industry primer - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

21 October 2015

Asia Pacific/China&Hong Kong

Equity Research

Advertising / New Media (Media CN (Asia))

China Media and Entertainment Sector

INDUSTRY PRIMER

"Internet + Movie": Online ticketing becoming

the No.1 channel

Figure 1: Online ticketing revenue and % contribution to total movie box office

4.9 13.6

29.038.0

48.7

60.0

71.5

84.3

22%

46%

70% 72%75% 77% 78% 80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2013 2014 2015F 2016F 2017F 2018F 2019F 2020F

Rmb Bn

Online ticketing revenue % contribution to total movie box office revenue

Source: Company data, Credit Suisse estimates

■ Fast development in online ticketing sector. Fuelled by both the boom in

China's box office and the rise in O2O, the online ticketing sector has

expanded exponentially in the past five years, recording Rmb13.5 bn revenue

in 1H15 and accounting for 66.5% of the total box office revenue. We estimate

the online ticketing market to grow to Rmb84 bn in 2020, contributing 80% of

the total movie box office in China. At the same time, online ticketing growth

also stimulates the expansion of the box office revenue.

■ Fierce competition with heavy price subsidy. Major internet players (Alibaba,

Baidu, and Tencent), along with media players (Wanda, Oriental Pearl) have

entered the online ticketing space by investing in the major players. Subsidy

from the online ticketing O2O platform is estimated to be Rmb2 bn in 2014 or

7% of the box office revenue. We continue to expect Baidu's subsidies to be

Rmb3.8 bn in the next three years. In our view, the battle will continue in the

short term until the market is consolidated with three to five dominant players.

■ Market opportunities to online ticketing O2O platform. Ticket price subsidy

has helped develop customers' movie watching habits, and the O2O platform

has the ability to influence their ticket-purchasing behaviour. When competition

eases and subsidy stops, the O2O platform could charge a service fee.

■ Stock calls. Growth in online ticketing should support the high growth in China's box office revenue, and we believe cinema chains will be the biggest beneficiary. Key beneficiaries in media sector include OSGH (1132 HK). Baidu O2O platform should benefit in the long-term as well.

Research Analysts

David Hao

852 2101 7310

Dick Wei

852 2101 7339

Evan Zhou

852 2101 6745

21 October 2015

China Media and Entertainment Sector 2

Focus charts Figure 2: Online ticketing revenue growth trend Figure 3: Market share of movie ticket channels (2Q15)

4.9

13.6

29.0

38.0

48.7

60.0

71.5

84.3179%

114%

31% 28%23% 19% 18%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2013 2014 2015F 2016F 2017F 2018F 2019F 2020F

Rmb Bn

Online ticketing revenue y-y

22%

46%

70% 72%75% 77% 78% 80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2013 2014 2015F 2016F 2017F 2018F 2019F 2020F

% contribution to total movie box office revenue

Source: Analysys Group, Credit Suisse estimates Source: Analysys Group, Credit Suisse estimates

Figure 4: Market share of major players (2Q15) Figure 5: Investment from internet and media companies

36%

21%

8%

6%

6%

5%

2%

Maoyan (猫眼), 36%

Gewara (格瓦拉), 22%

Wepiao (微票儿), 8%

Taobao (淘宝电影), 6%

Mtime (时光网), 6%

Wanda (万达电影), 5%

Maizuo (卖座网), 2%

Others (including Baidu Nuomi

百度糯米), 16%

Meituan Dianping

China Media Capital

Tencent

Alibaba

Wanda Cinema Line

Wanda Cinema Line

Huayi Brothers

Tencent

Alibaba

Baidu

Oriental Pearl

Maoyan (猫眼), 36%

Gewara (格瓦拉), 22%

Wepiao (微票儿), 8%

Taobao (淘宝电影), 6%

Mtime (时光网), 6%

Wanda (万达电影), 5%

Maizuo (卖座网), 2%

Others (including Baidu

Nuomi 百度糯米), 16% Source: Analysys Group Source: Credit Suisse Research

Figure 6: Production company and e-commerce subsidy

trend

Figure 7: Potential market size of online ticketing service

fee (assuming 5% take rate)

2

3.7 3.7

3.2

2.3

1.4

0.5

2

4.6 4.6

3.4

2.4

1.4

0.5

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

-

1

1

2

2

3

3

4

4

5

5

2014 2015F 2016F 2017F 2018F 2019F 2020F

Rmb Bn

Production company subsidy e-commerce subsidy

Production company (as % of total box office) e-commerce (as % of online box office)

1.5

1.9

2.4

3.0

3.6

4.2

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2013 2014 2015F 2016F 2017F 2018F

Rmb Bn

Potential Market Size of Online Ticketing Service fee (Rmb Bn) (Assuming 5% take rate)

Source: Credit Suisse estimates Source: Credit Suisse estimates

21 October 2015

China Media and Entertainment Sector 3

"Internet + Movie": Online ticketing becoming the No.1 channel Fast development of online ticketing sector

Fuelled by both the boom in China's movie box office revenue and the rise in the online to

offline (O2O) platform, the online ticketing services sector has expanded exponentially in

the past five years, recording Rmb13.5 bn revenue in 1H15, compared with Rmb13.6 bn in

full-year 2014 and Rmb4.9 bn in 2013—overtaking offline ticket sales as the No.1 channel

with 66.5% share. We estimate online ticketing to continue to grow, reaching Rmb84.3 bn

in 2020, and accounting for 80% of the domestic movie box office.

Fierce competition in online ticketing

As the market expands rapidly, many new players will likely enter the online movie ticket

seating selection space, including vertically focused movie sales websites (such as

Gewara, Mtime and Maizuo), e-commerce and O2O websites (such as Maoyan and

Taobao), social media websites (such as Wechat), and cinema line self-developed

websites (such as Wanda, China Film and Jinyi).

The industry is very segmented—with investment from BAT and other media giants, online

ticketing platforms are in heavy battle for market share with increasing subsidies. We continue

to expect Baidu's subsidies in online ticketing to be Rmb3.8 bn over the next three years.

How do customers choose ticket platforms? Customers normally choose ticket

platforms based on four factors: (1) availability, (2) price, (3) convenience and (4) other

value-added services. There are six major types of online ticketing business models: (1)

Groupbuy, (2) online ticket selection only, (3) e-commerce, (4) social and search platform,

(5) UGC (User Generated Content) and (6) cinema line.

Near-term, subsidies remain high

In our view, subsidies from online ticket platforms are likely to stay in the medium term due

to: (1) market still being fragmented, (2) BAT focusing on the entertainment space and (3)

attractive movie categories to win customers for other O2O categories.

What will be the impact if subsidy stops? In 2014, subsidy from e-commerce and

movie studios totalled ~Rmb4 bn, accounting for 13.5% of China's box office—Rmb2 bn of

that is from online ticketing platforms. In the long run, when the market is consolidated with

3-5 dominant players, subsidy will slow down or stop eventually and the market will grow

organically. We think the impact to China's movie box office and to online ticketing

platforms will be small. Movie watching and purchasing tickets online is becoming a habit

for customers, especially the younger generation, which grew up with the internet and

spend a great portion of their income on online consumption.

Potential market size for online movie ticketing

In mature markets, online ticketing platforms charge a service fee (5-10% of ticket price); we

believe this will be a major revenue stream for ticketing platforms in China in the long run.

Assuming a 5% take rate, the market size for the service charge would be Rmb4 bn by 2018.

Key policy update: On 8 July 2015, China Film Distribution and Exhibition Association

and China Film Producers' Association together issued the "Regulation on Movie Ticket

Sales and Marketing". According to the policy, online ticketing platforms have to pay the

minimum ticket price agreed in distribution agreements in case of a subsidy.

We estimate online ticketing

to continue to grow,

recording Rmb84.3 bn in

2020, and accounting for

80% of the domestic movie

box office

Online ticket platforms are in

fierce competition owing to

heavy ticket price subsidy

Customers choose platforms

based on availability, price,

convenience and other

value-added services

We believe subsidies are

likely to stay in the medium

term and will stop in the long

term; however, we think the

impact to the box office and

ticketing platforms will be

small if subsidies stop

21 October 2015

China Media and Entertainment Sector 4

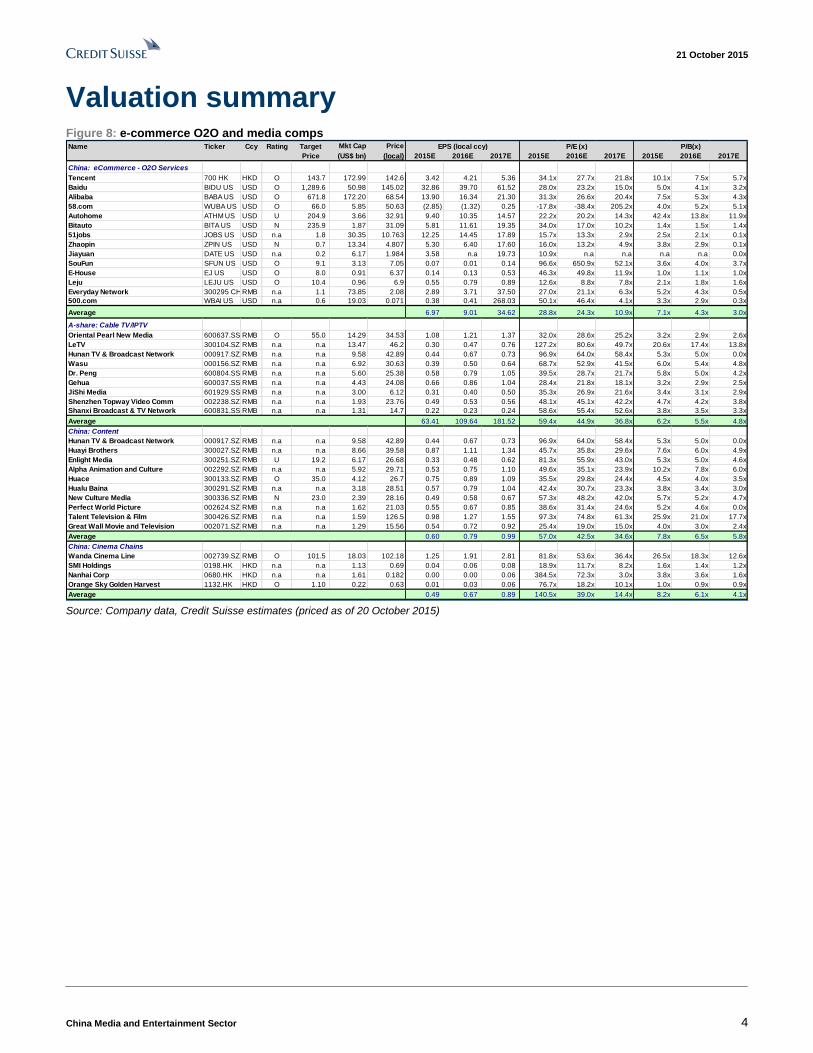

Valuation summary Figure 8: e-commerce O2O and media comps Name Ticker Ccy Rating Target Mkt Cap Price

Price (US$ bn) (local) 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E

China: eCommerce - O2O Services

Tencent 700 HK HKD O 143.7 172.99 142.6 3.42 4.21 5.36 34.1x 27.7x 21.8x 10.1x 7.5x 5.7x

Baidu BIDU US USD O 1,289.6 50.98 145.02 32.86 39.70 61.52 28.0x 23.2x 15.0x 5.0x 4.1x 3.2x

Alibaba BABA US USD O 671.8 172.20 68.54 13.90 16.34 21.30 31.3x 26.6x 20.4x 7.5x 5.3x 4.3x

58.com WUBA US USD O 66.0 5.85 50.63 (2.85) (1.32) 0.25 -17.8x -38.4x 205.2x 4.0x 5.2x 5.1x

Autohome ATHM US USD U 204.9 3.66 32.91 9.40 10.35 14.57 22.2x 20.2x 14.3x 42.4x 13.8x 11.9x

Bitauto BITA US USD N 235.9 1.87 31.09 5.81 11.61 19.35 34.0x 17.0x 10.2x 1.4x 1.5x 1.4x

51jobs JOBS US USD n.a 1.8 30.35 10.763 12.25 14.45 17.89 15.7x 13.3x 2.9x 2.5x 2.1x 0.1x

Zhaopin ZPIN US USD N 0.7 13.34 4.807 5.30 6.40 17.60 16.0x 13.2x 4.9x 3.8x 2.9x 0.1x

Jiayuan DATE US USD n.a 0.2 6.17 1.984 3.58 n.a 19.73 10.9x n.a n.a n.a n.a 0.0x

SouFun SFUN US USD O 9.1 3.13 7.05 0.07 0.01 0.14 96.6x 650.9x 52.1x 3.6x 4.0x 3.7x

E-House EJ US USD O 8.0 0.91 6.37 0.14 0.13 0.53 46.3x 49.8x 11.9x 1.0x 1.1x 1.0x

Leju LEJU US USD O 10.4 0.96 6.9 0.55 0.79 0.89 12.6x 8.8x 7.8x 2.1x 1.8x 1.6x

Everyday Network 300295 CHRMB n.a 1.1 73.85 2.08 2.89 3.71 37.50 27.0x 21.1x 6.3x 5.2x 4.3x 0.5x

500.com WBAI US USD n.a 0.6 19.03 0.071 0.38 0.41 268.03 50.1x 46.4x 4.1x 3.3x 2.9x 0.3x

Average 6.97 9.01 34.62 28.8x 24.3x 10.9x 7.1x 4.3x 3.0x

A-share: Cable TV/IPTV

Oriental Pearl New Media 600637.SS RMB O 55.0 14.29 34.53 1.08 1.21 1.37 32.0x 28.6x 25.2x 3.2x 2.9x 2.6x

LeTV 300104.SZ RMB n.a n.a 13.47 46.2 0.30 0.47 0.76 127.2x 80.6x 49.7x 20.6x 17.4x 13.8x

Hunan TV & Broadcast Network 000917.SZ RMB n.a n.a 9.58 42.89 0.44 0.67 0.73 96.9x 64.0x 58.4x 5.3x 5.0x 0.0x

Wasu 000156.SZ RMB n.a n.a 6.92 30.63 0.39 0.50 0.64 68.7x 52.9x 41.5x 6.0x 5.4x 4.8x

Dr. Peng 600804.SS RMB n.a n.a 5.60 25.38 0.58 0.79 1.05 39.5x 28.7x 21.7x 5.8x 5.0x 4.2x

Gehua 600037.SS RMB n.a n.a 4.43 24.08 0.66 0.86 1.04 28.4x 21.8x 18.1x 3.2x 2.9x 2.5x

JiShi Media 601929.SS RMB n.a n.a 3.00 6.12 0.31 0.40 0.50 35.3x 26.9x 21.6x 3.4x 3.1x 2.9x

Shenzhen Topway Video Comm 002238.SZ RMB n.a n.a 1.93 23.76 0.49 0.53 0.56 48.1x 45.1x 42.2x 4.7x 4.2x 3.8x

Shanxi Broadcast & TV Network 600831.SS RMB n.a n.a 1.31 14.7 0.22 0.23 0.24 58.6x 55.4x 52.6x 3.8x 3.5x 3.3x

Average 63.41 109.64 181.52 59.4x 44.9x 36.8x 6.2x 5.5x 4.8x

China: Content

Hunan TV & Broadcast Network 000917.SZ RMB n.a n.a 9.58 42.89 0.44 0.67 0.73 96.9x 64.0x 58.4x 5.3x 5.0x 0.0x

Huayi Brothers 300027.SZ RMB n.a n.a 8.66 39.58 0.87 1.11 1.34 45.7x 35.8x 29.6x 7.6x 6.0x 4.9x

Enlight Media 300251.SZ RMB U 19.2 6.17 26.68 0.33 0.48 0.62 81.3x 55.9x 43.0x 5.3x 5.0x 4.6x

Alpha Animation and Culture 002292.SZ RMB n.a n.a 5.92 29.71 0.53 0.75 1.10 49.6x 35.1x 23.9x 10.2x 7.8x 6.0x

Huace 300133.SZ RMB O 35.0 4.12 26.7 0.75 0.89 1.09 35.5x 29.8x 24.4x 4.5x 4.0x 3.5x

Hualu Baina 300291.SZ RMB n.a n.a 3.18 28.51 0.57 0.79 1.04 42.4x 30.7x 23.3x 3.8x 3.4x 3.0x

New Culture Media 300336.SZ RMB N 23.0 2.39 28.16 0.49 0.58 0.67 57.3x 48.2x 42.0x 5.7x 5.2x 4.7x

Perfect World Picture 002624.SZ RMB n.a n.a 1.62 21.03 0.55 0.67 0.85 38.6x 31.4x 24.6x 5.2x 4.6x 0.0x

Talent Television & Film 300426.SZ RMB n.a n.a 1.59 126.5 0.98 1.27 1.55 97.3x 74.8x 61.3x 25.9x 21.0x 17.7x

Great Wall Movie and Television 002071.SZ RMB n.a n.a 1.29 15.56 0.54 0.72 0.92 25.4x 19.0x 15.0x 4.0x 3.0x 2.4x

Average 0.60 0.79 0.99 57.0x 42.5x 34.6x 7.8x 6.5x 5.8x

China: Cinema Chains

Wanda Cinema Line 002739.SZ RMB O 101.5 18.03 102.18 1.25 1.91 2.81 81.8x 53.6x 36.4x 26.5x 18.3x 12.6x

SMI Holdings 0198.HK HKD n.a n.a 1.13 0.69 0.04 0.06 0.08 18.9x 11.7x 8.2x 1.6x 1.4x 1.2x

Nanhai Corp 0680.HK HKD n.a n.a 1.61 0.182 0.00 0.00 0.06 384.5x 72.3x 3.0x 3.8x 3.6x 1.6x

Orange Sky Golden Harvest 1132.HK HKD O 1.10 0.22 0.63 0.01 0.03 0.06 76.7x 18.2x 10.1x 1.0x 0.9x 0.9x

Average 0.49 0.67 0.89 140.5x 39.0x 14.4x 8.2x 6.1x 4.1x

EPS (local ccy) P/E (x) P/B(x)

Source: Company data, Credit Suisse estimates (priced as of 20 October 2015)

21 October 2015

China Media and Entertainment Sector 5

Fast development of online ticketing sector In 2010, the first online seating selection website, Gewara.com, was launched. Fuelled by

both the boom in China's movie box office revenue and the rise in O2O, the online

ticketing services sector has expanded exponentially in the past five years, recording

Rmb13.5 bn revenue in 1H15, compared with Rmb13.6 bn in the full-year 2014 and

Rmb4.9 bn in 2013. In 1H15, online ticketing overtook offline ticket sales as the No.1

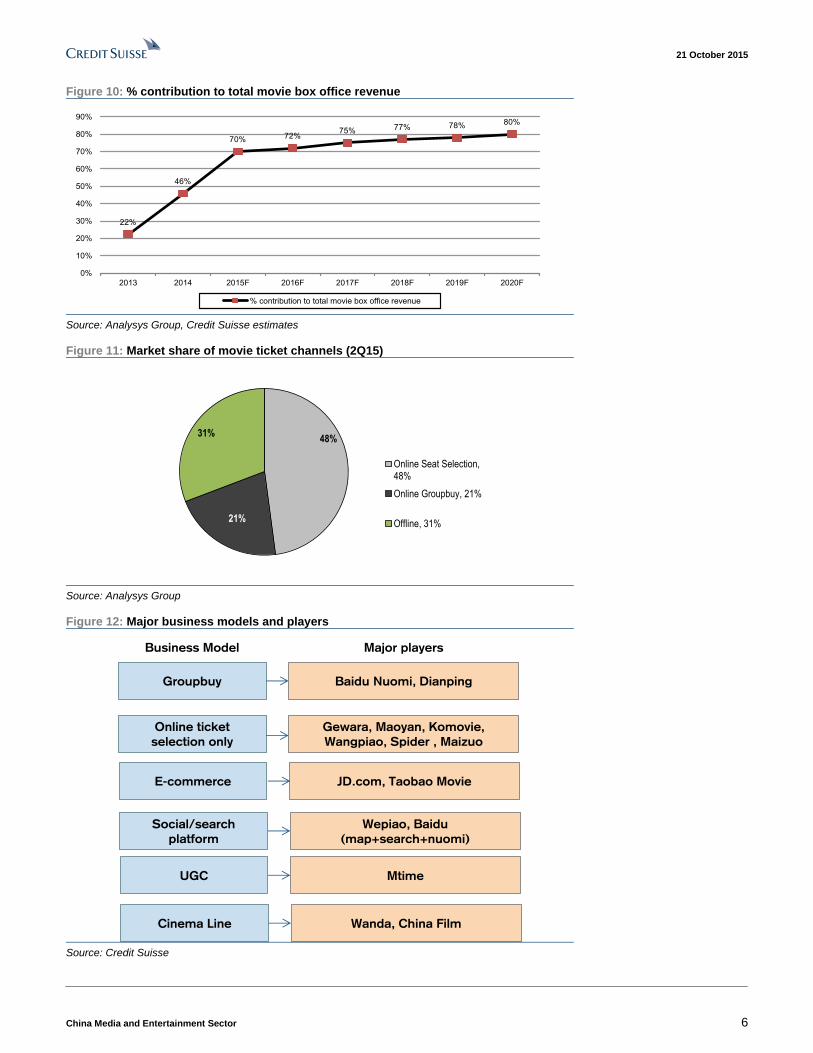

channel, with 66.5% of total box office. Its contribution was only 22.3% and 45.8% in 2013

and 2014, respectively. We estimate online ticketing to continue to grow, reaching

Rmb84.3 bn in 2020, and accounting for 80% of the domestic movie box office.

At the same time, growth in the online ticketing sector also stimulates the expansion in

China's movie box office by the following means:

1) Providing convenience to customers in the ticket purchasing process

2) Providing subsidy to ticket prices in order to attract price-sensitive customers

3) Enabling seat selection in advance, which helps both the customer and the

cinemas to lock in the service beforehand

4) Cultivating the movie watching habit, especially among internet users and the

young generation

Online ticketing is of two types:

1) Online ticket selection: customers select the specific movie cinema, movie, time

slot and seats online when they book the ticket. Every ticket is individually priced.

2) Groupbuy: customers buy a coupon for a cinema, but the movie and the time slot

are not specified. Customers will go to the cinema to redeem the coupon. The

availability of the movie and the seating is not guaranteed in advance.

Figure 9: Growth trend of online ticketing market

4.9

13.6

29.0

38.0

48.7

60.0

71.5

84.3179%

114%

31% 28%23% 19% 18%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2013 2014 2015F 2016F 2017F 2018F 2019F 2020F

Rmb Bn

Online ticketing revenue y-y

Source: Analysys Group, Credit Suisse estimates

Online ticketing overtook

offline ticket sales as the

No.1 channel, with 66.5% of

total box office in 1H15

21 October 2015

China Media and Entertainment Sector 6

Figure 10: % contribution to total movie box office revenue

22%

46%

70% 72%75% 77% 78% 80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2013 2014 2015F 2016F 2017F 2018F 2019F 2020F

% contribution to total movie box office revenue

Source: Analysys Group, Credit Suisse estimates

Figure 11: Market share of movie ticket channels (2Q15)

48%

21%

31%

Online Seat Selection,48%

Online Groupbuy, 21%

Offline, 31%

Source: Analysys Group

Figure 12: Major business models and players

Groupbuy

Online ticket

selection only

E-commerce

Social/search

platform

UGC

Cinema Line

Baidu Nuomi, Dianping

Gewara, Maoyan, Komovie,

Wangpiao, Spider , Maizuo

JD.com, Taobao Movie

Wepiao, Baidu

(map+search+nuomi)

Mtime

Wanda, China Film

Business Model Major players

Source: Credit Suisse

21 October 2015

China Media and Entertainment Sector 7

Figure 13: Front page of Baidu Nuomi movie section

Groupbuy Online seat selection

Source: Company website

Figure 14: Baidu Nuomi mobile app's online selection

page—applies to specific movie and time slot

Figure 15: Baidu Nuomi mobile app's Groupbuy page—

applies to a specific cinema

Online seat selection

Groupbuy

Source: Baidu Nuomi Application Source: Baidu Nuomi Application

21 October 2015

China Media and Entertainment Sector 8

Fierce competition in online ticketing As the market expands rapidly, many new players will enter the online movie ticket seating

selection space, including vertically focused movie sales websites (such as Gewara,

Mtime, and Maizuo), e-commerce and O2O websites (such as Maoyan and Taobao),

social media websites (such as Wechat), and cinema line self-developed websites (such

as Wanda, China Film and Jinyi). The industry is still in the early stage and largely

fragmented; by 2Q15, there are ~40 online movie ticketing websites in China, but less

than 10 of them have total revenue > Rmb300 mn. In the past year, the three biggest

internet players—Baidu, Alibaba and Tencent—have also entered the space. We are

expecting more industry consolidation in the next five years, and three to five major

players as the industry matures.

In order to gain a bigger market share, these movie ticket websites compete by providing

large amounts of subsidies to customers with low ticket prices—at a loss. Typically, movie

ticket websites, as a sales channel, agree on a fixed distribution price that they will pay to

movie cinema lines (~Rmb30-35, depending on the bargaining power of the production

studio, cinema line and movie ticket website). Any amount they charge above or below the

fixed price would be at their own profit or loss. In order to attract customers, many

websites offer ticket prices as low as Rmb1, Rmb9.9 or Rmb19.9. For the same ticket, if

customers purchase on-site at the cinema, it would cost them over Rmb40-100.

Figure 16: Market share of major online movie ticket selection websites (2Q15)

36%

21%

8%

6%

6%

5%

2%

Maoyan (猫眼), 36%

Gewara (格瓦拉), 22%

Wepiao (微票儿), 8%

Taobao (淘宝电影), 6%

Mtime (时光网), 6%

Wanda (万达电影), 5%

Maizuo (卖座网), 2%

Others (including Baidu Nuomi

百度糯米), 16%

Source: Analysys Group

The industry is very

fragmented at the moment;

we believe there will be

consolidation in the next 5

years, and 3-5 major players

as the market matures

Online ticketing platforms

are in fierce competition with

ticket price subsidies

21 October 2015

China Media and Entertainment Sector 9

Competition among BAT (Baidu, Alibaba and

Tencent) and other media giants

The three biggest internet players in China—Baidu, Alibaba, and Tencent, also known as

"BAT"—along with other media giants, such as Wanda Cinema Line, Oriental Pearl and

Huayi Brothers, have all entered the online ticketing sector. We believe the capital support

from these investors will continue to fund the movie ticket subsidy until the market

saturates with three to five dominant players. The involvement of these internet and media

companies will also help online ticketing players to expand along the industry value chain.

1) Maoyan (猫眼): Market share – 36%; cinemas covered – 4,000; cities

covered – 400

Maoyan.com, the biggest online ticketing seat selection website/application, is a

subsidiary of Meituan. Meituan, known as "China's Groupon," is the largest e-

commerce O2O services website offering local deals, and it is backed by Alibaba.

On 8 October 2015, Meituan announced it will be merged with Dianping, "China's

Yelp," which is invested in by Tencent with a 22% stake. As a result, Maoyan

could have support from both Alibaba and Tencent going forward. We expect this

support to include not only capital injection, which will support the continuous

movie ticket subsidy and marketing activities, but also traffic and other resources.

2) Gewara (格瓦拉): Market share – 22%; cinemas covered – 2,000; cities

covered – 300

Gewara.com, the second largest player and the first launched online seating

selection website, has received investment from China Media Capital (CMC),

which is backed by Oriental Pearl Media.

CMC is a private equity mainly focused on media and internet sectors, with

investments in a large number of quality assets in upstream content providers, such

as Time Warner, Oriental Dreamworks, Starry Production, TVB, China Sports Media

and Infront. Oriental Pearl is the largest multi-channel video programming distributor

in China; its parent company is Shanghai Media Group. Oriental Pearl and CMC

have also co-invested in several deals together with Wanda Group, which owns the

largest cinema line in China. CMC and Oriental Pearl will provide both upstream and

downstream resources and connection to Gewara.

3) Baidu Nuomi (百度糯米): Cinemas covered – 4,500; cities covered – 418

Baidu's O2O arm, Nuomi, has made movie ticketing one of its key businesses for

expansion this year. With traffic, technology and investment support from Baidu,

Nuomi's revenue and volume has increased significantly. Nuomi offers both online

seat selection and Groupbuy tickets.

During its promotional event "3/7 Girls Festival" this year, Baidu Nuomi sold over

a million tickets with a promotion price of Rmb3.7; this was six times the tickets

sold on the same day last year and accounted for 15% of total box office in China

on the date. 70% of those transactions were completed with Baidu Wallet. On

"7/7" (China's Valentine's Day) this year, Nuomi sold 1.7 mn tickets, accounting

for 25% of total tickets sold (6.8 mn) nationally on that day.

In April 2015, Baidu issued membership cards together with SMI, Dadi, China

Film, Poly, Bona, CGV, 17.5, Hengdian and other several cinema chains. All of

the 100k cards issued on 1 May were sold out on the same day. The movie

watching frequency of membership cardholders, 12 times per year, is significantly

higher than the average frequency of the Chinese audience, which is 4.8 times

per year.

BAT, and media giants,

such as Wanda and Oriental

Pearl, have all entered the

online ticketing sector

21 October 2015

China Media and Entertainment Sector 10

On 13 June 2015, Baidu established a strategic relationship with SMI Holdings,

the sixth largest cinema line in China. Meanwhile, SMI has also announced it will

stop selling tickets on Maoyan, the largest online ticketing website.

At the end of June, Baidu announced it will invest Rmb20 bn in O2O (Nuomi) over

the next three years. We estimate around 20% (Rmb3.8 bn) of that will be

invested in the movie category.

Baidu Nuomi has also organised other online and offline activities for its members

to boost movie ticket sales. For example, on 21 September 2015, Baidu Nuomi,

together with the "Lost in Hong Kong" movie production team, organised a special

early showing of the movie and received great success.

We believe Nuomi's market share will become one of the top 5 in the category

very shortly. Baidu Nuomi's movie ticket market share has not been separately

published by Analysys Group yet, as Baidu is one of the latecomers in the space.

4) Wepiao (微票儿): Market share – 8%; cinemas covered – 4,100; cities

covered – 420

Weipiao is the third largest player with 8% market share and it is a subsidiary of

Tencent. It is the official application of Wechat and QQ movie. As a result, it receives

all the traffic from Wechat and goes through Wechat Wallet's payment system.

5) Taobao Dianying (淘宝电影): Market share – 6%; cinemas covered –

2,500; cities covered – 244

It is the movie channel of Alibaba's e-commerce website Taobao, which is the

largest C to C (Customer to Customer) website in China.

6) Mtime (时光网): Market share – 6%

Mtime is the largest all-rounded movie content and service platform in China. It

has been invested in by Wanda Cinema Line with a 20% stake.

Compared to other online movie ticket sales websites, Mtime is "effectively

Fandango, IMDb, Rotten Tomatoes and Yahoo Movies rolled into one," as

described by The New York Times. Mtime has ~80 mn monthly active users,

including ~65 mn mobile users.

7) Wanda (万达电影): Market share – 5%

It is Wanda Cinema Line's official online ticket sales website. Wanda Cinema Line

has been the largest cinema line in China for six consecutive years with 14%

market share. In 2014, over 60% of Wanda's box office revenue came through the

online ticketing channels and 30% of that came from its own website/mobile

application. Wanda also has the largest membership system in China with 40 mn

members by end-1H15.

We expect the market share of Wanda's own website/application to continue to

see the rapid growth as its box office and membership grows. The Wanda brand

is creating stronger and stronger customer stickiness.

8) Maizuo (卖座网): Market share – 2%

Maizuo is invested in by Huayi Brothers, with the controlling stake (51%) in June

2014. Huayi is the largest movie production company in China.

21 October 2015

China Media and Entertainment Sector 11

Figure 17: Investment of major internet and media players in online ticketing

Meituan

Dianping

China Media

Capital

Tencent

Alibaba

Wanda Cinema

Line

Wanda Cinema

Line

Huayi Brothers

Tencent

Alibaba

Baidu

Oriental Pearl

36%

21%

8%

6%

6%

5%

2%

Maoyan (猫眼), 36%

Gewara (格瓦拉), 22%

Wepiao (微票儿), 8%

Taobao (淘宝电影), 6%

Mtime (时光网), 6%

Wanda (万达电影), 5%

Maizuo (卖座网), 2%

Others (including Baidu

Nuomi 百度糯米), 16%

Source: Analysys Group, Credit Suisse

How do customers choose ticket platforms?

Consumers normally choose ticket platforms based on four factors, in our view.

1) Availability: The availability of a customer's desired movie and cinema is the first

priority, therefore, the coverage of a ticketing platform is very important, especially

in Tier 3 and 4 cities.

2) Price: Chinese consumers are quite price-sensitive compared to consumers in

mature markets; therefore, we always see huge impact of pricing subsidies,

especially for non-frequent movie watchers.

3) Convenience: the convenience for a customer to finish the transaction is the last

mile to ensure the purchase. The transaction includes two parts—online payment

and offline ticket pick-up. Some of the players, such as Maoyan, have installed

offline ticketing machines in movie cinemas; hence, customers can print tickets

using these machines instead of waiting in lines.

4) Other value-added services, such as offline events (special showing, celebrity

meetings) and movie ratings.

There are six major types of online ticketing platforms as summarised below.

Customers choose ticketing

platforms based on

availability, price,

convenience, and other

value-add services provided

21 October 2015

China Media and Entertainment Sector 12

Figure 18: Summary of online ticketing business models

Business Model Major players Pros and Cons

Groupbuy Baidu Nuomi,

Dianping

These platforms typically offer both Groupbuy and online seat selection; for Groupbuy,

customers can buy tickets in advance without confirming the movie and show time.

With mature O2O and Groupbuy business model, these platforms have established

customer base and offline sales resources; other services offered on their websites can also

bring in movie tickets traffic.

Online ticket

selection only

Gewara, Maoyan,

Komovie, Wangpiao,

Spider, Maizuo

As specialised platforms, these companies are good at online and offline marketing and

promotional events' organisation.

Within the movie watcher community, they enjoy a high level of customer stickiness.

E-commerce Taobao Movie,

JD.com

Movie ticket is one category on these e-commerce platforms, therefore, they get the traffic

from the e-commerce website itself.

Many customers have downloaded their mobile application and registered as users

previously for their e-commerce services.

These platforms also have mature and trustworthy payment systems in place.

However, they might not have as much resources and experience for movie ticket subsidy

and offline collaboration.

Social and search

platform

Wepiao,

Baidu

(Search+Map+Nuomi)

Wepiao gets traffic from two of the largest social applications in China—Wechat and QQ—

both owned by Tencent. Users do not need to download an additional application and can

use Wechat Wallet for payment, which adds to the convenience level.

Baidu Nuomi receives traffic from Baidu map and search, two of the dominant applications in

China in the map and search sectors. In 1Q15, 25% of Nuomi movie ticket transactions

originated from and were completed on Mobile Baidu and maps.

UGC (user

generated

content)

Mtime, Douban Mtime is the largest all-rounded movie content and service platform in China, integrating

movie ticket sales with movie ratings and audience comments.

Users of these websites have a high level of loyalty, stickiness and consumption frequency.

The recommendations on these websites further stimulate users' movie watching behaviour.

Cinema line Wanda Cinema-line-owned ticketing platforms usually only offer tickets of their own cinemas and

provide convenience to members.

However, only the big cinema lines, such as Wanda, have the ability to do so given the

limited number of cinemas such websites can offer.

Source: Credit Suisse

21 October 2015

China Media and Entertainment Sector 13

Near-term, subsidies remain high According to our estimates, the subsidy from e-commerce and movie studios totalled

around Rmb4 bn in 2014; this accounted for 13.5% of the total movie box office in China.

The subsidy from e-commerce platforms alone was around Rmb2 bn, which accounted for

14.7% of the online box office in China.

We estimate the total subsidy to be Rmb8.4 bn, Rmb8.3 bn, and Rmb6.7 bn in 2015, 2016

and 2017, respectively. The total subsidy level will peak in 2015 at 20%, and slow down

going forward. E-commerce subsidy is estimated to be Rmb4.6 bn, Rmb4.6 bn and

Rmb3.4 bn in 2015, 2016 and 2017, with subsidy levels of 16%, 12% and 7% as a

percentage of online box office, respectively.

Subsidy is split between movie production company and O2O platform

Currently, the split is 50-50 between the movie production company (as marketing

expense) and the online ticketing platform. However, for big production movies or well-

known movie studios, the split may be 1:2 or 1:3 depending on their bargaining power.

Some movie studios, which are very confident about their production or have budget

constraints, may even refuse to contribute to the movie subsidy.

The subsidy is usually provided during the first 3 days of a movie's released in order to

boost the popularity of a movie; the box office in this period also significantly impacts the

scheduling in the following days.

For example, "Lost in Hong Kong" (港囧 ), a movie produced by Enlight Media and

released on 25 September 2015, has recorded Rmb1.6 bn in box office so far, out of

which at least Rmb0.1 bn is from the e-commerce subsidy (6% of total box office). The

lowest price for "Lost in Hong Kong" was Rmb9.9 on Maoyan, Rmb9.0 on Wepiao and

Rmb6.6 on Baidu Nuomi, which is at 72%, 74% and 81% discount, respectively, to the

movie's average ticket price of Rmb35.

Figure 19: Production company and e-commerce subsidy trend

2

3.7 3.7

3.2

2.3

1.4

0.5

2

4.6 4.6

3.4

2.4

1.4

0.5

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

-

1

1

2

2

3

3

4

4

5

5

2014 2015F 2016F 2017F 2018F 2019F 2020F

Rmb Bn

Production company subsidy e-commerce subsidy

Production company (as % of total box office) e-commerce (as % of online box office)

Source: Credit Suisse estimates

21 October 2015

China Media and Entertainment Sector 14

Figure 20: Subsidy as % of total box office (2014) Figure 21: E-commerce subsidy as % of e-commerce box

office (2014)

86%

14%

Non-subsidized BoxOffice, Rmb 26Bn

Total Subsidy, Rmb 4Bn

84%

16%

E-commerce BoxOffice, Rmb 11Bn

E-commerce Subsidy,Rmb 2Bn

Source: Credit Suisse Source: Credit Suisse

Subsidies from online ticket platform likely to stay in

the medium term

In our view, subsidies from online ticket platforms are likely to stay in the medium term due

to the following reasons:

1) Market is still fragmented,

2) BAT (Baidu, Alibaba, and Tencent) are focusing on the entertainment space, and

3) Movie is a good category to attract customers for other O2O categories. For example,

customers who purchase movie tickets on Baidu Nuomi will use Baidu Wallet; at the

same time, the user will create a user account and is more likely to use other O2O

services, such as restaurant Groupbuy, or other entertainment services.

What's the impact, if subsidy stops in the long term?

In the long term, when the market is consolidated with 3-5 dominant players, the subsidy

will decrease or stop eventually and the market will grow organically, in our view.

Impact to box office

We believe the impact to the total movie box office revenue in China will be small for the

following reasons:

1) With increasing disposable incomes, movie watching is now an affordable activity

instead of a luxury; customers are becoming less price-sensitive. Movie tickets in

China are still largely cheaper than other regions—the average ticket price in

China is Rmb35 vs Rmb60 in HK, Rmb50 in Singapore, Rmb56 in Taiwan and

Rmb50 in the US.

2) Movie watching has become a major offline entertainment for the younger

generation; frequent movie watchers who have formed the habit will not move

away from watching movies,

3) Some of the customers may move from online ticketing to offline retail, which

won't negatively impact the total box office,

4) The average ticket price will increase as a result.

We believe subsidy will

remain in the medium term

We think the impact to

China's movie box office will

be small if subsidy stops

21 October 2015

China Media and Entertainment Sector 15

Impact on online ticketing platform

We believe the impact on online ticketing platforms will also be marginal.

The online ticketing service not only provides price discounts, more importantly, it provides

convenience to customers by enabling them to purchase tickets and select seats in

advance. It also streamlines the payment process—customers do not have to wait in lines

at the cinema to buy tickets.

The online ticketing service has changed customers' behaviour and cultivated in them a

movie ticket purchasing habit. Once the habit is formed, it will become a new norm,

especially for the younger generation. According to Entgroup, the average age of the

movie-going audience in China is 21.5. In other words, the majority of the audience are

teens and young adults who use internet as an integral part of their life.

The merger between Kuaidi and Didi—two of the biggest car-hailing applications—is

another reference. Before the merger, the two companies were in an intensive battle for

market share by providing subsidies to users. Within two to three years, China taxi app

users exceeded to 150 mn (3Q14). The two companies have reduced subsidy after the

merger; however, users continue to use their application. Similar to online ticketing, taxi

apps also provide convenience and have changed people's lifestyle.

We think the impact to

China's online ticketing

platforms will also be

marginal

21 October 2015

China Media and Entertainment Sector 16

Potential market size for online movie ticketing Service charge opportunities

In mature markets, instead of offering discounts on movie tickets, online ticketing platforms

usually charge a service fee (5-10% of ticket price) on top of the ticket for the seat

selection service they provide:

1. Hong Kong: HK$8 (AMC and the Sky official ticket website)

2. The US: US$2.7 (tickets.fandango.com)

3. The UK: £0.6 (movietickets.com) or £0.75 (booking.myvue.com)

We think this will be the trend in the long term: service charge will be the major revenue

driver for online ticketing platforms. However, in the short term (next 2-3 years), given the

market is still in the development stage, the industry is segmented and Chinese

consumers are highly price sensitive, online ticketing platforms will not charge a service

fee, in our view. With the capital support from their investors—major internet, media

companies and venture capitals—online ticketing platforms will continue the battle with

heavy subsidies.

Figure 22: Potential market size of online ticketing service fee (assuming 5% take rate)

1.5

1.9

2.4

3.0

3.6

4.2

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2013 2014 2015F 2016F 2017F 2018F

Rmb Bn

Potential Market Size of Online Ticketing Service fee (Rmb Bn) (Assuming 5% take rate)

Source: Credit Suisse estimates

Key policy update

On 8 July 2015, China Film Distribution and Exhibition Association and China Film

Producers' Association together issued the "Regulation on Movie Ticket Sales and

Marketing" ("Regulation"). According to the Regulation, e-commerce companies have a

legal agency relationship (instead of a resale relationship) with cinema lines and charge

agency distribution fees. E-commerce companies can conduct sales and marketing

activities. Most importantly, the Regulation specified the following pricing policy:

Movie retail price, price mentioned in promotions (e.g., the original price marketed, but not

the discounted price) and transaction clearing price with cinema lines cannot be lower than

the minimum price specified in the distribution agreement.

■ If the discounted ticket price is lower than the distribution price, e-commerce

companies will provide the subsidy and pay the distribution price to cinema lines;

We think service charge will

be a new revenue stream

for online ticketing platforms

in China in the future

According to the new policy,

e-commerce companies

have legal agency

relationship with cinema

lines and charge agency

distribution fees; in the case

of subsidies, they still have

to pay the agreed minimum

ticket price to cinema lines

21 October 2015

China Media and Entertainment Sector 17

■ If the ticket price is higher than the distribution price, the actual price, excluding

service fee, will be used for transaction clearing with cinema lines.

In other words, any discount below the distribution price will be at the cost of the e-

commerce companies and will not negatively impact cinema lines and cinema chains

directly. However, there is indirect effect to retail tickets, given more customers use the

online channel to purchase tickets at a discount.

21 October 2015

China Media and Entertainment Sector 18

Companies Mentioned (Price as of 20-Oct-2015)

500.Com (WBAI.N, $20.2) 58.com Inc. (WUBA.N, $51.06) Alibaba Group Holding Limited (BABA.N, $72.65) Alpha Animation (002292.SZ, Rmb31.9) Autohome Inc. (ATHM.N, $35.17) BGCTV (600037.SS, Rmb25.63) Baidu Inc (BIDU.OQ, $154.68) Beijing Enlight Media Co. Ltd (300251.SZ, Rmb27.94) Bitauto Holdings Limited (BITA.N, $32.6) CCYS (002071.SZ, Rmb15.75) Dr. Peng (600804.SS, Rmb25.76) E-House China Holdings Ltd (EJ.N, $6.63) Everyday Network (300295.SZ, Rmb97.5) HLBN (300291.SZ, Rmb28.51) Huayi Brothers Media Corp (300027.SZ, Rmb39.58) JiShi Media (601929.SS, Rmb6.32) Jiayuan (DATE.OQ, $6.53) Leju Holdings Limited (LEJU.N, $6.59) Leshi (300104.SZ, Rmb53.14) Mitsui Engineering & Shipbuilding (7003.T, ¥197) Nan Hai Corporation Limited (0680.HK, HK$0.16) Orange Sky Golden Harvest Entertainment (Holdings) (1132.HK, HK$0.64, OUTPERFORM[V], TP HK$1.1) PWPIC (002624.SZ, Rmb21.03) SMI Holdings (0198.HK, HK$0.72) SXBN (600831.SS, Rmb14.78) Shanghai New Culture Media Group Co. Ltd (300336.SZ, Rmb31.52) Shanghai Oriental Pearl Media Co Ltd (600637.SS, Rmb36.31) SouFun (SFUN.N, $7.27) TIK (000917.SZ, Rmb42.89) Talent (300426.SZ, Rmb153.99) Topway (002238.SZ, Rmb23.76) Wanda Cinema Line Co Ltd (002739.SZ, Rmb104.33) Wasu (000156.SZ, Rmb33.0) Zhaopin Limited (ZPIN.N, $14.09) Zhejiang Huace Film & TV Co Ltd (300133.SZ, Rmb27.43)

Disclosure Appendix

Important Global Disclosures

I, David Hao, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Orange Sky Golden Harvest Entertainment (Holdings) (1132.HK)

1132.HK Closing Price Target Price

Date (HK$) (HK$) Rating

24-Sep-15 0.72 1.10 O *

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10 th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractiv e, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ra tings are based on a stock’s total

21 October 2015

China Media and Entertainment Sector 19

return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin Ame rican and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 1 2-month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, wh ich was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cov er multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 59% (34% banking clients)

Neutral/Hold* 26% (35% banking clients)

Underperform/Sell* 13% (23% banking clients)

Restricted 2%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdin gs, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Price Target: (12 months) for Orange Sky Golden Harvest Entertainment (Holdings) (1132.HK)

Method: We assign Orange Sky Golden Harvest Entertainment (Holdings) a DCF (discounted cash flow)-based target price of HKD1.10, based on 8.3% WACC (weighted average cost of capital) and 2.5% terminal growth; the valuation also implies 32x/18x FY16/17E P/E (price-to-earnings).

Risk: Risks that could impede achivement of our HK$1.10 target price for Orange Sky Golden Harvest Entertainment (Holdings) include: 1) consumption change shifting away from watching movies on silver screen; 2) oversupply in theatres and screens; 3) bad theatre investments.

Please refer to the firm's disclosure website at https://rave.credit-suisse.com/disclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names

The subject company (0680.HK, 002739.SZ, BABA.N, WUBA.N, BIDU.OQ, ZPIN.N, ATHM.N, BITA.N, SFUN.N, EJ.N) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (002739.SZ, BABA.N, WUBA.N, BIDU.OQ, ZPIN.N, ATHM.N, BITA.N, SFUN.N, EJ.N) within the past 12 months.

21 October 2015

China Media and Entertainment Sector 20

Credit Suisse has managed or co-managed a public offering of securities for the subject company (002739.SZ, BABA.N, WUBA.N) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (002739.SZ, BABA.N, WUBA.N, BIDU.OQ, ZPIN.N, ATHM.N, BITA.N, SFUN.N, EJ.N) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (300027.SZ, 0680.HK, 002739.SZ, 7003.T, BABA.N, WUBA.N, BIDU.OQ, ZPIN.N, ATHM.N, BITA.N, SFUN.N, EJ.N) within the next 3 months.

Credit Suisse has a material conflict of interest with the subject company (BABA.N) . Credit Suisse acted as the exclusive financial advisor to Alibaba Group in relation to its investment in Snapdeal.com.

Credit Suisse has a material conflict of interest with the subject company (BITA.N) . Credit Suisse is acting as financial advisor to Bitauto Holdings Ltd in relation to the investments by JD.com, Inc and Tencent Holdings Ltd in Bitauto.

Credit Suisse has a material conflict of interest with the subject company (EJ.N) . Credit Suisse is an exclusive financial advisor to the Special Committee of Independent Directors of China Real Estate Information Corporation's board of directors relating to the proposed going private transaction by E-House (China) Holdings Limited

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report may participate in events hosted by the subject company, including site visits. Credit Suisse does not accept or permit analysts to accept payment or reimbursement for travel expenses associated with these events.

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html.

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (002739.SZ, BABA.N, WUBA.N, ZPIN.N, BITA.N, SFUN.N, EJ.N, LEJU.N) within the past 3 years.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Credit Suisse (Hong Kong) Limited ..................................................................................................................... David Hao ; Dick Wei ; Evan Zhou

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

21 October 2015

China Media and Entertainment Sector 21

References in this report to Credit Suisse include all of the subsidiaries and affiliates of Credit Suisse operating under its investment banking division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who-we-are This report may contain material that is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse AG or its affiliates ("CS") to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates. The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in this report. Those communications reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other communications are brought to the attention of any recipient of this report. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgment at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR's, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS's own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS's website shall be at your own risk. This report is issued and distributed in Europe (except Switzerland) by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. This report is issued and distributed in Europe (except Switzerland) by Credit Suisse International, One Cabot Square, London E14 4QJ, England, which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. This report is being distributed in Germany by Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). This report is being distributed in the United States and Canada by Credit Suisse Securities (USA) LLC; in Switzerland by Credit Suisse AG; in Brazil by Banco de Investimentos Credit Suisse (Brasil) S.A or its affiliates; in Mexico by Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); in Japan by Credit Suisse Securities (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau (Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Investment Advisers Association, Type II Financial Instruments Firms Association; elsewhere in Asia/ Pacific by whichever of the following is the appropriately authorised entity in the relevant jurisdiction: Credit Suisse (Hong Kong) Limited, Credit Suisse Equities (Australia) Limited, Credit Suisse Securities (Thailand) Limited, regulated by the Office of the Securities and Exchange Commission, Thailand, having registered address at 990 Abdulrahim Place, 27th Floor, Unit 2701, Rama IV Road, Silom, Bangrak, Bangkok 10500, Thailand, Tel. +66 2614 6000, Credit Suisse Securities (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch, Credit Suisse Securities (India) Private Limited (CIN no. U67120MH1996PTC104392) regulated by the Securities and Exchange Board of India as Research Analyst (registration no. INH 000001030) and as Stock Broker (registration no. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th Floor, Ceejay House, Dr.A.B. Road, Worli, Mumbai - 18, India, T- +91-22 6777 3777, Credit Suisse Securities (Europe) Limited, Seoul Branch, Credit Suisse AG, Taipei Securities Branch, PT Credit Suisse Securities Indonesia, Credit Suisse Securities (Philippines ) Inc., and elsewhere in the world by the relevant authorised affiliate of the above. Research on Taiwanese securities produced by Credit Suisse AG, Taipei Securities Branch has been prepared by a registered Senior Business Person. Research provided to residents of Malaysia is authorised by the Head of Research for Credit Suisse Securities (Malaysia) Sdn Bhd, to whom they should direct any queries on +603 2723 2020. This report has been prepared and issued for distribution in Singapore to institutional investors, accredited investors and expert investors (each as defined under the Financial Advisers Regulations) only, and is also distributed by Credit Suisse AG, Singapore branch to overseas investors (as defined under the Financial Advisers Regulations). By virtue of your status as an institutional investor, accredited investor, expert investor or overseas investor, Credit Suisse AG, Singapore branch is exempted from complying with certain compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the "FAA"), the Financial Advisers Regulations and the relevant Notices and Guidelines issued thereunder, in respect of any financial advisory service which Credit Suisse AG, Singapore branch may provide to you. This information is being distributed by Credit Suisse AG, Dubai Branch, duly licensed and regulated by the Dubai Financial Services Authority (DFSA), and is directed at Professional Clients or Market Counterparties only, as defined by the DFSA. The financial products or financial services to which the information relates will only be made available to a client who meets the regulatory criteria to be a Professional Client or Market Counterparty only, as defined by the DFSA, and is not intended for any other person. This research may not conform to Canadian disclosure requirements. In jurisdictions where CS is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements. Non-U.S. customers wishing to effect a transaction should contact a CS entity in their local jurisdiction unless governing law permits otherwise. U.S. customers wishing to effect a transaction should do so only by contacting a representative at Credit Suisse Securities (USA) LLC in the U.S. Please note that this research was originally prepared and issued by CS for distribution to their market professional and institutional investor customers. Recipients who are not market professional or institutional investor customers of CS should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK or to other matters which are not authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority or in respect of which the protections of the Prudential Regulation Authority and Financial Conduct Authority for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available upon request in respect of this report. CS may provide various services to US municipal entities or obligated persons ("municipalities"), including suggesting individual transactions or trades and entering into such transactions. Any services CS provides to municipalities are not viewed as "advice" within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. CS is providing any such services and related information solely on an arm's length basis and not as an advisor or fiduciary to the municipality. In connection with the provision of the any such services, there is no agreement, direct or indirect, between any municipality (including the officials, management, employees or agents thereof) and CS for CS to provide advice to the municipality. Municipalities should consult with their financial, accounting and legal advisors regarding any such services provided by CS. In addition, CS is not acting for direct or indirect compensation to solicit the municipality on behalf of an unaffiliated broker, dealer, municipal securities dealer, municipal advisor, or investment adviser for the purpose of obtaining or retaining an engagement by the municipality for or in connection with Municipal Financial Products, the issuance of municipal securities, or of an investment adviser to provide investment advisory services to or on behalf of the municipality. If this report is being distributed by a financial institution other than Credit Suisse AG, or its affiliates, that financial institution is solely responsible for distribution. Clients of that institution should contact that institution to effect a transaction in the securities mentioned in this report or require further information. This report does not constitute investment advice by Credit Suisse to the clients of the distributing financial institution, and neither Credit Suisse AG, its affiliates, and their respective officers, directors and employees accept any liability whatsoever for any direct or consequential loss arising from their use of this report or its content. Principal is not guaranteed. Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

Copyright © 2015 CREDIT SUISSE AG and/or its affiliates. All rights reserved.

Investment principal on bonds can be eroded depending on sale price or market price. In addition, there are bonds on which investment principal can be eroded due to changes in redemption amounts. Care is required when investing in such instruments. When you purchase non-listed Japanese fixed income securities (Japanese government bonds, Japanese municipal bonds, Japanese government guaranteed bonds, Japanese corporate bonds) from CS as a seller, you will be requested to pay the purchase price only.

MD0212