industry outlook 2016 - listed companyptt.listedcompany.com/...industry-outlook-am3q2015.pdf ·...

TRANSCRIPT

PTT Auditorium17 November 2015

Industry Outlook 2016

Speakers

2

Economics

Oil & Refining

LNG & Gas

Petrochemical

Contents

Economics Oil & Refining LNG & Gas Petrochemical

3

Economics

Presented By:

Jittinan AukayanagulAnalyst

Economics and Industry Research Department

Economics Oil & Refining LNG & Gas Petrochemical

5

US Economy: inventories and a strong dollar dragging down growth

Economics Oil & Refining LNG & Gas Petrochemical

6

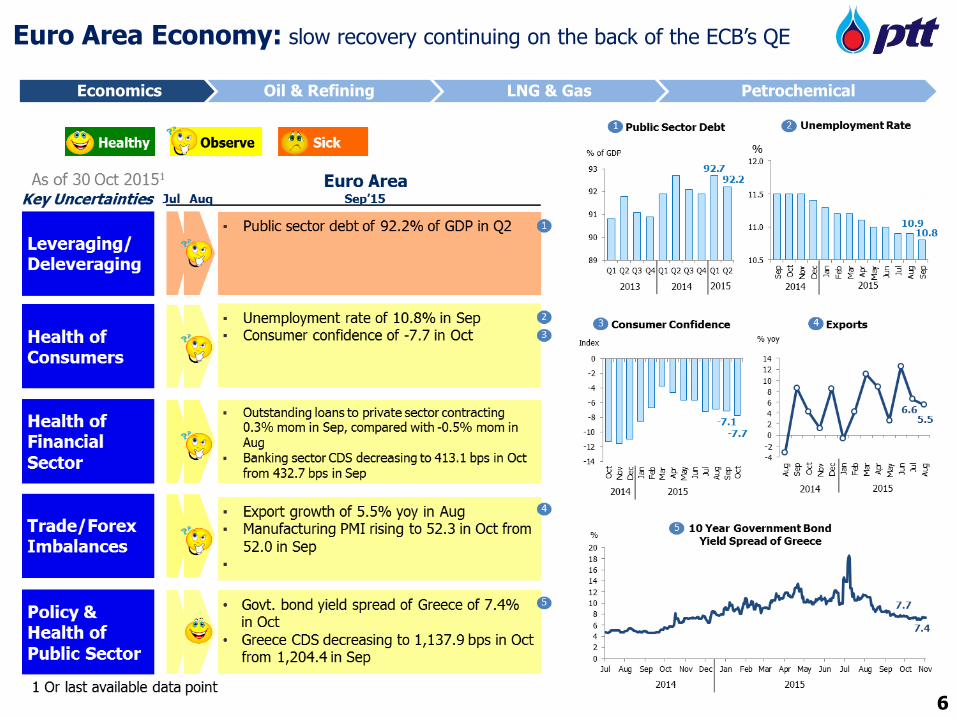

Euro Area Economy: slow recovery continuing on the back of the ECB’s QE

Economics Oil & Refining LNG & Gas Petrochemical

7

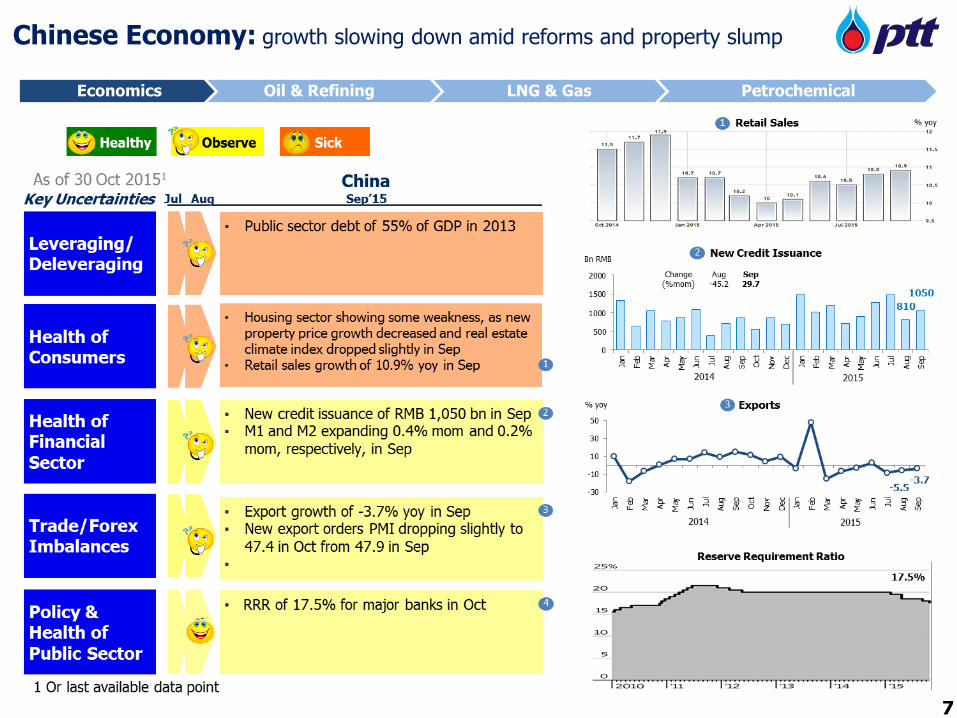

Chinese Economy: growth slowing down amid reforms and property slump

Economics Oil & Refining LNG & Gas Petrochemical

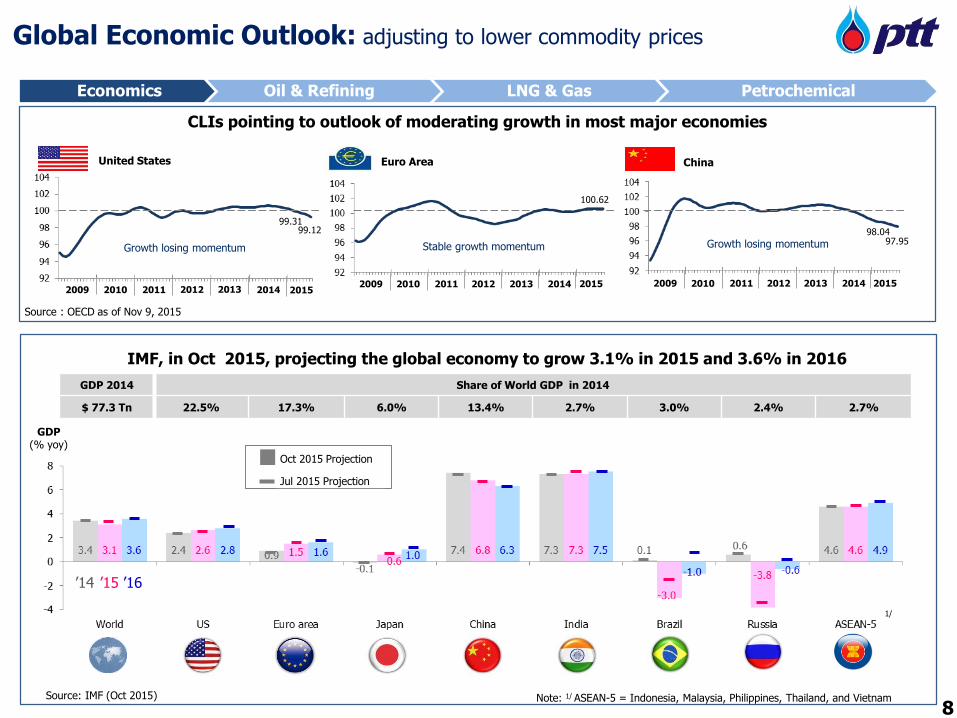

Global Economic Outlook: adjusting to lower commodity prices

GDP 2014 Share of World GDP in 2014

$ 77.3 Tn 22.5% 17.3% 6.0% 13.4% 2.7% 3.0% 2.4% 2.7%

China

2012201120102009 20132012201120102009 2013

Growth losing momentum98.04

United States Euro Area

Stable growth momentum

2012201120102009 2013

100.62

20142014 2014

99.1297.95

20152015 2015

99.31

CLIs pointing to outlook of moderating growth in most major economies

Source : OECD as of Nov 9, 2015

GDP(% yoy)

IMF, in Oct 2015, projecting the global economy to grow 3.1% in 2015 and 3.6% in 2016

1/

Source: IMF (Oct 2015) Note: 1/ ASEAN-5 = Indonesia, Malaysia, Philippines, Thailand, and Vietnam

’14 ’15 ’16

Apr 2015 Projection

Jul 2015 Projection Oct 2015 Projection

Jul 2015 Projection

Growth losing momentum

8

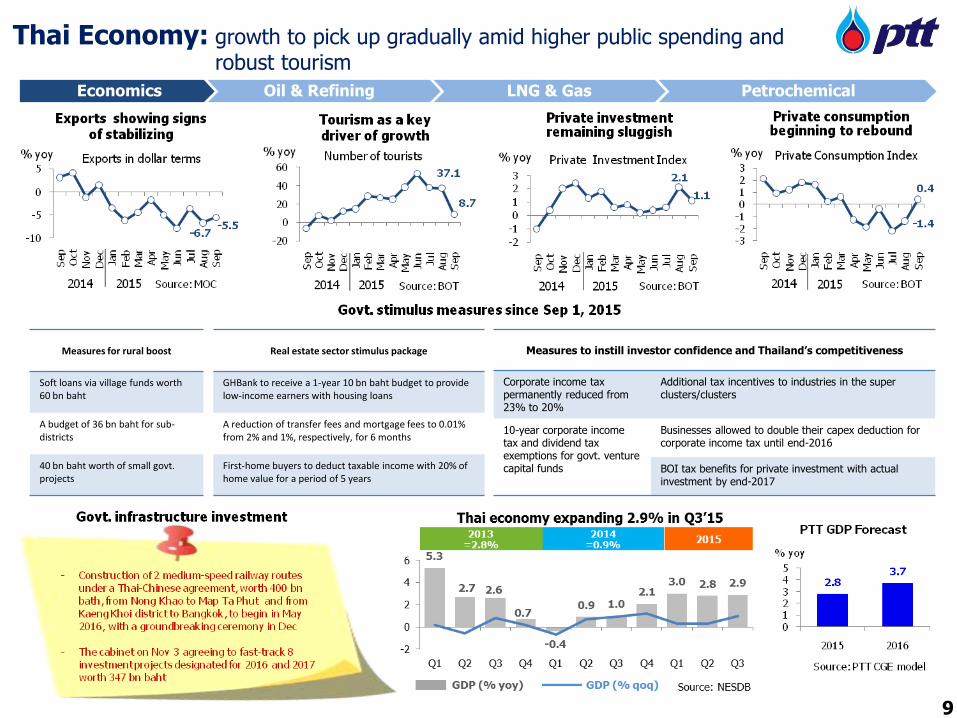

Thai Economy: growth to pick up gradually amid higher public spending and robust tourism

Economics Oil & Refining LNG & Gas Petrochemical

Measures for rural boost

Soft loans via village funds worth 60 bn baht

A budget of 36 bn baht for sub-districts

40 bn baht worth of small govt.projects

Real estate sector stimulus package

GHBank to receive a 1-year 10 bn baht budget to provide low-income earners with housing loans

A reduction of transfer fees and mortgage fees to 0.01% from 2% and 1%, respectively, for 6 months

First-home buyers to deduct taxable income with 20% of home value for a period of 5 years

Measures to instill investor confidence and Thailand’s competitiveness

Corporate income tax permanently reduced from 23% to 20%

Additional tax incentives to industries in the super clusters/clusters

10-year corporate income tax and dividend tax exemptions for govt. venture capital funds

Businesses allowed to double their capex deduction for corporate income tax until end-2016

BOI tax benefits for private investment with actual investment by end-2017

9

Economics

Oil & Refining

LNG & Gas

Petrochemical

Economics Oil & Refining LNG & Gas Petrochemical

Contents

10

Oil & Refining

Presented By:

Anintita PraokaewTeam Leader

Business Planning and Subsidiary Management Department

Economics Oil & Refining LNG & Gas Petrochemical

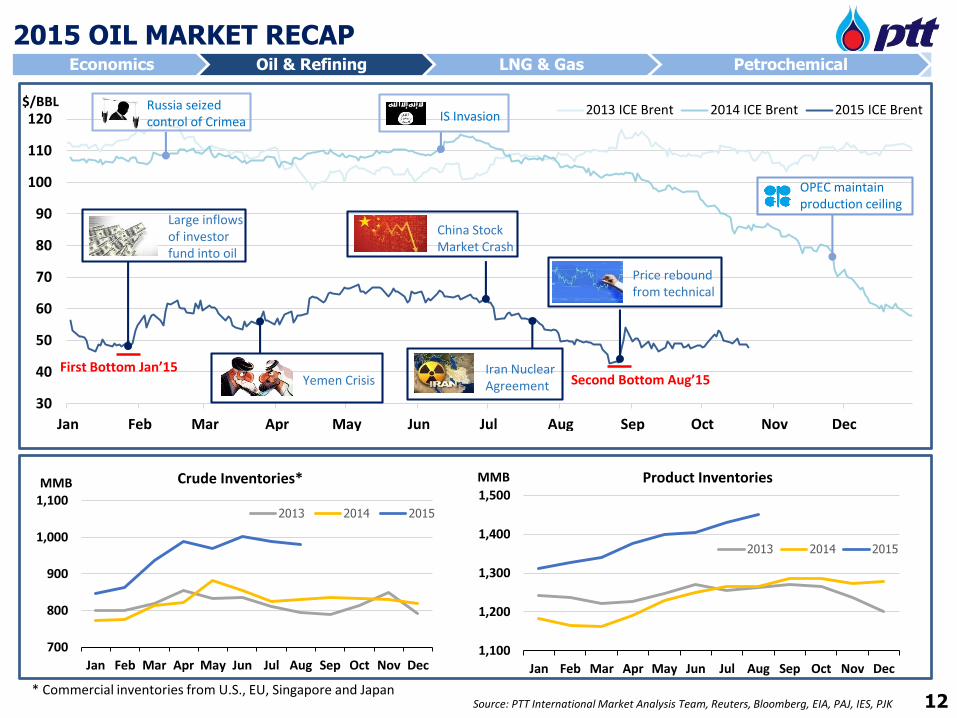

2015 OIL MARKET RECAP

30

40

50

60

70

80

90

100

110

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 ICE Brent 2014 ICE Brent 2015 ICE BrentIS InvasionRussia seized control of Crimea

OPEC maintain production ceiling

First Bottom Jan’15

Large inflows of investor fund into oil

Yemen Crisis

China Stock Market Crash

Iran Nuclear Agreement Second Bottom Aug’15

Price rebound from technical

$/BBL

Source: PTT International Market Analysis Team, Reuters, Bloomberg, EIA, PAJ, IES, PJK

700

800

900

1,000

1,100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MMB Crude Inventories*

2013 2014 2015

1,100

1,200

1,300

1,400

1,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MMB Product Inventories

2013 2014 2015

* Commercial inventories from U.S., EU, Singapore and Japan12

Economics Oil & Refining LNG & Gas Petrochemical

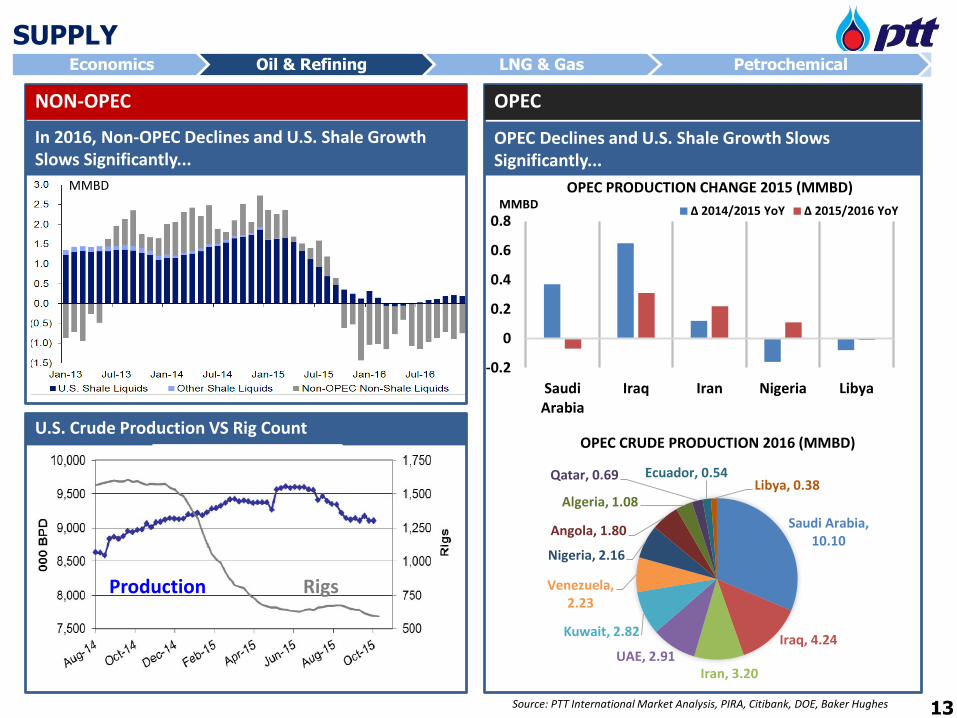

SUPPLY

Source: PTT International Market Analysis, PIRA, Citibank, DOE, Baker Hughes

-0.2

0

0.2

0.4

0.6

0.8

SaudiArabia

Iraq Iran Nigeria Libya

MMBDOPEC PRODUCTION CHANGE 2015 (MMBD)

∆ 2014/2015 YoY ∆ 2015/2016 YoY

Production Rigs

U.S. Crude Production VS Rig Count

In 2016, Non-OPEC Declines and U.S. Shale Growth Slows Significantly...

NON-OPEC

Saudi Arabia, 10.10

Iraq, 4.24

Iran, 3.20UAE, 2.91

Kuwait, 2.82

Venezuela, 2.23

Nigeria, 2.16

Angola, 1.80

Algeria, 1.08

Qatar, 0.69 Ecuador, 0.54Libya, 0.38

OPEC CRUDE PRODUCTION 2016 (MMBD)

OPEC Declines and U.S. Shale Growth Slows Significantly...

OPEC

MMBD

13

Economics Oil & Refining LNG & Gas Petrochemical

DEMAND

Source: PTT International Market Analysis Team, DOE, IEA, OPEC, Vitol, PIRA

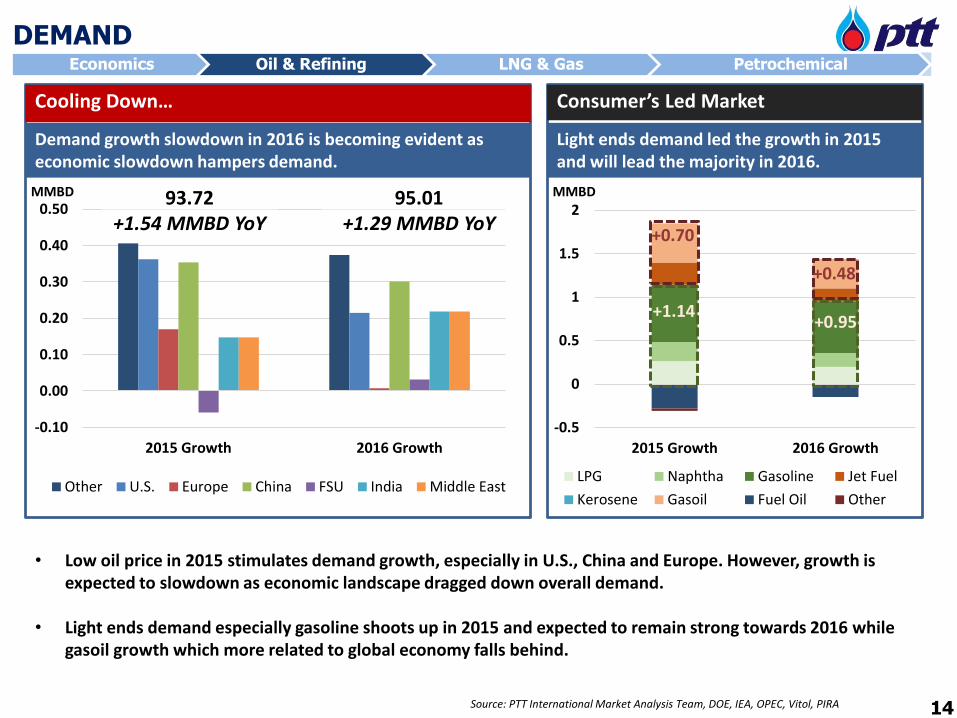

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

2015 Growth 2016 Growth

Other U.S. Europe China FSU India Middle East

95.01+1.29 MMBD YoY

93.72+1.54 MMBD YoY

Demand growth slowdown in 2016 is becoming evident as economic slowdown hampers demand.

Cooling Down…

-0.5

0

0.5

1

1.5

2

2015 Growth 2016 Growth

LPG Naphtha Gasoline Jet Fuel

Kerosene Gasoil Fuel Oil Other

+0.95+1.14

+0.70

+0.48

Light ends demand led the growth in 2015 and will lead the majority in 2016.

Consumer’s Led Market

• Low oil price in 2015 stimulates demand growth, especially in U.S., China and Europe. However, growth is expected to slowdown as economic landscape dragged down overall demand.

• Light ends demand especially gasoline shoots up in 2015 and expected to remain strong towards 2016 while gasoil growth which more related to global economy falls behind.

MMBD MMBD

14

Economics Oil & Refining LNG & Gas Petrochemical

REFINING BUSINESS

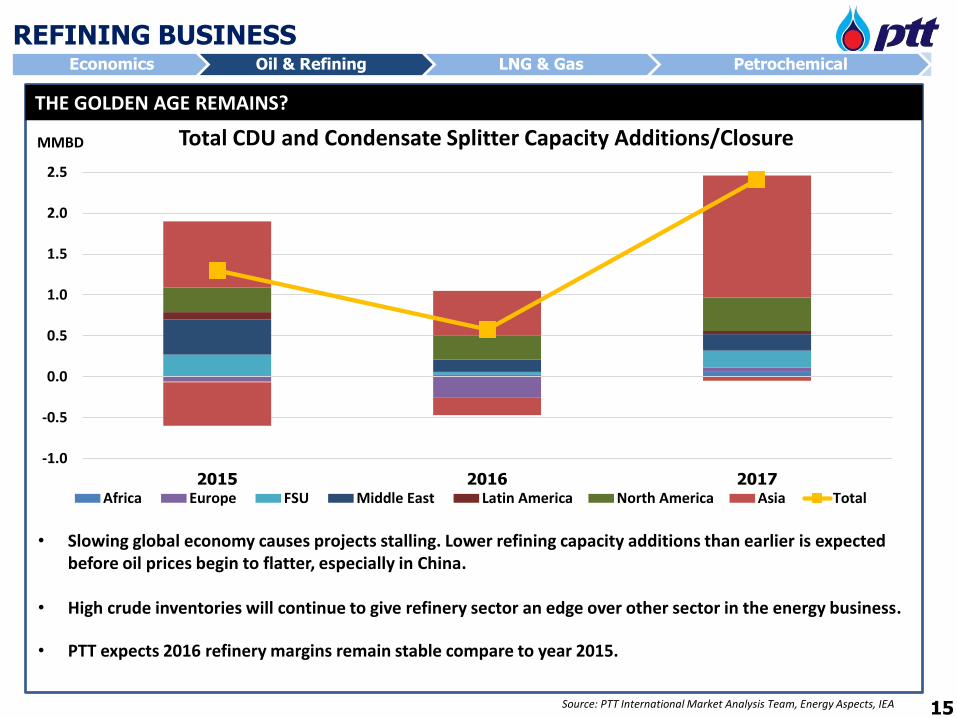

Source: PTT International Market Analysis Team, Energy Aspects, IEA

Total CDU and Condensate Splitter Capacity Additions/Closure

• Slowing global economy causes projects stalling. Lower refining capacity additions than earlier is expected before oil prices begin to flatter, especially in China.

• High crude inventories will continue to give refinery sector an edge over other sector in the energy business.

• PTT expects 2016 refinery margins remain stable compare to year 2015.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2015 2016 2017Africa Europe FSU Middle East Latin America North America Asia Total

MMBD

THE GOLDEN AGE REMAINS?

15

90

91

92

93

94

95

96

97

2014 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Demand Supply

Economics Oil & Refining LNG & Gas Petrochemical

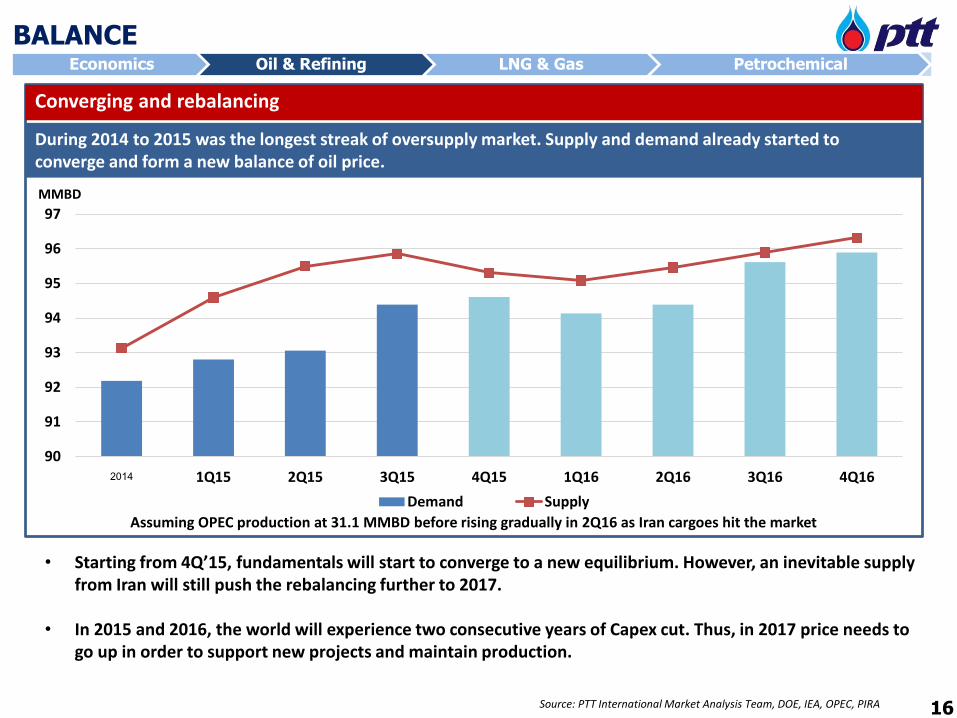

BALANCE

Source: PTT International Market Analysis Team, DOE, IEA, OPEC, PIRA

During 2014 to 2015 was the longest streak of oversupply market. Supply and demand already started to converge and form a new balance of oil price.

Converging and rebalancing

Assuming OPEC production at 31.1 MMBD before rising gradually in 2Q16 as Iran cargoes hit the market

MMBD

• Starting from 4Q’15, fundamentals will start to converge to a new equilibrium. However, an inevitable supply from Iran will still push the rebalancing further to 2017.

• In 2015 and 2016, the world will experience two consecutive years of Capex cut. Thus, in 2017 price needs to go up in order to support new projects and maintain production.

16

16

Economics Oil & Refining LNG & Gas Petrochemical

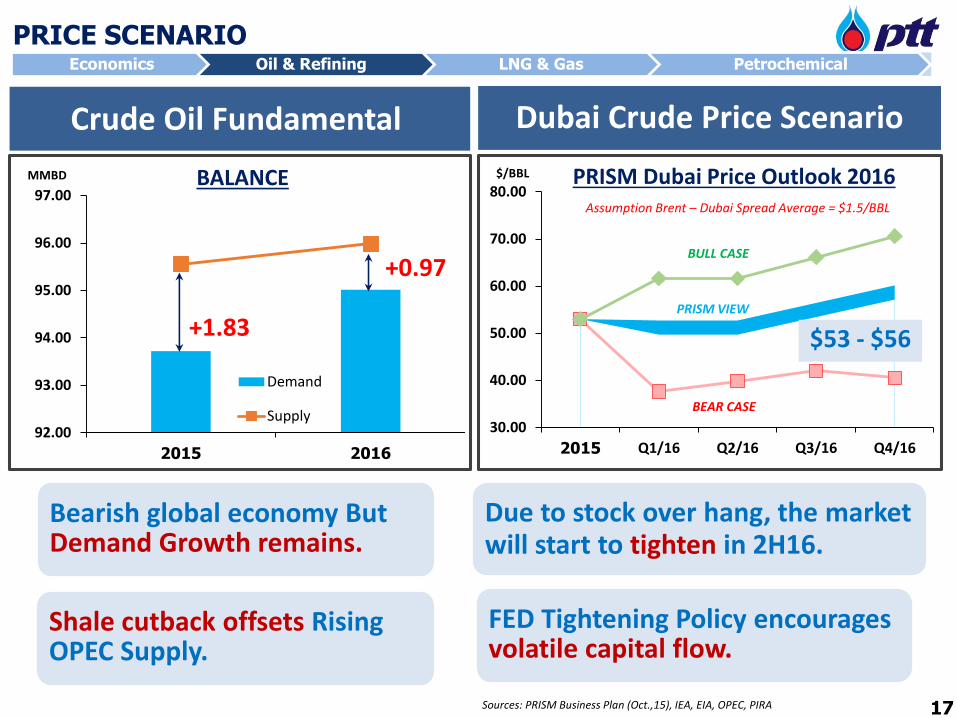

PRICE SCENARIO

Sources: PRISM Business Plan (Oct.,15), IEA, EIA, OPEC, PIRA

Bearish global economy ButDemand Growth remains.

Shale cutback offsets Rising OPEC Supply.

Due to stock over hang, the market will start to tighten in 2H16.

FED Tightening Policy encourages volatile capital flow.

30.00

40.00

50.00

60.00

70.00

80.00

2015 Q1/16 Q2/16 Q3/16 Q4/16

$/BBL

Dubai Crude Price ScenarioCrude Oil Fundamental

92.00

93.00

94.00

95.00

96.00

97.00

2015 2016

MMBD

Demand

Supply

+1.83

+0.97

BALANCE PRISM Dubai Price Outlook 2016Assumption Brent – Dubai Spread Average = $1.5/BBL

BULL CASE

BEAR CASE

PRISM VIEW

$53 - $56

17

Economics

Oil & Refining

LNG & Gas

Petrochemical

Economics Oil & Refining LNG & Gas Petrochemical

Contents

18

LNG & Gas

Presented By:

Dulyapun BuranawitTeam Leader

Liquefied Natural Gas Supply Department

19

Economics Oil & Refining LNG & Gas Petrochemical

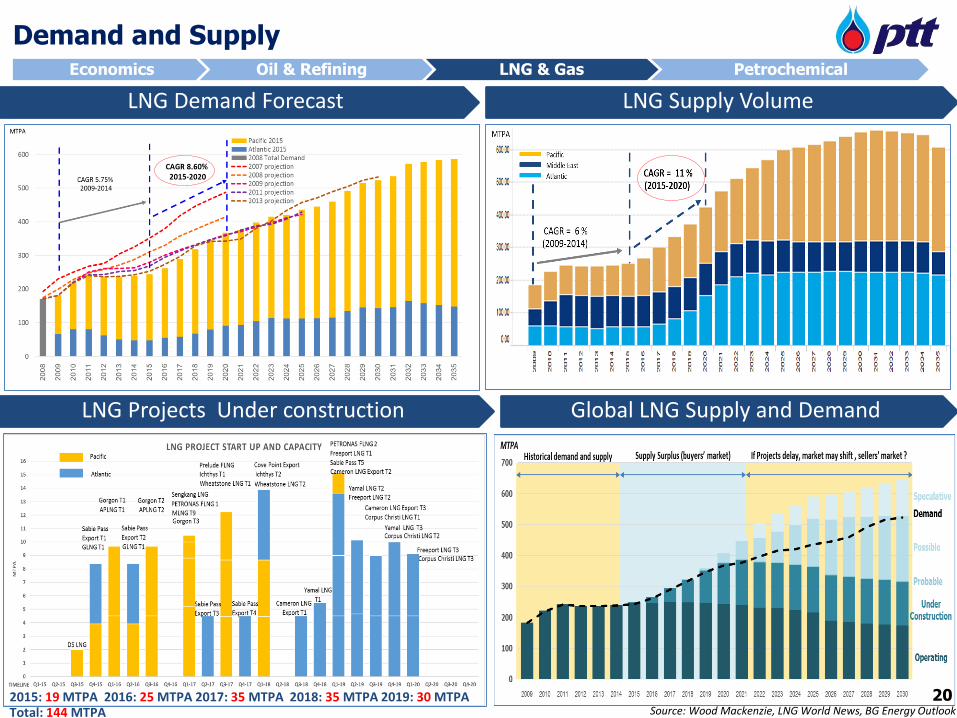

Demand and Supply

Global LNG Supply and Demand

LNG Demand Forecast LNG Supply Volume

LNG Projects Under construction

2015: 19 MTPA 2016: 25 MTPA 2017: 35 MTPA 2018: 35 MTPA 2019: 30 MTPATotal: 144 MTPA Source: Wood Mackenzie, LNG World News, BG Energy Outlook

20

20

LNG Price Outlook and Key Drivers 2016

Bull Bear

• New LNG demand from emerging countries in South East Asia, Middle East, and Eastern Europe

• Positive outcomes from United Nation climate change conference in Paris (Nov)

• Faster-than-expected depletion of indigenous gas in Europe/Asia/South America

• EU policy for guidance of emission trading system (EU ETS) and gas diversification from Russia

• New LNG supply from Australian and US projects (GLNG, APLNG, Gorgon, and Sabine Pass)

• Restart of nuclear power plants in Japan and new commercial operation plants in Korea

• Wildcard LNG projects in Angola and Yemen might start up their production in 2016

• Existing gas price structures in India and China discourage domestic gas consumption

Henry Hub Outlook 2016 LNG Price Outlook 2016

LNG Market Key Drivers for 2016

Source: Wood Mackenzie, PIRA Remark: HH excludes liquefaction fees and freight costs

Economics Oil & Refining LNG & Gas Petrochemical

HH 2016 2.7 – 3.2 $/MMBTU

Long term LNG Price7 – 9 $/MMBTU

Spot LNG Price6 - 7 $/MMBTU

Price divergence

21

Economics

Oil & Refining

LNG & Gas

Petrochemical

Economics Oil & Refining LNG & Gas Petrochemical

Contents

22

Petrochemical

Presented By:

Ekachai SirithammasanVice President

Petrochemicals Subsidiary Planning & Management Department

Economics Oil & Refining LNG & Gas Petrochemical

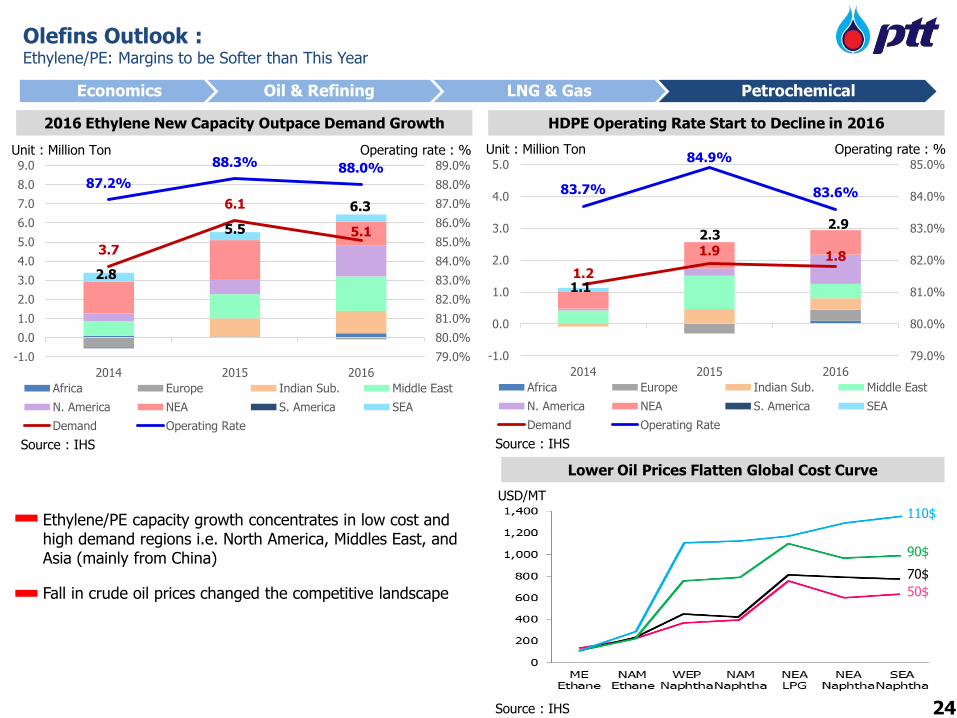

Olefins Outlook :Ethylene/PE: Margins to be Softer than This Year

Ethylene/PE capacity growth concentrates in low cost and high demand regions i.e. North America, Middles East, and Asia (mainly from China)

Fall in crude oil prices changed the competitive landscape

USD/MT

Lower Oil Prices Flatten Global Cost Curve

110$

90$

70$

50$

Source : IHS

2016 Ethylene New Capacity Outpace Demand Growth

Source : IHS

3.7

6.1

5.1

87.2%

88.3% 88.0%

79.0%

80.0%

81.0%

82.0%

83.0%

84.0%

85.0%

86.0%

87.0%

88.0%

89.0%

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2014 2015 2016

Africa Europe Indian Sub. Middle East

N. America NEA S. America SEA

Demand Operating Rate

Unit : Million Ton Operating rate : %

6.3

5.5

2.8

HDPE Operating Rate Start to Decline in 2016

Source : IHS

1.2

1.9 1.8

83.7%

84.9%

83.6%

79.0%

80.0%

81.0%

82.0%

83.0%

84.0%

85.0%

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2014 2015 2016

Africa Europe Indian Sub. Middle East

N. America NEA S. America SEA

Demand Operating Rate

Unit : Million Ton Operating rate : %

2.3

1.1

2.9

24

Economics Oil & Refining LNG & Gas Petrochemical

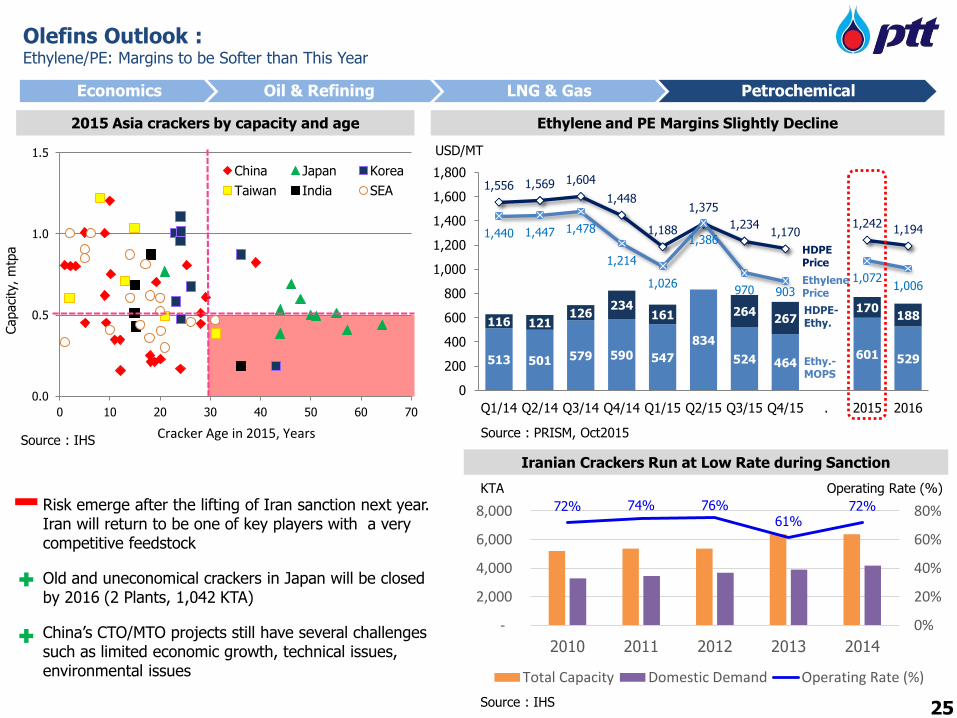

2015 Asia crackers by capacity and age Ethylene and PE Margins Slightly Decline

513 501 579 590 547

834

524 464601 529

116 121126

234161 264

267170

188

1,556 1,569 1,604

1,448

1,188

1,375

1,2341,170

1,2421,1941,440 1,447 1,478

1,214

1,026

1,386

970 9031,072

1,006

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 . 2015 2016

USD/MT

HDPE-Ethy.

Ethy.-MOPS

HDPE Price

Ethylene Price

72% 74% 76%61%

72%

0%

20%

40%

60%

80%

-

2,000

4,000

6,000

8,000

2010 2011 2012 2013 2014

Total Capacity Domestic Demand Operating Rate (%)

Iranian Crackers Run at Low Rate during Sanction

KTA Operating Rate (%)

Source : IHSSource : PRISM, Oct2015

Olefins Outlook :Ethylene/PE: Margins to be Softer than This Year

Risk emerge after the lifting of Iran sanction next year. Iran will return to be one of key players with a very competitive feedstock

Old and uneconomical crackers in Japan will be closed by 2016 (2 Plants, 1,042 KTA)

China’s CTO/MTO projects still have several challenges such as limited economic growth, technical issues, environmental issues

0.0

0.5

1.0

1.5

0 10 20 30 40 50 60 70

China Japan Korea

Taiwan India SEA

Cracker Age in 2015, Years

Capaci

ty, m

tpa

Source : IHS 25

Economics Oil & Refining LNG & Gas Petrochemical

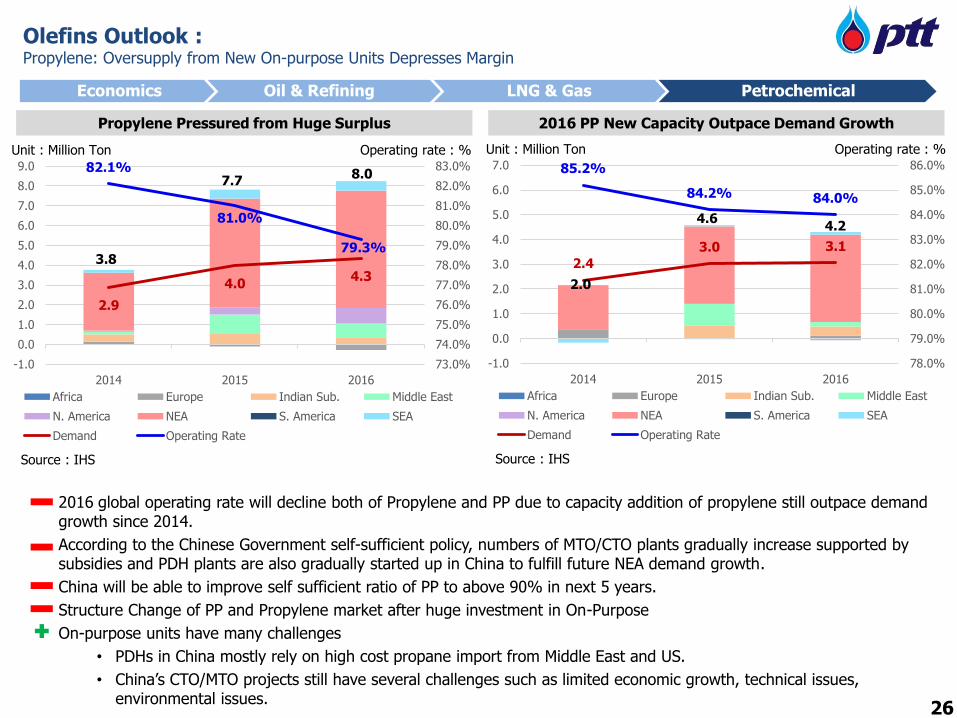

Propylene Pressured from Huge Surplus 2016 PP New Capacity Outpace Demand Growth

Source : IHS

2.9

4.04.3

82.1%

81.0%

79.3%

73.0%

74.0%

75.0%

76.0%

77.0%

78.0%

79.0%

80.0%

81.0%

82.0%

83.0%

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2014 2015 2016

Africa Europe Indian Sub. Middle East

N. America NEA S. America SEA

Demand Operating Rate

Unit : Million Ton Operating rate : %

Source : IHS

2.4

3.0 3.1

85.2%

84.2% 84.0%

78.0%

79.0%

80.0%

81.0%

82.0%

83.0%

84.0%

85.0%

86.0%

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2014 2015 2016

Africa Europe Indian Sub. Middle East

N. America NEA S. America SEA

Demand Operating Rate

Unit : Million Ton Operating rate : %

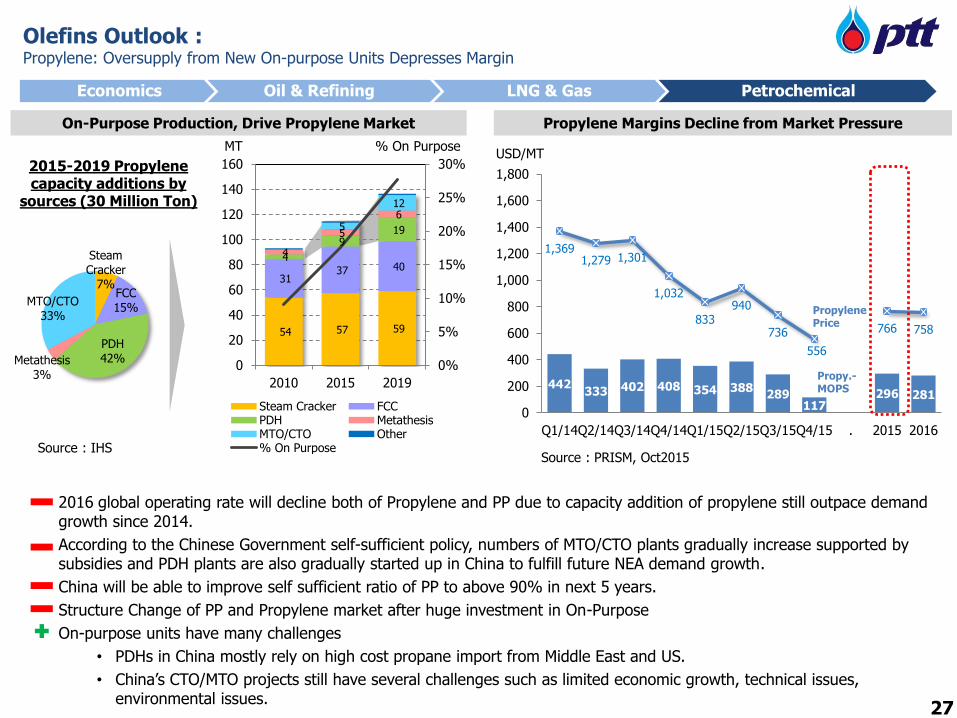

2016 global operating rate will decline both of Propylene and PP due to capacity addition of propylene still outpace demand growth since 2014.

According to the Chinese Government self-sufficient policy, numbers of MTO/CTO plants gradually increase supported by subsidies and PDH plants are also gradually started up in China to fulfill future NEA demand growth.

China will be able to improve self sufficient ratio of PP to above 90% in next 5 years.

Structure Change of PP and Propylene market after huge investment in On-Purpose

On-purpose units have many challenges

• PDHs in China mostly rely on high cost propane import from Middle East and US.

• China’s CTO/MTO projects still have several challenges such as limited economic growth, technical issues, environmental issues.

Olefins Outlook :Propylene: Oversupply from New On-purpose Units Depresses Margin

3.8

7.78.0

2.0

4.64.2

26

Economics Oil & Refining LNG & Gas Petrochemical

Source : IHS

Propylene Margins Decline from Market Pressure

442333 402 408 354 388

289117

296 281

1,3691,279 1,301

1,032

833940

736

556

766 758

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1/14Q2/14Q3/14Q4/14Q1/15Q2/15Q3/15Q4/15 . 2015 2016

USD/MT

Propy.-MOPS

Propylene Price

Source : PRISM, Oct2015

On-Purpose Production, Drive Propylene Market

Steam Cracker

7%FCC15%

PDH42%Metathesis

3%

MTO/CTO33%

2015-2019 Propylene capacity additions by

sources (30 Million Ton)

MT

54 57 59

31 37 40

4

9 19

4

5

6 5

12

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

160

2010 2015 2019

Steam Cracker FCCPDH MetathesisMTO/CTO Other% On Purpose

% On Purpose

Olefins Outlook :Propylene: Oversupply from New On-purpose Units Depresses Margin

2016 global operating rate will decline both of Propylene and PP due to capacity addition of propylene still outpace demand growth since 2014.

According to the Chinese Government self-sufficient policy, numbers of MTO/CTO plants gradually increase supported by subsidies and PDH plants are also gradually started up in China to fulfill future NEA demand growth.

China will be able to improve self sufficient ratio of PP to above 90% in next 5 years.

Structure Change of PP and Propylene market after huge investment in On-Purpose

On-purpose units have many challenges

• PDHs in China mostly rely on high cost propane import from Middle East and US.

• China’s CTO/MTO projects still have several challenges such as limited economic growth, technical issues, environmental issues.

27

Economics Oil & Refining LNG & Gas Petrochemical

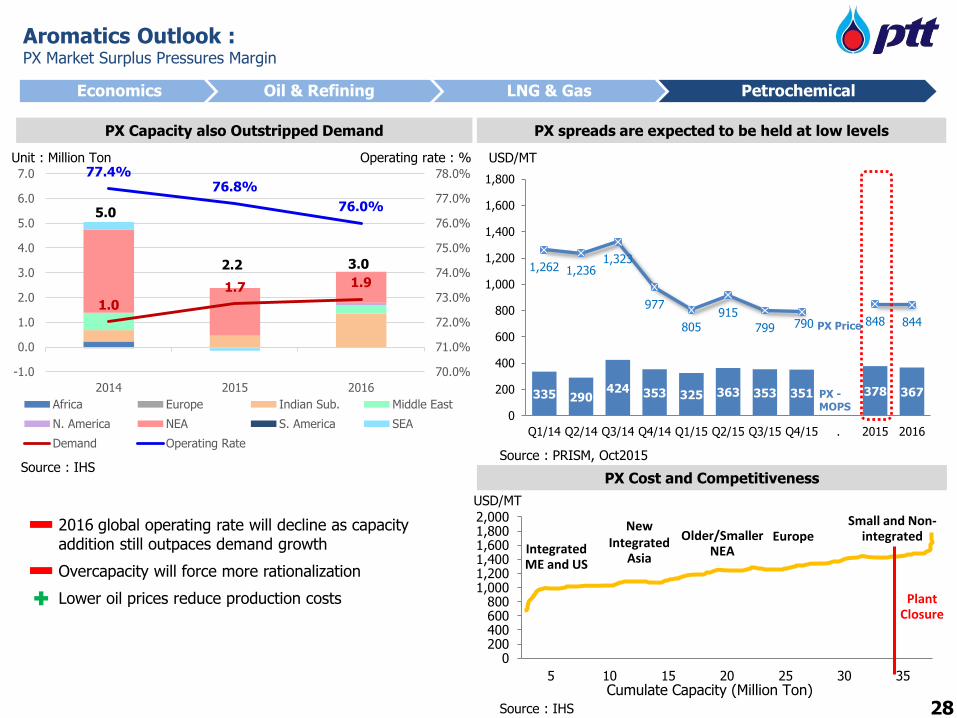

Aromatics Outlook :PX Market Surplus Pressures Margin

PX Capacity also Outstripped Demand

2016 global operating rate will decline as capacity addition still outpaces demand growth

Overcapacity will force more rationalization

Lower oil prices reduce production costs

PX spreads are expected to be held at low levels

335 290424 353 325 363 353 351 378 367

1,262 1,2361,323

977

805915

799 790 848 844

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 . 2015 2016

USD/MT

PX -MOPS

PX Price

Source : PRISM, Oct2015

PX Cost and Competitiveness

0200400600800

1,0001,2001,4001,6001,8002,000

5 10 15 20 25 30 35

Integrated ME and US

New Integrated

Asia

Older/Smaller NEA

EuropeSmall and Non-

integrated

PlantClosure

USD/MT

Cumulate Capacity (Million Ton)

Source : IHS

1.0

1.7 1.9

77.4%76.8%

76.0%

70.0%

71.0%

72.0%

73.0%

74.0%

75.0%

76.0%

77.0%

78.0%

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2014 2015 2016

Africa Europe Indian Sub. Middle East

N. America NEA S. America SEA

Demand Operating Rate

Unit : Million Ton Operating rate : %

5.0

2.2 3.0

Source : IHS 28

Economics Oil & Refining LNG & Gas Petrochemical

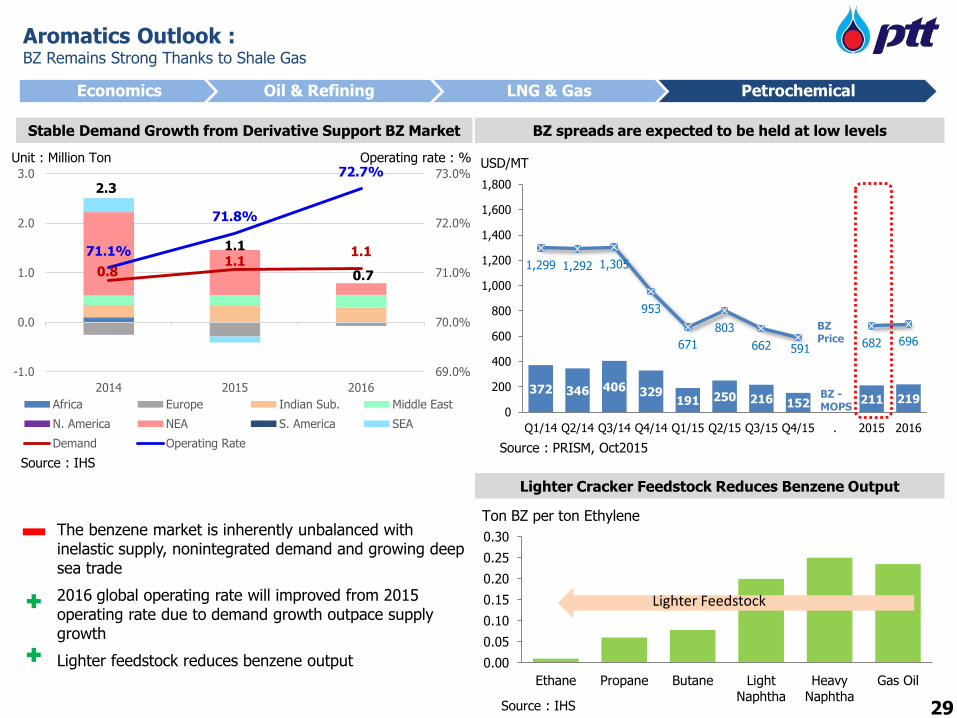

Aromatics Outlook :BZ Remains Strong Thanks to Shale Gas

Stable Demand Growth from Derivative Support BZ Market BZ spreads are expected to be held at low levels

372 346 406 329191 250 216 152 211 219

1,299 1,292 1,305

953

671

803

662 591 682 696

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 . 2015 2016

USD/MT

BZ -MOPS

BZ Price

Lighter Cracker Feedstock Reduces Benzene Output

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Ethane Propane Butane LightNaphtha

HeavyNaphtha

Gas Oil

Ton BZ per ton Ethylene

Lighter Feedstock

Source : IHS

0.81.1

1.171.1%

71.8%

72.7%

69.0%

70.0%

71.0%

72.0%

73.0%

-1.0

0.0

1.0

2.0

3.0

2014 2015 2016

Africa Europe Indian Sub. Middle East

N. America NEA S. America SEA

Demand Operating Rate

Unit : Million Ton Operating rate : %

Source : PRISM, Oct2015

The benzene market is inherently unbalanced with inelastic supply, nonintegrated demand and growing deep sea trade

2016 global operating rate will improved from 2015 operating rate due to demand growth outpace supply growth

Lighter feedstock reduces benzene output

2.3

0.7

1.1

Source : IHS 29

Thank youPTT Public Company Limited – Investor Relations Department

Tel. +66 2 537-3518, Fax. +66 2 537-3948, E-mail: [email protected] Website: http://www.pttplc.com

Disclaimer

The information contained in our presentation is intended solely for your personal reference only. In addition, such information contains projections and forward-looking

statements that reflect our current views with respect to future events and financial performance. These views are based on assumptions subject to various risks and

uncertainties. No assurance is given that future events will occur, that projections will be achieved, or that our assumptions are correct. Actual results may differ

materially from those projected.

Petroleum Reserves and Resources Information

In this presentation, the Company discloses petroleum reserves and resources that are not included in the Securities Exchange and Commission of Thailand (SEC) Annual

Registration Statement Form 56-1 under “Supplemental Information on Petroleum Exploration and Production Activities”. The reserves and resources data contained in

this presentation reflects the Company’s best estimates of its reserves and resources. While the Company periodically obtains an independent audit of a portion of its

proved reserves, no independent qualified reserves evaluator or auditor was involved in the preparation of reserves and resources data disclosed in this presentation.

Unless stated otherwise, reserves and resources are stated at the Company’s gross basis. This presentation may contain the terms “proved reserves”, “probable reserves”,

and/or “contingent resources”. Unless stated otherwise, the Company adopts similar description as defined by the Society of Petroleum Engineers.

Proved Reserves - Proved reserves are defined as those quantities of petroleum which, by analysis of geological and engineering data, can be estimated with reasonable

certainty to be commercially recoverable, from a given date forward, from known reservoirs and under current economic conditions, operating methods, and government

regulations.

Probable Reserves - Probable reserves are defined as those unproved reserves which analysis of geological and engineering data suggests are more likely than not to be

recoverable.

Contingent Resources – Contingent resources are defined as those quantities of petroleum which are estimated, on a given date, to be potentially recoverable from

known accumulations, but which are not currently considered to be commercially recoverable. The reasons for non commerciality could be economic including market

availability, political, environmental, or technological.

29

30

30

Q & A

31