inflation hedging it & trading it - company – deutsche...

TRANSCRIPT

Deutsche Bank Corporate Banking & Securities

Inflation Hedging it & Trading it

Inflation—Hedgingit&Tradingit Deutsche Bank

Introduction Whyinflation,whynow?

1.0 Deutsche Bank’s capabilities and credentials in this market 1.1HowDeutscheBank’sinflationofferingdiffersfrom competitors 2.0 MarketOverview–theriseandriseofinflationvolatility 2.1 ComponentsofInflationindices

3.0 InflationLinkedBonds 3.1 InflationLinkedBonds 3.2RealYieldandBreakevenInflationandInflationProtection 3.3IndexationandBreakevenInflation 3.4RiskMeasures,EMSovereignLinkers,Seasonality, andUSTIPS 3.5UKIndexLinkedGilts,EURSovereignLinkers,andother Important Markets 3.6ILBcouponfrequencyandsettlementcharacteristics

4.0 InflationSwaps 4.1 ILSSwapsandMarkets 4.2UKSwaps,CorporateLinkers,andUSSwaps 4.3ILSIndexation 4.4ILSPensionFunddemand

5.0 Assessing Relative Value 5.1 LinkerAssetSwapsandtheLeverageEffect 5.25sourcesofAssetSwapDifference 5.3Whatisthe‘Fair’PriceforInflationProtection? 5.4FairCreditSpreadofInflationLinkedBonds 5.5HedgewithBondsorSwaps 5.6 Summary

6.0 InflationOptions 6.1 InflationOptions 6.2Whoarethemajorplayersintheoptionsmarket? 6.3OptionProducts 6.4Whatarethetradingopportunities? 6.5 Option Strategies 6.6 Creating Optimal Hedges

7.0 Deflationtailrisk 7.1 DeflationTailRisk:DB5YearNote 8.0 CaseStudy–Zero-CouponOptionTrade

9.0 FurtherReading 9.1InflationHedgingforInstitutionalInvestors

10.0 Contacts 10.1DeutscheBankGlobalInflationTeam

Contents

Inflation—Hedgingit&Tradingit Deutsche Bank 4

There has never been a better timetotalkaboutinflation:

–Inflationhasbeenrunning above central bank targets again –Atthesametimemonetary policy seems to be constrained byhighunemployment, elevateddebtlevelsandfragile financialmarkets –Higheruncertaintyaboutthe inflationoutlookraisesthe incentivetohedgeinflationrisks –Anyinvestorwithabond portfolioisexposed.

Deutsche Bank is very strongly positioned to advise clients on whattodo:

–WewererecentlyvotedInterest RateDerivativesHouseofthe Year by Risk Magazine –Wehavealargeglobalinflation derivatives trading and structuring team –Wehaveextensiveexperience ofhelpingclientsfindinflation solutions.

TheDeutscheBankinflationteamhasdevelopedthisbriefingdocumentto:

–Setoutthechallenges andopportunitiesfacedby clients –Explaintheproductsand strategieswehavedeveloped.

TheDeutscheBankGlobalInflationteamcanhelp.

Introduction Whyinflation,whynow?

1Deutsche Bank’s credentials and capabilitiesintheInflationmarketHowDeutscheBank’sinflationofferingsdifferfromcompetitors

Inflation—Hedgingit&Tradingit Deutsche Bank 6

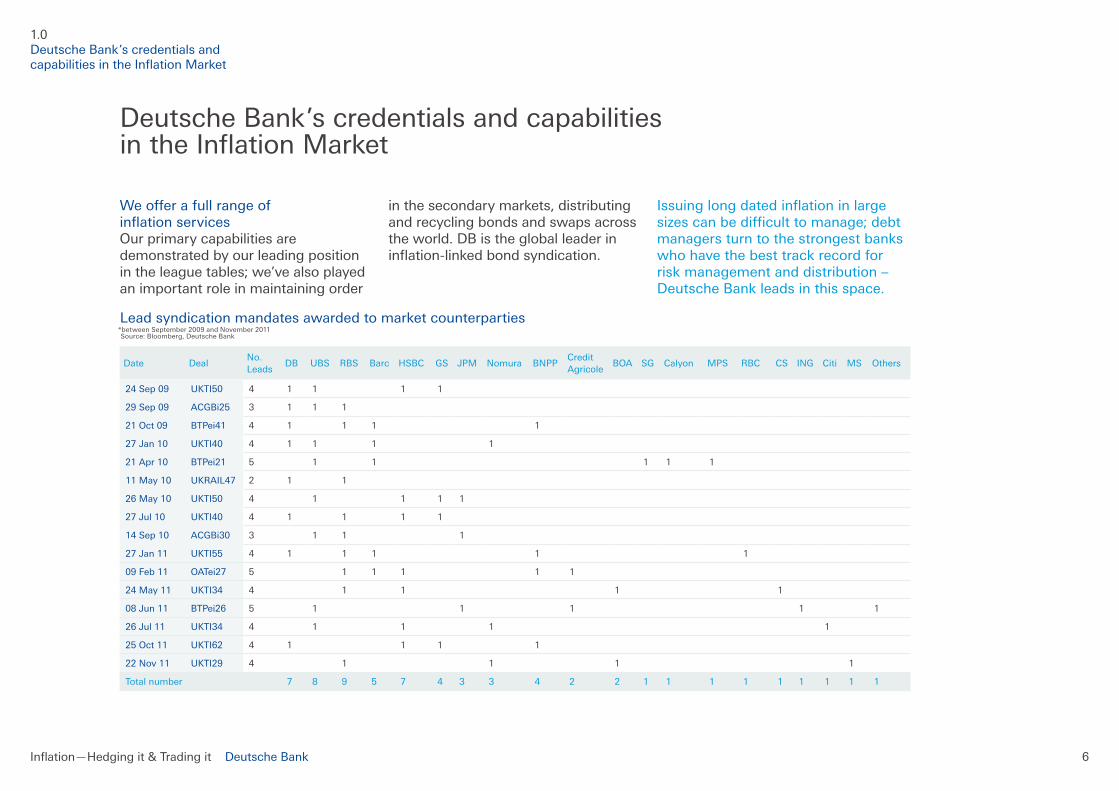

Weofferafullrangeof inflationservices Our primary capabilities are demonstrated by our leading position intheleaguetables;we’vealsoplayedan important role in maintaining order

Date DealNo.Leads

DB UBS RBS Barc HSBC GS JPM Nomura BNPPCredit Agricole

BOA SG Calyon MPS RBC CS ING Citi MS Others

24 Sep 09 UKTI50 4 1 1 1 1

29 Sep 09 ACGBi25 3 1 1 1

21 Oct 09 BTPei41 4 1 1 1 1

27 Jan 10 UKTI40 4 1 1 1 1

21 Apr 10 BTPei21 5 1 1 1 1 1

11 May 10 UKRAIL47 2 1 1

26 May 10 UKTI50 4 1 1 1 1

27 Jul 10 UKTI40 4 1 1 1 1

14 Sep 10 ACGBi30 3 1 1 1

27 Jan 11 UKTI55 4 1 1 1 1 1

09Feb11 OATei27 5 1 1 1 1 1

24 May 11 UKTI34 4 1 1 1 1

08 Jun 11 BTPei26 5 1 1 1 1 1

26 Jul 11 UKTI34 4 1 1 1 1

25 Oct 11 UKTI62 4 1 1 1 1

22Nov11 UKTI29 4 1 1 1 1

Total number 7 8 9 5 7 4 3 3 4 2 2 1 1 1 1 1 1 1 1 1

inthesecondarymarkets,distributingandrecyclingbondsandswapsacrosstheworld.DBisthegloballeaderininflation-linkedbondsyndication.

Issuinglongdatedinflationinlargesizescanbedifficulttomanage;debtmanagers turn to the strongest banks whohavethebesttrackrecordforriskmanagementanddistribution–Deutsche Bank leads in this space. Leadsyndicationmandatesawardedtomarketcounterparties

*betweenSeptember2009andNovember2011 Source:Bloomberg,DeutscheBank

Deutsche Bank’s credentials and capabilities intheInflationMarket

1.0 Deutsche Bank’s credentials and capabilitiesintheInflationMarket

Inflation—Hedgingit&Tradingit Deutsche Bank 7

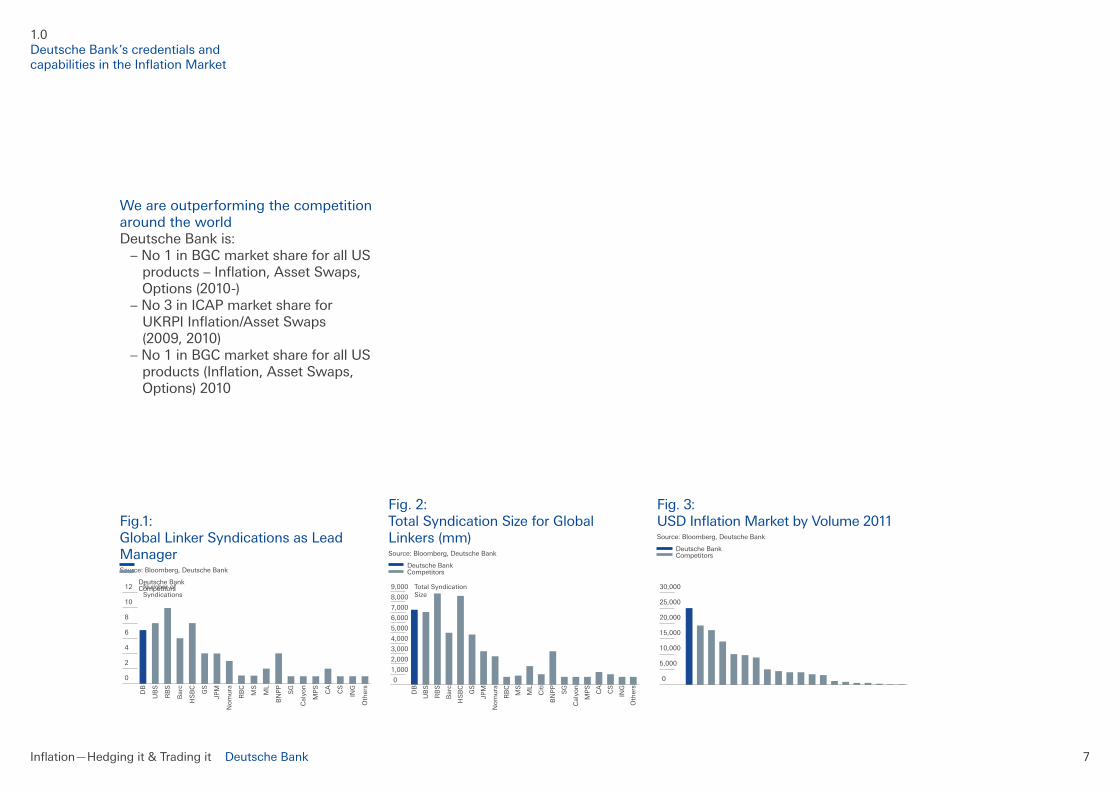

Weareoutperformingthecompetitionaroundtheworld DeutscheBankis: –No1inBGCmarketshareforallUS products–Inflation,AssetSwaps, Options(2010-) –No3inICAPmarketsharefor UKRPIInflation/AssetSwaps (2009,2010) –No1inBGCmarketshareforallUS products(Inflation,AssetSwaps, Options)2010 Fig.1: GlobalLinkerSyndicationsasLeadManager Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

Fig.2: TotalSyndicationSizeforGlobalLinkers(mm) Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

Fig.3: USDInflationMarketbyVolume2011 Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

DB

UB

S

RB

S

Bar

c

HS

BC

GS

JPM

No

mu

ra SG

BN

PP

RB

C

Cal

yon

MP

S

Oth

ers

ING

CS

CA

4

2

0

6

8

10

12 Number ofSyndications

MS

ML

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

DB

UB

S

RB

S

Bar

c

HS

BC

GS

JPM

No

mu

ra

BN

PP

Cit

i

SG

ML

MS

RB

C

Cal

yon

Oth

ers

ING

CS

CA

MP

STotal SyndicationSize

0 0

30,000

25,000

20,000

15,000

10,000

5,000

1.0 Deutsche Bank’s credentials and capabilitiesintheInflationMarket

Inflation—Hedgingit&Tradingit Deutsche Bank 8

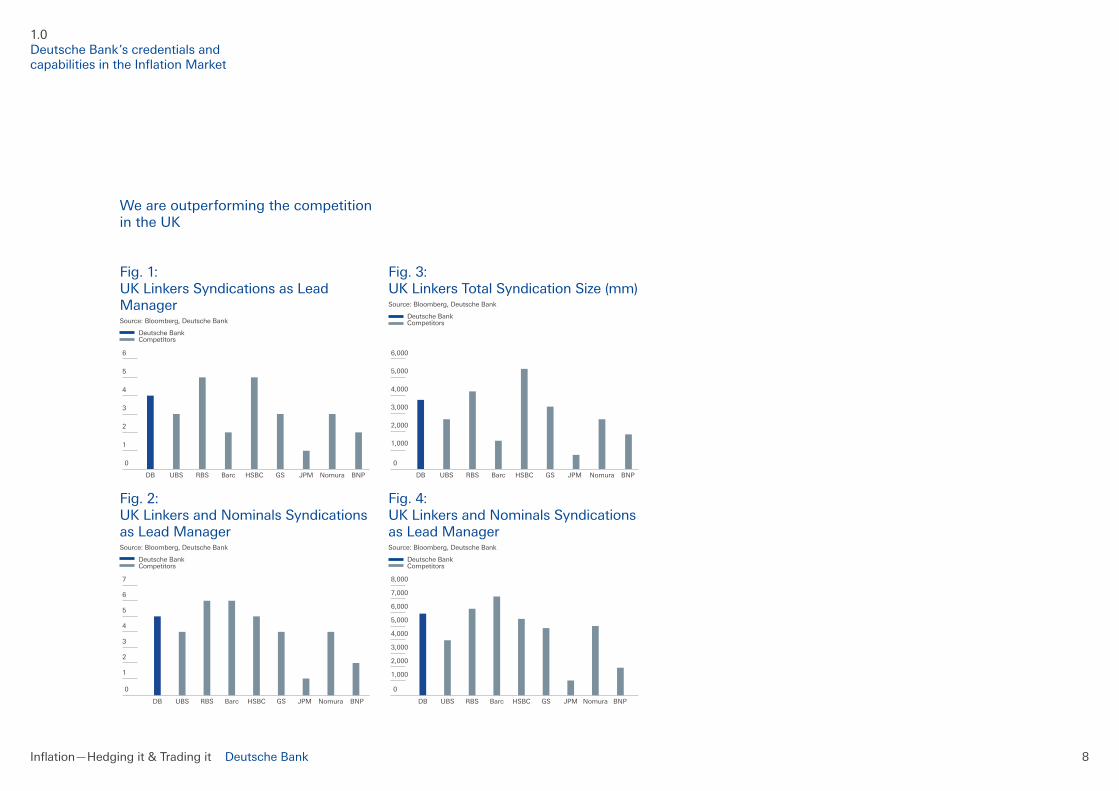

Weareoutperformingthecompetitionin the UK Fig.1: UKLinkersSyndicationsasLeadManager Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

Fig.2: UKLinkersandNominalsSyndicationsasLeadManager Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

Fig.3: UKLinkersTotalSyndicationSize(mm) Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

Fig.4: UKLinkersandNominalsSyndicationsasLeadManager Source:Bloomberg,DeutscheBank

Deutsche Bank Competitors

DB UBS RBS Barc HSBC GS JPM BNPNomura

7

6

5

4

3

2

1

0

DB UBS RBS Barc HSBC GS JPM BNPNomura

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

DB UBS RBS Barc HSBC GS JPM BNPNomura

6,000

5,000

4,000

3,000

2,000

1,000

0

6

5

4

3

2

1

DB UBS RBS Barc HSBC GS JPM BNPNomura

0

1.0 Deutsche Bank’s credentials and capabilitiesintheInflationMarket

Inflation—Hedgingit&Tradingit Deutsche Bank 9

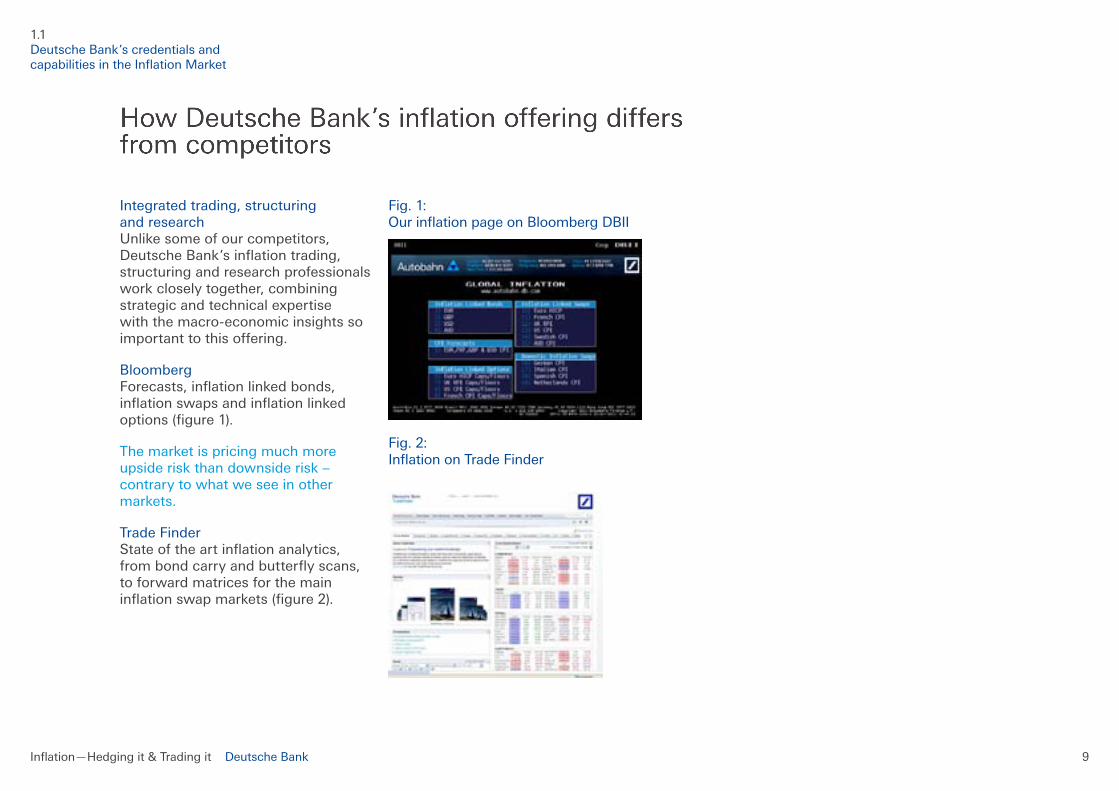

Integratedtrading,structuring and research Unlikesomeofourcompetitors,DeutscheBank’sinflationtrading,structuringandresearchprofessionalsworkcloselytogether,combiningstrategic and technical expertise withthemacro-economicinsightssoimportanttothisoffering.

Bloomberg Forecasts,inflationlinkedbonds,inflationswapsandinflationlinkedoptions(figure1).

The market is pricing much more upsideriskthandownsiderisk–contrarytowhatweseeinothermarkets.

TradeFinder Stateoftheartinflationanalytics,frombondcarryandbutterflyscans,toforwardmatricesforthemaininflationswapmarkets(figure2).

Fig.1: OurinflationpageonBloombergDBII

Fig.2: InflationonTradeFinder

1.1 Deutsche Bank’s credentials and capabilitiesintheInflationMarket

2MarketOverview

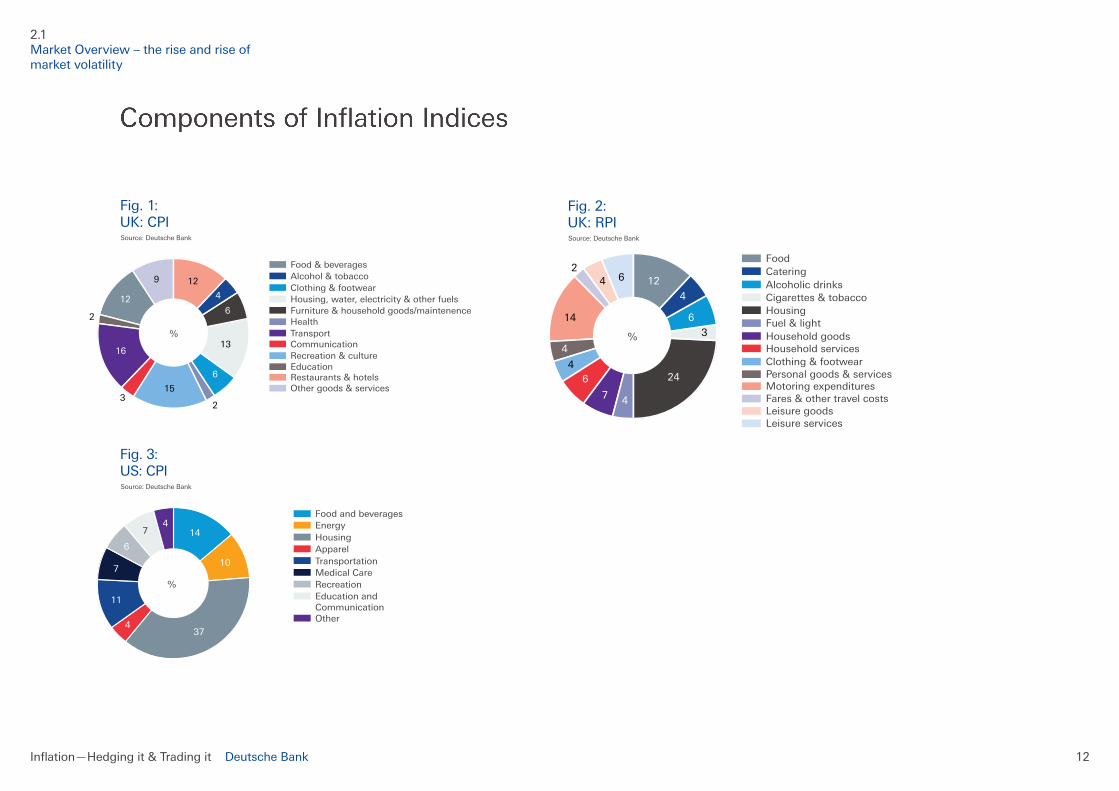

ComponentsofInflationindices

Inflation—Hedgingit&Tradingit Deutsche Bank 11

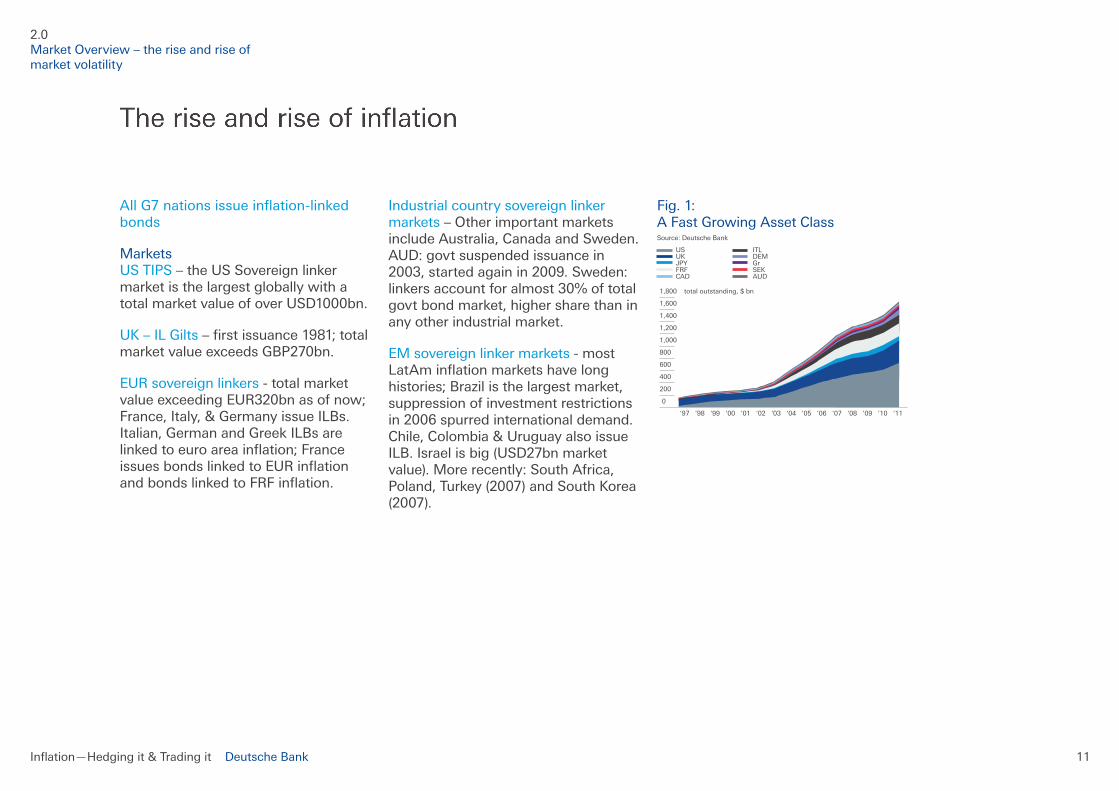

AllG7nationsissueinflation-linkedbonds

Markets USTIPS–theUSSovereignlinkermarketisthelargestgloballywithatotalmarketvalueofoverUSD1000bn.

UK–ILGilts–firstissuance1981;totalmarketvalueexceedsGBP270bn.

EURsovereignlinkers-totalmarketvalueexceedingEUR320bnasofnow;France,Italy,&GermanyissueILBs.Italian,GermanandGreekILBsarelinkedtoeuroareainflation;FranceissuesbondslinkedtoEURinflationandbondslinkedtoFRFinflation.

Industrial country sovereign linker markets–OtherimportantmarketsincludeAustralia,CanadaandSweden.AUD:govtsuspendedissuancein2003,startedagainin2009.Sweden:linkersaccountforalmost30%oftotalgovtbondmarket,highersharethaninany other industrial market.

EMsovereignlinkermarkets-mostLatAminflationmarketshavelonghistories;Brazilisthelargestmarket,suppressionofinvestmentrestrictionsin 2006 spurred international demand. Chile,Colombia&UruguayalsoissueILB.Israelisbig(USD27bnmarketvalue).Morerecently:SouthAfrica,Poland,Turkey(2007)andSouthKorea(2007).

Fig.1: AFastGrowingAssetClass Source:DeutscheBank

US ITL UK DEM JPY Gr FRF SEK CAD AUD

2.0 MarketOverview–theriseandriseofmarket volatility

‘97 ‘98 ‘99 ‘00 ‘09 ‘11‘10‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08

0

1,800 total outstanding, $ bn

1,200

1,400

1,600

1,000

800

600

400

200

Inflation—Hedgingit&Tradingit Deutsche Bank 12

Food and beverages

HousingApparelTransportationMedical CareRecreation

Other

Education andCommunication

Energy14

10

374

11

7

6

74

%

‘97 ‘98 ‘99 ‘00 ‘09 ‘10‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08

Food

Alcoholic drinks

HousingFuel & light

Catering

Cigarettes & tobacco

Clothing & footwearPersonal goods & servicesMotoring expendituresFares & other travel costsLeisure goodsLeisure services

Household goodsHousehold services

14

4

4

4

6

6

7

24

26

3

4

4

%

12

Food & beverages

Clothing & footwear

Furniture & household goods/maintenenceHealth

Alcohol & tobacco

Housing, water, electricity & other fuels

Recreation & cultureEducationRestaurants & hotelsOther goods & services

TransportCommunication

%13

4

6

6

12

16

15

23

2

129

2.1 MarketOverview–theriseandriseofmarket volatility

Fig.3: US:CPI Source:DeutscheBank

Fig.1: UK:CPI Source:DeutscheBank

Fig.2: UK:RPI Source:DeutscheBank

3InflationLinkedBonds

InflationLinkedBonds RealYieldandBreakevenInflationandInflationProtection IndexationandBreakevenInflation RiskMeasures,EMSovereignLinkers,SeasonalityandUSTIPS UKIndexLinkedGilts,EURSovereignandotherImportantMarkets ILBcouponfrequencyandsettlementcharacteristics

Inflation—Hedgingit&Tradingit Deutsche Bank 14

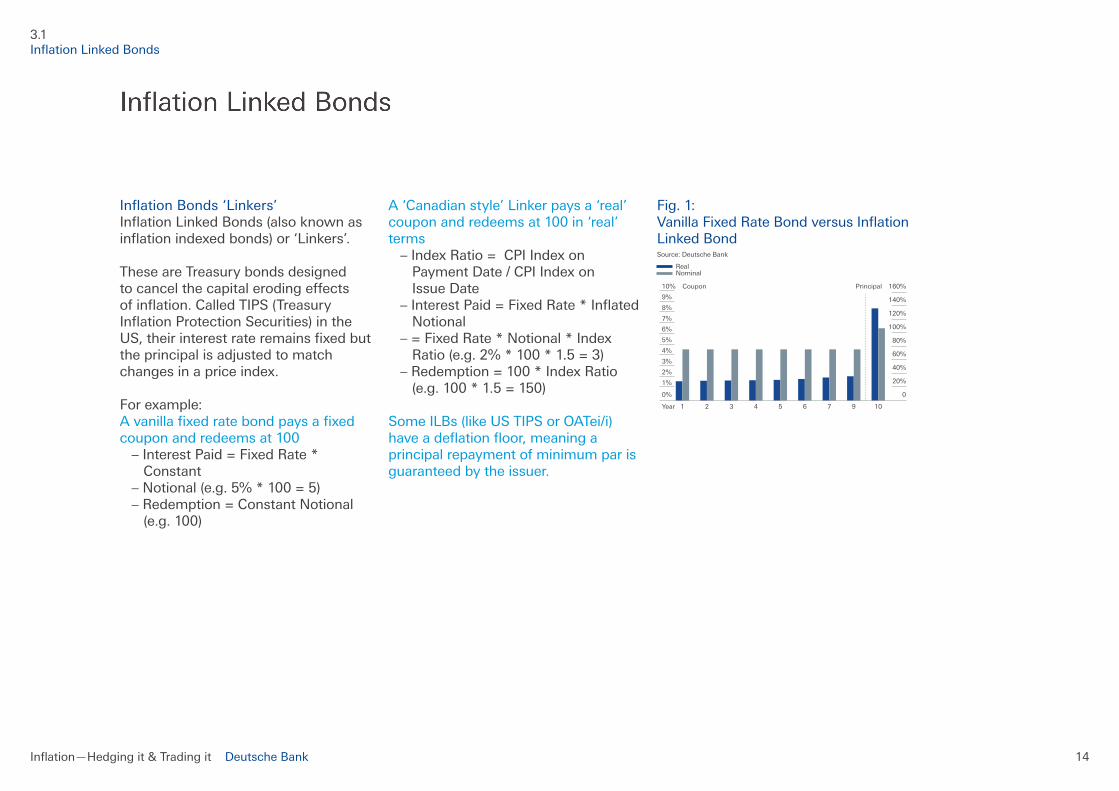

InflationBonds‘Linkers’ InflationLinkedBonds(alsoknownasinflationindexedbonds)or‘Linkers’.

These are Treasury bonds designed tocancelthecapitalerodingeffects ofinflation.CalledTIPS(Treasury InflationProtectionSecurities)inthe US,theirinterestrateremainsfixedbut the principal is adjusted to match changes in a price index.

Forexample: Avanillafixedratebondpaysafixedcoupon and redeems at 100 –InterestPaid=FixedRate* Constant –Notional(e.g.5%*100=5) –Redemption=ConstantNotional (e.g.100)

A‘Canadianstyle’Linkerpaysa‘real’coupon and redeems at 100 in ‘real’ terms –IndexRatio=CPIIndexon PaymentDate/CPIIndexon Issue Date –InterestPaid=FixedRate*Inflated Notional –=FixedRate*Notional*Index Ratio(e.g.2%*100*1.5=3) –Redemption=100*IndexRatio (e.g.100*1.5=150)

SomeILBs(likeUSTIPSorOATei/i)haveadeflationfloor,meaningaprincipalrepaymentofminimumparisguaranteed by the issuer.

Fig.1: VanillaFixedRateBondversusInflationLinkedBond Source:DeutscheBank

Real Nominal

3.1 InflationLinkedBonds

1 2 3 4 5 6 7 9 10

6%

5%

4%

3%

2%

1%

0%

Year

7%

8%

9%

10% Coupon Principal

80%

60%

40%

20%

0

100%

120%

140%

160%

Inflation—Hedgingit&Tradingit Deutsche Bank 15

RealYieldandBreakevenInflation Componentsofnominalinterestrate: –Realyield –ExpectedInflation –RiskPremium –LiquidityPremium

Issuing nominals means investors need compensationforinflationuncertainty.

Linkerssaveissuerstheriskpremiumby providing certainty about real cash flowsinthefuturei.e.theirincrease inpurchasingpoweris‘lockedin’.(figure1) Fig.1: ComponentsofNominalYield Source:DeutscheBank

InflationProtection Withpositiveinflation,theILB’scashflowswillincreaseovertimetosecuretheinvestor’spurchasingpower.

Compared to a nominal bond early couponpaymentswilltendtobelower,andthefinalrepaymentwilltendtobehigher.

Theexamplesbelowassumeanannualcouponandinflationat2%.(figures2and3). Fig.2: Nominalcashflows Source:DeutscheBank

CouponLinker(2%) NotionalConventional(rhs) CouponConventionalBond(4%) NotionalLinker(rhs)

Fig.3: Realcashflows(purchasingpower oftheCFs) Source:DeutscheBank

CouponLinker(2%) NotionalConventional(rhs) CouponConventionalBond(4%) NotionalLinker(rhs)

1 2 3 4 5 6 7 9 10

6%

5%

4%

3%

2%

1%

0%

7%

8%

9%

Nominal Yield

Breakeven RateIndex Linked Bond

RealYield

Inflation Expectations

RiskPremium Liquidity

Premium

1 2 3 4 5 6 7 8 9 not’l10

60

40

20

0

80

100

120

140

6

4

2

0

8

10

12

14

1 2 3 4 5 6 7 8 9 not’l10

60

40

20

0

80

100

120

6

4

2

0

8

10

12

3.2 InflationLinkedBonds

Inflation—Hedgingit&Tradingit Deutsche Bank 16

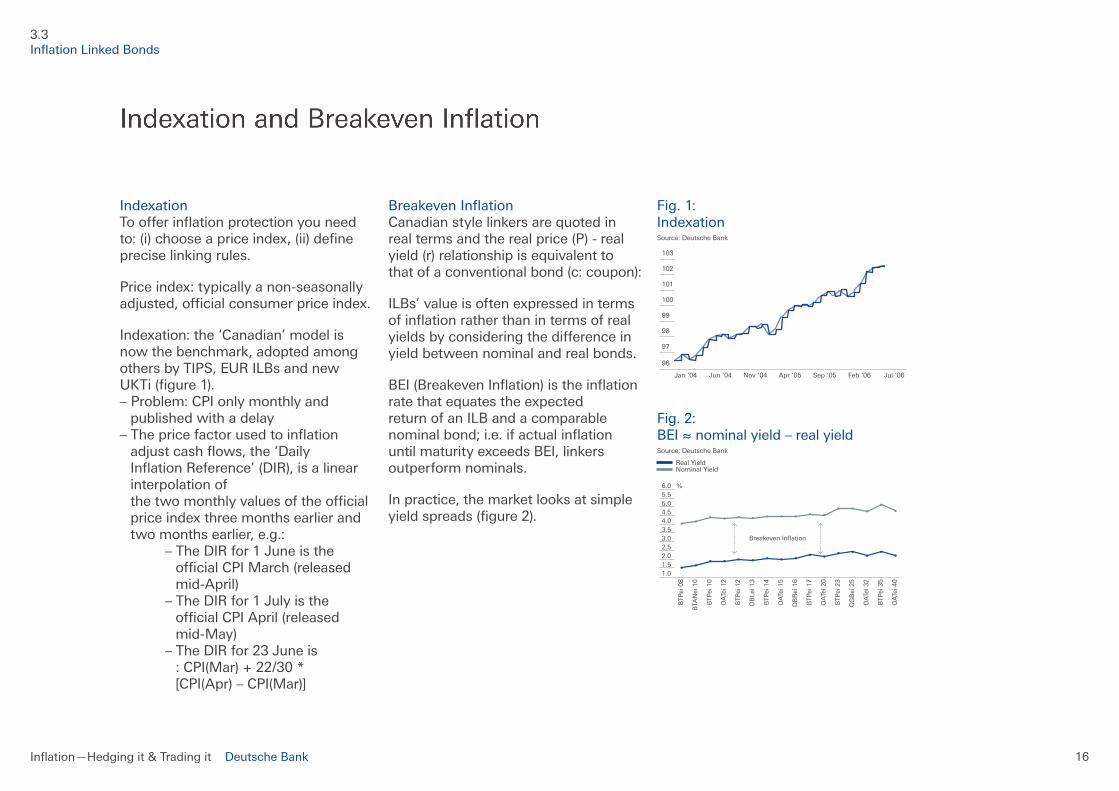

Indexation Toofferinflationprotectionyouneedto:(i)chooseapriceindex,(ii)defineprecise linking rules.

Priceindex:typicallyanon-seasonallyadjusted,officialconsumerpriceindex.

Indexation:the‘Canadian’modelisnowthebenchmark,adoptedamongothersbyTIPS,EURILBsandnewUKTi(figure1). –Problem:CPIonlymonthlyand publishedwithadelay –Thepricefactorusedtoinflation adjustcashflows,the‘Daily InflationReference’(DIR),isalinear interpolationof thetwomonthlyvaluesoftheofficial price index three months earlier and twomonthsearlier,e.g.: –TheDIRfor1Juneisthe officialCPIMarch(released mid-April) –TheDIRfor1Julyisthe officialCPIApril(released mid-May) –TheDIRfor23Juneis :CPI(Mar)+22/30* [CPI(Apr)–CPI(Mar)]

BreakevenInflation Canadianstylelinkersarequotedinrealtermsandtherealprice(P)-realyield(r)relationshipisequivalenttothatofaconventionalbond(c:coupon):

ILBs’valueisoftenexpressedintermsofinflationratherthanintermsofrealyieldsbyconsideringthedifferenceinyieldbetweennominalandrealbonds.

BEI(BreakevenInflation)istheinflationratethatequatestheexpectedreturnofanILBandacomparablenominalbond;i.e.ifactualinflationuntilmaturityexceedsBEI,linkersoutperformnominals.

Inpractice,themarketlooksatsimpleyieldspreads(figure2).

Fig.1: Indexation Source:DeutscheBank

Fig.2: BEI≈nominalyield–realyield Source:DeutscheBank

Real Yield NominalYield

Jan ‘04 Jun ‘04 Nov ‘04 Apr ‘05 Sep ‘05 Feb ‘06 Jul ‘06

100

99

98

97

96

101

102

103

BTP

ei 0

8

BTA

Nei

10

BTP

ei 1

0

OA

Tei 1

2

BTP

ei 1

2

OB

Lei 1

3

BTP

ei 1

4

OA

Tei 1

5

DB

Rei

16

BTP

ei 1

7

OA

Tei 2

0

BTP

ei 2

3

GG

Bei

25

OA

Tei 3

2

BTP

ei 3

5

OA

Tei 4

0

Breakeven Inflation

%

4.54.03.53.02.5

1.52.0

1.0

5.05.56.0

3.3 InflationLinkedBonds

Inflation—Hedgingit&Tradingit Deutsche Bank 17

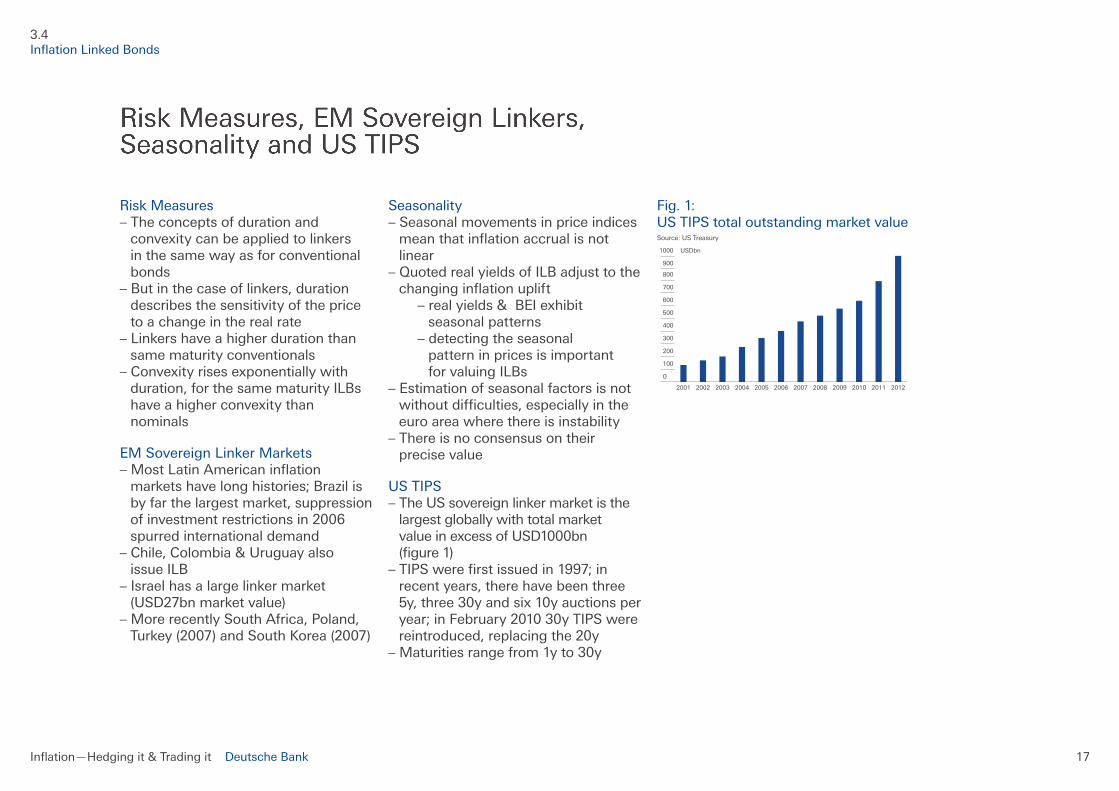

Risk Measures –Theconceptsofdurationand convexity can be applied to linkers inthesamewayasforconventional bonds –Butinthecaseoflinkers,duration describesthesensitivityoftheprice to a change in the real rate –Linkershaveahigherdurationthan same maturity conventionals –Convexityrisesexponentiallywith duration,forthesamematurityILBs have a higher convexity than nominals

EMSovereignLinkerMarkets –MostLatinAmericaninflation markets have long histories; Brazil is byfarthelargestmarket,suppression ofinvestmentrestrictionsin2006 spurred international demand –Chile,Colombia&Uruguayalso issueILB –Israelhasalargelinkermarket (USD27bnmarketvalue) –MorerecentlySouthAfrica,Poland, Turkey(2007)andSouthKorea(2007)

Seasonality –Seasonalmovementsinpriceindices meanthatinflationaccrualisnot linear –QuotedrealyieldsofILBadjusttothe changinginflationuplift –realyields&BEIexhibit seasonal patterns –detectingtheseasonal pattern in prices is important forvaluingILBs –Estimationofseasonalfactorsisnot withoutdifficulties,especiallyinthe euroareawherethereisinstability –Thereisnoconsensusontheir precise value

USTIPS –TheUSsovereignlinkermarketisthe largestgloballywithtotalmarket valueinexcessofUSD1000bn (figure1) –TIPSwerefirstissuedin1997;in recentyears,therehavebeenthree 5y,three30yandsix10yauctionsper year;inFebruary201030yTIPSwere reintroduced,replacingthe20y –Maturitiesrangefrom1yto30y

Fig.1: USTIPStotaloutstandingmarketvalue Source:USTreasury

3.4 InflationLinkedBonds

2001 2002 2003 2004 2005 2006 2007 2008 2009 2011 20122010

300

200

100

0

400

500

600

700

800

900

1000 USDbn

Inflation—Hedgingit&Tradingit Deutsche Bank 18

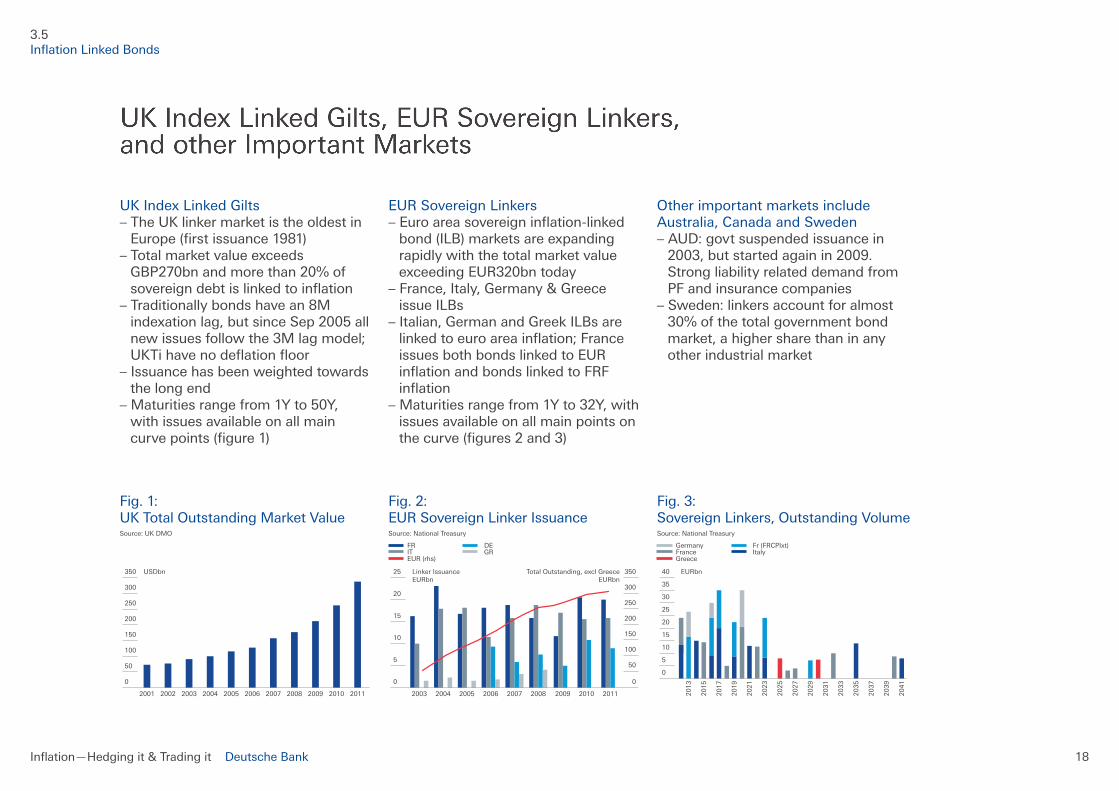

UKIndexLinkedGilts –TheUKlinkermarketistheoldestin Europe(firstissuance1981) –Totalmarketvalueexceeds GBP270bnandmorethan20%of sovereigndebtislinkedtoinflation –Traditionallybondshavean8M indexationlag,butsinceSep2005all newissuesfollowthe3Mlagmodel; UKTihavenodeflationfloor –Issuancehasbeenweightedtowards the long end –Maturitiesrangefrom1Yto50Y, withissuesavailableonallmain curvepoints(figure1)

Fig.1: UK Total Outstanding Market Value Source:UKDMO

EURSovereignLinkers –Euroareasovereigninflation-linked bond(ILB)marketsareexpanding rapidlywiththetotalmarketvalue exceedingEUR320bntoday –France,Italy,Germany&Greece issueILBs –Italian,GermanandGreekILBsare linkedtoeuroareainflation;France issuesbothbondslinkedtoEUR inflationandbondslinkedtoFRF inflation –Maturitiesrangefrom1Yto32Y,with issues available on all main points on thecurve(figures2and3)

Fig.2: EURSovereignLinkerIssuance Source:NationalTreasury

FR DE IT GR EUR(rhs)

Other important markets include Australia,CanadaandSweden –AUD:govtsuspendedissuancein 2003,butstartedagainin2009. Strongliabilityrelateddemandfrom PFandinsurancecompanies –Sweden:linkersaccountforalmost 30%ofthetotalgovernmentbond market,ahighersharethaninany other industrial market

Fig.3: SovereignLinkers,OutstandingVolume Source:NationalTreasury

Germany Fr(FRCPIxt) France Italy Greece

2001 2002 2003 2004 2005 2006 2007 2008 2009 20112010

50

0

100

150

300

200

250

350 USDbn

201120102009200820072006200520042003

5

10

15

0

20

25

50

100

150

0

200

250

300

350Linker IssuanceEURbn

Total Outstanding, excl GreeceEURbn

2031

2033

2015

2017

2019

2021

2023

2025

2027

2029

2035

2039

2037

2041

5

10

15

0

20

25

30

35

40 EURbn

2013

3.5 InflationLinkedBonds

Inflation—Hedgingit&Tradingit Deutsche Bank 19

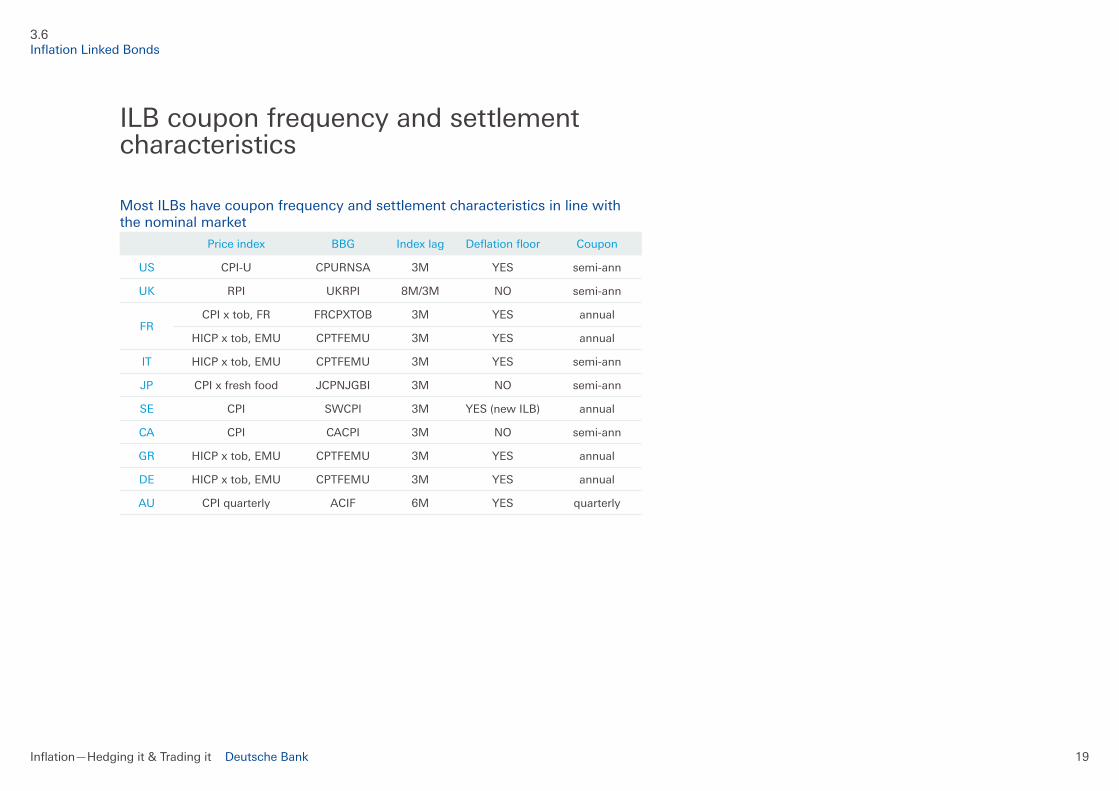

Priceindex BBG Index lag Deflationfloor Coupon

US CPI-U CPURNSA 3M YES semi-ann

UK RPI UKRPI 8M/3M NO semi-ann

FRCPIxtob,FR FRCPXTOB 3M YES annual

HICPxtob,EMU CPTFEMU 3M YES annual

IT HICPxtob,EMU CPTFEMU 3M YES semi-ann

JP CPIxfreshfood JCPNJGBI 3M NO semi-ann

SE CPI SWCPI 3M YES(newILB) annual

CA CPI CACPI 3M NO semi-ann

GR HICPxtob,EMU CPTFEMU 3M YES annual

DE HICPxtob,EMU CPTFEMU 3M YES annual

AU CPIquarterly ACIF 6M YES quarterly

3.6 InflationLinkedBonds

MostILBshavecouponfrequencyandsettlementcharacteristicsinlinewith the nominal market

ILBcouponfrequencyandsettlementcharacteristics

4InflationSwaps

ILSSwapsandMarkets UKSwaps,CorporateLinkersandUSSwaps ILSIndexation ILSPensionFundDemand

Inflation—Hedgingit&Tradingit Deutsche Bank 21

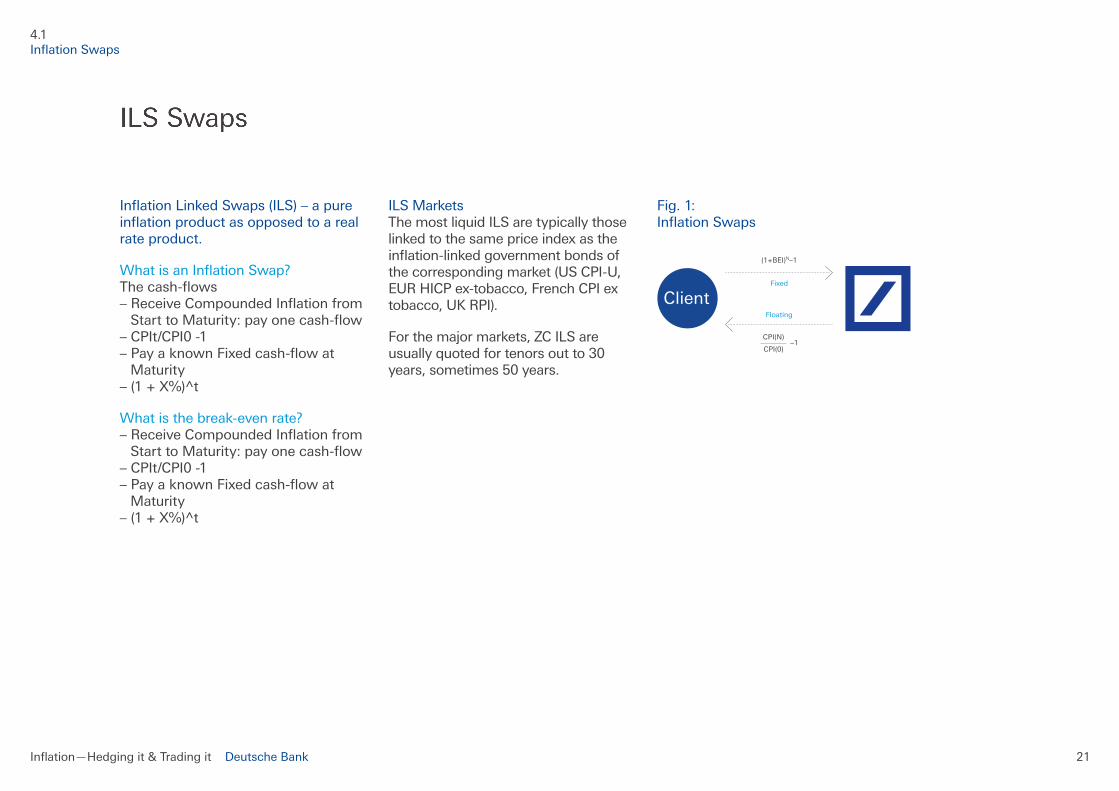

InflationLinkedSwaps(ILS)–apureinflationproductasopposedtoarealrate product.

WhatisanInflationSwap? Thecash-flows –ReceiveCompoundedInflationfrom StarttoMaturity:payonecash-flow –CPIt/CPI0-1 –PayaknownFixedcash-flowat Maturity –(1+X%)^t

Whatisthebreak-evenrate? –ReceiveCompoundedInflationfrom StarttoMaturity:payonecash-flow –CPIt/CPI0-1 –PayaknownFixedcash-flowat Maturity –(1+X%)^t

ILSMarkets ThemostliquidILSaretypicallythoselinked to the same price index as the inflation-linkedgovernmentbondsofthecorrespondingmarket(USCPI-U,EURHICPex-tobacco,FrenchCPIextobacco,UKRPI).

Forthemajormarkets,ZCILSareusuallyquotedfortenorsoutto30years,sometimes50years.

Fig.1: InflationSwaps

(1+BEI)N–1

Fixed

Floating

Client

CPI(N)

CPI(0)–1

4.1 InflationSwaps

Inflation—Hedgingit&Tradingit Deutsche Bank 22

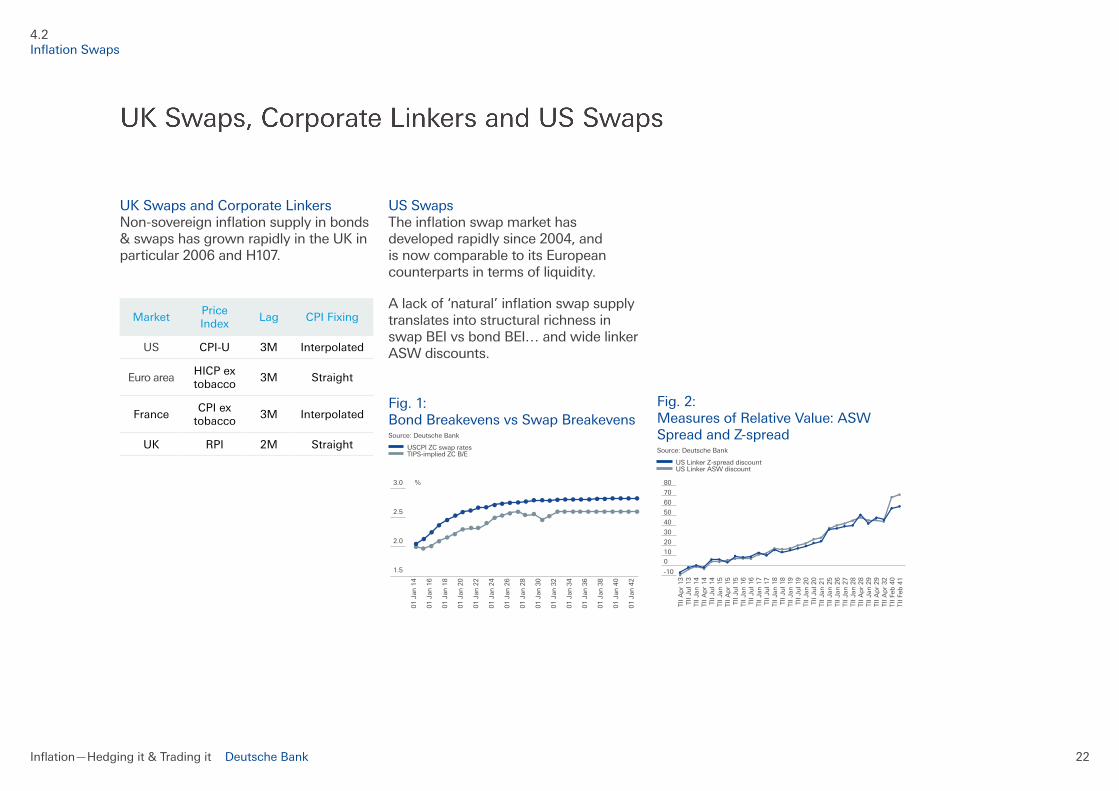

UKSwapsandCorporateLinkers Non-sovereigninflationsupplyinbonds&swapshasgrownrapidlyintheUKinparticular 2006 and H107.

MarketPriceIndex

Lag CPIFixing

US CPI-U 3M Interpolated

EuroareaHICPextobacco

3M Straight

FranceCPIex

tobacco3M Interpolated

UK RPI 2M Straight

USSwaps Theinflationswapmarkethasdevelopedrapidlysince2004,andisnowcomparabletoitsEuropeancounterpartsintermsofliquidity.

Alackof‘natural’inflationswapsupplytranslates into structural richness in swapBEIvsbondBEI…andwidelinkerASW discounts. Fig.1: BondBreakevensvsSwapBreakevens Source:DeutscheBank

USCPIZCswaprates TIPS-impliedZCB/E

Fig.2: MeasuresofRelativeValue:ASWSpreadandZ-spread Source:DeutscheBank

USLinkerZ-spreaddiscount USLinkerASWdiscount

4.2 InflationSwaps

01 J

an 1

4

01 J

an 1

6

01 J

an 1

8

01 J

an 2

0

01 J

an 2

2

01 J

an 2

4

01 J

an 2

6

01 J

an 2

8

01 J

an 3

0

01 J

an 3

2

01 J

an 3

4

01 J

an 3

6

01 J

an 3

8

01 J

an 4

0

01 J

an 4

2

1.5

2.0

2.5

3.0 %

TII A

pr

13

TII Ju

l 13

TII Ja

n 1

4TI

I A

pr

14

TII Ju

l 14

TII Ja

n 1

5TI

I A

pr

15

TII Ju

l 15

TII Ja

n 1

6TI

I Ju

l 16

TII Ja

n 1

7TI

I Ju

l 17

70

60

50

40

30

20

-10

10

0

80

TII Ja

n 1

8TI

I Ju

l 18

TII Ja

n 1

9TI

I Ju

l 19

TII Ja

n 2

0TI

I Ju

l 20

TII Ja

n 2

1TI

I Ja

n 2

5TI

I Ja

n 2

6TI

I Ja

n 2

7TI

I Ja

n 2

8TI

I A

pr

28

TII Ja

n 2

9TI

I A

pr

29

TII A

pr

32

TII Fe

b 4

0TI

I Fe

b 4

1

Inflation—Hedgingit&Tradingit Deutsche Bank 23

ILSIndexation ForFRCPIxt&USCPI,theindexationlagconventionisthesameasforthecorrespondinginflation-linkedbondmarkets –Strongdemandhasledtoalow levelofrealinterestrates,lockin lowfinancingcosts –PFIprojectswithinflationcomponent (usuallybonds,buttypically transformedintoASW) –Creditwrappingallowedcorporates toissuehighlyrateddebtwhich is more appealing to institutional investors

Buthasfallensignificantlyduringthecredit crisis.

Mainsources:regulatedutilities,PFIs,propertyleases,railwaycompanies,retailers,supranationals.

Alternativesupplyhasledtotwo-wayswapmarketandnarrowswap-bondB/Espread,butswaprichnesshasincreased again during the crisis.

4.3 InflationSwaps

ILSIndexation

Inflation—Hedgingit&Tradingit Deutsche Bank 24

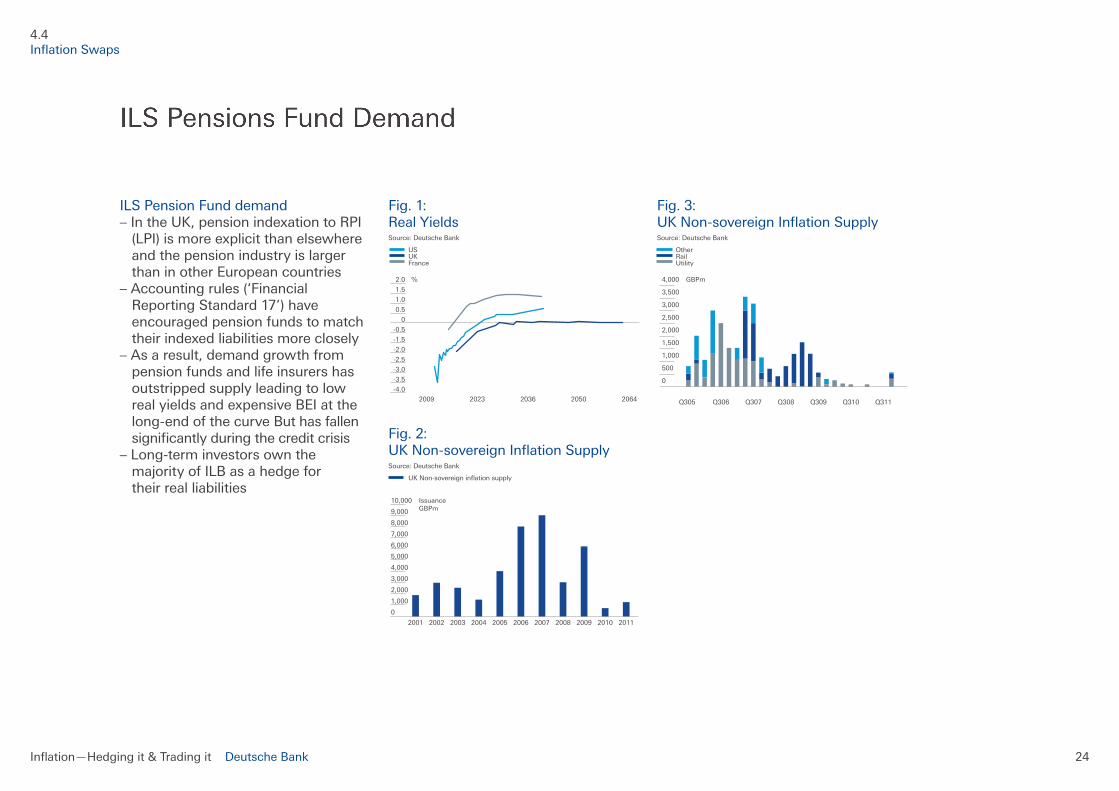

ILSPensionFunddemand –IntheUK,pensionindexationtoRPI (LPI)ismoreexplicitthanelsewhere and the pension industry is larger thaninotherEuropeancountries –Accountingrules(‘Financial ReportingStandard17’)have encouragedpensionfundstomatch their indexed liabilities more closely –Asaresult,demandgrowthfrom pensionfundsandlifeinsurershas outstrippedsupplyleadingtolow realyieldsandexpensiveBEIatthe long-endofthecurveButhasfallen significantlyduringthecreditcrisis –Long-terminvestorsownthe majorityofILBasahedgefor their real liabilities

Fig.1: Real Yields Source:DeutscheBank

US UK France

Fig.2: UKNon-sovereignInflationSupply Source:DeutscheBank

UKNon-sovereigninflationsupply

Fig.3: UKNon-sovereignInflationSupply Source:DeutscheBank

Other Rail Utility

4.4 InflationSwaps

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

0

-0.5

2.0

1.5

1.0

0.5

%

2009 2023 2036 2050 2064 Q311Q305 Q306 Q307 Q308 Q309 Q310

500

1,000

1,500

0

2,000

2,500

3,000

3,500

4,000 GBPm

2001 2002 2003 2004 2005 2006 2007 2008 2009 20112010

6,000

5,000

4,000

3,000

2,000

1,000

0

7,000

8,000

9,000

10,000 IssuanceGBPm

5Assessing Relative Value

LinkerAssetSwapandtheLeverageEffect 5SourcesofAssetSwapDifference Whatisthe‘Fair’PriceforInflationProtection? FairCreditSpreadofInflationLinkedBonds HedgewithBondsorSwaps Summary

Inflation—Hedgingit&Tradingit Deutsche Bank 26

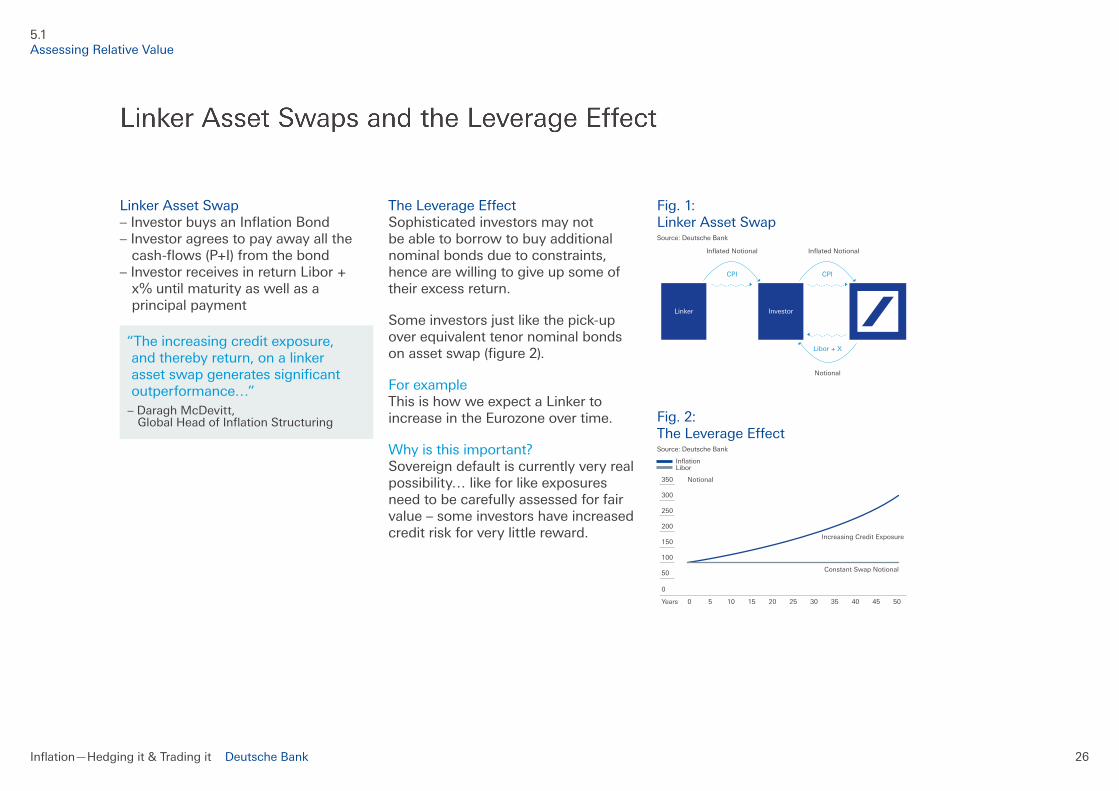

LinkerAssetSwap –InvestorbuysanInflationBond –Investoragreestopayawayallthe cash-flows(P+I)fromthebond –InvestorreceivesinreturnLibor+ x%untilmaturityaswellasa principal payment

TheLeverageEffect Sophisticated investors may not beabletoborrowtobuyadditionalnominalbondsduetoconstraints,hencearewillingtogiveupsomeoftheir excess return.

Someinvestorsjustlikethepick-upoverequivalenttenornominalbondsonassetswap(figure2).

Forexample ThisishowweexpectaLinkertoincreaseintheEurozoneovertime.

Whyisthisimportant? Sovereigndefaultiscurrentlyveryrealpossibility…likeforlikeexposuresneedtobecarefullyassessedforfairvalue–someinvestorshaveincreasedcreditriskforverylittlereward.

Fig.1: LinkerAssetSwap Source:DeutscheBank

Fig.2: TheLeverageEffect Source:DeutscheBank

Inflation Libor

5.1 Assessing Relative Value

Libor + X

Inflated Notional Inflated Notional

Notional

InvestorLinker

CPICPI

0 5 10 15 20 25

Constant Swap Notional

Increasing Credit Exposure

30 35 40Years 45 50

150

100

50

0

200

250

300

350 Notional

“Theincreasingcreditexposure,andtherebyreturn,onalinkerassetswapgeneratessignificantoutperformance…” –DaraghMcDevitt, GlobalHeadofInflationStructuring

Inflation—Hedgingit&Tradingit Deutsche Bank 27

5SourcesofAssetSwapDifference

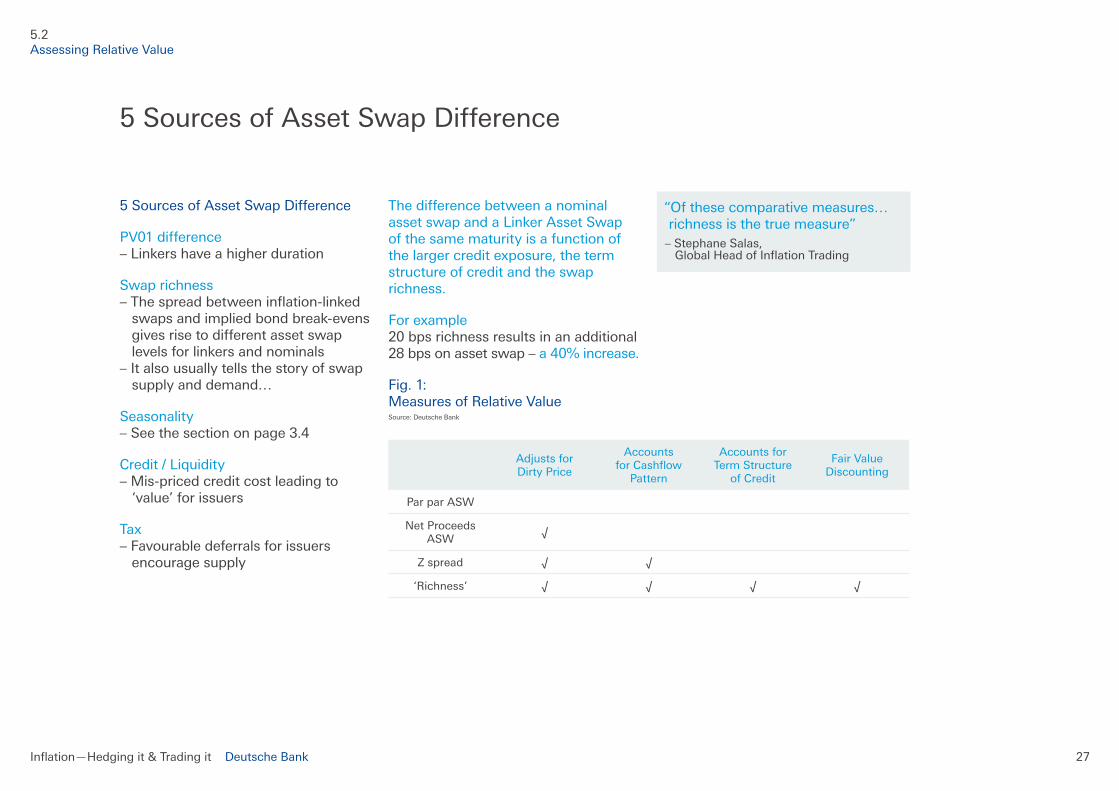

PV01difference –Linkershaveahigherduration

Swaprichness –Thespreadbetweeninflation-linked swapsandimpliedbondbreak-evens givesrisetodifferentassetswap levelsforlinkersandnominals –Italsousuallytellsthestoryofswap supplyanddemand…

Seasonality –Seethesectiononpage3.4

Credit/Liquidity –Mis-pricedcreditcostleadingto ‘value’forissuers

Tax –Favourabledeferralsforissuers encourage supply

ThedifferencebetweenanominalassetswapandaLinkerAssetSwapofthesamematurityisafunctionofthelargercreditexposure,thetermstructureofcreditandtheswaprichness.

Forexample 20 bps richness results in an additional 28bpsonassetswap–a40%increase.

Fig.1: MeasuresofRelativeValue Source:DeutscheBank

Adjustsfor DirtyPrice

Accounts forCashflowPattern

AccountsforTerm Structure

ofCredit

FairValueDiscounting

ParparASW

NetProceedsASW

√

Zspread √ √

‘Richness’ √ √ √ √

5.2 Assessing Relative Value

“Ofthesecomparativemeasures…richnessisthetruemeasure” –StephaneSalas, GlobalHeadofInflationTrading

5SourcesofAssetSwapDifference

Inflation—Hedgingit&Tradingit Deutsche Bank 28

Whatisthe‘Fair’PriceforInflationProtection?

Inflation‘Breakeven’isnotequaltomarketinflationexpectationsbutisafactorof –Inflationexpectations –‘RiskPremium’ –‘LiquidityPremium’

Inflationexpectationsovertheverylong run are hard to judge but tend to be based on current economic policy –ECBtargetrateis‘under,butclose to2%’

RiskPremiumincludes –Potentialchangeinmonetarypolicy target(e.g.4%plusorminus1% insteadofunder2%) –Abandonmentofmonetarypolicy infavourofemploymentor currency board –EURbreakup,expansionor succession –Asymmetricelasticityofinflation: wagesareeasiertoraisethantocut

Liquiditypremiumincludes –Relativedemandandsupplyfor inflationbondsvnominalbonds –Balancesheetcostsofholding inflationbondstorecycleinflation –Opportunitycostofcapitalforcash usedtohedgeinflation

5.3 Assessing Relative Value

“The biggest mistake people make withinflation-linkedbondsisthinkingthatthebreakeveninflationisthemarket’sexpectedinflationrate. It is not and should not be. Thebreakevenincludeswhatthemarketexpectsinflationtobeandthemajorportionoftheriskpremiumthatyoushouldfindin thenominalmarket,andtheliquiditypremium” –MarkusHeider, GlobalHeadofInflationResearch

Whatisthe‘Fair’PriceforInflationProtection?

Inflation—Hedgingit&Tradingit Deutsche Bank 29

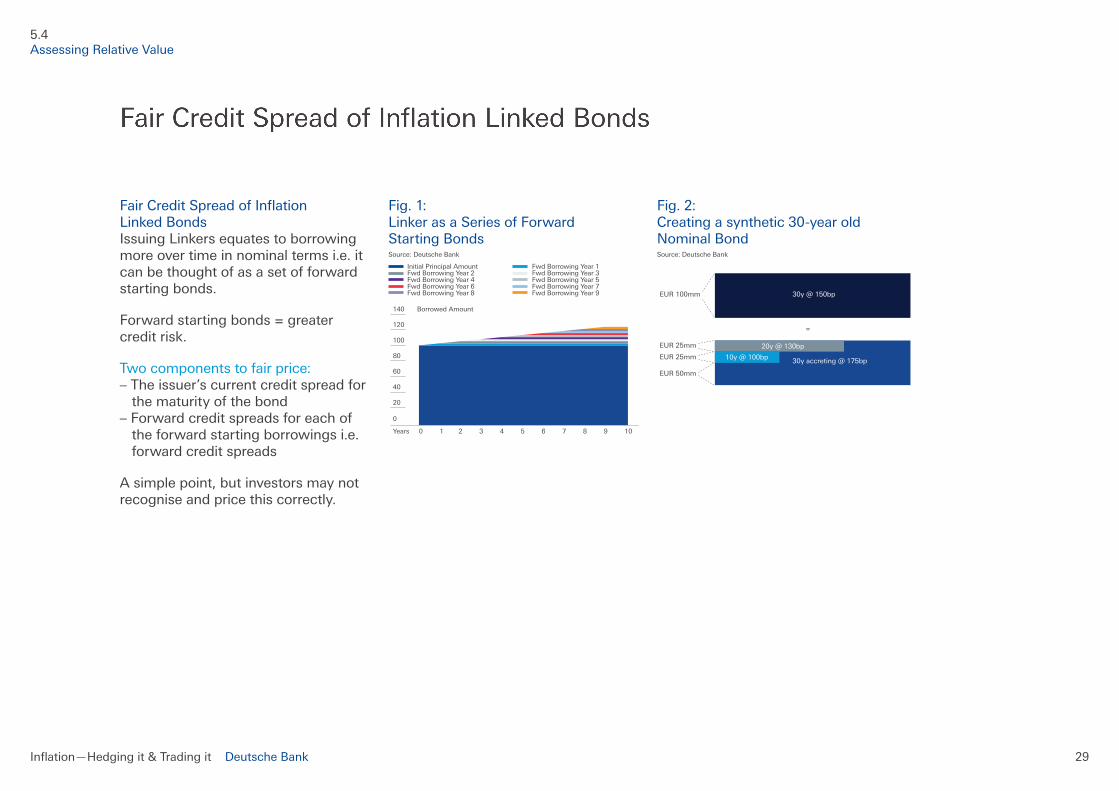

FairCreditSpreadofInflation LinkedBonds IssuingLinkersequatestoborrowingmore over time in nominal terms i.e. it canbethoughtofasasetofforwardstarting bonds.

Forwardstartingbonds=greatercredit risk.

Twocomponentstofairprice: –Theissuer’scurrentcreditspreadfor thematurityofthebond –Forwardcreditspreadsforeachof theforwardstartingborrowingsi.e. forwardcreditspreads

Asimplepoint,butinvestorsmaynotrecognise and price this correctly.

Fig.1: LinkerasaSeriesofForward Starting Bonds Source:DeutscheBank

InitialPrincipalAmount FwdBorrowingYear1 FwdBorrowingYear2 FwdBorrowingYear3 FwdBorrowingYear4 FwdBorrowingYear5 FwdBorrowingYear6 FwdBorrowingYear7 FwdBorrowingYear8 FwdBorrowingYear9

Fig.2: Creatingasynthetic30-yearoldNominalBond Source:DeutscheBank

5.4 Assessing Relative Value

0 1 2 3 4 5 6 7 8Years 9 10

60

40

20

0

80

100

120

140 Borrowed Amount

=

EUR 100mm

EUR 25mm

EUR 25mm

EUR 50mm

20y @ 130bp

10y @ 100bp 30y accreting @ 175bp

30y @ 150bp

Inflation—Hedgingit&Tradingit Deutsche Bank 30

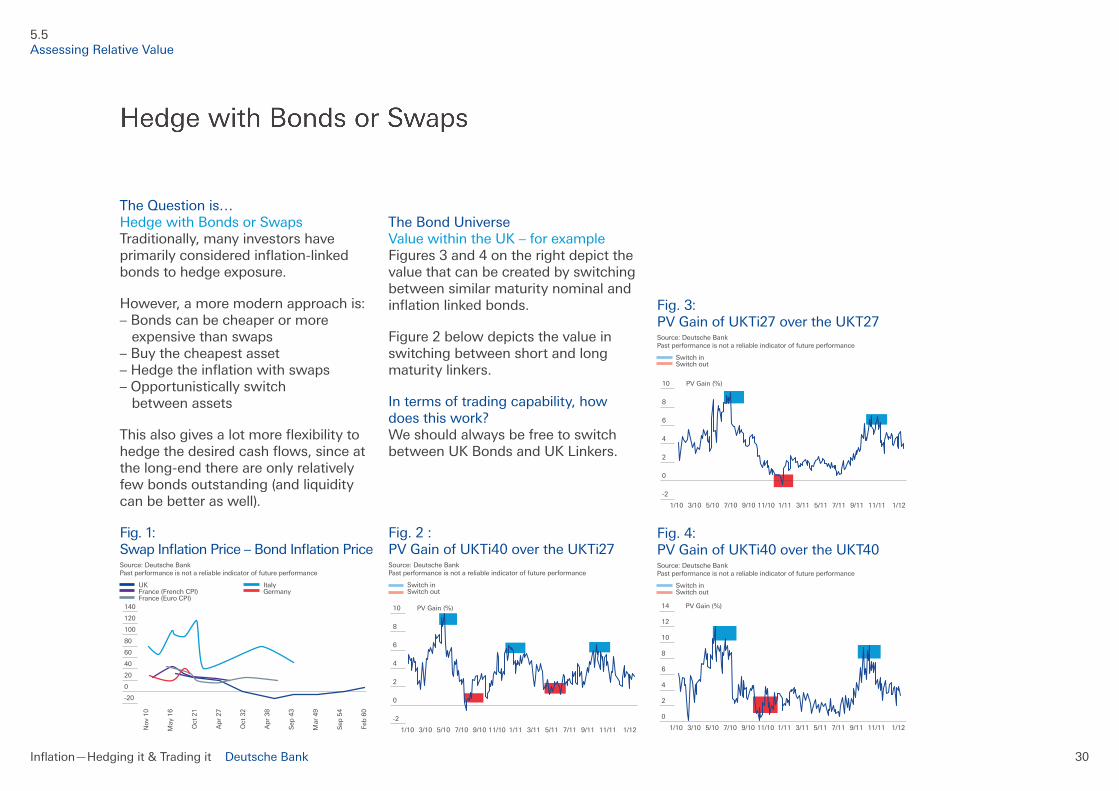

TheQuestionis… HedgewithBondsorSwaps Traditionally,manyinvestorshaveprimarilyconsideredinflation-linkedbonds to hedge exposure.

However,amoremodernapproachis: –Bondscanbecheaperormore expensivethanswaps –Buythecheapestasset –Hedgetheinflationwithswaps –Opportunisticallyswitch betweenassets

Thisalsogivesalotmoreflexibilitytohedgethedesiredcashflows,sinceatthelong-endthereareonlyrelativelyfewbondsoutstanding(andliquiditycanbebetteraswell).

Fig.1: SwapInflationPrice–BondInflationPrice Source:DeutscheBank Pastperformanceisnotareliableindicatoroffutureperformance

UK Italy France(FrenchCPI) Germany France(EuroCPI)

The Bond Universe ValuewithintheUK–forexample Figures3and4ontherightdepictthevaluethatcanbecreatedbyswitchingbetweensimilarmaturitynominalandinflationlinkedbonds.

Figure2belowdepictsthevalueinswitchingbetweenshortandlongmaturity linkers.

Intermsoftradingcapability,howdoesthiswork? WeshouldalwaysbefreetoswitchbetweenUKBondsandUKLinkers.

Fig.2: PVGainofUKTi40overtheUKTi27 Source:DeutscheBank Pastperformanceisnotareliableindicatoroffutureperformance

Switchin Switchout

Fig.3: PVGainofUKTi27overtheUKT27 Source:DeutscheBank Pastperformanceisnotareliableindicatoroffutureperformance

Switchin Switchout

Fig.4: PVGainofUKTi40overtheUKT40 Source:DeutscheBank Pastperformanceisnotareliableindicatoroffutureperformance

Switchin Switchout

5.5 Assessing Relative Value

Nov

10

May

16

Oct

21

Ap

r 27

Oct

32

Ap

r 38

Sep

43

Mar

49

Sep

54

Feb

60

40

20

0

60

80

120

100

140

-20

1/10 3/10 5/10 7/10 9/10 11/10 1/11 1/1211/119/115/11 7/113/11

2

-2

0

4

6

8

10 PV Gain (%)

1/10 3/10 5/10 7/10 9/10 11/10 1/11 1/1211/119/115/11 7/113/11

2

0

4

6

8

10

12

14 PV Gain (%)

1/10 3/10 5/10 7/10 9/10 11/10 1/11 1/1211/119/115/11 7/113/11

2

-2

0

4

6

8

10 PV Gain (%)

Inflation—Hedgingit&Tradingit Deutsche Bank 31

Tosumup… –Giventhedisplacementbetween inflationandnominalmarkets,there areopportunitiesforarbitrage –Assetswapspreadsonlinkers representapremiumforcreditthat ishardtoprice,andwhencoupled withdemand/supplyimbalancesand higherduration,theyofferapickup tonominalsforthesameunderlying issuer –Switchingbetweenequivalentrisk sovereigns/suprasovereignscan often,drivenbydynamicsofthe crosscurrencyswapsmarket, provideadditionalyieldpick-ups

–Thesedisplacementscanbe assessedbyavarietyofmetrics –Thevalueofswitchingisevident fromtheincrementalexcesspickup that is generated by selling the costlier asset to buy the cheapest assetfromtimetotime –Usedasasystematicstrategy this can yield substantial returns over medium term horizons –Theserepresentincredible opportunitiesfor‘asset-heavy’ investors,andthemarketswill likelynormalizewithtime,hence itisimportanttoactquickly

5.6 Assessing Relative Value

“Thereisn’toneriskfreecurve,thereare100,150,200…thekeyiswhendoyoupick‘thefruit’,whenisthebondcheapenough?” –DaraghMcDevitt, GlobalHeadofInflationStructuring

“…thereareincredibleopportunitiesforasset-heavyinvestors…itisimportanttoactquickly” –HaroonSana, GlobalHeadofRatesSales

Summary

6InflationOptions

InflationOptions Whoarethemajorplayersintheoptionsmarket? OptionProducts Whatarethetradingopportunities? Option Strategies Creating Optimal Hedges

Inflation—Hedgingit&Tradingit Deutsche Bank 33

Arelativelynewmarket,inflationoptionstradedbetweenEuropeandthe US have doubled every year since tradingstartedininflationswapsin2002/2003.2010sawaparticulargrowthspurt.

Longtermgrowthlookssettocontinueatthisexplosiverate,whichisclearlyindicativeofitsimportanceto clients and represents a substantial opportunity to DB as intermediary betweenbuyersandsellersofinflation.

Interbank volumes reached 50bn in 2010,upfrom13bnin2009,andjust1bn in 2005.

Fig.1: LondonOptionsVolumes Source:TullettPrebon

Fig.2: NYOptionsVolumes Source:TullettPrebon

6.1 InflationOptions

01

/09

03

/09

05

/09

07

/09

09

/09

11

/09

01

/10

03

/10

05

/10

07

/10

09

/10

11

/10

01

/11

03

/11

400

200

600

0

800

1,200

1,400

1,600

1,800 Volumes(millions)

01

/09

03

/09

05

/09

07

/09

09

/09

11

/09

01

/10

03

/10

05

/10

07

/10

09

/10

11

/10

01

/11

03

/11

1,000

2,000

0

3,000

4,000

5,000

6,000

7,000 Volumes(millions)

Inflation—Hedgingit&Tradingit Deutsche Bank 34

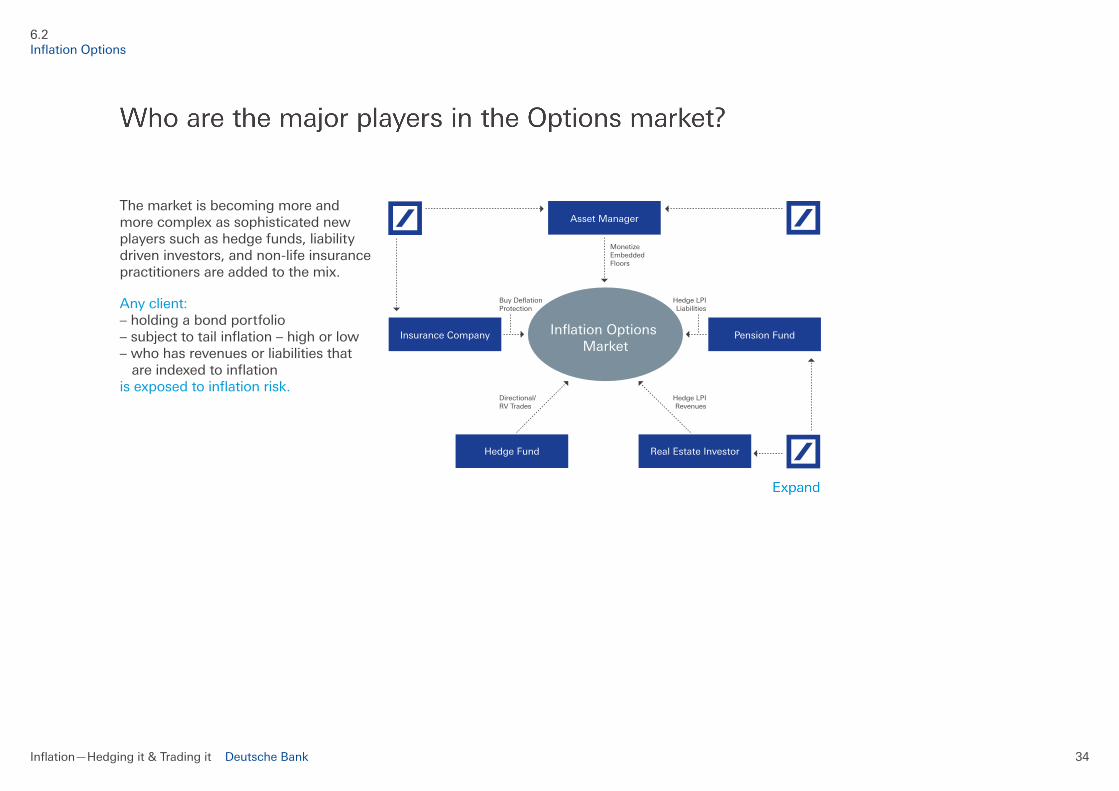

The market is becoming more and morecomplexassophisticatednewplayerssuchashedgefunds,liabilitydriveninvestors,andnon-lifeinsurancepractitioners are added to the mix.

Anyclient: –holdingabondportfolio –subjecttotailinflation–highorlow –whohasrevenuesorliabilitiesthat areindexedtoinflation isexposedtoinflationrisk.

6.2 InflationOptions

Hedge Fund Real Estate Investor

Asset Manager

Inflation Options Market

Insurance Company Pension Fund

Directional/RV Trades

Hedge LPIRevenues

Hedge LPILiabilities

Buy DeflationProtection

Monetize EmbeddedFloors

Inflation—Hedgingit&Tradingit Deutsche Bank 35

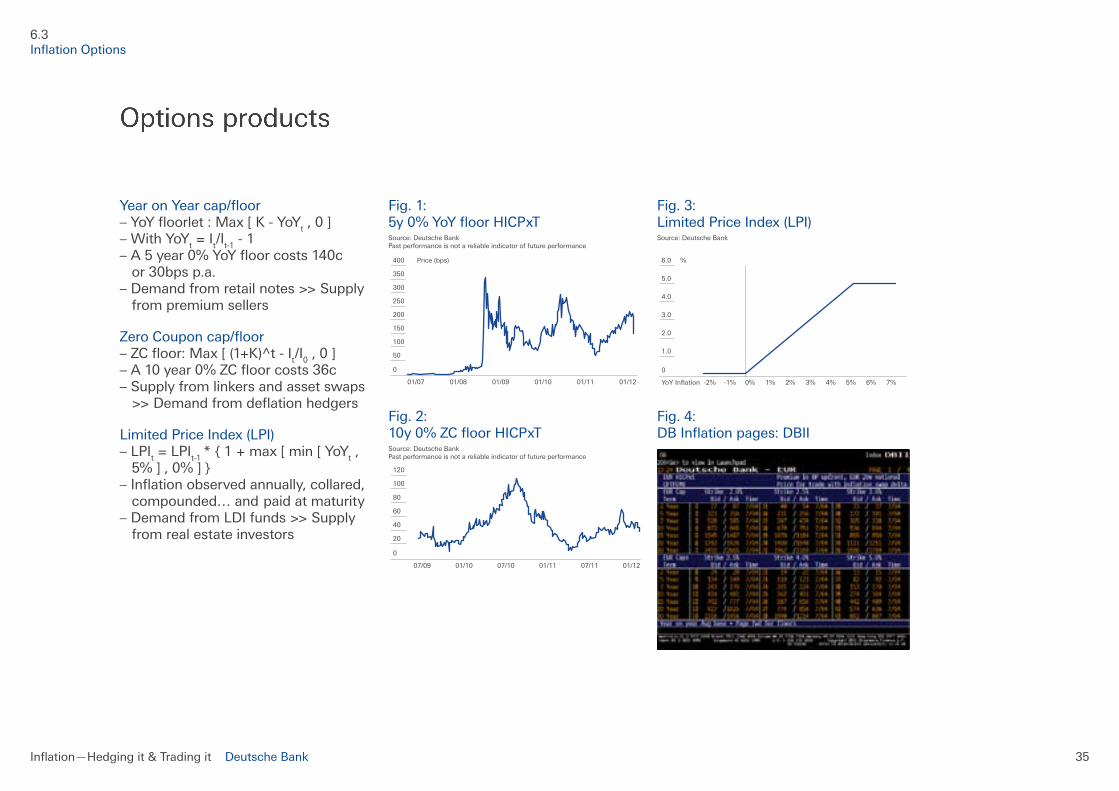

YearonYearcap/floor –YoYfloorlet:Max[K-YoYt,0] –WithYoYt=It/It-1-1 –A5year0%YoYfloorcosts140c or 30bps p.a. –Demandfromretailnotes>>Supply frompremiumsellers

ZeroCouponcap/floor –ZCfloor:Max[(1+K)^t-It/I0,0] –A10year0%ZCfloorcosts36c –Supplyfromlinkersandassetswaps >>Demandfromdeflationhedgers

LimitedPriceIndex(LPI) –LPIt=LPIt-1*{1+max[min[YoYt, 5%],0%]} –Inflationobservedannually,collared, compounded…andpaidatmaturity –DemandfromLDIfunds>>Supply fromrealestateinvestors

Fig.1: 5y0%YoYfloorHICPxT Source:DeutscheBank Pastperformanceisnotareliableindicatoroffutureperformance

Fig.2: 10y0%ZCfloorHICPxT Source:DeutscheBank Pastperformanceisnotareliableindicatoroffutureperformance

Fig.3: LimitedPriceIndex(LPI) Source:DeutscheBank

Fig.4: DBInflationpages:DBII

6.3 InflationOptions

07/09 01/10 07/10 01/11 07/11 01/12

40

20

60

80

0

100

120

-2%YoY Inflation -1% 0% 1% 2% 3% 4% 5% 6% 7%

1.0

2.0

0

3.0

4.0

5.0

6.0 %

01/07 01/08 01/09 01/10 01/11 01/12

100

50

150

200

0

250

300

350

400 Price (bps)

Inflation—Hedgingit&Tradingit Deutsche Bank 36

LPICollarsrepresentsagreatinflation-hedging alternative InflationriskforPensionfundsandotherliability-driveninvestorsisbig, 20–30%ofschemerisk.

Breakevensaredeemedexpensive:if,forexample,breakevenis3.7%andtheschemeexpectedinflationof2.8%,hedginglosesvalue(figure1).

What’sthesolution? Coverinflationriskbycreatinganinflationcollar –PayLPI –ReceiveRPI

Experthistoricalperspective MarkusHeider,responsibleforEuropeaninflationresearchatDBGlobalMarketsResearch,providesausefullongtermperspective:thisgraphshowshowthevolatilitywehaveseen in the last three years is nothing compared to the last 200 years. In the longrun,inflationisaveryvolatileentity,whichmeansriskandtherefore,opportunity.

Therelativestabilitywe’veseeninthelast20yearscanveryquicklychange.

Significantriskfactorscurrentlyincludegovernmentswithunsustainabledeficitsandglobalisation;theneedtohedgeinflationriskisbecomingincreasingly relevant.

Fig.1: Assumed Constant Year on Year InflationReturn Source:DeutscheBank

RPIZCSwap 100%LPICollar

Fig.2: Consumerpriceinflation,y/y%,11-yrMA Source:EHNet

UK US

1. USwarofIndependence 2. NapoleonicWarsdeficitmonetised 3. 1stIndustrialRevolution:productivity-leddeflation 4. US Civil War 5. 2ndIndustrialRevolution:productivityrebounds;goldfinds 6. FiscalmonetisationduringWWI 7. GreatDepression 8. FiscalmonetisationduringWWII 9. FiscalmonetisationduringVietnamWar;oilshocks 10.Volckerclampsdownoninflation

6.4 InflationOptions

-2%-3%-4% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8%

-30

40

50

30

20

10

0

-10

-20

Payoff

30y Breakeven3.55%

180017751750 1825 1850 1875 1900 1925 1950 1975 2000

-10

15

10

5

0

-5

2

3

4

5

6

7

8

9

10

1

“The catalyst that makes this trade workisinflationatabove5%–this5%strikeiscurrentlylowerthanspotinflation–achangefromthelastfiveyears” –NicolasTabardel, GlobalHeadofInflationVolatility andExotics

Inflation—Hedgingit&Tradingit Deutsche Bank 37

MarketvsEconomistExpectations UKRPIfutureinflation:themarketin the long term is pricing much moredownsideriskthanupsiderisk.IntheUK,therisksofinflationovershooting are much higher than them undershooting. This is contrary to whatweseeinothermarkets.

InEuropeandtheUS,thereismorebalance; caps are becoming more muchmoreexpensivethanfloors.

Consensus economist predictions indicate that market implied volatility istoohigh;tailsaretoofatandtheskewistoodeep.CapshavenonaturalsupplyinEuropeortheUSsothetailriskisalwaysexpensive(figure1).

InEurope,volatilityistoohigh,tailsaretoofat,andtheskewistoosteep.

Whatdoesthismean? Sellingvolatilitynowisagoodidea.

Theskewwaspricingfloorshigherthancaps;theskewisnowsymmetric(figure2).

Fig.1: Skewpricesfloorshigherthancaps Source:DeutscheBank

SPFprobdistributionfor5yinflforecast MarketImpliedProbabilityfromEURYoYcaps/floors 1. Deflationriskisoverpriced 2. Consensus economist predictions imply market implied volatility is too high 3. ‘FatTails’

Fig.2: Ratioofmarketimpliedprobabilityvs.EconomistExpectations Source:DeutscheBank

6.4 InflationOptions

0

25

30

35

20

15

10

5

<0 0 - 0.5 1.0 - 1.5 2.0 - 2.5 3.0 - 3.5 >4

%

0

25

20

15

10

5

<0 0 - 0.5 0.5 - 1 1 - 1.5 1.5 - 2

Inflation Print (%)

Value in selling ‘wings’distribution i.e. far out ofthe money caps and floor

2 - 2.5 2.5 - 3 3 - 3.5 3.5 - 4 >4

30

“Tail risk continues to remain overpricedwithbothtailsalmostequallyflat,reflectingthehighuncertaintyovertheinflation/deflationdebate” –NicolasTabardel, GlobalHeadofInflationVolatility&Exotics

Inflation—Hedgingit&Tradingit Deutsche Bank 38

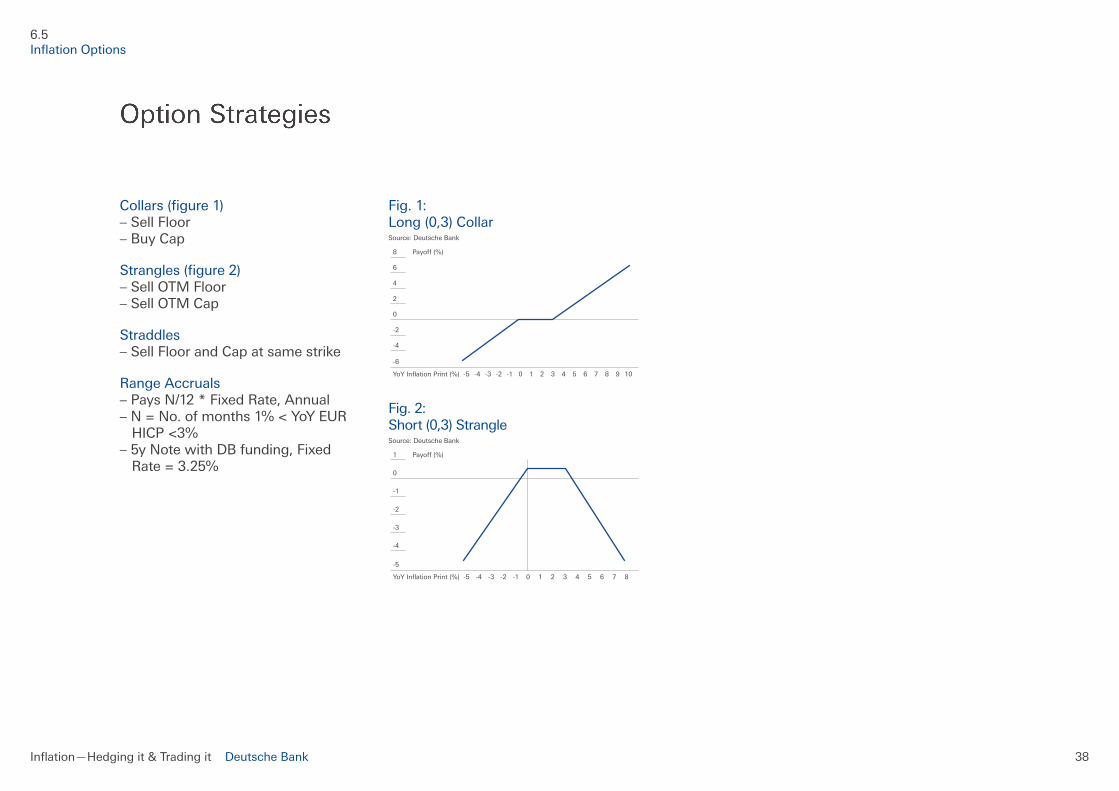

Collars(figure1) –SellFloor –BuyCap

Strangles(figure2) –SellOTMFloor –SellOTMCap

Straddles –SellFloorandCapatsamestrike

Range Accruals –PaysN/12*FixedRate,Annual –N=No.ofmonths1%<YoYEUR HICP<3% –5yNotewithDBfunding,Fixed Rate=3.25%

Fig.1: Long(0,3)Collar Source:DeutscheBank

Fig.2: Short(0,3)Strangle Source:DeutscheBank

6.5 InflationOptions

-6

8

6

4

2

0

-2

-4

-5 -3 -2-4 -1 1 20 3 654 7 8 9 10

Payoff (%)

YoY Inflation Print (%)

-5

1

0

-1

-2

-3

-4

-5 -3 -2-4 -1 1 20 3 654 7 8

Payoff (%)

YoY Inflation Print (%)

Inflation—Hedgingit&Tradingit Deutsche Bank 39

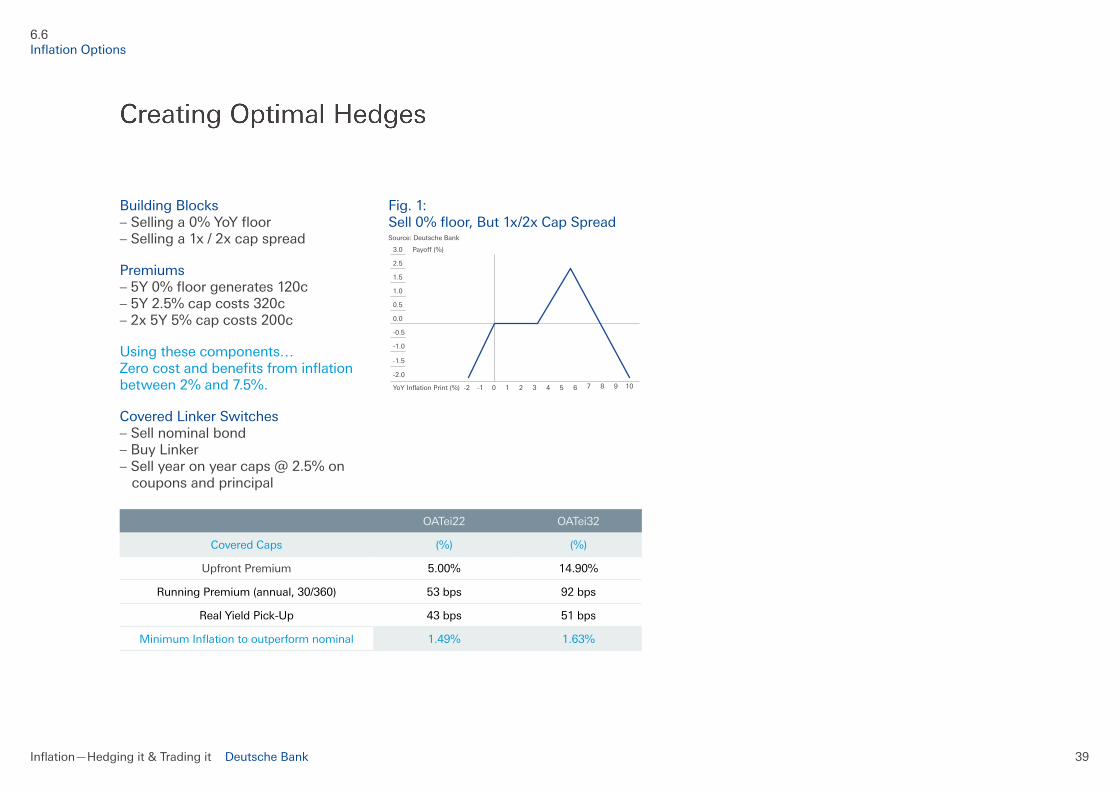

Building Blocks –Sellinga0%YoYfloor –Sellinga1x/2xcapspread

Premiums –5Y0%floorgenerates120c –5Y2.5%capcosts320c –2x5Y5%capcosts200c

Usingthesecomponents… Zerocostandbenefitsfrominflationbetween2%and7.5%.

CoveredLinkerSwitches –Sellnominalbond –BuyLinker –Sellyearonyearcaps@2.5%on coupons and principal

OATei22 OATei32

Covered Caps (%) (%)

UpfrontPremium 5.00% 14.90%

RunningPremium(annual,30/360) 53 bps 92 bps

RealYieldPick-Up 43 bps 51 bps

MinimumInflationtooutperformnominal 1.49% 1.63%

Fig.1: Sell0%floor,But1x/2xCapSpread Source:DeutscheBank

6.6 InflationOptions

-1.5

3.0

1.5

2.5

1.0

-2.0

0.5

0.0

-0.5

-1.0

-2 -1 1 20 3 654 7 8 9 10

Payoff (%)

YoY Inflation Print (%)

7DeflationTailRisk

DeflationTailRisk:DB5YearNote

Inflation—Hedgingit&Tradingit Deutsche Bank 41

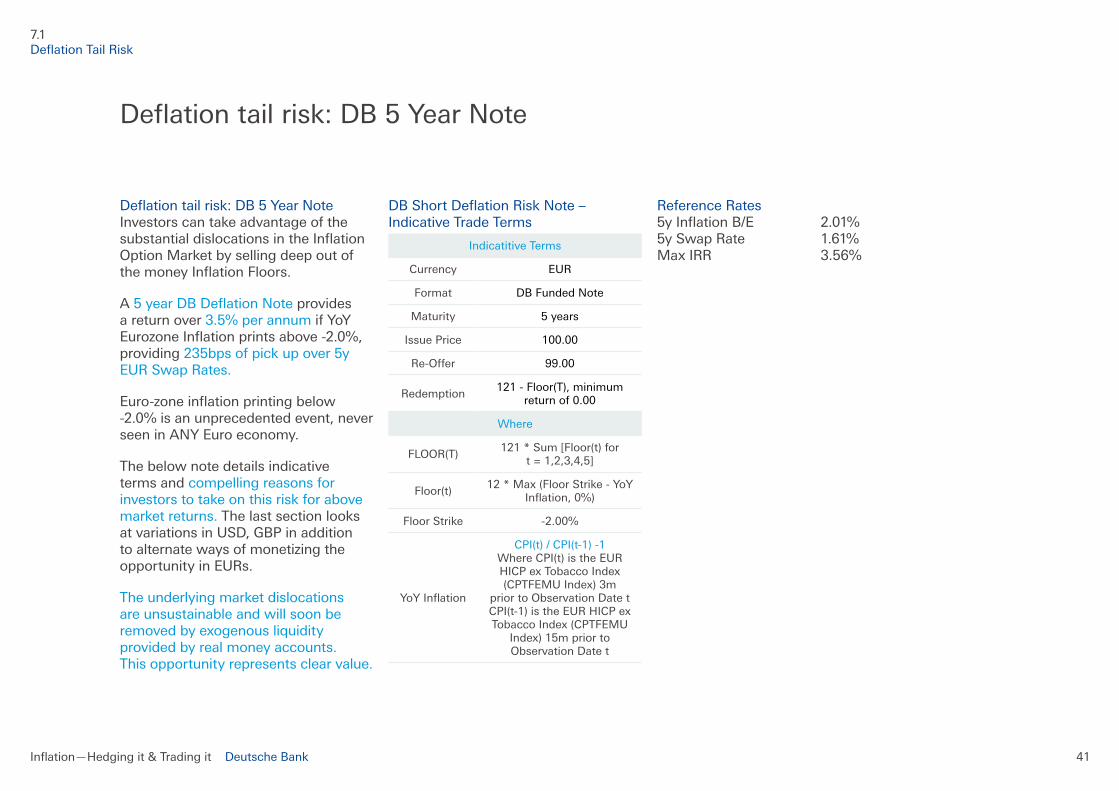

Deflationtailrisk:DB5YearNote InvestorscantakeadvantageofthesubstantialdislocationsintheInflationOptionMarketbysellingdeepoutofthemoneyInflationFloors.

A 5yearDBDeflationNote provides a return over 3.5%perannumifYoYEurozoneInflationprintsabove-2.0%,providing 235bpsofpickupover5yEURSwapRates.

Euro-zoneinflationprintingbelow-2.0%isanunprecedentedevent,neverseeninANYEuroeconomy.

Thebelownotedetailsindicativeterms and compellingreasonsforinvestorstotakeonthisriskforabovemarket returns. The last section looks atvariationsinUSD,GBPinadditiontoalternatewaysofmonetizingtheopportunityinEURs.

The underlying market dislocations areunsustainableandwillsoonberemovedbyexogenousliquidityprovided by real money accounts. This opportunity represents clear value.

DBShortDeflationRiskNote–Indicative Trade Terms

Indicatitive Terms

Currency EUR

Format DBFundedNote

Maturity 5 years

IssuePrice 100.00

Re-Offer 99.00

Redemption121-Floor(T),minimum

returnof0.00

Where

FLOOR(T)121*Sum[Floor(t)for

t=1,2,3,4,5]

Floor(t)12*Max(FloorStrike-YoY

Inflation,0%)

FloorStrike -2.00%

YoYInflation

CPI(t)/CPI(t-1)-1 WhereCPI(t)istheEURHICPexTobaccoIndex(CPTFEMUIndex)3m

prior to Observation Date t CPI(t-1)istheEURHICPexTobaccoIndex(CPTFEMU

Index)15mpriortoObservation Date t

ReferenceRates 5yInflationB/E 2.01% 5ySwapRate 1.61% MaxIRR 3.56%

7.1 DeflationTailRisk

Deflationtailrisk:DB5YearNote

8CaseStudy:Zero-CouponOptionTrade

Inflation—Hedgingit&Tradingit Deutsche Bank 43

Duringthefirstsixmonthsof2010,aToronto-basedinsurerpurchaseddeflationprotectionworth$21.539billioninnotional,paying$173.7millioninpremium.The10-yearzero-coupon0%optionsweredenominatedindollars,eurosandsterling,andwereexecuted by Deutsche Bank and Citi.

TheothersideofthetradewaslargelytakenbyCalifornia-basedfixed-incomemanagerPimco,whichreportedithadsoldmorethan$8billionof10-yearzero-coupon0%inflationfloorsinafilingdatedAugust27.Thefloorsweresoldinreturnformorethan$70millioninpremium,withDeutscheandCitiascounterparties.

Thetransactionmadeperfectsenseforbothparticipants.Fortheinsurer,the0%floorsactedasahedgeagainstdeflationandtheimpactthatwouldhaveonitsequityportfolio.Atthesametime,Pimcowasabletocashinon0%inflationfloorsembeddedinitssizableportfolioofTreasuryinflation-protectedsecurities(Tips).Dealerssaythe headlines generated by the trade hadapositiveimpactonthemarket,encouraging other clients to express

theirviewsonthedirectionofinflationbybuyingorsellingzero-couponoptions.

DaraghMcDevitt,DBGlobalHeadofInflationStructuringsaid,“Itsparkedinterest because you have very intelligentinvestorsonbothsideswhoaretakingoppositesidesofthetrade.”

SinceQ2,2010,quantitativeeasinghas encouraged more clients to sell impliedinflationvolatilityatlevelsthatlookexpensive.Inparticular,manymarket players have looked to play inflationvolatilityversusinterestratevolatility–forexample,bybuyinginterestratecapsandsellinginflationcaps at similar strikes. “We’ve seen a lotofclientscominginonthesamesideasPimco,viewingtheprobabilityofdeflationpricedinbytheseoptionstobeinflated.Theyareeithersellingthe options embedded in their bond portfolios,sellingtheoptionsoutrightorenteringintosomekindofinterestrateoptionsstrategy,”saysMcDevitt.

Thetransactionmadeperfectsenseforbothparticipants.Fortheinsurer,the0%floorsactedasahedgeagainstdeflationandtheimpactthatwouldhaveonitsequityportfolio.Atthesametime,Pimcowasabletocashinon0%inflationfloorsembeddedinitssizableportfolioofTreasuryinflation-protected securities.

8.1 Case Study

CaseStudy:Zero-CouponOptionTrade

Inflation—Hedgingit&Tradingit Deutsche Bank 44

9FurtherReading

Inflation—Hedgingit&Tradingit Deutsche Bank 45

InflationHedgingforInstitutionalInvestors Examiningdynamicassetallocationstrategiesforhighinflationscenariosandtheeffectoffinancialmarketchangesoninflationhedginginstruments.

WeeklyInflationResearchupdate

ResearchInflationMarketsGuide

InflationBigPictureStudy

Pleasegotogm.db.com/inflationformoreinformation.

9.1 FurtherReading

FurtherReading

Examining dynamic asset allocation

strategies for high inflation scenarios and

the effect of financial market changes on

inflation hedging instruments

INFLATION HEDGING FOR

INSTITUTIONAL INVESTORS

PU

BL

ISH

ED

BY

ALSO SPONSORED BY

MEDIA PARTNERS

JUNE | 2011

CLEAR PATH ANALYSIS IN PARTNERSHIP WITH

Global

7 October 2011

DB Inflation Report

Weekly Inflation Update

Deutsche Bank AG/London

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 146/04/2011.

Strategy Update

Change in breakevens, US & UK

-10

-5

0

5

10

15

20

25

30

2y 5y 10y 30y 2y 5y 10y 30y

1W change in BEI

carry adjusted

GBP USD

Change in breakevens, EUR & FRF

-10

-5

0

5

10

15

20

2y 5y 10y 30y 2y 5y 10y 20y

1W change in BEI

carry adjusted

EUR FRF

ILB rich/cheap vs nominals

-20

0

20

40

60

80

100

120

2012 2017 2023 2028 2034 2039 2045

GBP DEM

USD FRF

ITL

Rich (-) / cheap (+) vs nominal curve

Source: Deutsche Bank

Upcoming data

Mkt Indicator Date, GMT

FRF CPI Sep 12 Oct, 05:30

DEM CPI Sep 13 Oct, 06:00

EUR HICP Sep 14 Oct, 09:00

Research Team

Markus Heider (+44) 20 754-52167 [email protected]

Alex Li (1) 212 250-5483 [email protected]

Vanshree Verma (+44) 20 754-77583 [email protected]

Mac

ro

Glo

bal

Mar

kets

Res

earc

h

Economics: This week’s PPI data point to further upward pressure on UK and euro area consumer core inflation in the coming months. Business survey price balances have continued to fall in September however, which is consistent with the view that CPI inflation will slow in 2012.

Global: 10y EUR real rates look too high relative to USD against the recent data divergence. We prefer long-end TIPS and UKTi B/Es over OATei.

EUR: The ongoing deterioration in economic data remains challenging for B/Es. In RV, we prefer the 10y sector and the DBRei-20 in particular.

GBP: While real yield valuations are challenging, the scheduled new 50y linker issue should look attractive relative to nominal gilts (in B/E and ASW), RPI swaps and B/Es in other markets.

USD: Forward TIPS B/Es have diverged from survey-based measures of inflation expectations, although declines may be exaggerated by liquidity factors.

AUD: In our view, the market is underpricing inflation risk over the short term, with the gap between RBA inflation expectations and breakevens extremely wide. Our preferred trade is long the belly in 2y/5y/10y ZCS B/E butterfly.

Asia: Inflation in Thailand & South Korea fell more than expected in September, supporting our expectations of no policy rate change at the next CB meeting.

Inflation Markets Bond Yld BEI 1M fwd ASW ASW

discnt ZC Rate Sprd

ZC-BEICPI/RPI

fcst

US CPI

TII Apr-16 -0.65 1.53 1.51 -18 14 5y 1.87 34 spot 3.8

TII Jan-21 0.05 1.83 1.82 13 31 10y 2.30 48 Dec-11 2.9

TII Feb-41 0.90 2.02 2.02 76 54 30y 2.54 52 Jun-12 1.7

EA HICPxt

DBRei 16 -0.22 1.24 1.16 -65 20 5y 1.69 45 spot 2.5

DBRei 20 0.31 1.40 1.36 -48 26 10y 1.84 44 Dec-11 2.7

OATei 40 1.44 2.07 2.06 109 39 30y 2.11 4 Jun-12 1.8

FR CPIxt

BTANi-16 0.23 1.52 1.47 21 39 5y 1.88 36 spot 2.2

OATi-19 0.68 1.68 1.65 37 35 10y 2.07 39 Dec-11 2.1

OATi-29 1.29 2.10 2.09 98 37 20y 2.18 7 Jun-12 1.5

UK RPI

UKTi-16 -1.52 2.86 2.76 -31 15 5y 3.11 26 spot 5.2

UKTi-22 -0.37 2.80 2.76 9 32 10y 3.21 41 Dec-11 5.0

UKTi-40 0.18 3.15 3.14 44 33 30y 3.50 35 Jun-12 3.7Source: Deutsche Bank

Global

1 March 2011

Global Macro Issues Issues in Inflation

Deutsche Bank AG/London

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Economics

Research Team

Markus Heider (+44) 20 754-52167 [email protected]

Mac

ro

Glo

bal

Mar

kets

Res

earc

h

Eco

no

mic

s

Abstract

The uncertainty about the longer-term inflation outlook has risen substantially since the onset of the financial crisis in 2008. After 15 years or more of low and stable inflation, professional forecasters, investors and indeed central banks themselves now consider below and above target outcomes as possible, even probable. The non-standard reaction of economic policy during the crisis, the discussion about potential changes to monetary policy objectives, the run-up in public debt, but also apparent changes to the inflation process itself during the Great Moderation as well as the open inflation implications of structural trends like globalisation all have contributed to the rise in uncertainty. In this note we look at some of the main issues surrounding the inflation outlook and conclude that inflation risks for the coming years seem to be skewed to the upside of central bank targets.

March 2011

Global Inflation Markets

A guideMarkus [email protected]

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges i R t Bl b d th d D t i d f D t h B k d bj t i D t h B k d d kvia Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks

to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

10Contacts

Inflation—Hedgingit&Tradingit Deutsche Bank 47

Sales

Haroon Sana [email protected] +442075473671

MatthewYencken [email protected] +31282582010

Michael Durr [email protected] +442075473671

MatthewBlackwell [email protected] +6568831620

EdRubin [email protected] +12122500551

Tai-ZhongJiang(Tai-Chu) [email protected] +81351566186

Structuring

Daragh McDevitt [email protected] +442075452750

XavierAvila [email protected] +442075472731

Research

Markus Heider [email protected] +44207542167

AlexLi [email protected] +12122505483

Trading

Stephane Salas [email protected] +442075478809

AllanLevin [email protected] +12122507105

Katsuya Miyoshi [email protected] +81351566205

LionelArbey [email protected] +442075454941

Vaughan Harvey [email protected] +61282581848

Integratedsales,trading,structuring and research Unlikesomeofourcompetitors,DeutscheBank’sinflationsales,trading,structuringandresearchprofessionalsworkcloselytogether,combiningstrategicandtechnicalexpertisewiththemacro-economicinsightssoimportantwiththisoffering.

10.1 Contacts

Contacts–DeutscheBankGlobalInflationTeam

ThisdocumentisintendedfordiscussionpurposesonlyanddoesnotcreateanylegallybindingobligationsonthepartofDeutscheBankAGand/oritsaffiliates(“DB”).Withoutlimitation,thisdocumentdoesnotconstituteanoffer,aninvitationtoofferorarecommendationtoenterintoanytransaction.Whenmakinganinvestmentdecision,youshouldrelysolelyonthefinaldocumentationrelatingtothetransactionandnotthesummarycontainedherein.DBisnotactingasyourfinancialadviserorinanyotherfiduciarycapacitywithrespecttothisproposedtransaction.Thetransaction(s)orproducts(s)mentionedhereinmaynotbeappropriateforallinvestorsandbeforeenteringintoanytransactionyoushouldtakestepstoensurethatyoufullyunderstandthetransactionandhavemadeanindependentassessmentoftheappropriatenessofthetransactioninthelightofyourownobjectivesandcircumstances,includingthepossiblerisksandbenefitsofenteringintosuchtransaction.Forgeneralinformationregardingthenatureandrisksoftheproposedtransactionandtypesoffinancialinstrumentspleasegotohttp://www.globalmarkets.db.com/riskdisclosureswww.globalmarkets.db.com/riskdisclosures.Youshouldalsoconsiderseekingadvicefromyourownadvisersinmakingthisassessment.IfyoudecidetoenterintoatransactionwithDB,youdosoinrelianceonyourownjudgment.Theinformationcontainedinthisdocumentisbasedonmaterialwebelievetobereliable;however,wedonotrepresentthatitisaccurate,current,complete,orerrorfree.Assumptions,estimatesandopinionscontainedinthisdocumentconstituteourjudgmentasofthedateofthedocumentandaresubjecttochangewithoutnotice.Anyprojectionsarebasedonanumberofassumptionsastomarketconditionsandtherecanbenoguaranteethatanyprojectedresultswillbeachieved.Pastperformanceisnotaguaranteeoffutureresults.ThismaterialwaspreparedbyaSalesorTradingfunctionwithinDB,andwasnotproduced,reviewedoreditedbytheResearchDepartment.AnyopinionsexpressedhereinmaydifferfromtheopinionsexpressedbyotherDBdepartmentsincludingtheResearchDepartment.SalesandTradingfunctionsaresubjecttoadditionalpotentialconflictsofinterestwhichtheResearchDepartmentdoesnotface.DBmayengageintransactionsinamannerinconsistentwiththeviewsdiscussedherein.DBtradesormaytradeasprincipalintheinstruments(orrelatedderivatives),andmayhaveproprietarypositionsintheinstruments(orrelatedderivatives)discussedherein.DBmaymakeamarketintheinstruments(orrelatedderivatives)discussedherein.SalesandTradingpersonnelarecompensatedinpartbasedonthevolumeoftransactionseffectedbythem.Thedistributionofthisdocumentandavailabilityoftheseproductsandservicesincertainjurisdictionsmayberestrictedbylaw.Youmaynotdistributethisdocument,inwholeorinpart,withoutourexpresswrittenpermission.DBSPECIFICALLYDISCLAIMSALLLIABILITYFORANYDIRECT,INDIRECT,CONSEQUENTIALOROTHERLOSSESORDAMAGESINCLUDINGLOSSOFPROFITSINCURREDBYYOUORANYTHIRDPARTYTHATMAYARISEFROMANYRELIANCEONTHISDOCUMENTORFORTHERELIABILITY,ACCURACY,COMPLETENESSORTIMELINESSTHEREOF.DBisauthorisedunderGermanBankingLaw(competentauthority:BaFin-FederalFinancialSupervisingAuthority)andregulatedbytheFinancialServicesAuthorityfortheconductofUKbusiness.Thisdocumentisintendedfordiscussionpurposesonly.Youmaynotdistributethisdocument,inwholeorinpart,withoutexpresswrittenpermission.Withoutlimitation,thisdocumentdoesnotconstituteanoffer,aninvitationtoofferorarecommendationtoenterintoanytransaction.Theinformationcontainedinthisdocumentisbasedonmaterialwebelievetobereliable;however,wedonotrepresentthatitisaccurate,current,complete,orerrorfree.Assumptions,estimatesandopinionscontainedinthisdocumentconstituteourjudgmentasofthedateofthedocumentandaresubjecttochangewithoutnotice.Anyprojectionsarebasedonanumberofassumptionsastomarketconditionsandtherecanbenoguaranteethatanyprojectedresultswillbeachieved.Pastperformanceisnotaguaranteeoffutureresults.TheservicesdescribedinthisdocumentareprovidedbyDeutscheBankAGorbyitssubsidiariesand/oraffiliatesinaccordancewithappropriatelocallegislationandregulation.DeutscheBankSecuritiesInc.,asubsidiaryofDeutscheBankAG,conductsinvestmentbankingandsecuritiesactivitiesintheUnitedStates.DeutscheBankSecuritiesInc.isamemberofNYSE,FINRAandSIPC.Investmentsaresubjecttoinvestmentrisk,includingmarketfluctuations,regulatorychange,counterpartyrisk,possibledelaysinrepaymentandlossofincomeandprincipalinvested.Thevalueofinvestmentcanfallaswellasriseandyoumightnotgetbacktheamountoriginallyinvestedatanypointintime.©CopyrightDeutscheBankAG2012