inflation inflation foreign investments foreign investments central banks had $billions in reserves...

TRANSCRIPT

• Inflation Inflation • Foreign investmentsForeign investments• Central banks had $billions in reservesCentral banks had $billions in reserves• NAFTA took effect early 1994NAFTA took effect early 1994

Due to policy reforms and NAFTA, a lot of capital ($102 billion from 1990-1994) was flowing into Mexico making the peso appreciate in value.

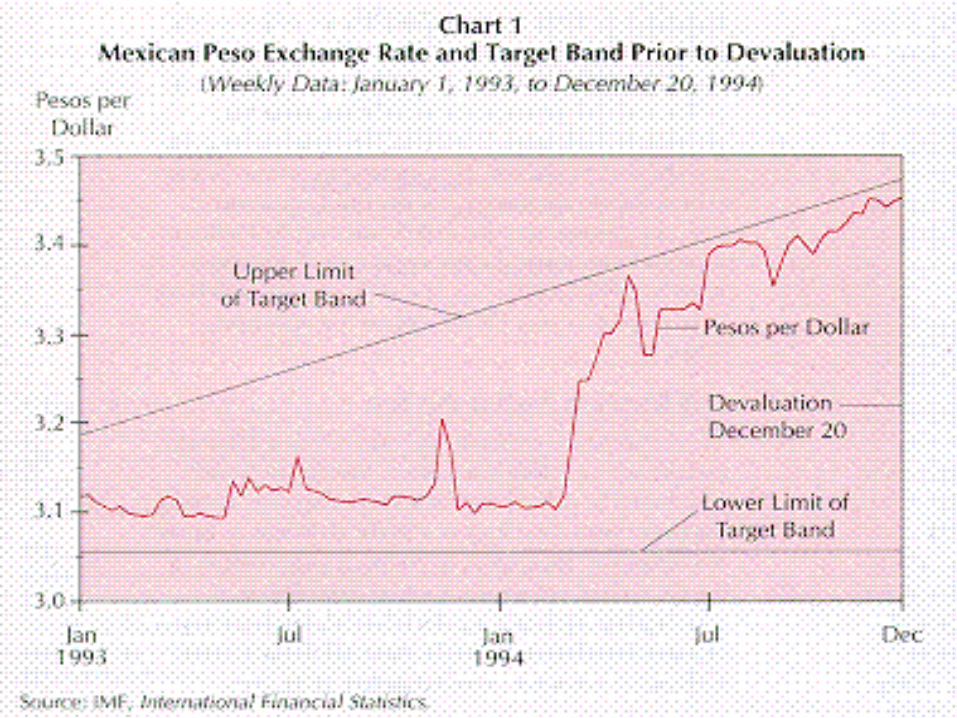

• The Mexican government kept the value of the peso within a crawling peg exchange rate with the USD. The exchange rate was controlled within a narrow target band whose upper limit was raised bit by bit for gradual nominal depreciation.

• But in real, price adjusted terms the peso was appreciating, contributing to the current account deficit

• Thus the peso became overvalued, meaning the exchange rate became too high for a sustainable equilibrium in the balance of payments.

• Higher interest rates (which causes external debt to rise even more) are needed to prop up an overvalued currency until the inevitable devaluation takes place.

• BUT…

CAUSES OF THE CRISIS

1. Political shocks*Elections

2. Rise in U.S. interest rates3. Shift from cetes tesobonos

Elections• Because of an upcoming presidential election on August 21, 1994, political

developments caused an increase in Mexico’s risk premium () due to increases in default risk and exchange rate risk: These events put downward pressure on the value of the peso, Mexico’s central bank had promised to maintain the fixed exchange rate, To do so, it sold dollar denominated assets, decreasing the money supply and increasing interest rates, To do so, it needed to have adequate reserves of dollar denominated assets. Did it?

The choices open to them were to:• raise interest rates even more to bring back capital inflow• reduce government expenditures to reduce domestic demand, decrease

imports and relieve pressure on the peso• devalue the peso to make exports more competitiveThe first two options were unattractive because they could have led to a

significant downturn in economic activity and could have further weakened Mexico’s banking system. Devaluing the peso would have undermined its commitment to maintaining a stable exchange rate – the basis of its success in attracting foreign capital.

• Because of an upcoming presidential election on August 21, 1994, political developments caused an increase in Mexico’s risk premium () due to increases in default risk and exchange rate risk: These events put downward pressure on the value of the peso, Mexico’s central bank had promised to maintain the fixed exchange rate, To do so, it sold dollar denominated assets, decreasing the money supply and increasing interest rates, To do so, it needed to have adequate reserves of dollar denominated assets. Did it?

The choices open to them were to:• raise interest rates even more to bring back capital inflow• reduce government expenditures to reduce domestic demand, decrease

imports and relieve pressure on the peso• devalue the peso to make exports more competitiveThe first two options were unattractive because they could have led to a

significant downturn in economic activity and could have further weakened Mexico’s banking system. Devaluing the peso would have undermined its commitment to maintaining a stable exchange rate – the basis of its success in attracting foreign capital.

Political Shocks

The Central Bank blamed a series of assassinations and other discouraging acts that political risk and investor confidence.

Banco de México had tried increasing domestic interest rates (from 10.1 % to 17.8% in March) on short-term (91-day), peso-denominated Mexican government bonds (cetes) in an attempt to stem the outflow of capital. Didn’t work. Investors too scared of an upcoming devaluationIn response to these investor concerns, the Mexican government issued large amounts of short-term, dollar-denominated bonds (tesobonos). Now any devaluation would be the government’s problem.Super vulnerable to a financial market crisis; its foreign exchange reserves had fallen to $12.9 billion,18 while it had tesobono obligations of $28.7 billion maturing in 1995.

March 1994

June/July 1994

September 1994

December 1994

Reserves $11 billion in four weeks

Reserves $2.5 billion in three weeks

Reserves $4 billion

Reserves $1.5 billion in three days

Shift from cetes tesobonos

Rise in U.S. interest rates

• In February 1994, the Federal Reserve raised its federal funds rate target because of inflationary pressures.

• The Mexican government thought it was only temporary and made no substantial policy changes.

Monetary and Fiscal Expansion Under a Fixed Exchange Rate

When the central bank buys and sells foreign assets to keep the exchange rate fixed and to maintain domestic interest rates equal to foreign interest rates, it is not able to adjust domestic interest rates to attain other goals.

In particular, monetary policy is ineffective in influencing output and employment.

A fiscal expansion increases aggregate demand

To prevent the domestic currency from appreciating, the central bank buys foreign assets, increasing the money supply and decreasing interest rates.

RESERVES

CURRENT ACCOUNT

During the Crisis• Maintain Salina’s popularity• Polarization of income and increased

poverty• Mass industrial layoffs• Dec 20: 15% devaluation of the peso• Dec 22: Mexican Gov. forced to let

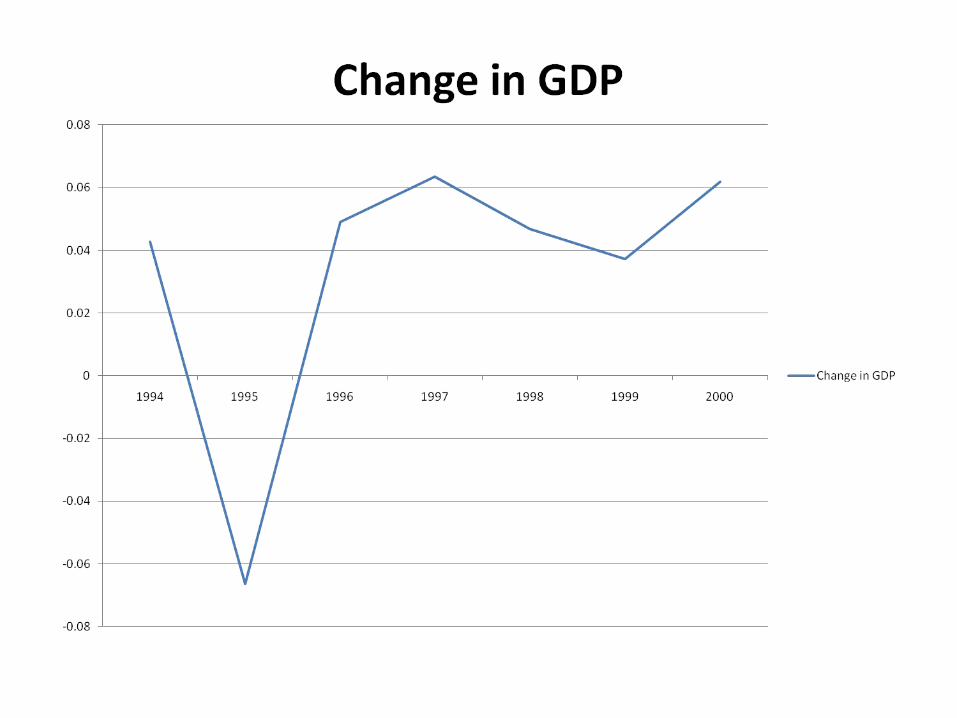

peso float• GDP contracted approx 7.2%

Unemployment

GDP

International Effects• Tequila Effect• Contagion: Similar macroeconomic conditions and

economic policies– Argentina– Philippines

Solving the Mexican Peso Crisis

• People were skeptical about helping Mexico in fear of causing moral hazard

• Initial line of credit proposal of $18 billion (half U.S, half other large institutions)

• On January 12, a second proposal of a $40 billion line of credit created by Clinton Adm.

• On January 31, they proposed a direct loan package of 20 billion provided by the U.S, 18 Billion from the IMF and $13 billion from the Bank of International Settlement

What Happened to Mexico?

• Peso weakened nonetheless and bottomed out at 7.45 pesos per U.S dollar

• Prices increased 30% in 1995 alone• Household income declined by 30%• Extreme poverty doubled• Stringent austerity helped peso regain its

strength

Mexico’s social expenditure as a per cent of GDP (UNICEF)

Mexico’s biggest mistake?

• Mexican could have avoided such a large crisis if they would have let the exchange rate float before December

• There may have still been a recession but a crisis could still have been avoided