india's economic performance and business imperatives- onboarding gst: one nation, one tax

TRANSCRIPT

12 Years Of Excellence

Onboarding GST: One Nation, One Tax

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Volume 6 November 2016

Developed & Researched By: Dipti Chawla, Payal Tuli, Mamatha Anand

Contributions By: Anshul Aggarwal, Harkishan Bhatia, Kaustuv Sen, Madhava Yathigiri, Mahesh Jaising, Nidhi Lukose, Poonam Harjani, Prashanth Bhat, Sarabjeet Singh, Saurabh Kanchan

Acknowledgements: Abhirath Bhat, Ankush Surana, Jyoti Bhowmick, Ketan Lohia, Netal M, Siddharth Tandon, Sonam Bhandari

Edited By: Mukesh Butani

Section A: Onboarding GST – One Nation, One Tax | p2

Section B: Macroeconomic Trends & Prospects | p24

Section C: Key Sector Updates | p26

Section D: BMR Thought Leadership | p38

References | p43

About BMR | p44

CONTENTS

Prologue

The streamlined and focused manner with

which the government has sought to

implement the nationwide goods and

service tax (GST) has never been

witnessed in India before. The approach of

the government seems precise and the

pace at which hurdles were cleared is

worthy of admiration. In a short span since

the passing of the GST legislation in Rajya

Sabha, several milestones crucial for

introduction of GST in India have been

achieved, including passage of the

Constitutional Amendment Bill by the

Parliament, setting up of the GST Council

and release of draft legislations. It is

remarkable to note how consensus was

achieved between the Government and

other political parties through constructive

dialogue on various nuances of GST.

Advancing the winter session, yet another

tell-tale sign, magnifies the government's

commitment towards speedy rollout of the

new regime.

Expected to bring greater tax parity across

the country, GST - a unified indirect tax,

would subsume significant number of

existing central and state levies. The

landmark reform seeks to harmonise

India's indirect tax regime, paving way for

realising the goal of 'One Nation, One Tax'.

As per the extant law, different activities

trigger different taxes - manufacturing

attracts excise, sale of goods attracts

value added tax (VAT) or central sales tax

(CST) and provision of services attracts

service tax. Under the proposed regime,

there would be just one single activity of

'supply' triggering the levy of GST. Central

GST (CGST) and State GST (SGST) would

apply together on any intra state supply

and an integrated GST (IGST) would apply

on inter-state supplies and imports into the

country, apportioned between the center

and the states at the backend. Save for a

few exceptions such as liquor and

specified petroleum products, GST would

apply on almost all goods and services.

Seeking to act as a panacea to the myriad

tax issues plaguing the industry (across

sectors), introduction of GST is likely to

enable businesses to focus on commercial

factors for making decisions and not tax

factors, as has been seen in the past.

Focused towards implementation, the

Government has adopted a collaborative

approach with open channels of

communication with all stakeholders.

Release of draft Model GST Law in June

ONBOARDING GST: ONE NATION, ONE TAX

Prologue

2

SECTION A

2016, release of subordinate

legislations for public feedback and

initiation of public awareness

campaigns are manifestations of the

fact.

With less than five months to go before

the current deadline of April 1, 2017

and the Government working

vigorously towards implementation of

GST, it is imperative that the

businesses get cognizant as to how

GST would impact each aspect of their

companies from an operational,

infrastructural and financial perspective

and brace themselves for this

gargantuan tax reform never witnessed

before in independent India.

The following sections of this quarterly

report presents an in-depth analysis of

developments on GST implementation

roadmap, insights on industry's

preparedness for the new regime and

makes assessment of implication on

key sectors of the economy (Section

A), followed by a review of

macroeconomic trends & prospects for

the Indian economy (Section B), key

sector updates (Section C), and an

exclusive Business Today - BMR

Advisors Survey on GST (Section D).

I hope you find the report informative

and useful and look forward to your

continued support.

Rajeev Dimri

“Our Government is committed to tax reforms,

in general, and implementing GST, in

particular, and I am confident that we shall be

able to get the constitutional amendment,

which shall pave the way for a landmark tax

reform”.- June 9, 2016, FM Arun Jaitley's foreword to 'Tax Dispute Resolution: Challenges and

Opportunities for India' – An ICRIER and BMR Advisors initiative, published by LexisNexis

3

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

GST will, at a basic level, affect the tax

positions and compliance requirements

for businesses. But more importantly,

GST would raise fundamental questions

on existing operating structures, legal

entity structures and transaction

structures which apart from various

commercial reasons, have been

configured to align with the existing

indirect tax framework and requirements.

GST - SECTORAL IMPACT ASSESSMENT

Section A: Onboarding GST – One Nation, One Tax

4

By Saurabh Kanchan

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Not only would GST impact the

various sectors of the economy

such as automobiles, FMCG,

defence, banking or information

technology, the level and degree

of impact is different across

sectors. A lot also depends on the

product or service offerings,

activity profile such as

manufacturing, services or trading

and geographical spread of the

businesses, their vendor and

customer base across States. For

instance, tax rate changes for

various categories of products

and services would directly

impact pricing and profitability of

businesses. Persistent issues

around double taxation of

transactions such as software,

intellectual property and works

contracts may get addressed.

While product companies have for

a long time been accustomed to

dealing with State boundaries

from a VAT perspective, GST

marks a fundamental shift for the

tax environment of service

companies. Taxation of services

under GST would be

decentralized at the State level.

This will impact the manner in

which service companies are

geographically oriented in terms

of customer services, contracting

structures with customers and

vendors, internal IT systems

alignment, tax team resources

and training, interface with tax

authorities and compliance

requirements.

Thus, as we go through the GST

repercussions on select sectors of

the economy in the following parts

of this section, it is useful to keep

in mind that GST would seep

through the several layers of

economic transactions

undertaken by businesses and the

new regime's effect would be all

pervasive.

The GST is expectedto impact

businessesacross

sectors.

5

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

SECTION B: SECTORAL UPDATES

166

Currently riddled with a plethora of taxes, this

sector, has much to look forward as the new

regime is set to turn the face of entire indirect

taxation policy. Some significant impacts of

the new regime on the sector are illustrated

below:

Ÿ Simpler and more certain tax environment

with elimination of some existing concepts

viz deemed manufacture, valuation on MRP

basis, dual taxation of goods/ services, etc.

Ÿ Streamlined movement of goods across

states with elimination of entry tax, CST and

possible discontinuation or simplification of

various statutory filings.

Ÿ Reduction in overall indirect tax incidence

from present 25-30 percent for most

manufactured goods to a standard rate of

around 18 per cent. As per the latest news

reports on GST Council discussions, it

appears that luxury vehicles may face a

higher rate of around 26 percent. Further,

an additional cess is being proposed on

the luxury segment. The overall tax impact

for luxury cars would, hence, depend

heavily on the rate and creditability of such

cess.

Ÿ Broadening of credit base with thinner list

of items covered under the restricted list.

However, credit restrictions on motor

vehicles may be continued under the new

law, except when used for specified

services.

Ÿ Credit of excise duty paid by dealers on the

inventory lying in stock at the time of

implementation is likely to be restricted

leading to a possible (short term) surge in

pricing of all manufactured goods.

Ÿ Questions concerning operational

efficiency of existing tax incentives policies

of State Governments with change in

principle of taxation policy from origin

based to destination based remain open.

Pursuant to the recent GST Council

discussions, it has been announced that

benefits being provided under such

policies will be preserved by way of refunds

from annual Centre and State budget.

However, since the State Government will

no longer tax supplies originating from its

State, it remains to be seen whether the

economic benefit which is presently

available to companies under such policies

will continue to remain the same under GST

or not.

Ÿ Taxation of stock transfers and trigger of tax

liability upon receipt of advance would

advance existing point of taxation for

goods, impacting working capital

requirements.

Ÿ Automobile industry is presently facing

litigation on inclusion of joint advertisement,

after sales service, pre-delivery inspection

charges etc. in transaction value for

payment of excise duty. These issues will

continue in light of the valuation rules.

Further, arriving at a fair value in case of

related party transactions, especially for

services is a new compliance requirement.

Ÿ Input credit availability under the GST

regime is dependent on the seller having

paid the tax to the account of government,

this is likely to pose a compliance

challenge for the sector.

Considering the complex indirect tax

structure as it exists today, GST is expected

to be a welcome step for the automobile

sector. Apart from tax simplification, ample

opportunities for business restructuring,

diversification and expansion would open up.

AutomobilesBy Payal Tuli and Poonam Harjani

Section A: Onboarding GST – One Nation, One Tax

GST is likely to usher positive changes for

the sector, presently riddled with issues of

double taxation, multiple tax levies, credit

restrictions etc. The approach is to have

fewer exemptions and ensure a moderate

GST rate overall, as exemptions distort the

regime. However, to ensure the sector is not

burdened with heavy tax costs resulting in

higher capital outlay, certain presently

available incentives and exemptions must be

continued. Key implications to the sector are

enumerated below:

Ÿ Subsumation of various taxes under GST

reduces complexities by eliminating levies

on various legs of same transaction and

the need to determine taxable event for

each such levy. This would ensure

smoother movement of goods across

states with lesser trade barriers.

Ÿ Free flow of credit across value chain

reduces tax costs thereby reducing the

cascading effect. (Excise duty, CST, entry

tax etc., will no longer be cost in the

system for project owners and

contractors, thereby reducing the project

cost).

Ÿ An overall tax on actual base value

without need to split the contract value

between goods and services (as is

required under the current regime which

leads to 110-145 per cent taxable base for

levy of VAT and Service Tax).

Ÿ New regime will reduce litigation for

contractors with regard to taxation of

interstate sales, in-transit sales and sale in

the course of import.

Ÿ Credit restrictions on GST paid on

construction activities (on the civil side)

would continue leading to increase in

costs of construction on account of higher

GST rates.

Ÿ Non-continuation of incentives under the

renewable energy sector will pose

challenges since it leads to increase in

cost of setting up and operation of

projects, possibly resulting in increase in

tariffs. Non-subsumation of electricity duty

under GST leads to cascading effect of

taxes, on account of non-creditability of

electricity duty paid.

Ÿ Potential cost increase for port and airport

projects due to increase in overall tax

costs as compared to present regime.

Infrastructure sector is a major building block

for development of the economy.

Government should endeavour to address

the concerns before GST implementation to

ensure robust growth of the sector, which is

crucial to sustain high growth in the long

term.

GST is likely to usher in positive changes for the infrastructure sector.

InfrastructureBy Prashanth Bhat and Nidhi Lukose

7

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

8

Being a unified indirect tax regime, GST will

eliminate multiple taxable events and

compliances bringing significant relief to the

sector grappling with myriad indirect tax

issues. Differing VAT practices in states with

respect to taxability, rates, valuation, etc.

have been road blocks. With free flow of

credit across the value chain, tax costs will

reduce, thereby reducing the cascading

effect of taxes. As a result, excise duty, CST,

entry tax etc., will no longer be cost in the

system for developers and contractors,

thereby reducing the construction cost.

Specific classification of construction/ works

contract activities as 'service' ensures levy of

tax is on actual base value without the need

to split contract value between goods and

services (as is required in the current regime

which leads to 110-145 per cent taxable

base for levy of VAT and service tax).

While at a macro level GST should bring

uniformity across States, resulting in fewer

litigations, aspects that need attention

include:

Ÿ While transfer of title in immovable property

has been specifically excluded from the

definition of ‘service’ under the current

regime, there is no such exclusion from the

definition of 'service' under GST. While this

may be an oversight, the exhaustive

definition of service does open up a debate

on taxability of various transaction in real

estate sector which do not transfer the title

but enjoyment of the property.

Ÿ Inclusion of free supplies of goods by

developers to contractors in transaction

value shall lead to dual tax cost in the

hands of developers, since developers

shall not be eligible for credits on such

procurement.

Ÿ Credit restrictions on commercial projects

continues under GST regime as well, which

may lead to increase in construction costs

on account of higher GST rates.

Ÿ Debate on taxability of development rights,

land aggregation transactions, secondary

market transfers, assignment of purchasing

rights in immovable property etc., are not

specifically addressed and are likely to

continue.

Real EstateBy Prashanth Bhat and Nidhi Lukose

Section A: Onboarding GST – One Nation, One Tax

1Joint Development Agreement

Ÿ There is no option of paying GST under the composition scheme for developers selling units

before completion. Sale of units are likely to attract GST rates as applicable to services, after

any abatements for land deductions that may be prescribed. This may have negative impact

on the mindset of home buyers, and could be perceived as inflationary given the full GST rate

on face of the invoice.

Ÿ Model Laws are silent on zero rating of supplies of goods and services to SEZ developers

and units. In fact, there is a possibility that developers may not get the benefit of refunds

given that the draft refund rules in their current form provide refunds for exporters i.e., units.

Hence, for developers it is a clear case of increased cost if benefits do not continue and

SEZs losing their sheen.

It is critical that the above concerns are addressed before the final GST laws are released for

the benefit of the sector and also home buyers.

Being a unified indirect tax regime,

GST will eliminate multiple taxable events and

compliances bringing significant relief to the sector

grappling with myriad indirect tax issues.

9

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

10

With India witnessing a retail and e-

commerce revolution due to rise in income

levels, urbanisation, changing customer

preferences etc., the sector is keenly

observing implementation of GST. E-

commerce is increasingly emerging as the

preferred mode of consummating retail

commercial transactions. Since the sector is

currently at a nascent stage, tax environment

around it is also still evolving. With absence

of clear legislative provisions, multiple

taxation authorities have been adopting

diverse tax treatments in order to apply

varied transaction taxes on e-commerce

transactions. This has left the sector

grappling with numerous indirect tax

controversies off-late.

Model GST Law has ushered a ray of hope

for the sectors. A special dedicated chapter

on e-commerce highlights the positive

government intent to afford certainty around

taxation for the sector under the new regime.

Thus, it is being envisioned that GST will lead

to an all India alignment of the tax treatment

with an aim to ensure a uniform indirect tax

treatment for this sector.

The implications of GST for this sector are

enumerated in brief below:

Ÿ Under the new regime a transaction will be

taxed by the consumption state thereby

hopefully mitigating situations of competing

claims by two or more States to levy tax on

the same transaction

Ÿ Elimination of entry tax would ensure ease

in movement of goods across states and

removal of trade barriers

Ÿ New GST regime will enhance the

availability of credit of taxes to traders

(including e-tailers) since they will be

entitled to input tax credits of various

distribution related input services. Further,

input service distributor facility, which is

presently not available to traders, would

enable better credit utlilisation.

Ÿ GST will also offer an opportunity for re-

creating supply chain modalities based on

commercial considerations rather than

taxation mechanism. Under the present

system, every company in the retail sector

plans its procurements and locations of its

warehouses and branches to optimise on

credits. Under GST, such tax

considerations are likely to go away.

Ÿ Following the GST Council's first meeting,

minimum exemption threshold has been

Retail and e-commerceBy Poonam Harjani

Section A: Onboarding GST – One Nation, One Tax

GST expected to address the ambiguities surrounding this sector.

affixed at INR 2 mn. This is a welcome step

for small retailers as compared to the

current VAT threshold limits, which are very

low in most States.

Ÿ Further, the Council has proposed that

assessees with annual turnover of less than

INR 15 mn are likely to be assessed by

State authorities only. This will save small

players from the hassle of being under the

administrative control of multiple tax

authorities under GST.

Ÿ GST mostly focusses on transparency with

respect to tax payments, credits etc. and

as a consequence requires more robust

and full proof compliance support from

assessees. The industry thus appears to be

a bit apprehensive of the magnified

compliance requirements in terms of

maintenance of records, returns,

departmental audits etc. Increased

compliances especially for e-commerce

players on account of collection of tax at

source (TCS) for sales and maintenance of

vendor records is an added compliance

burden.

Ÿ Model GST law requires more robust

transition provisions. Presently, the Law is

silent on transition of credits pertaining to

excisable stock lying with traders/dealers.

Ÿ Providing incentives, freebies and

discounts is a part and parcel of the trade.

Possible GST exposure on free supplies,

such as, free samples, freebies offered

under promotional schemes, etc. is likely to

increase working capital outflow.

Ÿ Since the GST law is currently evolving,

clarity on whether the platform operators

with no Indian business presence require

registration in India is awaited.

Model Law seeks to bring comfort to this

sector with the law makers aiming to define

clear taxation principles. As the Law would

evolve it is expected that the ambiguities

surrounding the sector would be suitably

addressed.

11

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

12

It is expected that GST would incrementally

impact banking and financial services

industry, relative to the manufacturing and

other services sector. Enumerated below are

some potential areas of impact:

Ÿ Level of compliances will see dramatic

uptick under GST. An entity operating on a

pan-India basis was hitherto filing 2 returns

per annum. Under the GST regime, it would

need to file 3 returns per month, in 29

States, over 12 months, in addition to

annual tax and information returns; totalling

1046 returns. In addition, the entity would

be subject to assessment in all 29 states.

The banking industry is currently making

representations to the Government on this.

Ÿ This sector is subject to a different set of

rules to determine the 'place of supply'

rules. However, the term 'banking and other

financial service' is yet to be defined. Also,

classification of services under the GST

regime would be based on the Services

Accounting Code (SAC). As a result, the

boundaries of this industry from a GST

perspective is unclear.

Ÿ Compliance is likely to increase manifold

for the banking sector which has pan India

presence. In wake of the same, cost of

doing business is likely to increase for the

sector

Ÿ Services such as investment banking to

overseas clients currently attract service

tax, while financial research, asset

management and advisory rendered to

overseas clients are tax free. As per the

draft place of supply rules, (all) such

services would be treated to have been

supplied in India. While this tax could be

rationalised based on the need of tax parity

between overseas and domestic clients,

the counter argument is that domestic

clients could potentially avail credit of such

GST charged by service providers, which

overseas clients will not be entitled to.

Ÿ The GST regulations require identification

of the location of 'supplier of service' since

GST would be reported and assessed in

state location. Such determination is

difficult for financial services. Certain

illustrations relate to:

Ÿ Credit card related functions such as

card issuance, statement generation,

accounting, risk management,

technology infrastructure could be

Level of compliances will increase manifold for banking and financial services sector under GST

Banking and financial servicesBy Kaustuv Sen

Section A: Onboarding GST – One Nation, One Tax

located in different states. The selection of the appropriate state to report GST on such

services would be difficult.

Ÿ Whether home or auto loans should be tagged to the state where stamp duty is paid on

the loan agreement or the automobile is registered.

Ÿ Financial services have a growing 'secondary' market beyond the ‘primary’ market

experienced by corporate and retail customers, such as securitisation transactions in loans,

distressed debt etc. Such transactions in unsecured debt may qualify as ‘actionable claims’, 2 3

e.g. personal loan and microfinance portfolios, PTCs issued by ARCs . Since transaction in

actionable claims are now treated as a service under GST regulations, such secondary

market may need to review the GST implications of its business.

Thus, the banking sector would possibly be mired with several intricate questions that would

hopefully be unravelled as the GST legislation shapes up.

132 Pass-through certificates3 Asset Reconstruction Companies

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

14

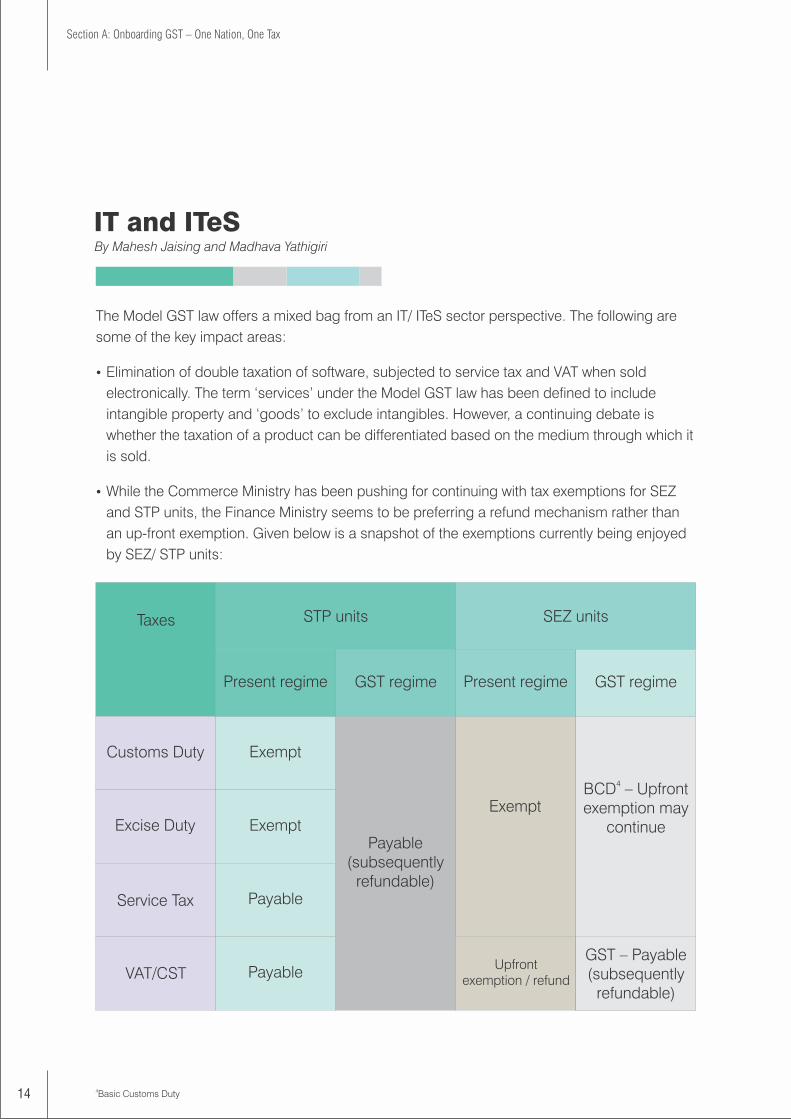

The Model GST law offers a mixed bag from an IT/ ITeS sector perspective. The following are

some of the key impact areas:

Ÿ Elimination of double taxation of software, subjected to service tax and VAT when sold

electronically. The term ‘services’ under the Model GST law has been defined to include

intangible property and ‘goods’ to exclude intangibles. However, a continuing debate is

whether the taxation of a product can be differentiated based on the medium through which it

is sold.

Ÿ While the Commerce Ministry has been pushing for continuing with tax exemptions for SEZ

and STP units, the Finance Ministry seems to be preferring a refund mechanism rather than

an up-front exemption. Given below is a snapshot of the exemptions currently being enjoyed

by SEZ/ STP units:

Taxes STP units SEZ units

Present regime Present regimeGST regime GST regime

Customs Duty Exempt

Payable (subsequently

refundable)

Exempt

4BCD – Upfront exemption may

continue

GST – Payable (subsequently

refundable)

Upfront exemption / refund

Exempt

Payable

Payable

Excise Duty

Service Tax

VAT/CST

4Basic Customs Duty

IT and ITeSBy Mahesh Jaising and Madhava Yathigiri

Section A: Onboarding GST – One Nation, One Tax

Ÿ Government, in past few budgets, has extended benefits for indigenous manufacturing of

tablet computers, mobile phones and consumer premise equipment. Based on such

benefits, industry players have setup manufacturing facilities in India. However, the request

has been to grandfather such benefits in a meaningful way. Hence, it would be worthwhile to

watch for the manner in which such benefits are carried forward.

Ÿ Under present service tax law, service providers operating from multiple locations can obtain

a single centralised registration and billing. However, the Model GST law requires every

supplier in each state to obtain registration and possibly to undertake billing from each

location, resulting in increase in compliance burden.

Ÿ The Model GST law prescribes certain transactions though undertaken without consideration

to be subjected to GST. As per the said schedule, services provided from the branch offices

to head offices may be subject to GST in situations where the billing is undertaken from head

office for which multiple branch offices have provided services to customer. This could

become a major area of concern for companies having pan India presence. In its absence,

the companies may be forced to file application for refund in multiple locations due to

accumulation of credit.

Undoubtedly, GST would usher in various benefits for the IT/ ITeS sector, which is hopeful that

the few issues aforementioned are ironed out so GST can be implemented smoothly and

successfully.

15

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

16

Ÿ Analyse impact from a business,

operational and financial perspective on

an immediate basis. Such an analysis

would aid the industry in taking a relook

at the costing/pricing of the goods

and/or services which drives business

performance in light of the revised tax

costs under the GST regime.

Ÿ Review existing business models and

analyse transaction flow under the new

law

Ÿ Analyse the impact of taxes under GST

on working capital and plan alternate

options, wherever required well in

advance to avoid any transition related

financial hardships. This would also aid

in drawing up a plan for the crucial last

quarter of fiscal 16-17 before

implementation of GST.

Ÿ Determining of key compliances to be

undertaken by the industry, which is

likely to be elaborate – and drawing out

a framework for being GST compliant

from day one

Ÿ Restructure or developing robust IT

systems aligned to meet requirements

under the new regime. This entails

complete automation of processes and

compliances (elucidated in detail in the

ensuing article)

Ÿ Training of personnel to embrace finer

nuances would be imperative for

successful implementation. Hence,

training requirements of different teams

in the company including tax teams,

business teams, procurement teams,

ought to be identified.

Ÿ Identify areas of advocacy and

engagement with the Government that

warrant representation to GST

authorities

Ÿ Planning and gearing up for possible

impact on businesses in the last quarter

before the roll-out.

While GST is all set to become a reality, the real question that looms

large is whether India Inc. has geared itself for the new regime of 5taxation, as elucidated in the Business Today – BMR Advisors Survey

(Section D of the report). It is imperative that India Inc. focuses on

addressing key issues.

GST PREPAREDNESS FROM AN INDUSTRY PERSPECTIVE

By Mamatha Anand

Section A: Onboarding GST – One Nation, One Tax

5 Business Today – BMR Advisors Survey on GST – Is India Inc. ready?, September 2016

Prepare for a myriad of changes

It may be discerned that the industry has substantial ground to cover before implementation.

Accordingly, it is vital that it acts fast chalking out an effective action plan with timelines since

the question is no longer if GST would be rolled-out, but it is the question of when.

While the companies are required to gear up in respect of various aspects as elaborated

above, such preparedness to a large extent will have to be based on host of draft GST

legislations which have been released to date. The final GST legislations are expected to be

available to industry only in the later part of the year with GST anticipated to be rolled out next

year, the industry is thus likely to face an uphill task in preparing itself.

17

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

It may be re-emphasised that GST will bring

structural changes in how businesses

operate with effects encompassing all their

departments, products and locations. The

ramifications of GST would not be limited to

only tax invoicing but rather impact every

aspect of corporate decision making, be it

production, inventory management, supply

chain management, delivery of service or

pricing.

Accordingly, Technology becomes an

important component when it comes to

managing a change in tax regime. The right

technological support ensures smooth

transition from the 'As-is' to 'Desired' stage.

With companies pursuing strategies involving

complex structure of products and services,

they must ensure that every module in their 6ERP complies with the change in tax

structure. The following factors need to be

ensured while implementing the technology

based changes:

Ÿ Changes in ERP masters, formats and

reports (e.g. vendor master, invoices,

purchase orders, sales register, etc.)

Ÿ Developing tax incidence points for each 7

entity (three GSTN numbers for each

entity in each state)

Ÿ Interaction with the government tax

reconciliation system based on GSTN

network

Ÿ Possible changes in accounting practices

as a result of consumption based tax

incidence

Ÿ Cohesiveness with the existing system to

ensure smooth transitions for pending

inventory

Ÿ Flexibility in ERP by having pre-emptive

provisions to incorporate subsequent

changes in the GST policy.

Process remodelling would also be required

to ensure that all business activities get

aligned to the changes in business

parameters with the advent of GST. For

instance, Vendor supply agreements may

change as the allocation of territory would be

based on market homogeneity rather than

tax jurisdiction, which would effectively mean

a revamped process flow of Order

Management and Purchase Management

modules.

A functional remodelling of process would

involve:

Ÿ Remodelling of process flows of business

activities such as ‘purchase to pay’ and

'order to cash'

Ÿ Updating and preparing policies related to

purchases, sales, intra-company

transactions, etc.

Ÿ Standard operating procedures (SOPs)

for submission of GST returns and

payments

Ÿ Change in vendor arrangements to

ensure tax compliance of vendors

Ÿ Change in arrangement with dealers as a

result of re-allocation of territories

Ÿ Reworking of organisation structure for

sales network

Ÿ Contingency plans in case of alterations

to GST policy

Ÿ Training of employees

IT infrastructure & process readinessBy Sarabjeet Singh and Harkishan Bhatia

Section A: Onboarding GST – One Nation, One Tax

186 Enterprise Resource Planning7 Goods and Services Tax Network

GST rules are still in draft stage with expectation

that the final rules once notified would give

companies a very limited bandwidth to

implement process related changes in the

business structure. Thus, businesses need to

start developing effective Project Management

(PM) strategies to efficiently plan, organize,

implement and control the change management

exercise to ensure all business functions are

aligned to a common goal, i.e. smooth transition

to GST. An effective PM strategy is required to

track timelines of all proposed changes across

entities and locations, manage change

management teams, relationships with external

consultants, map out different stakeholders, and

ensure compliance by vendors and dealers.

Further, the GST model is expected to evolve as

industry continues to advocate and suggest

changes to alter business impeding provisions

in the GST draft.

As next steps, businesses need to assess their

existing ERP systems and processes, map

movements of their products and services with

points of consumption and develop strategies /

practices to weed out inefficiencies in the

business activities which had crept in as a result

of tax distortions over the years. All these steps

would ensure that ability to conduct business is

not limited as a result of compliance with GST

framework. In the short term, GST

implementation would increase the compliance

cost for businesses but at the same time, it

presents an opportunity to standout in terms of

competitiveness. The result will depend on how

fast and effective businesses are in

implementing the change.

Industry will have

to tighten the nuts

and bolts of their

businesses.

19

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

20

With less than five months to go before the April 1, 2017 deadline, the Council has set its

wheels in motion, and held three meetings to deliberate on the nitty-gritties of the new system

and to iron-out differences on crucial first-principle issues. Key recommendations have been

made to firm up rollout which are very crucial as these recommendations will feed into drafting

of GST laws.

GST Council: cornerstone of GSTBy Payal Tuli and Anshul Aggarwal

Endorsing the spirit of co-operative federalism, the GST Council has been formulated to ensure

collaborative decision making and accelerate implementation of this landmark reform. Flagged

off by the Cabinet, the council has been set-up with representation of Central and State 8

Governments and aims to facilitate decisions factoring ground realities of both the states and

the center. Each key decision of the council would be taken with three-fourth majority – one-

third weightage for central government's vote and two-third for the collective votes of all states,

thus making a near-consensus between center and states an imperative for major decisions.

This bodes well for the GST as every decision taken by the Council would be based on majority

view, leaving less space for debate.

GST Council

Members

Union Minister of State in-charge of Revenue or Finance State Finance Ministers

Chairman

Union Finance Minister

Role and power

Ÿ Recommending critical parameters - rate of taxes, exemption list and threshold limits.

Ÿ Deciding technicalities of compensation to states for their revenue loss

Ÿ Recommending time-frame of bringing specified petroleum and allied products GST's

purview

Ÿ Formulating a robust and fair dispute resolution mechanism

Section A: Onboarding GST – One Nation, One Tax

8 The Council is chaired by the Union Finance Minister – Arun Jaitley and all the state finance ministers are part of the council. Additionally, a secretariat has been formulated, to support work of the council, which has IRS officers and members of Central Board of Excise & Customs as its members.

Key Decisions

Key decisions taken by the Council thus far are:

Ÿ Threshold limit fixed at INR 2 mn

Ÿ All cess levy to be subsumed under GST

Ÿ States to exercise control over assesses having turnover upto 15 mn

Ÿ Control over large sized assessees (with turnover exceeding INR 15 mn) would be exercised

either by the Centre or the State based on risk assessment formula

Ÿ Existing 1.1 million service tax assesses to be administered by the Central Govt., for initial

period

Ÿ Finalisation of the subordinate legislations for registration, payment, refund, returns and

invoice9

Ÿ The Centre had proposed a four tier tax rate structure to the States as follows:

- Lower rate of 4 percent for precious metals

- Lower rate of 6 percent for essential goods

- Two standard rates 12 and 18 percent applicable to goods and services

- Higher rate of 26 percent on luxury items, pan masala and tobacco products; In

addition, cess equivalent to the rate differential vis-à-vis the current regime may also be

levied on may be levied on ultra-luxury items

Contrary to expectations, no consensus was reached on the rates and industry would be

keenly watching out for the announcements post the meeting slated in early November.

The GST council has been entrusted with wide ranging powers which would have far reaching

consequences on how GST eventually shapes up and how business is conducted. Industry

expects that GST council will make unambiguous recommendations with utmost clarity to

mitigate litigation and promote ease of doing business. With public at large expecting the

council to decide reasonableness of GST rate to keep inflation under check, we expect the

council to remain proactive and receptive to the recommendations from various stakeholders.

Success of the Council would lie in assisting taxpayers and revenue department in overcoming

transition issues and bringing certainty, clarity and transparency under the new regime. This

can be attained by regular engagement and co-ordination with all stakeholders and issuance of

clarifications on a regular basis.

The effective functioning of the GST Council will have far reaching consequences on how GST eventually shapes up and how business is conducted.

21

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

9 As per last meeting of GST Council on October 18 and 19

22

GST is expected to bring about a paradigm shift in indirect taxation and consequently, manner of doing business, it is eagerly awaited and the developments closely observed in its run-up.

However, GST will evolve and mature over the next few years before it settles down as an ideal and comprehensive indirect tax regime for the country.

Section A: Onboarding GST – One Nation, One Tax

Key Takeaways

GST, hailed as one of India's biggest tax reforms, will turn India into a common market leading

to broadening of credit base and allowing greater ease of doing business with automated

registrations and compliances, albeit coupled with substantial and real time data exchange

with the tax authorities. As elaborated some sectors stand to gain vis-à-vis others.

The scheme of GST is in line with the 'Make in India' campaign of the Narendra Modi-led

government, which seeks to encourage investment in India. The implementation of GST will

significantly improve the competitiveness and performance of India's manufacturing sector.

GST will bring tax savings for this sector in the form of fewer taxes, elimination of cascading

taxes, seamless flow of input credits across the value chain, removal of dual taxation and

simplification of other concepts. Trading would also be amply incentivized under the GST with

traders being allowed the same credit eligibility as that of manufacturers.

It is also important to note that the GST regime in its initial implementation design, does leave

out a portion of the economic activity from its purview. This would occur due to exclusions for

specified petroleum products such as crude, petrol, diesel, aviation turbine fuel (ATF) and

natural gas, transfer of real estate, electricity and alcohol for human consumption combined

with anticipated exemptions for the education and healthcare sectors. Some of these products

and sectors may over a period of time, fold into the GST as well. Thus, the GST would evolve

and mature over the next few years before it settles down as an ideal and comprehensive

indirect tax regime for the country.

Keeping aside predictable teething issues specifically for the service industry elucidated earlier

in this report, holistically, the advent of GST is expected to provide a further boost to the Indian

economy with inclusive growth in industry, better investments and hopefully improved

consumer spending power. GST would bring about a paradigm shift in indirect taxation and

consequently, manner of doing business, it is eagerly awaited and the developments closely

observed in its run-up.

23

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Looking at the macro fundamentals in detail,

in Q1 of this fiscal, India grew at 7.1 per cent

with a 3.1 per cent contraction in investment

activity. The latter is due to de-growth in

capital goods sector, government's capital

expenditure pattern, and sluggish investment

activity in the private sector. Consumer price

index (CPI) inflation came down to 4.3 per

cent in September and is expected to drop

further following a good monsoon. Trade

deficit narrowed materially, falling by more

than 40 per cent to USD 34.7 bn (INR 2.3 tn)

in first five months of current fiscal, aided

largely by a double digit slide in imports

compared to a slight drop in exports. Growth

in industrial production continues to remain

volatile, with a contraction of 0.7 per cent

and 2.5 per cent in July and August

respectively compared to positive growth of

1.9 per cent in June.

There are signs of green shoots visible in

manufacturing with the purchasing

managers' index (PMI) and FICCI's

Economic Outlook Survey indicating a pick-

up in fresh orders for both domestic and

external sectors. Growth in the services

sector is becoming broad-based and

witnessing sharp acceleration due to new

business models. Businesses are optimistic

on better economic conditions. The positive

sentiments in the economy can also be seen

from sectors such as automobiles, which is

registering an increase in sales across most

segments. Railway, ports and international

air freight traffic, foreign tourist arrivals, and

domestic air passenger traffic are also

witnessing an improvement, thus providing

an underlying momentum for upturn.

In the external sector, continuous decline in

merchandise exports growth since the last

fiscal has largely been arrested with positive

growth expected in the second quarter.

While the pace of FDI inflows slowed in the

first two months of 2016-17, net portfolio

flows have remained robust.

India's GDP forecasts for the entire fiscal

(FY2016-17) have revealed mixed sentiments

- with some international bodies revising

their forecasts downward marginally and

others predicting an acceleration in growth.

All projections suggest that India would be

able to sustain its growth momentum and

register a strong GDP ranging between 7.4-

7.7 per cent. Detailed projection of India's

GDP by various agencies highlighted in the

table.

Unlike major world economies surviving on monetary and fiscal push for the last few

years, India is on a self-accelerating growth path, albeit one supported by low oil

prices, prudent macroeconomic management and reforms. Economic growth in

India is expected to stay high owing to a normal monsoon and general increase in

wages, which is likely to boost consumer demand. With revival in consumption and

benign interest rates (and inflation) situation, recovery in the investments cycle is

likely to set in coming quarters.

MACROECONOMIC TRENDS & PROSPECTS

SECTION B

Section B: Macro-economic Trends and Prospects

24

Looking at the balance of fiscal 16-17, the momentum of growth is expected to accelerate

mainly on account of two factors which will pull demand. Firstly, the normal monsoon this year

will bring down food inflation and bolster agricultural growth and rural demand. Another

stimulus to consumption spending is expected from the implementation of the seventh pay

commission. Growth will be triggered more from these domestic factors rather than externally,

especially since global economic growth continues to be anaemic.

Efforts to clean-up bank balance sheets to revive lending and reducing excessive leverage of

large corporations is setting the stage for recovery in quality of investment spending, which is

likely to drive higher growth. Enactment of legislation to allow a national value added Goods

and Services Tax (GST) is a milestone reform that is expected to create an integrated and

productive economy. Owing to chugging wheels of reforms, India jumped up 16 spots (highest

improvement) to 39th position among 138 economies in the recent Global Competitiveness

Index of the World Economic Forum.

RBI IMF ADB OECD FITCHGOLDMAN

SACHSWORLDBANK

7.6 7.4 7.4 7.4 7.7 7.77.6

Growth will be triggered from domestic factors rather than external, given anaemic global economic growth

25

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

KEY SECTOR UPDATESSECTION C

Section C: Key Sector Updates

26

Over the past few months, India's financial

sector has witnessed action, from the

passage of the GST bill to the decision of

merging the Union and Railway budgets and

the feat to achieve India's fiscal deficit target

et al. There has also been significant impetus

on two major fronts:

Ÿ Revision of criteria for second tranche of

capital infusion into PSU banks which

includes raising capital through public

offers and sale of non-core assets, to

assuage the PSU debt books.

Ÿ Decision to consolidate State Bank of

India and its associates, India's first ever

large-scale consolidation in the banking

history, creating a banking behemoth with

an asset strength of INR 37,000 bn.

Apart from these, there have been three

major developments described briefly below:

Nod to 100 per cent FDI in commodity

broking and other financial services

Soon after the recent monumental FDI

liberalisation decision in June, the

government took another path-breaking

decision to liberalise 100 per cent FDI in

financial services such as commodity

broking and 18 similar areas under Non-

Banking Financial Companies (NBFCs). This

decision is aligned with the government's

Ease of Doing Business endeavour and is

aimed at facilitating smoother entry into the

Indian market by doing away with the need of

seeking government approvals. With this,

FDI can now flow seamlessly into these

services under the automatic route, provided

they are regulated by a financial sector

regulator like the Reserve Bank of India (RBI)

and Securities and Exchange Board of India

(SEBI). Minimum capitalization norms have

also been eliminated. This pronouncement is

most certainly a boon for small and medium

enterprises (SMEs) and micro businesses in

non-urban areas as it promises to facilitate

faster sanction of loans with favourable

interest rates. It is also the second time that

the government has underscored its deeper

intent of uplifting the state of NBFCs in India -

- after it encouraged the sector in the Budget

2016-17 by appeasing the longstanding

demand of a 5 per cent deduction for

provision of bad and doubtful debts, hitherto

not allowed under the Income Tax Act.

Revised DTAA between India and Cyprus

Closely following the change to India-

Mauritius Treaty, the Union Cabinet recently

approved the signing of the revised double

taxation avoidance agreement (DTAA)

between India and Cyprus, after successfully

completing negotiations in June. The revised

DTAA, shall provide for source-based

taxation of capital gains on transfer of shares

instead of one based on residence. This is

considered as an improvement over the

earlier treaty which had led to distortion of

financial and real investment flows by

artificial diversion of investments from

countries of origin. Additionally,

grandfathering of investments made prior to

April 1, 2017, in respect of which capital

gains would be taxed in the country of

residence is aligned to India's treaty policy

for curbing tax evasion, round tripping and

base erosion or profit shifting. The amended

treaty has also paved the way for removal of

Cyprus from the list of 'Notified Jurisdictional

Areas', retrospectively from 2013.

Income Declaration Scheme 2016

Ministry closed its Income Declaration

Scheme (IDS) with a mop up of INR 652.5 bn

(USD 9.8 bn i.e. ~0.5 per cent of FY16 GDP),

marking tremendous success in India's

endeavour to combat black money in the

DEVELOPMENTS IN MINISTRY OF FINANCE

27

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

economy. A total of 64,275 persons declared

their unaccounted wealth under the window

to make the aggregate declared amount

largest ever for any such scheme in Indian

history.

According to Finance Minister, the figures are

likely to be revised upwards after the

tabulation of data is finalised. Out of the total

amount of INR 293.62 bn as tax and penalty

from these declarations, around INR 146.81

bn will flow into central government coffers in

the current financial year, while the remaining

amount will be collected in 2017-18. The

money would flow to the Consolidated Fund

of India and would be used for public

welfare.

Unprecedented success of the scheme

reveals a significant shift in the socio

economic mindset; the rush to embrace

amnesty opportunity reinforces the

government's relentlessness in ushering in

transparency. In alignment with the global

drive towards elimination of unaccounted

income and wealth (G20 transparency

measures), the success of IDS is a crucial

milestone for India in its fight against black

money.

As India's continuous negative growth in

exports since the last fiscal gets largely

contained, a gradual improvement in exports

performance is expected on account of

recovery in global demand and hardening

commodity prices. To boost exports and

attract investments, the Commerce Ministry

is taking several steps:

Ÿ Recommending that the Finance Ministry

raise tax holiday for start-ups from three to

seven years following vigorous requests

from start-ups

Ÿ Strengthening domestic industry and

boosting exports by leveraging

opportunities stemming from stimulus

programmes implemented by major

economies

Ÿ Setting-up two committees for expeditious

redressal of grievances on trade and

industry under headquarter and zonal

regional authority levels

Ÿ Setting-up a team of experts to examine

issues raised by the Global Innovation

Index and recommending ways to bolster

India's innovation ranking (presently 66 of

143 countries)

Ÿ Presenting proposals to the World Trade

Organisation (WTO) on ways to ease

trade in services, to leverage one of its

strongest competitive advantages

Additionally, the government has taken a

momentous step towards meeting its vision

of a transparent system by way of an end to

end Government e-Marketplace (GeM)

procurement system for goods and services

for government buyers. This comes as a

great relief to sellers as it obliterates the

tedious and time consuming tendering

process and cuts down transaction and

administrative costs. It shall also ensure

speedy payments by way of a 10-day

payment process mandate. This system

ensures transparency and reliability through

online authentication of suppliers and

government buyers using self-certification

and authentication through the Aadhaar, PAN

card and biometric attendance system.

DEVELOPMENTS IN MINISTRY OF COMMERCE AND INDUSTRY

Section C: Key Sector Updates

28

Bidding adieu to 5 year plans

As part of Modi government's resolve to

revise and upgrade institutions, the NITI

Aayog has been entrusted with a task of

working out a 15-year vision document,

which will encapsulate a roadmap for India's

development replacing the Nehruvian five-

year planning system followed for over six

decades. NITI Aayog has kick-started the

process with a four pronged focus – re-

engineering states' policies and aligning

them with the changing planning process at

the center, doing away with distinction

between plan and non-plan expenditure,

changing the financial year and merging the

rail and general budget.

The first vision document, will lay down

schemes, programmes and strategies to

achieve the long-term vision and come into

effect next fiscal. It will also be coterminous

with India's commitment to UNDP's 2030

sustainable development goals. Additionally,

a dashboard for monitoring, evaluation and

review of the implementation of vision

document shall be created. The first

Development Agenda shall be reviewed in

2019-29, in line with termination of 14th

Finance Commission, following which

reviews would be done every three years to

ensure alignment with changing financial

dynamics. Outcome-based monitoring of all

government programmes and ministries on a

yearly basis will also be undertaken. This

would help in keeping a tab on the progress

made. The new vision document shall cover

internal security and defence, hitherto not

covered under the 5 year plans. This

decision of marrying action on the ground

with planning is definitely a reason for cheer,

though, its success shall depend upon the

plan being translated into policy.

DEVELOPMENTS IN NITI AAYOG

29

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

India has witnessed a path-breaking thrust

and purpose in its foreign policy since the

formation of Modi government, with new

orientations that are less ambivalent, more

focused and more assertive. India's multi-

layered foreign policy has assumed center of

importance, starting from economic

diplomacy with a view to enhancing FDI

inflows, delicate and balanced management

of relations, defence diplomacy and energy

diplomacy covering coal, hydrocarbons,

solar, nuclear and renewable energy sectors.

A broad overview of Indian foreign policy in

past few months shows positive gains and

recognition of few challenges. India's

participation in international forums – G20

Summit (Hangzhou, China), BRICS Summit, th

14 Indo-Asean Summit and the East Asia

forum – were tremendously significant in

strengthening political, economic and

cultural ties with member countries.

Unlike previous G20 Summits, the summit

this time

had global

security as

one of its

main

agendas with Prime Minister Modi seizing the

opportunity to highlight India's challenges. 10Besides, Arvind Panagariya , India's chief

interlocutor at the summit, spoke about the

general sentiment against protectionism,

issue of excess capacity and resulting

international dumping; for which the

participating countries voiced their support

towards a multilateral approach. On the

sidelines of the G20 Summit, Indian Prime

Minister met Chinese President Xi Jinping

and held talks on bilateral conflicts between

the two countries over a raft of issues aimed 11at harmonising ties . China and India have

far more in common than differences and far

more areas of cooperation than competition.

India voiced its condemnation for the recent

terror attacks in the UN General Assembly,

receiving wide support from member

countries.

Highlighting key

economic

outcomes, the joint

declaration of the BRICS Summit, in Goa

marked satisfaction on operationalisation of

the New Development Bank (NDB) and the

Contingent Reserve Arrangement (CRA),

which augurs well for strengthening the role

of BRICS in the global economic order. With

the theme 'Building Responsive, Inclusive

and Collective Solutions', the BRICS nations

deliberated on security challenges,

strengthening economic ties and enhancing

connectivity and committed to lead by

example in implementation of the 2030

Agenda for Sustainable Development aimed

towards poverty eradication through a

balanced emphasis on economic, social and

environmental dimensions of sustainable

development. By inviting the BIMSTEC

countries to the summit, India clearly

revealed its stance for it's 'neighbourhood

first policy' and also played a sincere

interlocutor between the BRICS and

BIMSTEC as Brazil, Russia and South Africa

have very limited in-roads into the Bay of

Bengal littorals.

Drawing a link between Indian and South

African cultures during Prime Minister Modi's

four-nation visit to Africa, it became clear that

the visit was more than just diplomacy. Visits

to Mozambique, South Africa, Tanzania and

Kenya were accompanied by discussions on

securing lines of coal and natural gas,

funding capacity-building in energy

DEVELOPMENTS IN FOREIGN AFFAIRS

Section C: Key Sector Updates

30

10 Vice Chairman of NITI Aayog11Note: During his two day visit to China during the G20 Summit, PM Modi used the opportunity to meet many other world leaders. He met Australian Prime Minister Malcolm Turnbull, Deputy Crown Prince of Saudi Arabia Mohammad bin Salman, UK Prime Minister Theresa May,Turkish President Recep Tayyip Erdogan and Argentine President Mauricio Marci and held talks with them on key bilateral issues. He also informally met US President Barack Obama and French President Francois Hollande.

production and enhancing trade of pulses to

meet Indian demand shortfall. India has

diverse reasons to improve its ties with Africa

– sharing low-cost technologies and

pharmaceuticals, building solar and

renewable energy alliance and growing

markets for trade in goods. A stark 84 per

cent of India's imports from the Sub-Saharan

region comprise raw materials and non-

processed consumer goods.

PM Modi's visit to Vietnam marked

momentous forays into South-East Asia, a

10th anniversary in strategic partnership and th

a 45 anniversary of establishment of

diplomatic relations between the two

countries. India shares a special relationship

with Vietnam, ties that have deep roots in the

common struggle for liberation from foreign

rule and visit of Pandit Jawaharlal Nehru

following Vietnam's independence in 1954.

However, what makes the prime minister's

recent visit to Vietnam particularly significant

is the verdict on South China Sea by

Permanent Court of Arbitration at The Hague

in July, 2016, at behest of Philippines.

Although Vietnam was not party to the

dispute, it has substantial interests to harvest

energy and fishery in South China Sea has

been a source of concern. India's measured

statement post the verdict emphasised its

stance for freedom of navigation, maritime

security and openness of sea-lanes of

communication. The two countries also

signed 12 agreements in defence, capacity

building, training and human resource

development to cement their alliance.

Besides, India welcomed a host of foreign

dignitaries: President of Afghanistan, US

Secretary of State, President of Myanmar,

President of Egypt and Prime Minister of 12

Nepal paving the path towards stronger

internal diplomacy.

Top left to right: BRICS Summit 2016, Goa; External Affairs Minister Smt Sushma Swaraj meeting Chinese Foreign Minister Mr Wang Yi. PM Modi on a visit to Africa; G20 Summit, China; Sushma Swaraj speaking Bottom left to right:at the UN General Assembly

31

12 Minister of Foreign Affairs of Nepal, Minister of Foreign Affairs of Republic of Turkey, Foreign Affairs Minister of Maldives, Foreign Minister of China, Foreign Affairs and International Coorperation of the Democratic Republic of Congo, Deputy Prime Minister and Home Minister of Malaysia, Foreign Affairs Minister of Hungary also visited India during this period

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

DEVELOPMENTS IN MINISTRY OF DEFENCE

For India's rise as a global player, rapid

paced development of the defence industry

is a key imperative.

India's defence ties with the US gets big

boost

India and the US continued to strengthen

their defence partnership after the US

accorded India the status of 'Major Defence

Partner', announced during the visit of Indian

PM to Washington D.C in June 2016.

Bilateral defence ties received a further boost

with the visit of Indian Defense Minister

Manohar Parrikar to the US in end-August,

when both sides agreed on the significance

of Major Defence Partner framework to

facilitate innovative and advanced

opportunities in defence technology and

trade cooperation.

The Major Defence Partner classification

eliminates all previous barriers that come in

the way of defence strategic cooperation,

including co-production, co-development

projects and joint exercises. As part of the

framework:

Ÿ US will elevate defence, trade and

technology sharing with India to a level

commensurate with its closest allies and

partners;

Ÿ India will receive license-free access to a

wide range of dual-use technologies in

conjunction with steps that India has

committed to take to advance its export

control objectives; and

Ÿ US will continue to facilitate export of

goods and technology to support 'Make

in India' program and to develop a robust

defence industry

India signs agreement with France for 36

Rafale fighter jets

In a significant development towards

enhancing India's defence capabilities, India

concluded an inter-governmental agreement

(IGA) with France for the purchase of 36

Rafale fighter jets for USD 8.8 bn (INR 586.6

bn).

The agreement inked between the Defence

Ministers of the two countries on September

23, 2016 came after 17 months of intense

negotiations. It includes the delivery of

aircraft in fly-away condition, weapons,

simulators, spares, maintenance, and

performance based logistics support for five

years.

As part of the deal, French Giant Dassault

will begin aircraft deliveries after 36 months

and complete it in 67 months. From

development of Indian defence industry

perspective, the key features are:

Section C: Key Sector Updates

32

DEVELOPMENTS IN MINISTRY OF RAILWAYS

Rail – General Budget Merger

Ending a 92 year convention, the Union Cabinet recently

decided to merge the Railway budget with the General Budget

and agreed to advance the date of its presentation to February

such that its passage and presidential assent is completed

before end of the fiscal year.

This holds significance for the cash-strapped Indian Railways as

it will help save INR 100 bn annually by way of dividend

payments. In its report on restructuring of railways, an expert 13committee headed by Dr. Bibek Debroy made out a case for

abandoning a standalone railway budget. By subsuming it

within the Union budget, the railways will be equipped to raise

funds, from external agencies to invest in projects instead of

being restricted to the Indian Railway Finance Corporation to

mobilise funds. The merger may lead to a structural

transformation over the long run in terms of accounting and

operating on commercial principles like corporate bodies,

higher revenues, productivity and internal generation of funds

and better project implementation based on economic logic

rather than political considerations. However, it may also lead to

clarity issues over accounting items such as pension payments

and much will depend on the operational autonomy to the

railways. Additionally, the government's decision to advance the

budget shall lead to better planning and spending.

Ÿ 50 per cent offset clause under which French companies will invest half the value of contract

in India, which is expected to develop expertise domestically in the aerospace sector

Ÿ 74 per cent of the 50 per cent offset value should be exported from India. This is expected to

result in more than USD 3 bn (INR 200 bn) exports over the next seven years

Ÿ 6 per cent technology sharing component, which is being discussed with the Defence

Research and Development Organisation (DRDO)

3313 Dr. Debroy is permanent member of the NITI Aayog

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

DEVELOPMENTS IN MINISTRY OF ROAD TRANSPORT AND HIGHWAYS

DEVELOPMENTS IN MINISTRY OF POWER

Expediting highway projects and improving

port connectivity

Working to meet its target of awarding

25,000 km of road projects this fiscal, the

Ministry has kick-started a series of initiatives

to expedite major pending projects of the

National Highways Authority of India (NHAI).

These include, revamping the dispute

resolution mechanism and streamlining land

acquisition and regulatory clearances etc. in

coordination with other ministries. To revive

over 100 stalled NHAI projects languishing

due to poor performance of contractors,

public agitation, land acquisition, utility

shifting, delay in statutory clearances etc.,

the government has permitted one time fund

infusion under the public private partnership

(PPP) mode and rationalised compensation

to concessionaires for delays not attributable

to them. Additionally, regular meetings are

held with ministry officials, project

developers, state governments, contractors

and concessionaires etc. to ensure seamless

work on projects. The NHAI is planning to

take up 82 projects under the Bharatmala 14project to improve port connectivity and link

economic hubs to major and minor ports via

road and rail, which shall bring down

country's logistics costs considerably.

15The Power Ministry has been graded as one of the best performing ministries at the Centre

and it is evident that the recent initiatives have started bearing fruit. With an increased

availability of power resulting in fall in prices and gradual easing of transmission constraints,

the milestone of countrywide 24x7 supply seems achievable. The ministry has created a 16milestone through its UJALA initiative which has resulted in 55.7 million units of energy

savings, thereby reducing carbon emissions by over 45,000 tons.

To promote its objectives, the ministry has taken myriad steps:17

Ÿ Joint partnership with USAID to strengthen India's power grid to manage large-scale

integration of renewable energy

Ÿ Two funds of USD 1 bn each planned, to enable alternative financing options for stressed

power assets and renewable energy projects under the National Investment and

Infrastructure Fund (NIIF)18

Ÿ Nine unused gas-based power generation plants allotted 9.93 mmscmd (million standard

cubic metres a day) through a transparent and competitive reverse e-auction process

Section C: Key Sector Updates

34

14 Bharatmala Project is an umbrella scheme, launched for construction of roads along India's borders and coastal areas15 Key findings from an various surveys16 Unnat Jyoti by Affordable LEDs for all17 The US Agency for International Development18 Because of non-availability of fuel

Move towards non-conventional sources of

energy

India is set to launch its maiden tidal power

project under its vision of developing a 'blue

economy'. The Ocean Thermal Energy

Conversion (OTEC) project, which is planned

in Lakshadweep, is an outcome of three-and-

a-half decades of planning. This project has

an expected power generating capacity of 19200KW. A recent study conducted on

potential tidal and wave energy production in

India, revealed that India has a total

estimated tidal energy capacity of 8,000 MW.

With its coastline of around 2000 km, it is

well-placed to exploit ocean thermal energy

potential. According to CRISIL, there are four

operational tidal power plants in the world.

After France, Korea, Canada and China,

India would be the fifth country to generate

power from tidal waves. This is a step

towards the government's goal of providing

clean energy and holds potential for power

starved economy.

Additionally, the government has planned to

set up a grid-connected 1,000 MW wind

energy project which will supply power at a

price discovered through competitive

bidding and aims to encourage

competitiveness through scaling up of

project size and fulfillment of RPO 20

(renewable purchase obligation) of states

with scarce wind capacity. The centre has set

an ambitious target of achieving 175 GW of

power capacity from renewable energy

resources by 2022; of the 175 GW, 60 GW is

expected to come from wind power.

DEVELOPMENTS IN MINISTRY OF NEW AND RENEWABLE ENERGY

India is set to launch its maiden tidal power project under its vision of developing a 'blue economy'.

35

19 Study on Tidal & Waves Energy in India: Survey on the Potential & Proposition of a Roadmaphttp://www.ireda.gov.in/writereaddata/AFD_Tidal.pdf20 Non Solar Renewable Purchase Obligation

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

DEVELOPMENTS IN MINISTRY OF LAW AND JUSTICE

DEVELOPMENTS IN MINISTRY OF CORPORATE AFFAIRS

In the last quarter, the main thrust of Ministry

has been towards ensuring minimum

government maximum governance and

promoting ease of doing business.

An expert committee set up to examine the

Specific Relief Act, 1963 submitted its report

to the Minister recommending modifications

in the Act. The committee provided

guidelines for reducing the discretion

granted to Courts while granting

performance and injunctive reliefs.

The committee constituted to examine

Prevention of Corruption (Amendment) Bill,

2013 submitted its report to Rajya Sabha on

August 12, 2016. The Bill seeks to amend the

1988 Act to include (a) a bribe giver who

reports the matter to the police within seven

days may not be penalized, and (b) prior

sanction for investigating a public servant

must be given by the government instead of

the Lokpal.

The Lokpal and Lokayuktas (Amendment)

Bill, 2016 was introduced and passed in the

Lok Sabha on July 27, 2016. The Bill

retrospectively amends the Lokpal and

Lokayuktas Act, 2013 in relation to

declaration of assets and liabilities by public

servants.

As an initiative towards digital India and e-

governance, web portal named Legal

Information Management & Briefing System

(“LIMBS”) has been introduced for centrally

monitoring cases of Union of India pending

in various Courts and Tribunals.

Novel Mediation and Conciliation rules

Termed a 'giant leap' for mediation in India,

the Corporate Affairs Ministry has put in

place a new framework for mediation and

conciliation. This could soon become the

chosen alternative dispute resolution (ADR)

mechanism for resolving commercial

disputes in the country. Under this:

1. The regional director (RD) shall prepare

panel of experts, eligible to be appointed as 21

mediators

2. The Mediator or conciliator shall attempt to

facilitate voluntary resolution of disputes by

communicating views of each party to the

other; assisting them in identifying issues,

reducing misunderstandings and clarifying

priorities

3. The conciliation process shall be

completed within a period of three months

from date of appointment of experts

4. Any party aggrieved by the

recommendation may file objections to the

central government/tribunal/appellate tribunal