information memorandum...universal traders sacco society (uts) intends to raise its core capital for...

TRANSCRIPT

Page 0 of 42

INFORMATION MEMORANDUM

Page 1 of 42

OUR VISION

“Quality financial provider of choice”

OUR MISSION

“We exist to empower members and customers economically

and socially by providing quality and affordable financial

services”

OUR CORE VALUES

Honesty

Hard work

Professionalism

Transparency & Accountability

Integrity

Respect

Equality & Fairness

Confidentiality

Page 2 of 42

TABLE OF CONTENTS

1.0 GLOSSARY OF DEFINITIONS AND ABBREVIATIONS ................................................................ 4

2.0 ADDENDUM ............................................................................................................................... 5

3.0 FEATURES OF THE OFFER .......................................................................................................... 6

3.1 Share price ............................................................................................................................. 6

3.2 Important Dates .................................................................................................................... 6

3.3 Eligibility ................................................................................................................................. 7

3.4 Other Information ................................................................................................................. 7

4.0 THE SOCIETY INFORMATION .................................................................................................... 9

5.0 DISCLAIMER STATEMENTS ..................................................................................................... 10

6.0 USE OF PROCEEDS .................................................................................................................... 11

7.0 INDUSTRY OVERVIEW .............................................................................................................. 13

8.0 GOVERNANCE STRUCTURE ..................................................................................................... 14

8.1 Board of Directors ............................................................................................................... 14

8.2 Supervisory Committee ...................................................................................................... 15

Appendix 8 Senior Members of Staff ............................................................................................ 16

9.0 SELECTED FINANCIAL DATA .................................................................................................... 23

9.1 Membership Growth ........................................................................................................... 23

9.2 Statement of Financial Position ......................................................................................... 24

9.3 Statement of Comprehensive Income ............................................................................... 26

10.0 RISK FACTORS .......................................................................................................................... 26

10.1 Competition ......................................................................................................................... 26

10.2 Operational Risks ................................................................................................................ 27

10.3 Credit Risk ............................................................................................................................ 28

10.4 Liquidity Risk ........................................................................................................................ 28

10.5 Market Risk .......................................................................................................................... 29

10.6 Legal & Regulatory Risk ...................................................................................................... 30

11.0 APPENDICES .............................................................................................................................. 31

Appendix 1 Financial Summary ....................................................................................................... 31

Appendix 2Statement of Comprehensive Income 2011-2015 .......................................................... 0

Page 3 of 42

Appendix 3 Statement of Financial position 2011-2015 ................................................................... 2

Appendix 4 Projected Statement of Financial Position2016-2020 ................................................. 3

Appendix 5 Projected Statement of Comprehensive Income2016-2020 ....................................... 5

Appendix 6 Projected Financial ratios ............................................................................................. 7

Appendix 7 Organizational Structure .............................................................................................. 8

Page 4 of 42

1.0 GLOSSARY OF DEFINITIONS AND ABBREVIATIONS

ADM Annual Delegates Meeting

AGM Annual General Meeting

ATM Automated Teller Machine

BOD Board of Directors

BOSA Back Office Services Activity

CAK Co-operative Alliance of Kenya

CEO Chief Executive Officer

CCIA Co-op Consultancy & Insurance Agency

CSR Corporate Social Responsibility

DMS Document Management System

DT-Sacco Deposit –Taking Sacco

F&A Committee Finance & Administration Committee

FOSA Front Office Services Activity

ICT Information Communication Technology

KRA Kenya Revenue Authority

KUSCCO Kenya Union of Savings and Credit Co-operatives

MOU Memorandum of Understanding

NACOS National Co-operative Organizations

PAR Portfolio AT Risk

PESTLE Political, Economic, Social, Legal & Ecological/ Environment

SASRA Sacco Societies Regulatory Authority

Page 5 of 42

2.0 ADDENDUM

This Information memorandum has been prepared to enable members make informed

decisions on investing in Sacco shares. The information herein is intended for Sacco

members and other eligible people who may join the Sacco in line with the provisions of

the Sacco By-laws. The Information memorandum is not a prospectus for soliciting funds

from the general public.

Directors Statement

We, the undersigned, hereby declare that all the information stated in this Information

Memorandum is correct and consistent with the AGM Minutes, Board Minutes and

Audited reports.

Signed:

Simeon K. Kitheka Chairman ……………………………………

Lydia N. Kimondo Hon Secretary ………………………………

Raphael M. Muthike Treasurer ....……………………………….

Page 6 of 42

3.0 FEATURES OF THE OFFER

Universal Traders Sacco Society (UTS) intends to raise its core capital for expansion,

infrastructure improvement and introduction of new products.

3.1 Share price

The Offer price is as per the Society by-laws. The Society is targeting to sell a total of Five

million (5,000,000) shares at a price of Kes 100 per share. The price for the shares took

into consideration the following factors:

a) The Society’s robust over the counter market price; and

b) The earning potential of the Society;

The anticipated fair market value per share is not less than Kes.100.

Particulars Explanation

Par Value per share

Kes. 100

Average No. of shares per member

100

Targeted Shares

5,000,000

Maximum No. of shares per member

One fifth of the total shares issued

Targeted amount to be raised

Kes. 500,000,000

3.2 Important Dates

Activity Date

SASRA/CMA approvals

31st January 2017

Board/Staff/Members sensitization

1st February 2017 – 28th February 2017

Offer Period

1st March– 31st May 2017

Issue of Share certificates

31st July 2017

Page 7 of 42

3.3 Eligibility

The shares offer is open to members of the Society only. If an individual want to buy

the shares on offer and is not a member, he/she must register as a member first by

filing the membership form and meeting minimum member requirements.All shares

applied will be allotted only those applications that are :

1. A duly filled completed shares application form and subsequent payment.

2. Acceptance of a share, once issued shall not be refundable

3.4 Other Information

1. This Information Memorandum includes particulars given in pursuance of giving

pertinent information to members and potential members on Universal

TradersSACCO Society.

2. Universal TradersSACCO Society is registered as a Cooperative Society under the

Cooperative Societies Act under registration number C/S 6403.

3. Universal Traders Sacco is also regulated as a Deposit-Taking SACCO by the Sacco

Societies Regulatory Authority (SASRA) under Sacco Societies Act 2008.

4. The board of directors of Universal Traders SACCO Society verify that the

information contained herein is true and accurate to the best of the knowledge

and belief of the directors (who have taken all reasonable care to ensure that

such is the case) the information contained in this Information Memorandum is in

accordance with the facts and does not omit anything likely to affect the import

of such information.

5. The Shares are non-refundable but are freely transferable upon getting willing

member to buy off the shares subject to the Society by-Laws and subject also to

the restrictions set out in the SACCO Societies Act 2008.

Page 8 of 42

6. The SACCO has issued and paid up shares of Kes. 61,466,000.00 at 31st December

2016. As at 31st December 2016 it had a total active membership of 40,000

consisting of individual shareholders.

Business Name: Universal Traders Savings & Credit Co-operative Society Limited

Registered Office: Traders House Building Machakos Town L.R.No.BLOCK II/110

Street/Road: Syokimau Road

Postal Address: Telephone Numbers:

P.O. Box 2119- 90100 Machakos +254 44 2020571 +254 76127102

E-Mail address:

KRA PIN P051123374U

VAT

Our Advisors Co-op Consultancy & Insurance Agency Co-operative House, 13th Floor Haile-Selassie Avenue P.O. Box 48231- 00100 Nairobi [email protected] +254 3276 598/353 +254 711 049 598/ 353

Our Bankers: 1. The Co-operative Bank of Kenya Limited Machakos Branch P.O. Box 1250-90100 Machakos

2. Family Bank

Machakos Branch

Lawyers JM Mutua & Company Advocates P.O. Box XXX-90100 Machakos

Auditors Omanwa and Associates

Page 9 of 42

Certified Public Accountants Commerce House, Moi Avenue Nairobi P.O. Box 64447 -00620 Nairobi

4.0 THE SOCIETY INFORMATION

Universal Traders Sacco Society Limitedwas established in 1991 (CS\6403) as Masaku

Traders Sacco Society by a few business persons who had a vision of bringing the local

entrepreneurs together to respond to changes in the financial industry by forming an

organization where they could save and borrow to meet their economic needs. During

this period most Sacco Societies were for employee based and the common business

persons was left out to the fate of main financial institutions whose terms of borrowing

could not be met by many.

The vision then was to have the upcoming and existing Micro, Small and Medium sized

entrepreneurs pool their meagre savings together and eventually access credit facilities

at affordable terms through co-guaranteeing system. Most of the entrepreneurs lacked

collaterals demanded by the main stream financial institutions.

In 2006, Front Office Services Activity (FOSA) operations commenced in the Machakos

branch and later cascaded to other branches. Today, the society is licensed by Sacco

Societies Regulatory Authority (SASRA) as a Deposit-Taking Sacco Society (DT-Sacco) and

regulated under the SACCO Societies Act, 2008. The Society currently has over 35,000

members with an asset base of Kes.667 million and Kes.375 million in deposits.The

Society currently has 59members of staff.

The Society is popular with organized women groups, youth groups and self-help groups

and the informal merry-go-round groups who are involved in very valuable forms of

savings mobilizations for a common group purpose or for alleviating members’ financial

burdens.

Membership to the Society is through registration and buying of the minimum shares as

per the society By-laws. The Society served members under the traders’ common bond

until 2008 when the bond was expandedto cover the whole country where the Society

Page 10 of 42

has its operations. Membership today is diverse and incorporates traders, farmers, civil

servants, membership groups and associations. Most of UTS operations are in the larger

Machakos, Makueni, Kitui and Embu Counties. Its branch network includes Tala, Wote,

Embu, Kitui and Nzaikoni (Kathiani) in addition to its head office based in Machakos

Town.

The Society is in the process of consolidating its business to become the financial service

provider of choice in the SME and agriculture sectors in the South Eastern region of the

country. To achieve this, the Society plans to adopt technological advancements, engage

in research and innovation to position itself comfortably in the market. The Sacco

products and services are categorized along the Front Office Services (FOSA) and Back

Office Services (BOSA); Micro-Credit is also provided but as part of FOSA operations.

These include the following loan products and services: accounts for young children,

current and fixed deposits accounts, salaries accounts & loans; agricultural loans; e.g.,

mango loan products, dairy support loans (RABO bank); horticultural loans; emergency

loans; business loans and microfinance group based loans.

In offering these financial services UTS-Sacco has collaborated with other development

partners including; Micro Enterprise Support Programme Trust (MESPT), USAID/FIRM,

RABO Bank, Coffee Development Foundation, The Co-operative Bank of Kenya, World

Council of Credit Unions (WOCCU), Kenya Union of Savings and Credit Co-operatives

(KUSCCO), Cooperative University College of Kenya, Government of Kenya (Coffee

Development Fund). With support from all these partners UTS-Sacco has been able to

access financial and capacity building support that has facilitated its growth to a current

asset base of over Kes.667 million.

5.0 DISCLAIMER STATEMENTS

The Directors of the Issuer, having made all reasonable inquiries, confirm that this

Information Memorandum contains all information with respect to Universal Traders

SACCO Society by it which is material in the context of the Shares, that the information

contained in this Information Memorandum is true and accurate in all material respects

Page 11 of 42

and is not misleading, that the opinions and intentions expressed in this Information

Memorandum are honestly held and that there are no other facts the omission of which

would make any of such information or the expression of any such opinions or intentions

misleading. The Directors of the Issuer accept responsibility accordingly.

The Directors of the Issuer, whose names appear in this Information Memorandum,

accept responsibility for the information contained in this document. To the best of the

knowledge and belief of the Directors (who have taken all reasonable care to ensure that

such is the case) the information contained in this Information Memorandum is in

accordance with the facts and does not omit anything likely to affect the import of such

information.

No person has been authorised to give any information or make any representation

other than those contained in this Information Memorandum and if given or made, such

information or representation should not be relied upon as having been authorised by or

on behalf of the SACCO.

The distribution of this Information Memorandum and the offer or sale of the Shares may

be restricted by law to certain jurisdictions. Persons into whose possession this

Information Memorandum or any Shares may come must first inform him or herself

about and observe any such restrictions.

6.0 USE OF PROCEEDS

The proceeds of the offer will accrue 100% to UTS-Sacco. The gross proceeds on target

amount to Kes.500,000,000/-.

The Society is seeking these proceeds for the purpose of sustaining the growth

momentum and the aim is to increase the shareholders’ value as well as increase the

outreach and quality of service offering to the members. The entire net proceeds are

Page 12 of 42

therefore earmarked for business expansion initiatives and improvement of its service

delivery platforms. The table below provides a summary of the key investment areas:

Details Rational

ICT Systems To invest in a new robust reliable Management information

system that will be able to accommodate growth as well as

deliver innovative solutions such as the mobile banking and

interoperability with other payment systems in the country.

Regional Expansion The Society is in a growth phase and we expect to open ten

branches within the South Eastern region by 2020. This will

increase our market share hence better returns to the

shareholders

External borrowing The Society has been relying on external borrowing to fund

its operations. There is need to pay off some of the debts

hence reducing the society expenditure on interest paid to

external lenders

New products To introduce long term loan facilities to our members

Regulatory Compliance As our assets grow there is need to increase our core capital

to be within the prudential ratios set by the regulators.

The Share drive will also give UTS-Sacco shareholders and the Society the benefits of

liquidity and price discovery:

a) An opportunity for members of the Society to share in what we believe will

continue to be a successful cooperative venture;

b) An objective valuation of the shares of the Society and an enhancement of the

Society’s price discovery mechanism;

c) A mechanism of exchange of shares for the shareholders of the Society;

Page 13 of 42

d) An opportunity for the Society to enhance corporate governance structures,

corporate image and disclosure standards;

7.0 INDUSTRY OVERVIEW

The financial industry in Kenya is comprised of various players namely; Banks, Micro-

finance institutions, Savings and Credit Co-operative Societies, Foreign exchange

bureaus, Telecommunication companies and Rotating Savings and Credit Associations

(ROSCAs). The banks and Deposit-Taking Micro-Finance Institutions (DT-MFIs) are

licensed and supervised by the Central Bank of Kenya (CBK) while Deposit-Taking Sacco

Societies (DT-Saccos) are Licensed and supervised by the Sacco Societies Regulatory

Authority (SASRA).

FINANCIAL INDUSTRY LANDSCAPE

Central Bank

Banks (42)

DT-MFIs(13)

Forex Bureaus

SASRA

DT-Saccos

(177)

Department of Co-operatives

Non-DT-Saccos

(over 3000)

OTHERS (Unregulated)

ROSCAs

Groups

Shylockers

Page 14 of 42

8.0 GOVERNANCE STRUCTURE

The Society’s growth and achievements have largely as a result of sound and prudent

management by a widely experienced Board of Directors and highly competent

Management team. The Society has nine (9) Board of Directors and three (3) Supervisory

committee members.

8.1 Board of Directors

Mr.Simeon Kitheka

Chairman of the Board of

Directors

Mr. Fredrick M. Ngumbi

Vice Chairman of the Board of Directors

Mr. Raphael Muthike

Treasurer of the Board of

Directors

Mrs. Lydia Kimondo

Honarary Secretary of the Board of

Directors

Page 15 of 42

8.2 Supervisory Committee

Mr.Kelvus K. Muli

Member of the Board of Directors

Mrs.Margaret Nzioki

Member of the Board of Directors

Mr.Sila Mbolu

Member of the Board of Directors

Mrs. Sarah Nzau

Member of the Board of Directors

Mr. James Muema

Chairman

Mrs.Magdaleane Mutisya

Secretary

Mr.David Mutava

Member

Page 16 of 42

The Board of Directors is responsible for fostering the long-term business of the SACCO

consistent with their fiduciary responsibilities to shareholders and depositors.

The Board is committed to conducting the affairs of the SACCO with openness, integrity

and accountability and in accordance with the highest standards of corporate

governance. Each of the directors has signed a code of conduct which sets out the duties

and responsibilities of the directors.

As at the date of this Information Memorandum and for a period of at least two years

prior to the date of this Information Memorandum, no director of the Society:

a) Has or has had any petition under bankruptcy laws pending or threatened against

him; or

Has or has had any criminal proceedings in which he was convicted of fraud or any

criminal offence, nor been named the subject of any pending criminal proceedings or any

other offence or action either within or outside Kenya;

8.3 Senior Management

Appendix 8 Senior Members of Staff

Name of staff : Dominic Mutunga

Current Position : Chief Executive Officer

Years with Sacco : (8 Years)

Date of Birth : (1982)

Education & Key Qualifications

Page 17 of 42

Bachelor of Commerce (Finance Option) - KCA University

CPA (K)

Work Experience

Mr. Mutunga holds a Bachelor of Commerce in Finance and is a Certified Public

Accountantof Kenya. He has a vast experience in Financial Management and Co-

operative Movementaffairs. Before his appointment, he was the Head of Accounts and

Finance for a period of 5years. He has an extensive understanding of business strategy

development andimplementation and a Financial Consultant and advisor.

Name of Staff : Beatrice Kinyili

Current Position : Operations Manager

Years with the Sacco : (10 Years)

Date of Birth : (1981)

Work experience

Beatrice holds Bachelors of Arts (BA) degree from Egerton University and is currently

pursuing a Masters (MBA) degree; Strategic Management and leadership option at St

Paul’s University.She has over 8 years experience in the Banking sector and has

previously served as a Branch manager and Credit Manager at Universal Traders Sacco.

Currently, she is holding the position Operations Manager at Universal Traders Sacco.

Name of staff : CPA Mary KatheuNzomo

Current Position : Manager, Finance and Accounting

Years with Sacco : (2 Years, 3 Months)

Date of Birth : (1983)

Page 18 of 42

Education & Key Qualifications

MBA (Finance and Accounting) Mt. Kenya University (Continuing)

B.BM (Finance and Banking) Moi University

CPA (K)

Work experience

CPA Mary was confirmed as the Head of Finance and Accounting at Universal Traders

Sacco in January 2016 after acting in the same capacity for 11 months. She has an

extensive financial Accounting/reporting experience in the Banking, Manufacturing and

Insurance industries.

Name of staff : George Wamboye

Current Position : Credit Manager

Years with Sacco : (1 Year)

Date of Birth : (1972)

Education&Key Qualifications

Diploma (Micro Finance) Strathmore University

Diploma (HR Management) Kabete Institute

Work experience

Mr. Wamboye joined Universal traders Sacco in February 2016 and is currently the Credit Manager.

Name of Staff : Simon Kioko Nzioki

Page 19 of 42

Current Position : Internal Audit Manager

Date of Birth : (1982)

Education & Key Qualifications

Bachelor of Commerce (Finance Option) KCA University

CPA (K)

Member of ICPAK

Name of Staff : Peter Muema Kiamba

Current Position : Marketing Supervisor

Years with SACCO : (7 Years)

Date of Birth : (1975)

Education Qualifications

Diploma in Information Technology - Jomo Kenyatta University

Holder ofA+, N+ and CCNA, and part one of M.C.SE – M.C.P (Microsoft Certificate Professional) from Computer Pride Limited.

Work Experience

Mr. Kiamba has worked in various departments in Universal Traders Sacco since joining

the institution. He has worked in the I.T Department for 5 years and currently he was

appointed as Marketing supervisor and later Marketing Officer at Universal Traders

Sacco in 2016 from Computer Pride Limited. He has attended various professional

trainings organized by Co-operative Bank on various areas, Top Edge Consultants LTD –

on Pillar of Competitiveness and MESPT- Customer Service and Marketing Training.

Name of staff : AlfixNyamaiMakau

Current Position : Branch manager-Kathiani

Page 20 of 42

Years with Sacco : (1 Year, 1 Month)

Year of Birth : (1984)

Education Key Qualifications

BA (Economics) - University of Nairobi

Banking operations - Kenya school of monetary studies

Cpa-Kasneb-in progress

Work experience

Mr. Makau joined Universal traders Sacco in the year 2016 and is currently the Branch Manager, Kathiani Branch. He has been an Assistant Manager at Rafiki micro finance Bank and operations assistant at commercial bank of Africa before joining Universal traders Sacco.

Name of Staff : Michael Mutunga Nzuma

Current Position : Branch Manager Wote

Years in SACCO : (2 years, 3 months)

Year of Birth : 1980

Education &Key Qualifications

Bachelor of Commerce (Finance option). Diploma in Business administration (credit) Machakos University College Certificate in HRM(Distinction) University of Nairobi Certificate in Computer studies- Hammu office services.

Michael has some vast experience in Credit Management, Business development,

Banking and Business Strategic Management running for over nine years with SMEP

Microfinance Bank and hands on experience in Insurance Business Management from

Kenyan Alliance Insurance Company LTD.

Page 21 of 42

Name of staff : Dorcas kelikimeu

Current Position: Branch Manager Tala Branch

Years with Sacco: (8 Years)

Date of Birth :(1981)

Education &Key Qualifications

Bachelor of Commerce(HRM) Kenyatta university(Continuing) Diploma in Business administration (credit) Machakos University College Certificate in HRM(Distinction) University of Nairobi Certificate in Computer studies- Hammu office services.

Work experience

Ms. Dorcas Keli joined Universal traders Sacco in the year 2008 and is currently the Branch Manager Tala. She has been a teller, Micro credit officer, Micro credit lending supervisor, Bosa Loan officer and now the Branch Manager. She also worked as a Member care/ Controls staff ( Branch internal rotations, Marketing staff ( Before Tala Branch launch in year 2008)

She has 4 years working experience in Micro finance sector ( K-rep FSA) as a Branch Manager.

Name of staff: Juliet Mbinya Muia

Current Position: Ag. Branch Manager

Years with Sacco: 10 Years

Date of Birth: 1978

Education & Key Qualifications

Page 22 of 42

DBM (Diploma in Business Management): St. Paul University (Continuing)

Full secretarial St. Anuarite Institute

Work Experience

Ms. Juliet Mbinya Muia joined Universal Traders Sacco in the year 2006 and is currently the Acting Manager, Embu branch. She had been the secretary to the CEO, Marketing Officer, member care officer and controls clerk before her current position.

Name of Staff : Sylvester Ndolo Komu

Current Position : Branch Manager – Kitui

Years in SACCO : (2 Years, 3 Months)

Date of Birth : (1980)

Sylvester Komu joined UTS in November 2014 as a Branch Manager. He holds Diploma in Banking

and Financial services from the Kenya School of Monetary Studies. Komu is a Qualifier of the

Associate of Kenya Institute of Bankers ( AKIB ) having qualified in 2006.He is currently pursuing

BSC. In Business Administration at USIU.

Komu is a seasoned Banker by career. He worked at ABC Bank as a Management Trainee – Branch

operations, Risk and compliance and credit. Komu worked for Diamond Trust Bank as a senior

operations officer before joining Jamii Bora Bank as an operations Manager. Before Joining UTS

he was the credit operations officer at Speed Capital microfinance in charge of credit.

He is an active Associate member of the Kenya Institute of Bankers.

Page 23 of 42

9.0 SELECTED FINANCIAL DATA

Universal Traders SACCO has in the past achieved positive results in its key performance

indicators. In the last five years (2011-2015) information on some selected parameters is

as follows:

9.1 Membership Growth

The Society draws membership from the local community where the Society has offices.

Membership to the society is opened to individuals, Groups, Community Based

Organizations (CBOs) institutions and other corporate organizations.

The active membership of the Society has grown from 17,798 Members in 2010 to over

33,000 in 2015. This is 87% growth and the society is likely to grow membership at rate of

30% annually.

17,798

23,776

20,767

25,973 26,654

33,273

2010 2011 2012 2013 2014 2015

Active Membership 2010- 2015

Page 24 of 42

9.2 Statement of Financial Position

The financial position of the Society has been stable over the last five years. The figure

below shows the Society main assets are loans to members. These loans are income

generating assets.

The total assets of the Society have grown from Kes. 377.7 Million in 2011 to Kes. 666.7

million in 2015. This represents a 77% growth. Loans and advance contribute 78% of the

Society’s total Assets as at the close of 2015 financial year.

The Society’s loan portfolio is classified is well distributed to ensure low risk exposure.

The largest exposure is under Asset Finance (27%) and normal loans (27%) followed by

growth oriented loans at (21%). The chart below demonstrates the distribution.

Page 25 of 42

The Society Loans portfolio is classified as indicated in the chart below.

The performing loans are 90% of the total loan portfolio. The portfolio at risk (PAR) is 10%

.

90%

1% 2%2%

5%

Loan Classification Dec 2016

Performing Watch Substandard Doubtful Loss

Page 26 of 42

9.3 Statement of Comprehensive Income

The society has been making a surplus over the period (2011- 2015). However, some of the

surplus has been retained over the years to comply with the Sacco Societies Regulations

and also grow the institutional capital.

10.0 RISK FACTORS

Universal Traders Sacco Society has established a comprehensive framework for risk

Management that has been implemented across all business units. All risks to the DT-

Sacco Societies and those that are specific to UTS Sacco Society are monitored and

actively managed. There is continuous monitoring and assessment of the society’s limits

to ensure appropriate and timely intervention in line with the Society’s objectives,

strategies and current market conditions.

10.1 Competition

Universal Traders SACCO society is the largest member based Sacco society in the south

eastern region of Kenya. Competition in the sector is expected to grow even more than

has been experienced before. However, the potential market is still largely untapped

with basic banking services having a low penetration rate in the region, especially among

Page 27 of 42

the rural people. The Society has actively engaged vigorous mitigating strategies to

manage the competition. Among them is the development of customer driven products,

leveraging on technology to reach customers at their residences, establishment of new

branches and establishment of a marketing unit in the Society.

10.2 Operational Risks

Operational risk is a human error, system failures, and inadequate procedures and

controls within daily service or product delivery. Operational risk can be described as the

risk of loss arising from inadequate information systems; technology failures, breaches in

internal controls, fraud, unforeseen catastrophes, or other operational problems may

result in unexpected losses. Operational risk exists in all products and business activities.

Of key concern will be current staff competence, especially at management and technical

levels, and efficacy of internal controls. Operational risks may be in documentation,

processing and accounting of transactions and may result in unexpected loss. The risk

may also be attributed to inadequate procedures and control system failure and/or

human error. This risk is a function of internal controls, information systems, employee

integrity, and operating processes.

Although operational risk is difficult to measure, periodic reviews of procedures,

documentation and data processing are critical and helpful in establishing the levels of

risk. In order to mitigate this risk, the Society ensures that an effective, integrated

operational risk management framework that incorporates a clearly defined

organizational structure and work flow is maintained.

a) Each Unit in the Society has defined roles and responsibilities for all aspects of

operational risk management.

b) The Society has an established credit committee of the board that oversees all the

lending aspects of the Society.

c) All information technological services systems architecture is highly scalable and

require minimal lead-time to increase capacity to match growth in demand.

Page 28 of 42

d) Appropriate insurance cover to cover risks such as theft and employee infidelity

have been put in place.

e) Clear policies, processes and procedure manuals that clearly stipulate how the

operations of the Society should be carried out have been put inplace.

10.3 Credit Risk

Credit risk can be defined as the possibility that a loss could arise from non-payment or

late payment of a loan obligation of the member/customer. Credit risk encompasses both

the loss of income resulting from the organization inability to collect anticipated interest

savings as well as the loss of principle resulting from a loan default.

Credit risk includes transaction and portfolio risks. Transaction risk refers to the risk

within individual loans. The Society mitigates transaction risks through borrower

screening methods. Quality procedures for loan disbursement, monitoring and collection

are adhered to. Portfolio risk refers to the risk inherent in the composition of the overall

loan portfolio. Policies on loan diversification, maximum loan size, types of loans and

loan structure lessen this nature of risk. As with all financial institutions, the Society faced

with these risks.

Default will arise due to members over-borrowing, the effect of competitors,poor

recovery mechanisms, and loss of employment amongst other reasons. The

management has set minimum acceptable parameters within which the Society operates

to realizing long-term shareholder value enhancement.

The ultimate responsibility for ensuring that credit operations are properly administered

and maintained lies with the Board of Directors. The Society has comprehensive

procedures; competent staff and an information system that can effectively track the

administration and recovery process are in place.

10.4 Liquidity Risk

Page 29 of 42

Liquidity risk refers to the Society’s ability to meet obligations and other commitments at

all times at reasonable price. A Society faces liquidity risk when it’s unable to meet its

obligations on a timely basis and in a cost-efficient manner. It therefore refers to

sufficient sources of funds available to meet all commitments as required. Liquidity risk

may not be seen in isolation because it is often triggered by consequences of other

financial risks such as credit risk, market risk etc.

The Society seeks to ensure that it maintains sufficient funds at all times to meet its

operational needs, including maturing liabilities and to ensure compliance with the Sacco

Societies regulations. The following measures have been put in place to address liquidity

risk:

a) Maintaining an aggressive strategy aimed at increasing the deposits base.

b) Borrowing from other financial institutions.

c) Lending to our members’ subject to availability of funds.

Liquidity management is therefore an on-going effort to strike a balance between having

too much cash and too little cash. If the Society holds too much cash in form of deposits

it may not make sufficient returns to cover the costs of its operations, resulting in the

need to increase interest rates above competitive levels. If the Society holds too little

cash, it could face a crisis of confidence and lose clients who no longer trust the

institution to have funds available when needed. To achieve this, Society maintains

detailed estimates of cash projection inflows and outflows for term period so that net

cash requirement can be identified. Further, the Society to maintain investment

accounts that can easily be liquidated into cash or lines of credit with local banks to meet

unexpected needs.

The prerequisites of an effective liquidity risk management program include an informed

board, capable management, competent staff, efficient systems and procedures.

10.5 Market Risk

Market Risk is the risk that the value of on and off-balance sheet positions of a financial

institution will be adversely affected by movements in market rates or prices such as

Page 30 of 42

interest rates, foreign exchange rates, equity prices, credit spreads and/or commodity

prices resulting in a loss to earnings and capital.

The Society has not invested heavily in assets that may be affected by changes in the

market. However, the recent capping of interest rates for bank may affect our pricing

model. The management shall keep monitoring the market and adjust rates

appropriately to competitive levels.

10.6 Legal & Regulatory Risk

Legal and regulatory risk is the risk of loss emanating from non-compliance with the laws

of the land and regulatory guidelines of the sector. It arises out of violations of or non-

conformity with laws, rules and regulations, prescribed by a State. Cost of no-

conformance to rules, regulations or laws range from fines to lawsuits. Types of

offences and the values of such costs in the Sacco are clearly spelt out in the Co-

operative Act, Sacco Act 2008, Rules and the by-laws of specific co-operative societies

and Sacco Societies Regulatory Authority (SASRA) rules & regulations.

There is always the risk that changes in government and subsequent regulations and

legislature can always affect the operations of not only the Society but the sectors a

whole. This risk is not unique to the Society and the Board of Directors and Staff not only

ensures best practice but keep the Society abreast of the changes in the regulatory

framework in order to ensure compliance.

Page 31 of 42

11.0 APPENDICES

Appendix 1 Financial Summary

2011 2012 2013 2014 2015

Active Membership

23,776 20,767 25,973 26,654 33,273

Core Capital

69,443,553 83,789,443 97,220,219 94,340,063 98,043,632

Total Assets

377,690,513 390,460,285

571,059,493 561,353,932 666,755,312

Loan Book

283,310,659

299,921,101 359,647,266

403,855,548

523,121,578

Member Deposits

199,485,212 220,284,254 295,776,555 321,205,368 375,885,986

Page 0 of 42

Appendix 2Statement of Comprehensive Income 2011-2015

2011 2012 2013 2014 2015

Kes Kes Kes Kes Kes

REVENUE

Interest on loans and advances 62,934,498.00 72,050,744.00 88,783,473.00 93,177,588.00 102,157,515.00

Other interest income 637,183.00 1,597,749.00 324,156.00 329,471.00 386,641.00

Other operating income 1,399,605.00 1,399,605.00 6,639,639.00 3,374,584.00 4,516,753.00

Total net income 64,971,286.00 75,048,098.00 95,747,268.00 96,881,643.00 107,060,909.00

EXPENSES

Financial Expenses 5,312,985.00 5,205,192.00 13,828,168.00 12,898,392.00 15,931,666.00

Interest expense 7,579,891.00 9,324,926.00 6,223,981.00 9,497,197.00 15,380,358.00

Administration expenses 15,774,421.00 20,427,760.00 22,272,204.00 23,899,286.00 22,520,701.00

Personnel Expenses 17,538,918.00 20,697,078.00 27,198,377.00 34,757,473.00 35,240,513.00

Governance Expenses 3,907,013.00 3,814,544.00 4,854,655.00 7,046,135.00 5,327,333.00

Marketing Expenses 1,794,742.00 1,571,640.00 3,646,197.00 3,716,384.00 4,168,740.00

Depreciation and Amortization 4,353,726.00 5,355,118.00 3,053,894.00 2,720,352.00 3,153,096.00

Total Expenses 56,261,696.00 66,396,258.00 74,853,495.00 85,038,022.00 86,342,049.00

Net operating surplus before income tax

8,709,590.00 8,651,840.00 14,669,793.00 2,882,424.00 5,338,502.00

Less Income tax Expense (162,482.00) (239,662.00) (46,732.00) (139,621.00) (153,538.00)

Page 1 of 42

Net operating surplus after income Tax

8,547,108.00 8,412,178.00 14,623,061.00 2,742,803.00 5,184,919.00

Page 2 of 42

Appendix 3 Statement of Financial position 2011-2015

2011 2012 2013 2014 2015

KSHS

ASSETS

Cash and cash equivalents 69,872,411 57,112,735 167,852,179 111,452,662 97,072,945

Receivables and prepayments 8,584,572 15,707,523 28,395,658 28,460,796 30,868,025

Loans and advances 283,310,659 299,921,101 359,647,266 403,855,548 523,121,578

Financial Assets 3,804,326 3,823,596 3,845,675 3,863,340 3,884,610

Intangible Assets 3,926,618 6,044,424 4,553,318 6,007,295 4,933,238

Property,Plant and Equipment 8,191,927 7,850,906 6,765,397 7,714,291 6,874,916

TOTAL ASSETS 377,690,513 390,460,285 571,039,492 561,353,932 666,755,312

LIABILITIES AND EQUITY

LIABILITIES

Bank overdrafts - - 100,393,166 67,517,961 72,930,346

Members' Deposits 199,485,212 220,284,254 295,776,555 321,205,368 375,885,986

Current income tax 162,482 239,662 46,732 139,621 153,583

Payables Accruals 2,549,372 2,765,229 9,320,903 20,121,668 18,680,796

Payables to members and board 755,859 3,804,087 3,695,884 1,624,002 5,111,785

Borrowings 102,028,291 77,711,469 64,119,498 56,405,250 95,949,184

Grants and donations 3,265,744 1,866,139 466,534 - -

Total liabilities 308,246,960 306,670,840 473,819,272 467,013,870 568,711,680

EQUITY

Share capital 54,036,000 60,420,000 60,420,000 60,420,000 60,420,000

Reserves 15,407,553 23,369,443 36,800,219 33,920,063 37,623,632

Total equity 69,443,553 83,789,443 97,220,219 94,340,063 98,043,632

TOTAL LIABILITIES AND EQUITY 377,690,513 390,460,283 571,039,492 561,353,932 666,755,312

Page 3 of 42

Appendix 4 Projected Statement of Financial Position2016-2020 2015 2016 2017 2018 2019 2020

Kes. Kes. Kes. Kes. Kes Kes.

ASSETS

Cash & Cash Equivalent 24,142,599 51,995,815 154,288,198 135,606,603 194,660,922 199,076,077

Cash in hand(both local and foreign notes and coins) 4,347,836 8,695,672 13,043,508 19,565,262 29,347,893 44,021,840

Cash at bank:(placement with financial institutions) 19,794,763 43,300,143 141,244,690 116,041,341 165,313,029 155,054,238

Prepayments & Sundry Receivables 30,868,025 24,694,420 19,755,536 15,804,429 12,643,543 10,114,834

Financial Investments 3,884,610 3,907,217 3,930,049 3,953,110 3,976,402 3,999,927

Government Securities - Treasury Bills/bonds, - - - - - -

Other Securities - Commercial papers/Bonds - - - - - -

Balances with other SACCO Societies 2,260,666 2,283,273 2,306,105 2,329,166 2,352,458 2,375,983

Investments in companies - shares/stocks 1,623,944 1,623,944 1,623,944 1,623,944 1,623,944 1,623,944

Net Loan Portfolio 523,121,578 684,555,529 895,319,161 1,170,391,277 1,529,280,301 1,997,390,361

Gross Loan Portfolio 568,096,354 738,525,260 960,082,838 1,248,107,690 1,622,539,997 2,109,301,996

Allowance for Loan Loss 44,974,776 53,969,731 64,763,677 77,716,413 93,259,696 111,911,635

Accounts Receivables

Property & Equipment & Other assets 11,808,154 28,796,629 24,858,100 21,723,936 19,635,448 25,526,082

Investment Properties - - - - - -

Property & Equipment 6,874,916 8,937,391 11,618,608 15,104,190 19,635,448 25,526,082

Prepaid Lease rentals - - - - - -

Intangible Assets 4,933,238 19,859,238 13,239,492 6,619,746 - -

Other Assets - - - - - -

Total Assets 593,824,966 793,949,610 1,098,151,044 1,347,479,355 1,760,196,616 2,236,107,281

Page 4 of 42

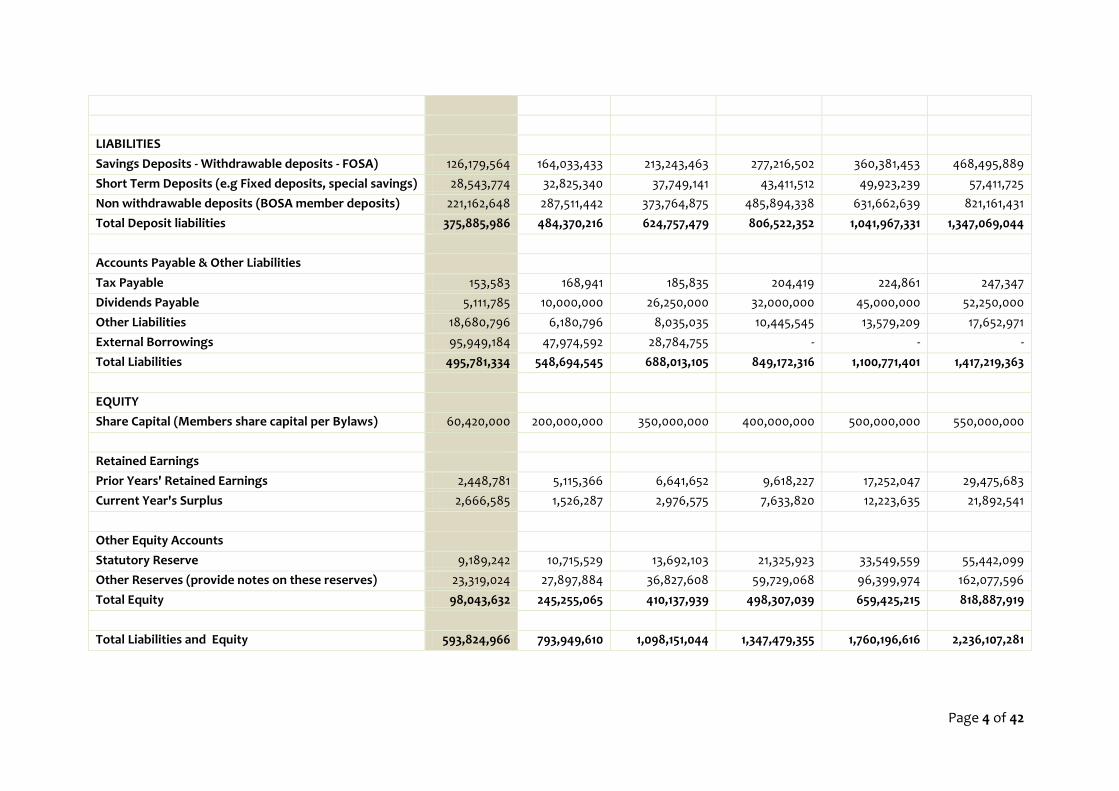

LIABILITIES

Savings Deposits - Withdrawable deposits - FOSA) 126,179,564 164,033,433 213,243,463 277,216,502 360,381,453 468,495,889

Short Term Deposits (e.g Fixed deposits, special savings) 28,543,774 32,825,340 37,749,141 43,411,512 49,923,239 57,411,725

Non withdrawable deposits (BOSA member deposits) 221,162,648 287,511,442 373,764,875 485,894,338 631,662,639 821,161,431

Total Deposit liabilities 375,885,986 484,370,216 624,757,479 806,522,352 1,041,967,331 1,347,069,044

Accounts Payable & Other Liabilities

Tax Payable 153,583 168,941 185,835 204,419 224,861 247,347

Dividends Payable 5,111,785 10,000,000 26,250,000 32,000,000 45,000,000 52,250,000

Other Liabilities 18,680,796 6,180,796 8,035,035 10,445,545 13,579,209 17,652,971

External Borrowings 95,949,184 47,974,592 28,784,755 - - -

Total Liabilities 495,781,334 548,694,545 688,013,105 849,172,316 1,100,771,401 1,417,219,363

EQUITY

Share Capital (Members share capital per Bylaws) 60,420,000 200,000,000 350,000,000 400,000,000 500,000,000 550,000,000

Retained Earnings

Prior Years' Retained Earnings 2,448,781 5,115,366 6,641,652 9,618,227 17,252,047 29,475,683

Current Year's Surplus 2,666,585 1,526,287 2,976,575 7,633,820 12,223,635 21,892,541

Other Equity Accounts

Statutory Reserve 9,189,242 10,715,529 13,692,103 21,325,923 33,549,559 55,442,099

Other Reserves (provide notes on these reserves) 23,319,024 27,897,884 36,827,608 59,729,068 96,399,974 162,077,596

Total Equity 98,043,632 245,255,065 410,137,939 498,307,039 659,425,215 818,887,919

Total Liabilities and Equity 593,824,966 793,949,610 1,098,151,044 1,347,479,355 1,760,196,616 2,236,107,281

Page 5 of 42

Appendix 5 Projected Statement of Comprehensive Income2016-2020

2015 2016 2017 2018 2019 2020

Kes. Kes. Kes. Kes. Kes. Kes.

Financial Income 107,060,909 133,574,886 173,801,374 226,172,821 294,371,220 383,202,414

Financial Income from Loans Portfolio 107,060,909 133,574,886 173,801,374 226,172,821 294,371,220 383,202,414

Interest on Loan Portfolio 102,157,515 132,804,770 172,646,200 224,440,060 291,772,079 379,303,702

Fees & Commission on Loan Portfolio 4,518,336 5,873,837 7,635,988 9,926,784 12,904,819 16,776,265

Financial Income from Investments in: 385,058 770,116 1,155,174 1,732,761 2,599,142 3,898,712

Government Securities

Deposit with Banks and Other Financial Inst.

Other Investments - dividend & Interest incomes from investments

385,058 770,116.00 1,155,174.00 1,732,761.00 2,599,141.50 3,898,712.25

Other Operating Income- Salary processing fees, transaction fees, membership fees

Financial Expense 21,287,129 30,803,581 42,279,040 48,201,772 65,531,743 78,516,818

Interest Expense on Deposits 6,891,512 8,958,966 11,646,655 15,140,652 19,682,847 25,587,702

Cost of External Borrowings 8,488,846 10,186,615 3,055,985 - - -

Dividend Expenses (on member shares) 1,711,785 10,000,000 26,250,000 32,000,000 45,000,000 52,250,000

Other Financial Expense 4,194,986 1,658,000 1,326,400 1,061,120 848,896 679,117

Net Financial Income/(Loss) 85,773,780 102,771,305 131,522,335 177,971,050 228,839,477 304,685,596

Allowance for Loan Loss 9,379,457 8,994,955 10,793,946 12,952,735 15,543,283 18,651,939

Provision for Loan Losses 9,379,457 8,994,955 10,793,946 12,952,735 15,543,283 18,651,939

Value of Loans Recovered

Operating Expenses 72,767,606 85,975,976 105,659,678 126,644,795 151,953,157 176,323,607

Page 6 of 42

Personnel Expenses 35,240,513 40,526,590 46,605,578 55,926,694 67,112,033 80,534,440

Governance Expenses 5,327,333 6,392,800 7,671,360 9,205,631 11,046,758 13,256,109

Marketing Expenses 4,168,740 5,419,362 7,045,171 9,158,722 11,906,338 15,478,240

Depreciation and Amortization Charges 3,153,096 3,783,715 8,513,359 9,364,695 10,301,165 5,150,582

Administrative Expenses 24,877,924 29,853,509 35,824,211 42,989,053 51,586,863 61,904,236

Net Operating Income 3,626,717 7,800,374 15,068,710 38,373,519 61,343,037 109,710,050

Net Income (Before Taxes and Donations) 3,626,717 7,800,374 15,068,710 38,373,519 61,343,037 109,710,050

Taxes (Incomes taxes & Other payable to KRA) 153,583 168,941 185,835 204,419 224,861 247,347

Net Income/(After Taxes and Donations) 3,473,134 7,631,433 14,882,875 38,169,100 61,118,176 109,462,703

Page 7 of 42

Appendix 6 Projected Financial ratios

2015 2016 2017 2018 2019 2020

Total Asset value of on-balance sheet items as per 2.8 above

593,824,966

793,949,610

1,098,151,044

1,347,479,355

1,760,196,616

2,236,107,281

Total Asset value of off-balance sheet items as per 3 above

- - - - - -

Total Assets (4.1 + 4.2) 593,824,966

793,949,610

1,098,151,044

1,347,479,355

1,760,196,616

2,236,107,281

Total Deposits Liabilities (As per Balance Sheet) 375,885,986

484,370,216

624,757,479

806,522,352

1,041,967,331

1,347,069,044

Core capital to Assets Ratio (1.1.12/4.3%) 16% 31% 37% 37% 37% 37%

Minimum Core Capital to Assets Ratio Requirement 10% 10% 10% 10% 10% 10%

Excess (deficiency) (4.5 less 4.6) 6% 21% 27% 27% 27% 27%

Institutional Capital to Assets Ratio(1.1.13/4.3)% 6% 6% 5% 7% 9% 12%

Minimum Institutional to Assets Ratio requirement 8% 8% 8% 8% 8% 8%

Excess/(Deficiency) (4.8 less 4.9) -2% -2% -3% -1% 1% 4%

Core capital to Deposits Ratio (1.1.12/4.4%) 26% 50% 65% 62% 63% 61%

Minimum Core Capital to Deposits Requirement 8.00% 8.00% 8.00% 8.00% 8.00% 8.00%

Excess (Deficiency) (4.11 less 4.12) 18% 42% 57% 54% 55% 53%

Page 8 of 42

Appendix 7Organizational Structure

Page 9 of 42