indonesia business and investment dialoguethe finest from the amazon of the sea indonesia business...

TRANSCRIPT

THE FINEST FROM THE AMAZON OF THE SEA

Indonesia Business and Investment DialogueASEAN JAPAN CENTRE

March 2017

Corporate Presentation

Delivering Integrated Fishery Solutions

CORPORATEPROFILE

WORLD’S FISHERY PRODUCTION & TRADE | INDONESIA FISHERY INDUSTRY

FAVORABLE ECONOMY ATMOSPHERE | EXPECTATION ON JAPAN

WHY INVEST DPUM | THE TRANSFORMATION

INTEGRATED BUSINESS MODEL| PEERS BAROMETER

AWARD & CERTIFICATIONS |

SHAREHOLDER |

WORLD’S FISHERY PRODUCTION & TRADE

CORPORATE PRESENTATION 2

4.7%

5.3%

5.6%

6.3%

17.7%

RUSIA

INDIA

USA

INDONESIA

CHINA

Source: FAO, 2012

FISHERY COMMODITIES EXPORT• Indonesia occupies position 11 with the export figure of

2.1% from the total export of USD140 billion.• Indonesia's export figure is lower due to transshipment

and impact the export figures are unrecorded.

2.6%

4.1%

4.5%

5.8%

6.3%

13.0%

INDONESIA

RANK 6TH -10TH COUNTRIES

USA

VIETNAM

THAILAND

NORWAY

CHINA

Source: FAO, 2012

WORLD'S CAPTURE PRODUCTION• Indonesia’s 2nd largest capture production

country.• In 2012, Indonesia contribute 6,3% from 93,4

million tonnage capture production in the world

INDONESIA FISHERY INDUSTRY

CORPORATE PRESENTATION 3

2010 2011 2012 2013 2014 2015

SEAWEED FISH FARMER CAPTURE TOTALID PRODUCTION (MILLION TON/YEAR)

2010 2011 2012 2013 2014 2015 %CAGR

SEAWEED 3.9 5.2 6.5 9.3 10.1 10.8 22.5FISH FARMER 2.4 2.8 3.2 4.0 4.3 4.4 13.3CAPTURE 5.4 5.7 5.8 6.1 6.5 6.5 3.9TOTAL 11.7 13.6 15.5 19.4 20.8 21.7 13.2

GOVT SUPPORT1. Prohibition on foreign construct vessels to operate2. Prohibition to harvest on breeding ground and spawning ground3. Prohibition on any open sea transshipment, ensuring all fisheries to be processed locally4. Presidential Decree No. 7 Year 2016 related economic acceleration in maritime sector5. Open market for investment in cold storage and fishery process.

2010 2011 2012 2013 2014 2015

ID DEMAND 2010 2011 2012 2013 2014 2015 %CAGRKG PERCAPITA/YEAR 30.5 32.3 33.9 35.2 38.1 41.1 6.2

Source: ID Marine Affair & Fisheries Minister

Source: ID Marine Affair & Fisheries Minister

FAVORABLE ECONOMY ATMOSPHERE 2017

CORPORATE PRESENTATION 4

8.34 8.22

7.79

2014 2015 2016

1.58 1.79 2.00

2014 2015 2016

5.94 6.18

5.50

2014 2015 2016

114

122 125

2014 2015 2016

UNEMPLOYEMENT RATE (%) PERCENTAGE OF POOR REGIONAL MIN. WAGES (MILLION)

53.27 37.04

50.77

2014 2015 2016

3.60 3.35

1.97

2014 2015 2016

5,227

4,593

5,416

2014 2015 2016

12,383

13,788 13,05

1

2014 2015 2016

85 3,016

90,161

Jul-16 Aug-16 Sep-16

CONSUMER INDEX RATE INFLATION RATE (%) EXCHANGE RATE (USD/IDR)

CRUDE OIL PRICE (US$/BBL) MARKET SENTIMENT (IHSG) T. A. REDEMPTION FEE (Rp, BILLION)

Source: Bloomberg & Badan Pusat Statistik, September 2016

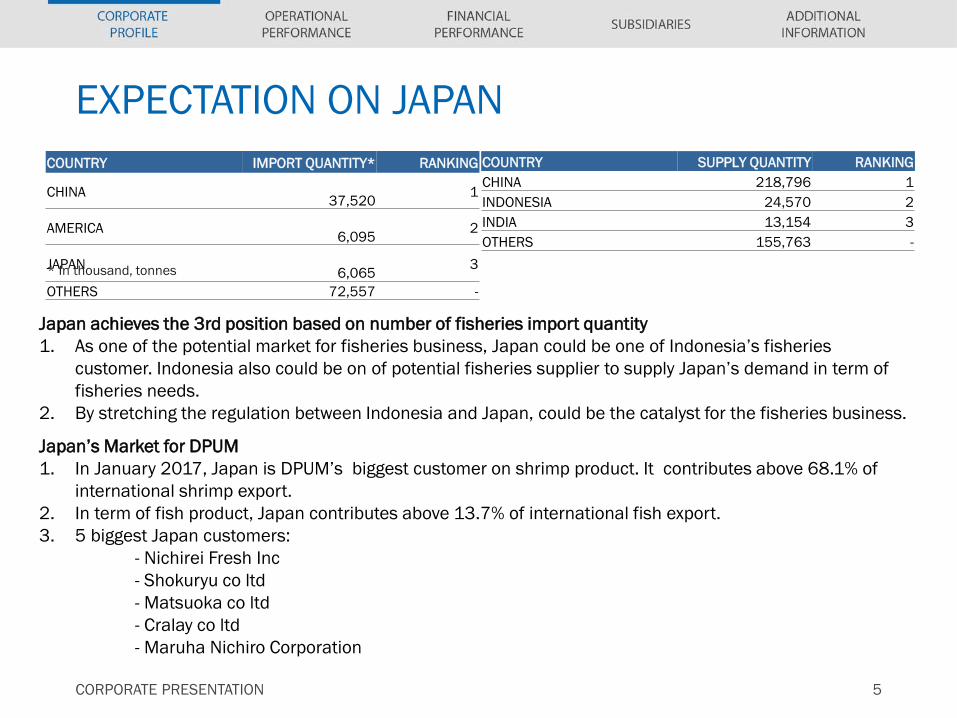

EXPECTATION ON JAPAN

CORPORATE PRESENTATION 5

COUNTRY IMPORT QUANTITY* RANKING

CHINA 37,520 1

AMERICA 6,095 2

JAPAN 6,065 3

OTHERS 72,557 -* In thousand, tonnes

Japan achieves the 3rd position based on number of fisheries import quantity1. As one of the potential market for fisheries business, Japan could be one of Indonesia’s fisheries

customer. Indonesia also could be on of potential fisheries supplier to supply Japan’s demand in term of fisheries needs.

2. By stretching the regulation between Indonesia and Japan, could be the catalyst for the fisheries business.

COUNTRY SUPPLY QUANTITY RANKINGCHINA 218,796 1INDONESIA 24,570 2INDIA 13,154 3OTHERS 155,763 -

Japan’s Market for DPUM1. In January 2017, Japan is DPUM’s biggest customer on shrimp product. It contributes above 68.1% of

international shrimp export.2. In term of fish product, Japan contributes above 13.7% of international fish export.3. 5 biggest Japan customers:

- Nichirei Fresh Inc- Shokuryu co ltd- Matsuoka co ltd- Cralay co ltd- Maruha Nichiro Corporation

WHY INVEST DPUM

CORPORATE PRESENTATION 6

External FactorsBig Economy A member of G20 countriesSolid Economy IMF estimate ±6.64% CAGR in 2017-2020Big Population Fourth largest in the worldBiggest Achipelago Approximately ±65 of total IDs territory is marine area with 17.000 islandsStrategic Geographical Marine Indonesia is a tropical archipelago and home of two oceans (Pacific & Indian) Potential Resources Indonesia is the 2nd largest capture production country. Govt Deregulation Prohibition on foreign construct vessels to operate in Indonesia's marine.

Internal FactorsStrong Revenue Growth CAGR 2013-2016 CAGR 90.5% Good Profitability Average net margin ±12%Good Product Quality Certificate of Registration from Food and Drug Administration (FDA) of USStrong Resource Base Indonesia’s water, the amazon of the sea.Sustainable Business The renewable resources ensure the sustainability of the business.Long Track Record Having been running the fisheries business since 2005.Experienced Management Having expirience in related business ±12 years.

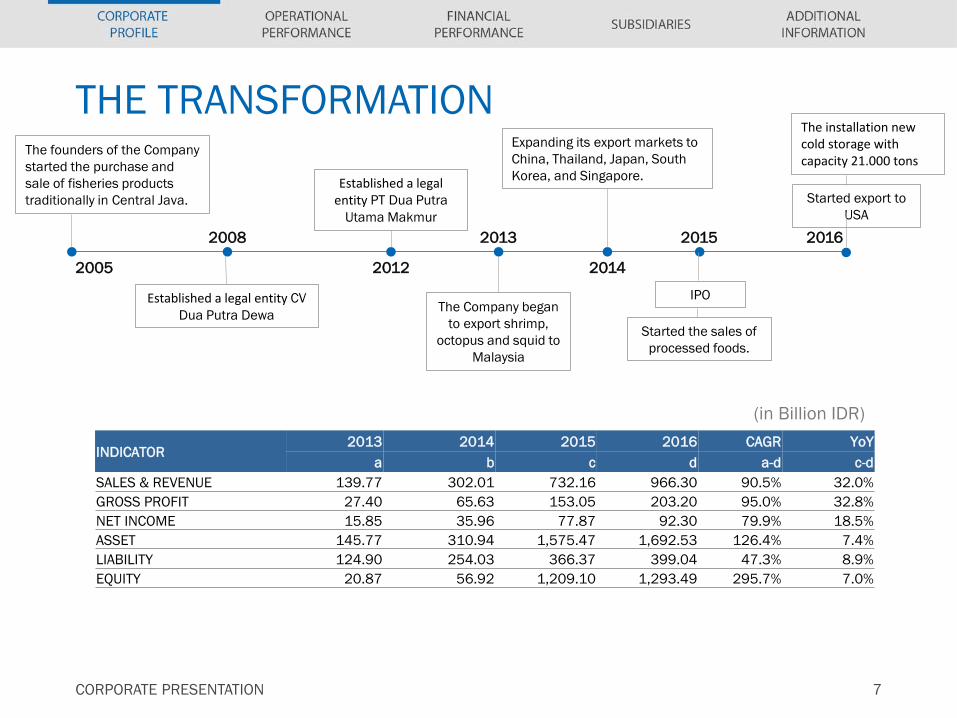

THE TRANSFORMATIONThe founders of the Company started the purchase and sale of fisheries products traditionally in Central Java.

2005

Established a legal entity CV Dua Putra Dewa

2008

Established a legal entity PT Dua Putra

Utama Makmur

2012

The Company began to export shrimp,

octopus and squid to Malaysia

2013

Expanding its export markets to China, Thailand, Japan, South Korea, and Singapore.

2014

2015

Started export to USA

The installation new cold storage with capacity 21.000 tons

IPO

2016

CORPORATE PRESENTATION 7

Started the sales of processed foods.

(in Billion IDR)

INDICATOR2013 2014 2015 2016 CAGR YoY

a b c d a-d c-dSALES & REVENUE 139.77 302.01 732.16 966.30 90.5% 32.0%GROSS PROFIT 27.40 65.63 153.05 203.20 95.0% 32.8%NET INCOME 15.85 35.96 77.87 92.30 79.9% 18.5%ASSET 145.77 310.94 1,575.47 1,692.53 126.4% 7.4%LIABILITY 124.90 254.03 366.37 399.04 47.3% 8.9%EQUITY 20.87 56.92 1,209.10 1,293.49 295.7% 7.0%

INTEGRATED BUSINESS MODEL

CORPORATE PRESENTATION 8

FISHERMANPARTNERSHIP

FISH SUPPLY

SHRIMP SUPPLY

CONTRACT SUPPLIERS

FISH FARMER SME

PROCESSING PLANT

COLD STORAGE DISTRIBUTION

IMPORT

EXPORT

PEERS BAROMETER

CORPORATE PRESENTATION 9

INDICATOR DUA PUTRA UTAMA MAKMUR TBK

DHARMA SAMUDERA FISHING INDONESIA TBK

CENTRAL PROTEINA PRIMA TBK SEKAR LAUT TBK

ESTABLISHED 2012 1973 1980 1966

CHANNEL

Malaysia, Thailand, Vietnam, China, Japan,

Taiwan, Singapore, South Korea, India, Bahrain,

USA, Australia

China, Canada, Rusia, Vietnam, Korea, Europe,

USAEurope, Japan, USA Import (data is n/a)

PRODUCT

Fish Frozen, Shrimp Frozen, Seafood Value

Added Custom, Seafood Processed

Tuna, Fish Fillet, Octopus, Cuttlefish, others

Shrimp Processed, Shrimp Feed and others

feed

Canning, Codiment, crakers and cereals

COLD STORAGE 25.000 T Yes (data is n/a) Yes (data is n/a) N/A

FISHERMAN PARTNERSHIP Yes No No No

AWARD & CERTIFICATIONS

CORPORATE PRESENTATION 10

Food and Drug Administration (FDA) Registry

The United States FDA

Certificate of Implementation of Hazard Analysis & Critical Control Point

(HACCP)Frozen Fish, Shrimp & CephalopodMarine Affair & Fisheries Minister

Quality Management ISO 9001:2008

SHAREHOLDER

CORPORATE PRESENTATION 11

PT DUA PUTRA UTAMA MAKMUR TBKTOTAL SHARE: 4,175,000,000

PT PANDAWA INVESTAMA UOB KAY HIAN PTE LTD PUBLIC

48.29% 22.32% 29.39%

PUBLIC OWNERSHIP DISTRIBUTION

Source: Company Data, December, 2016

DOMESTICMESA & MESOP 0.40%RETAIL 28.99%

OPERATIONALPERFORMANCE

PROCESSING PLANT | PROCESSED PRODUCTS| OPERATIONAL HIGHLIGHTS

ONE OF THE LARGEST PROCESSING PLANT

CORPORATE PRESENTATION 13

INDICATOR 2016CAPACITYCOLD STORAGE (UNIT) 3CAPACITY COLD STORAGE (TON) 25,000 VESSEL (UNIT) 0PRODUCTION CAPACITY (TON/DAY) 30 FACILITY (UNIT)CONVEYOR BELT SYSTEM 9 VACCUM PACK MACHINE 1 METAL DETECTOR 1 CONTACT FREEZER 9 ICE FLAKE MACHINE 4 TUNNEL FREEZER 7 SPIRAL 1 FRYER MACHINE 1

VALUE ADDED SEAFOOD – PROCESSED PRODUCTS

CORPORATE PRESENTATION 14

Nobashi BreadedShrimp

CookedShrimp

CuttlefishSashimi

Sushi Ebi

Tempura Breaded fish

Fillet fishCrab Cake

Calamari

OPERATIONAL HIGHLIGHTS

CORPORATE PRESENTATION 15

4Q15 4Q16 ∆ % YoY OPERATIONAL 12M15 12M16 ∆ % YoY11,384,442 8,333,864 (26.8) GROUP 30,166,298 32,709,475 8.4 11,138,475 7,745,201 (30.5) FISH (KG) 29,290,235 31,326,194 7.0

245,967 588,663 139.3 SHRIMP (KG) 876,063 1,383,281 57.9 92 125 36.0 YIELD FISH (IDR/KG) 20,217 25,004 23.7

4,817 2,128 (55.8) YIELD SHRIMP (IDR/KG) 159,797 132,306 (17.2)10,985,914 7,722,086 (29.7) DOMESTIC 28,838,398 28,040,286 (2.8)10,975,095 7,406,016 (32.5) FISH (KG) 28,823,487 27,583,157 (4.3)

10,819 316,070 2,821.5 SHRIMP (KG) 14,911 457,129 2,965.8 398,529 611,778 53.5 INTERNATIONAL 1,327,900 4,669,189 251.6 163,381 339,185 107.6 FISH (KG) 466,748 3,743,037 701.9 235,148 272,593 15.9 SHRIMP (KG) 861,152 926,152 7.5

4Q15 4Q16 CONTRIBUTION 12M15 12M16100.0% 100.0% GROUP 100.0% 100.0%

96.5% 92.7% DOMESTIC 95.6% 85.7%3.5% 7.3% INTERNATIONAL 4.4% 14.3%

FINANCIALPERFORMANCE

INCOME STATEMENT SUMMARY | OPERATING REVENUE |

BALANCE SHEET SUMMARY | CASH FLOW SUMMARY | CASH & NET GEARING

INCOME STATEMENT

CORPORATE PRESENTATION 17

CONSOLIDATED INCOME STATEMENT (in Billion IDR)

4Q15 4Q16 ∆ % YoY INDICATOR 12M15 12M16 ∆ % YoY

245.40 316.24 28.9 SALES AND REVENUE 732.16 966.30 32.0 (202.95) (274.22) 35.1 COST OF SALES & REVENUE (579.11) (763.11) 31.8

42.44 42.01 (1.0) GROSS PROFIT 153.05 203.20 32.8 (7.47) (23.62) 216.1 GENERAL & ADM (15.62) (58.71) 275.8 (8.60) (8.44) (1.8) FINANCE CHARGES (23.69) (34.55) 45.8

(15.52) 2.41 (115.5) OTHERS (EXPENSES)/INCOME (21.73) 9.83 145.3 10.84 12.35 13.9 OPERATING PROFIT 92.00 119.77 30.2

7.97 (1.95) (124.5) TAX (14.14) (27.47) 94.3 18.81 10.40 (44.7) NET INCOME 77.87 92.30 18.5

4Q15 4Q16 RATIO 12M15 12M16

17.3% 13.3% GROSS PROFIT MARGIN 20.9% 21.0%4.4% 3.9% OPERATING PROFIT MARGIN 12.6% 12.4%7.7% 3.3% NET MARGIN 10.64% 9.55%

OPERATING REVENUE SEGMENT

CORPORATE PRESENTATION 18

(in Billion IDR)

4Q15 4Q16 ∆ % YoY REVENUE SEGMENT 12M15 12M16 ∆ % YoYBY REGION & PRODUCT

194.79 247.23 26.9 DOMESTIC 576.96 648.60 12.4 193.58 214.65 10.9 FISH 575.36 598.69 4.1

1.21 32.58 2,594.2 SHRIMP 1.60 49.91 3,022.7 50.61 69.01 36.4 INTERNATIONAL 155.20 317.70 104.7

6.44 21.73 237.6 FISH 16.81 184.60 998.2 44.17 47.29 7.1 SHRIMP 138.39 133.11 (3.8)

245.40 316.24 28.9 TOTAL 732.16 966.30 32.0

4Q15 4Q16 REVENUE CONTRIBUTION 12M15 12M16BY REGION

79.4% 78.2% DOMESTIC 78.8% 67.1%20.6% 21.8% INTERNATIONAL 21.2% 32.9%

100.0% 100.0% TOTAL 100.0% 100.0%BY PRODUCT

81.5% 74.7% FISH 80.9% 81.1%18.5% 25.3% SHRIMP 19.1% 18.9%

100.0% 100.0% TOTAL 100.0% 100.0%

BALANCE SHEET

CORPORATE PRESENTATION 19

CONSOLIDATED BALANCE SHEET (in Billion IDR)

*Current assets decerease 32.2% due to cash uses for aquisition of fixed assets IDR376.58Billion

INDICATOR FY15 3Q16 ∆ % 4Q16 ∆ % CURRENT ASSET 955.28 647.47 (32.2) 701.13 (26.6)NON CURRENT ASSET 620.18 990.35 59.7 991.40 59.9 TOTAL ASSET 1,575.47 1,637.83 4.0 1,692.53 7.4 CURRENT LIABILITY 191.38 168.16 (12.1) 232.78 21.6 NON CURRENT LIABILITY 175.00 186.75 6.7 166.26 (5.0)TOTAL LIABILITY 366.37 354.91 (3.1) 399.04 8.9 TOTAL EQUITY 1,209.10 1,282.92 6.1 1,293.49 7.0 TOTAL LIABILITY & EQUITY 1,575.47 1,637.83 4.0 1,692.53 7.4

CONTRIBUTIONTOTAL ASSET 100.0% 100.0% 100.0%TOTAL LIABILITY 23.3% 21.7% 23.6%TOTAL EQUITY 76.7% 78.3% 76.4%

GROUP CASH & NET GEARING

CORPORATE PRESENTATION 20

DEBT STRUCTURE

COVENANT

√ NET GEARING MAX 2.0 TIMES (12M16: 0.2 TIME)

√ NET WORTH DECREASE <25% (12M16 : INCREASE 18.5%)

√ DER MAX 3 0 TIMES (12M16 : 0.2 TIME)

(in Billion IDR)

598.

8

39.1

40.8

239.

8

271.

4

309.

7

1,20

9.1

1,28

2.9

1,29

3.5

(0.3)

0.2 0.2

(0.9)

(0.7)

(0.5)

(0.3)

(0.1)

0.1

0.3

1.0

201.0

401.0

601.0

801.0

1,001.0

1,201.0

1,401.0

FY15 3Q16 4Q16

CASH FINANCIAL DEBT EQUITY NET GEARING

46.6%53.4%

SHORT TERM LONG TERM

ADDITIONALINFORMATION

TARGET

TARGET

CORPORATE PRESENTATION 22

INDICATOR FY2016 FY2017 ∆ % YoYFINANCIAL (IDR, Billion)SALES AND REVENUE 966.30 1,432.49 48.2 GROSS PROFIT 203.20 300.57 47.9 OPERATING PROFIT 119.77 221.27 84.7

NET INCOME 92.30 154.71 67.6

ASSET 1,692.53 1,906.98 12.7 LIABILITY 399.04 478.31 19.9 EQUITY 1,293.49 1,428.67 10.5 OPERATIONAL PRODUCTION (KG) 32,709,475 35,123,040 7.4

Head Office

Jl. Raya Pati Juwana Km. 7Desa Purworejo Rt.01 Rw. 05Kecamatan Pati, Kabupaten PatiJawa Tengah 59111 - IndonesiaTel : +62-21 4199011 Fax : +62-21 4199010Email : [email protected]

Investor Relations

Nariba Office Suites, 6th floorJl. Mampang Prapatan Raya No. 39Jakarta Selatan 12790 - IndonesiaTel : +62-21 7919990 Fax : +62-21 7991529Email : [email protected]

www.duaputra.com