ingevity · on high-growth end-use applications 125 projected market growth and share by product...

TRANSCRIPT

Ingevity

CJS 19th Annual New Ideas for the New Year Investor Converence

January 9, 2018

1

Disclaimer

2

This presentation contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward looking statements generally include the words “may,” “could,” “should,” “believes,” “plans,” “intends,” “targets,” “will,” “expects,” “suggests,” “anticipates,” “outlook,” “continues,” “forecast,” “prospect,” “potential” or similar expressions. Forward-looking statements may include, without limitation, expected financial positions, results of operations and cash flows; financing plans; business strategies and expectations; operating plans; synergies and the potential benefits of the acquisition of Perstorp Holding AB’s (“Perstorp”) Capa™ caprolactone business (the “acquisition”); the anticipated timing of the closing of the acquisition; capital and other expenditures; competitive positions; growth opportunities for existing products; benefits from new technology and cost-reduction initiatives, plans and objectives; and markets for securities. Like other businesses, Ingevity is subject to risks and uncertainties that could cause its actual results to differ materially from its expectations or that could cause other forward-looking statements to prove incorrect. Factors that could cause actual results to materially differ from those contained in the forward-looking statements, or that could cause other forward-looking statements to prove incorrect, include, without limitation, risks related to the satisfaction of the conditions to closing the acquisition (including the failure to obtain necessary regulatory approvals) in the anticipated timeframe or at all; risks that the expected benefits from the proposed acquisition will not be realized or will not be realized within the expected time period; the risk that the businesses will not be integrated successfully; significant transaction costs; unknown or understated liabilities; general economic and financial conditions; international sales and operations; currency exchange rates and currency devaluation; compliance with U.S. and foreign regulations; attracting and retaining key personnel; conditions in the automotive market or adoption of alternative technologies; worldwide air quality standards; government infrastructure spending; declining volumes in the printing inks market; the limited supply of crude tall oil (“CTO”); lack of access to sufficient CTO; access to and pricing of raw materials; competition from producers of substitute products and new technologies; and new or emerging technologies; a prolonged period of low energy prices; the provision of services by third parties at several facilities; natural disasters, such as hurricanes, winter or tropical storms, earthquakes, floods, fires; other unanticipated problems such as labor difficulties including renewal of collective bargaining agreements, equipment failure or unscheduled maintenance and repair; protection of intellectual property and proprietary information; information technology security risks; government policies and regulations, including, but not limited to, those affecting the environment, climate change, tax policies and the chemicals industry; and lawsuits arising out of environmental damage or personal injuries associated with chemical or other manufacturing processes. These and other important factors that could cause actual results or events to differ materially from those expressed in forward-looking statements that may have been made in this document are and will be more particularly described in our filings with the U.S. Securities and Exchange Commission, including our Form 10-K for the year ended December 31, 2017 and our other periodic filings. Readers are cautioned not to place undue reliance on Ingevity’s projections and forward-looking statements, which speak only as the date thereof. Ingevity undertakes no obligation to publicly release any revision to the projections and forward-looking statements contained in this presentation, or to update them to reflect events or circumstances occurring after the date of this presentation. The financial results for Perstorp’s Capa™ caprolactone business in this presentation have been derived from unaudited financial records prepared by Perstorp, without adjustment to conform to the accounting policies and methodologies used by Ingevity. Neither Perstorp’s, nor Ingevity’s auditors, have audited, reviewed, compiled or performed any procedures with respect to the financial results of Perstorp’s Capa™ caprolactone business . The accounting policies and methodologies used by Perstorp’s Capa™ caprolactone business differ in certain respects from those used by Ingevity. The audited financial statements of Perstorp’s Capa™ caprolactone business will be delivered to Ingevity prior to closing. The actual audited results of Perstorp’s Capa™ caprolactone business therefore may differ from those provided herein due to the completion of the financial closing and auditing procedures under U.S. GAAP, application of financial adjustments, and other developments.

Non-GAAP Financial Measures

This presentation includes certain non‐GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures.

Reconciliations of non‐GAAP financial measures to GAAP financial measures are provided within the Appendix to this presentation. Investors are

urged to consider carefully the comparable GAAP measures and the reconciliations to those measures provided.

Ingevity Announces

Agreement to Acquire

Perstorp’s CapaTM

Caprolactone

Division

Announced December 10, 2018

Transaction Overview

Transaction

Value

Cash purchase price of €590 million (~$675 million1)

~11x 2018E adjusted EBITDA2

Assumes no synergies or tax benefits

Expected EPS accretive in year one

To be financed under existing credit facilities and cash

Pro forma 2018E net leverage: ~3.5x

Expected to deleverage to below 3.0x by end of 2019

Ingevity has reached an agreement to acquire the CapaTM

caprolactone division of Perstorp Holding AB

Anticipated closing late in the first quarter of 2019, subject to

regulatory approvals and other customary conditions

To be integrated into Performance Chemicals segment as

“Engineered Polymers”

Financing

Summary

(1) EUR / USD exchange rate: 1.15; purchase price subject to customary closing adjustments

(2) Earnings before interest, taxes, depreciation and amortization.

4

CapaTM Caprolactone Business Overview

5

Capa holds the #1 market position in caprolactone technologies, with only two other major competitors worldwide

Caprolactone is a critical input to many high-growth end-use applications

Note: Caprolactone is not caprolactam

Highly profitable and scalable business

Expected 2018 sales of ~$175 million (1)

Adj. EBITDA of ~$60 million Adj. EBITDA margins of mid-30s percent

Single plant operation in Warrington, U.K.

Experienced management team with approximately 90 employees globally

Revenue by Product and Geography (2018E)

Source: Company information

Polyols

47%

Thermoplastics

25%

HDO

3%

Caprolactone

25% Americas

31%

EMEA

44%

APAC

25%

(1) EUR / USD exchange rate: 1.15

Market Use Benefits End-Products

Coatings Capa Polycaprolactonesfor High-Performance Polyurethane Coatings

• High gloss• Weathering resistance• Flexibility• Toughness• Self-healing

• Aerospace coatings• Automotive coatings• Specialty flooring

coatings• Windmill coatings

Resins Capa-based Polyurethane dispersions and UV-curable resins

• Wear resistance• Anti-weathering• Cracking resistance

• Automotive and aerospace coatings

• Wood flooring coatings• Leather coatings

Elastomers Capa Polyols for thermoplastic polyurethane or cast elastomers

• Durability• Resistance to wear and

tear• Thermal stability• Ease of processing

• Tires for forklifts• Skateboard wheels• Roller coaster wheels• Running shoe soles• Gaskets and O-rings

Adhesives Capa Thermoplastics for hot melt adhesives and Capa Polyols for liquid polyurethane adhesives

• Strong adhesion and bonding

• Various substrates• Durability and heat

resistance• Flexibility

• Food packaging• Textiles• Laminates• Tapes• Shoes and consumer

products

Bioplastics Capa-based biodegradable thermoplastics

• Durability• Tear resistance• Printability

• Biopolymer bags and films

• Food packaging• Plasticware• Paper coatings

CapaTM Caprolactone End-Uses and Benefits

6

Source: Company information

Value-creating Acquisition Consistent with Our Strategy

Strategic Rationale Strong, market-leading business focused

on high-growth end-use applications

Complementary fit with Ingevity business model and capabilities

– Technology-focused relationships drive customer intimacy

– Similar manufacturing process and approach

Provides new avenues for strategic growth and value creation

Top-tier financial profile, immediately accretive

7

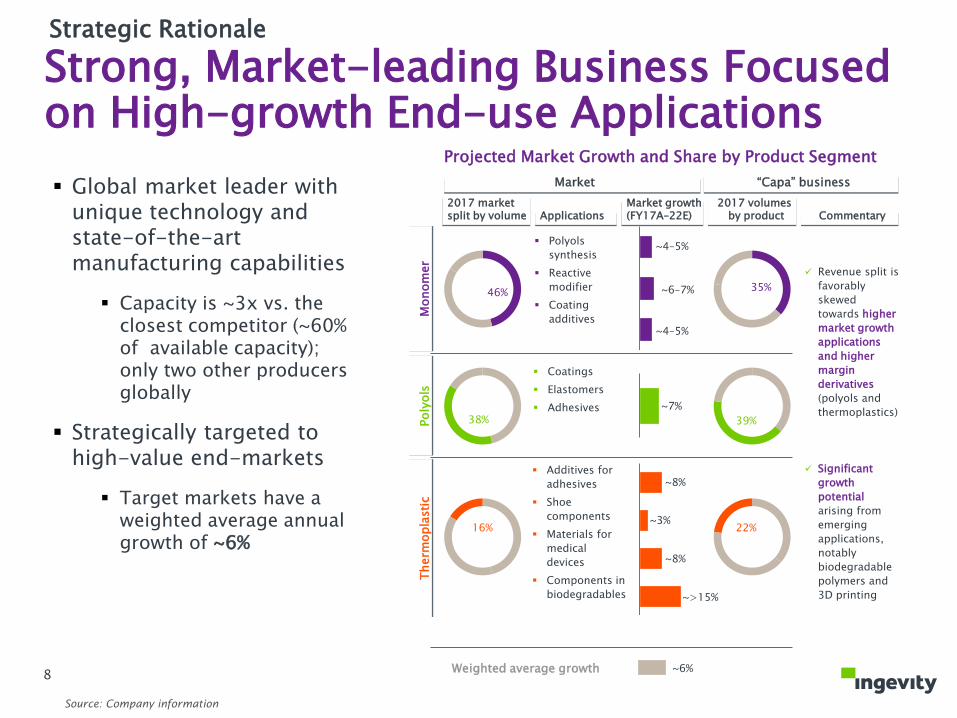

Strong, Market-leading Business Focused on High-growth End-use Applications

125

Projected Market Growth and Share by Product Segment

Monom

er

Poly

ols

Th

erm

opla

sti

c

46%

Polyols

synthesis

Reactive

modifier

Coating

additives

~4–5%

~6–7%

~4–5%

38%

Coatings

Elastomers

Adhesives ~7%

Additives for

adhesives

Shoe

components

Materials for

medical

devices

Components in

biodegradables

~8%

16%~3%

~8%

~>15%

Weighted average growth ~6%

35%

39%

22%

Revenue split is

favorably

skewed

towards higher

market growth

applications

and higher

margin

derivatives

(polyols and

thermoplastics)

Significant

growth

potential

arising from

emerging

applications,

notably

biodegradable

polymers and

3D printing

2017 market split by volume Applications

Market growth (FY17A–22E)

Market

2017 volumesby product

“Capa” business

Commentary

Global market leader with unique technology and state-of-the-art manufacturing capabilities

Capacity is ~3x vs. the closest competitor (~60% of available capacity); only two other producers globally

Strategically targeted to high-value end-markets

Target markets have a weighted average annual growth of ~6%

Source: Company information

8

Strategic Rationale

Technology-focused Relationships Drive Customer Intimacy

9

Resins & Coatings

31%

Adhesives

8%Elastomers

27%

Bioplastics

5%

Caprolactone

and Other

29%

Ingevity

overlap

Revenue by End-use Applications (2018E)

Source: Company information

Deep customer knowledge backed by 40 years of technical expertise and process know-how

Long-standing, loyal customer base with no customer representing more than 10% of sales

Proven expertise to develop tailored applications and technology solutions depending on customer needs

Potential for channel synergies over time in end-use applications where Ingevity participates, particularly coatings and adhesives

Leverage Ingevity corporate and functional resources

Strategic Rationale

Similar Manufacturing Process and Approach“Capa”

Cyclohexanone

Caprolactone

Thermoplastics

Adhesives

Bioplastics

Shoe Counters

Medical Devices

Caprolactone

Polyols

Adhesives

Coatings

Elastomers

Hydrogen

Peroxide

Hexanediol

(HDO)

Caprolactone

Lactides

Coatings

Elastomers

Compounds

3D printing

Black Liquor

SoapSulfuric acid

Rosin Fatty Acid

Rosin Esters

Adhesives

Inks

Paper size

Rubber

emulsifiers

Dimers &

Diacids

Lubricants

Intermediates

Coatings

Raw material Intermediate

Derivatives Co-product

Bio Fractions

Crude Tall Oil

(CTO)

Specialty

Formulations

Pavement

preservation

Evotherm

Oil well

service

additives

Oil

production

chemicals

Caprolactone

Monomer

Source: Company information

BasicProducts

High-Value Derivatives

10

Ingevity Performance Chemicals

Strategic Rationale

Raw Materials

Provides New Avenues for Strategic Growth and Value Creation

11

Continued growth supported by end-market macro trends in core and emerging applications

Biodegradable polymers, medical devices, 3D printing, etc.

Untapped potential for caprolactone to increase penetration via technology substitution within existing key market segments

Strong track record of innovation and new business development

Platform for further bolt on M&A opportunities in strategically-targeted, value-added thermoplastics, resins and bioplastics

Strategic Rationale

Top-tier Financial Profile, Immediately Accretive

12

2013A 2018E

Revenue Growth (2013A – 2018E)

Compelling financial profile: Strong historical growth Sustainable adj. EBITDA

margins in mid-30%s Modest capital intensity

Improves Performance Chemical segment adj. EBITDA margins by ~300bps on 2018 pro forma basis

Accretive to Ingevity overall adj. EBITDA margins by ~100 bps on 2018 pro forma basis

Expands product diversity, global reach and growth platform of Performance Chemicals segment

Expected EPS accretive in year one

Pro forma impact to PC segment revenue mix (1)

Engineered Polymers

19%Industrial Specialties

50%

Oilfield Tech. 12%

PavementTech. 19%

APAC13%

North America

64%

EMEA21%

(1) Last Twelve Month (“LTM”) from Sept. 30, 2018; standalone Ingevity product mix: 61% Industrial Specialties; 15% Oilfield Tech, 24%

Pavement Tech; Standalone Ingevity geographic mix: 73% North America, 15% EMEA; 2% South America; 10% APAC. LTM revenue of Capa

has been derived from unaudited financial records prepared by Capa, without adjustment to conform to the accounting policies and

methodologies used by Ingevity. Refer to the Disclaimer on Slide 2 of this presentation for further information regarding these financial

measures.

Strategic Rationale

South America

2%

Value-creating Acquisition Consistent with Our Strategy Furthers our purpose of purifying, protecting and

enhancing the world around us

Provides a complementary, growth platform in new and existing end-use applications

Business aligned with Ingevity strengths:

• Technology-based customer partnerships

• Reaction / purification process and derivativeproduct approach

Top-tier financial metrics and pro forma impacts translate into compelling value creation opportunity

Financed under existing facilities at comfortable leverage levels; rapid deleveraging given excellent cash generation profile of combined business

Ingevity welcomes the Capa organization and looks forward to building an even stronger Ingevity together!

13

Ingevity Overview

Performance Materials

Performance Chemicals

2017 Sales $349 million $163 million $78 million $382 million

2017 Segment EBITDA (1) $142 million $101 million

Market Position

#1 in automotive #1 or #2#1 or #2 in oil-based

muds#1 or #2

Applications Automotive

Process purification

Pavement preservation

Recycling

Evotherm® technologies

Well Service Additives

Production and Downstream

Adhesives

Agrochemicals

Lubricants

Inks

Intermediates

Select Competitors

Select Customers

Carbon TechnologiesPavement

TechnologiesOilfield Technologies

Where We Compete

(1) Please see appendices included at the end of this presentation for Ingevity's use of non-GAAP financial measures, definitions of those financial

measures as well as the reconciliation to the nearest GAAP financial measure.

Industrial Specialties

15

Revised 2018 Outlook and Guidance

($M)

Item

Current FY18

Guidance

Issued 10/25/2018

Revenue $1,100 to $1,130

Adjusted EBITDA (1)

$306 to $314

Adjusted tax rate (1)

22 - 24%

Capital

expenditures$90 to $95

Free Cash Flow (2)

$120 to $130

Net Debt Ratio (3)

~2.0x

16

PERFORMANCE CHEMICALS:

Continuing recovery in oilfield

Seasonality of pavement technologies

Favorable outlook for industrial specialties, especially in high

margin niches applications

Partial success with tall oil rosin (TOR) price increases

Price improvement in tall oil fatty acid (TOFA)

G-P pine chemicals acquisition synergy acceleration

Higher 4Q outage costs

Modest inflationary cost pressures

Full-year double-digit EBITDA growth

PERFORMANCE MATERIALS:

Continued moderation of revenue growth due to U.S. and

Canada automotive regulatory timing

China early adoption has begun

EU Euro 6d has also started

Significant 4Q outage costs

Modest inflationary cost pressures

Full-year double-digit EBITDA growth

(1) A reconciliation of Net Income to Adjusted EBITDA or Adjusted tax rate as projected for 2018 is not provided because we do not forecast Net Income as we

cannot, without unreasonable effort, estimate or predict with certainty various components of Net Income. These components, net of tax, include additional

separation costs associated with the separation from WestRock; further restructuring and other income (charges), net; additional acquisition and other related

costs associated with the acquisition of Georgia-Pacific’s pine chemical business; and revisions due to future guidance and assessment of U.S. Tax Reform.

Additionally, discrete tax items could drive variability in our projected effective tax rate. All of these components could significantly impact such financial

measures. Further, in the future other items with similar characteristics to those currently included in Adjusted EBITDA, that have a similar impact on

comparability of periods, and which are not known at this time, may exist and impact Adjusted EBITDA.

(2) Non-GAAP measure which represents Cash from Operations expected to range from $210M to $225M for FY2018 less Capital Expenditures.

(3) Defined as total debt including capital lease obligation excluding deferred financing fees less cash and cash equivalents and restricted investment divided by

annual adjusted EBITDA.

North America

71%

South America

2%

EMEA

17%

AsiaPac

10%Industrial Specialties

61%

Oilfield13%

Pavement26%

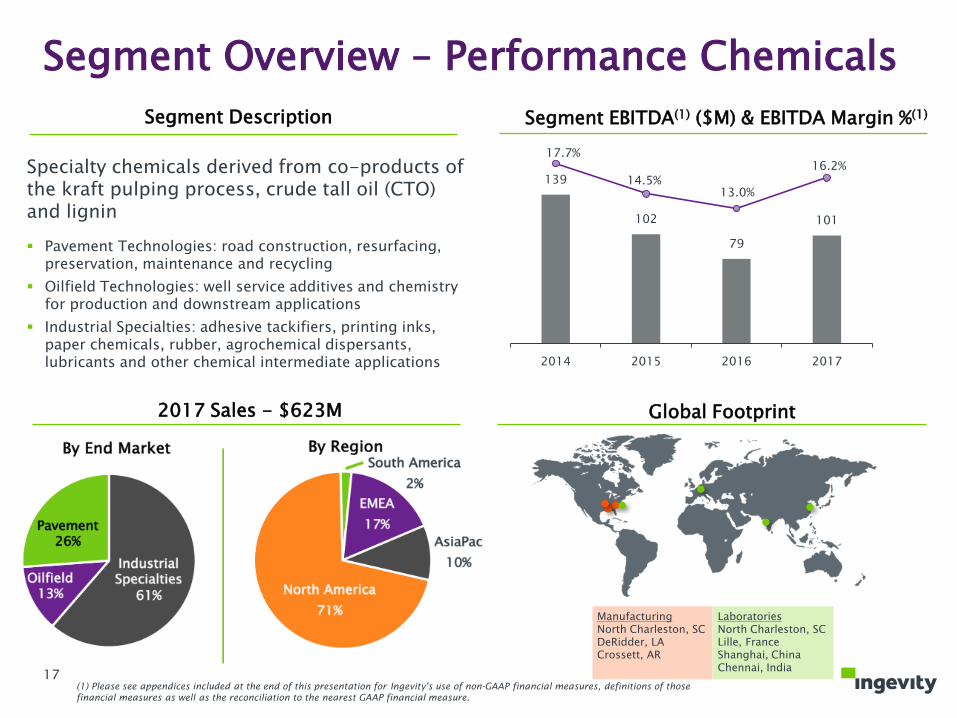

Segment Overview – Performance Chemicals

2017 Sales - $623M

By End Market By Region

Segment Description Segment EBITDA(1) ($M) & EBITDA Margin %(1)

ManufacturingNorth Charleston, SCDeRidder, LACrossett, AR

LaboratoriesNorth Charleston, SCLille, FranceShanghai, ChinaChennai, India

Global Footprint

139

102

79

101

17.7%

14.5% 13.0%

16.2%

(1.0%)

4.0%

9.0%

14.0%

19.0%

2014 2015 2016 2017

0

20

40

60

80

100

120

140

160

180

Specialty chemicals derived from co-products of the kraft pulping process, crude tall oil (CTO) and lignin

Pavement Technologies: road construction, resurfacing, preservation, maintenance and recycling

Oilfield Technologies: well service additives and chemistry for production and downstream applications

Industrial Specialties: adhesive tackifiers, printing inks, paper chemicals, rubber, agrochemical dispersants, lubricants and other chemical intermediate applications

17(1) Please see appendices included at the end of this presentation for Ingevity's use of non-GAAP financial measures, definitions of those

financial measures as well as the reconciliation to the nearest GAAP financial measure.

Biorefinery

DerivativeProducts

Pavement preservation

Evotherm (warm mix asphalt)

Asphalt recycling

Oil well service additives

Oil production & downstream chemicals

Rubber emulsifiers

Lubricants

Intermediates

Adhesives

Inks

Paper size

Rubber emulsifiers

Renewable Forests Tall Oil Fatty Acid

IntermediateProducts

Distilled Tall Oil

Tall Oil Rosin

CTO

Pine Chemicals Value ChainEnhanced value from intermediates and derivative products

18

Business Overview – Pavement Technologies

2017 Sales - $163M

By End Application By Region

Business Description Business Unit Sales

Specialty Additives for Global Asphalt Paving(1)

Construction37%

Preservation63%

132

148 149

163

100

110

120

130

140

150

160

170

2014 2015 2016 2017

Asphalt additives derived from tall oil fatty acid, lignin, amines, surfactants and polymers

Pavement Preservation: emulsifiers for specialty ultra-thin maintenance layers

Evotherm Technologies: additives for road construction in the fast growing category of warm mix asphalt

2022~$600M

2016$400M

Emulsifiers, engineered modifiers, adhesion promoters, warm mix additives, specialty polymers

3 yr CAGR +7.3%

North America

79%

EMEA8%

AsiaPac8%

South America5%

19(1) Management Estimates

North America

86%

EMEA9%

AsiaPac3%

South America2%

Drilling69%

Production31%

Business Overview - Oilfield Technologies

2017 Sales - $78M

By End Application By Region

Business Description Business Unit Sales

2016 Specialty Chemicals for Global Oilfield(1) ($M)

127

78

59

78

0

20

40

60

80

100

120

140

2014 2015 2016 2017

Specialty intermediates and TOFA used in Drilling, Production and Transportation of Crude Oil

Emulsifiers for manufacture of oil-based muds Rheology modifiers and wetting agents for used muds Imidazolines and specialty derivatives for corrosion

inhibition TOFA as raw material by integrated production service

companies TOFA and dimers part of lubricant packages in water-

based muds

(38.5%) +32.8%

(25.0%)

Emulsifiers, rheology modifiers, corrosion inhibitors, cementing agents

Drilling$500

Production$2,300

Cementing &

Stimulation$2,500

20(1) Management Estimates

TOFA & Derivative

23%

Rosin & Derivative

53%

Biofractions, Dispersants,

Other24%

Business Overview – Industrial Specialties

2017 Sales - $382M

By Material By Region

Business Description Business Unit Sales

Global Rosin & Fatty Acids(1)

Industrial chemicals based on tall oil fatty acid, tall oil rosin, and lignin for the following applications:

Tall Oil Rosin Ink resins Adhesives tackifiers Paper sizing Rubber emulsifiers

527 476

400 382

0

100

200

300

400

500

600

2014 2015 2016 2017

Industrial Specialties

(9.7%)

(4.4%)(16.0%)

North America

65%

EMEA22%

AsiaPac11%

South America

2%

Gum Rosin Resin 38%

TOR Resin16%

Terpene Resin 3%

Hydrocarbon Resin 43%

Global Resins – 2,400KT

TOFA<1%

Tallow 4%

Sunflower10%

Canola17%

Soybean29%

Palm40%

Select Fatty Acids –175KT

Tall Oil Fatty Acid Lubricants Coatings Cleaners

Biofractions Pharma phytosterols Renewable energy Roofing

Lignin Agchem dispersants Dyes dispersants

21(1) Management Estimates

Automotive

89%

Process

Purification

11% AsiaPac23%

EMEA13%

South America1%

North America63%

Segment Overview – Performance Materials

2017 Sales

By End Market By Region

Segment Description Segment EBITDA(1) ($M) & EBITDA Margin %(1)

Global Footprint

97 88

123

142 38.8%

34.4%

41.0% 40.6%

17.0%

22.0%

27.0%

32.0%

37.0%

42.0%

2014 2015 2016 2017

0

20

40

60

80

100

120

140

160

180Specialty wood-based, chemically activated carbons engineered to have the optimal porosity for gasoline evaporative emissions control:

Canisters - High capacity and superior durability granular and pellet activated carbons

“Near Zero” Canister Solutions - Activated carbon honeycombs and bulk media to control diffusion emissions

Air Intake Systems - Activated carbon sheets and honeycombs to control engine diffusion emissions

Powdered activated carbons used in purification processes for water treatment, food & beverage and chemical & pharmaceutical applications

ActivationCovington, VAWickliffe, KYZhuhai, China

Pellet ExtrusionCovington, VAWujiang, ChinaZhuhai, China

HoneycombWaynesboro, GA (JV)

Labs/Testing:North Charleston, SCZhuhai, China

(1) Please see appendices included at the end of this presentation for Ingevity's use of non-GAAP financial measures, definitions of those

financial measures as well as the reconciliation to the nearest GAAP financial measure.

22

25-35 grams/day

1970–80s technology / 0.5-1.0LOne Day Parking

1990s technology / 2.0-3.0L• Multi-day parking & running loss• Plus refueling control

Modern technology“Near Zero”2.0-3.0L + scrubber

India - China - Europe Japan - Brazil - S. Korea

US & Canada (current)China (July 2020)

U.S. & Canada (phase in 2017-2022)

Control TechnologyEmission Sources and Impact

Products That Enable Regulatory Compliance75%(1) of the world’s gasoline vehicles are currently using 70s-80s technology

Parking

13 grams/

hour driving

Running loss

75 ml / refueling

Refueling

(1) IHS

Globally, 8M gallons per day “back in the tank”

+

+

=

19%

Vehicle Sales Distribution and China 6 Adoption MapEstimated Percentages of 2019 China 6

Light Vehicle (LV) Sales

Based on Published Announcements

Yangtze

River

Delta

Pearl River

Delta

Fenwei

Plain

Chengdu-

Chongqing

Area

Henan7.0%

6.5%

Hainan0.7%

7.1%

4.1%3.0%

20.7%

Tianjin1.1%

5.9%Guangzhou

2.5%Shenzhen1.8%

Data Source: IHS, China Car Insurance Data, Ingevity estimate

Methodology: 2018 H1 sales percentages

http://www.gov.cn/xinwen/2018-07/03/content_5303212.htm

http://www.gov.cn/zhengce/content/2018-07/03/content_5303158.htm

As of Jan 1, 2019, ~8% of new LVs

sold will be expected to be China 6 compliant

As of July 1, 2019, ~63% of new LVs sold will be

expected to be China 6 compliant

Beijing1.9%

~8% ~8%

~44%

~11%

January-June2019

July-December2019

2019 LV Sales Forecast = ~26.5 million

Estimated Early China 6 Implementation

Hebei

In addition to the January 1, 2019 announced regions/cities, the China State Council has directed many major cities and areas to adopt China 6 by July 1, 2019

Effective Jan 1, 2019 (Hainan,Tianjin,Guangzhou, Shenzhen, Shandong 7 cities)

Effective July 1, 2019 (entire region)

Effective July 1, 2019 (State Council selected provinces and/or cities)

No later than July 1, 2020

Effective Jan 1, 2020 (Beijing,Tianjin)

Shandong 7 cities3.0%

https://www.henan.gov.cn/2018/09-21/692225.html

http://zfgb.tj.gov.cn/2018/system/2018/08/30/010002405.shtml

http://hebei.hebnews.cn/2018-08/28/content_7007692.htm

http://www.dtdjzx.gov.cn/staticPage/zcfg/sdzcwj/20180808/2458231.html

Adsorbed Natural Gas (ANG)Market drivers provide tremendous growth potential and deliver value across a range of vehicle users

Per-vehicle carbon content for

ANG is 100x an automotive

emissions control canister

Ingevity’s carbon adsorbents enable safe, low-pressure storage of natural gas

A hybrid, bi-fuel vehicle can service 75% of daily usage miles with natural gasoline

“At home” refueling leverages the infrastructure network already available in nearly 60 million U.S. homes and over 5 million businesses

Fuel savings for natural gas users range from $1.00 to $1.50 per gasoline gallon equivalent (GGE) compared to conventional gasoline1

Safety

Range

Convenience

Value

Auto Canister: 2 pounds ANG Monolith: 200 pounds

Value delivered to key stakeholders

Natural Gas Utility Infrastructure utilization

Natural Gas Producer Increased gas demand

Automotive OEMa) Alternative fuel option where

EVs are challengedb) Bi-fuel with a single powertrain

Vehicle Owner Sustainable fuel savings for individual and fleet operations

ANG has 2x NG volume at 900 psi

1Assumes $2.50/gal average gasoline price and $1.00/GGE natural gas cost (US Energy Information Administration)

25

Appendix

26

Non-GAAP Financial MeasuresIngevity has presented certain financial measures, defined below, which have not been prepared in accordance with U.S.

generally accepted accounting principles (“GAAP”) and has provided a reconciliation to the most directly comparable financial

measure calculated in accordance with GAAP. These financial measures are not meant to be considered in isolation or as a

substitute for the most directly comparable financial measure calculated in accordance with GAAP. The company believes

these non-GAAP measures provide investors, potential investors, securities analysts and others with useful information to

evaluate the performance of the business, because such measures, when viewed together with our financial results computed

in accordance with GAAP, provide a more complete understanding of the factors and trends affecting our historical financial

performance and projected future results.

Ingevity uses the following non-GAAP measures:

Adjusted EBITDA is defined as net income (loss) plus provision for income taxes, interest expense, depreciation and

amortization, separation costs and restructuring and other (income) charges.

Adjusted EBITDA Margin is defined as Adjusted EBITDA divided by Net Sales

Segment EBITDA is defined as segment operating profit plus depreciation and amortization.

Segment EBITDA Margin is defined as Segment EBITDA divided by Net Sales.

The Company also uses the above financial measures as the primary measures of profitability used by managers of the

business and its segments. In addition, the Company believes Adjusted EBITDA, Adjusted EBITDA Margin, Segment EBITDA

and Segment EBITDA Margin are useful measures because they exclude the effects of financing and investment activities as

well as non-operating activities. These non-GAAP financial measures are not intended to replace the presentation of financial

results in accordance with GAAP and investors should consider the limitations associated with these non-GAAP measures,

including the potential lack of comparability of these measures from one company to another. Reconciliations of these non-

GAAP financial measures are set forth within the following pages.

27

Reconciliation of Net Income (GAAP) to Adjusted EBITDA (Non-GAAP)

28

Years EndedDecember 31,

In millions, unaudited 2017 2016

Net income (loss) (GAAP) $ 145.0 $ 44.4

Provision (benefit) for income taxes 29.8 42.6

Interest expense, net 15.8 17.9

Separation costs 0.9 17.5

Depreciation and amortization 40.4 38.8

Restructuring and other (income) charges, net 3.7 41.2

Acquisition costs 7.1 —

Adjusted EBITDA (Non-GAAP) $ 242.7 $ 202.4

Net sales $ 972.4 $ 908.3

Net income (loss) margin 14.9% 4.9%

Adjusted EBITDA margin 25.0% 22.3%

Reconciliation of Segment Operating Profit (GAAP) to Segment EBITDA (Non-GAAP)

29

In millions (unaudited)Years EndedDecember 31,

Performance Materials 2017 2016

Segment operating profit (GAAP) $ 122.0 $ 106.9

Depreciation and amortization 19.8 16.4

Segment EBITDA (Non-GAAP) $ 141.8 $ 123.3

Net sales $ 349.3 $ 301.0

Segment operating margin 34.9% 35.5%

Segment EBITDA margin 40.6% 41.0%

Performance Chemicals

Segment operating profit (GAAP) $ 80.3 $ 56.7

Depreciation and amortization 20.6 22.4

Segment EBITDA (Non-GAAP) $ 100.9 $ 79.1

Net sales $ 623.1 $ 607.3

Segment operating margin 12.9% 9.3%

Segment EBITDA margin 16.2% 13.0%

Unaudited Pro Forma Segment EBITDA

30

Performance Materials

In millionsPro Forma

AdjustmentsUnaudited

Pro Forma

Segment operating profit (GAAP) $ 79.7 $ (2.7) (A) $ 77.0

Depreciation and amortization 11.1 11.1

Segment EBITDA (Non-GAAP) $ 90.8 $ 88.1

Performance Chemicals

In millionsPro Forma

AdjustmentsUnaudited

Pro Forma

Segment operating profit (GAAP) $ 86.6 $ (7.9) (A) $ 78.7

Depreciation and amortization 23.5 23.5

Segment EBITDA (Non-GAAP) $ 110.1 $ 102.2

Adjusted EBITDA (Non-GAAP) (B) $ 200.9 $ 190.3

The following unaudited pro forma measures are derived from the historical financial statements of Ingevity, prepared in accordance with U.S. generally

accepted accounting principles. These unaudited pro forma measures include adjustments required by SEC Staff Accounting Bulletin Topic 1:B-3 and Article

11 of SEC Regulation S-X. For more information regarding the Ingevity’s unaudited pro forma combined statements of operations for the year ended

December 31, 2015, see “unaudited pro forma combined financial statements” in the Ingevity’s registration statement on Form 10 and amendments thereto

(the “Form 10”), copies of which may be obtained by visiting the web site of the Securities and Exchange Commission, or the SEC, at www.sec.gov. Pro

forma adjustments give effect as if the adjustments had occurred on January 1, the first day of each respective fiscal year.

Reconciliation of Segment Operating Profit (GAAP) to Pro Forma Segment EBITDA (Non-GAAP)Year Ended December 31, 2015

(A) We have entered into agreements to obtain audit and certain compliance functions as a stand-alone public company as well as compensation agreements with certain members of our executive

team. Prior to the completion of the separation, we will also enter into agreements to obtain insurance coverage according to quotations we have received based on our individual loss history, credit

profile and selected insurance coverage. These expenses will represent recurring costs in excess of the amounts historically allocated to Ingevity.

(B) Adjusted EBITDA is the sum of Performance Materials and Performance Chemicals Segment EBITDA

Unaudited Pro Forma Segment EBITDA

31

Performance Materials

In millionsPro Forma

AdjustmentsUnaudited

Pro Forma

Segment operating profit (GAAP) $ 89.5 $ (2.6) (A) $ 86.9

Depreciation and amortization 9.9 9.9

Segment EBITDA (Non-GAAP) $ 99.4 $ 96.8

Performance Chemicals

In millionsPro Forma

AdjustmentsUnaudited

Pro Forma

Segment operating profit (GAAP) $ 123.8 $ (7.2) (A) $ 116.6

Depreciation and amortization 22.4 22.4

Segment EBITDA (Non-GAAP) $ 146.2 $ 139.0

Adjusted EBITDA (Non-GAAP) (B) $ 245.6 $ 235.8

Reconciliation of Segment Operating Profit (GAAP) to Pro Forma Segment EBITDA (Non-GAAP)Year Ended December 31, 2014

(A) We have entered into agreements to obtain audit and certain compliance functions as a stand-alone public company as well as compensation agreements with certain members of our executive

team. Prior to the completion of the separation, we will also enter into agreements to obtain insurance coverage according to quotations we have received based on our individual loss history, credit

profile and selected insurance coverage. These expenses will represent recurring costs in excess of the amounts historically allocated to Ingevity.

(B) Adjusted EBITDA is the sum of Performance Materials and Performance Chemicals Segment EBITDA