industrial fasteners institute fasteners institute . ... introduction this is the thirteenth ifi...

TRANSCRIPT

Annual Report

2012

I ND U S TR I A L F A S T E N ER S I NS T I TU T E 2 0 1 2

OFFICERS Chairman, David L. Monti ........................................................................... Fall River Manufacturing Co., Inc. Vice Chairman, Steve Paddock .................................................................................................... Böllhoff, Inc. Immediate Past Chairperson, Jennifer Johns Friel .................................................. Mid West Fabricating Co.

BOARD OF DIRECTORS Preston Boyd .................................................................................................................. Tramec Hill Fastener J. J. McCoy .............................................................................................................................. Nucor Fastener Jim Springer ............................................................................................................ Industrial Nut Corporation Larry Valeriano .................................................................................... California Screw Products Corporation Pat Wells ............................................................................................................... The Young Engineers, Inc. Owe Carlsson .......................................................................................................... Alcoa Fastening Systems Mark Quebbeman ........................................................................................................... Semblex Corporation David Lomasney ................................................................................... MacLean-Fogg Component Solutions David Hebert ............................................................................................................................. SFS intec, Inc. Bruce Smith .............................................................................................. Carpenter Technology Corporation

DIVISION OFFICERS DIVISION I: INDUSTRIAL PRODUCTS Chairman, Brad Tinney .......................................................................................... Birmingham Fastener, Inc. Vice Chairman .................................................................................................................................. Vacancy DIVISION II: AEROSPACE PRODUCTS Chairman, Donnie Autry ......................................................................................................... MacLean-ESNA Technical Chairman, Owe Carlsson ........................................................................ Alcoa Fastening Systems Vice Chairman, Mike Lawler ................................................................................................. PennEngineering DIVISION III: AUTOMOTIVE PRODUCTS Chairman, Jason Surber .................................................................................................................... ATF, Inc. Vice Chairman .................................................................................................................................. Vacancy

ASSOCIATE SUPPLIERS’ DIVISION (ASD) Chairman, Alan Hariton .............................................................................. Hariton Machinery Company, Inc. Vice Chairman, Matt Delawder ......................................................................................................... SWD Inc.

T A B L E OF C O NTE N TS EXECUTIVE SUMMARY ............................................................................................................................... 1 INTRODUCTION ........................................................................................................................................... 1 General Economic Environment ....................................................................................................... 3 The Fastener Industry....................................................................................................................... 4 Automotive ........................................................................................................................................ 5 Aerospace ........................................................................................................................................ 6 Industrial Products ............................................................................................................................ 8 Imports/Exports ................................................................................................................................ 8 Government Affairs ........................................................................................................................... 9 INSTITUTE OPERATIONS .......................................................................................................................... 13 MEMBERSHIP SERVICES ......................................................................................................................... 15 ENGINEERING TECHNOLOGY ACTIVITIES ............................................................................................. 18 Fastener Standards Activities ......................................................................................................... 18 ASME Standards Revisions ............................................................................................................ 19 ASTM Standards Revisions ............................................................................................................ 20 SAE Standards Revisions ............................................................................................................... 21 ISO Standards Revisions ................................................................................................................ 21 IFI Standards Revisions.................................................................................................................. 23 Educational Programs .................................................................................................................... 23 IFI Products and Publications ......................................................................................................... 24 DIVISION I: INDUSTRIAL PRODUCTS ....................................................................................................... 25 DIVISION II: AEROSPACE PRODUCTS ..................................................................................................... 25 DIVISION III: AUTOMOTIVE PRODUCTS .................................................................................................. 26 ASSOCIATE SUPPLIERS’ DIVISION (ASD) ............................................................................................... 26 2010 – 2015 STRATEGIC PLAN ................................................................................................................. 27 2013-14 CALENDAR ................................................................................................................................... 38

1

EXECUTIVE SUMMARY

In brief summary of what you will read in the 2012 Annual Report, the following is highlighted:

• The fastener industry again had a good year in a continuing recovery from the recession. Automotive joined aerospace in realizing steady growth in sales volume, though aerospace production fell due to continuing delivery problems with new model aircraft. Industrial products did well depending on what segment is served. Even housing showed solid signs of recovery by year end. IFI had a $21,215 profit from operations and a $150,730 total profit net of unrealized gains. IFI now has $1,572,670 in Reserves.

• The U.S. economy showed 2.2% GDP growth, while Europe largely remained in recession and China’s GDP growth slowed to 7.1%. In parts of Asia, the earthquake/tsunami hangover continued and many manufacturers continued to rethink their logistics. The “produce-in-the-region-for-the-region” model gained in popularity. Mexico is probably becoming the most popular destination for manufacturing expansion, particularly in automotive.

• Presidential politics, a Congressional partisan divide, U.S. debt and serious uncertainty about the government’s ability to rationally govern depressed most new capacity investment and manufacturing employment leaving company’s generally with healthy balance sheet, profitable operations but with unrealized potential market share gains and a whole lot of cash in their coffers.

• As the year ended, the “fiscal cliff”, taxes and the national debt resulted in a shift from optimism about the future to some real pessimism looking forward. The kick-the-can down the road resolution of the “cliff” pleased the stock market but did not supply the certainty business needed to invest or hire.

INTRODUCTION

This is the thirteenth IFI Annual Report to the Membership summarizing the operations, financial position and value delivered to our members, while depicting the economic, political and business environment in which we operated in 2012. It also projects what that environment is projected to look like in 2013. We are going to dispense with the graphs this year, as they would all simply point to slow but stubborn growth. In general, 2012 was a good year for the fastener industry with strong growth in the automotive, aerospace and energy sectors, some government stimulated growth in construction and even a turnaround in housing. U.S. GDP growth will settle out to have been about 2.2% with 2013 expected to be worse at about 1.7%, largely due to continuing business uncertainty limiting business investment and hiring, and with small and

2

medium size business inheriting higher taxes due to the failure to truly deal with the “fiscal cliff”. The Congressional Budget Office projects the handling of the “fiscal cliff” will add $4 trillion in new U.S. debt over the next 10 years, a national debt now standing at $16.1 trillion. This tends to point to what could be another possible credit downgrade, meaning new investment would be overseas, not in the U.S. Solving this debate on fiscal policy will not be easy because it is really a dispute on the role of the state in people’s lives. The year end U.S. trade deficit was about $500 billion (mostly China & oil) and the Federal deficit was greater than $1 trillion. The ISM ending 2012 was positive and indicative of the continuing very slow recovery at 50.7, with New Orders flat at 50.3, Backlog down at 48.5, Production also down 1.1 points to 52.6 and Exports continuing up 3.5 points to 51.5. U.S. fastener exports were up with the top five buyers being Canada, Mexico, the U.K., China and France. Deliveries were up 4.4 points to 54.7. These numbers reflect some stability in manufacturing but no rush to expansion. For perspective, China’s PMI ended 2012 at 50.6, a real slow down, with a potential further negative impact on raw material prices. In 2012 the U.S. economy added 1.8 million jobs (150,000/month average) but 356,000/month is needed to reduce unemployment to the 6% range, which is not happening now or in 2013. Unemployment in 2013 probably stays at 7.8% or possibly rises. It’s been rumored that the Obama Administration’s best jobs program has been in convincing Americans that they don’t want a job, or to settle for part-time work, or the true unemployment rate would be 14.4%. Operationally, as noted, IFI ended 2012 with a $21,215 profit from Operations, and a $150,730 overall profit, excluding unrealized gains. We also added $189,094 for a very healthy $1,572,670 in Reserves at market value. On staff we continue with Joe Greenslade, Director Technical Engineering; Bob Hill, Div. I – Industrial Products Manager; Pat Meade, Div. II – Aerospace Fasteners Manager; John O’Brien, Div. III – Automotive Industries Fastener Group Manager; Barbara Grachanin and Michelle Lightfoot, Administrative Assistants and Rob Harris, Managing Director. The Laurin Baker Group continues as our Washington Representatives; Bev Malcolm handling Meeting Planning; Walthall & Drake as our Auditors and with Jones Day as legal counsel. At year end we purchased, installed and commenced training on Quick Books as our accounting system, as the old MAS-90 system would not be supported in 2013 without an investment many times more expensive than purchasing Quick Books. The transition was effective 01/01/2013.

3

GENERAL ECONOMIC ENVIRONMENT The “Introduction” provided a healthy dose of 2012 economic results, particularly in North America, so here we will try to put it in perspective vs. the world, as the world situation impacts and is a drag on the U.S. economy. Countries which are in economic recovery are the U.S., China and Brazil. Those where there is some expansion, i.e., thus providing a market for U.S. goods, include Canada, Mexico, western South America, Russia, Australia, S.E. Asia, Turkey and Poland. Countries currently considered at economic risk include Argentina, S. Africa, India, Sweden and most of Central Europe. Countries still in recession are the U.K., France, Spain, Italy, Portugal, Japan, Finland and Greece. For 2013, GDP growth is expected to be +2% in the U.S., +1% in Germany and the U.K., +0.6% in Japan, +3.5% in Russia, +4.6% in Brazil, +6.2% in India and an amazingly low +7.8% in China vs. double digit growth the last several years. Many think Western dominance of the world economy has already ended, but looking at key countries’ relative share of world GDP, it’s the U.S. with 29.4%, China with 9.4%, Japan with 8.7%, the U.K, with 5.2%, Brazil with 3.4% and India with 2.7%. Our internal consumption in the U.S. is the key to our dominance of the world’s economy and that won’t be overtaken for quite a while. China is surging forward, but their internal demographics are already starting to apply the brakes. For the 10 years from 2002 to 2012, their population grew from 1.284 billion people to 1.347 billion, while the number of urban dwellers increased from 39% of the population to 51%. Average per capita income over the same time period for urban dwellers grew a whopping 372% from $931/year to $3,461 which explains a lot about why shipping jobs to China is now an iffy thing, and their internal consumption has a long way to go to anywhere catch up to western countries. That keeps them an export driven economy, bad for everyone, even the Chinese. Focusing on manufacturing, the U.S. remains the No. 1 manufacturer in the world, with China expected to pass us in the next few years. That stems from it being 20% more expensive to manufacture here than our 10 closest competitors. This is because we have the highest tax rates on business in the world and the regulatory burden we operate under also adds 11% to our costs, with air and water regulations alone adding 6.2% (vs. 3.5% in the U.K. for comparison). U.S. health care costs have risen 83% in the last 10 years while product sales prices have only risen an average of 2.1%. That’s simple math! No tort reform has been enacted yet and that cost U.S. business $250 billion in 2012, or 2% of GDP. Adding to all these basic cost of operations issues is the fact that our No. 1 competitor – China – is still allowed to manipulate its currency with the Yuan still being about 30% under valued. We are still “top dog” but the burden is heavy and the current Administration seems intent on adding to it.

4

There are, however, those who still see promise in the future. They believe though we may slog thru 2013, while in 2014 things really start to take off everywhere except Europe and Japan. They see the U.S. making real progress on the debt issue and that it will stabilize with the debt-to-domestic product ratio staying at about 73% for the next decade – still too high but not at 100%+ like most of southern Europe. Their aging population makes it very difficult to recover by growing revenues versus our positive birth rate and continuing immigration, which makes for a bigger pie from which to draw. There is already a legislated cap on new discretionary spending through 2021, the “fiscal cliff” deal tax additions increase government revenues by about $740 billion and either “sequestration,” or an equivalent approach to cutting debt will cut spending by $2.3 trillion. That’s a $3 trillion impact on U.S. debt over a 10 year period. THE FASTENER INDUSTRY We have little new information on the industry as we have not purchased Freedonia or any other group’s industry studies in at least eight years. As noted, in keeping with general industry performance, fastener sales to the automotive, aerospace and energy sectors were very strong and most other sectors OK, with even home sales at a 3 year high. The best information available would show: U.S. Fastener Consumption $14.0 B U.S. Made & Used in U.S.: $9.2 B Imported $4.8 B U.S. Exported: $3.2 B Total U.S. Produced $12.4 B Freedonia’s latest publicly available data showed 2011 world sales at $64.4 B with $14.1 B in the U.S.; $24.65 B in Asia of which $9.5 B was in China and $6.5 B in Japan; $16.3 B in Europe and $9.35 B all other. Worldwide sales growth averaged 5.2% with 3.7% in North America; 7.4% in Asia (10.8% in China) and W. Europe 2.6%. The projection for sales in 2016 is $82.9 B with $18.5 B in North America; $32.5 B in Asia (China $15.9 B). Fastener manufacturers reported capacity utilization on average down to 69.3% from a 73% average in 2011. It is expected capacity utilization will increase very slightly in 2013. Finding capable employees remained a key concern in 2012 and IFI continued to expand its industry training programs. Our program with El Camino College training aerospace fastener manufacturing personnel continued with multiple groups graduating and entering the industry. Similarly, our IFI/FTI fastener specialist training programs continued to expand with week long programs in LA and Cleveland and the two day automotive program in

5

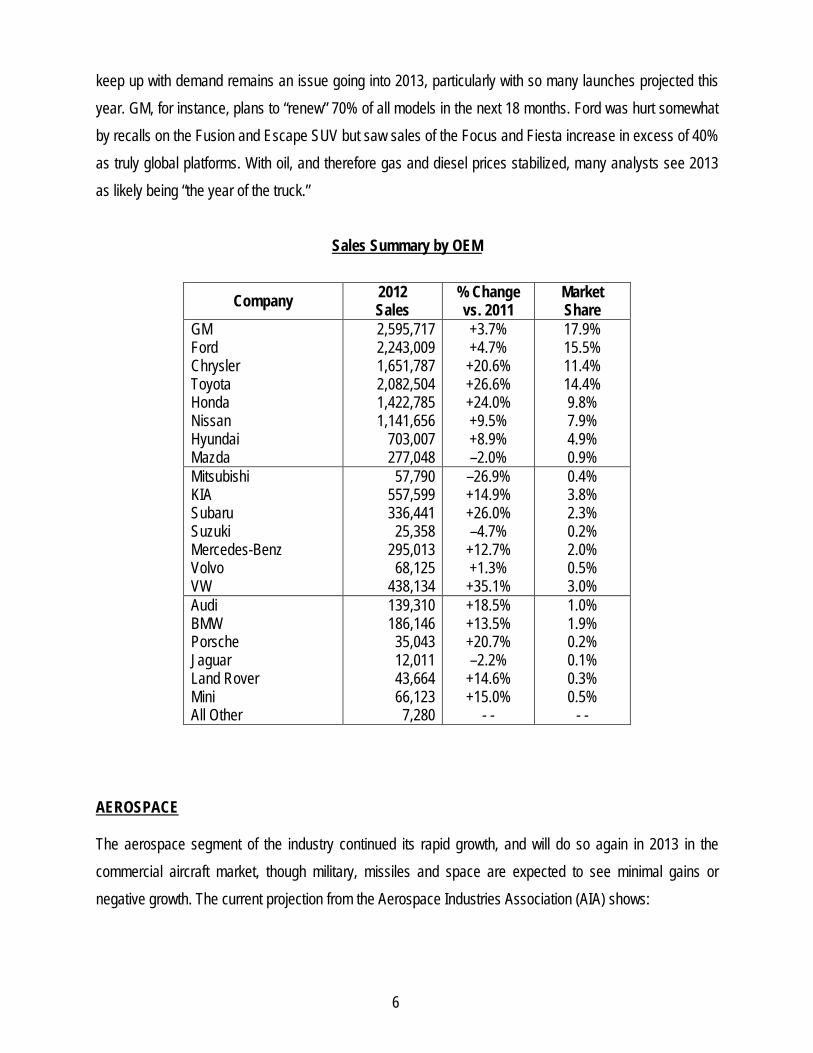

Detroit. In 2013 this will further expand to three full week programs with two in Cleveland and one in LA, two 2 day automotive programs with 1 each in Detroit and Cleveland and a new 2-3 day aerospace program in the LA area and two new hydrogen embrittlement workshops, one each in Detroit and LA. The IFI/FTI workshops generated $25,766 in new revenue for IFI. The availability, supply and pricing of raw material – mainly CHQ and IQ wire and rod – was less of an issue than in past years with more than 50% reporting no availability problems but about a third reporting steel price increases of up to 10%. The slow down in China definitely took pressure off the market. Wire rod prices seemed to nicely track the scrap market though CHQ mills worked hard at resisting much of a collapse in prices. During the year, we saw spot market prices for wire FOB mill rise for some as noted but in the 2/H they generally eased down from $660-680/NT to the $640-660 range in the face of import prices from China hitting $585-605/NT. Turkish wire was a little higher in the $620-640/NT range, all port of entry. The wire rod supplied to the U.S. from offshore sources which totaled 1,067,850 (up 8% vs. 2011) is interesting, with about 425,000 M/T coming into the U.S. from Canada, 78,000 M/T into the U.S. from Mexico and 564,800 M/T coming into the U.S. from offshore elsewhere. Total wire rod consumption in the U.S. was projected to be about 3.5 M M/T. Oil prices ended the year significantly down from their highs for the year at about $95/barrel. U.S. oil imports were also way down and expected to fall further with increased domestic supply. The current $90-100 oil price range was substantially maintained due to Saudi production cut backs. The new domestic oil production outlook for North America is further exacerbating European manufacturing competitiveness in world markets, as does our relatively weak dollar. AUTOMOTIVE The automotive manufacturing segment of the economy continued at a very healthy pace in North America with sales of greater than 14.5 million units. At year end the 12/12 pace was 15.4 million units which probably will cool but still points to higher sales again in 2013. In fact, ALIX PARTNERS are projecting 14.8 M units in 2013 and 15.3 M in 2014. IHS has projected that China will add 5 M units of new production between now and 2019, including Jeep, and that the losers will be all non-German European and some Japanese production. It is expected that both of these areas will add new capacity in North America. In 2012 the automotive market share was GM 17.9% up 3.7%, Ford 15.5% up 4.7%, Chrysler 11.4% up 21% with Toyota at 14.4%, Honda 9.8% and Hyundai/KIA 8.7%. The concern about the tiers suppliers’ ability to

6

keep up with demand remains an issue going into 2013, particularly with so many launches projected this year. GM, for instance, plans to “renew” 70% of all models in the next 18 months. Ford was hurt somewhat by recalls on the Fusion and Escape SUV but saw sales of the Focus and Fiesta increase in excess of 40% as truly global platforms. With oil, and therefore gas and diesel prices stabilized, many analysts see 2013 as likely being “the year of the truck.”

Sales Summary by OEM

Company 2012 Sales

% Change vs. 2011

Market Share

GM Ford Chrysler Toyota Honda Nissan Hyundai Mazda

2,595,717 2,243,009 1,651,787 2,082,504 1,422,785 1,141,656

703,007 277,048

+3.7% +4.7% +20.6% +26.6% +24.0% +9.5% +8.9% –2.0%

17.9% 15.5% 11.4% 14.4% 9.8% 7.9% 4.9% 0.9%

Mitsubishi KIA Subaru Suzuki Mercedes-Benz Volvo VW

57,790 557,599 336,441 25,358

295,013 68,125

438,134

–26.9% +14.9% +26.0% –4.7%

+12.7% +1.3% +35.1%

0.4% 3.8% 2.3% 0.2% 2.0% 0.5% 3.0%

Audi BMW Porsche Jaguar Land Rover Mini All Other

139,310 186,146 35,043 12,011 43,664 66,123

7,280

+18.5% +13.5% +20.7% –2.2%

+14.6% +15.0%

- -

1.0% 1.9% 0.2% 0.1% 0.3% 0.5%

- -

AEROSPACE

The aerospace segment of the industry continued its rapid growth, and will do so again in 2013 in the commercial aircraft market, though military, missiles and space are expected to see minimal gains or negative growth. The current projection from the Aerospace Industries Association (AIA) shows:

7

AIRCRAFT Total Related Sales Year Sales Civil Military Missiles Space Products Change 2012 $217.87B $60.59B $58.24B $23.13B $44.90B $31.01B +3.4% 2013 $223.55B $67.48B $56.81B $21.84B $45.60B $31.82B +3.0%

BOEING regained its position as No. 1 in civil aircraft sales and deliveries (585) in 2012 and that was before selling an additional 50 aircraft late in December. With their backlog they added more than 5,000 new jobs in Washington state alone in addition to completing staffing in Charleston, SC. BOEING also pressed ahead on several new aircraft – the 737-MAX, the 787-9 and 787-10, which was approved by their Board, but the 777X has not yet been given full approval. Their plans call for delivery of ten 787s/month, with 844 cumulative orders in hand, but teething pains continue to plaque the aircraft. They also will increase 737 deliveries from 35 to 38 aircraft/month. With the 787, Boeing outsourced not just the manufacture but also the design of large segments of the aircraft, an approach not expected to be repeated in the immediate future, given the aircraft’s problems. AIRBUS also did well with the A320 NEO outselling the 737 by 680 aircraft, but AIRBUS also had some misfires on other programs. The A350 is competing well against the 777 and 787, primarily by consuming 25% less fuel, but the future of the A380 is raising questions with 18 airlines having ordered to date with 262 firm orders, 36 options and 97 deliveries. In 2012, 9 new orders were received; a major slow down. BOEING’S market outlook says there is lots of work to come with their analysis showing that while the demand for commercial aircraft in 2010 was 19,410 planes, in 2020 it is projected to be 28,500 planes and now has grown to 39,530 in 2030 – 104% growth in the next 20 years with the market for the aircraft split as follows: Asia/Pacific – 300% growth N. Africa/Middle East – 190% growth N. America – 40% growth It is noted that the major growth will be in the single and twin isled aircraft, not in the jumbos. The other major finding, already happening, is the shift of long haul market share away from North America and Europe to the “Gulf 3” – EMIRATES, ETIHAD & QATAR with their new equipment, superlative airports and ideal geographical location to service all continents.

8

INDUSTRIAL PRODUCTS

As noted earlier, which industrial markets you supply largely determine your 2012 results. Most were “OK” to “Good” with the exception of non-residential construction. In that segment the energy segment did well (about $55 B in projects) but most other construction showed little growth over 2011. JOHN DEERE and agriculture in general had a very strong year. DEERE had revenues of about $3.6 B up 13% vs. 2011 and net income up 9% from the prior year. This was DEERE’S highest ever revenues and profits and they entered 2013 holding over $5 B in cash. Heavy truck sales recovered nicely in 2012 with over 230,000 class 8 units sold vs. 160,000 units in 2011 and even worse the four years preceding that. Other class trucks had similar 2012s, mostly due to replacement requirements and not absolute market growth. CATERPILLAR had a record year with $65.9 B in sales (+10% vs. 2011) and record profits. 2013 is expected to be impacted by the economic slow down in China and Europe which drives down the demand for raw materials – iron ore, etc. – big consumers of CAT equipment. CAT’s profits were affected by a $580 M write down in China due to accounting malfeasance. CAT says uncertainty requires caution in projecting 2013 sales of between $60-68 B, and that’s a lot of uncertainty! Perhaps most interesting in the appliance sector was that the U.S. Department of Commerce found dumping by Mexico and S. Korea in the large washer segment. The assigned dumping margins ranging from 9% to just over 82% which has impacted shipping from those countries. As usual, appliance tends to follow new housing (plus replacements) so the residential construction recovery is expected to bode well for appliance in 2013. IMPORTS/EXPORTS

IFI’s 2012 Import/Export Report will show a continuing shift in import totals and their country of origin.

• Fastener Imports totaled $4,813.876 in value or 3,105,341,531 ($1.55/lb.) pounds in weight.

• Fastener Exports totaled $3,227.797 in value or 960,857,760 ($3.36/lb.) pounds in weight.

• The top export countries of origin were:

9

Country Value ($M) % of Total % Change vs. 2011 World 4,813.876 100 + 10.6 Taiwan 1,426.342 29.6 + 3.9 China 1,129.385 23.5 + 10.8 Japan 730.065 15.2 + 30.3 Canada 281.577 5.9 – 4.2 Germany 254.196 5.3 + 9.5 S. Korea 195.895 4.1 + 37.8 Italy 107.147 2.2 + 5.4 Mexico 104.290 2.2 + 36.5 India 97.614 2.0 + 1.8 UK 87.245 1.8 + 10.6

GOVERNMENT AFFAIRS

The 2012 elections produced plenty of things to love or lament for both political parties and most citizens, but it seems to us that after all the sound and fury and a record amount of money spent, not much has changed. President Obama was reelected with 332 electoral votes—a lopsided victory from that standpoint. However, he did so with only 50 percent of the popular vote and with fewer total votes than in 2008. It seems clear that while the majority of voters were willing to give the President some more time, many of his original supporters were disillusioned. Democrats gained two seats in the Senate after Republicans managed to lose at least four races they were favored to win, including 2 incumbents. The new Senate breakdown will be 53 Democrats, 45 Republicans and 2 Independents who will caucus with the Democrats. That gives Majority Leader Harry Reid 55 votes—still short of the 60 votes needed to cut off debate. In the House, Republicans retained control with 233 seats and Democrats have 200 (there are two vacancies). As you have heard us say after every election, there’s no rest for the weary, and this year was no exception. Congress returned shortly after the election for a Lame Duck Session to resolve the fiscal crisis facing the country due to the January 1 expiration of the 2001 and 2003 Bush tax cuts affecting rates on income, interest, dividends, and estates; and the automatic budget cuts (sequestration) that kicked in at the same time unless Congress acted.

10

Ever been bungee jumping? In fact, President Obama and Congress actually managed to take the country over the so-called “Fiscal Cliff” on December 31 by failing to reach agreement on tax increases and spending cuts that expired at midnight that day. They then narrowly averted disaster with a “compromise” that jerked us back up on January 1. While the “compromise” did extend the expiring tax rates put in place by President George W. Bush in 2001 and 2003 for a large majority of individuals, it failed to address the looming spending cuts (other than to postpone them for two months). And by the way, while everybody was mesmerized by the death-defying leap off the cliff and the subsequent rebound, the U.S. also neared its statutory borrowing limit again, which means the debt ceiling will need to be raised pretty soon or we’ll face yet another financial crisis. Oh, and the continuing resolution funding the federal government expires on March 27th. So the adrenaline rush of being jerked back up the cliff may lead to severe headaches in the near future as pending automatic spending cuts, the debt ceiling, and a potential government shutdown once again create the possibility of economic turmoil. But for the moment, here’s a rundown of key provisions in the fiscal cliff compromise that might impact fastener manufacturers: The income tax brackets of 10%, 25%, 28% and 33% were permanently extended. The 35%

bracket was increased to 39.6% for individuals earning more than $400,000 ($450,000 for couples filing jointly). The President had urged that the 39.6% bracket start at incomes of $200,000 ($250,000 for couples filing jointly). This impacts fastener companies that are organized as “pass-through” entities (S Corps, LLCs or Partnerships) since the owners of those types of businesses pay taxes at the applicable individual rates.

The capital gains and dividend tax rates of 15% were permanently extended for individuals earning less than $400,000 ($450,000 for couples filing jointly). Above those levels, the rates will be 20% on both capital gains and dividends.

The Research and Development Tax Credit was extended for two years. The increased expensing of certain investments (Section 179) was extended for one year. The 50% bonus depreciation was extended for one year. The production tax credit for wind projects was extended for one year and now includes any project

on which construction has started by January 1, 2014. Even though the first 3 months of the year will be largely dominated by the series of looming economic crises, we also expect to see work begin on comprehensive tax reform, beginning in the House Ways &

11

Means Committee. IFI has been communicating with Members of Congress for the past year to ensure that they understand the makeup of the fastener industry and the key elements of comprehensive tax reform that will determine whether it is positive or negative for manufacturing in general and fastener manufacturers in particular. Outside of tax reform, the theme for the next two years will likely be regulatory action rather than legislative action. Agencies went relatively quiet in the months leading up to the election and they will now be emboldened in their agendas. In addition, even if Congressional action could undo the Agencies’ work, the President can veto that action and his veto would likely not be overridden. Unfortunately, that will mean that we have to play defense during public comment periods on proposed rules, and any adverse actions will require court action to overturn. Employee Free Choice Act/National Labor Relations Board (NLRB)/Department of Labor (DOL) We would not be surprised to see the Employee Free Choice Act reintroduced in the 113th Congress. However, given that the business community remains firmly opposed, the House remains in Republican hands and Senate Democrats still don’t have 60 votes required to break a filibuster, it is unlikely to pass. That doesn’t mean we won’t have to fight it, just to be sure. In fact, we expect most of the activity on labor/management issues to be on the agency side, particularly at the NLRB and the Department of Labor. IFI is an active member of the Coalition for a Democratic Workplace, which is involved in litigation against the NLRB’s ambush rule, poster rule and several cases affecting site access and bargaining units. Those cases will proceed in 2013 and we will keep you posted. We also expect DOL will issue the “persuader” rule soon, which affect employers’ ability to get advice and counsel on union issues, and we expect litigation will ensue. We will need to continue to mount whatever Congressional defenses we can, but the reality is that the last line of defense on NLRB issues for the next two years will likely be the courts. Export Controls Reform Beginning under the Bush Administration and continuing in the Obama Administration, efforts have been underway to revise and streamline the export controls regulations, and IFI has participated in this process. The key factor in determining whether parts such as fasteners are subject to export controls, and if so, to what extent, is whether they are “specially designed” for a military item that is subject to export controls. On August 3rd, IFI submitted comments on the proposed final definition of “specially designed” issued by

12

the Department of State and the Department of Commerce (Federal Register / Vol. 77, No. 118 / Tuesday, June 19, 2012). Generally IFI supports the Administration’s approach, and believes that the proposed definitions of “specially designed” would retain the International Traffic in Arms Regulations (ITAR) control of ONLY those critical fasteners that contribute to the properties of key U.S.-origin aircraft having low observable features or characteristics. All other fasteners would be subject to control under the Export Administration Regulations (EAR), but only if they are “specially designed” for military end items. We believe this is the right approach, as it retains the ability to control fasteners that meet the definition of “specially designed” while creating a streamlined “decision tree” process for determining which fasteners no longer warrant controls under ITAR or EAR. Energy There will continue to be a lot of discussion about the need for an “all of the above” energy policy. There is some renewed hope on increasing oil and gas exploration off the coastal states because the Senator that held the issue up for years has retired. The President is expected to approve the Keystone pipeline now that the election is over, and we expect natural gas exploration to continue at a robust pace but the federal government could begin to regulate hydraulic fracturing next year. Workforce Development The issue of workforce development will continue to be a hot topic as the House and Senate work on competing authorization bills. Conclusion With the possible exception of tax reform, 2013 will seem like more of the same—fighting to keep bad legislation from passing, but not being able to pass regulatory reform that would help manufacturing. Still, new Members of Congress and new Committee assignments always bring new opportunities to educate Washington about the industry! We remain honored to be able to serve industry in that capacity.

13

INSTITUTE OPERATIONS

The Institute did well again this year with the previously noted positive balances both from Operations and including special projects. Reserves continued to build to $1,572,670 at market value at year end. We continued to clean up the Balance Sheet and write off inventory we are no longer selling. Sales of the Inch Fastener Standards, 8th Edition continued to decline, as projected, but this project has generated a steady stream of new revenue in both the hard cover and, with the change in delivery system to a dongle based computer key, electronic version too. Selling the desktop printed version has eliminated the excess inventory problem encountered with earlier editions. The IFI Technology Connection subscription sales continued to grow; hitting $80,100 in revenue in 2012, and this is a sale that keeps on generating repeat revenue every year. The Institute’s Annual Meeting at the Four Seasons, Dallas, TX and the Fall Meeting at the Omni Parker House, Boston, MA were both very good events, rich in take home value and offered great networking opportunities. The Boston venue offered a great look back into America’s history and Dallas offered the opportunity to play golf in a near tornado on a classic PGA Course, and a true Texas Hold ‘em Tournament. The blend of technical, business, government affairs and economic forecasts were parts of both programs and favorable comments were received from many attendees. These meetings together were subsidized to the tune of $11,874 against a Board pre-approved subsidy of $15,000 to maintain meeting content and adjust meeting fees so additional attendees from a Member company would have lower cost. Coordination with other associations both in similar industries and those representing key customer segments continued. Our office co-location with the Precision Metalforming Association (PMA) continued to produce cost savings and joint activity opportunities. Our information exchange program with the Original Equipment Suppliers Association (OESA) continues as does the co-location of our Aerospace Division meetings with the Aerospace Locknut Manufacturers Association (ALMA) and our support provided to the Aerospace Industries Association (AIA). Our participation with the National Association of Manufacturers (NAM) has us cooperating on a variety of industry and government affairs initiatives. This expands the depth and breadth of our influence in Washington as does our work with The Laurin Baker Group. Within the fastener industry, our coordination with the NFDA, MWFA, Pac-West Distributors Association and the Fastener Industry Coalition (FIC) continued when common cause was identified, but we have and will retain our world recognized independent identity. We teamed up with Pac-West to develop Fastener Training Institute training programs in Cleveland, Detroit and Los Angeles. Educational involvement continued a key theme in 2012 as Division II continued to work with the State of California Community College system on

14

the Aerospace Fastener Manufacturing curriculum at El Camino College under the auspices of the California Center for Applied Competitive Technologies. For this program actual fastener manufacturing equipment has been installed and hands on training occurs. Many graduates are now working at IFI companies. In addition to our IFI/FTI workshops, we are also offering metallurgy and heat treating web-based seminars. These efforts are a step forward in IFI formalizing the fastener training aspects of our fastener industry mission and at the Board’s direction will be further enhanced in 2013.

15

MEMBERSHIP SERVICES

Trade associations exist to afford collective representation of an industry’s interests that individual companies cannot easily do sufficiently on their own. Their mission is to influence customers, governments and the public in the interests of the industry. Today trade associations are almost a necessity in a globally competitive business world, and almost all governments recognize them as institutions that advance the nation’s industries in ways no other organization could. Members, and non-members contemplating IFI membership, frequently ask can I afford to be a member of a trade association? Is the money I pay worth the investment? By joining this association will I gain opportunities and information to better run my business? What key issues is our industry facing that an association can deal with better than I can on my own? These are the key questions as to why companies join associations. IFI’s challenge remains to provide a value proposition in which the reward consistently exceeds the cost. This is particularly true when confronted with difficult times, customers who don’t want to understand the industry and its issues and government decisions that directly impact the association’s members. The association is the venue where ideas and information can be exchanged to the benefit of all. What, therefore, is it that IFI strives to provide its members?

1) Networking opportunities with peers and key suppliers to the industry is almost everyone’s first consideration.

2) A voice and source of advocacy for the industry which is recognized by the public, the industry’s customers, and the government.

3) A forum to collectively develop and share the cost of information gathering, training, carrying out industry specific technical and business oriented projects, and as a vehicle to coordinate projects of joint interest to the industry and with the key customers of and the suppliers to the industry.

4) A mechanism by which to represent the industry on technical and standards-based issues nationally and internationally in the interest of the member companies and their supply base.

5) The vehicle to coordinate with other associations in N. American manufacturing’s best interest.

These are the functions performed by the IFI’s Divisions, Committees, Working Groups and by the Staff of the Institute, under the supervision of the Board of Directors. For 2012, the scope of these activities is briefly summarized below. IFI provided qualified staff to attend industry and government meetings requiring more than 60 days of travel on behalf of Members. This shared representation is a saving as Members who do not all, therefore, have to attend these meetings themselves. This also allows for coordination amongst

16

and between the various bodies and activities rationalizing the decisions being reached by the industry. Over the course of the year IFI staff and/or designated Company members will attend multiple day meetings of the following:

• ASTM – F-16 • ASME – B-18 and B-1 • SAE – Fastener Committee and E-25 • International Standards Organization (ISO) – TC2 • Aerospace Industries Association working group and regular NASC meetings • The Aerospace Government/Industries Working Group (GIFWG) on fasteners • At the National Association of Manufacturers (NAM)

- International Economic Policy Committee and the Subcommittee on China - Coalition for a Sound Dollar - Coalition for the Future of Manufacturing - Associations Council - OSHA Policy Group - NLRB Working Group

• Selected consortium dealing with issues of importance to the industry • The Research Council on Bolted Joints • The Metalworking Industries Associations Executive Committee • The Automotive Industries Action Group (AIAG) – Packaging & Logistics and Quality Committees • The Metalworking Manufacturing Coalition • The Original Equipment Suppliers Association (OESA) meetings, workshops and seminars on the

automotive supply chain. The Institute thus provides the vehicle by which Member companies can coordinate and collaborate with other like-minded organizations on issues of concern. These relationships leverage the political reach of the Membership in government affairs and on issues of business concern. This spreads the cost of such activities over a broader base and makes accessible the best thinking of the combined groups without incurring the costs belonging to multiple organizations. Key groups the IFI regularly coordinates with include:

17

Fastener Organizations: Other Metalworking Organizations:

• European Industrial Fastener Institute (EIFI) • Precision Metalforming Association (PMA) – stamping & pressing

• Fastener Institute of Japan (FIJ) • Precision Machined Parts Association (PMPA) – screw machine

• Brazilian Fastener Institute (SINPA) • Spring Manufacturers Institute (SMI) – spring making

• Taiwan Industrial Fasteners Institute (TIFI) • Forging Industry Association (FIA) – forging

• Chinese Fastener Association • Tooling & Manufacturing Association (TMA) – tools & molds

• National Fastener Distributors Association (NFDA) • American Bearing Manufacturing Association (ABMA) – bearings

• Pac-West Distributors Association • American Gear Manufacturing Association (AGMA) – gears

• Midwest Fastener Distributors Association • American Iron & Steel Institute (AISI) – steel mills

• Other Distributor organizations • Metal Treating Institute (MTI) – heat treat, platings & coatings

• National Tooling & Manufacturing Association (NTMA) - CNC

• National Association of Manufacturers (NAM)

Other key Institute activities include developing and/or acquiring and disseminating industry information. These surveys and studies are also able to be done on a shared cost basis. Included are:

• IFI “Import/Export Report”

• Reports on the global raw materials markets

• Benchmarking Surveys

• Washington newsletters from a variety of Association sources (NAM, AIA, Credit-Suisse, etc.)

• Periodic e-mails, broadcast faxes and website updates on critical issues impacting the industry

• Regular economic updates Finally, at our Annual Spring, Fall, and periodic Divisional meetings, critical issues speakers and presentations were hosted on a shared cost basis. In 2012 these included:

• Clare Zempel’s Economic Forecasts

• Laurin and Jennifer Baker’s IFI Government Affairs Briefings

• Current Issues in Supplier Contracts by Automotive Supply Chain Attorney Dan Sharkey

• Metallurgical Implications of Heat Treat Strategy Changes by Salim Brahimi

• Winning Business Strategies in Tough Economic Times by Craig Fitzgerald of Plante Moran

18

• A First Hand Look at How Washington Works in a Crisis by Secretary Gordon England, twice Secretary Navy and Under Secretary of Defense & Homeland Security

• “Reshoring” by Harry Moser

• Auto OEM Cost Recovery Strategies by Kim Korth of IRN, Inc.

• Reports on Fastener Activities in Europe and Brazil by the Chairmen of their Fastener Associations

Developing common opportunities and dealing with common problems, along with networking, are what drives most memberships in most trade associations. Your participation in the IFI is always appreciated and gives you a voice in deciding what those issues will be and how they will be dealt with. Perhaps most important, it is an insurance policy providing you a seat at the table and your entrée to proactively help in shaping the future your business will exist in. ENGINEERING TECHNOLOGY ACTIVITIES IN 2012

IFI Technical Staff Roles:

The role of the technical staff of the IFI is to support the membership with technical assistance of all types including quality issue consultation, manufacturing consultation, application engineering assistance, and standards interpretations. Another highly valuable role of the technical staff is the participation in all standards groups creating mechanical fastener related standards to assure that unnecessarily arduous and impractical requirements are not introduced into newly created and/or revised existing standards. Additionally, the technical staff is involved in creating non-dues revenue programs and products. These include the creation of training programs, the teaching of same, and the creation of printed and web based technical resource materials. Fastener Standards Activities:

A huge part of the IFI technical activities involve the maintenance and creation of fastener related standards. The IFI technical staff participates in the American Society of Mechanical Engineers (ASME) B18 Fastener Committee, American Society of Testing and Materials (ASTM) F-16 Fastener Committee, SAE Fastener Committee, SAE Ship Systems Fastener Committee, International Standards Organization (ISO) TC2

19

Fastener Committee, Research Council for Steel Construction (RCSC), and the IFI Standards Working Groups. In addition to serving directly on these committees, the IFI staff also liaisons with other committees within each of those organizations on issues that in some way relate to fasteners. Some of these liaison activities during 2012 involved two trips to Europe to work with the ISO TC 44 Committee on Welding and Testing Procedures in which they are developing two standards specifically related to the testing of mechanical fasteners. This is important because these are non-fastener people creating standards for testing mechanical fasteners. The IFI staff is involved in these standards activities to protect the interests of North American fastener suppliers from having impractical requirements imposed on them in the future. Another such liaison activity is with the ASTM B 01 committee. They are the custodians of ASTM B633 which covers the electroplating of steel product. Many years ago this was the only electroplating standard available. In the 1990s the F-16 Fastener Committee created ASTM F1941 exclusively for the electroplating of threaded fasteners. In 2007, ASTM B633 was revised to require all products that were 1000 MPa (145,000 psi) to be baked after plating whereas ASTM F1941 does not require baking after electroplating until 1276 MPa (185,000 psi). Many users are still specifying ASTM B633 out of habit instead of specifying ASTM F1941 as they should. This results in tremendous unnecessary costs to the suppliers and end users because they must bake many lots of Grade 5 bolts and all Grade 8 bolts. The baking thresholds were set in ASTM F1941 after extensive research proving that baking below the 1276 MPa level is not needed. The IFI staff is working with the ASTM B 01 committee members to try to come to some revised language in B633 to direct fastener users to F1941. This work is carrying over into 2013. Keeping up with all of these activities requires participation in at least eleven multi-day meetings and dozens of web conferences each year. Standards Revisions Activities in 2012: The technical staff participated in the revision of the following fastener standards issued during 2012: ASME

ASME B18.2.6M-2012 Metric Fasteners for Use in Structural Applications ASME B18.7.1M-2007 (R2012) Metric General Purpose Semi-Tubular Rivets ASME B18.9-2012 Plow Bolts ASME B18.12-2012 Glossary of Terms for Mechanical Fasteners

20

ASTM ASTM A193/193M-2012a Standard Specification for Alloy-Steel and Stainless Steel Bolting for High Temperature or High Pressure Service and Other Special Purpose Applications ASTM A194/194M-2012a Standard Specification for Carbon and Alloy Steel Nuts for Bolts for High Pressure or High Temperature Service, or Both ASTM A307-12 Standard Specification for Carbon Steel Bolts, Studs, and Threaded Rod 60???000 PSI Tensile Strength ASTM A489-12 Standard Specification for Carbon Steel Lifting Eyes ASTM A490-2012 Standard Specification for Structural Bolts, Alloy Steel, Heat Treated, 150 ksi Minimum Tensile Strength ASTM A490M-12 Standard Specification for High-Strength Steel Bolts, Classes 10.9 and 10.9.3, for Structural Steel Joints (Metric) ASTM A574-2012 Standard Specification for Alloy Steel Socket-Head Cap Screws ASTM A574M-12 Standard Specification for Alloy Steel Socket-Head Cap Screws (Metric) ASTM F467M-06a(2012) Standard Specification for Nonferrous Nuts for General Use (Metric) ASTM F468M-06(2012) Standard Specification for Nonferrous Bolts, Hex Cap Screws, and Studs for General Use (Metric) ASTM F468-12 Standard Specification for Nonferrous Bolts, Hex Cap Screws, Socket Head Cap Screws, and Studs for General Use ASTM F541-12 Standard Specification for Alloy Steel Eyebolts ASTM F547-06(2012) Standard Terminology of Nails for Use with Wood and Wood-Base Materials ASTM F592-84(2012) Standard Terminology of Collated and Cohered Fasteners and Their Application Tools ASTM F606M-12 Standard Test Methods for Determining the Mechanical Properties of Externally and Internally Threaded Fasteners, Washers, and Rivets (Metric) ASTM F680-80(2012) Standard Test Methods for Nails ASTM F788-12 Standard Specification for Surface Discontinuities of Bolts, Screws, and Studs, Inch and Metric Series ASTM F812-12 Standard Specification for Surface Discontinuities of Nuts, Inch and Metric Series ASTM F835-2012 Standard Specification for Alloy Steel Socket Button and Flat Countersunk Head Cap Screws

21

ASTM F879-12 Standard Specification for Stainless Steel Socket Button and Flat Countersunk Head Cap Screws ASTM F880-12 Standard Specification for Stainless Steel Socket, Square Head, and Slotted Headless-Set Screws ASTM F901-2012 Standard Specification for Aluminum Transmission Tower Bolts and Nuts ASTM F1470-12 Standard Practice for Fastener Sampling for Specified Mechanical Properties and Performance Inspection ASTM F1503-02(2012) Standard Practice for Machine/Process Capability Study Procedure ASTM F1789-12 Standard Terminology for F-16 Mechanical Fasteners ASTM F2280-12 Standard Specification for “Twist Off” Type Tension Control Structural Bolt/Nut/Washer Assemblies, Steel, Heat Treated, 150 ksi Minimum Tensile Strength ASTM F2882-12 Standard Specification for Screws, Alloy Steel, Heat Treated, 170 ksi Minimum Tensile Strength ASTM F2882M-12 Standard Specification for Screws, Alloy Steel, Heat Treated, 1170 MPa Minimum Tensile Strength [Metric] ASTM F2281-04(2012) Standard Specification for Stainless Steel and Nickel Alloy Bolts, Hex Cap Screws, and Studs, for Heat Resistance and High Temperature Applications ASTM F2660-12 Standard Test Method for Qualifying Coatings for Use on A490 Structural Bolts Relative to Hydrogen Embrittlement

SAE SAE J995-2012 Mechanical and Material Requirements for Steel Nuts

ISO ISO 888-2012 Fasteners — Bolts, screws and studs—Nominal lengths and thread lengths ISO 898-2-2012 Mechanical properties of fasteners made of carbon steel and alloy steel— Part 2: Nuts with specified property classes — Coarse thread and fine pitch thread ISO 898-5-2012 Mechanical properties of fasteners made of carbon steel and alloy steel — Part 5: Set screws and similar threaded fasteners with specified hardness classes — Coarse thread and fine pitch thread ISO 4032-2012 Hexagon regular nuts (style 1) — Product grades A and B ISO 4033-2012 Hexagon high nuts (style 2) — Product grades A and B ISO 4034-2012 Hexagon regular nuts (style 1) — Product grade C

22

ISO 4035-2012 Hexagon thin nuts chamfered (style 0) — Product grades A and B ISO 4036-2012 Hexagon thin nuts unchamfered (style 0) — Product grade B ISO 4161-2012 Hexagon nuts with flange, style 2 — Coarse thread ISO 4162-2012 Hexagon bolts with flange — Small series — Product grade A with driving feature of product grade B ISO 7040-2012 Prevailing torque type hexagon regular nuts (with non-metallic insert) — Property classes 5, 8 and 10 ISO 7041-2012 Prevailing torque type hexagon nuts (with non-metallic insert), style 2 — Property classes 9 and 12 ISO 7042-2012 Prevailing torque type all-metal hexagon high nuts — Property classes 5, 8, 10 and 12 ISO 7043-2012 Prevailing torque type hexagon nuts with flange (with non-metallic insert), style 2 — Product grades A and B ISO 7044-2012 Prevailing torque type all-metal hexagon nuts with flange, style 2 — Product grades A and B ISO 7719-2012 Prevailing torque type all-metal hexagon regular nuts — Property classes 5, 8 and 10 ISO 7720-2012 Prevailing torque type all-metal hexagon nuts, style 2 — Property class 9 ISO 8673-2012 Hexagon regular nuts (style 1) with metric fine pitch thread — Product grades A and B ISO 8674-2012 Hexagon high nuts (style 2) with metric fine pitch thread — Product grades A and B ISO 8675-2012 Hexagon thin nuts chamfered (style 0) with metric fine pitch thread — Product grades A and B ISO 10509-2012 Hexagon flange head tapping screws ISO 10511-2012 Prevailing torque type hexagon thin nuts (with non-metallic insert) ISO 10512-2012 Prevailing torque type hexagon regular nuts (with non-metallic insert) with metric fine pitch thread — Property classes 6, 8 and 10 ISO 10513-2012 Prevailing torque type all-metal hexagon high nuts with metric fine pitch thread — Property classes 8, 10 and 12 ISO 10642-2004 Amd1-2012 Hexagon socket countersunk head screws AMENDMENT 1

23

ISO 10663-2012 Hexagon nuts with flange, style 2 — Fine pitch thread ISO 12125-2012 Prevailing torque type hexagon nuts with flange (with non-metallic insert) with metric fine pitch thread, style 2 — Product grades A and B ISO 12126-2012 Prevailing torque type all-metal hexagon nuts with flange with metric fine pitch thread, style 2 — Product grades A and B ISO 15072-2012 Hexagon bolts with flange with metric fine pitch thread — Small series — Product grade A ISO 16047-2005 Amd1-2012 Fasteners — Torque/clamp force testing AMENDMENT 1

IFI IFI-134-2012 Structural Positive Locking, Self-Plugging Blind Rivets Educational Programs: Fastener Training Institute: An important role of the technical staff of the IFI is to participate in the development and presentation of fastener related technical training. Several years ago the IFI entered into a collaboration agreement with the Fastener Training Institute (www.fastenertraininginstitute.com) for the development and presentation of various technical training courses related to mechanical fasteners. The IFI staff participated in presenting the following classes in 2012:

• Fastener Training Week – January in Los Angeles, California and July in Independence, Ohio • Automotive Fastener Training – April in Dearborn, Michigan

A new course is under development specifically targeting Division II members entitled Aerospace Fastener Training. The first class is planned for the second half of 2013. At the end of each day and at the end of each course participants have been asked to fill out feedback surveys. So far, 100% of all participants have indicated they are going to recommend that their associates attend these classes in the future. Because of this strong, positive feedback, the Fastener Week Training is being expanded from two to three programs and the Automotive Training Program is being increased from one to two programs during 2013. Online Training and Webinar Programs: The IFI has been working in conjunction with Dr. Michael Pfeifer on the creation of online courses and webinars related to the metallurgical aspects of fastener technology. The IFI now offers two online training courses and is developing a series of webinars.

24

Online courses: • The Principles of Metallurgy • The Principles of the Heat Treating of Steel Fasteners • The Corrosion of Metals

Webinars:

The first webinar was offered in December of 2012. There were 26 participants. The feedback was very favorable. Below is a list of the webinars under development. The first was presented in 2012 and the others are planned for 2013.

• The Principles of Quench and Temper • The Corrosion of Metals • Failure Modes of Fasteners and How to Recognize Them • Failure Analysis of Fastener Failures

IFI Products and Publications:

• IFI Technology Connection: The IFI Technology Connection continues to grow slowly. Most new subscribers are opting for the subscription that allows all of their employees and customers to access the Connection through the secure area of their website. During 2012 a new module entitled Fastener Finishes was added. This is a great advancement for solving corrosion issues for end users. By using this module users can define their application requirements including whether or not the finish must be RoHS/REACH compliant, the required color, and the required number of salt spray resistance hours the fasteners must meet. Once the user has selected these, a list of all of the fastener finishes that meet those requirements is output. By clicking on the finish name the user can get additional information about the finish and a website for finding sources for the finishes.

• Digital Standards Books for Multiple Users:

During 2012 the IFI KEY™ version of fastener standards was introduced. Both the IFI 8th Edition Inch Fastener Standards Book and the ISO Fastener and Screw Thread Handbook are now available in the IFIKEY™ format. This new version of digital standards book allows a purchaser to load the book on as many personal computers as they want within a department or company, but they can only open the book when the IFI KEY is plugged into the USB port of a computer. This is a digital version of a

25

hard cover book that can be passed from desk to desk, but only one person at a time can use the book. One big advantage of the IFI KEY version over a hard cover book is that the user can use the screen shot tool on their computer to capture data to share with others. The IFI KEY is very secure and cannot be duplicated.

• Technical Book Publishing:

During 2012 the IFI technical staff compiled a series of published articles authored by Bengt Blendulf, a long time teacher of fastener technology in the fastener industry, into a hard cover book. The book is entitled, Mechanical Fastening and Joining. Distribution will begin in January or February of 2013. This is a very comprehensive book on mechanical joint technology that will be a tremendous tool for the suppliers and end users of mechanical fasteners. Other fastener technology books on subjects such as fastener tightening, thread understanding, and failure analysis are planned for the future.

OUR DIVISIONS

DIVISION I: INDUSTRIAL PRODUCTS

Division I is those manufacturers who supply fasteners and formed parts to the makers of industrial products, the construction industry and to distribution. Most of our fastener standards are developed for this segment of the industry. The Division meets twice yearly and often hosts speakers on topics of timely interest to the whole membership. Many of our technical special projects are triggered by the needs of this segment. This Division provides support to our technical engineering activities, to the Research Council on Structural Connections and to the Bolting Technology Council. Our activities with ASTM, ASME and ISO are largely driven by Division I. The Division was very ably chaired by Brad Tinney, BIRMINGHAM FASTENER, INC. The Division joined the Aerospace and Automotive Divisions with the addition of Bob Hill as Division Manager. Bob is focused on membership development and membership retention in equal parts. DIVISION II: AEROSPACE PRODUCTS

Division II manufacturers supply very specialized products to the aerospace industry and the Department of Defense. Their products are frequently made from the more exotic materials and often have complex geometry in their design. Their supply to the government means they must comply with defense procurement agency constraints. This Division has an Affiliate Member category which are those key

26

distributors in the supply chain providing product to the major aerospace airframe, engine and flight component OEMs. The Division tends to be quite active in government affairs due to the many regulations governing the sale and use of the products their fasteners go into. This Division has been the fastest growing in the IFI, has an extremely capable Division Manager in Pat Meade. The Division successfully participated in the start up of a community college program to train machinery operators for the industry and graduates are being hired into industry. The Division was very ably chaired by Donnie Autry, MACLEAN-ESNA. The Technical Chairman was Owe Carlsson, ALCOA FASTENING SYSTEMS and that position is now held by Mike Lawler, PENNENGINEERING. DIVISION III: AUTOMOTIVE INDUSTRY FASTENER GROUP (AIFG)

Division III represents those manufacturers supplying product to the automotive OEMs and the Tiers that supply the OEMs. It meets bimonthly, frequently in the Detroit area to facilitate participation. Because of the nature of the automotive industry – frequently confrontational and always price and volume driven – the Division never lacks for projects to undertake, new business and legal issues to learn and best practices lessons from which all can benefit. The Division coordinates activities with USCAR, AIAG and OESA. This Division also has a very experienced Division Manager in John O’Brien. The Division hosts the annual “John D. Fischer” Memorial Golf Tournament in which Division members, the Institute’s current and past officers and Associate Division members participate. The 2012 winning team for the golf tournament was Steve Paddock, Porter McLean, Alan Hariton and Bill Drypen. The group was ably chaired by David Hebert, SFS INTECH, INC. and Jason Surber, ATF, INC. ASSOCIATE SUPPLIERS’ DIVISION

The Associate Division members are the key suppliers of the raw material, machinery, equipment and services used in the production of fasteners/formed parts. They provide the Institute expertise in their particular area and brief Members on new technology, operational practices, business developments and trade issues impacting their ability to supply the fastener manufacturing market. Without the associate suppliers, there would be no industry. Twice a year they provide very focused briefings on one of their particular areas of expertise, a unique value to the Members. This group was chaired by Alan Hariton, HARITON MACHINERY COMPANY, INC.

27

Industrial Fasteners Institute

2010 - 2015 Strategic Plan

Approved: 12/7/09 / 9/18/11 Review

And 4th Quarter 2012 Update Vision: To be the globally recognized, North American focused, leading association representing the interests of the manufacturers of mechanical fasteners and formed parts, and the key suppliers to the industry, fostering their working together to shape the future of the industry. Mission: To represent the industry to its suppliers, customers, the government, and the public at large to advance the competitiveness, products, and innovative technology of the Member Companies in a global marketplace. Operational Values: To be Member driven, Board led, focused on continuous improvement in the process of serving our members in their voluntary participation in the development of business, technical and government affairs programs, and issues important to the industry’s success. Original Strategic Plan Committee Members: Ed Plomer – Illinois Tool Works, Larry Valeriano – California Screw Products Corporation, Karl Hutter – Click Bond, Inc., John Grabner – Cardinal Fastener & Specialty Co., Inc., Herman van Maaran – Kamax L.P., Don George – ND Industries, Inc., Rob Harris – IFI Update Committee: Dave Monti, Chairman; Ed Plomer; Larry Valeriano; Mark Quebbeman; Dave Lomasney;

Rob Harris; Joe Greenslade

28

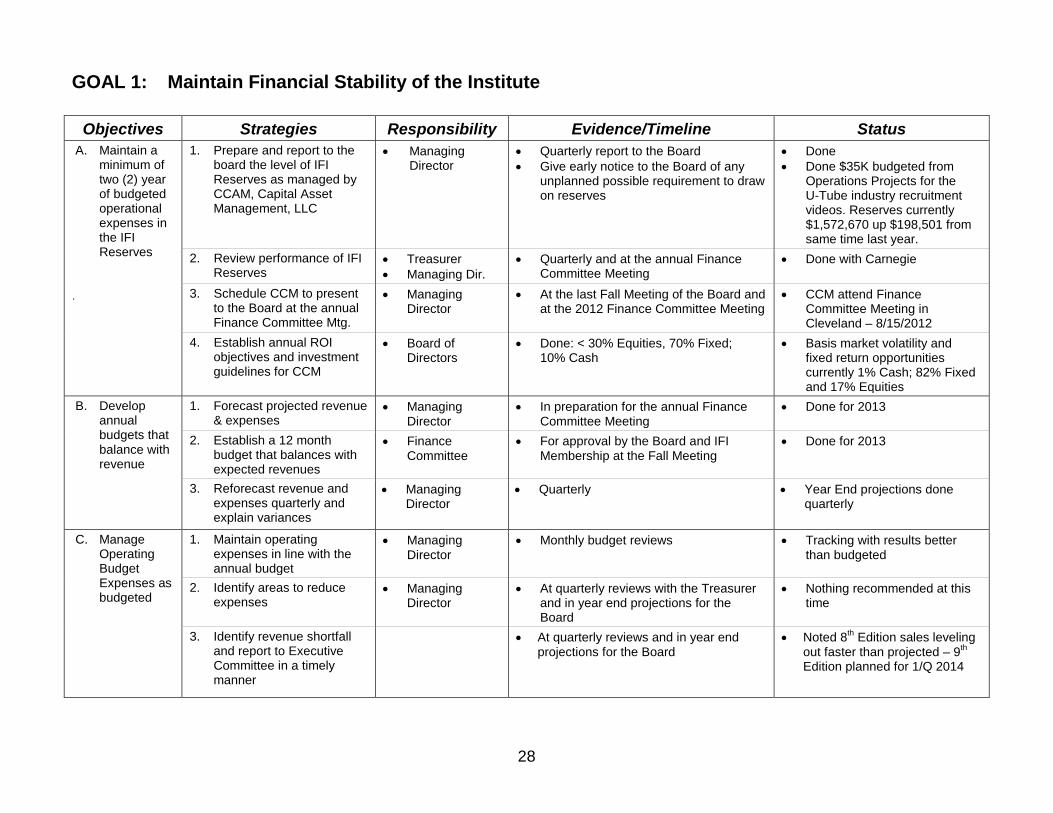

GOAL 1: Maintain Financial Stability of the Institute

Objectives Strategies Responsibility Evidence/Timeline Status A. Maintain a

minimum of two (2) year of budgeted operational expenses in the IFI Reserves

.

1. Prepare and report to the board the level of IFI Reserves as managed by CCAM, Capital Asset Management, LLC

• Managing Director

• Quarterly report to the Board • Give early notice to the Board of any

unplanned possible requirement to draw on reserves

• Done • Done $35K budgeted from

Operations Projects for the U-Tube industry recruitment videos. Reserves currently $1,572,670 up $198,501 from same time last year.

2. Review performance of IFI Reserves

• Treasurer • Managing Dir.

• Quarterly and at the annual Finance Committee Meeting

• Done with Carnegie

3. Schedule CCM to present to the Board at the annual Finance Committee Mtg.

• Managing Director

• At the last Fall Meeting of the Board and at the 2012 Finance Committee Meeting

• CCM attend Finance Committee Meeting in Cleveland – 8/15/2012

4. Establish annual ROI objectives and investment guidelines for CCM

• Board of Directors

• Done: < 30% Equities, 70% Fixed; 10% Cash

• Basis market volatility and fixed return opportunities currently 1% Cash; 82% Fixed and 17% Equities

B. Develop annual budgets that balance with revenue

1. Forecast projected revenue & expenses

• Managing Director

• In preparation for the annual Finance Committee Meeting

• Done for 2013

2. Establish a 12 month budget that balances with expected revenues

• Finance Committee

• For approval by the Board and IFI Membership at the Fall Meeting

• Done for 2013

3. Reforecast revenue and expenses quarterly and explain variances

• Managing Director

• Quarterly • Year End projections done quarterly

C. Manage Operating Budget Expenses as budgeted

1. Maintain operating expenses in line with the annual budget

• Managing Director

• Monthly budget reviews

• Tracking with results better than budgeted

2. Identify areas to reduce expenses

• Managing Director

• At quarterly reviews with the Treasurer and in year end projections for the Board

• Nothing recommended at this time

3. Identify revenue shortfall and report to Executive Committee in a timely manner

• At quarterly reviews and in year end projections for the Board

• Noted 8th Edition sales leveling out faster than projected – 9th Edition planned for 1/Q 2014

29

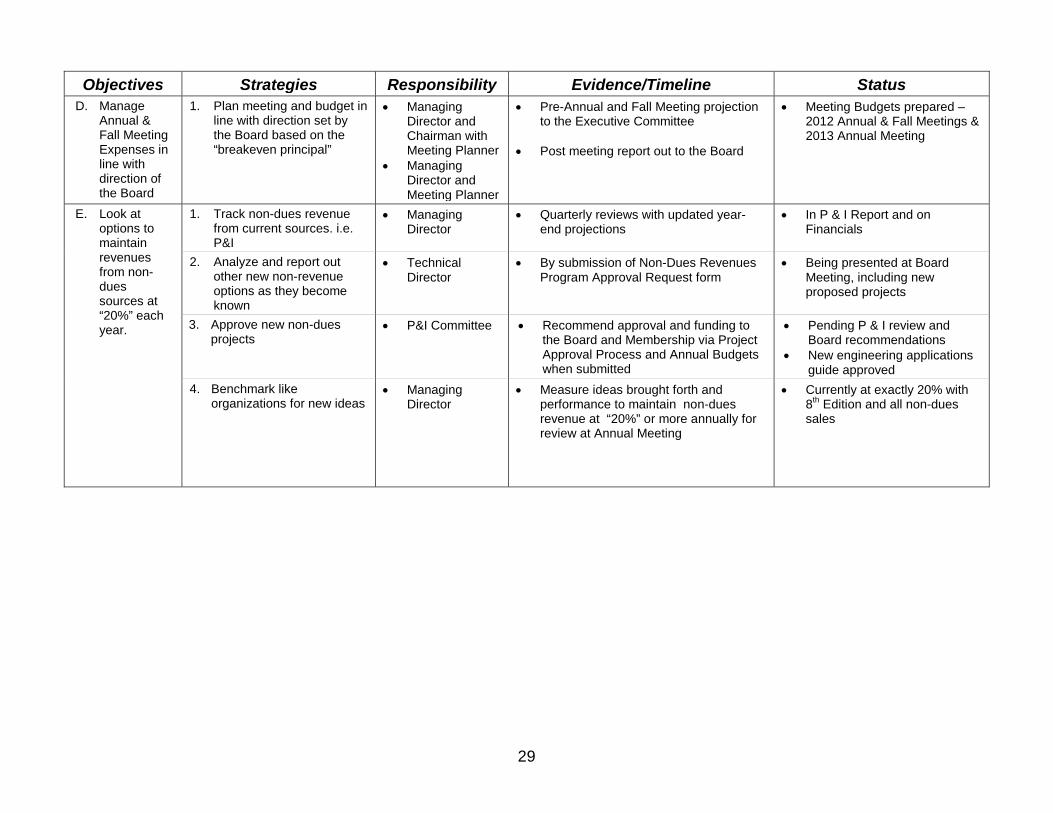

Objectives Strategies Responsibility Evidence/Timeline Status D. Manage

Annual & Fall Meeting Expenses in line with direction of the Board

1. Plan meeting and budget in line with direction set by the Board based on the “breakeven principal”

• Managing Director and Chairman with Meeting Planner

• Managing Director and Meeting Planner

• Pre-Annual and Fall Meeting projection to the Executive Committee

• Post meeting report out to the Board

• Meeting Budgets prepared – 2012 Annual & Fall Meetings & 2013 Annual Meeting

E. Look at options to maintain revenues from non-dues sources at “20%” each year.

1. Track non-dues revenue from current sources. i.e. P&I

• Managing Director

• Quarterly reviews with updated year-end projections

• In P & I Report and on Financials

2. Analyze and report out other new non-revenue options as they become known

• Technical Director

• By submission of Non-Dues Revenues Program Approval Request form

• Being presented at Board Meeting, including new proposed projects

3. Approve new non-dues projects

• P&I Committee • Recommend approval and funding to the Board and Membership via Project Approval Process and Annual Budgets when submitted

• Pending P & I review and Board recommendations

• New engineering applications guide approved

4. Benchmark like organizations for new ideas

• Managing Director

• Measure ideas brought forth and performance to maintain non-dues revenue at “20%” or more annually for review at Annual Meeting

• Currently at exactly 20% with 8th Edition and all non-dues sales

30

GOAL 2: Have a Clear Value Proposition and Communicate Effectively

Objectives Strategies Responsibility Evidence/Timeline Status A. Develop and

implement communication tools to inform the members and the industry on relevant matters

1. Identify methods to communicate effectively with all members

• Managing Director

• Technical Director • P&I Committee

Establish a process to start with an agenda item at the Annual Mtg.

• Define initial deliverables to accomplish objective

- IFI Annual Report and a summary abstract

- Other (to be defined) – “State of the Industry” periodically, quarterly? Semi-annual?

• Define schedules for other deliverables • Nuts and Bolts Quarterly news release • Monthly Technical Update along with Hit

List update

• Done • New projects defined & 4

editions delivered • Done Monthly

B. Provide annual reviews and bi-annual updates of the Strategic Plan

1. Review Plan for accuracy and alignment with goals

2. Make adjustments when necessary

• Strategic Plan Committee

• Acceptance of proposed changes at the Annual Meeting by the Board

• Provided for review with these comments

C. Review the value proposition to be clear to all current and prospective members

1. Provide a one-page summary of what the IFI is, does, and stands for, for current and prospective members (see Goal 2A)

• Managing Director

• For approval by the Board at the 2010 Annual Meeting and delivered to the Membership and prospective new members thereafter

• Completed by Jennifer Johns Friel and John O’Brien

31

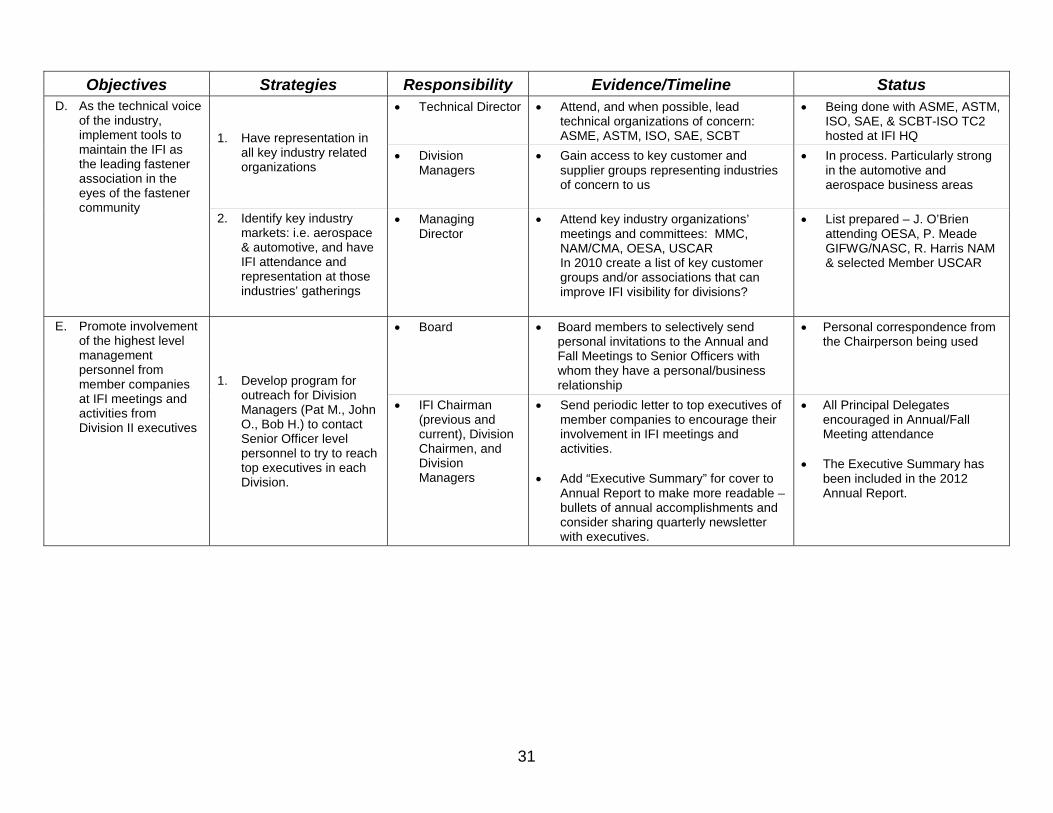

Objectives Strategies Responsibility Evidence/Timeline Status D. As the technical voice

of the industry, implement tools to maintain the IFI as the leading fastener association in the eyes of the fastener community

1. Have representation in all key industry related organizations

• Technical Director • Attend, and when possible, lead technical organizations of concern: ASME, ASTM, ISO, SAE, SCBT

• Being done with ASME, ASTM, ISO, SAE, & SCBT-ISO TC2 hosted at IFI HQ

• Division Managers

• Gain access to key customer and supplier groups representing industries of concern to us

• In process. Particularly strong in the automotive and aerospace business areas

2. Identify key industry markets: i.e. aerospace & automotive, and have IFI attendance and representation at those industries’ gatherings

• Managing Director

• Attend key industry organizations’ meetings and committees: MMC, NAM/CMA, OESA, USCAR In 2010 create a list of key customer groups and/or associations that can improve IFI visibility for divisions?

• List prepared – J. O’Brien attending OESA, P. Meade GIFWG/NASC, R. Harris NAM & selected Member USCAR

E. Promote involvement of the highest level management personnel from member companies at IFI meetings and activities from Division II executives

1. Develop program for outreach for Division Managers (Pat M., John O., Bob H.) to contact Senior Officer level personnel to try to reach top executives in each Division.

• Board

• Board members to selectively send personal invitations to the Annual and Fall Meetings to Senior Officers with whom they have a personal/business relationship

• Personal correspondence from the Chairperson being used

• IFI Chairman (previous and current), Division Chairmen, and Division Managers

• Send periodic letter to top executives of member companies to encourage their involvement in IFI meetings and activities.

• Add “Executive Summary” for cover to Annual Report to make more readable – bullets of annual accomplishments and consider sharing quarterly newsletter with executives.

• All Principal Delegates encouraged in Annual/Fall Meeting attendance

• The Executive Summary has

been included in the 2012 Annual Report.

32

GOAL 3: Maintain Position as the Industry’s Top Technical Resource and Facilitator

Objectives Strategies Responsibility Evidence/Timeline Status A. Staff IFI

appropriately to support a strong technical presence

1. Maintain a Technical Director as a key employee of the Institute

2. Review job description to maintain role in line with the IFI mission

• Managing Director

• Technical Director on staff at all times and jointly ID potential protégés

• Written job description review annually • J. Greenslade protégé for succession

planning

• Done • Distributed & reviewed • Laurence Claus contracted

with for 2013 on a project basis for Technical Director evaluation

3. Promote a web-based technical database (ITC)

• Technical Director

• IFI Technology Connection • Completed and earning revenue - $62,380 profit in 2012

B. Maintain participation in key industry standards and technical committees

1. Identify and participate in national and international committees and organizations that promote fastener standards, manufacturing, and technology

• Technical Director

• Annual report of committees’ work to the Board at the Annual and Fall Meetings

• List of IFI staff and company participants on various standards organizations. (web site, annual report, membership directory?)

• In Board Notebooks and IFI Annual Report

• Provided

C. Expand training options for fastening, fastener manufacturing, and other processes associated with same, i.e., heat treat, plating & coating, etc.

1. Recognizing the need to promote fastener manufacturing excellence, methods, new developments, and applications, create training resources through alignment with relevant organizations to advance such education such as the Fastener Training Institute and El Camino College

• Technical Director and Division Managers

• Report to Board at Annual and Fall Meetings IFI’s participation in educational groups of interest—target would be one group per Division over the five-year period

• IFI/FTI three week fastener training classes in 2013

• IFI/FTI auto fastener training in Detroit & Cleveland in 2013

• Training classes netted IFI $18,564 in 2012

• Technical Director

• To solicit interest in IFI as a participant in the educational arena, submit not less than three articles for publication in technical magazines annually

• Completed in 2011 by Joe Greenslade & Pat Meade and in process for 2012

2. Evaluate developing an annual IFI Scholarship program with a key educational institution or organization

• Managing Director and Technical Director

• Introduce concept for discussion at the 2010 Annual Meeting

• Discussed at 2012 spring Board meeting & decision to delay action

33

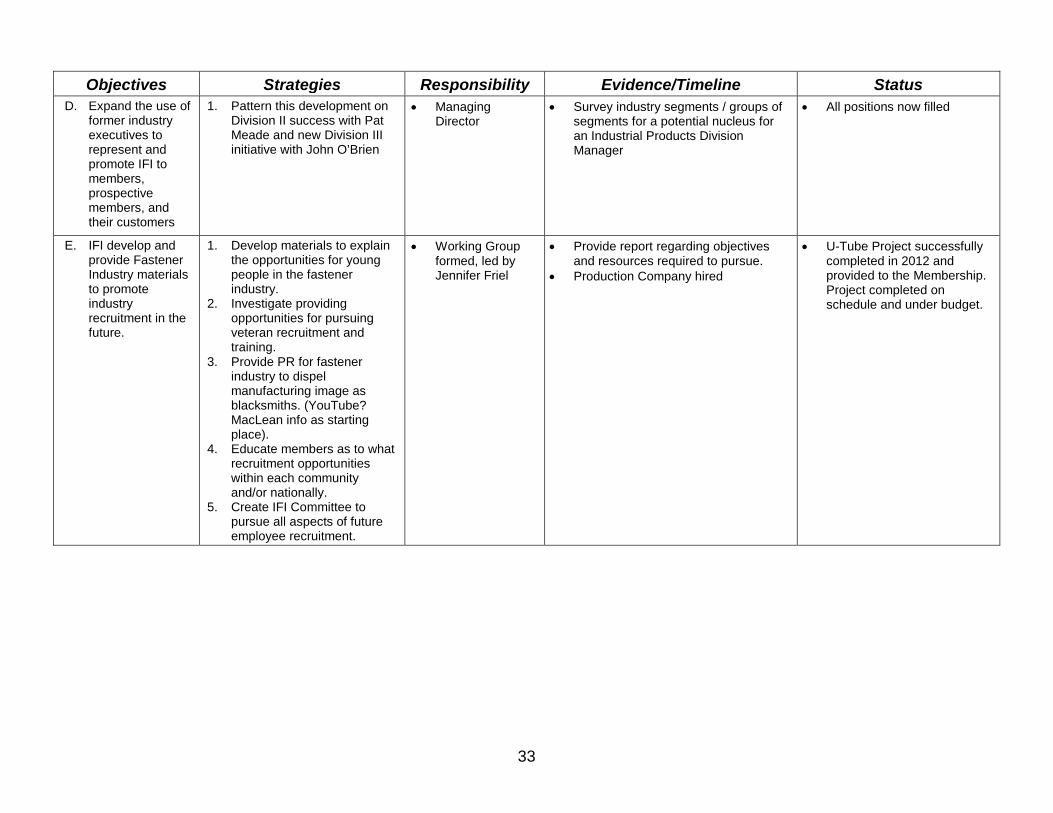

Objectives Strategies Responsibility Evidence/Timeline Status D. Expand the use of

former industry executives to represent and promote IFI to members, prospective members, and their customers

1. Pattern this development on Division II success with Pat Meade and new Division III initiative with John O’Brien

• Managing Director

• Survey industry segments / groups of segments for a potential nucleus for an Industrial Products Division Manager

• All positions now filled

E. IFI develop and provide Fastener Industry materials to promote industry recruitment in the future.

1. Develop materials to explain the opportunities for young people in the fastener industry.

2. Investigate providing opportunities for pursuing veteran recruitment and training.

3. Provide PR for fastener industry to dispel manufacturing image as blacksmiths. (YouTube? MacLean info as starting place).