indian gaar: is uncertainty causing a setback to … file5/3/2018 · the indian taxation system is...

TRANSCRIPT

INDIAN GAAR: IS UNCERTAINTY CAUSING A SETBACK TO

FOREIGN INVESTMENTS?

Ameya Mithe & Rohan Shrivastava

Abstract

This paper discusses the historical view point of anti-avoidance in light of

Judicial Anti-Avoidance Rule in India and United Kingdom. It deals with

intricacies of treaty override and analyses its permissibility under the

Constitution. The paper focuses on the uncertainty impending around due to the

limited grandfathering of investments and clarifications made thereon. This paper

also addresses the uncertainty in application of SAAR and GAAR and the

possibility of their co-existence. The authors have elucidated the effects of GAAR

on Foreign Investments and have pin pointed the investors‘ concerns. At the end

the paper, the authors analyse the Indian GAAR in comparison with its

contemporary in the UK to show how certainty can be achieved in a statutory

GAAR. The paper aims to bring into light the uncertainty looming around the

current structure of GAAR in India and showing the repercussions of such

uncertainty on Foreign Investments.

1. INTRODUCTION

The Indian taxation system is at such a point of inflection, that it defies the wisdom of

great thinkers by making the word ‗certain‘ an inappropriate adjective to describe tax. The

advent of the much dreaded General Anti-Avoidance Rule (hereinafter ‗GAAR‘) in Chapter

X-A of the Income Tax Act, 1961 (hereinafter ‗the Act‘) has marked a threshold in the

process of tax planning, which brings in a very dense atmosphere of uncertainty among the

investors. This is not because of the introduction of a statutory GAAR itself, but because of

the confusion which the current structure of the GAAR as introduced in the Act has created at

so many levels. The Finance Act, 2013, although being an improvement to its predecessor in

Students of Law, Symbiosis Law School, Pune; E-mails: [email protected],

[email protected]. Authors would like to thank Mr. Sriram P. Govind, Associate Nishith Desai

Associates for his invaluable guidance and support. They would also like to thank Advocate Mihir C.

Naniwadekar, Bombay High Court, Mumbai for his valuable suggestions and discussions.

VOL. 1] INDIAN JOURNAL OF TAX LAW 56

terms of GAAR, has not done enough to clarify the position. It is much feared, and correctly

so, that GAAR as it exists in the Act gives wide powers to the Revenue to question each and

every arrangement, or a step in or a part thereof, of an investor, with a scope that these

powers may be abused to an extent that the ultimate onus of escaping the scrutiny falls on the

investor himself. The drafting of the GAAR provisions give a wide scope of discretion in

favour of the Income Tax Department (hereinafter ‗Department‘) to do so, and a very

negligible opportunity for an assessee to challenge the authority of the Department in this

regard. The clarifications by the Finance Ministry, followed by the recently notified GAAR

Rules1 have failed to adequately answer several questions, and the answers to the questions

they have answered have not been entirely satisfactory. Such an ambiguous situation has

cropped an atmosphere of uncertainty in the midst of investors.

The appetite of a country for tax being insatiable, and the ingenuity displayed by the

modern taxpayers of playing with the letter of the law has led to a change in approach of the

tax authorities and the courts for preventing the erosion of tax base, or rather, for maximising

the coffers of the government. A country which adopts a statutory GAAR appears to have

exercised its choice of prioritizing prevention of erosion of tax base over the principle of

certainty in taxation. Certainty in taxation is viewed as an inseparable principle to govern the

tax policy of an economy. Adam Smith, cited as the ―father of modern economics‖, has

premised four basic canons of taxation, of which ‗Certainty‘ is the second canon of taxation.2

The uncertainty in taxation encourages the insolence, and the favours of corruption, of an

order of men who are naturally unpopular, even where they are neither insolent nor corrupt.3

The effect of uncertainty can deter the investors from the economy or can lead to exploitation

of taxpayers. The need of certainty, at very basic level, can be understood with the aid of an

example. Suppose there is a ―standard‖ providing that motorists should ―drive carefully‖.

This can mean anything and can be interpreted to suit one‘s own convenience. On the other

hand, if there is a ―rule‖ stating that motorists should not exceed a speed limit of 60 kmph,

there is no scope for confusion and everyone knows what the rule means. Such certainty is

missing out from the present structure of GAAR.

1 Income Tax (17th Amendment) Rules, 2013, CBDT Notification dated 23/09/2013. The notification

inserted Rules 10U to 10UC in the Income Tax Rules, 1962.

2 ADAM SMITH, AN INQUIRY INTO THE NATURE AND CAUSES OF THE WEALTH OF NATIONS 676, (Unabridged ed., 1776).

3 Id., at 677; Certainty is also described as one of the ten principles envisaged by the American Institute of

Certified Public Accountants (AICPA) in one of its report of 2001. Certainty in addition to other

principles makes a structure more fair and workable.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 57

The present structure of GAAR needs many more clarifications with respect to various

aspects so that a certain degree of certainty is achieved. The Press release4 issued by Finance

Minister, on behalf of the government, accepted most of the recommendations of the Expert

committee set up to look into the grievances on GAAR. But even after such acceptance the

uncertainty looms upon. The authors are not of the view of opposing the introduction of

GAAR in India. The authors are trying to propose that the present structure of GAAR needs

much more certainty and it should also keep up the investor‘s legitimate interests.

2. INDIA’S JUDICIAL ANTI-AVOIDANCE RULE

Years of judicial interpretation have resulted in a settled position of distinguishing

between tax evasion and tax avoidance in terms of legal consequences. ―Avoidance of tax is

not tax evasion and it carries no ignominy with it, for it is sound law and, certainly, not bad

morality, for anybody to so arrange his affairs as to reduce the brunt of taxation to a

minimum.‖5 On the other hand tax evasion as an illegal means of preventing tax liability has

been accepted unanimously by the judiciary.6 Therefore, tax planning as distinguished from

tax evasion, has historically been an accepted right of a tax payer. This right was given

judicial protection in the famous case of IRC v. Duke of Westminster.7 In the words of Lord

Tomlin in this case-

―Every man is entitled if he can to order his affairs so that the tax attaching

under the appropriate Acts is less than it otherwise would be. If he succeeds in

ordering them so as to secure this result, then, however unappreciative the

Commissioners of Inland Revenue or his fellow tax gatherers may be of his

ingenuity, he cannot be compelled to pay an increased tax.‖

The supposed doctrine that in revenue cases ‗the substance of the matter‘ may be

regarded as discrete from the form or the strict legal position, was given its quietus by the

House of Lords in the Westminster case.8 This case settled the law that a taxpayer‘s

4 PRESS INFORMATION BUREAU, GOVERNMENT OF INDIA, Major Recommendations of Expert Committee on

GAAR accepted, (14 January 2013, New Delhi).

5 Aruna v. State of Madras, (1965) 55 ITR 642, 648 (Mad).

6 David F. Williams, Tax and Corporate Social Responsibility, available at

http://www.kpmg.co.uk/pubs/Tax_and_CSR_Final.pdf (June 07 2013, 10:50 AM).

7 IRC v. Duke of Westminster, [1935] All ER 259.

8 KANGA, PALKHIWALA AND VYAS, THE LAW AND PRACTICE OF INCOME TAX, (9th ed., 2004) (hereinafter

‗KANGA‘).

VOL. 1] INDIAN JOURNAL OF TAX LAW 58

transaction can be judged only under the letter of the law, and to give regard to the underlying

substance of the transaction seems to involve substituting ―the uncertain and crooked cord of

discretion‖ for ―the golden and straight mete wand of the law‖. In other words, this principle,

often known as the Westminster principle, allows for individuals and corporations to

structure their financial arrangements in such a way as to attract minimum tax liability, so

long as the structure is within the four corners of the law.9

There was a significant change in approach after the Second World War when the

House of Lords began to emphasize on purposive interpretation in tax law. The Ramsay

principle, which was established by the House of Lords in WT Ramsay v. IRC10

is often seen

as ―the New approach‖ to anti-avoidance.11

This principle is seen in contradistinction to the

Westminster principle as it authorizes the court to ascertain the legal nature of the transaction

in order to determine tax liability in light of the nature and purpose of the statute. This

judgement emerged as an antidote to a preordained series of self-cancelling transactions with

no business purpose other than avoidance of tax, designed to give a single composite result.12

The House of Lords stood to ignore the individual steps for the purpose of tax, and decided to

ascertain the true legal effect of the series as a whole.13

This decision was followed

subsequently in Burmah Oil14

and Dawson.15

This trilogy of cases was interpreted by the Inland Revenue to give rise to a new

judicial doctrine superseding the Westminster Principle, which empowers the Revenue to

question every single transaction lacking business purpose, and which is entered into with the

motive of minimising a taxpayer‘s burden.16

This misconception has been finally laid to rest

in the later decisions of Craven v. White17

and Macniven18

where the two seemingly distinct

9 Prateek Andharia, Azadi no more?, LETS TALK ABOUT THE LAW, available at

http://letstalkaboutthelaw.wordpress.com/2011/09/25/azadi-no-more/#comments (12 June 2013, 10:15

AM).

10 W.T. Ramsay v. IRC, [1981] 54 TC 101 (hereinafter ‗Ramsay‘).

11 MURRAY & PROSSER, TAX AVOIDANCE, 11 (2012).

12 THURONYI VICTOR, COMPARATIVE TAX LAW, 176 (2003).

13 Id.

14 IRC v.Burmah Oil Co. Ltd., [1982] STC 30 (hereinafter ‗Burmah Oil‘).

15 Furniss v. Dawson, [1984] STC 153 (hereinafter ‗Dowson‘).

16 Barclays Mercantile Business Finance Limited v. Mawson (Her Majesty‘s Inspector of Taxes), [2004]

UKHL 51.

17 Craven v. White, [1988] 3 All ER 495.

18 Macniven v. Westmoreland Investments, [2001] 1 All ER 865.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 59

doctrines of Westminster and Ramsay were reconciled. These decisions emphasized that in

Ramsay, both, Lord Fraser and Lord Wilberforce, were careful to stress that they were not

departing from the Westminster principle. The Ramsay principle, it has been held, does not

make it a judicial function to strike down every step which is taken to mitigate the burden of

tax, and it is still open to a taxpayer to choose the most tax efficient alternative out of the

multiple alternatives available to him.19

Thus, the Ramsay principle has been reinterpreted as

a parallel rule of statutory construction, and not anew judicial doctrine.20

Now, the Indian judicial system has been experimenting with anti-avoidance for quite

some time, and has referred to the Westminster principle on numerous occasions. The Indian

equivalent of the Westminster case is Raman & Co.21

wherein Shah J. legitimized the use of a

device ―to divert the income before it accrues or arises‖ to a taxpayer, and recognized that

the effectiveness of such device ―depends not on considerations of morality, but on operation

of the Income tax Act.‖

Indian judiciary for the first time, although temporarily, announced its complete

intolerance to tax avoidance in the form of a separate opinion of Chinnappa Reddy, J in

Mcdowells.22

This opinion was only meant to supplement the majority judgment delivered by

Ranganath Misra, J. who had legitimized tax planning not involving ‗colourable devices‘,

‗dubious methods‘ and ‗subterfuges‘ under the guise of tax planning.23

Chinnappa Reddy, J.,

in his controversial separate opinion, placed a radical position of law stating therein that ―the

ghost of Westminster has been exorcised in England‖ in light of Ramsay,24

Burma Oil,25

and

Dawson,26

and that any transaction aimed at avoiding tax must be disregarded.27

Mcdowell led to a lot of litigation since the Revenue saw in the case more than that was

justified by treating every instance of tax saving as intended avoidance, susceptible to the

19 Supra note 17.

20 Judith Freedman, Converging Tracks? Recent Developments in Canadian and UK Approaches to Tax

Avoidance, 53 CANADIAN TAX JOURNAL (2005).

21 CIT v. Raman & Co., (1968) 67 ITR 11, 17 (SC).

22 Mcdowell and Co. Ltd. v. Commercial Tax Officer, (1985) 154 ITR 148 (SC) (hereinafter ‗Mcdowell‘).

23 Id.

24 Ramsay, supra note 10.

25 Burma Oil, supra note 14.

26 Dawson, supra note 15.

27 McDowell, supra note 22.

VOL. 1] INDIAN JOURNAL OF TAX LAW 60

Mcdowell‘s rule.28

Then the Supreme Court later emerged as the tax planner‘s messiah in

Azadi29

and diluted the evil initiated by Mcdowell. It carefully examined Ramsay, and relying

on Craven v. White30

and Macniven,31

negatived the erroneous decision of Justice Reddy,

upheld the Westminster principle as being ―alive and kicking‖ in the country of its birth, and

hence the law of the land in India too.

In the recently decided Vodafone case32

the apex court has held that there is no conflict

between Azadiand and Mcdowell, since Azadi upholds the majority decision in Mcdowell and

only departs from it to the extent of the separate opinion of Reddy, J.33

However, K.S.

Radhakrishnan, J., while reiterating the right of a taxpayer to arrange his affairs in the most

tax efficient manner, has also stated that it is equally important for a transaction to have a

business or commercial substance. Moreover, he also emphasized on the necessity of an

―effective legislative measure‖ with respect to tax-avoidance ―what is inequitable and

undesirable.‖34

Thus, to say that the Courts have been tolerant to tax avoidance, and that the

very introduction of a legislative GAAR topples the existing position of taxation law in India

is counterfactual.

Since the landmark judgement in Vodafone, there have been some landmark decisions

which have upheld the stance of the Judiciary on anti-avoidance, which has not been

undermined by the government‘s recent efforts to stretch the arms of taxation even beyond its

own jurisdiction in the name of tax avoidance. The Andhra Pradesh High Court upheld the

28 IYENGAR SAMPATH, LAW OF INCOME TAX, 232 (11th ed., 2011).

29 Union of India v. Azadi Bachao Andolan, (2003) 263 ITR 706 (SC) (hereinafter ‘Azadi‘).

30 Craven v. White, supra note 17.

31 Macniven v. Westmoreland Investments, supra note 18.

32 Vodafone International Holdings BV v. Union of India, (2012) 341 ITR 1 (SC) (hereinafter ‗Vodafone‘).

33 In the Majority Judgement in Mcdowell, RanganathMisra, J., held in para 45 that ―tax planning may be

legitimate provided it is within the framework of the Law.‖ In the latter part of that para, he stated that

―colourable devices cannot form a part of tax planning‖ and that it is the duty of every taxpayer to pay

taxes without any subterfuges. This para is to be read with ¶ 46 where he states that "on this aspect one of

us, Chinnappa Reddy, J. has proposed a separate opinion with which we agree". This is the statement in

the majority opinion which had created the confusion that the majority agreed with the Justice Reddy‘s

separate opinion in its entirety. However the phrase ―this aspect‖ expresses the majority‘s agreement

with the separate opinion only with respect to tax avoidance with the use of colourable devices and

subterfuges. The Separate opinion makes repeated references to this aspect. Although, he makes a number of observations with regard to the need to depart from the Westminster principle, these must be

read as only in the context of artificial tax avoidance. Such a reading of the Mcdowellcase removes any

perceived conflict between the Mcdowell and Azadi. See, per S.H. Kapadia, C.J., Vodafone, Id., ¶ 64.

34 Macniven v. Westmoreland Investments, supra note 18, at ¶55.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 61

arrangement in Sanofi35

as being tax legitimate and rejected the application of the

retrospectively amended section 9 of the Act on the basis that the same cannot override a tax

treaty.

India‘s judicial anti-avoidance rule is restricted to sham transactions or colourable

devices.36

Thus, in general, the principle of form over substance has prevailed in India, with

the courts occasionally examining the substance of a transaction to determine its true legal

effect. GAAR, however, is a codification of the substance over form doctrine, empowering

the department to ascertain not only the legal substance, but also commercial or economic

substance, consequently superseding the Supreme Court decisions in Azadi and Vodafone.

3. TREATY OVERRIDE

With the introduction of Chapter X-A in the Act, GAAR was given an apparent

overriding effect over the DTAAs of India with various other countries. This effect is sought

to be achieved by the insertion of sub-section 2A in Section 90 of the Act, which makes

GAAR applicable whether its provisions are beneficial to the assessee or not. The

qualification of the provision with a non-obstante clause clearly eliminates the interference of

sub-section (2) of S.90 with the applicability of the provisions of GAAR.37

This makes

GAAR paramount Law in terms of international transactions, notwithstanding the existence

of an international treaty governing that transaction.

3.1 INTERNATIONAL LAW ON TREATY OVERRIDE

35 Sanofi Pasteur Holding v. The Department of Revenue, (2013) 213 Taxman 504 (AP); In this case,

Institut Merieux (IM) and Groupe Industriel Marcel Dassault (GIMD), both French companies, held 80 per cent and 20 per cent shares, respectively, in ShanH SAS (ShanH), another French company. ShanH,

in turn, held shares in Indian company Shantha Biotechnics Ltd. (SBL). In August 2009, IM and GIMD

sold its shareholding in ShanH to another French company, Sanofi Aventis. The transaction was carried

out in France. The bone of contention was similar to that in the Vodafone case, where the Revenue

Authorities contended that the transaction was a tax avoidance transaction, and that in reality the

controlling interest in SBL was sold, and therefore it should be taxed in India. Moreover, the authorities

also contended that the transaction was hit by the retrospective amendment to S. 9 of the Income tax Act,

which overruled the Supreme Court judgment in the Vodafone Case.

36 Killick Nixon v. DCIT, ITA No. 5518/2012, decided on 06/03/2012. The Hon‘ble Bombay High Court

relied on the Vodafone case and observed that ―where a transaction is sham and not genuine as in the

present case then it cannot be considered to be a part of tax planning or legitimate avoidance of tax liability.‖

37 S. 90A of the Income Tax Act, 1961 incorporates the DTAAs into the domestic law, and subsection (2)

thereof provides for the application of the Act over the DTAAs to the extent to which it is more

beneficial to the assessee concerned.

VOL. 1] INDIAN JOURNAL OF TAX LAW 62

Article 26 of the Vienna Convention on the Law of Treaties codifies the accepted

International law principle of pacta sunt servanda and states that ―treaties are binding on the

parties to it and must be performed by them in good faith.‖ Article 27 of the Convention acts

as a corollary to this principle by prohibiting parties to a treaty from ―invoking the provisions

of its internal law as a justification for its failure to perform a treaty.‖ Thus the Convention

places reciprocal obligations on the parties to a treaty, and all such parties are under the same

obligation to perform a treaty in good faith.38

Although India is not a party to the Convention,

the abovementioned principles are binding on India as part of customary international Law.39

The Convention is a law-making treaty40

on all the international treaties entered into by

its parties.41

However, the principle of pacta sunt servanda is subject to certain limitations,

and an international treaty is often not considered unconditionally sacrosanct. The OECD

commentary recognizes two conflicting approaches followed by different states as regards

cases which result in abuse of treaty provisions. As per the first approach, certain States

consider the right of taxation as emanating solely from the domestic law, which is narrowed

by the application of DTAAs. Therefore, an abuse of the provisions of a treaty is in effect

considered an abuse of the provisions of domestic law. Thus, to the extent that domestic anti

abuse rules are a part of the domestic tax law for determining which facts result in a tax

liability, they are not addressed by the tax treaties and are therefore not affected by them.42

The other States consider some abuses as being abuses of the provisions of the treaty

themselves rather than abuse of domestic law, and view to combat them by a more rational

construction of the treaty itself, especially in terms of those transactions which aim to claim

38 Edwards-Ker, Michael, Tax Treaty Interpretation, Ph.D Thesis, QUEEN MARY AND WESTFIELD

COLLEGE, UNIVERSITY OF LONDON (1994).

39 Vellore Citizens Welfare Forum v. Union of India, (1996) 5 SCC 647.

40 A law-making treaty is one which establishes general patterns of behaviour for the parties over a certain

period of time in certain areas. See, M. FITZMAURICE & A. QUAST, LAW OF TREATIES, Study Guide,

(UNIVERSITY OF LONDON, 2007), http://www.londoninternational.ac.uk/sites/default/files/law_treaties.pdf

(03 June 03 2014, 06.00 PM).

41 Interpretation of Human Rights Treaties, ICELANDIC HUMAN RIGHTS CENTRE

http://www.humanrights.is/en/human-rights-education-project/human-rights-concepts-ideas-and-

fora/part-i-the-concept-of-human-rights/interpretation-of-human-rights-treaties, (09 June 2014, 06:42

PM); European Court of Human Rights in Wemhoff v. Federal Republic of Germany, 2122/64 [1964]

ECHR 4, the court has noted that because the Convention is a ‗law-making treaty, it is [...] necessary to

seek the interpretation that is most appropriate in order to realise the aim and achieve the object of the treaty‘.

42 OECD (2012), Model Tax Convention on Income and on Capital 2010 (updated 2010), Commentary on

Article 1 concerning the persons covered by the convention, ¶ 9.2, OECD PUBLISHING available at

http://dx.doi.org/10.1787/978926417517-en (09 June 2014, 07:00 PM).

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 63

benefits which a treaty does not intend to confer. This approach attempts to uphold the

principle of good faith in respect of interpretation of treaties, as enshrined in Article 26 of the

Vienna Convention.43

Both these approaches nonetheless recognize the rights of States to

prevent the conferment of benefits under a treaty when arrangements constituting an abuse of

treaties have been entered into.44

3.2 LEGAL POSITION IN INDIA

The issue can be narrowed down to the legal position in India regarding interface

between an international treaty and a subsequent legislative enactment.45

Although this issue

has not been directly dealt by the Constitution, a harmonious reading of some of the

constitutional provisions can be a helpful guide in determining the same. The Indian

Constitution directs the State to endeavour to foster respect for international law and treaty

obligations.46

From a combined reading of Article 246 of the Constitution along with the

relevant entries in List I of the 7th Schedule, particularly entries 13 and 14, it can be

concluded that treaty making power is primarily a parliamentary function. In addition, the

Parliament is also authorized to ―make any law for the whole or any part of India for

implementing any treaty with any country or countries or any decision made in any

international conference, association, or other bodies.‖47

This power is not fettered by the

legislative competence of the states under Lists II and III of the 7th Schedule, and has an

overriding effect over the same.

The Executive power under the Constitution extends to matters in respect of which the

Parliament is empowered to make laws, in the absence of a parliamentary legislation and

subject to constitutional limitations.48

Thus, it is only in the absence of such Parliamentary

legislation regarding procedure for entering into treaties that it is left upon the Executive to

43 Id., ¶ 9.3.

44 Id., ¶ 9.4.

45 Amit M. Sachdeva, Can the Proposed Tax Code Override Indian Tax Treaties?, TAX NOTES

INTERNATIONAL, available at

http://www.vaishlaw.com/article/Indian%20DTC%20and%20Tax%20Treaties-Amit%20Sachdeva.pdf (14 June 2013, 06:40 PM).

46 The Constitution of India, 1950, Article 51.

47 Id., Article 253.

48 Id., Article 73.

VOL. 1] INDIAN JOURNAL OF TAX LAW 64

do the same.49

The bottom line however remains that so far as implementation of

international treaties is concerned, the constitutional mandate is clear that it is only the

Parliament which has exclusive power to make laws for implementation of treaties and

international agreements.50

As stated above, that unlike other jurisdictions, the treaty making power under the

Indian Constitution is not conferred on the executive, but is placed squarely within the

domain of the Parliament.51

Articles 246(1)52

and 253 are merely enabling provisions, and do

not place an obligation on the Parliament to implement treaties through enactment.53

The

Parliament being so empowered is equally competent to choose not to legislate in order to

give effect to such treaty. The scheme of international taxation in India is such that all the

DTAAs are entered into by India under S.90 of the Act. Thus they are essentially delegated

legislation.54

They are considered to be mini legislations containing in them all the relevant

aspects or features which are at variance with the general taxation laws of the respective

countries.55

They hold an important position in the scheme of Indian income-tax legislation,

inasmuch as they lay down an alternate scheme of taxation.56

In ABN Amro Bank N V v.

JCIT,57

the Tribunal observed that in case of any conflict between a tax treaty and a domestic

law, the former must yield to the law passed independently by the parliament. This decision

is based on the principle laid down by the Supreme Court in the case of Gramophone

49 Treaty Making Power under Our Constitution, NATIONAL COMMISSION TO REVIEW THE WORKING OF

THE CONSTITUTION, (January 8, 2001) available at http://lawmin.nic.in/ncrwc/finalreport/v2b2-3.htm.

(25 June 2014, 05.00 PM).

50 BIMAL N. PATEL, II INDIA AND INTERNATIONAL LAW, 17 (2008).

51 ―If the national executive, the government of the day, decide to incur the obligations of a treaty which involve alteration of law, they have to run the risk of obtaining the assent of Parliament to the necessary

statute or statutes.‖ See, Per Lord Atkin, Attorney General for Canada v. Attorney General of Ontario,

[1937] AC 326, 347. Also see, Gujarat v. VoraFiddali, AIR 1964 SC 1043, where the Supreme Court

held that in India Treaties occupy the same status, and adopt the same treaty practice as in United

Kingdom; Shiva Kant Jha, Treaty Making Power: The Context, SHIVAKANTJHA.ORG,

http://www.shivakantjha.org/openfile.php?filename=articles/3_treaty-making.htm#_ftn4 (06 July 2013,

3:33 PM).

52 Read with entries 13 and 14 of List I, The Constitution of India, 1950, supra note 46.

53 Id., Article 253 reads ―Parliament has power to make any law...for implementing any treaty‖, and does

not read as ―Parliament shall make a law...‖

54 Azadi, supra note 29.

55 DCIT v. Boston Consulting Group Pvt. Ltd., (2005) 93 TTJ 293 (Mum).

56 Kotak Mahindra Primus Ltd. v. DDIT, (2006) 105 TTJ 293 (Mum); Western Union Financial Services

Inc.v. ADIT, (2006) 101 TTJ 56 (Del).

57 ABN Amro Bank N V v. JCIT, (2005) 96 TTJ 1041(Kol).

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 65

Company58

that in the event of a conflict between a municipal law and an international law,

―the sovereignty and integrity of the Republic and the supremacy of the constituted

Legislature in making the laws may not be subjected to external rules….‖ However, there are

few decisions in India which deal with the issue of tax treaty override in light of S. 90 of the

Act. The Apex Court in Azadi59

ventured into this sphere to some extent but the conclusion of

the Court is of little significance in the context of GAAR because the court declared the

overriding effect of a treaty over the provisions of the Act where a notification regarding

implementation of a treaty is issued pursuant to S. 90 of the Act. This is hardly the issue in

question today. Moreover, the Court has quoted the findings of a Report60

with respect to

anti-abuse provisions to be incorporated either in the treaty or in the domestic legislation, but

has refused to opine on the same. However, the Court in Vodafone61

has recognized that lack

of clarity and appropriate provisions in the statute or treaty regarding circumstances when

Judicial Anti-Avoidance Rule would apply has generated litigation in India,62

thus

recognizing the importance of a statutory law on the same.

Since all the DTAAs are in the form of delegated legislation under S. 90 of the Act,

under the scheme of Indian taxation law and Constitutional Law, there seems to be no

restriction on the power of the Parliament to legislate in a manner so as to override a treaty,

just as the Parliament can amend or overturn an earlier enacted law.63

4. GRANDFATHERING OF INVESTMENTS

The Finance Bill, 2012 brought in an environment of uncertainty and fear among

investors who were cynical about the lack of protection to existing structures and

arrangements. This resulted in a major withdrawal of investments from the economy and loss

of confidence in the Government as such a major change in tax law was undertaken without

58 Gramophone company of India Ltd. v. Birendra Bahadur Pandey, AIR 1984 SC 667.

59 Azadi, supra note 29.

60 Report of Working Group on Non Resident Taxation, MINISTRY OF FINANCE AND COMPANY AFFAIRS,

GOVERNMENT OF INDIA (January 2003), available at http://finmin.nic.in/reports/NonResTax.pdf. (25

June 2014, 05.00 PM).

61 Vodafone, supra note 32.

62 Id., per Kapadia, C.J., ¶ 68.

63 Sohrab E. Dastur (Senior Advocate), Principles of Interpretation of issues in Double Taxation Avoidance

Treaties,TAXATION, http://itaxation.wordpress.com/2008/08/31/principles-of-interpretation-of-issues-in-

double-taxation-avoidance-treaties/, (02 June 2013, 4:10 PM).

VOL. 1] INDIAN JOURNAL OF TAX LAW 66

any consultation from investors.64

Moreover, the legitimate expectations of the investors were

denied as they had set up their structures and planned investments under the umbrella of

Azadi65

as the law of the land. The newly introduced GAAR, over and above giving

unconditional power to the department, also seemed to target these investors who believed

the department to be capable of sending Show Cause Notices under the law even for existing

structures in the absence of any grandfathering clause.66

The Parliamentary Standing Committee on Finance, with respect to the Direct Taxes

Code Bill, 2010 (hereinafter ‗DTC Bill‘), had recommended the grandfathering of all existing

structures against application of GAAR provisions contained therein.67

The Shome

Committee report68

which was prepared to give recommendations to the Finance Ministry

after consulting various investors corrected the same as this ―would allow an impermissible

arrangement to exist in perpetuity if created before commencement of GAAR and

grandfathered under GAAR provisions.‖69

In addition, it gave an example similar to the

instant case where if the recommendations of the Standing Committee70

are to be followed,

then a conduit company incorporated in a favourable jurisdiction in 2008 will enjoy tax

exemption indefinitely for all the future investments made by it.71

Thus, it was recommended

that ―investments (though not arrangements)‖ should be grandfathered.72

This

recommendation sought to extend the grandfathering provision to the date of applicability of

GAAR.

64 Since the announcement of Budget 2012 on March 16 (2012), net FII inflows have slowed dramatically,

showing an effective daily average drop of 95% since March 16. See, Nicolas De Boursac, FIIs will quit

Indian markets if swords of GAAR, indirect transfer rules hang over their heads, THE ECONOMIC TIMES,

(May 6, 2012) http://articles.economictimes.indiatimes.com/2012-05-06/news/31588238_1_net-fii-

inflows-gaar-global-funds, (10 July 2013, 06:53 PM).

65 Azadi, supra note 29.

66 A grandfathering clause is a provision which states that the old law will continue to apply in some

existing situations, whereas the new law will apply to all future cases.

67 49TH REPORT OF STANDING COMMITTEE ON FINANCE (2011-12), MINISTRY OF FINANCE (DEPARTMENT OF

REVENUE), The Direct taxes Code Bill, 2010 (hereinafter ‗STANDING COMMITTEE‘).

68 EXPERT COMMITTEE 2012, Report on General Anti-Avoidance Rules (GAAR) in Income Tax act, 1961,

(September 2012) (hereinafter ‗SHOME‘).

69 Id., at 40.

70 STANDING COMMITTEE, supra note 68.

71 SHOME, supra note 68, at 40.

72 Id., at 41.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 67

The press release73

issued by the Finance Ministry later in the financial year accepted

the major recommendations, but only partially accepted the recommendation with respect to

grandfathering of investments. Although investments were grandfathered, the exemption was

provided only to those undertaken before the date of August 30, 2010, which was the date on

which the DTC Bill was tabled in the Lok Sabha. Thus, though the relief of deferment of

GAAR to April 1, 2016 was provided to the investors, investments made after August 2010

and before April 2016 were left totally unprotected. The press release has been crystallized in

the form of the recently notified GAAR Rules.74

The authors are of the view that the restriction of relief of grandfathering only to

investments made before a date in the past (August 30, 2010) selected on arbitrary

considerations (hereinafter ‗limited grandfathering‘) smacks of an intention of the

Government to keep the ambit of GAAR as wide as possible.

There are two major reservations which the authors have regarding the reasonability of

the limited grandfathering as introduced through the GAAR Rules.

a) Whether the limited grandfathering in the GAAR Rules can be challenged as

unconstitutional?

There is no doubt about the fact that GAAR shall be applied prospectively as regards

income and is not intended to target income received or accrued before its date of

enforcement.75

However, the limited grandfathering of investments only till August 2010

may trigger challenge on grounds of retrospectivity.

A retrospective law has been defined by the Supreme Court, using the definition given

in ‗Words and Phrases, Permanent Edition, Volume 37A‘ as ―one which takes away or

impairs vested or accrued rights acquired under existing laws, or creates a new obligation,

imposes a new duty, or attaches a new disability, in respect of transactions or considerations

already past.‖76

The investors, who have undertaken investments, have done so in light of the

73 Supra note 4.

74 Supra note 1.

75 Speech of Finance Minister whilst moving amendments to Finance Bill, 2012, May 7, 2012; Draft

guidelines regarding implementation of General Anti Avoidance Rules (GAAR) in terms of §101 of the

Income Tax Act, 1961; SHOME, supra note 69; Explanatory memorandum to Finance Bill, 2013.

76 Virender Singh Hooda and Ors. v. State of Haryana and Anr., AIR 2005 SC 137.

VOL. 1] INDIAN JOURNAL OF TAX LAW 68

conclusive position of law as declared by the Supreme Court in Azadi77

as regards the

precedence of form over substance. This position has been followed in effect in subsequent

cases including the recent decision of Dynamic India Fund I.78

This decision has also been

approved by the Supreme Court in the recent landmark judgement of Vodafone BV.79

With

the law so clearly in place, they have acquired a vested right under it, and imposing GAAR

on these investments ―imposes a new duty, or attaches a new disability, in respect to

transactions or considerations already past.‖80

Therefore, it may be argued that such an

application of GAAR makes it a retrospective law under the aforementioned definition.

It is a cardinal principle of construction that every statute is considered to be prima

facie prospective, unless it is made to have retrospective application either expressly or by

necessary implication.81

As explained above, GAAR has been given a retrospective effect

through the Income Tax Rules. However, it is a well settled principle of Administrative Law

that a retrospective law can even be introduced through a delegated legislation, if the parent

statute so authorizes.82

An administrative body has power to give retrospective effect to a rule

only to the extent to which the parent statute so permits it. The Supreme Court in Yadav83

has

held in addition to the above, that the rule making authority must show that there was

sufficient, reasonable and rational justification to apply the rules retrospectively.

The Income-Tax Rules are made by the Central Board of Direct Taxes (―CBDT‖) under

Section 295 of the Act. Sub-section (4) of this section expressly authorizes the CBDT to give

retrospective effect to the rules. However, retrospective effect cannot be so given if it

prejudicially affects the interests of the assesse, unless the contrary is permitted by the section

of the statute for the purpose of which the rule is made.84

Whether the limited grandfathering

provision prejudicially affects the interests of the assessee or not is again a moot point. If the

rule is challenged on the ground of retrospectivity in light of the limited grandfathering

77 Azadi, supra note 29.

78 In re, Dynamic India Fund I, AAR No. 1016/2010.

79 Vodafone, supra note 32.

80 Supra note 76.

81 Zile Singh v. State of Haryana, (2004) 8 SCC 1; Keshvan v. State of Bombay, AIR 1951 SC 124; Gem

Granites v. Commr.of Income Tax, (2005) 1 SCC 171.

82 The State of Madhya Pradesh v. Tikamadas, AIR 1975 SC 1429; Income Tax Officer, Alleppey v. M.C.

Ponnoose, AIR 1970 SC 385.

83 B.S. Yadav and Ors. v. State of Haryana, AIR 1981 SC 561.

84 Union of India v. Dr. S. Krishna Murthy, (1989) 4 SCC 689.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 69

provision, then the court may look it from two angles. It may be argued that the GAAR as

originally introduced does not impliedly grandfather past investments, and therefore a

grandfathering provision, even if limited, provides a relief to the assessees, and is in fact not

prejudicial to their interests. On the other hand it may even be argued that the GAAR has an

implied grandfathering, and a limited grandfathering provision introduced through the rules

limits the relief to the investors, and attempts to apply GAAR to past investments. To this

extent the rule may be struck down for being prejudicial to the interests of the assessees since

chapter X-A does not permit (either expressly or impliedly) making of a retrospective rule for

its purpose. Moreover, even if so authorized, the board has to give a reasonable and rational

justification to such retrospective application of GAAR provisions in light of the Yadav

ruling.

Assuming that the board has an implied authority to apply GAAR retrospectively (in

terms of investments and not income), then the constitutional validity of the limited

grandfathering needs to be determined. It has been upheld on several occasions that a

retrospective law legitimately passed cannot be challenged except on the grounds of violation

of fundamental rights.85

The authors are of the opinion that if GAAR is applied to all past

investments after the date of August 30, 2010, even if through an express law validly passed,

it is open to challenge on the ground of violation of Article 14 and 19 (1) (g) of the

Constitution.

Article 14 permits the Legislature (including the delegate) to make reasonable

classification of persons, objects and transactions for the purpose of achieving specific ends.86

However, such a classification must be founded on an intelligible differentia and this

differentia must have a rational relation to the object sought to be achieved by the statute.87

Also, it is a well- established Constitutional law principle, recognized by the Supreme Court,

85 State of Gujarat and Anr. v. Raman Lal Keshav Lal Soni, AIR 1984 SC 161; This follows from the

general constitutional mandate that no law, whether prospective or retrospective, can be made which

contravenes fundamental rights; The Constitution of India, Article 13, supra note 47.

86 Western U.P. Electric Power and supply Co. Ltd. v. State of Uttar Pradesh, AIR 1970 SC 21; R.K. Garg v. Union of India, AIR 1981 SC 2138.

87 State of West Bengal v. Anwar Ali Sarkar, AIR 1952 SC 75; Budhan v. State of Bihar, AIR 1955 SC

191; Harakchand v. Union of India, AIR 1970 SC 1453; State of Bombay v. F.N. Balsara, AIR 1951 SC

318.

VOL. 1] INDIAN JOURNAL OF TAX LAW 70

that Article 14 is violated not only when equals are treated unlike, but also when unequals are

treated alike, i.e., if there is similar treatment of groups situated in dissimilar circumstances.88

The limited grandfathering provision satisfies both sides of the aforementioned

inequalities. Firstly, it treats the similarly placed investments before and after the date of

August 30, 2010 differently by imposing retrospective burden on the latter while exempting

the former. The basis of classification is that since the DTC Bill was tabled on August 30,

2010, investors undertaking investments after this date are aware of the possibility of GAAR

provisions contained therein to have effect in the near future. However, the tabling of a bill is

just the first step in the process of enactment. The fact that the DTC Bill has not yet been

enacted further goes against the government‘s reasoning. Therefore the classification of

investments on the basis of their timing with respect to such arbitrary date does not qualify as

―intelligible differentia‖ having a ―rational nexus with the object sought to be achieved‖.

Secondly, the limited grandfathering provision also affords similar treatment to investments

made before and after the date of applicability of GAAR, consequently treating unequals

equally. Thus, it is argued that the provision violates every facet of equality guaranteed under

Article 14.

Article 19(1)(g), in granting the right to practice any profession, or to carry on any

occupation, trade or business, carries with it a further safeguard against imposition of an

unreasonable tax burden.89

In determining whether the retrospectivity of a law is so arbitrary

and burdensome as to violate Article 19(1)(g),90

the criteria declared by the Supreme Court

include the period of retrospectivity and the degree of any unforeseen financial burden

imposed for the past period.91

The investors having acquired a vested right to invest, in light

88 Chiranjit Lal v. Union of India, AIR 1951 SC 41; Om Narain v. Nagar Palika, Shahjahanpur, (1993) 2

SCC 242.

89 Prateek Andharia, The Validity of Retrospective Amendments to the Income Tax Act: Section 9 of the Act

and the Ishikwajma Harima Case, 4 NUJS L.REV. 269 (2011).

90 The Constitution of India, supra note 47; the freedoms under Article 19 are available only to ―citizens‖.

Since many of the investors affected by GAAR will be corporations, their locus standi for a challenge

under Article 19 is questionable, i.e., even if the corporation is Indian in every sense, e.g., it is registered

in India, has Indian capital and all of its shareholders and directors are Indian, it can claim no right under

Art. 19; State Trading Corporation of India v. The Commercial Tax Officer, AIR 1963 SC 1811; Tata

Engineering v. State of Bihar, AIR 1965 SC 40. However, in the course of time, the rigours of the above

pronouncements have been diluted by resorting to the strategy of joining a natural person along with a

company in the writ petition challenging violation of Art. 19(1)(g). See, M.P. JAIN, INDIAN

CONSTITUTIONAL LAW, 801 (5th ed., 2008); Sakal Papers v. Union of India, AIR 1962 SC 305; R.C.

Cooper v. Union of India, AIR 1970 SC 564; Bennett Coleman & Co. v. Union of India, AIR 1973 SC

106.

91 Ujagar Prints v. Union of India, (1989) 3 SCC 488.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 71

of various judgements of the Supreme Court as discussed above, the retrospective burden of

scrutiny for the purposes of GAAR under Section 144BA of the Act will be imposed on

them. This burden is completely unforeseen as the DTC Bill tabled in the Lok Sabha on

August 30, 2010 is far from a conclusive Law capable of directing the investors on their

proposed investments. An unforeseen retrospective burden of taxation denies the taxpayer the

rightful opportunity of carrying out cost-benefit analysis of the proposed transaction and to

decide whether or not to enter into such a transaction.92

b) The protection of grandfathering should have been afforded not only to the

transfer of existing investments, but also to returns accruing or arising from

these investments.

The Shome Committee report has recommended the grandfathering of investments to

cover exit of such investments even after the date of commencement of GAAR (the date of

grandfathering being the same as the date of commencement of GAAR).93

This is because

most of the foreign investment in India being made from Mauritius and Singapore, the same

is made on the condition of availing of treaty benefits, which include non-taxation of capital

gains in India on exit or sale of such investments.94

This scope of grandfathering has been

accepted and followed in the GAAR Rules which limits the protection of grandfathering only

to the transfer of investments. Thus, the tax benefit on sale of grandfathered investments even

after the date of commencement of GAAR would not attract the provisions of GAAR.

In the opinion of the authors, the grandfathering provision must be broad enough even

to cover returns from investments such as dividends, interests etc. Thus, in light of the limited

grandfathering provision, if an investment made before August 30, 2010 is grandfathered,

and if such investment otherwise qualifies as an impermissible avoidance arrangement, then

the consequences of GAAR should not apply to the returns accruing or arising from such

investments even after this date.

92 Pradip R. Shah, Retrospective Amendments – High-time for Introspection by India, CA CLUB INDIA,

(April 1, 2010) http://www.caclubindia.com/articles/retrospective-amendments-hightimefor-

introspection-by-india-5144.asp (07 May 2014, 4:35 PM).

93 SHOME, supra note 68, at 41.

94 Id., at 40.

VOL. 1] INDIAN JOURNAL OF TAX LAW 72

5. GAAR AND ITS COUNTER PRODUCTIVITY TO FOREIGN

INVESTMENTS

5.1 TAX AS A VARIABLE OF FOREIGN INVESTMENT

―India needs investment for employment generation and advancement of its economy

and everyone needs to keep that in mind.‖95

The ex-chief justice of India implanted the

comment, aftermath of Vodafone96

judgement, with the intention of reminding the

government‘s rough neck policies of tax collection which were driving away the foreign

investments from the country. The ex-chief justice, from his own personal experience,

reiterated the importance of a sensible tax strategy to attract foreign investors. Globalisation

is a fact which cannot go unnoticed. Globalisation and taxation are two faces of the same

coin. Modern International taxation practice also views taxation as a means for directing and

regulating the flow of investments.97

In this era, scope of taxation is a factor which makes or

breaks the foreign investment in any country. ―A country which is as yet developing, both in

its global economic confidence and in its taxation regime, needs the encouragement and

support of its contemporaries.‖98

Justice Swatanter Kumar, a party to the Vodafone judgment,

reinstituted the need of framing the law and policies in consonance with the current economic

scenario of the country. Another significant concern pointed out by the Hon‘ble judge was

the administration of tax laws in a complex and unfriendly manner. He prioritized the need

from simplification of tax laws to simplified and friendly administration of tax laws.

The policy makers introducing or revising its FDI Policy may rely on one or more

economic models or frameworks to examine the possible channel of influence. The Policy

Framework for investment99

primarily focuses on developing and transition economies. Tax,

one of the issues influencing FDI, has to be studied keeping in mind various factors which

may affect FDI in such countries. In setting the tax burden on inbound investment, policy

95 Spare Vodafone – Save Thousands of Job: Ex Chief Justice Kapadia, (May 17, 2013), available at

http://www.itatonline.org/articles_new/index.php/spare-vodafone-save-thousands-of-jobs-ex-chief-

justice-kapadia/ (27 July 2014, 01:13 PM).

96 Vodafone, supra note 32.

97 Justice Swatanter Kumar, Complex Tax Laws & Hostile Tax Dept Are Responsible For Tax Avoidance,

(January 26, 2013) available at http://www.itatonline.org/articles_new/index.php/complex-tax-laws-hostile-tax-dept-are-responsible-for-tax-avoidance/ (27 July 2014, 1:07 PM).

98 Id.

99 OECD (2007), Tax Effects on Foreign Direct Investments- No.17, OECD PUBLISHING available at

http://www.oecd.org/tax/tax-policy/39866155.pdf (05 July 2014, 4:15 PM).

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 73

makers are encouraged to assess whether their host country offers attractive risk/return

opportunities, taking into account framework conditions, (e.g. political/monetary/fiscal

stability; legal protection; public governance) market characteristics and the prevalence of

location-specific profits.100

The authors are of the view that the impediment created by the tax

authorities/governments by imposing taxes with discretionary powers and uncertainty, deter

the foreign investors to make the location specific decision in favour of the host countries.101

Therefore, this issue can be mooted on two facets i.e. first on the scheme of discretionary

power and second on the scheme of legal uncertainty.102

On the point of discretionary power, it can be contended that the present structure of

statutory GAAR, introduced by the government, overlay a gigantic scope of exercising

discretion at the lowest level by the Assessing Officer. Difficulty to administer discretionary

regime results in delays and uncertainty for investors. This can even increase the overall cost

of making an investment in some countries.103

If the overall cost of the investment will

increase, then why would an investor look forward to such investment?

On the question of legal uncertainty, ―legal certainty‖ would imply dynamic and

efficient substantive laws clearly stating the rights, obligations, and liabilities of all business

parties, rule-based business transactions, and procedural law providing prompt and

inexpensive means to the courts, an institutional framework that supports business

development and sustainability, strict adherence to the principles of ‗rule of law‘ and

‗supremacy of the law‘, and an efficient and independent judiciary. Legal uncertainty on the

other hands always occurs when individual actors are uncertain of the effects of the

100 Id.

101 ―The sudden and unprecedented move in the [Budgetary] bill has undermined confidence in the policies

of the government of India toward foreign investment and taxation and has called into question the very

rule of law.‖ Rahul Bedi, George Osborne says Indian tax plans could harm investment, THE

TELEGRAPH, (April 2, 2012), available at

http://www.telegraph.co.uk/finance/newsbysector/industry/9179558/George-Osborne-says-Indian-tax-

plans-could-harm-investment.html (07 July 2014, 7:30 PM).

102 The tax uncertainty now anticipated creates significant risk that these global funds will choose to avoid

the Indian capital markets altogether and redirect their resources to other opportunities. Nicholas de

Boursac, FIIs will quit Indian markets if swords of GAAR, indirect transfer rules hang over their heads,

THE ECONOMIC TIMES, (May 6, 2012) available at http://articles.economictimes.indiatimes.com/2012-05-06/news/31588238_1_net-fii-inflows-gaar-global-funds (07 July 2014, 7:50 PM).

103 Jacques Morisset & Neda Pirnia, How Tax Policy and Incentives affect the Foreign Direct Investment: A

Review, THE WORLD BANK AND INTERNATIONAL FINANCE CORPORATION FOREIGN INVESTMENT

ADVISORY SERVICE, Policy Research Working Paper No. 2509, 22, (December 2000).

VOL. 1] INDIAN JOURNAL OF TAX LAW 74

provisions of the dominant legal system on the results of their actions.104

The objective legal

uncertainty, which does not form a reliable and sure basis for decisions, always affects the

investment decisions. This uncertainty can be best explained with an example mentioned in

the first section of this paper wherein the uncertainty is created by the standard laid down for

driving speed. If there is a legal uncertainty in the minds of the investors for decision making,

then how would a foreign investor make such an investment? The foreign investors will be

more deterred, as the cost of international legal disputes is much greater than domestic

disputes.105

Therefore the discretionary power entrusted in Chapter X-A in favour of tax authorities

and uncertainty looming in the minds of foreign investors, will result in loss of foreign

investor‘s confidence in the economy and tax structure.106

This loss may defeat the purpose

of revising the FDI Policy. Moreover, cases like Vodafone give a reason to foreign investors

to ponder over their investment decisions.107

The controversy over introduction of GAAR has haunted not only the foreign investors

but also raised concerns in the minds of countries from where the investments are brought in

India. Mauritius, top investing country through FDI with 38%,108

is also concerned over the

effects of Indian GAAR on their role as a preferred investment route to India.109

Not only

Mauritius, this concern is raised from every corner of the world to maintain the balance

between the reform measures in the form of FDI and introduction of GAAR.110

The

104 Martin Zaglar & Cristiana Zanzottera, Corporate Income Taxation Uncertainty and Foreign Direct

Investment, WU International Taxation Research Paper Series No. 2012-07, 3, (2012).

105 Hanno von Freyhold, Volkmar Gessner, Enzo L. Vial & Helmut Wagner, Cost of Judicial Barriers for Consumers in the single Market, A REPORT FOR THE EUROPEAN COMMISSION, BRUSSELS, 117, (Oct.-

Nov.,1995).

106 Supra note 101.

107 Investors into India rely on good governance, a predictable regulatory regime and a hassle-free, rules-

based business environment because they are making major long-term commitments, large sums of

money, long gestation and long operation periods, needing as much predictability and consistency as

possible. See, Singapore PM Lee Hsien Loong says business environment in India 'complicated', THE

INDIAN EXPRESS, (July 11, 2012).

108 Fact Sheet on Foreign Direct Investment From April, 2000 to April, 2013, (April, 2013)

http://dipp.nic.in/English/Publications/FDI_Statistics/2013/india_FDI_April2013.pdf (20 June 2014,

06.00 PM).

109 Mauritius is looking to balance India‘s concerns over misuse of a tax treaty between the two countries,

with its desire to remain a preferred investment route into India, according to a Mauritius delegation

comprising officials from the investment promotion board and financial sector regulators. See, Remya

Nair, Mauritius to address India‘s concerns over tax treaty, THE ECONOMIC TIMES, 9 (July 11, 2013).

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 75

government unleashed huge FDI reforms in order to attract foreign investments in the country

in light of the harsh economic environment;111

but how far these reforms will prove to be

adequate enough to regain the investor‘s confidence, keeping in mind the upcoming GAAR

in two years, is still a pending question to be answered.

It is an economic reality, as mentioned in detail above, that FDI flows towards a

location with a strong governance infrastructure which includes enactment of laws and a

well-oiled legal system. Certainty is integral to rule of law. Certainty and stability form the

basic foundation of any fiscal system. Certainty in tax policy is crucial for taxpayers

(including foreign investors) to make rational economic choices in the most efficient manner.

In the opinion of the authors, it is for the government of the day to have certainty

incorporated in the Treaties and in the laws so as to avoid conflicting views. Investors should

know where they stand. It also helps the tax administration in enforcing the provisions of the

taxing laws. This would serve the purpose of having an anti-avoidance rule as well as the

investors will not lose confidence in the economy.

5.2 GOVERNMENT EFFORTS TO ATTRACT FOREIGN INVESTMENT

Foreign Direct Investment (―FDI‖) is an investment involving a long term relationship

and reflecting a lasting interest and control of a resident entity in one economy in an

enterprise resident in an economy other than that of the foreign direct investors.112

The initiation of new economic policy in 1991 is remarked as the stepping stone of

Indian foreign investment regime. The removal of restrictive and regulated trade practices, by

the policymakers, was welcomed by the foreign investors then. Subsequently, with the

process of reforms, India has witnessed a change in the flow of FDI in the country. The

whole reform process has turned the investors‘ faces towards India making it a preferred

investment destination.113

110 With the introduction of General Anti-Avoidance Rules (GAAR) which were intended to plug taxation

loopholes and the announcement on retrospective amendments to income tax law have affected business

sentiments and investors‘ confidence globally. See, Follow Obama order on FDI, reforms: CII, THE

INDIAN EXPRESS, (17 July, 2013).

111 To lure foreign money, boost growth, India eases FDI curbs, THE HINDUSTAN TIMES, (17 July, 2013).

112 UN Conference on Trade and Development, World Investment Report, Foreign Direct Investment and

the Challenge of Development, (1999).

113 Id.

VOL. 1] INDIAN JOURNAL OF TAX LAW 76

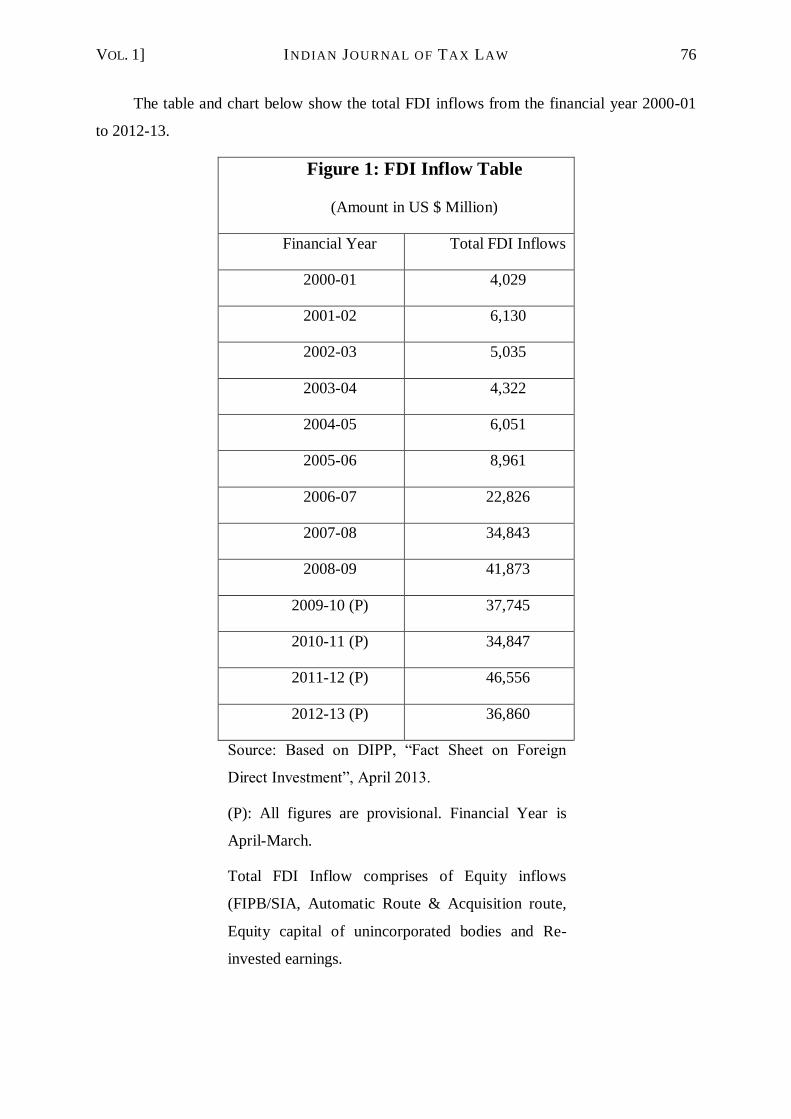

The table and chart below show the total FDI inflows from the financial year 2000-01

to 2012-13.

Figure 1: FDI Inflow Table

(Amount in US $ Million)

Financial Year Total FDI Inflows

2000-01 4,029

2001-02 6,130

2002-03 5,035

2003-04 4,322

2004-05 6,051

2005-06 8,961

2006-07 22,826

2007-08 34,843

2008-09 41,873

2009-10 (P) 37,745

2010-11 (P) 34,847

2011-12 (P) 46,556

2012-13 (P) 36,860

Source: Based on DIPP, ―Fact Sheet on Foreign

Direct Investment‖, April 2013.

(P): All figures are provisional. Financial Year is

April-March.

Total FDI Inflow comprises of Equity inflows

(FIPB/SIA, Automatic Route & Acquisition route,

Equity capital of unincorporated bodies and Re-

invested earnings.

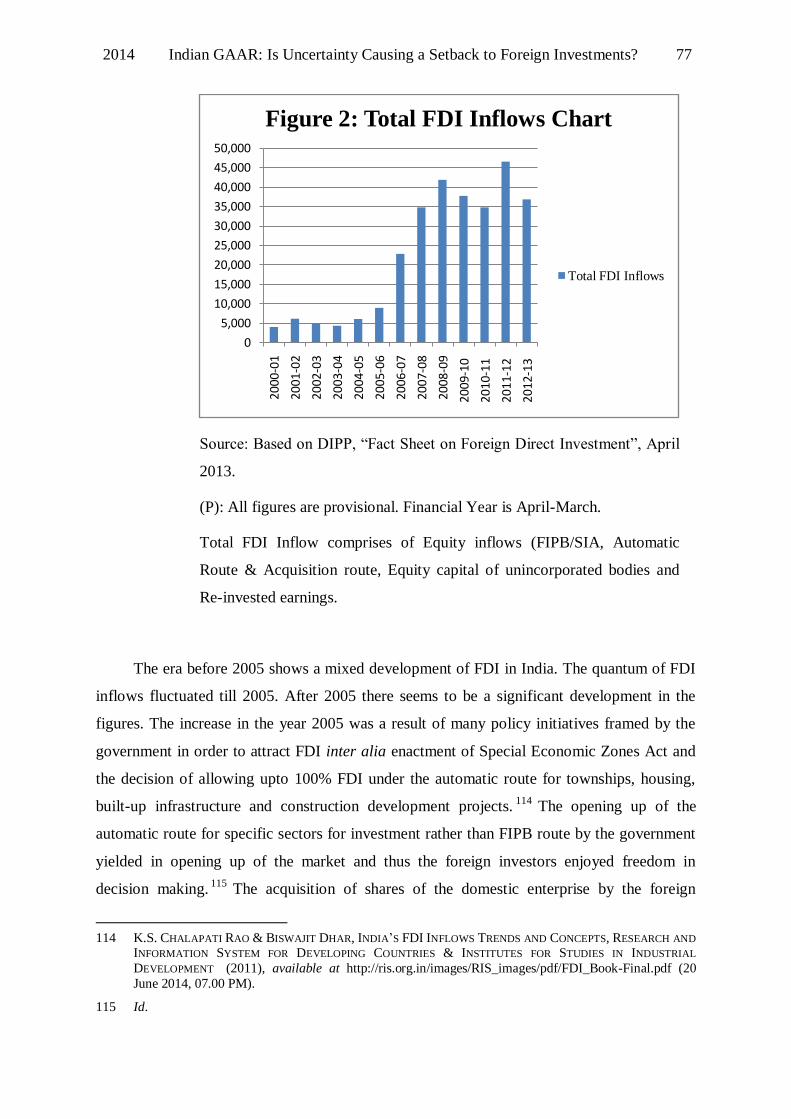

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 77

Source: Based on DIPP, ―Fact Sheet on Foreign Direct Investment‖, April

2013.

(P): All figures are provisional. Financial Year is April-March.

Total FDI Inflow comprises of Equity inflows (FIPB/SIA, Automatic

Route & Acquisition route, Equity capital of unincorporated bodies and

Re-invested earnings.

The era before 2005 shows a mixed development of FDI in India. The quantum of FDI

inflows fluctuated till 2005. After 2005 there seems to be a significant development in the

figures. The increase in the year 2005 was a result of many policy initiatives framed by the

government in order to attract FDI inter alia enactment of Special Economic Zones Act and

the decision of allowing upto 100% FDI under the automatic route for townships, housing,

built-up infrastructure and construction development projects.114

The opening up of the

automatic route for specific sectors for investment rather than FIPB route by the government

yielded in opening up of the market and thus the foreign investors enjoyed freedom in

decision making.115

The acquisition of shares of the domestic enterprise by the foreign

114 K.S. CHALAPATI RAO & BISWAJIT DHAR, INDIA‘S FDI INFLOWS TRENDS AND CONCEPTS, RESEARCH AND

INFORMATION SYSTEM FOR DEVELOPING COUNTRIES & INSTITUTES FOR STUDIES IN INDUSTRIAL

DEVELOPMENT (2011), available at http://ris.org.in/images/RIS_images/pdf/FDI_Book-Final.pdf (20

June 2014, 07.00 PM).

115 Id.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

20

09-

10

20

10-

11

20

11-

12

20

12-

13

Figure 2: Total FDI Inflows Chart

Total FDI Inflows

VOL. 1] INDIAN JOURNAL OF TAX LAW 78

investors was also one of the prominent reasons behind the increase in FDI inflow after

2005.116

The increase in inflow of FDI since 2005 is a result of policy initiatives taken by the

government. Emergence of service sector over the manufacturing sector was also responsible

for the rise in FDI.117

Increase in inflow of foreign capital from tax haven countries also

contributed towards rise in FDI in India.118

The relationship between growth and FDI in a

country is positive i.e. higher the growth rate leads to more FDI.119

The authors propose to draw a comparative analysis between the FDI during the time of

Azadi120

and that during the time when the Finance Bill, 2012 was introduced. The decision

in Azadi was given in October 2003, i.e., in the Financial Year 2003-04. As is evident from

the table and the graph shown hereinabove, the FDI inflows in that Finance Year were below

the 5000 mark, which is 10 times lesser than its peak in 2011-12, which is the Financial Year

when GAAR was first introduced. The Supreme Court had upheld the Circular 789,121

thereby validating treaty shopping. It had emerged as the tax planner‘s messiah by upholding

the Westminster principle as being applicable even today, and is viewed as a watershed in the

Indian Jurisprudence on international taxation.122

The Supreme Court had adapted a

favourable attitude towards foreign investors at a time when the government was not too

committed towards attracting foreign investment. This was a time even before the major

reforms took place in 2005 as mentioned above.

Ironically, the controversial Finance Bill, 2012 which increased uncertainty and

discretionary power (both of which are deterrents to foreign investment), was introduced at

the time when FDI inflows were at their peak because of committed measures being taken by

the Government. The Finance Act, 2012 proved to be a nightmare for the foreign investors in

India. Apart from introducing the much dreaded GAAR, it also brought in a retrospective

amendment to S. 9 of the Act by broadening the definition of capital asset being a share or

116 Id.

117 Id.

118 Id; Singapore replacing US at number 2 after Mauritius and in top 10 investing countries, Cyprus and

UEA were also added as they are tax havens.

119 Chandana Chakraborty & Peter Nunnenkamp, Economic Reforms, FDI, and Economic Growth in India:

A Sector Level Analysis, 36 WORLD DEVELOPMENT 1192 (2008), available at

http://58.194.176.234/gjtzx/uploadfile/200904/20090401152836328.pdf.

120 Azadi, supra note 29.

121 CBDT Circular No.789, 13-4-2000. The Circular clarifies that a Certificate of residence issued by the

Mauritian authorities will constitute sufficient evidence for accepting status of residence as well as

beneficial ownership for the purpose of availing benefits under the India-Mauritius double tax treaty.

122 KANGA, supra note 8.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 79

interest in a company incorporated outside so as to include underlying Indian assets of that

company within the definition. This was specifically done to overrule the Supreme Court

Judgment in Vodafone123

which had held otherwise. The enactment also disturbed the settled

position of law declared by Azadi by overriding the Circular 789.124

The enactment shook the

confidence of foreign investors, and was predicted, in India as well as abroad, to have adverse

impact on inflow of foreign investment.125

Thus, in the opinion of the Authors, the current structure of GAAR is counterproductive

to the Governments efforts at increasing inflow of foreign investment. This argument is

supported by figures showing that the annual FDI flow fell by 38% in India in the financial

year 2012-13126

despite all the Government efforts in the nature of reforms, targeted at

attracting foreign investments to India.127

The FDI attracted in November 2012 was a two-

year low.128

Even after an improvement in GAAR through the Finance Act, 2013, and the GAAR

Rules, many of the recommendations of the Shome Committee report which aim at greater

certainty have not been included. The government is introducing new and heavy FDI reforms,

but it is doubtful whether this is going to help the foreign investors in fading out the

123 Vodafone, supra 32.

124 Finance Bill, 2012 introduced sub-section (4) to S. 90 of the Act which required the assessee, being a

foreign resident, to have a ―certificate, containing such particulars as may be prescribed‖ in order to avail

the benefits of the tax treaty.‖ This disturbed the settled position of a Tax Residency Certificate being a

sufficient proof of residence.

125 Senior Advocate Harish Salve comments in Finance Act 2012. Mr. Slave also said that GAAR will affect

foreign investments. See, Proposed Change to Finance Bill to impact Foreign Investment, THE

ECONOMIC TIMES, (28 April, 2012) http://articles.economictimes.indiatimes.com/2012-04-

28/news/31453430_1_impact-foreign-investment-tax-case-income-tax-act (26 July 2014, 11:00 PM).

Italy Trade commissioner raises concern. See, Retrospective Amendment to I-T Act may FDI in India,

THE BUSINESS STANDARD, (20 May, 2012) http://taxmantra.com/inflow-fdi-impacted-retrospective-

amendment-laws.html (26 July 2013, 10:00 PM).

126 Annual FDI flow dips 38%, THE TELEGRAPH, (03 June, 2013) available at

http://www.telegraphindia.com/1130603/jsp/business/story_16965052.jsp#.UfEO99Kotf8 (23 July 2014,

04:30 PM).

127 The government had taken several policy decisions in the past few months to attract foreign investments.

Important among these include, allowing FDI in multi-brand retail and civil aviation sectors and seeking

legislative approval for increasing FDI cap in insurance and pension sectors. See, FDI dips by 38% to $ 22.4 billion in 2012-13, THE TIMES OF INDIA, (03 June, 2013) available at

http://timesofindia.indiatimes.com/business/india-business/FDI-dips-by-38-to-22-4-billion-in-2012-

13/articleshow/20392486.cms (26 July 2014, 1:30 PM).

128 Supra note 126.

VOL. 1] INDIAN JOURNAL OF TAX LAW 80

ambiguity around or the effect of the retrospective amendments on indirect transfers or non-

acceptance of certain key recommendations of the Shome Committee on GAAR.129

The government is still continuously making efforts in order to attract FDI in India in a

desperate attempt to spur the economy and to stem the rupee‘s slide. Recently on July 16,

2013 the government raised caps in a range of sectors such as telecom, asset reconstruction

firm, credit information services, defence etc.130

The Government has also been taking

measures to attract other forms of foreign investment. The Qualified Foreign Investor (QFI)

scheme was introduced in 2011-12 by allowing foreign investors to invest in Mutual Funds,

which was further expanded on 1st January, 2012 to allow them to invest directly in the

Indian Equity Market. FII investments in debt securities have also been progressively

enhanced and debt limit allocation mechanism for FII has been rationalised by allowing

reinvestment to FII, and adopting First Come First Serve (FCFS) method of allocating limits

in case of the long term infra bonds. Rationalisation has also taken place in the terms and

conditions for FII investment scheme in infrastructure debt and non-resident investment

scheme in terms of the lock-in period and residual maturity criterion.131

Furthermore, the

Chandrasekhar Committee132

formed by the SEBI published its report on June 12, 2013,

wherein it recommended the merging of existing FIIs, Sub-accounts, and QFIs into a single

investor class to be termed as Foreign Portfolio Investor (FPI) with the aggregate limit as

24%. As regards Foreign Venture Capital Investor (FVCI), the committee recommended the

considerable expansion of the present list of 9 sectors. Consequently, the Government is

expected to prepare a negative list so that the rest of the sectors are open to Venture Capital

Fund (VCF) activity.133

These efforts of the government are expected to be received stoically by foreign

investors since a lot of other key issues in India still linger in a cloud of uncertainty, and these

129 Indian Budget & its Impact for Foreign Investors, 5(33) SKP Tax Alert, (March 2013), available at

http://www.skpgroup.com/newsletters/tax-alerts/skp-tax-alert-V-33-Indian-Budget-and-its-impact-for-

foreign-investors.html (25 June 2014, 05.00 PM).

130 Supra note 111.

131 PRESS INFORMATION BUREAU, GOVERNMENT OF INDIA, Government takes several initiatives to attract

foreign investment, (December 6, 2012) available at http://pib.nic.in/newsite/erelease.aspx?relid=90127 (12 June 2014).

132 Report of the Committee on Rationalization of Investment Routes and Monitoring of Foreign Portfolio

Investments, SECURITIES AND EXCHANGE BOARD OF INDIA (June 12, 2013).

133 Id.

2014 Indian GAAR: Is Uncertainty Causing a Setback to Foreign Investments? 81

issues include the current tax structure.134

The authors being concerned only with GAAR, the

government efforts to attract foreign investments will go in vain unless the uncertainty in

GAAR is addressed.

6. CONCLUSION: CONTEMPORARY SETTING AN EXAMPLE

The Authors would like to reiterate their position that they are not opposed to the

concept of a statutory GAAR, but are critics of the form in which the Indian GAAR has been

drafted, and is expected to be implemented. A statutory GAAR in itself is not characterized

by uncertainty and unfettered power which is a major deterrence to the inflow of foreign

investment. These are characteristics which are unique to the Indian GAAR and should not

lead to a prejudicial generalisation against the concept of a statutory GAAR. This can be

evidently seen from the GAAR introduced in the UK, which became effective recently on

July 17, 2013 when the Finance Bill, 2013 received the royal assent.135

Although the two GAARs are contemporaries, the approaches followed by the two are

completely different. Philip Baker QC,136

while comparing the Indian GAAR as introduced in

the Finance Bill, 2012 and the draft UK GAAR in the Aaronson Report,137

states that ―The

Aaronson GAAR seems to have bent over backwards in trying to achieve as much certainty as

possible. One wonders whether the draftsman of the Indian GAAR has not tried to bend over

backwards in the opposite direction.‖138

The Aaronson Report advocated a moderate and focussed Anti-Avoidance Rule for the

UK, which aims at targeting abusive and contrived arrangements without disturbing

reasonable tax planning. The Report rejected the idea of a broad spectrum GAAR as being

unnecessary to the UK tax system, and a GAAR along the lines of the Report was accepted

134 Reforms Fail to enthuse Foreign Investors, EQUITY MASTER‘S-THE 5 MINUTE WRAP UP, available at

http://www.equitymaster.com/5MinWrapUp/detail.asp?date=07/22/2013&story=2&title=Reforms-fail-

to-enthuse-foreign-investors (27 July 2014, 8:46 PM).

135 Christopher Groves et al, United Kingdom: UK Finance Act 2013-Royal Assent on 17 July 2013,

WITHERS WORLDWIDE, (July 27, 2013) available at

http://www.mondaq.com/x/254390/Income+Tax/UK+Finance+Act+2013+Royal+Assent+on+17+July+2

013 (27 June 2014, 08:50 PM).

136 Philip Baker, Tax Barrister and Queens Counsel, United Kingdom.

137 REPORT BY GRAHAM AARONSON QC, GAAR Study, November 11, 2011(hereinafter ‗AARONSON‘).

138 Philip Baker, The UK GAAR and the Indian GAAR, available at

http://www.taxmann.com/taxmannflashes/flashst13-6-12_DTL_3-UKGAAR.pdf (23 July 2013, 3:42

PM) (hereinafter ‗Baker‘).

VOL. 1] INDIAN JOURNAL OF TAX LAW 82

by the Government in the Budget of 2012.139

Thus, the GAAR which has recently come into

force in the UK is along the lines of the GAAR suggested by the Aaronson Report, with some

material differences reflecting the formal consultation process.140

One of the major causes of uncertainty in the Indian GAAR is that it is extremely broad

and targets an ―impermissible avoidance arrangement‖, the main purpose of which is to

obtain a tax benefit, and this condition must be qualified with any of the stipulated conditions

which include misuse or abuse of the legislation and deemed lack of commercial

substance.141