inefficiency and bank failures a joint bayesian estimation of a hazards model and a stochastic...

TRANSCRIPT

IntroductionLiterature Review

MethodologyApplicationReferences

Inefficiency and Bank FailuresA Joint Bayesian Estimation of a Hazards Model

and a Stochastic Frontier Model

Jim Sánchez González

Advisers:Diego Restrepo Tobón

Andres Ramírez Hassan

Universidad EAFITMedellín-Colombia

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Briefs I

Assessing the effects of inefficiency over the probability offailures is challenging.

The usual approach consist of estimating inefficiency and theprobability of failure separately, to then investigate theirconditional correlation.

This approach leads to inconsistent, biased, and inefficientestimators.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Briefs II

We develop a method to simultanously estimate a ProportionalHazards model and a Stochastic Frontier model using Bayesiantechniques.

Through simulation exercises we show that our proposalperforms better than tow-stages maximum likelihood.

Empirically, we find that inefficiency plays a statitical andeconomically significant role in determining the time to failure.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Contents

1 Introduction

2 Literature Review

3 MethodologyMethodologySimulation Exercise

4 ApplicationDataResults

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Contents

1 Introduction

2 Literature Review

3 MethodologyMethodologySimulation Exercise

4 ApplicationDataResults

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Introduction

The usual approach to estimate the effect of inefficiency over theprobability of failure consists in a two stages procedure.

An inefficiency measure is estimated using a Stochastic Frontier or aData Envelope Analysis approach. Then, failure indicators areregressed on these estimates.

This method yields inconsistent, biased, and inefficient estimatorsbecuase the second equation does not consider the first equation’sestimation error.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Contents

1 Introduction

2 Literature Review

3 MethodologyMethodologySimulation Exercise

4 ApplicationDataResults

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Literature Review I

Logit, Probit,

Extreme Value

Hazards Models

Discriminant Analysis,

Profile AnalysisCox Propor-

tional, Mixture

Financial, Economic InefficiencySFM

DEA

Two-stage approach Joint methods

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Literature Review II

Discriminant Analysis, Profile AnalysisBeaver (1966)[JAR]. Financial Ratios as Predictors of Failure.Altman (1968)[JF]. Financial Ratios, Discriminant Analysis andthe Prediction of Corporate Bankruptcy.

Logit, Probit, Extreme ValueOhlson (1980)[JAR]. Financial Ratios and the ProbabilisticPrediction of Bankruptcy.

Time-varying ModelsCox (1972)[JRSS]. Regression Models and Life-Tables.Whalen (1991)[FC]. A Proportional Hazards Model of BankFailure: An Examination of Its Usefulness as an Early WarningTool

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Literature Review I

Logit, Probit,

Extreme Value

Hazards Models

Discriminant Analysis,

Profile AnalysisCox Propor-

tional, Mixture

Financial, Economic InefficiencySFM

DEA

Two-stage approach Joint methods

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Literature Review III

InefficiencyWheelock and Wilson (1995)[RES]. Explaining Bank Failures:Deposit Insurance, Regulation, and Efficiency.Barr and Siems (1997). Bank Failure Prediction Using DEA toMeasure Management Quality.Wheelock and Wilson (2000)[RES]. Why do Banks Disappear?The Determinants of U.S. Bank Failures and Acquisitions.

Joint estimationTsionas and Papadogonas (2006)[EE]. Firm Exit and TechnicalInefficiency.Almanidis and Sickles (2015)[RISE]. Banking Crises, EarlyWarning Models, and Efficiency.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Literature Review I

Logit, Probit,

Extreme Value

Hazards Models

Discriminant Analysis,

Profile AnalysisCox Propor-

tional, Mixture

Financial, Economic InefficiencySFM

DEA

Two-stage approach Joint methods

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Literature Review III

InefficiencyWheelock and Wilson (1995)[RES]. Explaining Bank Failures:Deposit Insurance, Regulation, and Efficiency.Barr and Siems (1997). Bank Failure Prediction Using DEA toMeasure Management Quality.Wheelock and Wilson (2000)[RES]. Why do Banks Disappear?The Determinants of U.S. Bank Failures and Acquisitions.

Joint estimationTsionas and Papadogonas (2006)[EE]. Firm Exit and TechnicalInefficiency.Almanidis and Sickles (2015)[RISE]. Banking Crises, EarlyWarning Models, and Efficiency.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Contents

1 Introduction

2 Literature Review

3 MethodologyMethodologySimulation Exercise

4 ApplicationDataResults

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Stochastic Frontier Model

Consider the next Stochastic Frontier Model

Ln Cai = Ln C∗i (w, y) + µi + ηi

where, µi ∼ N(0, h−1

µ

)and ηi ∼ N+

(0, h−1

η

). Then,

L (c |β, hµ, η) ∝ hN2µ exp

[−1

2hµ∑

i

(ci − xiβ − ηi)′(ci − xiβ − ηi)

]

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Proportional Hazards Model

Let yi = y1, y2, . . . , yn be the duration time, which follows anExponential distribution with parameter λ = exp (z′iγ + δηi).Likewise, let vi = v1, v2, . . . , vn be a censoring indicator; wherevi = 0 if yi is censored and vi = 1 if yi is the failure time.

Then, the likelihood function can be expressed as,

L (y|γ, δ, η) = exp

[∑i

νi (z′iγ + δηi)

]exp

[−∑

i

yi exp (z′iγ + δηi)

]

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Conditional Posterior Distributions

We follow the literature and assume Normal distributions forβ, γ, and δ and assume Gamma distributions for the errorprecision parameters (hµ and hη).

With the priors and the likelihood functions defined; andassuming that after conditioning on η the production and theprobability of failure are independent we can compute theconditional posterior distribution for the parameters followingthe Bayes theorem.

π (θ|y, c) ∝ L (y|θ, η)L (c|θ, η)π (η|θ)π (θ)

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Estimation Procedure

We implement a Markov-Chain Monte Carlo (MCMC) algorithm forthe estimation of the parameters. Specifically a procedure known asMetropolis within Gibbs algorithm.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Algorithm I

At the gth iteration

Sample β|y, c ∼ N (µ1, B1); where,

B1 =

[hµ∑

i

x′ixi + Σ−10

]−1

µ1 = B1

[hµ∑

i

x′i (ci − ηi) + Σ−10 B0

]

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

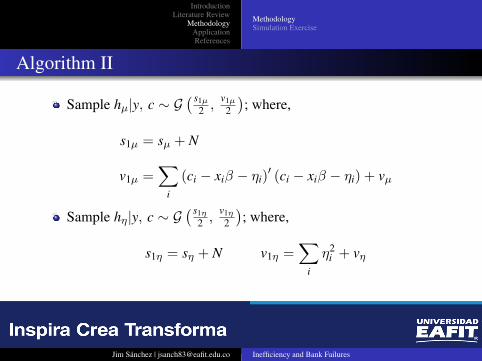

Algorithm II

Sample hµ|y, c ∼ G( s1µ

2 ,v1µ2

); where,

s1µ = sµ + N

v1µ =∑

i

(ci − xiβ − ηi)′ (ci − xiβ − ηi) + vµ

Sample hη|y, c ∼ G( s1η

2 ,v1η2

); where,

s1η = sη + N v1η =∑

i

η2i + vη

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Algorithm IIIConditional posterior distribution for γ

π (γ|y, c) ∝ exp

[∑i

νi (z′iγ + δηi)−∑

i

yi exp (z′iγ + δηi)

−12

(γ − Γ0)′Ω−1

0 (γ − Γ0)

]Conditional posterior distribution for δ

π (δ|y, c) ∝ exp

[∑i

νi (z′iγ + δηi)−∑

i

yi exp (z′iγ + δηi)

−12

hδ (δ −∆0)′(δ −∆0)

]

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Algorithm IV

Conditional posterior for each inefficiency

π (η | y , c) ∝ exp

[∑i

νi (z′iγ + δηi)−∑

i

yi exp (z′iγ + δηi)

−12

hµ

∑i

(ci − xiβ − ηi)′(ci − xiβ − ηi)−

12

hη

∑i

η2i

]

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

MethodologySimulation Exercise

Simulation Results

MAE PAE RSE MSESample set = 50

Joint Bayesian 0.54186 0.54186 0.72645 0.52772Two-stage MLE 51.98920 33.75922 201.19973 40,481.33151

Sample set = 250Joint Bayesian 0.20859 0.20859 0.24809 0.06155Two-stage MLE 17.70118 11.49428 49.07837 2,408.68674

Sample set = 1,000Joint Bayesian 0.33877 0.33877 0.34185 0.11686Two-stage MLE 1.27013 0.82476 6.34006 40.19640

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Contents

1 Introduction

2 Literature Review

3 MethodologyMethodologySimulation Exercise

4 ApplicationDataResults

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Data I

Reports on Condition and Income (Call Reports).Federal Reserve Bank of Chicago.U.S. commercial banks

Federal Deposits and Insurance Corporation (FDIC).Failure date.

Quarterly financial information from 2001 to 2010.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Data II

0

20

40

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Year

Fai

lure

s

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Difference in Mean: Welch’s TestVariable Failing firms Non-failing firms t-statisticy1 (Securities) 36,568.32 64,558.96 3.61 *y2 (Loans) 260,383.03 204,422.90 8.31 *w1 (Price Fixed assets) 0.41 0.35 12.53 *w2 (Price Labor) 77.71 65.68 11.92 *w3 (Price Borrowed funds) 0.03 0.02 2.80 *C1 (Equity / Assets) 0.06 0.10 3.74 *A1 (Loans / Assets) 0.74 0.65 15.91 *A2 (REL / Loans) 0.80 0.72 19.23 *A4 (Provission / Loans) 0.04 0.01 1.73A6 (Provission / Assets) 0.03 0.01 1.64E1 (Profits / Equity) -0.31 0.17 -0.28L1 (Profits / Assets) 0.85 0.78 21.85 *Assets 342,301.64 310,881.06 20.79 *Inefficiency 0.49 0.35 5.85 *Efficiency 0.63 0.72 15.24 *

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Estimation Results

Bayesian estimation ML estimationMean P. 2.5th P. 50th P. 97.5th Estimates t-test

σµ 0.1132 0.1085 0.1134 0.1182 0.1910 67.6902 *ση 0.4241 0.4154 0.4242 0.4323 0.4748 42.0861 *Camel C1 -0.8951 -1.3528 -0.9481 -0.3024 -1.7093 -0.7440Camel A1 0.3335 -0.1580 0.3607 0.8531 -2.9353 -1.8433Camel A2 0.8491 0.5460 0.8222 1.3124 5.1231 6.9988 *Camel A4 -0.0243 -0.4028 -0.0056 0.3351 -1.3209 -0.0767Camel A6 0.2379 -0.3378 0.3256 0.6807 3.5461 0.1415Camel E1 -3.1125 -3.5663 -3.3133 -1.4301 -3.0999 -10.1207 *Camel L1 0.8802 0.1849 0.9969 1.3206 1.5193 1.2945Ln Assets -0.6514 -0.7136 -0.6567 -0.5690 -0.7880 -11.4693 *Ineff η 0.3351 0.0176 0.3249 0.6509 0.3079 0.6262

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Effect of Efficiency

Recall that yi ∼ Exp (λ)and that λ = exp (z′γ + δη)

Besides, We know that theEfficiency = exp (−η).

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9

Prop

ortio

nal M

ean

Tim

e to

Fai

lure

Efficiency

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Returns to Scale

1.00 1.05 1.10 1.15 1.20 1.25 1.30 1.35

0 5

010

015

0

0

2000

4000

6000

8000

RTS

Fir

ms

Den

sity

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Empirical Densities of Efficiencies

0

10

20

0.6 0.7 0.8 0.9

Eff

dens

ity

Firms2129

3885

5203

6165

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Concluding Remarks I

We propose a method, based in Bayesian techniques, to estimatesimultaneously a Stochastic Frontier model and a Hazardsmodel. This method allows us to solve the econometrics flawsseen in two-stages estimation and to perform statistical inferenceof functions of the parameters.

Through simulation exercises, we show that the estimation errorof the two-stage maximum likelihood is higher than the oneobserved if we use the simultaneous Bayesian estimation.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

DataResults

Concluding Remarks IIUsing U.S. commercial banks data from 2001 to 2010, we find that:

More inefficient banks have a lower mean time to failure.

Most banks have cost elasticities between zero and one.

The banks in the sample present increasing returns to scale.

In terms of economic policy, we have that:

Bigger banks, measured by their total assets, have a smaller probabilityof failure and also have increasing returns to scale.

Regulators should not heavily restrict mergers and acquisitionsbetween commercial banks and should consider the banks efficiencylevel when assesing the banks’ risk of failure.

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

Thank you all!

Comments are also welcome [email protected].

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

References I

Almanidis, P., & Sickles, R. C. (2015). Banking Crises, Early Warning Models, andEfficiency.

Altman, E. I. (1968). Financial Ratios, Discriminant Analysis and the Prediction ofCorporate Bankruptcy. The Journal of Finance, 23(4), 589–609. doi:10.2307/2978933

Barr, R. S., & Siems, T. F. (1997). Bank Failure Prediction Using DEA to MeasureManagement Quality. In Interfaces in computer science and operationsresearch (pp. 341 – 365). Boston, Massachusetts: Springer U.S. doi:10.1007/978-1-4615-4102-8_15

Beaver, W. H. (1966). Financial Ratios as Predictors of Failure. Journal ofAccounting Research, 4, 71–111. doi: 10.2307/2490171

Cox, D. R. (1972). Regression Models and Life-Tables. Journal of the RoyalStatistical Society. Series B (Methodological), 34(2), 187–220. Retrievedfrom http://www.jstor.org/stable/2985181

Jim Sánchez | [email protected] Inefficiency and Bank Failures

IntroductionLiterature Review

MethodologyApplicationReferences

References II

Ohlson, J. A. (1980). Financial Ratios and the Probabilistic Prediction ofBankruptcy. Journal of Accounting Research, 18(1), 109–131. doi:10.2307/2490395

Tsionas, E. G., & Papadogonas, T. A. (2006). Firm Exit and Technical Inefficiency.Empirical Economics, 31, 535 – 548. doi: 10.1007/s00181-005-0045-2

Whalen, G. (1991). A Proportional Hazards Model of Bank Failure: An Examinationof Its Usefulness as an Early Warning Tool. Federal Reserve Bank ofCleveland, Economic Review, 27(1), 21–31.

Wheelock, D. C., & Wilson, P. W. (1995). Explaining Bank Failures: DepositInsurance, Regulation, and Efficiency. The Review of Economics andStatistics, 77(4), 689–700. Retrieved fromhttp://www.jstor.org/stable/2109816

Wheelock, D. C., & Wilson, P. W. (2000). Why do Banks Disappear? TheDeterminants of U.S. Bank Failures and Acquisitions. The Review ofEconomics and Statistics, 82(1), 127–138. Retrieved fromhttp://www.jstor.org/stable/2646678

Jim Sánchez | [email protected] Inefficiency and Bank Failures