indonesia industry focus indonesian multi-finance … the auto penetration ... other developing...

TRANSCRIPT

ed-CK / sa- MA, PY

Bridging gaps with the under-banked Multi-finance companies are capillaries of the financial

system that channels funds to the unbankable population;

crucial to financial inclusion Fragmented industry with the largest player capturing 8%

of loan market share; most big players are backed by banks

or auto dealers Auto sales, the main driver of growth; multi-purpose

financing gaining popularity; leasing and factoring may

resurface with commodity prices recovering Undemanding valuations given high ROE in this high risk-

high return segment; BFIN is our preferred listed proxy;

stock liquidity is however limited

Proxy to the unbankable population. Indonesia has among the lowest bankable population in the world at 36% of the country’s adult population. The government’s push towards improving financial inclusion opens opportunities to the multi-finance companies which are able to meet the financing needs of the lower income households. These companies typically serve the non-banking population in Indonesia, providing them with access to financing. Execution and monitoring mechanisms are manual and labour intensive but have proven to be effective. The risk profiles of multi-finance companies are higher than banks but the returns are also more lucrative, judging from the well-managed multi-finance companies we have screened.

Consumer financing is its driving force; new avenues opening

up; potential M&A opportunities. While the multi-finance companies largely focus on consumer financing, the regulators are gradually opening more financing options. In 2014, Otoritas Jasa Keuangan (OJK) officially allowed multi-finance companies to finance multi-purpose loans, refinancing and infrastructure loans. Multi-finance companies used to see leasing for heavy equipment as a growth driver but that has since declined as commodities’ prices slumped three years ago. OJK is also working towards bridging the gap with banks in terms of regulations. We believe this move will gradually mitigate risks to the multi-finance companies as an investment option, and perhaps, also an avenue to consolidate the currently fragmented sector as well as potential M&A opportunities.

Recovery in commodity prices and auto sales a positive boost;

regulatory changes could add fuel to auto sales. Commodity prices have held up quite well to date and are expected to boost purchasing power in the near term. Receivable growth has also accelerated to +7.2% in February 2017 (vs -1% in January 2016). We expect the flow-through of this positive development to be gradual. The visible turnaround for the auto industry would bode better for the multi-finance companies. The relaxation of down payment rules should also add fuel to auto sales. We expect financing growth to recover to 8% in 2017, driven by auto financing.

BFIN is a good listed proxy; opportunities among the top 20

multi-finance companies. Selected listed multi-finance companies are attractive; BFIN (BUY, TP Rp5,000) is our pick. The main concern investors may have is the limited stock liquidity. We highlight ADMF, BCAF, and MTF, which are subsidiaries to banks, and ASDF (4W market leader) and FIF (2W market leader), which are Astra-related companies – these have strong parent companies. We believe they are opportunities among smaller multi-finance companies, both organic and inorganic, in this current operating environment.

JCI : 5,616.50

Analyst Sue Lin LIM +65 8332 6843 [email protected]

Benedictus Agung SWANDONO +6221 3003 4935 [email protected]

STOCKS/COMPANIES

* Not listed Source: DBS Bank, DBSVI, Bloomberg Finance L.P. Closing price as of 13 Apr 2017

Multi-finance companies: Market share of top 20 players

Note: Based on outstanding on balance sheet net receivables. Data represents 2015 numbers Source: Infobank, DBS Bank, DBSVI

Multi-finance companies: Financing activities y-o-y growth

Source: OJK, BI, DBSVI

8%7% 7% 7%

5%

4%

3%3% 3% 2% 2% 2% 2% 2% 2% 2% 1% 1% 1% 1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

ASD

F

FIF

AD

MF

C.J

. Pow

er

Oto

M

TAFS

Dip

o S.

F

BFIN

Sum

mit

O.F

Man

diri

T.F

Indo

mob

il F,

I

Buss

an A

.F

CFI

N

BCA

F

CIM

B F.

Mits

ui L

easi

ng

Orix

I.F

Sury

a A

rtha

N.F

MPM

F.

WO

MF

26.4%

4.1%

31.0% 32.3%

23.1%

15.2%

5.2%

-0.8%

6.7%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

-

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013 2014 2015 2016Total Financing Financing growth y-o-y

Rp bn % growth

DBS Group Research . Equity 18 Apr 2017

Indonesia Industry Focus

Indonesian Multi-finance Companies

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price

Performance (%)

Rp US$m Rp 3 mth 12 mth Rating

BFI Finance Ind (BFIN( 4,100 493 5,000 17.1 57.7 BUY Clipan Finance (CFIN) 298 89.4 300 15.5 13.7 HOLD Adira Dinamika Multifinance (ADMF) 6,625 471 Not Rated 4.0 105.0 N/A Astra Sedaya Finance (ASDF)* - - Not Listed N/A N/A N/A BCA Finance (BCAF)* - - Not Listed N/A N/A N/A Federal International Finance (FIF)* - - Not Listed N/A N/A N/A Mandiri Tunas Finance (MTF)* - - Not Listed N/A N/A N/A

Industry Focus

Page 2

Table of Contents

Investment Summary 3

Opportunities with the unbankable population 4

A. Financial inclusion, a key to growth 4

B. The multi-finance industry landscape 5

C. Prospects for the multi-finance industry 9

Key drivers to the multi-finance industry 11

A. Automotive industry 11

B. Leasing and heavy equipment 13

Key players and market position 15

A. 4-wheeler market 18

B. 2-wheeler market 19

Regulatory framework for multi-finance companies 20

Valuation and recommendation 23

A. Valuation tables 24

B. P/BV Bands 25

Company Guides 27

BFI Finance (BFIN) 28

Clipan Finance (CFIN) 36

Company Profiles (Non-rated) 44

Adira Dinamika Multifinance (ADMF) (Non-rated; Listed) 45

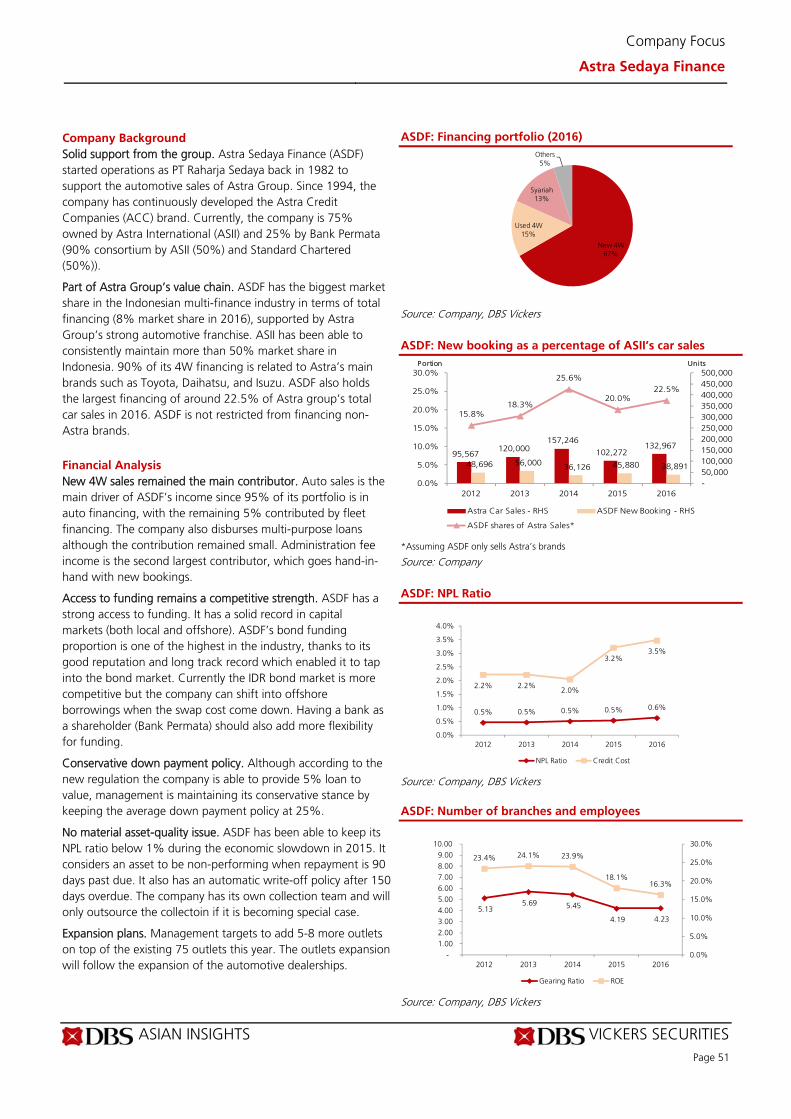

Astra Sedaya Finance (ASDF) (Non-rated; Not listed) 50

BCA Finance (BCAF) (Non-rated; Not listed) 55

Federal International Finance (FIF) (Non-rated; Not listed) 60

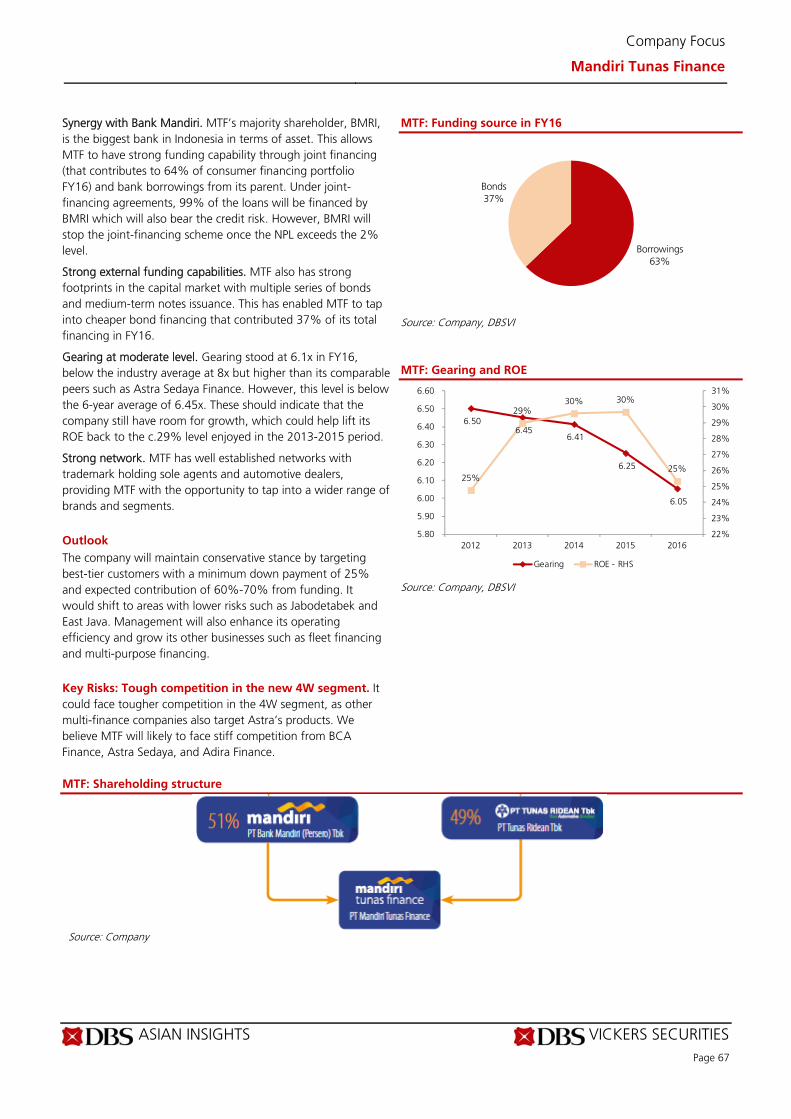

Mandiri Tunas Finance (MTF) (Non-rated; Not listed) 65

Industry Focus

Page 3

Investment Summary

Multi-finance companies – bridging gaps with the under-banked. Indonesia has among the lowest bankable population in the world at 35.9% of the country’s adult population. Banking with the unbankable population includes looking at instances in micro lending, especially in the rural areas. The initiation of the branchless banking agenda has addressed this to some extent. But beyond that, the need to further reach out to the unbankable population lies in the hands of the multi-finance companies which cover both urban and rural areas. The government’s push towards improving financial inclusion opens opportunities for the multi-finance companies which are able to meet the financing needs of the lower income households. Multi-finance companies are licensed to offer a range of services, including leasing, consumer financing (bulk of its business), credit card financing and factoring. But unlike banks, they are not allowed to accept deposits. Similar to banks, multi-finance companies are governed by Otoritas Jasa Keuangan (OJK), the regulatory arm of the Minister of Finance (MoF).

Turning optimistic; three critical factors to watch. We expect an improvement in financing demand in 2017. The Multi-finance Company Association (APPI/Asosiasi Perusahaan Pembiayaan Indonesia) recently announced its forecast of 10% financing growth for 2017 on the back of an improving economy and improved commodity price trends. We identified three critical factors that will drive multi-finance companies’ earnings in 2017: (1) lower credit cost, (2) higher NIM and better growth, and (3) well controlled expenses. Note that some multi-finance companies had to accelerate provisions as they had to change how NPLs were classified following stricter regulations to streamline recognition similar to the banks; this caused provisions to be higher in 2016. We expect NIM expansion in 2017 on the back of lower funding cost as the banks have started to price down their loans, which means multi-finance companies now enjoy lower funding costs via bank borrowings (one of the main sources of funding for multi-finance companies). Meanwhile, asset yields are expected to stay constant as the interest rates offered to the customers are not sensitive towards the change in interest rate environment. In addition, operating costs are expected to be flat as the companies have not been aggressive in expanding their service points.

Auto industry recovery, key driver for multi-finance companies’ growth. With consumer financing dominating the multi-finance companies’ loan portfolio, the auto industry would be the key growth driver. Leasing growth relies mainly on heavy equipment financing which in turn unfortunately is dependent on commodity prices. Both these segments have been in the doldrums in the past two years. The near-term exuberance for

commodity prices might not sustain throughout the year but we believe the positive impact should be gradually felt. We expect the auto industry to pick up in 2017, boosting the growth prospects of the multi-finance companies.

Long-term potential, especially for 4W. The auto penetration rate in Indonesia remains one of the lowest in the region. Based on data by Badan Pusat Statistik (BPS)/ Indonesian Statistics Centre and automotive association, in 2015 there are only 13.7m cars and 99m motorcycles outstanding on Indonesian roads (vs its population of 250m). The penetration rate for 4-wheeler vehicles (4W) is a mere 5%, lower than other developing countries like Malaysia and Thailand. However, 2-wheeler vehicles’ (2W) penetration is much higher at 40% in 2015.

Fragmented industry; obvious market leaders. There are a total of 201 multi-finance companies, with the top 20 companies commanding 65% (financing) market share. Each of them caters to its own niche by specialising in several categories such as products financed (4W, 2W, heavy equipment (HE), etc) and by geographical reach. Multi-finance companies are typically owned by banks (both domestic and foreign), brand-holding sole agents (Agen Tunggal Pemegang Merek, ATPM) of cars and foreign principals of car makers (e.g. Astra International), and a few which are family/individual-owned. The strong multi-finance companies are those affiliated to banks and ATPMs. The largest player, Astra Sedaya Finance (ASDF) has only 8% market share, marginally higher among the top 6 multi-finance companies, which indicates how fragmented the industry is.

Top players have better profitability metrics than banks. Compared to banks, multi-finance companies generate better returns. Generally, the major multi-finance players record higher ROE and ROA as the benefits of higher asset yield outweigh the negatives of higher cost of funds, operating cost, and credit cost. The higher asset yield is due to the ability to tap the unbankable market, an advantage that banks lack. But it requires heavy infrastructure and labour to tap into this market while its elevated credit cost is due to the higher risk profile of the customers compared to banks.

Opportunities among multi-finance companies. We believe they are opportunities among the multi-finance companies, both organic and inorganic, in this current operating environment. Among the listed players, our pick would be BFIN. Indirect plays would be via banks which own the larger multi-finance companies such as BCAF (100% owned by Bank Central Asia, BBCA) and ADMF (Bank Danamon, BDMN).

Industry Focus

Page 4

Opportunities with the unbankable population

Indonesia has among the lowest bankable population in the world at 35.9% of the country’s adult population. Banking with the unbankable population includes looking at instances in micro lending, especially in the rural areas. The initiation of the branchless banking agenda has addressed this to some extent. But beyond that, the need to further reach out to the unbankable population lies in the hands of the multi-finance companies which cover both urban and rural areas. The government’s push towards improving financial inclusion opens opportunities for the multi-finance companies which are able to meet the financing needs of the lower income households. A. Financial inclusion, a key to growth The state of financial inclusion in Indonesia: Indonesia has lagged behind other developing countries in terms of financial inclusion. A survey conducted by World Bank in 2014 indicated that only 36% of the adult population has a formal account in a financial institution. This is lower than the average of East Asia and Pacific countries (69%), average of lower middle- income countries (42%), and even ASEAN peers such as Thailand (78%). In terms of lending, the statistics is even less encouraging. Only 13% of the adult population borrowed from financial institutions. However it is quite surprising that 42% of these people prefer to borrow money from family or friends. This indicates that there are plenty of untapped markets for lending in Indonesia. Poor infrastructure and education are few reasons of why these markets remain isolated from the modern world. Indonesia: Banking penetration rate

*The numbers are as % of adult population (age 15+) Source: Little Data Book on Financial Inclusion 2015, DBS Bank, DBSVI

Indonesia: Many are excluded from the financial system

*The numbers are as % of adult population (age 15+) Source: Little Data Book on Financial Inclusion 2015, DBS Bank, DBSVI Who are the unbankable? Reaching out the unbankable has become a challenge mainly due to Indonesia’s unique geographical features and underdeveloped infrastructure. Furthermore, the potential businesses in these areas are too small for financial institutions to set up their branches. The operating cost to reach out to rural areas has outweighed the benefits due to the small-scale nature of such operations. Indonesia: Geographical and economic mapping

* Banking penetration defined as percentage of respondents reported to have an account at a financial institution Note: BRI – Bank Rakyat Indonesia (Indonesia People’s Bank), BPR – Bank Perkreditan Rakyat (People’s Credit Bank/rural banks), BKD – Badan Kredit Desa (Village Credit Board), LKBD – Lembaga Keuangan Bukan Bank (Non-bank Financial Fund) Source: KPMG

36%

69%

42%

78%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Indonesia East Asia & Pacfific

Lower Middle Income Countries

Thailand

% of adult population with financial insititution account

13%

42%

11%

28%

8%

33%

15%

31%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Borrowed from a financial institution

Borrowed from familiy or friends

Indonesia East Asia & Pacfific

Lower Middle Income Countries Thailand

Industry Focus

Page 5

Indonesia: Economic pyramid

Note: <USD1.9 a day, 96m people; USD 1.9-USD4.5, 107m people Source: World Bank, KPMG, DBS Bank, DBSVI Multi-finance companies are crucial proxies for financial inclusion: Multi-finance companies should be seen as the capillaries of financial system where it can channel stream of funds to the unbankable space in more remote areas. Their operations should not be viewed as ‘shadow banking’ as their existence fits well with the regulators’ intention to improve financial inclusion in the country. Since 2014, the government has allowed the multi-finance companies to disburse multi-purpose financing which provides a simple and fast underwriting process. As an anecdotal example, BFI Finance (BFIN) can underwrite multi-purpose financing over 1-2 days. A looser regulatory environment has enabled multi-finance companies to be more flexible. On the flipside, multi-finance companies are not allowed to gather deposits from customers and tend to draw funding from banks, either by bank borrowings, joint financing, or channelling. They can also issue bonds to gather larger chunks of financing. Multi-finance companies’ customers are not typical banking customers. Consumer financing customers are mostly in the lower income bracket and deemed unbankable by larger banks. These consumers may not have sufficient collateral, work in the informal sector, and may not have verifiable credit history. Some do not have proper documentation such as a tax identification (ID) card, which is needed to apply for a bank loan. The implied higher risk also means multi-finance companies are able to charge higher rates than banks. Cost is also higher as multi-finance companies typically need a larger network to remain close to its customer base. The business is also fairly labour intensive, especially for collections and sales. Service over pricing. Lower income customers are not sensitive towards interest rates charged on their loans as long as they

can cope with the monthly instalment. They prefer financing companies that provide fast approval and easy service. Auto-related loans dominate financing segments currently. Currently, consumer financing dominates c.70% of the total loan portfolio of multi-finance companies and this mainly involves auto-related financing. However, as the market for automotive financing becomes more saturated, we should see other form of financing such as multi-purpose financing, refinancing and also infrastructure loans gathering growth pace. Furthermore, the government has allowed multi-finance companies to participate in disbursing subsidised micro loans (Kredit Usaha Rakyat/KUR). B. The multi-finance industry landscape A fragmented industry. There are 201 financing companies in operation in 2016. Over the past 10 years, several had their licenses revoked due to non-compliance with regulations, the most common being inadequate capital. Prior to the Asian Financial Crisis, there were over 212 multi-finance companies nationwide. They typically provide financing for consumption needs (vehicle financing), leasing, factoring and credit cards. Currently, the majority of multi-finance companies focus on consumer financing (motorcycles, 2-wheelers (2W) and cars, 4-wheelers (4W), new and used) and leasing. Factoring remains a small part of the industry. Credit cards are no longer a feature among the multi-finance companies and it has become the target segment of banks. However, we noted that a handful of multi-finance companies are getting back into the game. New multi-finance company licences are still available. Last year, PT Group Lease Finance Indonesia, a joint venture between PT J Trust bank and Group Lease PLC in Thailand, was granted a licence. Multi-finance companies: Financing activities (Aug 2016)

Note: OJK changed breakdown category data since Sep 2016 Source: OJK, BI, DBS Bank, DBSVI

1-2 m people

203 m people

44 m people

1. Upper class: >USD 22.1 a day

2. Middle class:USD 4.5 - USD 22.1 a day

3. Poor:<USD 4.5 a day

Conventionalbanking and insurance markets

Microfinance market

Leasing27%

Factoring3%Consumer

Financing70%

Cars and motorcycles are collectivelyreferred as consumer financing

Industry Focus

Page 6

Change of financing classification by OJK from Sep 16. We note that OJK has changed the classification for its financing activities from Sep 16. Rather than “by type”, the classification is now “by purpose” – investment, working capital and multi-purpose loans – appears to be more similar to the banks’ classification. For example, the passenger 2W and 4W (for personal use) financing is included under “multi-purpose loans”. Commercial automotive financing with tenors of less than two years is considered “working capital financing”, while tenors of more than 2 years fall into “investments financing”. Multi-finance companies: Financing activities (Feb 2017)

Note: OJK changed breakdown category data based on financing activities since Sep 2016. Source: OJK, DBS Bank, DBSVI Overall growth has moderated since 2011. Despite growing at a faster rate compared to the banks, financing growth has moderated in the past five years. There has been a confluence of factors contributing to the moderating growth, the main one being the steep fall in commodity prices apart from regulatory changes. After the relaxation of the minimum down payment (DP) regulation in June 2015 (please see details in the table on page 21), automotive sales growth started to pick up and swing into the positive territory. We noted, however, that 4W sales recovered faster compared to 2W. We believe that the low commodity price environment was more detrimental to the purchasing power of ex-Java buyers who usually rely on 2W transport. 4W sales, on the other hand, are more related to the economic activity in major cities and urbanised areas which experienced lesser impact from softer commodity prices.

Multi-finance companies: Automotive sales vs CPO price

Source: Bloomberg Finance L.P., Gaikindo, AISI Multi-finance companies: Financing activities y-o-y growth

Source: OJK, BI, DBS Bank, DBSVI Auto: Volume sales improvement after DP rule relaxation

Source: Gaikindo, AISI, DBS Bank, DBSVI

28%

13%

59%

Investments Working Capital Multipurpose

-1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

-500

1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500

Dec

-95

Feb-

97

Apr

-98

Jun-

99

Aug

-00

Oct

-01

Dec

-02

Feb-

04

Apr

-05

Jun-

06

Aug

-07

Oct

-08

Dec

-09

Feb-

11

Apr

-12

Jun-

13

Aug

-14

Oct

-15

Dec

-16

CPO Price (MYR/ton) - LHS 4W ('000 units) - LHS

2W ('000 units) - RHS

26.4%

4.1%

31.0% 32.3%

23.1%

15.2%

5.2%

-0.8%

6.7%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

-

50

100

150

200

250

300

350

400

450

2008 2009 2010 2011 2012 2013 2014 2015 2016Total Financing Financing growth y-o-y

Rp bn % growth

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

l-15

Aug

-15

Sep-

15O

ct-1

5N

ov-1

5D

ec-1

5Ja

n-16

Feb-

16M

ar-1

6A

pr-1

6M

ay-1

6Ju

n-16

Jul-1

6A

ug-1

6Se

p-16

Oct

-16

Nov

-16

Dec

-16

4W y-o-y growth 2W y-o-y growth

LTV Relaxation

Industry Focus

Page 7

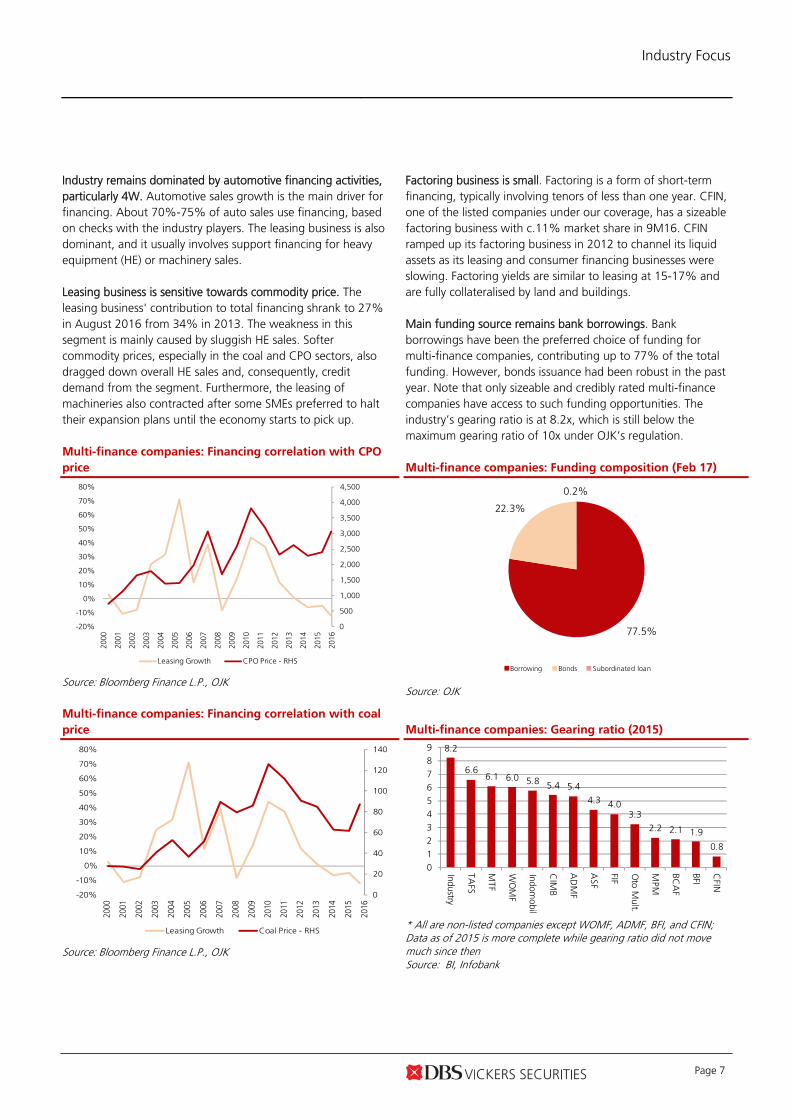

Industry remains dominated by automotive financing activities, particularly 4W. Automotive sales growth is the main driver for financing. About 70%-75% of auto sales use financing, based on checks with the industry players. The leasing business is also dominant, and it usually involves support financing for heavy equipment (HE) or machinery sales. Leasing business is sensitive towards commodity price. The leasing business' contribution to total financing shrank to 27% in August 2016 from 34% in 2013. The weakness in this segment is mainly caused by sluggish HE sales. Softer commodity prices, especially in the coal and CPO sectors, also dragged down overall HE sales and, consequently, credit demand from the segment. Furthermore, the leasing of machineries also contracted after some SMEs preferred to halt their expansion plans until the economy starts to pick up. Multi-finance companies: Financing correlation with CPO

price

Source: Bloomberg Finance L.P., OJK Multi-finance companies: Financing correlation with coal

price

Source: Bloomberg Finance L.P., OJK

Factoring business is small. Factoring is a form of short-term financing, typically involving tenors of less than one year. CFIN, one of the listed companies under our coverage, has a sizeable factoring business with c.11% market share in 9M16. CFIN ramped up its factoring business in 2012 to channel its liquid assets as its leasing and consumer financing businesses were slowing. Factoring yields are similar to leasing at 15-17% and are fully collateralised by land and buildings. Main funding source remains bank borrowings. Bank borrowings have been the preferred choice of funding for multi-finance companies, contributing up to 77% of the total funding. However, bonds issuance had been robust in the past year. Note that only sizeable and credibly rated multi-finance companies have access to such funding opportunities. The industry’s gearing ratio is at 8.2x, which is still below the maximum gearing ratio of 10x under OJK’s regulation.

Multi-finance companies: Funding composition (Feb 17)

Source: OJK Multi-finance companies: Gearing ratio (2015)

* All are non-listed companies except WOMF, ADMF, BFI, and CFIN; Data as of 2015 is more complete while gearing ratio did not move much since then Source: BI, Infobank

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Leasing Growth CPO Price - RHS

0

20

40

60

80

100

120

140

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Leasing Growth Coal Price - RHS

77.5%

22.3%

0.2%

Borrowing Bonds Subordinated loan

8.2

6.66.1 6.0 5.8 5.4 5.4

4.3 4.03.3

2.2 2.1 1.9

0.8

0123456789

Industry

TAFS

MTF

WO

MF

Indomobil

CIM

B

AD

MF

ASF

FIF

Oto M

ult.

MPM

BCA

F

BFI

CFIN

Industry Focus

Page 8

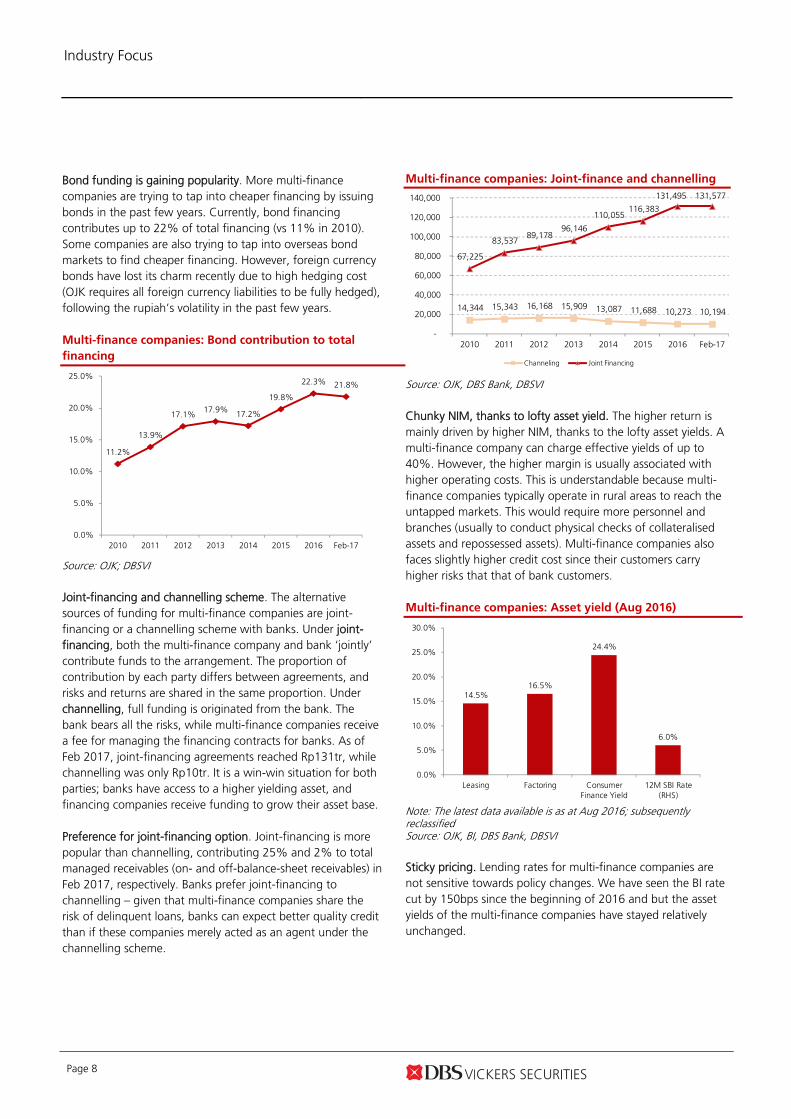

Bond funding is gaining popularity. More multi-finance companies are trying to tap into cheaper financing by issuing bonds in the past few years. Currently, bond financing contributes up to 22% of total financing (vs 11% in 2010). Some companies are also trying to tap into overseas bond markets to find cheaper financing. However, foreign currency bonds have lost its charm recently due to high hedging cost (OJK requires all foreign currency liabilities to be fully hedged), following the rupiah’s volatility in the past few years.

Multi-finance companies: Bond contribution to total

financing

Source: OJK; DBSVI Joint-financing and channelling scheme. The alternative sources of funding for multi-finance companies are joint-financing or a channelling scheme with banks. Under joint-financing, both the multi-finance company and bank ‘jointly’ contribute funds to the arrangement. The proportion of contribution by each party differs between agreements, and risks and returns are shared in the same proportion. Under channelling, full funding is originated from the bank. The bank bears all the risks, while multi-finance companies receive a fee for managing the financing contracts for banks. As of Feb 2017, joint-financing agreements reached Rp131tr, while channelling was only Rp10tr. It is a win-win situation for both parties; banks have access to a higher yielding asset, and financing companies receive funding to grow their asset base. Preference for joint-financing option. Joint-financing is more popular than channelling, contributing 25% and 2% to total managed receivables (on- and off-balance-sheet receivables) in Feb 2017, respectively. Banks prefer joint-financing to channelling – given that multi-finance companies share the risk of delinquent loans, banks can expect better quality credit than if these companies merely acted as an agent under the channelling scheme.

Multi-finance companies: Joint-finance and channelling

Source: OJK, DBS Bank, DBSVI Chunky NIM, thanks to lofty asset yield. The higher return is mainly driven by higher NIM, thanks to the lofty asset yields. A multi-finance company can charge effective yields of up to 40%. However, the higher margin is usually associated with higher operating costs. This is understandable because multi-finance companies typically operate in rural areas to reach the untapped markets. This would require more personnel and branches (usually to conduct physical checks of collateralised assets and repossessed assets). Multi-finance companies also faces slightly higher credit cost since their customers carry higher risks that that of bank customers. Multi-finance companies: Asset yield (Aug 2016)

Note: The latest data available is as at Aug 2016; subsequently reclassified Source: OJK, BI, DBS Bank, DBSVI Sticky pricing. Lending rates for multi-finance companies are not sensitive towards policy changes. We have seen the BI rate cut by 150bps since the beginning of 2016 and but the asset yields of the multi-finance companies have stayed relatively unchanged.

11.2%

13.9%

17.1%17.9% 17.2%

19.8%

22.3% 21.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2010 2011 2012 2013 2014 2015 2016 Feb-17

14,344 15,343 16,168 15,909 13,087 11,688 10,273 10,194

67,225

83,537 89,178

96,146

110,055 116,383

131,495 131,577

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2010 2011 2012 2013 2014 2015 2016 Feb-17

Channeling Joint Financing

14.5%16.5%

24.4%

6.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Leasing Factoring Consumer Finance Yield

12M SBI Rate (RHS)

Industry Focus

Page 9

Multi-finance companies: Asset yield vs 12M SBI Rate

Source: OJK, BI, DBS Bank, DBSVI

Asset quality issues to be monitored; mostly regulatory driven. Multi-finance companies have been plagued with asset-quality deterioration during the previous economic downcycle, bringing the NPL ratio to a high of 2.2% in August 2016, from 1.45% in Dec 2015. In September 2016, OJK changed its NPL recognition category to be more similar with that for the banks (five categories) from three categories previously. The reclassification saw the NPL ratio starting from a high of 3.4% in Sep 2016. However, it moderated to 3.0% by end-Feb 2017. Moreover, we also witnessed the spike in credit cost which reached 2.51% in August 2016, ending the year at 2.88%, vs 2.36% in December 2015. Multi-finance companies: NPL ratio

*OJK reclassified NPL ratio for multi-finance companies to be more similar with that for banks since September. The reporting adjustment resulted in the spike of NPL ratio Source: OJK, DBS Bank, DBSVI

Multi-finance companies: Changes in NPL recognition

Overdue Before Sep 2016 3 Category

After Sep 2016 5 Category

On time payment Current

Current 90 days in arrears Special Mention 90-120 days in arrears Sub Standard 120- 180 days in arrears Doubtful Doubtful more than 180 days in arrears Loss Loss

Note: Red font considered NPL Source: OJK, DBS Bank, DBSVI

Multi-finance companies: Credit cost

Source: OJK, BI, DBS Bank, DBSVI C. Prospects for the multi-finance industry Turning optimistic. We expect an improvement in financing demand this year. The Multi-finance Company Association (APPI/Asosiasi Perusahaan Pembiayaan Indonesia) recently announced its forecast of 10% financing growth this year on the back of an improving economy and higher commodity prices. However, we believe it is an optimistic number as the sustained positive growth needs to be supported by real improvements in purchasing power and business confidence which we have yet to see. Multi-finance companies: Financing growth vs GDP growth

Source: OJK, BPS, DBS Bank, DBSVI Earnings growth traction should improve from here. We believe earnings should recover in 2017 on the back of lower credit cost due to improved commodity prices which can help boost purchasing power, especially in the lower income segment. We do not expect much deviation on NIM due to the stable yields and cost of funds of the multi-finance companies. Operating costs are also expected to be flat as the companies have not been aggressive in expanding their service points.

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

10%

12%

14%

16%

18%

20%

22%

24%

26%

Blended Yield 12M SBI Rate (RHS)

2.5%2.3%

2.0%2.0%

1.6%1.4%1.4%1.4%

1.6%1.6%

2.0%2.2%

2.2%2.2%

2.2%

3.4%3.2%3.2%3.3%3.2%

3.0%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

NPL NPL*

1.77%1.82%

2.24%

1.95%

1.76%

2.13%

2.36%

2.88%

1.50%

1.70%

1.90%

2.10%

2.30%

2.50%

2.70%

2.90%

3.10%

2009 2010 2011 2012 2013 2014 2015 2016

4.1%

31.0%32.3%

23.1%

15.2%

5.2%‐0.8%

6.7%8%

4.6%

6.1%6.5%

6.2%5.8%

5.0%4.7%

5.0%5.3%

0%

1%

2%

3%

4%

5%

6%

7%

‐5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2009 2010 2011 2012 2013 2014 2015 2016 2017F

Total Financing (% y‐o‐y) Real GDP Growth (%y‐o‐y)

Industry Focus

Page 10

Multi-finance companies: Earnings growth

*Average earnings growth of BFIN and CFIN Source: OJK, Companies, DBS Bank, DBSVI Potential NIM expansion. We expect NIM expansion on the back of lower funding cost as the banks have started to price down their loans, which means multi-finance companies now enjoy lower funding costs via bank borrowings. Meanwhile, asset yields are expected to be constant as the interest rates offered to the customers are not sensitive towards the change in interest rate environment. Multi-finance customers typically are more concerned about monthly instalments (whether they are able to pay), fast approval, and easy service more than interest rates. The higher reliance on bond financing could lower funding costs. Bond financing has been gaining popularity and the data shows that bond financing portion is on the uptrend. This might lower the blended cost of funds further as bond financing is typically cheaper than bank financing. Multi-finance companies: NIM

Source: Companies, DBS Bank, DBSVI Operating expenses should remain in check. Historically, cost to income ratio were stable around 40%. The slight uptick in 2015 is mainly due to weakening profitability – largely

attributed to the slowdown in the automotive business and heavy equipment. A slight improvement in 2016 was triggered by some cost efficiency measures. We noted that ADMF and MTF had successfully improved their cost-to-income ratio in 2016 via network and employee rationalisation. Multi-finance companies: Cost-to-income ratio

Source: Companies, DBS Bank, DBSVI Improvement in asset quality. Multi-finance companies reported lower NPL ratios in 2016. However, the multi-finance companies we met were hesitant to turn bullish. Better commodity price would be positive for their customers, especially for commercial heavy equipment leasing and factoring but these customers need a sustained high commodity price to help their distressed cash flow. However, we believe that positive asset-quality trends may come from the portfolio shift towards customer financing and tighter financing approval. Multi-finance companies: NPL ratio

Source: Companies, DBS Bank, DBSVI

14%

2%

33%

19%

-16%-13%

2%

27%30%

17%

9% 10%

-10% -3%

28%

9%

17%

-20%

-10%

0%

10%

20%

30%

40%

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F

Industry Earnings Growth Average*

13.1%12.4% 12.0% 12.2%

12.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2012 2013 2014 2015 2016

BCA Finance Mandiri Tunas Finance FIF

ASDF ADMF BFIN

CFIN Average - RHS

%%

37.5 36.3 38.040.0 39.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2012 2013 2014 2015 2016

BCA Finance Mandiri Tunas Finance FIF

ASDF ADMF BFIN

CFIN Average

%%

1.09 0.96 1.00

1.21 1.13

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0

0.5

1

1.5

2

2.5

2012 2013 2014 2015 2016

BCA Finance Mandiri Tunas Finance FIF

ASDF ADMF BFIN

CFIN Average - RHS

%%

Industry Focus

Page 11

Key drivers for the multi-finance industry

With consumer financing dominating the loan portfolio of multi-finance companies, the auto industry would be the key growth driver. Leasing growth relies mainly on heavy equipment financing which in turn unfortunately is dependent on commodity prices. Both these segments have been in the doldrums in the past two years. The near-term exuberance of commodity prices might not sustain throughout the year but we believe the positive impact would be moderate. We expect the auto industry to pick up slightly this year, boosting the growth prospects of multi-finance companies. A. Automotive Industry Outlook Improved auto sector outlook for 2017; expect a stronger 2H17. 2016 industry sales came in slightly lower than our expectation, with FY16 volume growing 4.8% y-o-y (we forecasted 5% y-o-y). Meanwhile, 2W demand is still weak as FY16 sales volume shrank 8%, mainly driven by weak ex-java sales due to sustained low commodity prices. We are less optimistic about the 2W segment and expect only 2% volume growth in FY17. Astra International’s management has guided that sales in FY17 will be second-half-heavy while the first half of the year should see flat volume growth. Temporary support from commodity prices. Sustained high CPO prices should help automotive sales, especially in the ex-Java areas. However, purchasing power in the commodity-related regions has yet to show significant improvement so far. We believe the high commodity prices need to be sustained long enough to allow the positive effects to spill over to the auto sector. Therefore, we only expect modest growth (c.5% for 4W and c.2% for 2W) this year. Long term-potential is still there, especially for 4W. The auto penetration rate in Indonesia remains one of the lowest in the region. Based on data by Badan Pusat Statistik (BPS)/Indonesian Statistics Centre and automotive association, in 2015 there are only 13.7m cars and 99m motorcycles outstanding on Indonesian roads (vs its population of 250m). The penetration rate for 4W is a mere 5%, lower than other developing countries like Malaysia and Thailand. However, 2W penetration is much higher at 40% in 2015.

Auto penetration in developing countries

Source: CEIC, BPS, Gaikindo, DBS Bank, DBSVI Auto: 4W sales trend – recovery after being severely hit

Source: Gaikindo, DBS Bank, DBSVI Auto: 2W sales trend – slower growth

Source: AISI, DBS Bank, DBSVI

Indonesia, 4.68%

China, 4.52%

India, 2.68%

Thailand, 15.22%

Malaysia, 32.17%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0% 5% 10% 15% 20% 25% 30% 35%

Car ownership ratio

GD

P p

er c

apit

a U

S$

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016F

2017F

2018F

CAGR: 5%

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016F

2017F

2018F

CAGR: 2%

Industry Focus

Page 12

Penetration is low, but is it that low? Only half the population can buy a car. Despite the appeal of a low 4W penetration rate in Indonesia, we argue that only around half of the Indonesian population can afford a car. Income equality has become the key feature in the Indonesian economy. This can be seen in the increase in Gini coefficient to 0.4 in 2016 vs 0.36 in 1996. Data from BPS indicates that the top 20% of the Indonesian population contributes to 48% of total expenditure, as shown in the chart below. Indonesia: Inequality is an important feature

Source: BPS 2014, DBS Bank, DBSVI Indonesia: Auto loan penetration

Note: Calculated as number of vehicles divided by national population Source: BPS, Gaikindo, AISI, DBS Bank, DBSVI Affordability estimates. We estimate how much the price of a car an average Indonesian can afford in each segment. Using the nominal GDP per capita as a proxy of income, we estimated that the top 20% of the working population (with age 15-64) have an average annual income of Rp176m/year. Assuming 30% of the income is allocated to car installment, dual income, 25% down payment, and 4 years installment period, we believe that the families in this class can afford a Rp350m car (please see the following table).

Auto: Price segmentation based on income

Income Brackets

Pop. (m person)*

Annual GDP Nominal 2016 (Rp tr)

Annual GDP per Capita (Rp m)

Capability of monthly installment per family (Rp m)**

Ideal Price Segment (Rp m)***

Top 20% 34,046 5,988 176 8.8 350

Middle 40% 68,092 4,292 63 3.2 125

Bottom 40% 68,092 2,134 31 1.6 60

Total 170,230 12,415 73 3.6

* Productive age (age 15-64) is 66.9% of total population, based on World Bank data in 2014 **Assuming dual income and installment is maximum 30% of monthly income. Calculated as: annual GDP per capita* 2 * 30% / 12 *** ideal price segment is based on credit simulation on Astra Credit Companies website assuming 25% down payment and 4 years tenor Source: BPS; Gaikindo; AISI; DBS Bank, DBSVI Small MPVs are favourite. The affordability analysis might explain why the small multi-purpose vehicles (MPV) (Avanza, Xenia, Mobilio, and Ertiga) have become the favourite cars in Indonesia. The prices of those cars fall in the income range of the top 20% and middle 40% segments. Some brands like Innova have also moved up to the higher-end target market segments to capture the more affluent customers. Auto: Price and units sold by top 10 brands in 2016

Source:Gaikindo, DBS Bank, DBSVI LCGC segment has the lowest penetrated market; strong growth ability. We believe the middle 40% market offers the biggest potential due to its huge population. Based on the assumption we have laid out earlier, people in this segment can afford a car with price tags of around Rp125m. This might be suitable for low-cost green cars (LCGC) which are usually priced around Rp100m-150m per unit. This segment has been barely penetrated. LCGC sales have not even reached 1m units vs the potential market of 51m units (assuming 102m people in the middle segment use one car per two persons).

17%

40%

35%

40%

48%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Expenditure Population

Top 20%

Middle 40%

Bottom 40%

-

50

100

150

200

250

300

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

F20

15F

2016

F20

17F

2018

F

Population (mn) 2W penetration 4W penetration

6.1mn

- 50,000 100,000 150,000 200,000

Motorcycle (Rp17m)

Ayla (Rp110m)

Agya (Rp120m)

BRV (Rp130m)

Calya (Rp140m)

Xenia (Rp170m)

Avanza (Rp200m)

Mobilio (Rp200m)

Brio Satya (Rp240m)

HR-V (Rp300m)

Innova (Rp350m)

Unit Sold in 2016

LCGC235,171 units/

22.1% of total industry sales

Industry Focus

Page 13

Auto: Market size for each segment

Note: Number of families are calculated as working population (age 15-64) divided by two. Source: BPS, Gaikindo, DBS Bank, DBSVI LCGC is gaining market share. LCGC car volume saw a significant increase in market share, especially during the economic slowdown in 2015. The market share of LCGC cars swelled to 22% in 2016 from 14% in 2014. The strong penetration rate is due to LCGC’s well-accepted value proposition to the lower-income consuming class which is price sensitive. LCGC cars also offer better fuel efficiency. It can carry 5-7 passenger cars, which is also a strong selling point for young families in Indonesia. Auto: LCGC is gaining market share

Source: Gaikindo, DBS Bank, DBSVI

B. Leasing and heavy equipment Sluggish leasing growth in 2016. Leasing shrank by 12% in Aug 2016, the weakest growth since the GFC. Low commodity prices such as coal and CPO hit the demand for new heavy equipment (HE), resulting in a 44% contraction for Komatsu HE (the market leader in Indonesia) annual sales volume. Furthermore, the soft economic conditions also dragged down the sales of trucks and machinery, which eventually translate into low leasing demand. The leasing business is more cyclical by nature compared to consumer financing. Moderately higher coal prices in 2017. Our coal price assumption for FY17 onwards is at US$65 per ton, supported by supply and demand rebalancing following China’s intention to limit its coal production volume as well as the stickier-than-expected Chinese coal demand in the short to medium term. Besides the China coal production cut, coal restocking for the 4Q16 winter season provided a short-term cushion for coal prices. A recovery in sight, but we are not overly bullish on coal price outlook. While the coal price benchmark has risen by more than 25% in 2H16, we believe it is more due to supply disruption rather than demand improvement. We have not seen any structural improvement in demand from key importers like China; beyond the upcoming capacity under construction. Beyond 2016, we believe the supply and demand situation is improving, even though a structural supply and demand recovery is not in sight yet. The higher coal price trend of late is not expected to translate into a full-fledged coal price recovery cycle. Newcastle coal price trend and forecast (US$/ton)

Source: Bloomberg Finance L.P., DBS Bank, DBSVI

17

34

34

Top 20%

Middle 40%

Bottom 40%

Regular Car Segment (Rp350m/unit)

LCGC Segment (Rp125m/unit)

Used Car/Motorcycle Segment (Rp60m/unit)

Million families

14%16%

22%

0%

5%

10%

15%

20%

25%

2014 2015 2016

LCGC Share

0

20

40

60

80

100

120

140

Industry Focus

Page 14

Leasing: Hampered by low commodity prices

Note: HE sales as of 3Q16; the latest data available is as at Aug 2016; subsequently reclassified Source: companies, OJK, DBS Bank, DBSVI;

Demand for heavy equipment leasing should recover. The leasing business is highly dependent on HE volume which in turn depends on commodity prices. We expect the improvement in HE sales to come from higher demand from the mining and construction sectors. With a recovery in commodity prices, we should at least expect the leasing business of the multi-finance companies to stop sliding.

39%

-8%

14%

44%

37%

12%

-5% -5%

-12%

-20%

-10%

0%

10%

20%

30%

40%

50%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2008 2009 2010 2011 2012 2013 2014 2015 8M16

HE Industry Sales Leasing Growth - RHS

Units

Industry Focus

Page 15

Key players and market position

Who’s who in the Indonesian multi-finance industry? The industry is very fragmented. As mentioned above, there are a total of 201 multi-finance companies, with the top 20 companies commanding 65% (financing) market share. While we profile all the multi-finance companies in the industry by business type and ownership, we will focus on the top companies to analyse their strategies and profitability. We will also narrow our analysis on the multi-finance companies by focusing on consumer financing which forms the bulk of their business. Fragmented market. The industry is fragmented and each company caters to its own niche. The top 20 multi-finance companies have a combined market share of 65%. Each of them caters to its own niche by specialising in several categories such as product financed (4W, 2W, HE, etc) and geographical reach. The biggest player (Astra Sedaya Finance, ASDF) only has 8% market share, marginally higher among the top 4 companies. Some multi-finance companies invest in huge branch network, such as BFIN (204 branches) and Adira Finance (201) for local presence and to gain the local knowledge in specific geographical areas. Synergy with banks and automotive players. Multi-finance companies are typically owned by banks (both domestic and foreign), brand-holding sole agents (ATPM) of cars and foreign principals of car makers (e.g. Astra), and a few which are family/individual-owned. The strong multi-finance companies are those affiliated to banks or car makers and ATPMs. ATPMs seek to team up with multi-finance companies to support their sales. Some ATPMs have their own financing companies. The Astra Group, which is the ATPM for Toyota, Daihatsu and Isuzu cars and Honda motorcycles, has Astra Sedaya Finance, Toyota Astra Finance for 4W/car financing and Federal International Finance for 2W/motorcycle financing. The Indomobil Group also has its own financing firms – Indomobil Finance Indonesia for 4W/car financing and Suzuki Finance Indonesia for 2W/motorcycle financing.

Multi-finance companies: Market share of top 20 players

Note: Based on outstanding on balance sheet net receivable. Data represents 2015 numbers Source: Infobank, OJK, DBS Bank, DBSVI Multi-finance companies: Breakdown by business type

Note: Others include leasing, factoring, and multi-purpose financing; data represents 2015 numbers Source: Company annual reports & websites, DBS Bank, DBSVI

Multi-finance companies: Breakdown by ownership

Source: DBS Bank, DBSVI

8%7% 7% 7%

5%

4%

3%3% 3% 2% 2% 2% 2% 2% 2% 2% 1% 1% 1% 1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

ASD

F

FIF

AD

MF

C.J

. Pow

er

Oto

M

TAFS

Dip

o S.

F

BFIN

Sum

mit

O.F

Man

diri

T.F

Indo

mob

il F,

I

Buss

an A

.F

CFI

N

BCA

F

CIM

B F.

Mits

ui L

easi

ng

Orix

I.F

Sury

a A

rtha

N.F

MPM

F.

WO

MF

96%

2%

41%

100% 100%

38%

96%

37%

100%

58%

89%

58%

100%19%

4% 9%1%

62%

4%

44% 42%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%A

SDF

FIF

AD

MF

Oto

M

TAFS

BFIN

Sum

mit

O.F

Man

diri

T.F

Indo

mob

il F,

I

BCA

F

CFI

N

4W 2W Others

INDEPENDENT

BANK RELATEDAUTO RELATED

FIF

MPM FinanceTAFS

Indomobil Fin.

ASDF

Mandiri TF

Adira

BCA FinanceClipan Finance

CIMB Niaga AF

BFINOto MultiarthaSummit Oto F.

Industry Focus

Page 16

Top players have better profitability metrics than banks. Compared to banks, multi-finance companies generate better returns. Generally, the major multi-finance players record higher ROE and ROA as the benefits of higher asset yield outweigh the negatives of higher cost of funds, operating cost, and credit cost. The higher asset yield is due to the ability to tap the unbankable market, an advantage that banks lack. But it requires vast infrastructure to tap into this market while the high credit cost is due to the high risk profile of customers.

Multi-finance companies (vs banks): ROE

Note: Data represents 2015 numbers Source: Infobank, OJK, BI, DBS Bank, DBSVI Multi-finance companies vs banks: ROA

Notes: Data represents 2015 numbers Source: Infobank, OJK, BI, DBS Bank, DBSVI

Multi-finance companies: Comparison with banks

Multifinance Companies

(Rp bn) Banks

(Rp bn)

NIM 12.9% 7.14% Credit Cost 2.89% 1.64% Opex/loan 8.00% 3.6% NPL 1.11% 2.18%

(All ratios using average three years of data for banks and multi-finance covered in this report) Note: Data represents 2016 numbers Source: OJK, BI, DBS Bank, DBSVI

Leveraging on banks’ balance sheet through joint financing to enhance ROE. Multi-finance companies, especially the ones related with banks, often use joint financing to enhance returns and therefore ROE. That explains why BCAF, MTF, and ADMF can offer lower effective loan rates for their products but can yet enjoy astronomical asset yields and ROEs. This is the key benefit of having a bank as a shareholder; as it can use the bank’s balance sheet to grow more aggressively and achieve higher ROE. Automotive-related companies also can use joint financing/channelling but the portion is usually smaller. Take ASDF, for example. Comparatively, it does not have a significant joint financing portion for its managed receivables and has relatively low asset yield and ROE.

18%

29%

16%

8%

15%

21%17%

30%

56%

20%

12%

20%

12%10%

15% 13%

8%

0%

10%

20%

30%

40%

50%

60%

ASD

F

FIF

AD

MF

Oto

M

TAFS

Dip

o S.

F

BFIN

Man

diri

T.F

BCA

F

BBC

A

BMRI

BBRI

BBN

I

BDM

N

BBTN

BTPN

PNBN

3%

6%

2% 2% 2%3%

6%

4%

16%

3%2%

3%2% 2% 1%

2%1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

ASD

F

FIF

AD

MF

Oto

M

TAFS

Dip

o S.

F

BFIN

Man

diri

T.F

BCA

F

BBC

A

BMRI

BBRI

BBN

I

BDM

N

BBTN

BTPN

PNBN

Industry Focus

Page 17

Multi-finance companies: Top 20 players (by asset size) – 2015 Company Asset

2015 (Rp bn)

Financing 2015

(Rp bn)

Liabilities 2015

(Rp bn)

Equity 2015

(Rp bn)

Gearing Ratio

Major Product

Financed

ROE Number of

Branches

Astra Sedaya Finance 30,392 27,542 24,699 5,693 4.34 4W% 18.1% 61 Central Java Power 29,880 24,425 24,088 5,792 4.31 Power Plant 25.3% N/A

Federal International Finance 28,734 25,962 23,011 5,723 4.02 2W% 29.2% 169

Adira Dinamika Multi Finance 27,744 24,919 23,383 4,361 5.36 4W, 2W 15.8% 654

Oto Multiartha 22,288 19,717 17,301 4,986 3.25 4W 8.3% 72

Toyota Astra Financial Services 17,804 15,986 15,548 2,256 7.17 4W 15.1% 27

Dipo Star Finance 14,304 11,967 12,087 2,216 4.74 4W 20.9% 31

BFI Finance Indonesia 11,770 9,898 7,751 4,019 1.93 Multipurpose 17.0% 204

Summit Oto Finance 10,575 9,120 6,655 3,920 1.73 2W 6.1% 133

Mandiri Tunas Finance 9,203 8,482 8,030 1,173 6.55 4W 29.6% 88

Indomobil Finance Indonesia 8,913 8,085 7,597 1,316 4.90 4W, 2W 6.4% 80

Bussan Auto Finance 8,880 7,566 7,276 1,604 5.07 4W, 2W 0.2% 188

BCA Finance 6,824 5,707 4,634 2,190 2.12 4W 56.2% 60

Orix Indonesia Finance 6,727 4,950 4,533 2,194 2.11 4W, 2W, HE 9.9% 10

Surya Artha Nusantara Finance 6,693 5,260 5,285 1,408 3.66 HE 7.9% 15

Clipan Finance 6,647 6,430 3,048 3,599 0.85 4W 8.4% 45

CIMB Niaga Auto Finance 6,438 5,903 5,459 979 5.73 4W, 2W, HE 8.6% 68

Mitsui Leasing Capital Indonesia 5,910 5,638 4,860 1,051 4.78 4W, HE 7.0% 15

Wahana Ottomitra Multiartha 5,306 4,190 4,451 856 6.02 2W 2.2% 99

Mitra Pinasthika Mustika Finance 5,240 4,671 3,548 1,692 2.19 4W, 2W, HE 1.3% 91

Notes: Data represents 2015 numbers Source: Infobank, OJK, BI, DBS Bank, DBSVI

Multi-finance companies: Shareholding structure of the top 20 players

Company Shareholder 1 Shareholder 2

Astra Sedaya Finance PT Astra International 75% PT Bank Permata Tbk.25%

Central Java Power Summit Power Capital Limited (UK) 50% Summit Power Global Management I B.V (Netherlands) 25%

Federal International Finance PT Astra International, Tbk. 99,99% PT Asrya Kharisma 0,01%

Adira Dinamika Multi Finance PT Bank Danamon Indonesia 75,00% Mega Value Profit Limited 17,42%

Oto Multiartha Sumitomo Corporation 85% PT Sumitomo Indonesia 10%

Toyota Astra Financial Services PT Astra International 50%; Toyota Financial Services Corporation 50%

Dipo Star Finance MC Automobile Holding Asia B.V. 85% PT MC Auto Consulting Indonesia 10%

BFI Finance Indonesia Trinugraha Capital & Co SCA 44,10% Lainnya 55,90%

Summit Oto Finance Sumitomo Corporation 85,00% PT Sumitomo Indonesia 10,00%

Mandiri Tunas Finance Bank Mandiri 51% PT Tunas Mobilindo Parama 49%

Indomobil Finance Indonesia PT Indomobil Sukses International, Tbk. 99,875% PT IMG Sejahtera Langgeng 0,125%

Bussan Auto Finance Mitsui & Co., Ltd Japan 58,33% Yamaha Motor Co.,Ltd Japan 17,67%

BCA Finance PT Bank Central Asia Tbk. 99,58% PT Bank Central Asia Tbk. 99,58%

Orix Indonesia Finance Orix Corporation 96,02% Yayasan Kesejahteraan Karyawan BI 3,98%

Surya Artha Nusantara Finance PT Sedaya Multi Investama 60% Marubeni Corporation, Jepang 35%

Clipan Finance PT Bank Pan Indonesia, Tbk. 54,35% Public 45,65%

CIMB Niaga Auto Finance PT Bank CIMB Niaga Tbk. 99,94% -

Mitsui Leasing Capital Indonesia JA Mitsui Leasing, Ltd. 85% PT Matahari Artha Nusantara 15%

Wahana Ottomitra Multiartha Tbk PT Bank Internasional Indonesia 62,00% PT Wahana Makmur Sejati 17,59%

Mitra Pinasthika Mustika Finance PT Mitra Pinasthika Mustika Tbk 59,99% JACCS Co, Ltd 40,00%

Notes: Data represents 2015 numbers Source: Infobank, OJK, BI, DBS Bank, DBSVI

Industry Focus

Page 18

Multi-finance companies: Joint-financing arrangements

Joint-financing & Channelling

Portion* Joint-financing Partner

Joint-financing Facility Amount

(bn)

Joint-financing Portion

Agreement

Effective Interest Rate Offered

Yield on Consumer Financing FY16

ROA FY16 (%)

BCA Finance 89% Bank BCA n.a 95% 7% - 27% 35% 14%

Mandiri Tunas Finance

64% Bank Mandiri 20,500 99% 14,1%- 4W 21.8% 2W

15.5% - Others 20% 2.9%

FIF 16%

TAFS Unlimited 70%-99%

25.1% - 42.6% 28% 6.1%

PT Bank Permata Tbk 6,100 90%-99% PT Bank Permata Tbk - Syariah 3,000 90%-99%

PT Bank Commonwealth 3,000 70%-99%

PT Bank CIMB Niaga 2,500 70%-99% PT Bank CIMB Niaga - Syariah 3,000 90%-99% PT Surya Artha Nusantara Finance 2,000 70%-99%

PT Bank Sahabat Keluarga 1,000 70%-99%

PT Astra Sedaya Finance 300 70%-99%

PT Bank Panin Syariah 500 90%-99%

ASDF 22%

PT Bank Permata Tbk 10,700 90%

7.1% - 29.6% 16% 3%

PT Bank Commonwealth 2,000 90% PT Sahabat Finansial Keluarga 1,000 90%

PT Bank CIMB Niaga Tbk 1,000 90%

PT Bank OCBC NISP Tbk 500 90%

ADMF 40% PT Bank Danamon n.a 99% 17%-22% - 4W

33% - 41% - 2W 24% 3.7%

PT Bank Commonwealth n.a 99%

BFIN 18%

PT Bank Rakyat Indonesia 600 Channelling 16% – 21%- 4W 38%-41% - 2W

14%-18% - Prop. 21% 6.3% PT Bank Mandiri Tbk 500 95%

PT Bank Maybank Indonesia Tbk 0.5 95%

CFIN 3% PT Bank Pan Indonesia Tbk 2,000 Channelling 17.20% 16% 3.1%

* % of managed receivables, gross of unearned interest Source: Annual reports, DBSVI, DBS Bank

A. 4-wheeler (4W) market space 4W market dominated by Astra and bank-backed parentage. We note that the top six players that dominate this segment have 77% of the estimated new 4W financing market in terms of unit financed. Astra Sedaya Finance (ASDF) is the market leader in this segment, thanks to the backing of its automotive distributor and bank parent, Bank Permata. In terms of nominal value of new financing, however, BCAF is the market leader with Rp30.7tr new bookings in FY16 (including joint financing), thanks to the strong consumer banking franchise which enables it to tap into customers in the affluent class segment.

Top 4W players: Market share in terms of unit financed

Assuming 70% of new 4W domestic sales using financing Source: Companies, DBS Bank, DBSVI

BCAF15%

ASDF18%

MTF13%TAFS

11%

OTO M14%

ADMF6%

Others23%

Industry Focus

Page 19

Top 4W players: New bookings for new 4W in 2016

*Data for Oto Multiarta (OTO M) is a management target in 2016 ** Data for BCAF is an estimation based on disclosed market share Source: Companies, DBS Bank, DBSVI

Top 4W players: Market share movement

Source: Companies, DBS Bank, DBSVI B. 2-wheeler (2W) market space 2W market dominated by FIF and ADMF. In the new 2W financing segment, we see three dominant players in this segment – led by Federal International Finance (FIF), Adira Dinamika Multifinance (ADMF), and WOM Finance (WOMF). In the past five years, we note that FIF has consistently been increasing market share, supported by Honda’s strong performance. We understand that nearly half of Honda’s sales are financed through FIF. Honda saw its market share rise gradually to 74% in FY16 from 58% five years ago; this has been the main driver for FIF’s strong performance.

Top 2W players: Market share movement

Notes: Assuming 70% of new 2W sales using financing. WOMF number for 2016 using annualised 9M16 number. Source: Companies, DBS Bank, DBSVI Top 2W players: Market share in 2016

Notes: Assuming 70% of new 2W sales using financing. WOMF number for 2016 using annualised 9M16 number. Source: Companies, DBS Bank, DBSVI

Top 2W players: Market share of 2W brands

Source: Gaikindo

133

114 100 99

82

48

-

20

40

60

80

100

120

140

ASDF BCAF** OTO M* MTF TAFS ADMF

New

Thousands Unit

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

2012 2013 2014 2015 2016

BCAF ASDF MTF TAFS OTO M ADMF

24.0%24.2%

26.6%

31.5%34.6%

22.4%18.1% 18.1% 17.2% 17.5%

7.9% 7.2% 7.8% 7.6%5.7%

0.3% 0.3% 0.3% 0.3% 0.1%0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2012 2013 2014 2015 2016

FIF ADMF WOMF MTF

34.6%

17.5%5.7%0.1%

42.1%

FIF ADMF WOMF MTF Others

58%61%

64%69%

74%

34% 32% 30% 28%23%

6% 5% 3% 2% 1%2% 2%2%

2%2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2012 2013 2014 2015 2016

Honda Yamaha Suzuki Others

Industry Focus

Page 20

Regulatory framework for multi-finance companies

Regulated by OJK. Multi-finance companies are licensed to offer a range of services, including leasing, consumer financing, credit card financing and factoring. These companies target the financing needs of the lower income households. But unlike banks, they are not allowed to accept deposits. Similar to banks, multi-finance companies are governed by OJK, the regulatory arm of the Minister of Finance (MoF). Prior to the formation of OJK in 2011, multi-finance companies were under the purview of Bapepam. OJK issued 28/POJK.05/2014 to regulate the licensing and the institution of multi-finance companies. The main takeaways from the regulation include: Steps to incorporate a multi-finance company: Establishment of Limited Liability Company. Limited

liability company is the most common legal entity for a multi-finance company in Indonesia. For further details in establishing a limited liability company, please refer to the Indonesian Investment Coordinating Board (BKPM/Badan Koordinasi Penanaman Modal) website http://www.bkpm.go.id/en/investment-procedures

Obtain licence from OJK. The directors need to obtain a licence from OJK. The proposal needs to follow the formats and be attached with all the documents required in accordance to 28/POJK.05/2014.

Fit and proper test for the directors and commissioners. OJK will decide in 30 days or less after all the documents

have been submitted properly. If OJK perceives the documents to be incomplete, OJK will notify the applicant in 20 days or less.

Companies that already have obtained the licence must start the business in two months or less.

Capital requirements: Minimum paid-up capital of Rp100bn (USD7.5m) for a

limited liability entity. Maximum foreign ownership is 85% of paid-up capital. For publicly listed entity: Maximum floating shares of

85%. Local ownership needs to be maintained at a minimum level of 15% of the non-listed shares.

Foreign labour restriction: Companies can only hire a non-Indonesian employee as

consultant, advisor, or high-ranked officials (director or one level below directors.

Membership requirement in other organisations: Multi-finance companies must join the membership of the

appointed credit bureau. Multi-finance companies must join the membership of the

appointed association.

Credit bureau: Multi-finance companies can subscribe to credit history

data for customers from Bank Indonesia (BI checking) and Pefindo (private credit rating agency/credit bureau).

Multi-finance companies can also retrieve information on blacklisted customers from the relevant association (APPI/Asosiasi Perusahaan Pembiayaan Indonesia).

Merger and acquisition: OJK defines controlling shareholder as >=25% ownership

of a person or entity or proven to have been controlling the company directly or indirectly.

Approval from OJK must be obtained before a change in controlling shareholder.

Acquisition cost for new 4W dealership: By releasing SE OJK No.1/seojk.05/2016, OJK puts the cap

on acquisition cost (commission paid to the dealer in % terms of the revenue from one customer) at 15%.

Regulators also put a cap of 20% acquisition cost for 2W financing, based on our checks with industry players.

Regulations/restrictions in operating a multi-finance company. OJK also stipulates the conduct of a multi-finance company. The table below summarises the requirements/restrictions: Multi-finance companies: Regulations/restrictions for

operating a multi-finance company

Requirement/restrictions under POJK No 29/POJK.05/2014

Non Performing Financing max 5% Financing to Asset Ratio min 40% Minimum Equity Rp100bn Gearing Ratio max 10% Foreign currency liabilities must be fully hedged Cannot gather deposits directly from customers

Source: OJK, DBS Bank, DBSVI NPL classification similar to banks now. Multi-finance companies have started to implement an NPL classification that is similar to that for banks (NPL as loans with 90 days past due) effective from Jan 2016. It has also been reflected in the Sep 16 NPL figures, which jumped to 3.4% from 2.2% in Aug 16 (refer to the earlier section on page 9). However, there are still deviations for the write-off policies, depending on the level of conservatism.

Industry Focus

Page 21

Collection and write-off policies may vary; provisions are regulated. Multi-finance companies may implement different collection and write-off policies. Adira Finance, for example, implements a 210-day automatic write-off policy while Mandiri Tunas Finance implements 180 days. Provisioning, however, is more regulated. The companies need to set aside 100% provisioning after 180 days overdue. LTV regulation for auto financing. The loan-to-value (LTV) regulation has been an effective tool that is often used by OJK to manage the multi-finance industry. Prior to 2013, there were no LTV criteria instituted for multi-finance companies. Despite that, there were some multi-finance companies which were more prudent than others (having their own LTV criteria).

During the boom times for 2W and 4W in 2010-2013, some multi-finance companies gave out financing without any down payment requirement. Relaxing the LTV criteria. In 2015, OJK relaxed the stringent LTV regulation to stimulate the sluggish economic growth. OJK has further relaxed the minimum down payment requirement in May 2016 by issuing circular letter OJK NO.47/SEOJK.05/2016. With the new regulation, the minimum down payment was relaxed to as low as 5% for multi-finance companies with NPLs lower than 1%. This is a significant relaxation compared with the previous regulation which required 15%-20% down payment.

Multi-finance companies: Minimum down payment regulation changes

Current Regulation Previous Regulation

NPF ≤ 5% NPF>5% For Syariah Entity

Before June 2015 Vehicle NPF ≤

1% 1%<NPF ≤3%

3%<NPF ≤5%

NPF ≤ 5%*

NPF>5% Conv. Syariah Conv. Syariah

2W 5% 10% 15% 15% 20% 15% 10% 20% 15% 15% 20%

4W - Productive 5% 10% 15% 15% 20% 15% 15% 20% 20% 15% 20%

4W - Consumptive 5% 10% 15% 20% 25% 20% 20% 25% 25% 20% 25%

Source: OJK, DBS Bank, DBSVI *For companies who do not meet the minimum financial health

Regulatory framework of the multi-finance companies

Source: Indonesian Multi-finance Companies Association (APPI/Asosiasi Perusahaan Pembiayaan Indonesia)

Industry Focus

Page 22

Multi-finance companies: How regulatory changes affected financing growth in the multi-finance industry

Source: BI, OJK, DBS Bank, DBSVI

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Feb-

11

Apr

-11

Jun-

11

Au g

-11

Oct

-11

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Au g

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Au g

-13

Oct

-13

Dec

-13

Feb-

14

Apr

-14

Jun-

14

Au g

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

Au g

-15

Oct

-15

Dec

-15

Feb-

16

Apr

-16

Jun-

16

Aug

-16

Oct

-16

Dec

-16

Feb-

17

In March 2012, BI implemented minimum down payment of 25% for 2W, and 30% for non-commercial 4W.

In June 2015, BI relaxed minimum down payment to 15% for 2W and 20% for non-commercial 4W.

OJK issued 29/POJK.05/2014 which enabled MFCsto disburse mutipurpose and infrastructure financing

Further relaxation of down payment regulation. Miniimumdown payment can be as low as 5%, depends on NPL level

Industry Focus

Page 23

Valuation and recommendation

Trading at a discount to banks. The listed multi-finance companies are trading at a significant discount to the banks despite the fact that most of them have superior ROE. The strong and established ones such as BFIN and ADMF have much better NIM which compensates for their higher operating costs and credit costs. This translates into higher ROE levels. Some other good names such as ASDF, BCAF, MTF and FIF are not listed. The listed multi-finance companies are trading at a significant discount compared to the banks. On average, the listed multi-finance companies trade at 0.8x FY16 BV vs banks‘ 1.3x FY16 BV. We have used historical BV as most of the other listed multi-finance companies do not have consensus forecasts. Upside is attractive but discount with the banks will still prevail. We highlight that multi-finance companies generally have riskier business models as well as governance issues. Furthermore, there are also views that multi-finance companies can still enjoy their current niche position because the banks are still getting good margins from the bigger ticket size loans. This means that the banks (without any multi-finance companies as subsidiaries or associates) could decide to enter the financing business if they want to. The gap in regulatory supervisory and corporate governance will narrow. The regulators have been proactively issuing supportive regulations for multi-finance companies. Recently, OJK has pushed for multi-finance companies to adopt NPL recognition and provisioning policies that are similar to banks’. Going forward, we would not discount the possibility of the introduction of more uniformed regulations vis-à-vis banks, including capital requirements. BFIN (BUY, TP Rp5,000) is our top pick. We like BFIN for its unique business model that has proven to be resilient even during economic downturns. It has a strong value proposition that is supported by its back-end processes, which enables it to expand into the refinancing business. BFIN is currently underleveraged with a net gearing of below 2x, much lower than the industry average and regulatory limit. We believe that its currently high ROE of c.20% can further improve if it decides to gear up and grow more aggressively, albeit prudently. CFIN (HOLD, TP Rp 300) has a lot of potential. CFIN offers a wider range of financing products: leasing, consumer financing (mostly used cars), and factoring. Recently, it is expanding its new 4W financing business by teaming up with its bank parent

(Panin Bank) through a channelling arrangement. CFIN is also underleveraged with a gearing ratio of below 1x and still has ample of room to grow. Indirect plays via banks for unlisted multi-finance companies: Bank Central Asia (BBCA) – BCAF. BCAF’s business is

mainly in new 4W financing, with some used 4W financing. It targets the top-tier customers with lower risk by offering very competitive pricing. It uses BBCA’s balance sheet through a joint-financing arrangement with low cost of funds, which translates into lower pricing for the products offered.

Bank Mandiri (BMRI) – MTF. MTF is consistently growing market share for its new 4W financing business, thanks to the strong synergies with its bank and dealer parentage.

Bank Danamon (BDMN) – ADMF. ADMF has a strong track record, brand name, and network across Indonesia. It had previously focused on the 2W financing business and 4W commercial segment. However, its new 4W financing business is gaining importance as ADMF is trying to rebalance its business portfolio following the weak commercial and 2W performance in the past few years. ADMF also derives a lot of synergies with its bank parent (BDMN) in terms of cross-selling bank, insurance, and financing products.

Astra International’s gold mine – ASDF, FIF, and TAFS. ASDF, FIF, and Toyota Astra Financial Services (TAFS) are the subsidiaries of the Astra Group and part of its automotive business value chain. They mostly offer Astra-related brands such as Toyota and Daihatsu for 4W and Honda for 2W. Both ASDF and FIF are the market leaders in the new 4W and 2W financing space, thanks to the support of the Astra Group which has also been performing well in the past few years. Opportunities among multi-finance companies. We believe they are opportunities for the smaller multi-finance players, both organic and inorganic, in this current operating environment. For example, when Bank Maybank Indonesia (BNII) sold WOM Finance (WOMF) to Reliance Group, WOMF’s share price spiked up by 43%. Key concern: Stock liquidity. The main concern investors may have is the limited stock liquidity. The size of these companies is also much smaller compared to the banks. Key risks for the sector. Weakening automotive business and lower commodity prices. A spike in inflation can also erode the purchasing power of middle- to low-income earners which are the main customers of multi-finance companies.

Industry Focus