indonesia recent economic development, challenges and

TRANSCRIPT

Indonesia Recent Economic Development,

Challenges and Policy Response

Mirza Adityaswara

Senior Deputy Governor

April 4th 2018

#

2

‘17 ‘18 ‘19 ‘17 ‘18 ‘19 ‘17 ‘18 ‘19

WORLD 3.2 3.7 3.8 3.8 3.8 3.9 3.7 3.7 3.9 3.9

AE 1.7 2.4 2.3 2.1 2.3 2.3 2 2.3 2.3 2.2

US 1.5 2.3 2.6 2.4 2.3 2.6 2.2 2.3 2.7 2.5

Euro 1.8 2.5 2.3 2.0 2.4 2.1 1.8 2.4 2.2 2.0

Japan 1 1.8 1.2 0.9 1.7 1.3 1.1 1.8 1.2 0.9

EM 4.3 4.6 4.8 5.0 5.2 5.3 5.2 4.7 4.9 5.0

China 6.7 6.9 6.7 6.5 6.8 6.5 6.3 6.8 6.6 6.4

India 7.1 6.4 7.2 7.5 6.4 7.4 7.4 6.7 7.4 7.8

WTV 1.4 4.5 4.5 4.5 4.7 4.6 4.4

Oil (USD per barel)* 41 52 60 57 52.7 59.9 56.4

IHex 5.4 21.7 2.8 -2.9

LIBOR 3 month 0.7 1.26 2.33 2.72

Jan'182016

Bank Indonesia CF WEO

Feb ‘18 Jan ‘17

-3.59-4.24 -4.26

-2.37-2,23

-5.0-4.5-4.0-3.5-3.0-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.53.03.54.0

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

*

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% GDP

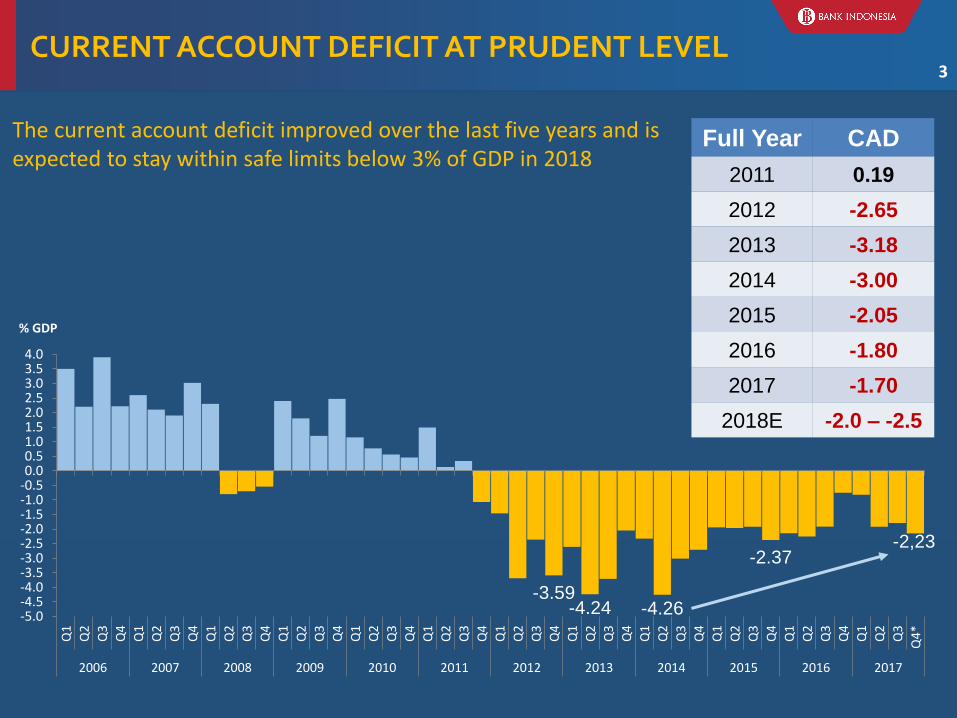

Full Year CAD

2011 0.19

2012 -2.65

2013 -3.18

2014 -3.00

2015 -2.05

2016 -1.80

2017 -1.70

2018E -2.0 – -2.5

The current account deficit improved over the last five years and is expected to stay within safe limits below 3% of GDP in 2018

CURRENT ACCOUNT DEFICIT AT PRUDENT LEVEL3

CURRENT ACCOUNT DEFICIT COMPARISON4

3.01.0

5.7

25.0

16.1

-5.7

0.22.6 2.5

23.0

11.2

-9.0

-1.7

11.7

-0.1

19.3

3.0

-3.8

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

ID TH PH SG MA TR

2006 2011 2017 Source: bloomberg

% GDP

5

* Provisional figure, ** very provisional figure, ***(e) forecast

(10.00)

-

10.00

20.00

30.00

40.00

50.00

1 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111 3 5 7 9111

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

CPI Core VF AP

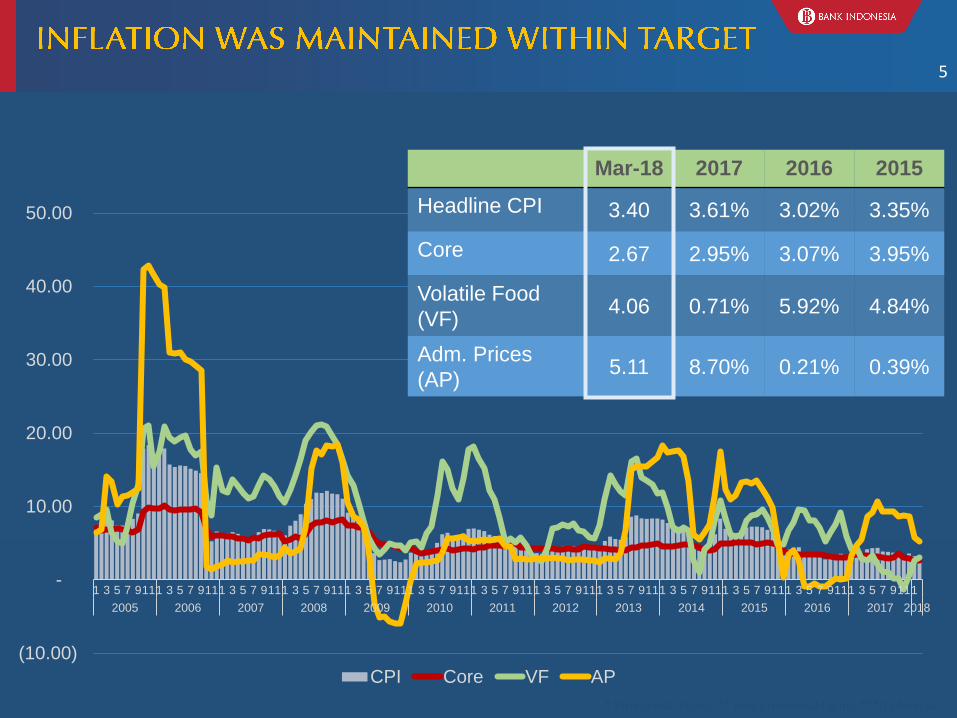

Mar-18 2017 2016 2015

Headline CPI 3.40 3.61% 3.02% 3.35%

Core 2.67 2.95% 3.07% 3.95%

Volatile Food

(VF)4.06 0.71% 5.92% 4.84%

Adm. Prices

(AP)5.11 8.70% 0.21% 0.39%

29

PDRB ≥ 7,0% 5,0% ≤ PDRB < 6,0% 4,0% ≤ PDRB < 5,0% PDRB < 0%6,0% ≤ PDRB < 7,0% 0% ≤ PDRB < 4,0%

KALTARA6,17

Source: BPS

KALTARA6,46

4

ACEH4,19

SUMUT5,12

RIAU2,71

SUMBAR5,29 JAMBI

4,64

BENGKULU4,99

SUMSEL5,51

LAMPUNG5,17

KEP. RIAU2,01

KEP. BABEL4,51

KALBAR5,17

KALTENG6,74

KALSEL5,29

BANTEN5,71 JABAR

5,29

DKI6,22

JATENG5,27 JATIM

5,45

BALI5,59

NTB0,11

NTT5,16

SULUT6,32GORONTALO

6,74

SULTENG7,14

SULBAR6,67

SULSEL7,23

SULTRA6,81

MALUKU5,81

MALUT7,67 PAPBAR

4,01

PAPUA4,64

KALTIM3,13

DIY5,26

#

7

-10.0

-9.0

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

%

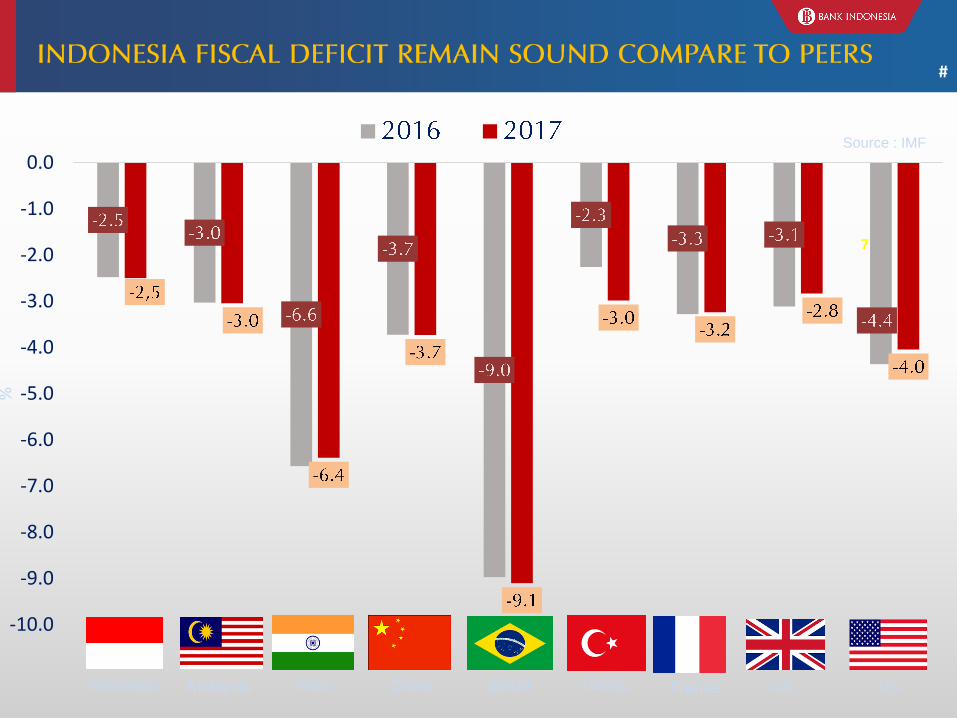

Indonesia Malaysia USIndia China Brazil Turkey

Source : IMF

UKFrance

8

8

Loan to Deposit Ratio (%)Liquidity Ratio

Capital Adequacy Ratio (%)NPL Gross & Coverage Ratio

As of Jan’18

111.12%

45.84%

88.72%

40%

50%

60%

70%

80%

90%

100%

110%

120%

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Feb

'18

23.71

16.0

23.25

15

16

17

18

19

20

21

22

23

24

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

Jan-17

Jul-17

Jan-18

109

50

23

8.5

0

5

10

15

20

25

30

35

40

45

0

20

40

60

80

100

120

140

160

180

200AL/NCD AL/DPK (RHS)

2.88

116

0

20

40

60

80

100

120

140

160

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

NPL (%) Coverage Ratio% (rhs)

Further relaxation of LTV for property loans (Sept)

Strengthening systemic surveillance & Crisis Management Protocol (April)

E-money for social transfer (Nov)

Financial Technology (FinTech) Office (Nov)

New Rupiah issuance (Dec)

Obligation to use IDR in domestic transaction (March)

Non-cash movement (GNNT)

Market-based exchange rate stability consistent with fundamental Dual intervention in the FX market and purchases of government bonds

from secondary market in time of distress (capital reversal) or large mis-alignment

• BI 7-day RR Rate cut of 25bps to 4.50% (Aug)

• Further BI 7-day RR Rate cut of 25 bps to 4.25% (Sept)

• Further lowering RR by 100bps to 6.5% (Feb)

• Lowering RR by 50bps to 7.5% (Nov)

Policy Rate cuts of 150bps

Moving from BI Rate (12 month) to BI 7-day Reverse Repo Rate (Aug)

1. Monetary Policy

Policy Rate

Reserve Requirement

2. Exchange Rate Policy

3. Macroprudential Policy

• Relaxation of LTV for property and automotive loans (June)

• BI Rate cut of 25bps (Feb)

• Implementation of RR Averaging (Aug): RR fixed 5%; RR Averaging 1.5%

Initiative to issue macroprudentialregulation on Financing to Funding Ratio (FFR)

4. Payment System Policy

National Payment Gateway (June)

Modernized cash management underway

2015 2016 2017

Impacts of LTV Relaxation

Monetary Transmission

Policy Rate↓ 200 bps

(Jan‘16 – Sept’17)

RR↓ 150 bps

(Dec’15 –Mar’16)

Deposit Rate(Jan’16 – Jan’18)

↓ 196 bps (5.98%)

Lending Rate(Jan’16 – Jan’18)

↓151 bps (11.32%)

Deposit(Jan’17 – Jan’18 (LBU)

Total ↑ Rp403 T (8.36% yoy)

Lending

(Jan’17 – Jan’18 (LBU)Total ↑ Rp319 T (7.40% yoy)

Des-16 Des-17

Construction 20.33 15.48

Real Estate 22.22 5.67

Housing 7.67 10.53

Total 7.86 8.24

LoanGrowth % (yoy)

9

#

11

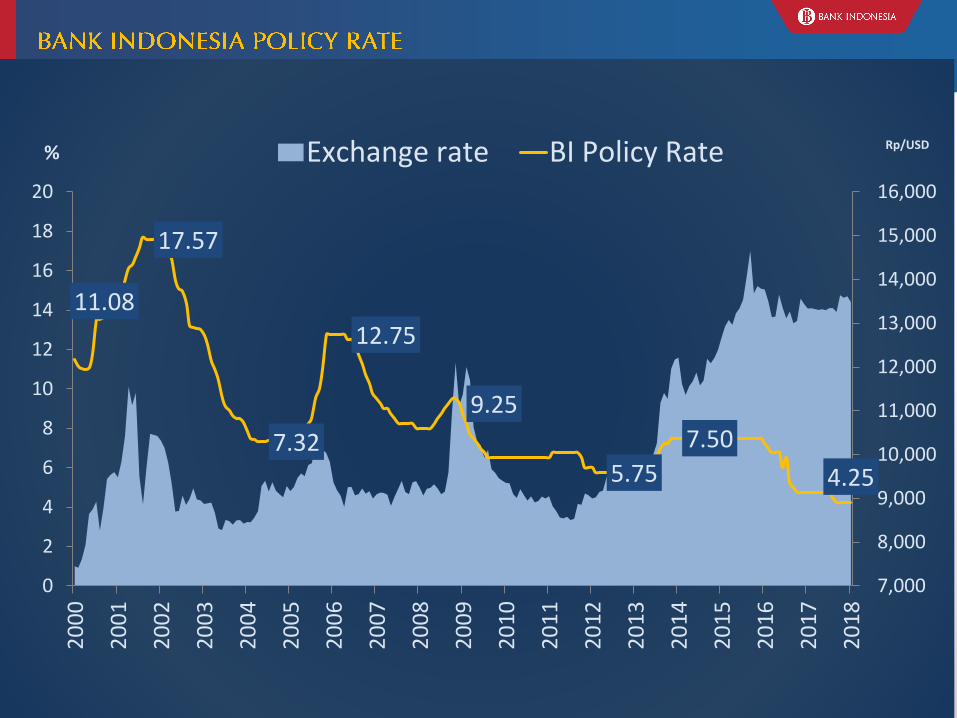

11.08

17.57

7.32

12.75

9.25

5.75

7.50

4.25

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

0

2

4

6

8

10

12

14

16

18

20

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

Rp/USD% Exchange rate BI Policy Rate

12

21.6 B

2018

18.6 B2017

99% are related to digital payment, 0.11% to

personal finance and 0.08% to Business FinanceProjection of transaction value (statista, 2018)

*Transaction Value

Forecasted

Transaction value

(Increasing by 16.13%)*

Actor

(Growing by 34.29%)**

1882017

1402016

Source: Data Statista

INTERNETuser ratio to

adult population

(Nov‘16) 2

51,8%

MOBILE PHONERatio to adult

population (Jan'16)1

YOUNG GENERATION (10-29 year)3

26,4% (2010)

24,9% (2016) (estimation)

59,2 million unitTotal

60,34% Total PDB

Share

20164SME126%

Source: 1 Kominfo, 2016; 2 APJII, 2016; 3BPS, 2013; 4Kementerian KUKM, 2016 dan BI, CNN

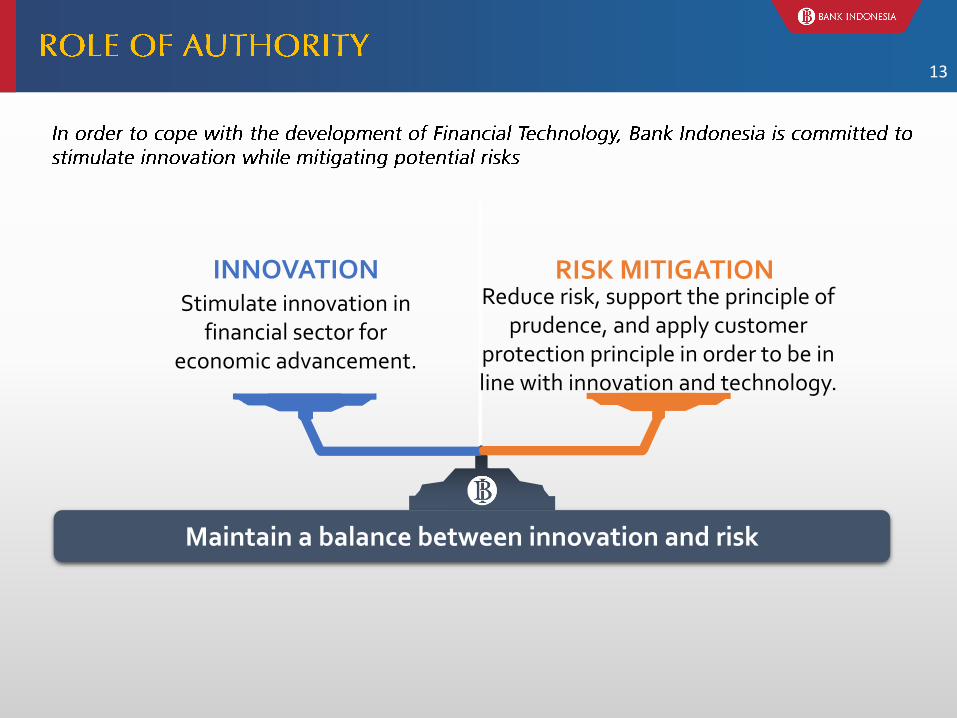

13

Reduce risk, support the principle of prudence, and apply customer

protection principle in order to be in line with innovation and technology.

RISK MITIGATIONStimulate innovation in

financial sector for economic advancement.

INNOVATION

Maintain a balance between innovation and risk

14

Regulation on

National Payment

Gateway

Nov 2016

Financial

Technology

Office

Jul 2017

Regulation on

Payment Transaction

Processing

Sept 2017Des 2016 Nov 2017

Regulation on

AML/CFT for

Non-Bank FI

Regulation on

Financial

Technology

Nov 2017

Regulatory

Sandbox

#

Family Hope Program(Program Keluarga Harapan -

PKH)

Non Cash Food Assistance (Bantuan Pangan Non Tunai -

BPNT)

• The Family Hope Program (PKH) is a program that provides cash to very poor households. Rp 1,89 million /year will be granted for each household. PKH will be granted every February, May, August, and November.

• As of December 2017, PKH is distributed to6,0 million households on non-cash basis.

• PKH will be expanded to 10 millionhouseholds in 514 regencies/cities in 2018.

• BPNT is a poverty alleviation and socialprotection program that is managed by thecentral government. It provides subsidized riceand eggs to low-income households. Rp 110thousand/month will be granted for eachhousehold as BPNT that can be used incertain stores which called e-warong.

• As of December 2017, BPNT was distributed to1,2 million households in 44 cities.

• BPNT will be expanded to 10 millionhouseholds in 217 regencies/cities on the25th of each month in 2018.

#

•

•

Thank You

17