infrastructure project finance (ipf) guidelines and regulations

DESCRIPTION

Infrastructure Project Finance (IPF) Guidelines and Regulations. Infrastructure, Housing & SME Finance Department. Benefits of Infrastructure Development. Development of Infrastructure enhances Public Assets - PowerPoint PPT PresentationTRANSCRIPT

INFRASTRUCTURE PROJECT FINANCE (IPF) GUIDELINES AND REGULATIONS

Infrastructure, Housing & SME Finance Department

BENEFITS OF INFRASTRUCTURE DEVELOPMENT

Development of Infrastructure enhances Public Assets

Quality infrastructure improves the investment climate

for foreign direct investment (FDI) by reducing costs

Enhances export competitiveness

Creates employment

Improves living conditions of public

Higher tax revenue of government

IMPEDIMENTS TO INFRASTRUCTURE PROJECT FINANCING IN PAKISTAN

Transaction amount in the infrastructure sector is sizable

compared to the size of many banks/DFIs

Project financing is not a high priority due to reluctance to

undertake long term payback ventures

There is a lack of specialized project finance expertise

within commercial banks/DFIs

Absence of long-term debt instruments/bond market

TREND IN IPF

Based on data collected from Banks/DFIs on Infrastructure Project Financing, it has been observed that financing has decreased over the years

TOTAL AMOUNT OUTSTANDING UNDER INFRASTRUCTURE PROJECT FINANCING (YEARLY)

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec'13200

220

240

260

280

300

320

234.4

275.9

298.5

280.7

288.6

255.2

Bill

ion

R

s

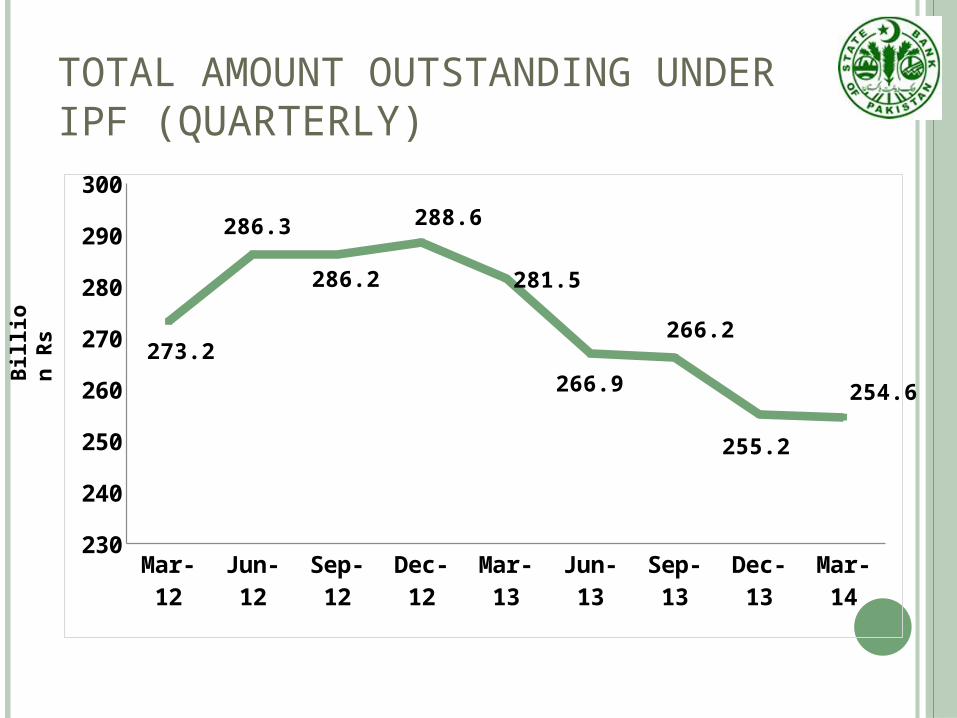

TOTAL AMOUNT OUTSTANDING UNDER IPF (QUARTERLY)

Bill

ion

R

s

Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14230

240

250

260

270

280

290

300

273.2

286.3

286.2

288.6

281.5

266.9

266.2

255.2

254.6

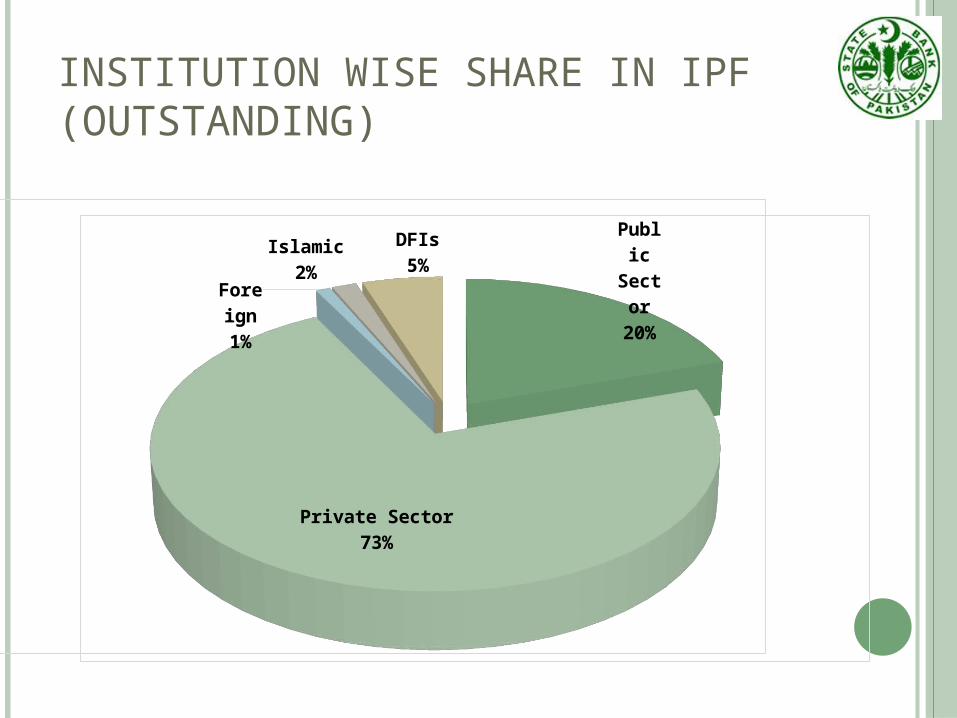

INSTITUTION WISE SHARE IN IPF (OUTSTANDING)

Public Sector20%

Private Sector73%

Foreign1%

Islamic2%

DFIs5%

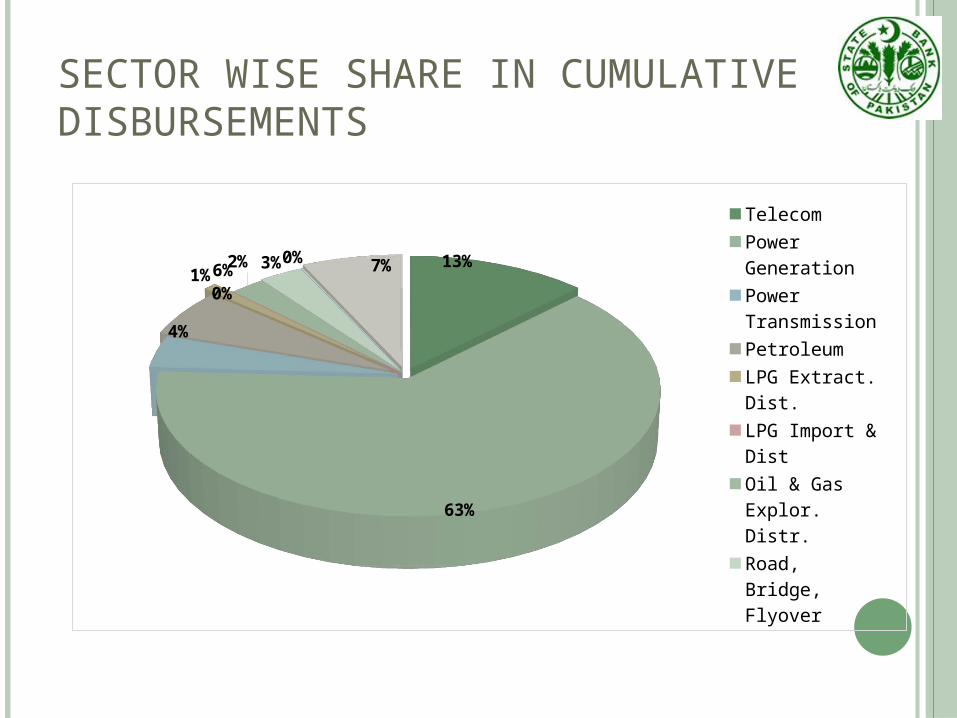

SECTOR WISE SHARE IN CUMULATIVE DISBURSEMENTS

13%

63%

4% 6%

1%

0%2%

3%0%

7%

Telecom

Power Genera-tion

Power Trans-mission

Petroleum

LPG Extract. Dist.

LPG Import & Dist

Oil & Gas Explor. Distr.

Road, Bridge, Flyover

Water Supply, Sanitation

Any other

SBP INITIATIVES

Issuance of Guidelines on Infrastructure Project Financing

Capacity development programs for Banks/DFIs

Establishment of Infrastructure Task Force

Facilitation in establishment of Infrastructure Development

Finance Institution (IDFI) – (Concept Paper Preparation) Consultation with various stakeholders through workshops,

seminars and working groups.

Quarterly Infrastructure Project Financing review.

INFRASTRUCTURE DEVELOPMENT AND FINANCING INSTITUTION (IDFI)

Need Asset / Liability mismatch in banks/DFIs as most of the deposits are of short

tenor. Lack of adequate funding for large infrastructure projects

IDFI will perform a broad array of activities:• Project Development – need identification, conceptualization, pre-feasibility

reports, commercial viability aspects, identification of potential investors• Use of innovative structural / financial techniques to enhance project viability• Evaluate infrastructure projects for potential investment• Project Finance – equity participation, loan syndication, other services• Facilitate access to Viability Gap Fund• Tariff and other advisory services• Facilitate co-ordination of project sponsors with relevant ministries and

government departments• Performance Monitoring• May help government in PPP policy formulation

Primary focus will be on:Power SectorSpecial Economic ZonesAgricultural Infrastructure including warehousing,

cold chains etc.

Other sectors like road, railway and port etc. would also be considered later on subject to capacity enhancement

Long term funding mechanism to develop a financial climate conducive to large scale infrastructure projects

INFRASTRUCTURE DEVELOPMENT AND FINANCING INSTITUTION (IDFI)

IDFI Scope and Structure

• Proposed IDFI to be established as a special DFI with suggested Equity Distribution as follows:- Banks/DFIs - 25%- GoP or government organizations - 25%- Multilateral Agencies - 50%

• The company will issue long term papers/Bonds/Sukuk to generate funds from local market and also seek funding and guarantee lines from international MLAs to support/finance infrastructure projects in Pakistan. By issuing bonds/Sukuk, it would help develop capital market.

SBP Guidelines/Regulatory Framework - History Relaxation in Prudential Regulations for Infrastructure Project Financing (IPF) vide BPD Circular

No.25 dated July 04, 2003 (http://www.sbp.org.pk/bpd/2003/C25.htm). Debt equity relaxed to 80:20 for the Infrastructure projects “Concession Agreement/License/Right of Way” issued by Government accepted as a collateral

Updated IPF Guidelines in August 31, 2010 vide No. IHFD/11 /191/ 2010. The salient features of the revised guidelines:- Includes the requirement for establishing a mechanism for generating feasibility reports and

assessing risk mitigation means in the development, construction, start-up and operation stages of the project.

Banks and DFIs to establish a proper process for the continuous monitoring of project implementation to ensure proper utilization of the credit while relevant bank accounts will be subject to audit by the SBP.

Banks and DFIs encouraged to accept Concession Agreement/Lisence issued by a government agency as collateral.

The institutions to ensure adequate insurance coverage against all potential risks applicable to the project.

At no point shall the bank’s exposure to the risk exceed the bank’s equity, and the exposure availed by any borrower shall also not exceed 10 times the borrower’s equity.

13

SBP Guidelines – Areas Covered

14

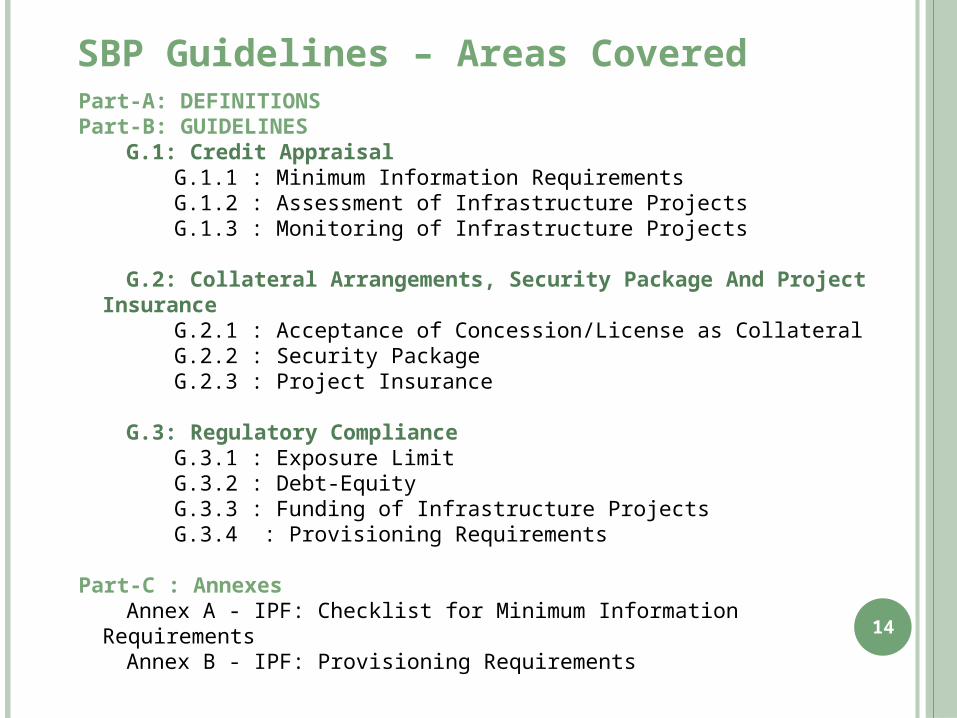

Part-A: DEFINITIONSPart-B: GUIDELINES

G.1: Credit AppraisalG.1.1 : Minimum Information RequirementsG.1.2 : Assessment of Infrastructure ProjectsG.1.3 : Monitoring of Infrastructure Projects

G.2: Collateral Arrangements, Security Package And Project Insurance G.2.1 : Acceptance of Concession/License as CollateralG.2.2 : Security PackageG.2.3 : Project Insurance

G.3: Regulatory ComplianceG.3.1 : Exposure LimitG.3.2 : Debt-EquityG.3.3 : Funding of Infrastructure ProjectsG.3.4 : Provisioning Requirements

Part-C : AnnexesAnnex A - IPF: Checklist for Minimum Information RequirementsAnnex B - IPF: Provisioning Requirements

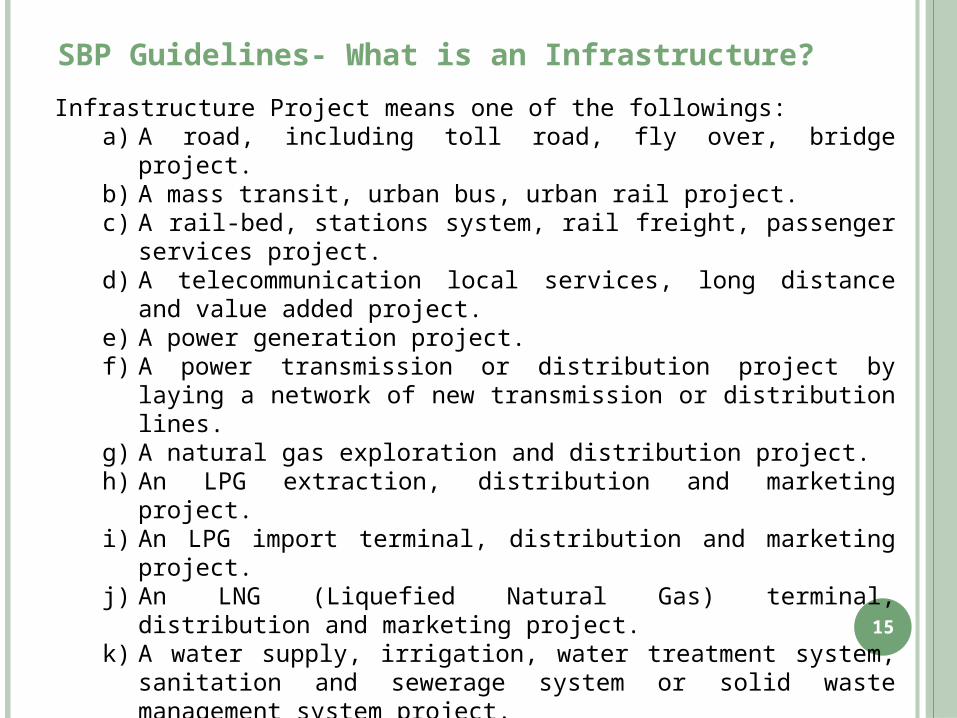

SBP Guidelines- What is an Infrastructure?

15

Infrastructure Project means one of the followings: a) A road, including toll road, fly over, bridge project.b) A mass transit, urban bus, urban rail project.c) A rail-bed, stations system, rail freight, passenger services project.d) A telecommunication local services, long distance and value added project.e) A power generation project.f) A power transmission or distribution project by laying a network of new

transmission or distribution lines.g) A natural gas exploration and distribution project.h) An LPG extraction, distribution and marketing project.i) An LPG import terminal, distribution and marketing project.j) An LNG (Liquefied Natural Gas) terminal, distribution and marketing project.k) A water supply, irrigation, water treatment system, sanitation and sewerage

system or solid waste management system project.l) A dam, barrage, canal project.m) A primary and secondary irrigation, tertiary (on-farm) irrigation project.n) A port, channel dredging, shipping, inland waterway, container terminals

project.o) An airport.p) A petroleum extraction, refinery, pipeline project.q) Any other infrastructure project of similar nature, notified by SBP.

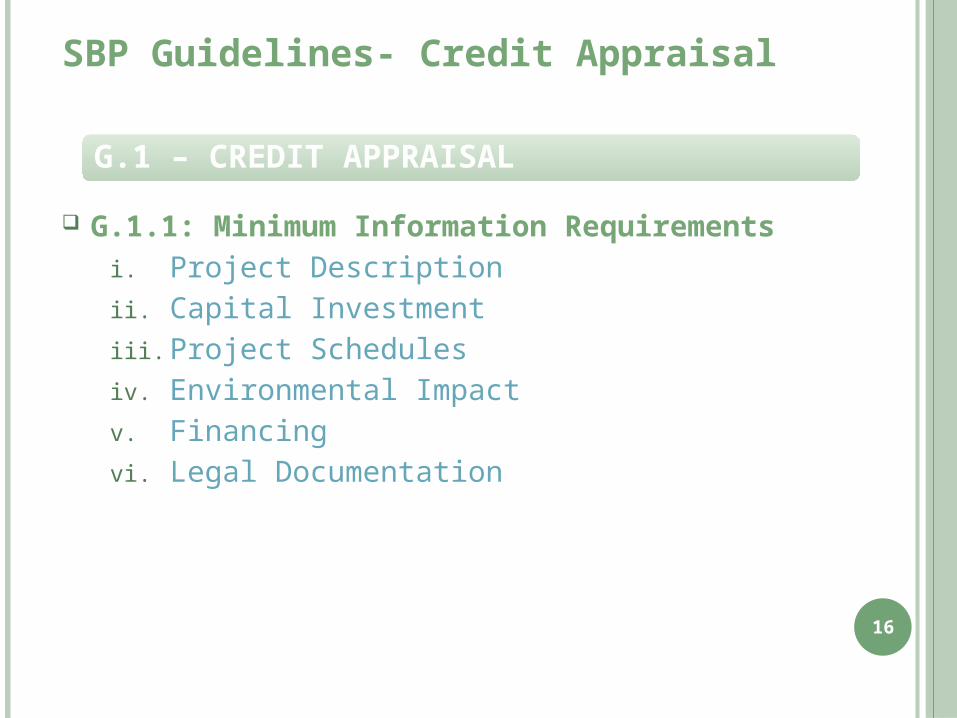

SBP Guidelines- Credit Appraisal

G.1.1: Minimum Information Requirementsi. Project Descriptionii. Capital Investmentiii. Project Schedulesiv. Environmental Impactv. Financingvi. Legal Documentation

16

G.1 – CREDIT APPRAISAL

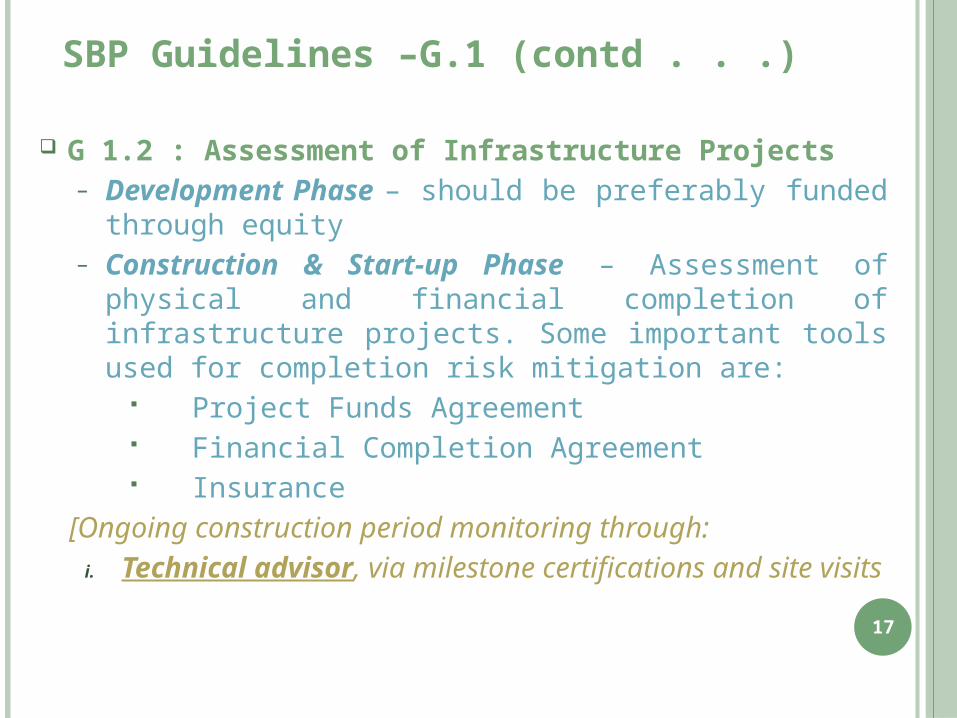

SBP Guidelines –G.1 (contd . . .)

G 1.2 : Assessment of Infrastructure Projects– Development Phase – should be preferably funded through

equity – Construction & Start-up Phase – Assessment of physical and

financial completion of infrastructure projects. Some important tools used for completion risk mitigation are:

Project Funds Agreement Financial Completion Agreement Insurance

[Ongoing construction period monitoring through:i. Technical advisor, via milestone certifications and site visits

17

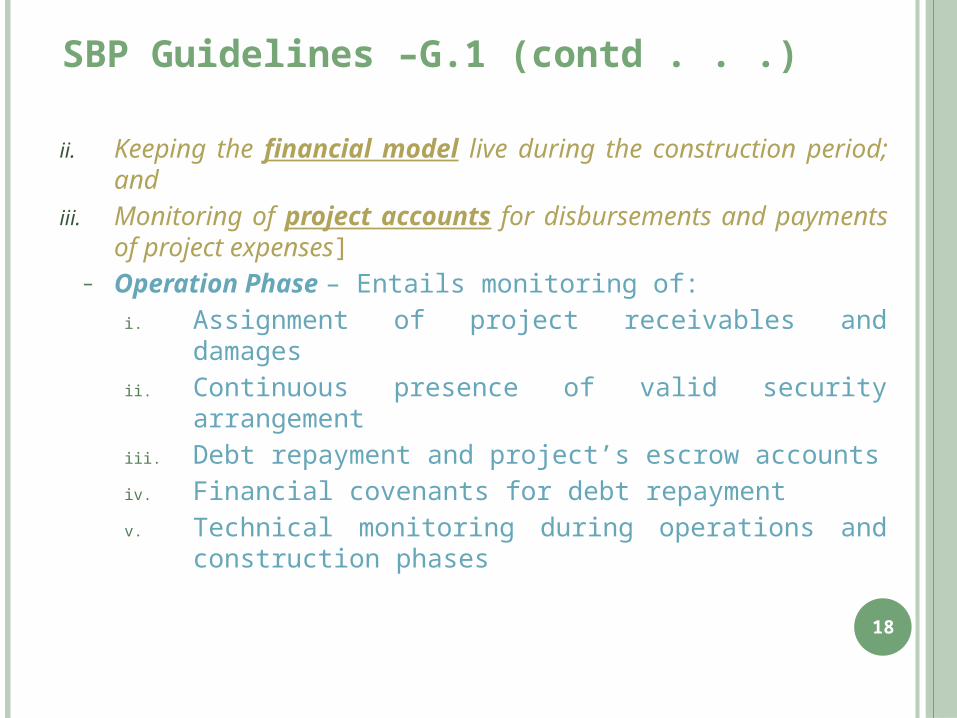

ii. Keeping the financial model live during the construction period; and

iii. Monitoring of project accounts for disbursements and payments of project expenses]

– Operation Phase – Entails monitoring of:i. Assignment of project receivables and damagesii. Continuous presence of valid security arrangementiii. Debt repayment and project’s escrow accountsiv. Financial covenants for debt repaymentv. Technical monitoring during operations and

construction phases

18

SBP Guidelines –G.1 (contd . . .)

G.1.3 : Monitoring of Infrastructure Projects

Monitoring for assignment of Project Receivables and

Payments for Damages.

Monitoring for ensuring enforcement of Security

Projects escrow accounts for Monitoring of Repayment of

Debt.

Financial Covenants for Repayment of Debt.

Technical Monitoring during Development and Operation

Phase.19

SBP Guidelines –G.1 (contd . . .)

SBP Guidelines- G.2

G.2.1: Acceptance of Concession/license as collateral –

encumbrance free, assignable, transferable in the event of default

G.2.2: Security Package –

– Primary Security – first charge over project receivables and

accounts

– Secondary Security – standard security package of the lenders

including hypothecation, mortgage, insurance assignment, share

pledge, assignment over rights under all project documents etc

G.2.3: Project Insurances - construction all risks, third party liability,

marine, accidental, loss of profit, terrorism insurance etc.

20

G.2 – COLLATERAL ARRANGEMENT, SECURITY PACKAGE & PROJECT INSURANCE

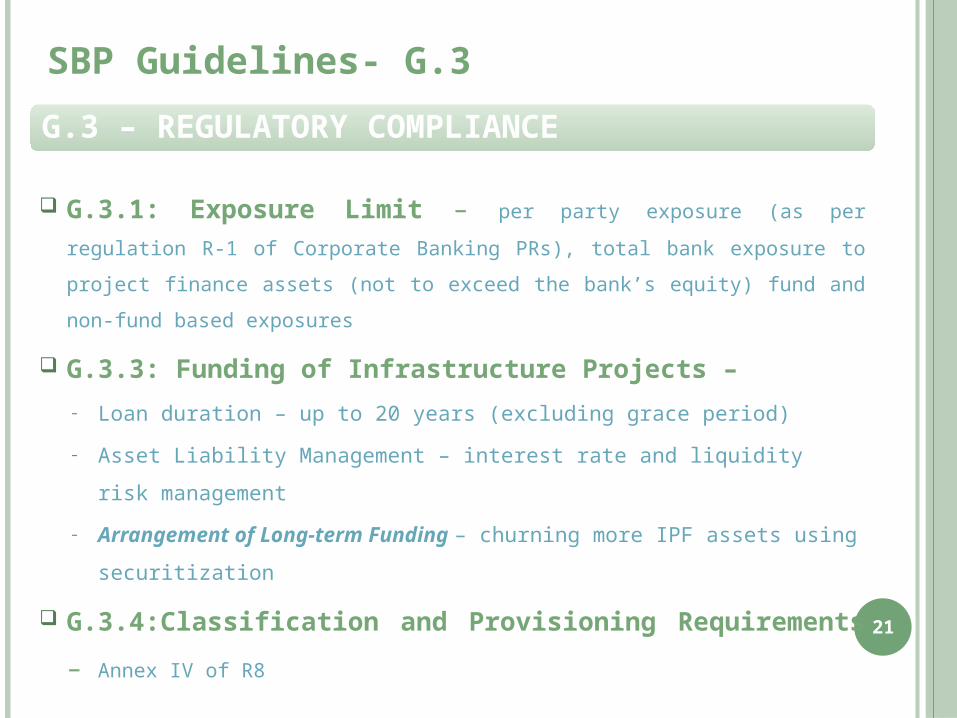

SBP Guidelines- G.3

G.3.1: Exposure Limit – per party exposure (as per regulation R-1 of

Corporate Banking PRs), total bank exposure to project finance assets (not to

exceed the bank’s equity) fund and non-fund based exposures

G.3.3: Funding of Infrastructure Projects – – Loan duration – up to 20 years (excluding grace period)

– Asset Liability Management – interest rate and liquidity risk management

– Arrangement of Long-term Funding – churning more IPF assets using

securitization

G.3.4:Classification and Provisioning Requirements – Annex

IV of R821

G.3 – REGULATORY COMPLIANCE

PR R-1: Limit on Exposure to a Single Person/Group

22

5. For the purpose of this regulation banks/DFIs are required to follow the guidelines given at Annexure-I.

Effective Date For Single Person For Group

Total O/S (Fund & Non Fund

Based) exposure limit

Fund based O/S Limit

Total O/S (Fund & Non Fund

Based) exposure limit

Fund based O/S Limit

31-12-2009 30 20 45 35

31-12-2010 30 20 40 35

31-12-2011 30 20 35 30

31-12-2012 30 20 30 25

31-12-2013 25 25 25 25

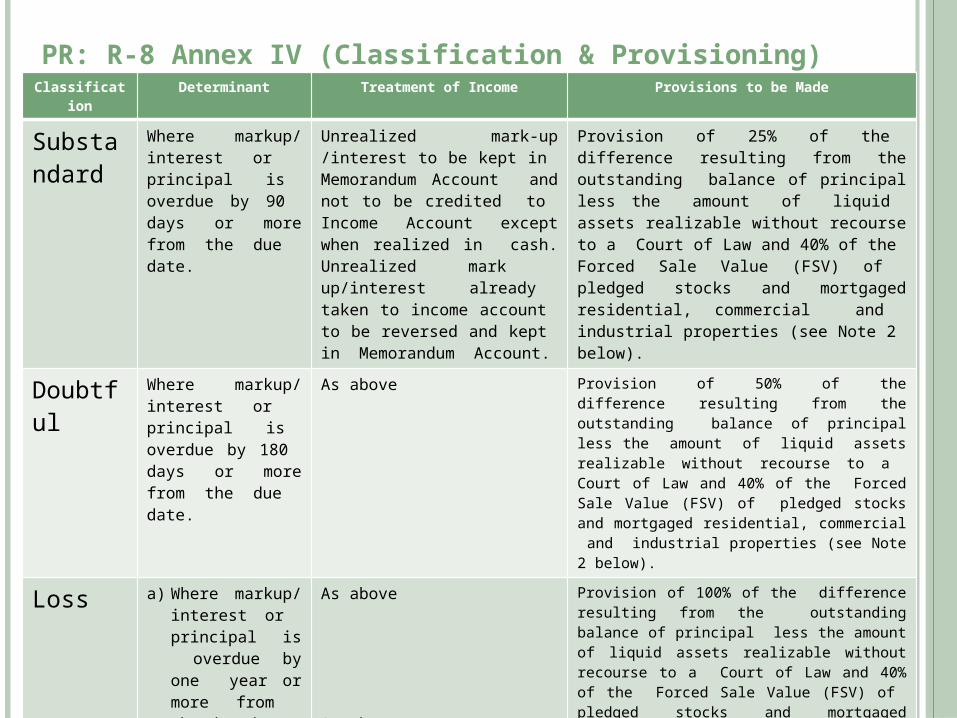

PR: R-8 Annex IV (Classification & Provisioning)

23

Classification Determinant Treatment of Income Provisions to be Made

Substandard

Where markup/ interest or principal is overdue by 90 days or more from the due date.

Unrealized mark-up /interest to be kept in Memorandum Account and not to be credited to Income Account except when realized in cash. Unrealized mark up/interest already taken to income account to be reversed and kept in Memorandum Account.

Provision of 25% of the difference resulting from the outstanding balance of principal less the amount of liquid assets realizable without recourse to a Court of Law and 40% of the Forced Sale Value (FSV) of pledged stocks and mortgaged residential, commercial and industrial properties (see Note 2 below).

Doubtful Where markup/ interest or principal is overdue by 180 days or more from the due date.

As above Provision of 50% of the difference resulting from the outstanding balance of principal less the amount of liquid assets realizable without recourse to a Court of Law and 40% of the Forced Sale Value (FSV) of pledged stocks and mortgaged residential, commercial and industrial properties (see Note 2 below).

Loss a) Where markup/ interest or principal is overdue by one year or more from the due date

b) Where Trade Bills (Import/Export or Inland Bills) are not paid/adjusted within 180 days of the due date.

As above

As above

Provision of 100% of the difference resulting from the outstanding balance of principal less the amount of liquid assets realizable without recourse to a Court of Law and 40% of the Forced Sale Value (FSV) of pledged stocks and mortgaged residential commercial and industrial properties (see Note 2 below). Benefit of FSV against NPLs shall not be available after 3 years from the date of classification of the Loan/Advance. However, the 40% benefit of FSV of land (open plot and separate valuation of land if building is constructed) shall be available for 4 years from the date of classification of loan. As above.

Notes :1. Classified loans/advances that have been guaranteed by the Government would not require provisioning, however, mark up/interest on such accounts

to be taken to Memorandum Account instead of Income Account.2. FSV shall be determined in accordance with the guidelines contained in Annexure-V to these Regulations.

List of abbreviations used

24

SPV Special Purpose VehicleSECP Securities & Exchange Commission of PakistanBPD Banking Policy Department, State Bank of Pakistan - Now Banking Policy and Regulation DepartmentSBP State Bank of PakistanDFI Development Finance InstitutionLPG Liquefied Petroleum GasLNG Liquefied Natural GasIPF Infrastructure Project FinanceNIT National Investment TrustCOI Certificate of InvestmentNBFC Non-banking Financial CompanyTFC Term Finance CertificatePFA Project Funds AgreementLOU Letter of UnderstandingMOU Memorandum of UnderstandingFCA Financial Completion AgreementEPC Engineering, Procurement and ConstructionO & M Operation and MaintenanceCAR Contractor’s All RiskALM Asset Liability ManagementNPV Net Present Value

THANK YOU

25