innovation imperatives for financial services€¦ · · 2018-04-07innovation imperatives for...

TRANSCRIPT

cognizant reports | september 2012

• Cognizant Reports

Executive SummaryFrom time immemorial, capital markets have evolved to address ever-changing investor require-ments, tastes and risk appetites (see Figure 1, next page). The ensuing innovations can be classified in three broad categories: financial instruments, trading infrastructure and execution.

The emergence in the early 20th century of specialized markets for listed securities begat what is today’s continuous innovation in financial instruments. Numerous equity and debt instru-ments have emerged over the years to address evolving market needs, as well as to help financial and non-financial firms better manage risk.

The rise in electronic trading in the 1980s marked a key turning point in the innovation continuum. Today’s algorithm-driven software for high-fre-quency trades represents yet another significant disruptive shift. Over the horizon is the promise of self-learning trading algorithms competing with each other, requiring minimal degrees of human intervention. Moreover, as alternative trading venues have emerged to enable large institutions to trade anonymously at a reduced cost, we now

Innovation Imperatives for Financial Services In today’s heavily regulated era, the innovation agenda for financial services firms should be to enhance transparency, focus on competencies and ensure compliance. Improving data and risk management will be critical, as well as revitalizing post-trade infrastructures to boost efficiency and reduce costs.

have a market in which change appears to be the only constant.

However, there is a downside to fast and furi-ous instrument innovation. For starters, some investment instrument innovations that emerged in the last decade have been tied to the ongoing global financial crisis. Asset-backed securities, for example, were at the core of the sub-prime mortgage crisis of 2007-2008; derivative instru-ments like these are believed to have set off the full-blown global economic crisis that ensued.1 Given their ubiquity, and the interconnectedness of the financial services industry with the broader economy, financial instruments are typically associated with economic crises.

In the post-subprime financial market landscape, a key imperative for regulators, industry groups and organizations is to create mechanisms that enhance market safety while permitting innova-tion to flower and take hold. This can be achieved by preventing the adverse consequences of over-regulation, while ensuring continued rules harmo-nization by regulatory bodies worldwide to suit the increasingly globalized nature of the business.

cognizant reports 2

Capital market firms must improve their data and risk management capabilities. Risk manage-ment should be viewed as a critical compliance and business imperative. It is the key to ensuring compliance, enhanced transparency, healthier business practices and, perhaps most importantly, to rebuild the trust that was lost following last decade’s financial industry crisis. Back-office func-tions, a hitherto ignored area, deserves a neces-sary upgrade to revitalize the post-trade function by enhancing efficiency and reducing costs.

Financial Instrument Innovations Financial instruments have come a long way since the advent of listed stocks that allowed trading on exchanges, aiding in the development of formal marketplaces and liquidity. Some of the innova-tions that sought to address the requirement of capturing market needs include:

• Mutual funds, which extended professionally managed, diversified asset portfolio benefits to a wider investor population, while helping households acquire financial assets.

• Hedge funds to address the needs of investors with high net worth and a far higher appetite for risk.

• Exchange traded funds (ETF) to provide attrac-tive investment opportunities at far lower costs by focusing on passive investing that mimics select indices.

Meanwhile, instruments emerged to provide risk management benefits. They include:

• Commodity and interest rate futures, which allow businesses to hedge their exposure to adverse commodity price/interest rate movements.

• Inflation indexed bonds, which allow better management of the risks incurred by the adverse impact of a rise in inflation.

• Catastrophe bonds, which insure against the impact of natural calamities.

• Credit default swap (CDS) or credit derivatives, which allow institutions to hedge the credit risks of loans they originate.

Another significant area of innovation is securi-tization to allow firms to convert streams of loan receivables into tradable securities that are sold to investors with a high tolerance for risk; these instruments enable institutions to extend more credit and meet liquidity demands.

Uniqueness of Instrument Innovations Innovations in financial instruments differ vastly from innovations in other industries, whose benefits and potential downsides are clear. Unlike a drug whose ill effects may be limited to only those who consumed it, the adverse impact of financial instruments affects the entire economy, not just the parties involved in specific transac-

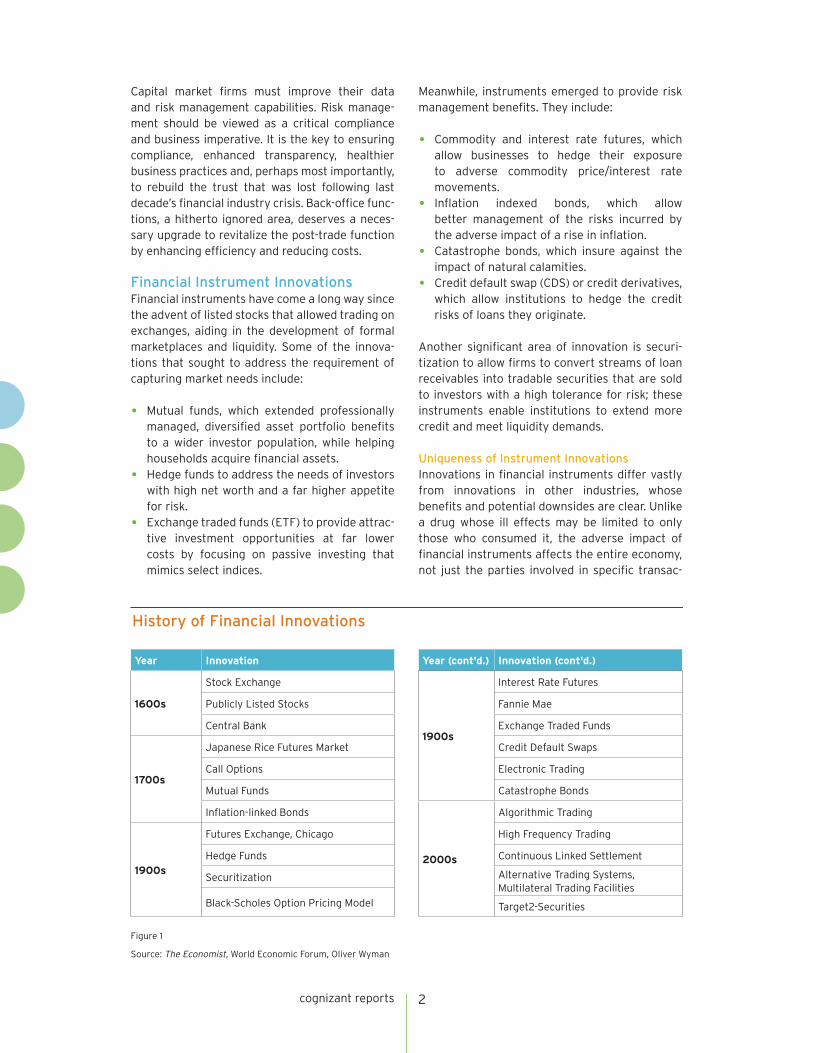

History of Financial Innovations

Year Innovation

1600s

Stock Exchange

Publicly Listed Stocks

Central Bank

1700s

Japanese Rice Futures Market

Call Options

Mutual Funds

Inflation-linked Bonds

1900s

Futures Exchange, Chicago

Hedge Funds

Securitization

Black-Scholes Option Pricing Model

Figure 1

Source: The Economist, World Economic Forum, Oliver Wyman

Year (cont'd.) Innovation (cont'd.)

1900s

Interest Rate Futures

Fannie Mae

Exchange Traded Funds

Credit Default Swaps

Electronic Trading

Catastrophe Bonds

2000s

Algorithmic Trading

High Frequency Trading

Continuous Linked Settlement

Alternative Trading Systems, Multilateral Trading Facilities

Target2-Securities

cognizant reports 3

tions. This is a result of the interconnectedness of financial systems with the general economy, which transmits the benefits and negative impacts of innovations somewhat equally.

In fact, securities firms are both creators and followers of innovation. They both experiment with and adopt new instruments from competi-tors to create investment standards that build markets and house revenue streams.2 Robert Merton calls this phenomenon “the innova-tion spiral,”3 in which institutions devise new instruments to meet their emerging needs that they then standardize and promulgate into the markets, spreading their breadth and depth.

These instruments continuously mutate, extend-ing the cycle of standardization and adoption. Interestingly, the never-ending hunt for invest-ment returns and competition motivates players to evolve key instruments. ETF, an innovation that sought to provide diversification benefits a la market indices to small investors at far lower costs, is one example. Today’s ETFs invest in a wide array of assets, from commodities through equities.

Trading, Execution and Infrastructure Innovations

the floor of the stock exchange, yelling to desk-based traders, backed by powerful computers.

Then came high-speed algorithmic trading, which replaced human traders with software that generates trading orders based on underlying algorithms. High frequency trading (HFT) has already captured around half of the trading volumes today and is set to rise further (see Figure 2).

In the previous era, traders’ physical proximity to the stock exchange floor mattered; however, what matters now is the co-location of servers to achieve trade execution speed advantage, since the difference of a few milliseconds of latency can result in losses or gains of millions of dollars. While algorithm-driven HFT is criticized for causing incredible market volatility,4 high-frequency trad-ing has upped the ante for institutions to improve their execution speeds. The next wave of innova-tions on this front will likely come from trading software driven by self-learning algorithms.5

Trading venues have also shifted, driven primar-ily by the desire to consider multiple sources of liquidity in search of better execution. They include alternative trading systems (ATS) in the U.S. and Canada and multilateral trading facilities (MTFs) in Europe, which have given rise to dark liquidity pools. In the U.S., ATSs are gradu-ally gaining market share from the traditional exchanges (see Figure 3, next page).

Figure 2

Source: “Playing with Fire,” The Economist, Feb. 25, 2012

Rise of the MachinesAlgorithmic trading, as a percent of total trading

0

10

20

30

40

50

60

70Equities

forecast

Futures

ForeignExchange

FixedIncome

Options

2004 ‘06 ‘08 ‘10 ‘12 ‘14

U.S.

Europe Asia

0

10

20

30

40

50

60

70

2004 ‘06 ‘08 ‘10

Technological advancements have transformed securities trading over the past few decades. The big game changer is electronic trading. Trading has evolved from the days when brokers thronged

cognizant reports 4

The dark pools are driven by the desire for ano-nymity to minimize the market impact cost, as well as the cost of transactions. Another motive is to prevent competitors’ trading algorithms from sniffing their orders in transparent markets. Regulatory frameworks provide pre-trade trans-parency waivers to dark liquidity pools, subject to certain conditions.6

Despite the strides made in increasing the effi-ciency of trading venues and securities trading firms’ front offices, inefficiencies still persist in the post-trade infrastructure. The middle and back offices that handle trade confirmations and settlement remain plagued by excessive manual intervention; the lack of automation here is lead-ing to time delays and revenue losses. In the wake of the recent crisis, firms rushed to automate back-office functions to save money, improve operational efficiency and ensure regulatory compliance, overlooking the key functional areas where continued innovation could help drive pro-ductivity gains and competitive advantage.

The need for back-end support systems will increase, as the need for participants to com-ply with the Dodd-Frank Act and the European Market Infrastructure Regulation initiative drives over the counter (OTC) derivatives to be routed through exchanges and swap execution facilities (SEFs). Trades routed through exchanges or SEFs could give rise to the use of algorithms applied to derivatives trading. Greater automation will restrict dealers’ abilities to differentiate on price,

thus forcing them to compensate by leveraging better access to their clients.7 With the arrival of central counterparties (CCPs), post-trade events in OTC derivatives will increase, requiring mar-ket participants to implement systems that allow straight through processing of these trades.8

Meanwhile, regulatory moves toward CCP-enabled clearing, as well as margin requirements for OTC trades that are not cleared through a CCP, have sparked fears that a bulk of these trades could move to smaller markets in Asia. While such fears appear exaggerated, margin requirements could result in an end to exotic OTC trades.9

The Target2-Securities (T2S) platform is another infrastructure innovation that is taking place to reduce the cost and risk of cross-border trans-actions in Europe. In the Eurozone, cross-border transactions are considered to be more expensive than in the U.S. T2S is expected to overcome this challenge, along with several of the “Giovannini barriers” identified by the Giovannini Group in its 2001 and 2003 reports.

Given the complicated nature of the cross-border trading cycle in the Eurozone, this is a welcome move that could help reduce settlement and oper-ational risks and enable a move toward shorter settlement cycles of T+2. But continued delays have meant that the project has experienced repeated delays and is expected only in 2015. (For additional insight, see “Target2-Securities Platform: Implications for the Post-Trade Arena.”)

Figure 3

Source: “U.S. Securities and Exchange Commission Organizational Study and Reform,” The Boston Consulting Group, March 2011.

* Exchanges include BATS, NASDAQ, NYSE Area and regional exchanges

Percent of U.S. Equity Market Volume

0

20

40

60

80

2008 2009 2010 2011E

77

2327

3538

Exchanges*

Alternative Trading Systems

73

6562

Growing market share of alternative trading systems

cognizant reports 5

Amid the ongoing financial crisis, financial instrument innovation of the early 21st century is being closely examined for the severe adverse economic consequences that ensued. Given their ubiquity, financial instruments are typically found at the center of economic crises. Innovations per se are neither evil nor good. They can evolve and be applied to meet specific objectives. The objec-tives are influenced by a host of external and internal factors. As The Economist recently put it, “When bubbles froth, innovations are used inap-propriately — to take on exposures that should not have been, to manufacture risk rather than transfer it, to add complexity.10” This is also sum-marized11 by Steve Kohlhagen, an advisory board member at the Stanford Institute for Economic Policy Research (SIEPR), who said that blaming financial innovation for crises is like blaming the Wright brothers for 9/11.

The systemic significance of innovations arises when the markets for these instruments grow wider and deeper and pose unintended conse-quences.12 ETF’s rapid growth is a case in point (see Figure 4). A Kauffman Foundation report13 warns of potential systemic risks that can arise due to the growing influence of ETF investments, which are increasing correlations among index constituents.

The benign or malignant consequences of finan-cial innovations are determined by three sources

— the environment, innovation itself and the area of application.14

Environmental forces that shape markets and drive innovation typically change over time and influence outcomes. Innovations attempted in an unhealthy environment that provides the wrong incentives are likely to produce negative outcomes. On the contrary, a healthy environ-ment that fosters a long-term view that encour-ages firms to appropriately assess attendant risks can lead to positive outcomes.15 In the run-up to the recent crisis, the environment was beset by a host of adverse factors, including the following:

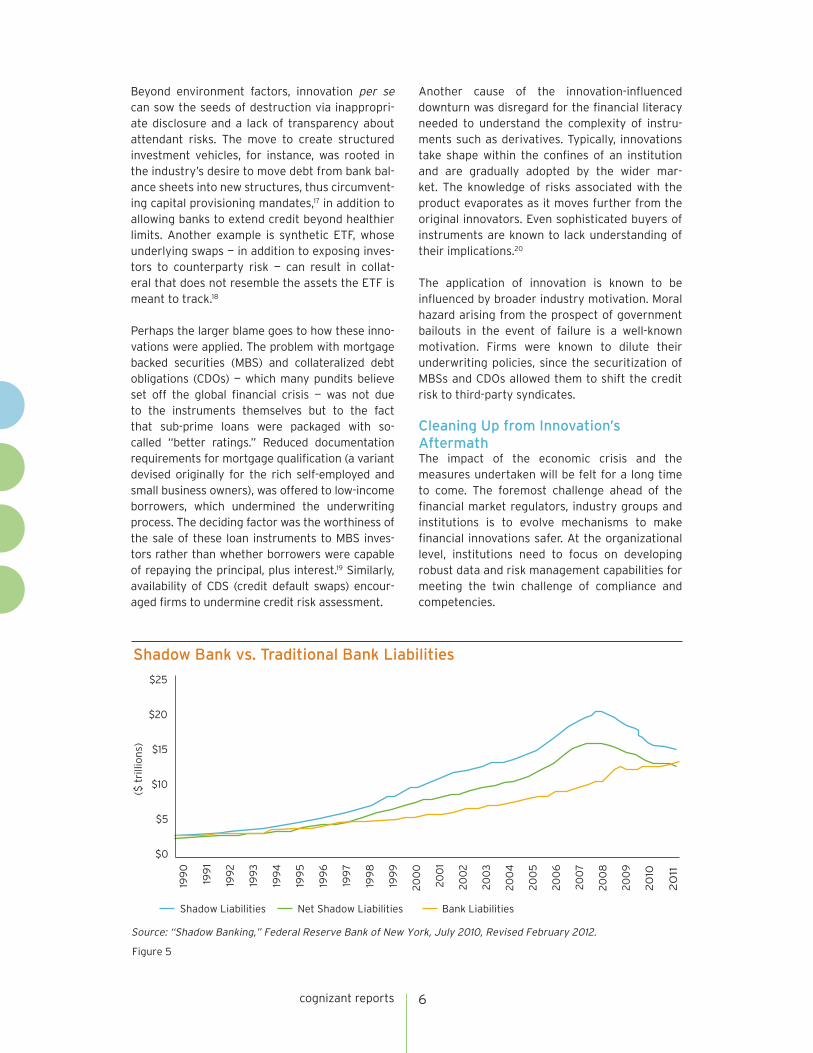

• Prolonged deregulation paved the way for shadow banking (see Figure 5, next page) to flourish.

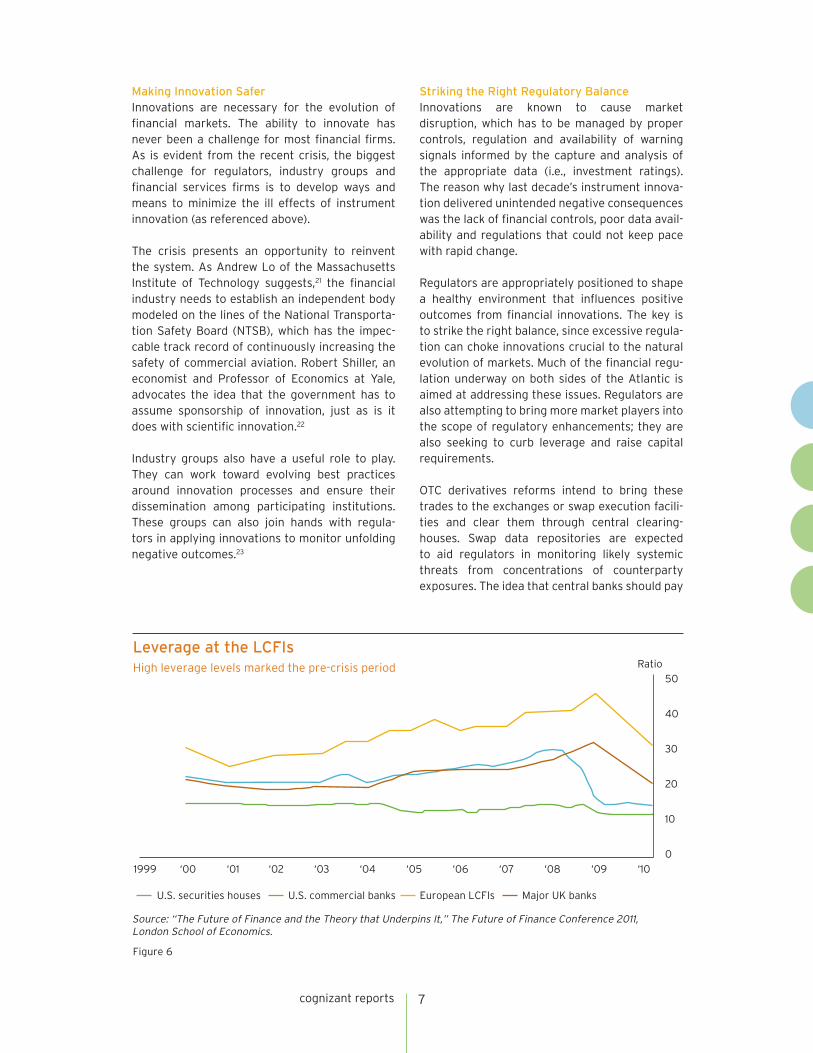

• Institutions took part in opaque OTC derivatives, coupled with high leverage (see Figure 6, page 7).

• Central banks remained solely focused on inflation targeting, even as asset prices bubbled.

• Environmental factors such as overt tax incentives for debt, a prolonged rise in prop-erty values and easy availability of mortgages even for subprime borrowers, incented individ-uals to expose their household balance sheets to excessive debt.

• At the institutional level, back offices that process trades remained largely anti-quated,16 even as the front offices made head-way to meet increasing market demand.

Figure 4

Source: “Playing with Fire,” The Economist, Feb. 25, 2012

Here to Stay

0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2000 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11

CommodityFixed IncomeEquity

Exchange-traded funds, assets in trillions

Innovation’s Role in Financial Market Crises

cognizant reports 6

Beyond environment factors, innovation per se can sow the seeds of destruction via inappropri-ate disclosure and a lack of transparency about attendant risks. The move to create structured investment vehicles, for instance, was rooted in the industry’s desire to move debt from bank bal-ance sheets into new structures, thus circumvent-ing capital provisioning mandates,17 in addition to allowing banks to extend credit beyond healthier limits. Another example is synthetic ETF, whose underlying swaps — in addition to exposing inves-tors to counterparty risk — can result in collat-eral that does not resemble the assets the ETF is meant to track.18

Perhaps the larger blame goes to how these inno-vations were applied. The problem with mortgage backed securities (MBS) and collateralized debt obligations (CDOs) — which many pundits believe set off the global financial crisis — was not due to the instruments themselves but to the fact that sub-prime loans were packaged with so-called “better ratings.” Reduced documentation requirements for mortgage qualification (a variant devised originally for the rich self-employed and small business owners), was offered to low-income borrowers, which undermined the underwriting process. The deciding factor was the worthiness of the sale of these loan instruments to MBS inves-tors rather than whether borrowers were capable of repaying the principal, plus interest.19 Similarly, availability of CDS (credit default swaps) encour-aged firms to undermine credit risk assessment.

Another cause of the innovation-influenced downturn was disregard for the financial literacy needed to understand the complexity of instru-ments such as derivatives. Typically, innovations take shape within the confines of an institution and are gradually adopted by the wider mar-ket. The knowledge of risks associated with the product evaporates as it moves further from the original innovators. Even sophisticated buyers of instruments are known to lack understanding of their implications.20

The application of innovation is known to be influenced by broader industry motivation. Moral hazard arising from the prospect of government bailouts in the event of failure is a well-known motivation. Firms were known to dilute their underwriting policies, since the securitization of MBSs and CDOs allowed them to shift the credit risk to third-party syndicates.

Cleaning Up from Innovation’s Aftermath

Figure 5

($

tri

llio

ns)

Source: “Shadow Banking,” Federal Reserve Bank of New York, July 2010, Revised February 2012.

Shadow Bank vs. Traditional Bank Liabilities

Shadow Liabilities Net Shadow Liabilities Bank Liabilities

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

$0

$5

$10

$15

$20

$25

The impact of the economic crisis and the measures undertaken will be felt for a long time to come. The foremost challenge ahead of the financial market regulators, industry groups and institutions is to evolve mechanisms to make financial innovations safer. At the organizational level, institutions need to focus on developing robust data and risk management capabilities for meeting the twin challenge of compliance and competencies.

cognizant reports 7

Making Innovation SaferInnovations are necessary for the evolution of financial markets. The ability to innovate has never been a challenge for most financial firms. As is evident from the recent crisis, the biggest challenge for regulators, industry groups and financial services firms is to develop ways and means to minimize the ill effects of instrument innovation (as referenced above).

The crisis presents an opportunity to reinvent the system. As Andrew Lo of the Massachusetts Institute of Technology suggests,21 the financial industry needs to establish an independent body modeled on the lines of the National Transporta-tion Safety Board (NTSB), which has the impec-cable track record of continuously increasing the safety of commercial aviation. Robert Shiller, an economist and Professor of Economics at Yale, advocates the idea that the government has to assume sponsorship of innovation, just as is it does with scientific innovation.22

Industry groups also have a useful role to play. They can work toward evolving best practices around innovation processes and ensure their dissemination among participating institutions. These groups can also join hands with regula-tors in applying innovations to monitor unfolding negative outcomes.23

Striking the Right Regulatory BalanceInnovations are known to cause market disruption, which has to be managed by proper controls, regulation and availability of warning signals informed by the capture and analysis of the appropriate data (i.e., investment ratings). The reason why last decade’s instrument innova-tion delivered unintended negative consequences was the lack of financial controls, poor data avail-ability and regulations that could not keep pace with rapid change.

Regulators are appropriately positioned to shape a healthy environment that influences positive outcomes from financial innovations. The key is to strike the right balance, since excessive regula-tion can choke innovations crucial to the natural evolution of markets. Much of the financial regu-lation underway on both sides of the Atlantic is aimed at addressing these issues. Regulators are also attempting to bring more market players into the scope of regulatory enhancements; they are also seeking to curb leverage and raise capital requirements.

OTC derivatives reforms intend to bring these trades to the exchanges or swap execution facili-ties and clear them through central clearing-houses. Swap data repositories are expected to aid regulators in monitoring likely systemic threats from concentrations of counterparty exposures. The idea that central banks should pay

Figure 6

Source: “The Future of Finance and the Theory that Underpins It,” The Future of Finance Conference 2011, London School of Economics.

Leverage at the LCFIs

U.S. securities houses U.S. commercial banks European LCFIs Major UK banks

1999 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10

0

10

20

30

40

50

RatioHigh leverage levels marked the pre-crisis period

cognizant reports 8

serious attention to asset price bubbles is gaining ground, while the appropriate ways and means of doing so are still being debated.24 Neverthe-less, the potential dangers of over-regulation and the lack of regulatory harmonization worldwide threaten to undercut ongoing reforms in markets that today are far more interconnected globally than ever before. Finding the right level of regula-tion and harmonization is necessary for ensuring a healthier and better marketplace.

Improve Data and Risk Management Institutions must improve data and risk manage-ment to survive market uncertainties. Financial services organizations, banks and capital markets firms, in particular, should focus their efforts on building a culture that devotes greater attention to reputation and refrains from pursuing innova-tions that may undermine it. Organizational inno-vation processes need to be reinvented and inte-grated into an enterprise-wide risk management framework.25

Risk management should be viewed as a key business and compliance imperative. As the crisis abates, financial firms need to continually focus on compliance, risk management, cost efficien-cies and rebuilding client trust. Their technology infrastructure has not kept pace with the wave of instrument innovation that swept across the industry over the past decade.

Financial firms need to give high priority to making technological enhancements to their banking systems, as this is crucial for achieving several key objectives, from improving processes, to creating transparency and enhancing compli-ance. To achieve this, they need to overhaul their legacy banking systems, a key part of which is creating consistent data structures across the organization. No wonder enterprise data man-agement has emerged as an important area of focus for financial services firms as they look to prepare for a highly regulated future.

Integrated data structures will enable hitherto siloed data to be standardized, removing incon-sistencies and errors, thus enabling a single version of the truth for all concerned functional departments. This will have several benefits, the most important being reduced complexity and

improved reporting for compliance purposes. Moreover, the use of advanced analytical tools on the “big data” accumulated through new instruments, as well as the return to greater trad-ing volumes of all securities, can reveal hidden insights that can guide financial firms toward greater efficiencies, better product and service innovation and a forecast of emerging trad-ing scenarios and opportunities by combining historic data with expected events.

Improved data management is also crucial for another top priority: better risk management, which is a top agenda item for regulators seek-ing to safeguard systemic stability. Consequently, the risk management function, hitherto a domain of a few experts equipped with quantitative tools, has now moved to the top of the corpo-rate agenda. The view that risk management was predominantly a compliance issue is giving way to a more proactive and holistic approach. As a result, firms need to take an enterprise-wide stance that allows them to move beyond a fragmented understanding of their risk exposure.

Looking AheadTo say these are trying times for financial ser-vices firms would be a vast understatement. Among the many challenges these firms face is a severe crisis of confidence that undermines their strategic thinking and move-forward plan-ning activities. Regaining investor “trust,” which is the real capital for financial firms, remains a work in progress. No matter how difficult this is to resolve, firms must view trust building as an opportunity to reinvent and reorient their innova-tive capabilities to better serve not only investors but also their own interests.

The key to this resides in laying the right cultural foundation. As Robert Shiller suggests in his book Finance and the Good Society,26 “The financial crisis reminds us that innovation has to be accom-plished in a way that supports the stewardship of society’s assets. And the best way to do this is to build good moral behavior into the culture of Wall Street through the creation and observance of best practices in its various professions — CEOs, traders, accountants, investment bankers, law-yers and philanthropists.”

cognizant reports 9

Footnotes1 “Playing with Fire,” The Economist, Feb. 25, 2012, http://www.economist.com/node/21547999.

2 Ibid

3 Robert C. Merton and Zvi Bodie, “A Conceptual Framework For Analyzing The Financial System,” WP#95-062, July 18, 1994, http://www.nek.lu.se/NEKeno/Finance%20B/A%20Framework%20for%20Analyzing%20the%20Financial%20System.pdf.

4 Leo King, “Official: Trading Software Did Not Cause Financial Crash,” Computerworld UK, Jan. 27, 2011, http://www.computerworlduk.com/news/it-business/3258231/official-trading-software-did-not-cause-financial-crash/.

5 Dave Cliff, Dan Brown, Philip Treleaven, “Technology Trends in the Financial Markets: A 2020 Vision,” Government Office for Science, Foresight, 2010, http://www.bis.gov.uk/assets/foresight/docs/com-puter-trading/11-1222-dr3-technology-trends-in-financial-markets.

6 Ibid

7 “OTC Derivatives Market: Update on Current Regulatory Initiatives,” Deutsche Bank Research, Nov. 14, 2011, http://www.dbresearch.de/PROD/DBR_INTERNET_EN-PROD/PROD0000000000280806/OTC+derivatives+market%3A+Update+on+current+regulatory+initiatives.PDF.

8 “OTC Trading: Impact of The CCP Model,” Cognizant Technology Solutions, 2011.

9 Clare Dickinson, “U.S. and European OTC Trades Set to Dominate After Move to Exchange Clearing,” Hedge Funds Review, April 18, 2012, http://www.hedgefundsreview.com/hedge-funds-review/news/2168333/audio-european-otc-trades-set-dominate-exchange-clearing.

10 “Playing with Fire, The Economist.

11 Comment by Steve Kohlhagen, SIEPR Advisory Board, while moderating the discussion on “Financial Innovation and the Economic Crisis” SIEPR Economic Summit 2012, http://www.youtube.com/watch?v=tk93jQcUc-s.

12 “Playing with Fire,” The Economist.

13 Chris Flood, “Kauffman Foundation Attacks ETF Industry,” Financial Times, Nov. 9, 2010, http://www.ft.com/intl/cms/s/0/367cfd78-ec04-11df-b50f-00144feab49a.html#axzz1xC5DJayA.

14 “Rethinking Financial Innovation: Reducing Negative Outcomes While Retaining the Benefits,” World Economic Forum and Oliver Wyman, 2012, http://www.oliverwyman.com/world-economic-forum-and-oliver-wyman-report-rethinking-financial-innovation.htm.

15 Ibid

16 “The Case for More Functional, Utility-Like Trade Management Systems,” Cognizant Technology Solu-tions, March 2011, http://www.cognizant.com/insightswhitepapers/Trade-Management-Systems.pdf.

17 “Rethinking Financial Innovation,” World Economic Forum and Oliver Wyman.

18 “Playing with Fire,” The Economist.

19 “Rethinking Financial Innovation,” World Economic Forum and Oliver Wyman.

20 “Playing with Fire,” The Economist.

About Cognizant

Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process outsourcing services, dedicated to helping the world’s leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 50 delivery centers worldwide and approximately 145,200 employees as of June 30, 2012, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world.

Visit us online at www.cognizant.com for more information.

World Headquarters

500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters

1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 207 297 7600Fax: +44 (0) 207 121 0102Email: [email protected]

India Operations Headquarters

#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2012, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

Credits

Author Rajeshwer Chigullapalli, Head of the Thought Leadership Practice, Cognizant Research Center

AnalystAkhil Tandulwadikar, Senior Research Analyst, Cognizant Research Center

Subject Matter ExpertSudhir Gupta, Assistant Vice-President, Cognizant Banking and Financial Services Practice

DesignHarleen Bhatia, Creative DirectorSuresh Sambandhan, Designer

21 Andrew W. Lo, “The Financial Industry Needs Its Own Crash Safety Board,” Financial Times, March 2, 2010, http://www.ft.com/intl/cms/s/0/011cbf2e-2599-11df-9bd3-00144feab49a.html#axzz26MIhrCOz.

22 “Surveying the Economic Horizon: A Conversation with Robert Shiller,” McKinsey Quarterly, April 2009, https://www.mckinseyquarterly.com/Surveying_the_economic_horizon_A_conversation_with_Robert_Shiller_2345.

23 “Rethinking Financial Innovation,” World Economic Forum and Oliver Wyman.

24 “Should, or Can, Central Banks Target Asset Prices?” The International Economy, Fall 2009, http://www.international-economy.com/TIE_F09_AssetPriceSymp.pdf.

25 “Rethinking Financial Innovation,” World Economic Forum and Oliver Wyman.

26 Robert J Shiller, Finance and the Good Society, Princeton University Press, 2012, http://press.princ-eton.edu/titles/9652.html.