informalitylac_oxford2016

TRANSCRIPT

Informality in Latin America:

Taxes and beyond

Angel Melguizo

Latin American Unit, OECD Development Centre

III CAF-Oxford Conference Understanding the

Challenges of Informality in Latin America

St Antony’s College, University of Oxford - Nov 4, 2016

Did informality decrease during the

commodity boom? – Yes, but not enough

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

BOL

NIC

PER

HON

PRY

GUA

SLV

MEX

COL

DOM

VEN

ECU

ARG

PAN

BRA

CRI

CHL

URY

Formality in LAC (% contributors/workers)

2006

2014

Source: Mejia, C. and A. Melguizo (2016), “La reforma de las pensiones en América Latina: acuerdos de partida,

principios, instrumentos e indicadores”. In Carranza, Melguizo and Tuesta (eds.), Ideas para reforma de

pensiones. Forthcoming.

Lauenburg, 1890

Macondo Por Hernando Nossa

• Informal is normal in Latin America

• Latin American hour: Productivity, inclusion and

governance

• Taxes and informality: in it together?

• Beyond taxes: a way forward

Informality in Latin America: Taxes and

beyond

• Informal is normal in Latin America

• Latin American hour: Productivity, inclusion and

governance

• Taxes and informality: in it together?

• Beyond taxes: a way forward

Informality in Latin America: Taxes and

beyond

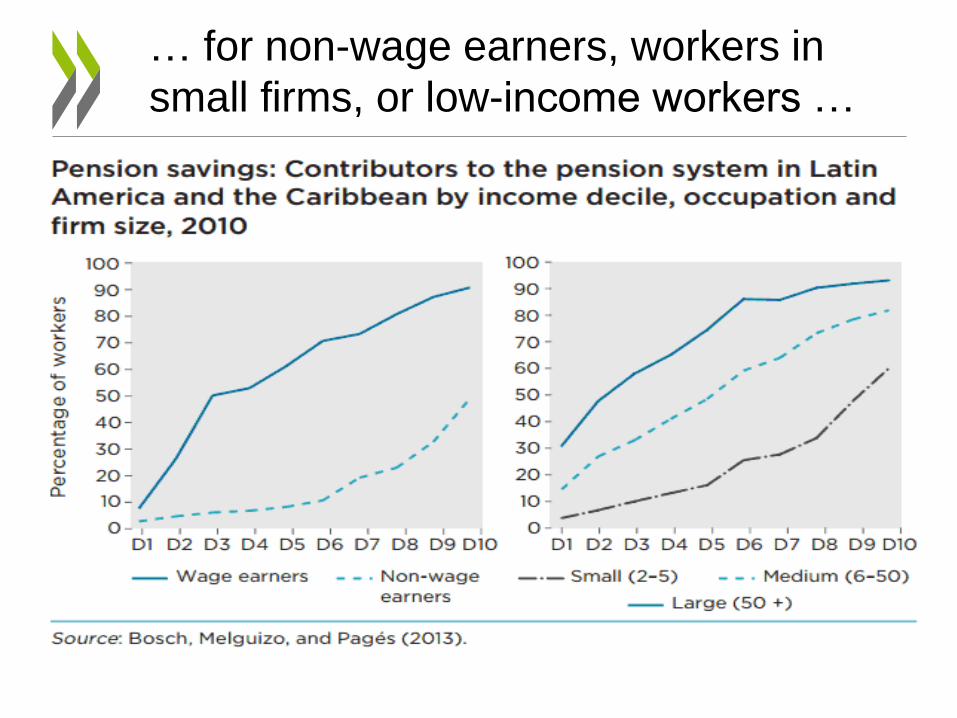

Informal is normal in Latin America…

… for non-wage earners, workers in

small firms, or low-income workers …

… and the emerging middle class

43

23

34

39

21

35

15

20

25

30

35

40

45

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Poor (under $4) Vulnerable ($4-$10) Middle class ($10-$50)

Source: World Bank Equity Lab.

LAC population distribution by per capita income level

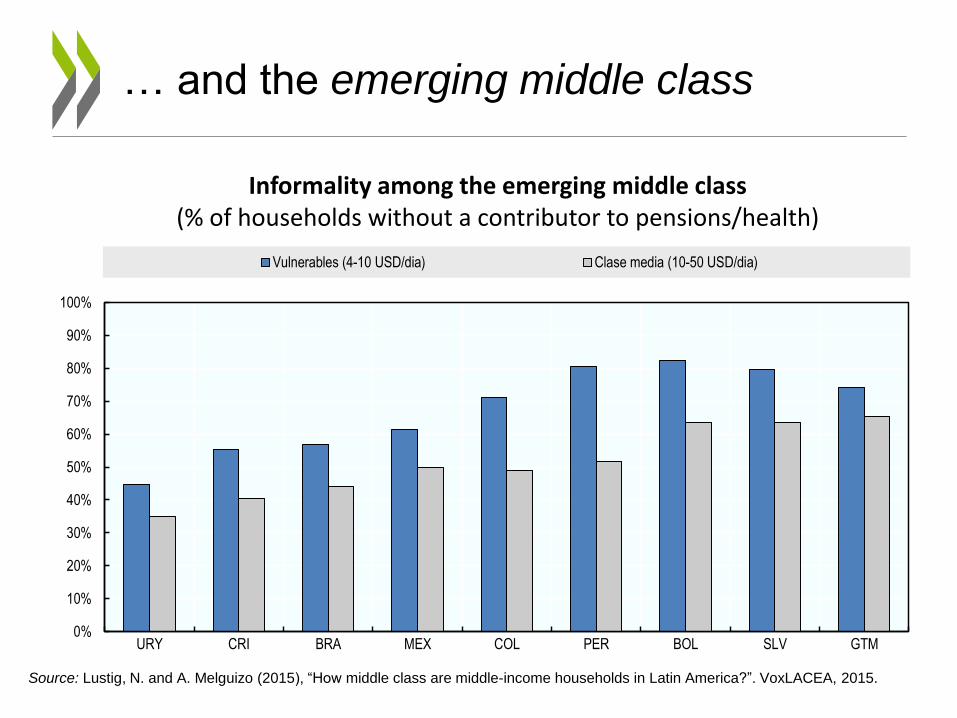

… and the emerging middle class

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

URY CRI BRA MEX COL PER BOL SLV GTM

Vulnerables (4-10 USD/dia) Clase media (10-50 USD/dia)

Informality among the emerging middle class (% of households without a contributor to pensions/health)

Source: Lustig, N. and A. Melguizo (2015), “How middle class are middle-income households in Latin America?”. VoxLACEA, 2015.

• Informal is normal in Latin America

• Latin American hour: Productivity, inclusion

and governance

• Taxes and informality: in it together?

• Beyond taxes: a way forward

Informality in Latin America: Taxes and

beyond

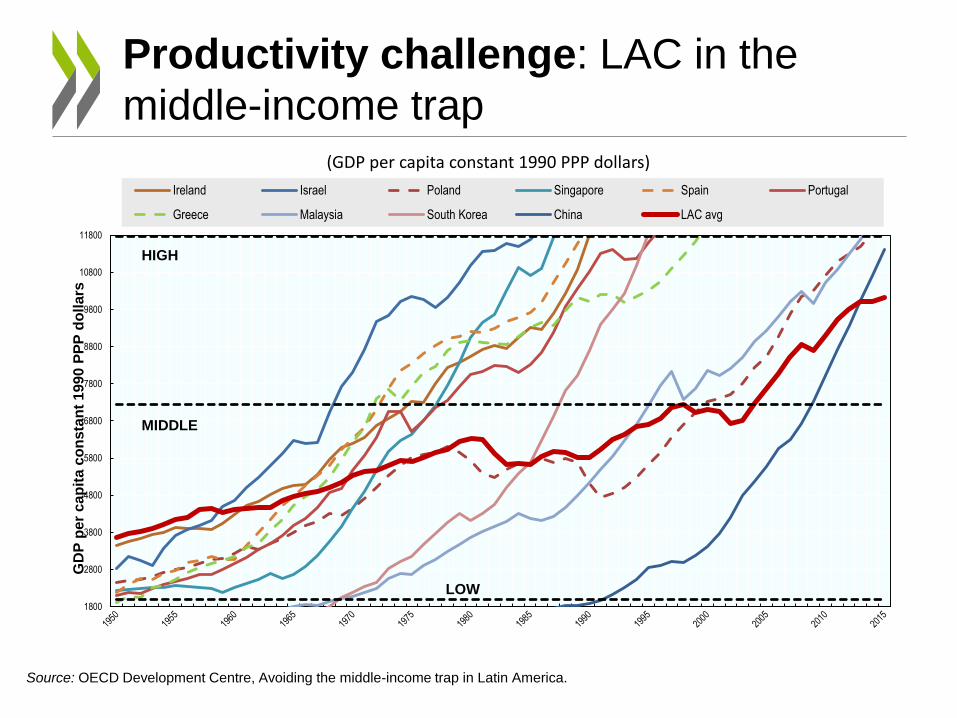

Productivity challenge: LAC in the

middle-income trap

1800

2800

3800

4800

5800

6800

7800

8800

9800

10800

11800

GD

P p

er

cap

ita

co

nsta

nt

199

0 P

PP

do

lla

rs

Ireland Israel Poland Singapore Spain Portugal

Greece Malaysia South Korea China LAC avg

HIGH

MIDDLE

LOW

(GDP per capita constant 1990 PPP dollars)

Source: OECD Development Centre, Avoiding the middle-income trap in Latin America.

Inclusion challenge: middle-class

vulnerability is transmitted to the youth

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15 16 17 18 19 20 21 22 23 24 25 26 27 28 29

Extreme poor

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15 16 17 18 19 20 21 22 23 24 25 26 27 28 29

Moderate poor

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15 16 17 18 19 20 21 22 23 24 25 26 27 28 29

Vulnerable

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15 16 17 18 19 20 21 22 23 24 25 26 27 28 29

Middle class

NEET Informal StudentFormal

Source: OECD/ECLAC/CAF (2016), Latin American Economic Outlook 2017

Governance challenge: informality

impacts trusts in politics/policies

Source: OECD/ECLAC/CAF (2016), Latin American Economic Outlook 2017

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

%

Youth (15-29) Adult (30-64)

Trust in elections (%, 2014)

• Informal is normal in Latin America

• Latin American hour: Productivity, inclusion and

governance

• Taxes and informality: in it together?

• Beyond taxes: a way forward

Informality in Latin America: Taxes and

beyond

Informalities

Workers

Costs > Benefits Benefits > Costs

Costs > Benefits

Firms

Benefits > Costs

Preference Exclusion

Optimal formality

Do channels exist? Evasion

Source: Bosch, M., C. Pages and A. Melguizo (2013), Better Pensions, Better Jobs. IDB

• Difficulty for long-term planning

• Imperfect design of social insurance – Not representative economic/labour model – Enforcement (e.g. channeled through the wage bill)

• Disincentives to formality for firms/workers – Non-wage labour costs and labour regulations

(e.g. mininum wage) – Non-contributory benefits

• Low trust in the State and/or financial sector

• Low productivity

Informality: usual (and less usual)

suspects

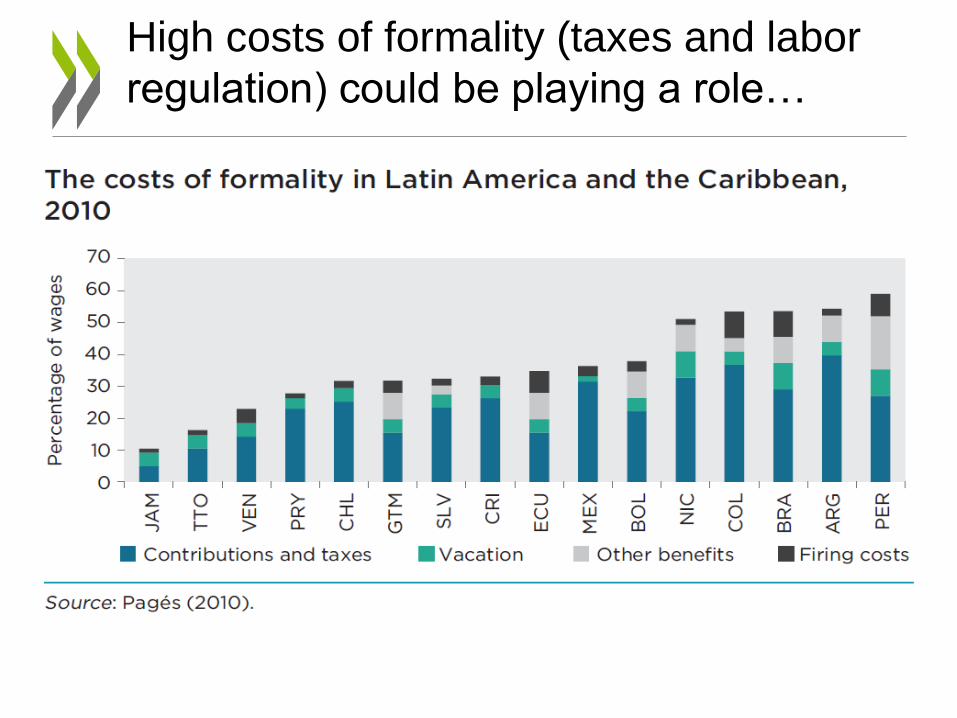

High costs of formality (taxes and labor

regulation) could be playing a role…

… especially when interacting with labor

regulations

Source: Bosch, M., C. Pages and A. Melguizo (2013), Better Pensions, Better Jobs. IDB

Comparable statistics for 20 LAC countries on taxes on wages:

- Social contributions (compulsory; private+public) and personal income tax

- Formal dependent worker

- By levels of income (deciles and USD)

- By family composition (single/couple; children)

Special focus: theoretical costs (taxes) to formalise

Taxing wages in Latin America: data

first

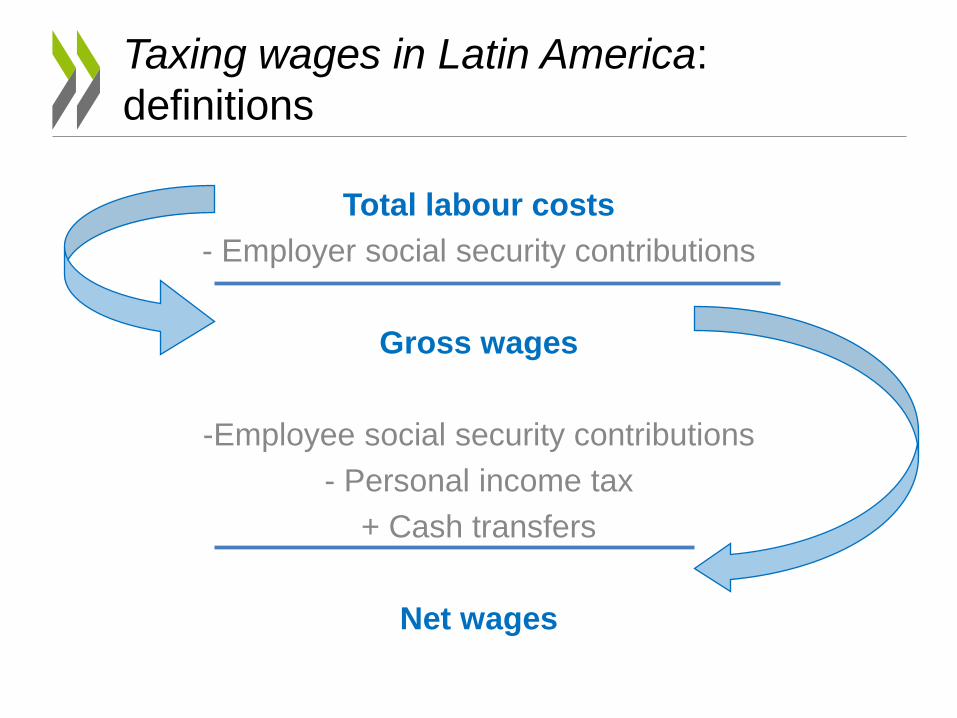

Taxing wages in Latin America:

definitions

Total labour costs

- Employer social security contributions

Gross wages

-Employee social security contributions

- Personal income tax

+ Cash transfers

Net wages

Labour costs in LAC are heterogeneous,

and lower than in OECD (wages&taxes)

Labour costs in Latin America and OECD (Average wage earner; social contributions and personal income tax; 2013)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

Jam

aica

Nic

arag

ua

Per

u

Hon

dura

s

El S

alva

dor

Trin

idad

and

Tob

ago

Dom

inic

anR

epub

lic

Gua

tem

ala

Bol

ivia

Mex

ico

Ven

ezue

la

Col

ombi

a

Ecu

ador

Uru

guay

Par

agua

y

Pan

ama

Bra

zil

Cos

ta R

ica

Chi

le

Arg

entin

a

LAC

OE

CD

Net wages Tax wedge

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

Labour costs are relatively low due to low

taxes on wages (22% vs 36%)…

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

… explained by the personal income tax

(average formal worker is exempted)

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

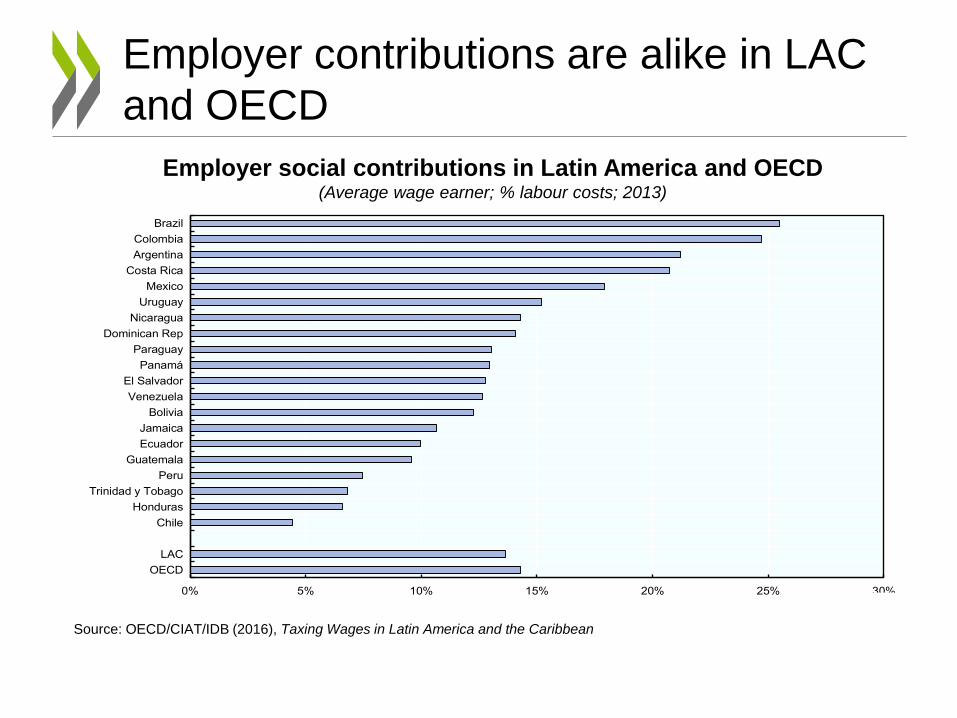

Employer contributions are alike in LAC

and OECD

0% 5% 10% 15% 20% 25% 30%

OECD

LAC

Chile

Honduras

Trinidad y Tobago

Peru

Guatemala

Ecuador

Jamaica

Bolivia

Venezuela

El Salvador

Panamá

Paraguay

Dominican Rep

Nicaragua

Uruguay

Mexico

Costa Rica

Argentina

Colombia

Brazil

Employer social contributions in Latin America and OECD (Average wage earner; % labour costs; 2013)

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

What about those who are informal?

Calculating (tax) costs of formalisation..

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Tasa de informalidad Costo teórico de formalización

Informality and theoretical tax costs of formalisation in Latin America (Average LAC wage earner by income decile; % wages; 2013)

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

Americas Latinas

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Chile

Tasa de informalidad Costo teórico de formalización

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Centroamérica

Tasa de informalidad Costo teórico de formalización

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Colombia

Tasa de informalidad Costo teórico de formalización

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

Taxes and informality are correlated for low

and middle-income workers (vulnerable)

Source: OECD/CIAT/IDB (2016), Taxing Wages in Latin America and the Caribbean

Taxes and informality: in it together?

Theoretical indetermination and not conclusive

empirics

- minimum wage

- coordination of wage bargaining

- taxes/pensions linkage

- direct vs indirect taxes

- short vs long-term

Source: Gonzalez-Paramo, J.M. and A. Melguizo. (2013), Who pays labour taxes and social contributions? A

meta-analysis approach. SERIES, 4, 247-71

• Informal is normal in Latin America

• Latin American hour: Productivity, inclusion and

governance

• Taxes and informality: in it together?

• Beyond taxes: a way forward

Informality in Latin America: Taxes and

beyond

Procrastination and overconfidence traps

Source: Bosch, M., C. Pages and A. Melguizo (2013), Better Pensions, Better Jobs. IDB

Have you thought about financing your retirement?

• Difficulty for long-term planning

• Imperfect design of social insurance – Nor representative economic/labour model – Enforcement (e.g. channeled through the wage bill)

• Disincentives to formality for firms/workers – Non-wage labour costs and labour regulations (e.g.

minwage) – Non-contributory benefits

• Low trust in the State and/or financial sector

• Low productivity

Usual suspects beyond taxes

• Global: interactions between social protection

(pensions, health) and taxes + Coordination among institutions

(regulation, supervision, administration)

• Efficiency: incentives to formal labour

participation

• Innovation: supervision and compliance

mechanisms

• Transparency: simple goals; public debate

and political agreements

Principles of a pro-formality agenda

Incentives for formal jobs (including tax cuts)

Enforce/re-design (especially for self-employed)

Increase information and financial education

Open databases

Impact evaluation

Innovate

Comunication

Channels

Default options

Policy goals and levers

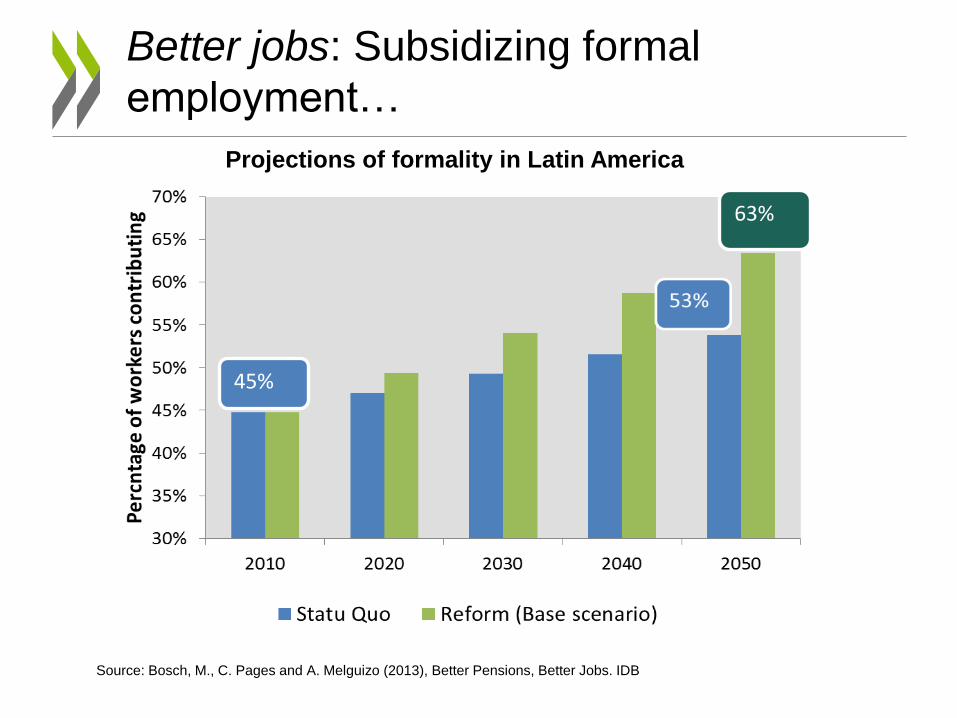

Better jobs: Subsidizing formal

employment…

45%

63%

Projections of formality in Latin America

Source: Bosch, M., C. Pages and A. Melguizo (2013), Better Pensions, Better Jobs. IDB

Better jobs: … and productive

development policies (skills)

0

10

20

30

40

50

60

70

80

90

%

Firms reporting difficulties to hire in LAC, China and OECD countries, 2014

Source: OECD/ECLAC/CAF, Latin American Economic Outlook 2017: Youth, Skills and Entrepreneurship , based on Manpower Group (2015).

• Informal is normal in Latin America • 55% workers

• Also a middle-class challenge

• Addressing productivity, inclusion and governance need formalisation

• Taxes and informality: in it together? • Yes: taxes on wages can be burdensome, especially for the

transition informality-formality

• Beyond taxes: a way forward – Comprehensive pro-formality package: incentives

(monetary & nudge`s) and productive development policies

Informality in Latin America: Summing up

• Better Pensions, Better Jobs

https://publications.iadb.org/handle/11319/462?locale-

attribute=es

• Pensions at a Glance in LAC

http://www.oecd.org/publications/oecd-pensions-at-a-glance-

pension-glance-2014-en.htm

• Taxing Wages in LAC

http://www.oecd.org/development/taxing-wages-in-latin-

america-and-the-caribbean-2016-9789264262607-en.htm

• Latin American Economic Outlook 2017

www.latameconomy.org

Main references

www.oecd.org/dev

Twitter.com/OECD_Centre

www.facebook.com/OECDDevelopmentCentre

www.youtube.com/user/DevCentre

www.flickr.com/photos/oecd_development_centre