industry trends from the trenches - govcon360 | 360...

TRANSCRIPT

Industry Trends From The Trenches

Presented By: Christine Williamson, CPA, Member In Charge

Kristen Soles, CPA, Member

Agenda

• DCAA / DCMA Trends / Power & Balance Shifts • DCAA / DCMA Focus • Preparing for What Lies Ahead • Business Systems Trends

– DCAA “new” opinions – Audit Approach & Workprograms

• General Trends

Proprietary and Confidential 2

The Stage (Frustration)

• Agencies frustrated by their: – Inability to close out contracts – Inability to award new contracts – Budget uncertainties

• GAO findings re DCMA • The DCAA frustrated by continuous scrutiny and

frequent Senate Hearings with their buddies Brown & McCaskill

• Government contractors frustrated by all of the above and then some

Proprietary and Confidential 3

The Backlog of (RFP) Proposal Review Audits

• In FY 2010, DCAA issued reports in response to only 11,788 assignments while cancelling 16,298 assignments with no report issued (proposal review audits).

• Average time to conduct proposal review audits in 2009 – 28 days, in 2010 – 74 days.

Proprietary and Confidential 4

So What’s The Plan?

• A shift in power, the DCMA taking more into their own hands

• A shift in proposal audit dollar value focus, essentially dramatically reducing backlog with the stroke of a pen for DCAA

• Hiring hiring and more hiring • Movement away from sole audit reliance on the

DCAA

Proprietary and Confidential 5

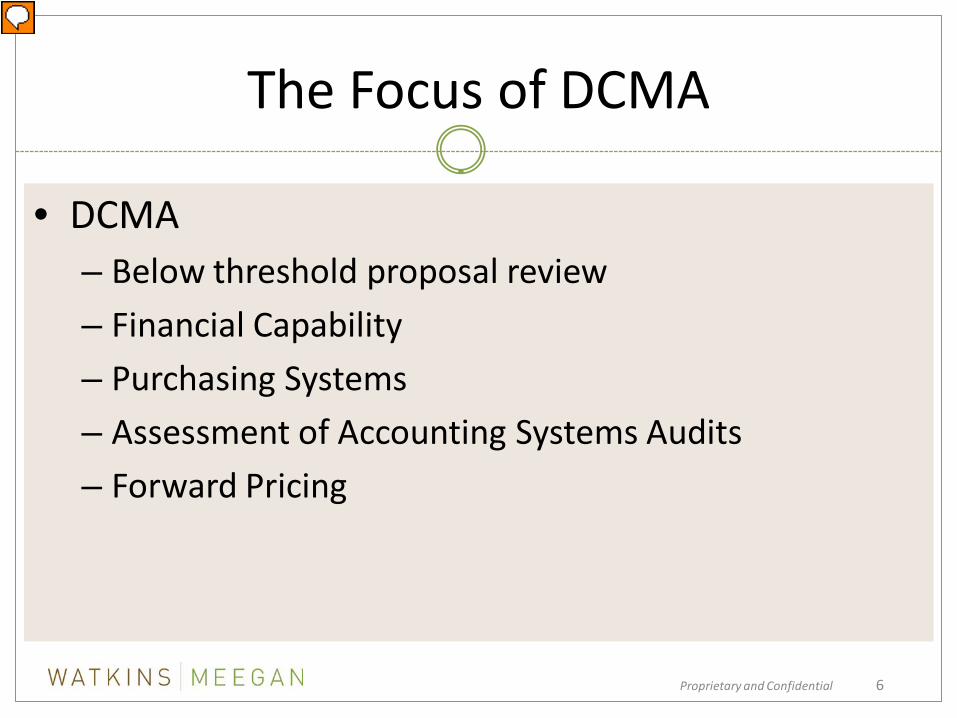

The Focus of DCMA

• DCMA – Below threshold proposal review – Financial Capability – Purchasing Systems – Assessment of Accounting Systems Audits – Forward Pricing

Proprietary and Confidential 6

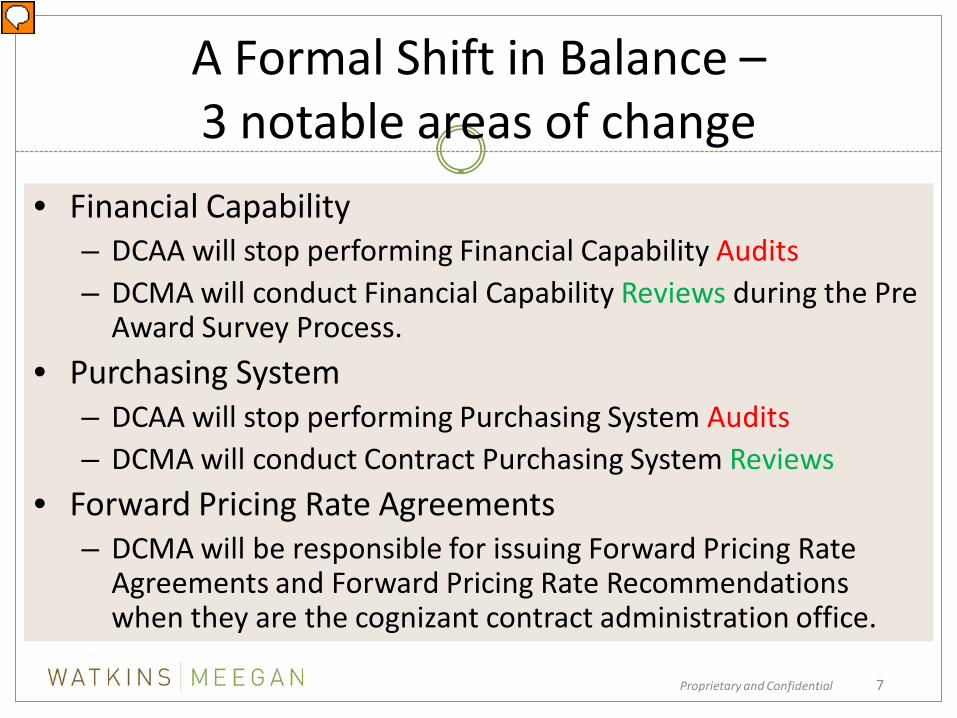

A Formal Shift in Balance – 3 notable areas of change

• Financial Capability – DCAA will stop performing Financial Capability Audits – DCMA will conduct Financial Capability Reviews during the Pre

Award Survey Process. • Purchasing System

– DCAA will stop performing Purchasing System Audits – DCMA will conduct Contract Purchasing System Reviews

• Forward Pricing Rate Agreements – DCMA will be responsible for issuing Forward Pricing Rate

Agreements and Forward Pricing Rate Recommendations when they are the cognizant contract administration office.

Proprietary and Confidential 7

The Pen Stroke Reduction

• DCMA responsible for: – field price reviews on cost type proposals less than

$100M and; – fixed type proposals under $10M will be sent to

DCMA [for review by DCMA pricing specialists]. (DCAA will be responsible for audits of proposals above

these thresholds)

Proprietary and Confidential 8

DCAA / DCMA Projected Hires

Proprietary and Confidential 9

PROJECTED DCAA Hires 2012 – 262 2013 – 434

DCMA Hires 2012 – 796

2013 – 1,178

An Informal Shift in Power/Balance

• Agency use of third party independent CPA firms in order to speed up procurement

• Contractor voluntarily using third party independent CPA firms in order to get a seat at the table

• Prime’s requiring sub’s to get their third party CPA firm to review their accounting system (subcontracting requirements)

Proprietary and Confidential 10

GAO Report

Proprietary and Confidential 11

DOE Response

• DOE Director of Management Ingrid Kolb said: “DCAA’s growing timeliness problems have led to

problems with contract close-outs. The problems are so bad, she said, that DOE is turning to private firms to do the audits instead, even

though private firms cost significantly more on an hourly basis than DCAA auditors.”

Proprietary and Confidential 12

DOE Audits

• Response (FAQ) from the DOE re: the new 316 audit requirements…

“The DCAA would never agree to perform A-133 or our 316 audits… DCAA has scaled back what

they did for us and we have put in place a contract for a commercial firm to take over

indirect rate, incurred costs, accounting system audits etc… DCAA is really simply just another

audit firm.”

Proprietary and Confidential 13

Example Question in an RFP Verification of Adequate Accounting System

• Because of the need for contractors to respond to Cost Reimbursement task orders, to be eligible for award, offerors must have verification from the Defense Contract Audit Agency (DCAA), the Defense Contract Management Agency (DCMA), any federal civilian audit agency, or a third-party accounting firm of an accounting system that has been audited and determined adequate for determining costs applicable to this contract in accordance with FAR 16.301-3(a)(1).

• As such, the offeror must provide in its proposal, a contact name and contact information (i.e., phone number, address, email address) of its representative at its cognizant DCAA, DCMA, federal civilian audit agency, or third-party accounting firm and submit, a copy of the Pre-Award Survey of Prospective Contracting Accounting System (SF 1408), provisional billing rates, and/or forward pricing rate agreements.

Proprietary and Confidential 14

The Focus of DCAA

• DCAA – Focus on clearing up the backlog of incurred cost

submissions / contract closeout (huge) – Accounting System Audits – Larger proposal reviews

• > $100M CPFF • > $10M FFP

Proprietary and Confidential 15

DCAA Incurred Cost Audits

Proprietary and Confidential 16

MR. FITZGERALD: “Well, Senator Brown, to be very upfront with you, our cost-incurred audits, which are the audits that we do at the end of the contract and many times they're needed to do to close out the contract, that workload -- that backlog has quadrupled over the last 10 years. “

Related Trends We’ve Seen

• Contractor reaction to RFP’s and getting the competitive advantage – CAS on the shelf – SF1408 or mock audit readiness – ICQ (Internal Control Questionnaire) annually – CPSR readiness – FFP issued if can’t or haven't passed accounting

system audit (agency reaction)

Proprietary and Confidential 17

Related Trends We’ve Seen, Cont.

• Notices from the DCAA requesting provisional rate submissions by Feb 1 for that fiscal year (haven’t seen that in awhile.)

• Actual questions coming back on provisional rate submissions from the DCAA.

• Pre-award surveys of contractor accounting systems still on the rise, probably the most common activity we’ve seen.

Proprietary and Confidential 18

Trends We’re NOT Seeing, But Should

• Preparation for the wave of DCAA incurred cost audits:

– A review of contracts that have not been closed out – A closeout team or process in place to review old contracts

and determine adequate closeout documentation is in place – A review of old contracts to determine if they are eligible for

quick closeout. Why deal with the DCAA if you don’t have to? – Contractors review of which contracts require an incurred cost

submission and the timely filing thereof. – Close out Subcontractor Costs

Proprietary and Confidential 19

Quick Closeout (more trends)

• The Quick Closeout Method FAR 42.708 – Contract physically complete – Unsettled indirect costs to be allocated to contracts are

relatively insignificant. Indirect cost amounts are considered insignificant if

• Total unsettled indirect costs to be allocated to any one contract does not exceed $1,000,000

• Cumulative unsettled indirect costs allocated to one or more contracts in a single fiscal year do not exceed 15% of the estimated total unsettled indirect costs allocable to cost type contracts for that fiscal year. Contracting officer may waive this

• Agreement can be reached on a reasonable estimate of allocable dollars

Proprietary and Confidential 20

Hybrid Contracts or IDIQ (more trends)

• We’re seeing a trend of more hybrid type contracts which can be complicated to set up and monitor.

• Some hybrid contracts are being inappropriately reported on incurred cost submissions.

• Some contractors are mislead about what type of contract they have.

Proprietary and Confidential 21

Rate True Up (more trends)

FROM DCAM • if significant deviations between billing rates and incurred rates

occur during the year, or at year end, adjustments to the billing [should be unilaterally made by the contractor (don’t wait to be requested to do so by the contracting officer)].

• This process ensures that at year end the amount of indirect costs reimbursed is as close to the certified amount as possible. Incurred cost billings are cumulative, and therefore, should reflect the impact of any of these adjustments as soon as they are known.

• The contractor should have procedures and controls in place to ensure the prompt adjustment of billings to reflect these adjustments in indirect rates and direct costs

Proprietary and Confidential 22

Proprietary and Confidential 23

Preparing For The Storm

• You will need: – Plenty of Water – Snacks – A Shoulder to Cry On – To Know What to Expect

Proprietary and Confidential 24

DCAA Rules of Engagement

• Effective for 2011 and reiterates and clarifies coordination and communications with the contracting officer and contractor at each phase of the audit

• Contractors are entitled to: – An Entrance Conference – Discussions of preliminary audit findings to ensure the auditor

has all pertinent facts – An Exit Conference – For audits involving costs subject to negotiations the

contractor is entitled to a copy of the draft report to include opinion, exhibits and notes, statements of conditions or recommendations to the CO

Proprietary and Confidential 25

Prepare for Multi-Year Audits

• MRD 12-PPD-006 (R) Multi-Year Audit Techniques • Allows DCAA to audit 2-5 years with 1 audit report

and 1 workpaper package • Has to be non major contractors <$100 million and

can’t do it if contractor has more than $250M ADV. • Contractor must have similar contracts types

throughout the time period, no significant change in business systems, no significant organizational changes.

Proprietary and Confidential 26

Business Systems Trends

• Estimating, Purchasing, Accounting, EVMS, MMAS, and Property

• More audit related trends with a heavy internal control focus

• One size fits all • Policies & Procedures revised

Proprietary and Confidential 27

Related Trends We’ve Seen

• Audits are founded on internal controls, government contractors are catching on (clarity report)

• Review and Revision of internal control policies • Draft Guidance on new business rule criteria for

audits and new opinion basis (presentation given by N. Woods Regional Audit Manager on March 30, 2012)

• New workprograms due from DCAA June 2012

Proprietary and Confidential 28

Top Audit Issues / Deltek Clarity Report

• 2009 & 2010 1. Indirect Rates 2. Labor & Timekeeping 3. Unallowable Costs

• 2011 1. Labor & Timekeeping 2. Indirect Rates 3. Internal Control Systems

Proprietary and Confidential 29

2011 GAO Report on DCMA

• We examined the status of three business systems for the 17 defense contractors responsible for programs included in this review, as provided by the cognizant ACO. We found a substantial number of systems that had not been audited within the DCAA time frames; 12 of the contractors had at least one system without a current and timely audit.

• ACO’s noted that their DCAA counterparts were unable to provide clear and firm time frames for when the next audits would take place. In some cases, ACOs reported that expected audits planned by DCAA for a given fiscal year were not completed, so were moved back to the next year or canceled.

• When business systems are not audited in a timely manner, the government is at increased risk of paying for unallowable and unreasonable costs, as a contractor’s cost structure or accounting procedures may change over time.

Proprietary and Confidential 30

Expiration Dates

• Beware, that accounting system adequate opinion from 2007 isn’t gonna cut it, they expire!

Proprietary and Confidential 31

2011 GAO Report on DCMA

• Amid Ongoing Effort to Rebuild Capacity, Several Factors Present Challenges in Meetings Its Missions – Identified Risks: – the agency had lost the majority of its contract cost/price analysts.

Loss of this skill set, according to DCMA, meant that many of its pricing-related contract administration responsibilities, such as negotiating forward pricing rate agreements and establishing final indirect cost rates and billing rates, were no longer performed to the same level of discipline and consistency as in prior years.

– A key external risk to DCMA’s ability to effectively carry out its responsibility to determine the adequacy of defense contractor business systems comes from delays in obtaining audits from DCAA.

– Another potential risk for DCMA is a recent DOD policy change that increased the dollar threshold at which DCAA will conduct certain audits; as a result, DCMA’s own pricing workload will increase.

Proprietary and Confidential 32

The Workload Divide

Proprietary and Confidential 33

Goodbye Adequacy

• DCAA no longer opines as to whether the system is adequate or inadequate, they approve or disapprove a system nor do they recommend withhold or suspension of payments to the CO. Their report will opine as to whether the contractor is in compliance with the criteria for each system. • The CO determines adequate or inadequate

based on the report..this is new.

Proprietary and Confidential 34

The New Accounting System Audit

Proprietary and Confidential 35

Response to Uncertainties

• Contractors are telling us they are responding to as many RFP as they have the expertise to do so.

• The consensus is the amount of RFP’s issued might decline and contractors are trying to get settled in to ride the storm. Bottom line, beef up your backlog now.

• Current win rates remain at approximately 30%, contractors are banking on volume rather than that “one big” proposal.

Proprietary and Confidential 36

Bid Protests

• The amount of bid protests are on the rise as contractors compete on a smaller playing field (with more players).

• In the middle market we have seen more bid protests related to conflicts of interest and pricing issues

Proprietary and Confidential 37

Trends We’re NOT Seeing, But Should

• It’s imperative to win new work but equally important to hold on to the work you do get. With the increase in bid protest we should see an uptick in the number of government contractors that: – Review / revise / create compliance documents and

polices and procedures around • Conflicts of Interest both within the organization and for related

parties and subcontractors to include annual training. • Pricing and the integration of the pricing vs. the technical teams

within the contracts departments as well as the independent review of the finance department.

Proprietary and Confidential 38

Other Trends

• In general, Senior Management at Government Contractors seem tired and frustrated.

• Insourcing is turning around. The pendulum for what was once thought to be the end to government contracting is swinging.

• Lowest cost technically acceptable is squelching innovation and costing more in the long run.

• Award and funding lead times are getting longer • Many more T for C calculations this year with related

disclosures in the financial statements this audit season.

Proprietary and Confidential 39

Why Do It?

• That which does not kill us makes us stronger… in all honesty: – The federal government is the largest buyer in the

world, that’s a big market – It’s stable, this industry will not have a .com bust – They’re good for the money

Proprietary and Confidential 40