 455 461 473 543 618 712 797 871 942 Indonesia 699 807 773 928 1,100 1,188 1,309 1,640 1,812 1,950 Japan 24,560 36,811 32,234 30,809 33,180 36,076 35,672 34,188 33,668 34,865 Korea 6,154 10,891 10,177 11,504 12,711 14,181 16,444 18,392 19,485 20,634 Pakistan 443 539 509 502 563 655 728 830 893 960 Phillipines 718 994 914 966 982 1,038 1,154 1,345 1,503 1,591 Russia n/a 1,768 2,096 2,379 2,975 4,104 5,323 6,856 8,209 9,508 Singapore 12,091 23,077 20,692 21,113 22,066 25,330 26,879 29,917 32,506 34,461 South Africa

3,039 2,986 2,633 2,440 3,622 4,666 5,160 5,384 5,680 6,036

Sri Lanka 494 884 841 870 949 1,031 1,200 1,355 1,549 1,704 Turkey 2,698 2,995 2,126 2,675 3,463 4,289 5,062 5,408 5,882 6,113 United Kingdom

17,404 24,542 24,286 26,541 30,470 36,019 37,042 39,213 43,735 46,259

United States

23,208 34,771 35,491 36,311 37,641 39,841 41,960 44,190 45,490 47,160

19

1990 2000 2001 2002 2003 2004 2005 2006 2007E 2008E

GDP-PPP based (US $ billion) Brazil 797 1,269 1,317 1,366 1,402 1,513 1,594 1,701 1,805 1,912 China 1,507 4,960 5,500 6,106 6,859 7,766 8,817 9,984 11,207 12,518 India 1,148 2,427 2,587 2,744 3,004 3,337 3,730 4,159 4,555 4,973 Indonesia 346 625 663 705 754 815 886 960 1,038 1,129 Japan 2,351 3,259 3,350 3,413 3,548 3,732 3,946 4,171 4,346 4,519 Korea 344 761 809 880 927 998 1,069 1,156 1,229 1,307 Pakistan 149 268 280 294 315 348 387 423 462 502 Phillipines 184 305 318 338 362 395 428 462 497 537 Russia n/a 1,038 1,117 1,190 1,304 1,438 1,576 1,727 1,877 2,032 Singapore 38 97 97 102 108 120 132 145 155 164 South Africa

284 417 439 463 487 523 566 606 644 683

Sri Lanka 34 70 71 75 81 88 96 104 113 122 Turkey 252 439 416 457 493 553 611 661 708 758 United Kingdom

1,013 1,578 1,653 1,717 1,800 1,912 2,006 2,122 2,225 2,327

United States

5,698 9,638 9,944 10,279 10,761 11,499 12,229 13,021 13,675 14,385

GDP-(PPP based) share in world total (%) Brazil 2.97 2.82 2.79 2.76 2.67 2.67 2.60 2.57 2.55 2.53 China 5.61 11.02 11.65 12.34 13.06 13.68 14.39 15.08 15.83 16.55 India 4.27 5.39 5.48 5.55 5.72 5.88 6.09 6.28 6.43 6.58 Indonesia 1.29 1.39 1.40 1.42 1.44 1.44 1.45 1.45 1.47 1.49 Japan 8.75 7.24 7.09 6.90 6.76 6.57 6.44 6.30 6.14 5.98 Korea 1.28 1.69 1.71 1.78 1.77 1.76 1.75 1.75 1.74 1.73 Pakistan 0.55 0.60 0.59 0.60 0.60 0.61 0.63 0.64 0.65 0.66 Philippines 0.69 0.68 0.67 0.68 0.69 0.70 0.70 0.70 0.70 0.71 Russia n/a 2.31 2.37 2.41 2.48 2.53 2.57 2.61 2.65 2.69 Singapore 0.14 0.22 0.21 0.21 0.21 0.21 0.22 0.22 0.22 0.22 South Africa

1.06 0.93 0.93 0.94 0.93 0.92 0.92 0.92 0.91 0.90

Sri Lanka 0.13 0.16 0.15 0.15 0.15 0.16 0.16 0.16 0.16 0.16 Turkey 0.94 0.98 0.88 0.92 0.94 0.97 1.00 1.00 1.00 1.00 United Kingdom

3.77 3.51 3.50 3.47 3.43 3.37 3.28 3.20 3.14 3.08

United States

21.20 21.41 21.06 20.78 20.49 20.25 19.96 19.66 19.31 19.02

20

1990 2000 2001 2002 2003 2004 2005 2006 2007E 2008E

Current account balance (US $ bn) Brazil -3.79 -24.23 -23.22 -7.64 4.18 11.68 14.19 13.65 8.94 3.26 China 12.00 20.52 17.41 35.42 45.88 68.66 160.82 238.54 303.65 358.62 India -7.89 -4.60 1.41 7.06 8.77 0.78 -6.85 -19.30 -23.77 -24.57 Indonesia -3.20 7.99 6.90 7.82 8.11 1.56 0.31 9.73 7.51 5.67 Japan 43.94 119.61 87.79 112.61 136.24 172.07 165.69 170.36 166.59 159.14 Korea -2.01 12.25 8.03 5.39 11.95 28.17 14.98 6.09 3.08 -0.17 Pakistan -1.38 -0.22 0.33 2.83 4.06 1.81 -1.53 -5.00 -5.64 -5.60 Philippines -2.69 -2.23 -1.76 -0.35 0.28 1.63 1.96 3.35 2.83 2.68 Russia n/a 46.84 33.94 29.12 35.41 58.59 83.35 95.60 72.90 67.80 Singapore 3.12 10.72 12.00 12.09 22.33 21.54 28.61 36.29 39.64 41.94 South Africa

1.55 -0.17 0.33 0.92 -1.81 -6.92 -9.18 -16.42 -17.42 -17.39

Sri Lanka -0.38 -1.07 -0.18 -0.24 -0.07 -0.64 -0.66 -1.10 -1.48 -1.75 Turkey -2.56 -9.82 3.39 -1.52 -8.04 -15.60 -22.71 -31.46 -31.39 -30.83 United Kingdom

-39.77 -37.65 -31.51 -24.79 -24.39 -35.41 -53.73 -68.12 -81.40 -87.98

United States

-78.97 -415.15 -388.96 -472.44 -527.52 -665.29 -791.50 -856.66 -834.62 -866.15

21

Current account balance (% of GDP) Brazil -0.70 -3.80 -4.20 -1.50 0.80 1.80 1.60 1.30 0.80 0.30 China 3.10 1.70 1.30 2.40 2.80 3.60 7.20 9.10 10.00 10.50 India -2.50 -1.00 0.30 1.40 1.50 0.10 -0.90 -2.20 -2.40 -2.30 Indonesia -2.50 4.80 4.30 4.00 3.50 0.60 0.10 2.70 1.80 1.30 Japan 1.40 2.60 2.10 2.90 3.20 3.70 3.60 3.90 3.90 3.60 Korea -0.80 2.40 1.70 1.00 2.00 4.10 1.90 0.70 0.30 0.00 Pakistan -2.90 -0.30 0.50 3.90 4.90 1.80 -1.40 -3.90 -4.00 -3.60 Philippines -6.10 -2.90 -2.50 -0.50 0.40 1.90 2.00 2.90 2.10 1.90 Russia n/a 18.00 11.10 8.40 8.20 9.90 10.90 9.80 6.20 5.00 Singapore 8.50 11.60 14.00 13.70 24.20 20.10 24.50 27.50 27.10 26.60 South Africa

1.40 -0.10 0.30 0.80 -1.10 -3.20 -3.80 -6.40 -6.40 -6.00

Sri Lanka -4.70 -6.50 -1.10 -1.40 -0.40 -3.20 -2.80 -4.10 -4.80 -5.10 Turkey -1.70 -5.00 2.40 -0.80 -3.30 -5.20 -6.30 -8.00 -7.30 -6.80 United Kingdom

-4.00 -2.60 -2.20 -1.60 -1.30 -1.60 -2.40 -2.90 -3.10 -3.10

United States

-1.40 -4.20 -3.80 -4.50 -4.80 -5.70 -6.40 -6.50 -6.10 -6.00

1990 2000 2001 2002 2003 2004 2005 2006 2007E 2008E Population (Persons millions) Brazil 147 171 174 176 179 182 184 187 189 192 China 1,143 1,267 1,276 1,285 1,292 1,300 1,308 1,314 1,321 1,327 India 835 1,015 1,029 1,046 1,062 1,079 1,096 1,113 1,130 1,147 Indonesia 180 205 208 211 214 216 219 222 225 228 Japan 123 127 127 127 128 128 128 128 128 128 Korea 43 47 47 48 48 48 48 48 48 48 Pakistan 108 138 140 143 147 150 153 155 158 161 Philippines 62 76 78 80 81 84 85 87 89 90 Russia 148 147 146 145 145 144 144 143 142 141 Singapore 3 4 4 4 4 4 4 4 4 5 South Africa

37 45 45 46 46 46 47 47 48 48

Sri Lanka 16 18 19 19 19 19 20 20 20 20 Turkey 55 66 67 68 69 71 72 73 74 75 United Kingdom

57 59 59 59 60 60 60 61 61 61

United States

250 282 285 288 291 294 297 300 303 306

Source: IMF