innovation in motion: electrification

TRANSCRIPT

INNOVATION IN MOTION:ELECTRIFICATION

Monday, June 28 | 8:30 AM EDT

FORWARD LOOKING STATEMENTS

This presentation, as well as other statements made by Aptiv PLC (the “Company”), contain forward-looking statements that reflect, when made, the Company’s current views with

respect to current events, certain investments and acquisitions and financial performance. Such forward-looking statements are subject to many risks, uncertainties and factors

relating to the Company’s operations and business environment, which may cause the actual results of the Company to be materially different from any future results. All

statements that address future operating, financial or business performance or the Company’s strategies or expectations are forward-looking statements. Factors that could cause

actual results to differ materially from these forward-looking statements include, but are not limited to, the following: global and regional economic conditions, including conditions

affecting the credit market; uncertainties posed by the novel coronavirus (COVID-19) pandemic and the difficulty in predicting its future course and its impact on the global

economy and the Company’s future operations; fluctuations in interest rates and foreign currency exchange rates; the cyclical nature of global automotive sales and production; the

potential disruptions in the supply of and changes in the competitive environment for raw material integral to the Company’s products; the Company’s ability to maintain contracts

that are critical to its operations; potential changes to beneficial free trade laws and regulations such as the United States-Mexico-Canada Agreement; the ability of the Company to

integrate and realize the expected benefits of recent transactions; the ability of the Company to attract, motivate and/or retain key executives; the ability of the company to avoid

or continue to operate during a strike, or potential work stoppage or slow down by any of its unionized employees or those of its principal customers; and the ability of the

Company to attract and retain customers. Additional factors are discussed under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and

Results of Operations” in the Company’s filings with the Securities and Exchange Commission. New risks and uncertainties arise from time to time, and it is impossible for us to

predict these events or how they may affect the Company. It should be remembered that the price of the ordinary shares and any income from them can go down as well as up. The

Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events and/or otherwise, except

as may be required by law.

APTIV’S RIGHT TO PLAY

B I L L P R E S L E Y

APTIV PERFECTLY POSITIONED FOR GREATER VEHICLE ELECTRIFICATION

=

FULL SYSTEM-LEVEL CAPABILITIES100+YEARS OF AUTOMOTIVE ENGINEERING EXPERIENCE

+

UNIQUE TECHNOLOGY PORTFOLIO

NERVOUS SYSTEMSIGNAL & POWER SOLUTIONS (S&PS)

BRAINADVANCED SAFETY

& USER EXPERIENCE

(AS&UX)

SIGNAL & POWER SOLUTIONS

GLOBAL ARCHITECTURE AND COMPONENTS LEADER IN:

HIGH SPEED / FIDELITY DATA DISTRIBUTION

MULTI-VOLTAGE ELECTRICAL DISTRIBUTION

AUTOMOTIVE-GRADE INTERCONNECTS

ENGINEERED FASTENING SOLUTIONS

EXPANDING LEADERSHIP POSITION IN LOW AND HIGH POWER SOLUTIONS

LOW VOLTAGE

Unique design, systems integration, and optimization capabilities

Global footprint and quality manufacturing

CONTENT ON

1 OUT OF 3.5GLOBAL VEHICLES

HIGH VOLTAGE

Leveraging our global scale and capabilities in low voltage

Content and margin accretive to S&PS and total Aptiv

CONTENT ON

1 OUT OF 22020-2022 BEV VEHICLES

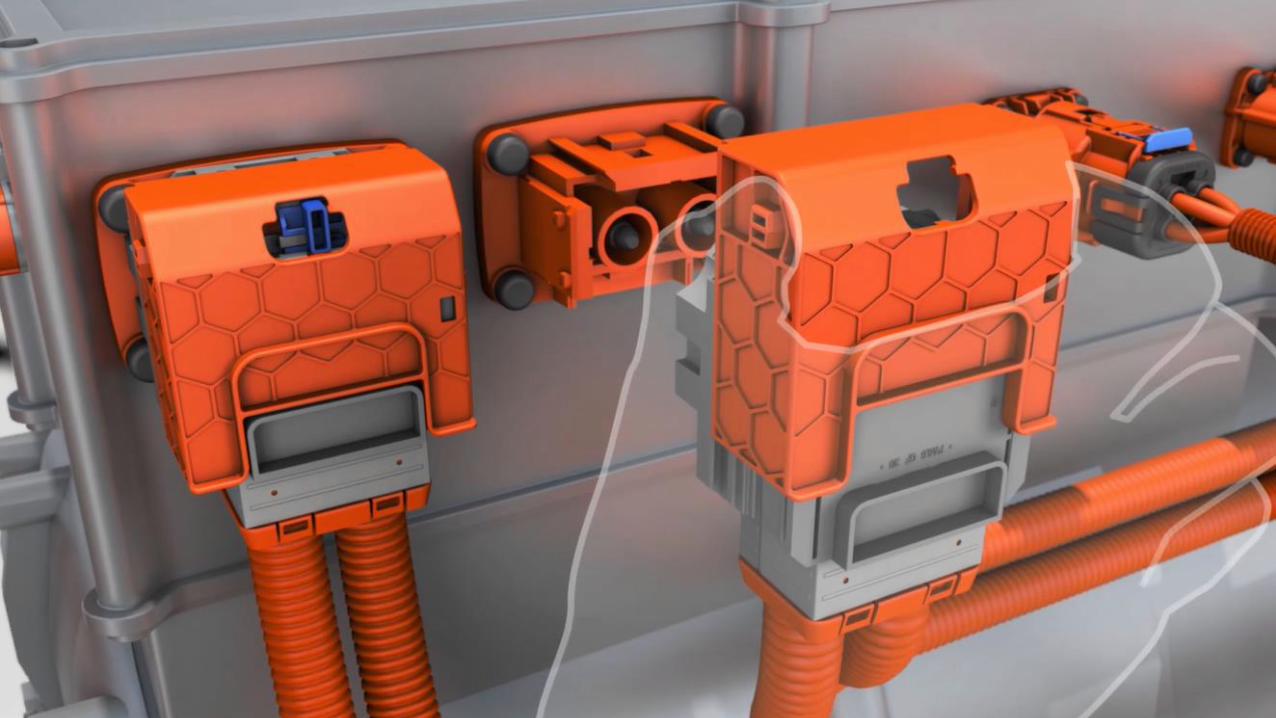

HIGH VOLTAGE BUSBARS

HIGH VOLTAGE CONNECTORS

INTERNAL BATTERY CONNECTIONS

CHARGING CABLE SETS AND INLETS

CHARGER

HIGH VOLTAGE CABLES

POWER DISTRIBUTION BOXES AND BATTERY DISCONNECT UNITS

BROADEST AND MOST RELEVANT PORTFOLIO OF HIGH VOLTAGE TECHNOLOGIES

ADDRESSABLE CPV*

LOW VOLTAGE

• Low Voltage Wiring

• Low Voltage Connectors

• Cable Management

DECREMENTAL CONTENT

– Engine Harness

– ICE Device Connector

HIGH VOLTAGE

+ High Voltage Cables

+ High Voltage Connectors

+ High Voltage Busbars

+ Battery Disconnect Units (BDU)

+ Power Distribution Boxes (PDB)

+ Charger & Charging Cable Set/Inlet

+ HV Cable Management Solutions

TOTAL NET CPV** Midpoint of total addressable content per vehicle (CPV).

+ $500

– $150

+ $850

= $1200

TRADITIONAL INTERNAL COMBUSTION ENGINE (ICE)

BATTERY ELECTRIC

PROVIDING END-TO-END SOLUTIONS THAT ENABLE A MORE EFFICIENT PATH TO VEHICLE ELECTRIFICATION

FULL SYSTEM-LEVEL CAPABILITIES TECHNOLOGY INNOVATION

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

INNOVATIONS SOLVING CUSTOMER CHALLENGES

CUSTOMER CHALLENGES

FASTER CHARGING RELIABILITY / PERFORMANCE PACKAGING / WEIGHT / COSTS SAFETY / SECURITY

INNOVATIONS SOLVING CUSTOMER CHALLENGES

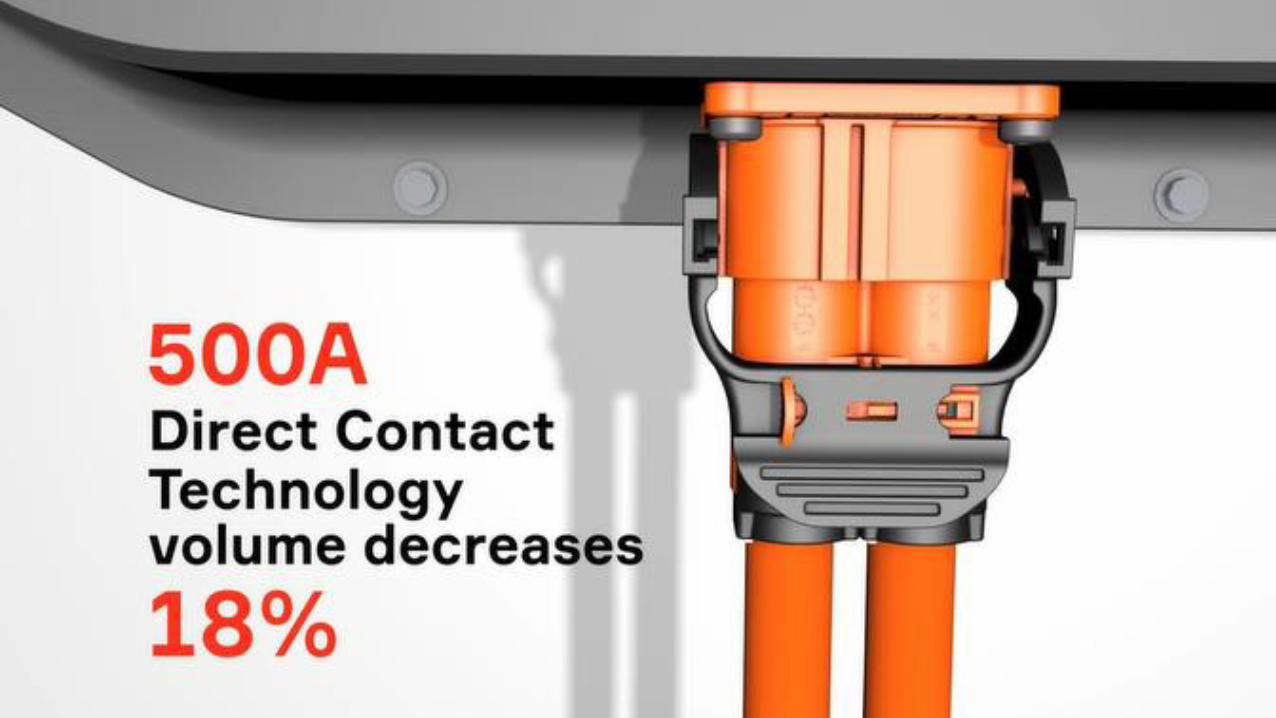

• 32 AMP CHARGER

• ACTIVE COOLED INLETS

• 400 AMP INTERCONNECTS

• DIRECT CONTACT TECHNOLOGY

ENABLING ARCHITECTURE OPTIMIZATIONDESIGN FOR AUTOMATION VERTICAL INTEGRATION

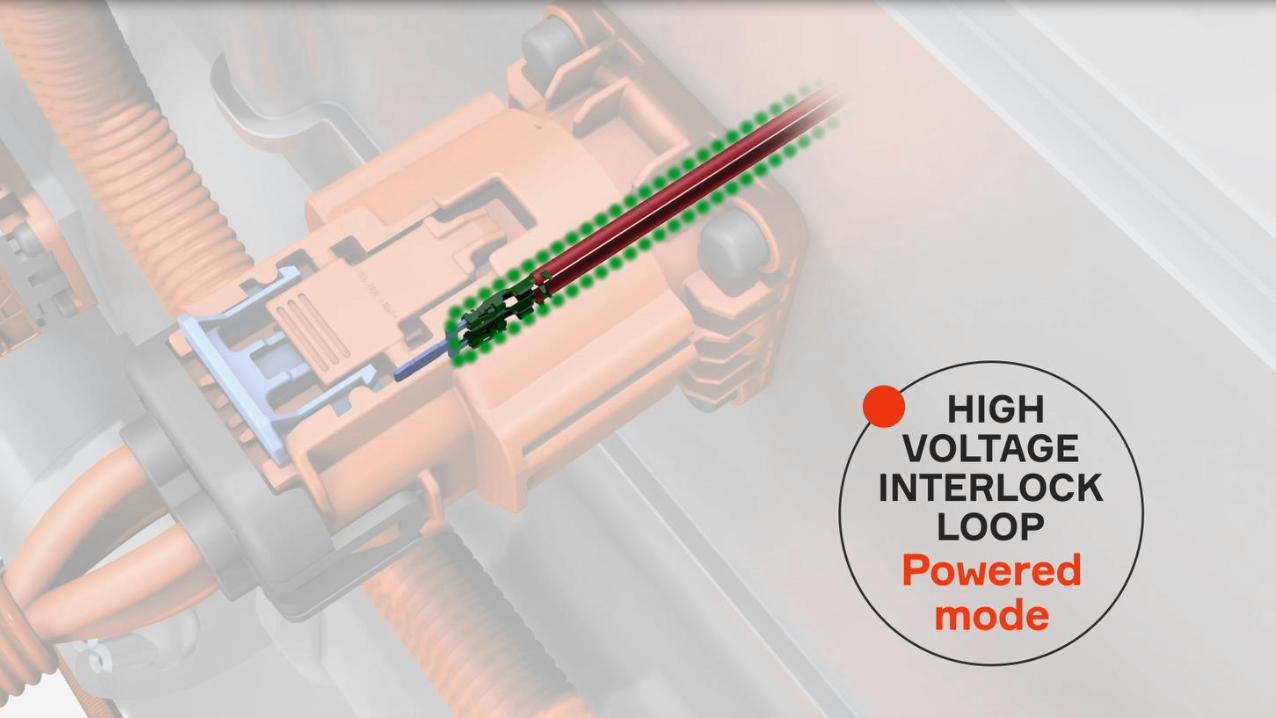

CUSTOMER CHALLENGES

FASTER CHARGING RELIABILITY / PERFORMANCE PACKAGING / WEIGHT / COSTS SAFETY / SECURITY

APTIV SOLUTIONS

• SHIELDED SOLUTIONS

• SEALING AND ARC PROTECTION SOLUTIONS

• ERGONOMIC TECHNOLOGY

• HV INTERLOCK LOOP CIRCUITS

• APTIV SPLICE TECHNOLOGY

• BUSBARS

• CABLE MANAGEMENT

• ALUMINUM CABLE

• SMART CHARGINGINTERFACE CONTROLLER

• BATTERY DISCONNECT UNITS

• POWER DISTRIBUTION UNITS

ARCHITECTURE OPTIMIZATION

FULL-SYSTEM SOLUTIONS DELIVER UNPARALLELED SYSTEM OPTIMIZATION

E R I C R O W L A N D

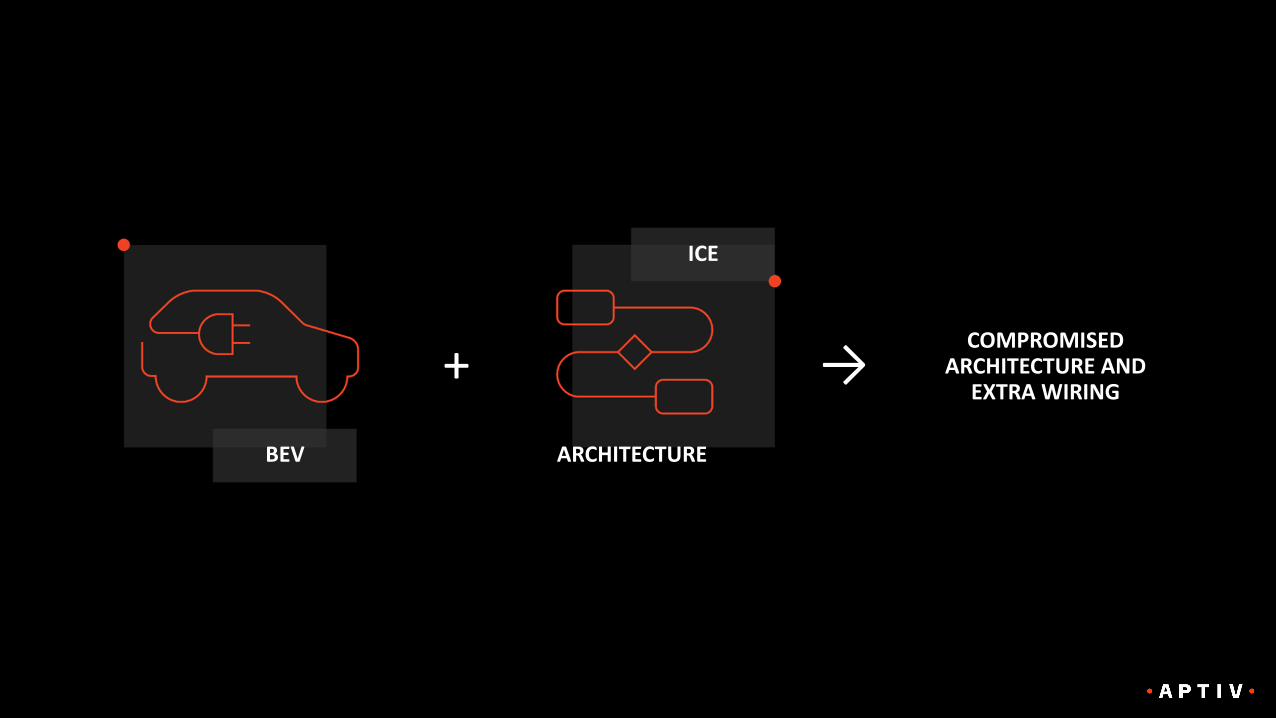

ICE → BEV

COMPROMISEDARCHITECTURE AND

EXTRA WIRING

BEV ARCHITECTURE

ICE

→+

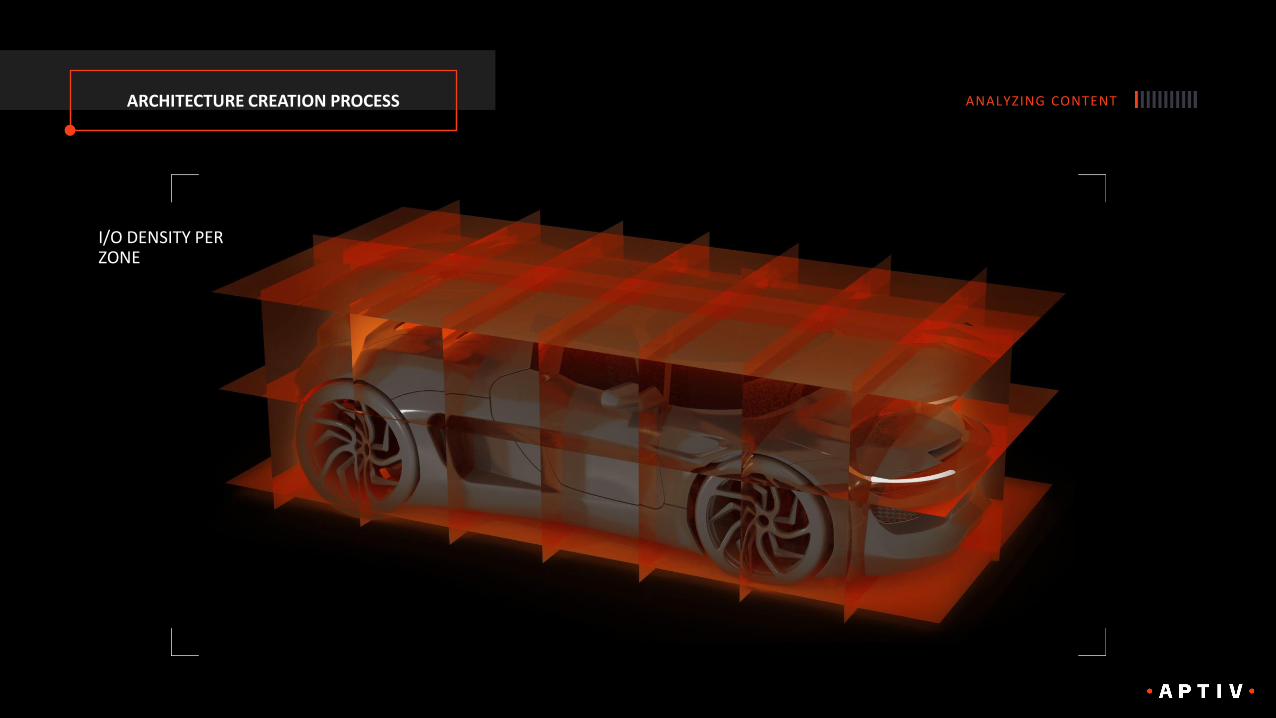

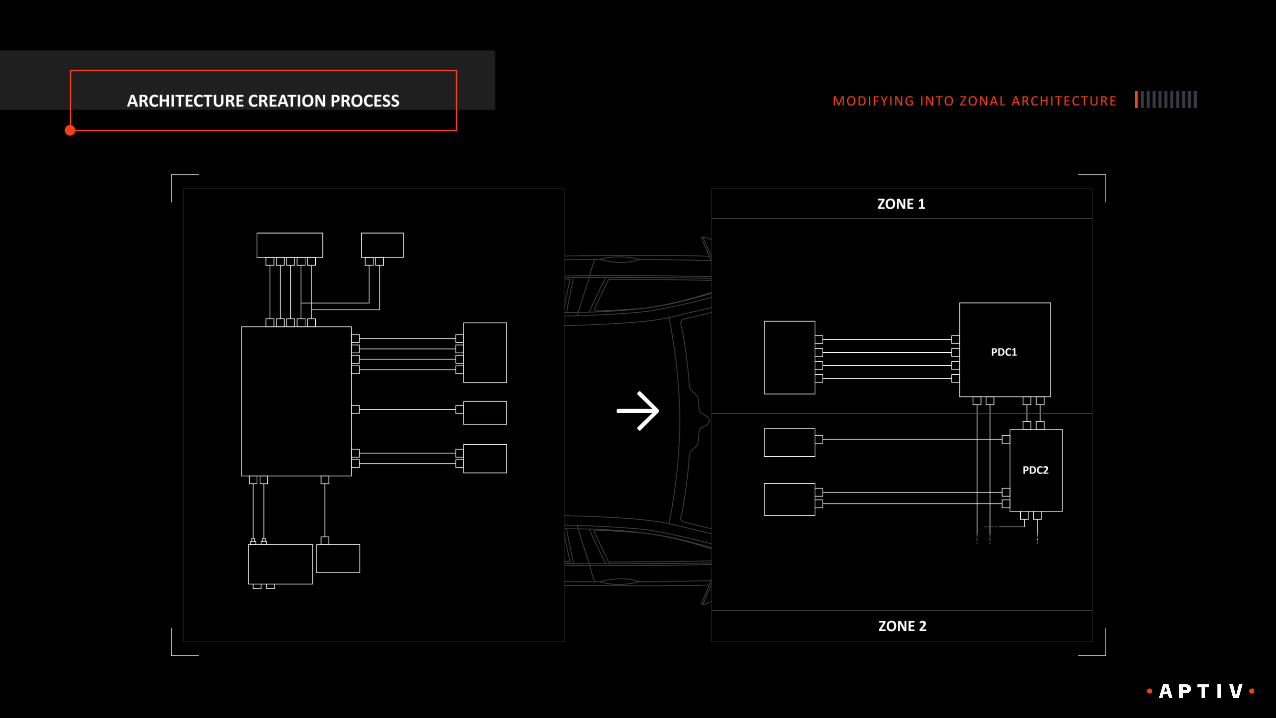

ARCHITECTURE CREATION PROCESS

ARCHITECTURE CREATION PROCESS

LOADING OEM WIRING DATA

ARCHITECTURE CREATION PROCESS ENRICHING AND MODELINGARCHITECTURE CREATION PROCESS

ARCHITECTURE CREATION PROCESS ANALYZING CONTENTARCHITECTURE CREATION PROCESS

I/O DENSITY PER ZONE

ARCHITECTURE CREATION PROCESS ANALYZING CONTENTARCHITECTURE CREATION PROCESS

I/O DENSITY PER ZONE

ARCHITECTURE CREATION PROCESS MODIFYING INTO ZONAL ARCHITECTURE

ZONE 2

ZONE 1

PDC1

PDC2

→

ARCHITECTURE CREATION PROCESS FINDING BEST VARIANT

CRITERION 3

CRITERION 2 CRITERION 4

CRITERION 1 CRITERION 5

CRITERION N

Ref mit G

Arch 1 mit G

EVALUATION METRICS FUNCTIONAL AVAILABILITY AFTER CRASH

ARCHITECTURE CREATION PROCESS RESULTS

PDC

CVC

OSP

PDC

PDC

SMART VEHICLE ARCHITECTURE

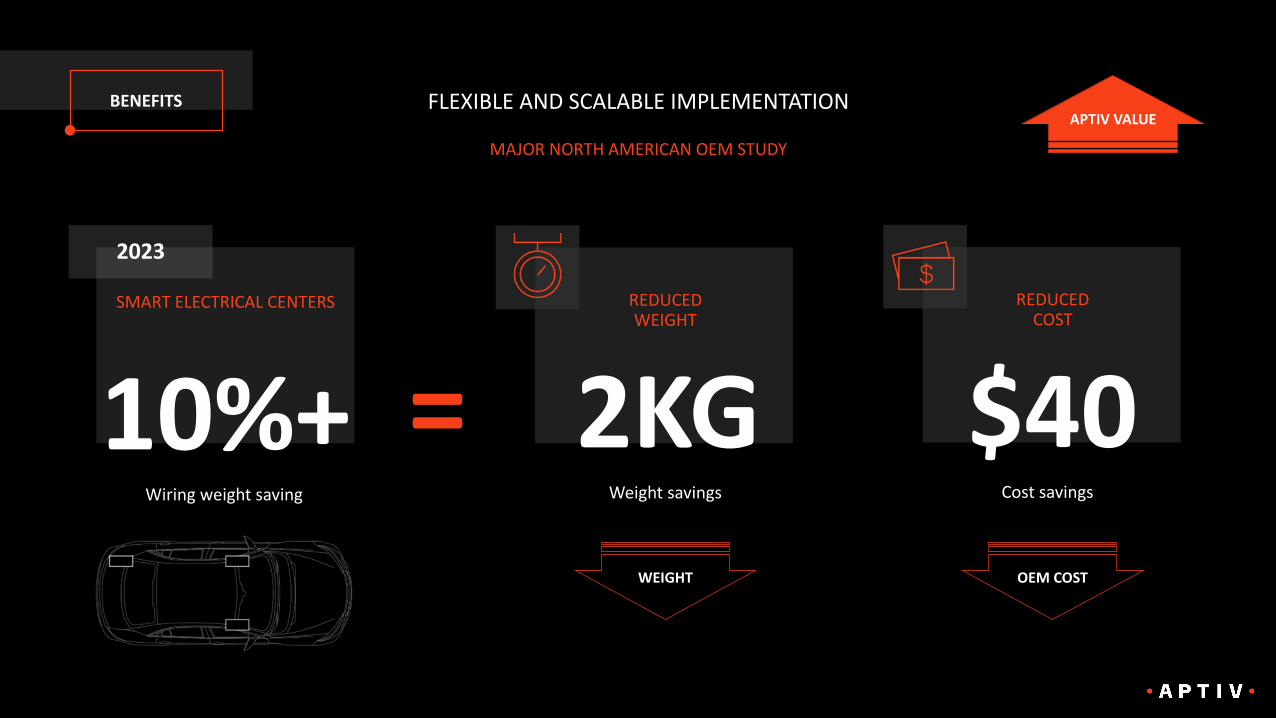

BENEFITS

BENEFITS REDUCED COMPLEXITY

BENEFITS FLEXIBLE AND SCALABLE IMPLEMENTATION

2025

FULL ZONALARCHITECTURE

20%+Wiring weight saving

2028+

FULL SVA™

30%+Wiring weight saving

2023

SMART ELECTRICAL CENTERS

10%+Wiring weight saving

BENEFITS

MAJOR NORTH AMERICAN OEM STUDY

REDUCED COST

$40Cost savings

FLEXIBLE AND SCALABLE IMPLEMENTATION

=OEM COST

APTIV VALUE

REDUCED WEIGHT

2KGWeight savings

WEIGHT

2023

SMART ELECTRICAL CENTERS

10%+Wiring weight saving

BENEFITS

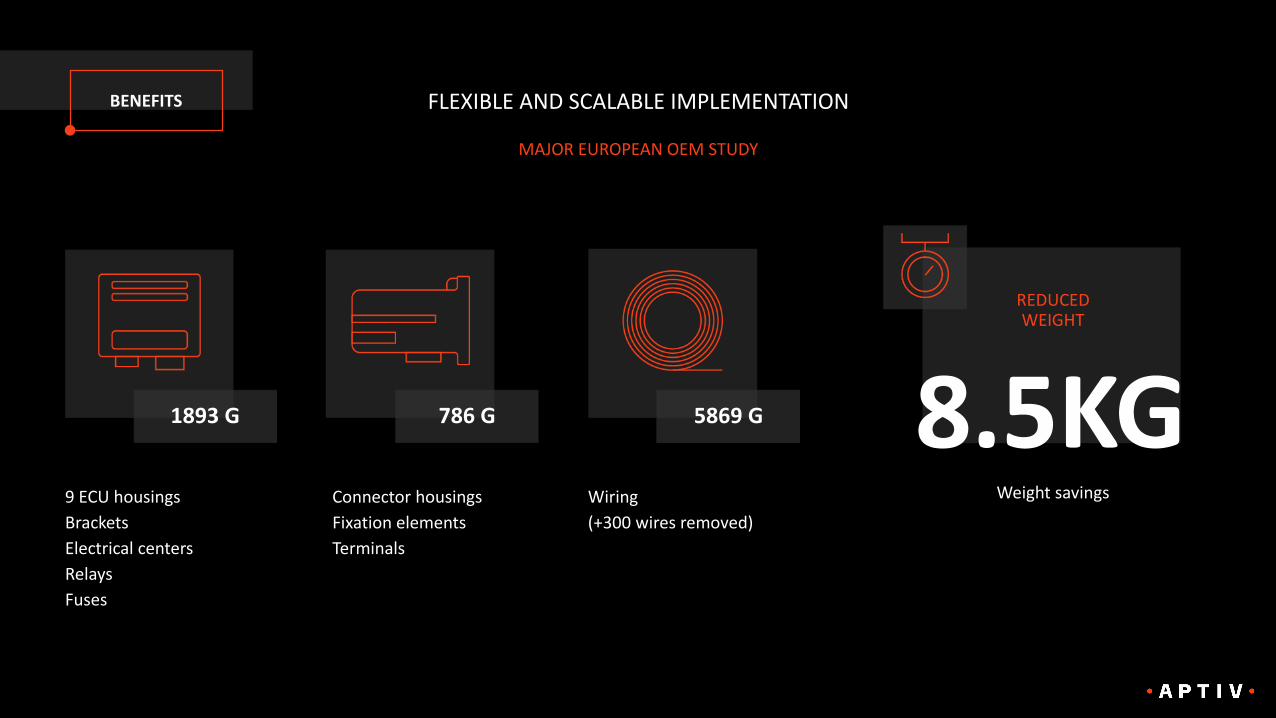

MAJOR EUROPEAN OEM STUDY

REDUCED COST

$55Cost savings

FLEXIBLE AND SCALABLE IMPLEMENTATION

= 8.5KG

REDUCED WEIGHT

Weight savings

2025

FULL ZONALARCHITECTURE

20%+Wiring weight saving

WEIGHT COST

APTIV VALUE

BENEFITS

MAJOR EUROPEAN OEM STUDY

REDUCED WEIGHT

8.5KGWeight savings

FLEXIBLE AND SCALABLE IMPLEMENTATION

9 ECU housings

Brackets

Electrical centers

Relays

Fuses

1893 G

Connector housings

Fixation elements

Terminals

786 G

Wiring

(+300 wires removed)

5869 G

BENEFITS

– Dock & Lock™ OEM Assembly automation

– Flat Backbone wiring

2028+

FULL SVA™

30%+Wiring weight saving

FLEXIBLE AND SCALABLE IMPLEMENTATION

BENEFITS

BENEFITS

BENEFITS

B I L L P R E S L E Y

GLOBAL SCALE & MANUFACTURING EXCELLENCE

TECHNICAL CENTERS34ENABLING APTIV TO DELIVER CONSISTENT PRODUCT AND SERVICE OFFERINGS IN ALL REGIONS

GLOBAL SCALE WITH INDUSTRY-LEADING CAPABILITIES

MANUFACTURING SITES GLOBALLY52

APTIV ADDRESSING KEY CUSTOMER CHALLENGES

AUTOMATING COMPONENTS

AUTOMATING ASSEMBLY

MINIATURIZATION

Component miniaturization and increased wire density

QUALITY

Automation required for AV content specifications

LABOR

Global labor cost increases and lack of labor availability

2XAUTOMATION

POTENTIAL

SVATM ARCHITECTURE

Simple connections

Short wires, other partitioning possible

40-80%Automation potential of wires

20-40%Automation potential of wires

Complex connections

Long wires, mega harness

DISTRIBUTED OR DOMAIN ORIENTED ARCHITECTURE

GREATER MANUFACTURING AUTOMATION

AUTOMATING COMPONENTS

AUTOMATING ASSEMBLY

BETTER QUALITY

IMPROVED RELIABILITYAND PERFORMANCE

ENHANCED PERFORMANCE

APTIV PROVIDING TANGIBLE CUSTOMER BENEFITS

SIGNIFICANT COST SAVINGS

PARTNER-OF-CHOICE

APTIV IS A TRUSTED PARTNER TO BOTH TRADITIONAL AND EMERGING EV PLAYERS

J O S I E A R C H E R

PARTNER-OF-CHOICE

WHY WE WIN

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

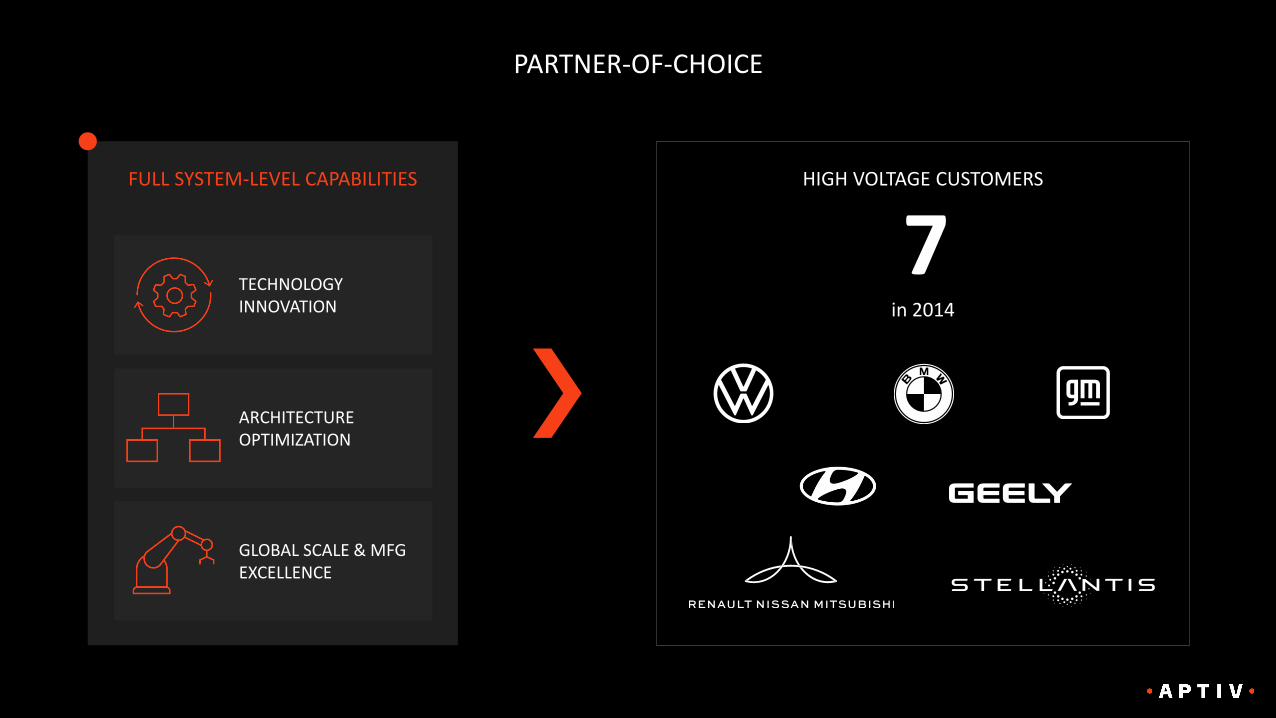

HIGH VOLTAGE CUSTOMERS

in 2014

7

PARTNER-OF-CHOICE

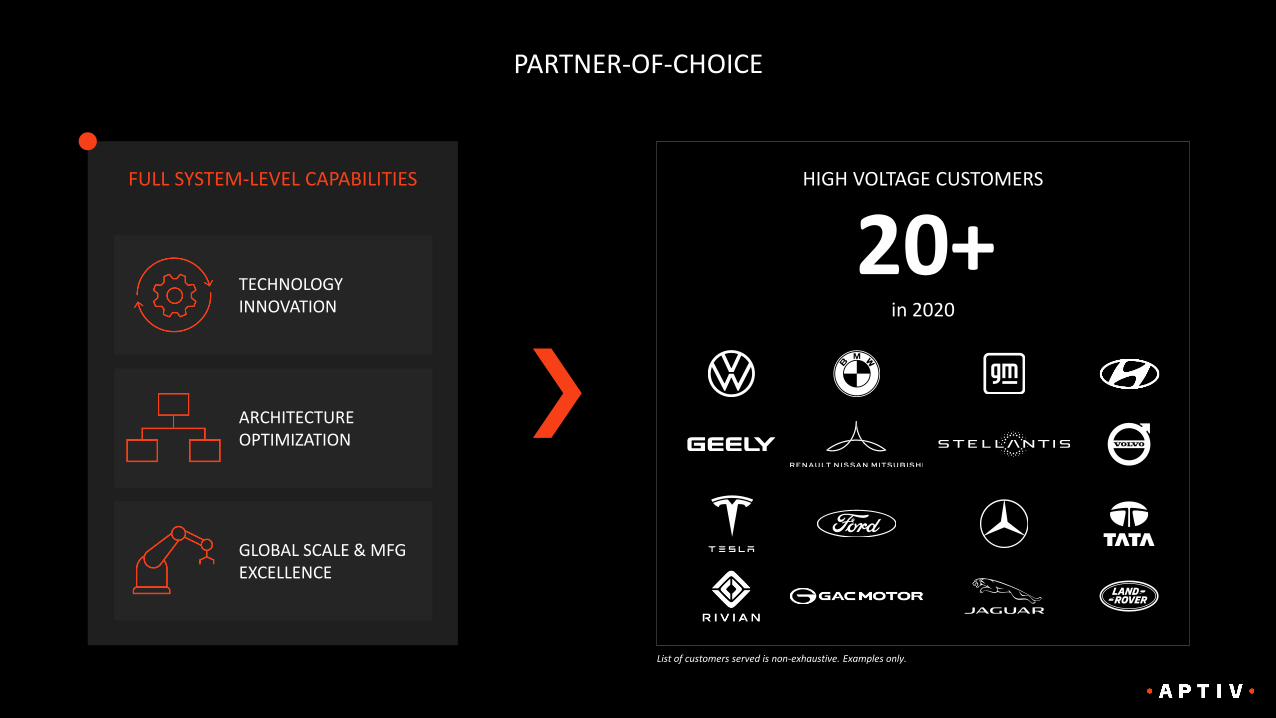

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

HIGH VOLTAGE CUSTOMERS

in 2020

20+

PARTNER-OF-CHOICE

List of customers served is non-exhaustive. Examples only.

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

HIGH VOLTAGE CUSTOMERS

in 2023

25+

PARTNER-OF-CHOICE

List of customers served is non-exhaustive. Examples only.

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

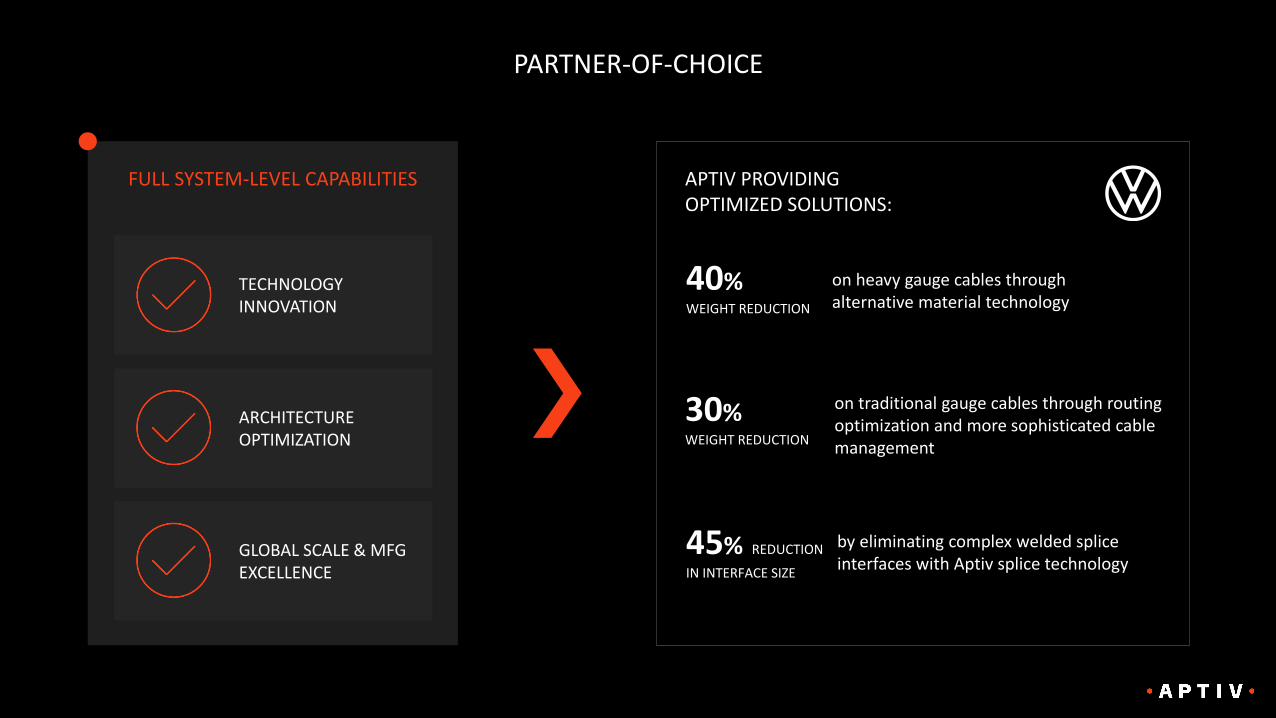

APTIV PROVIDING OPTIMIZED SOLUTIONS:

40%WEIGHT REDUCTION

on heavy gauge cables through alternative material technology

30%WEIGHT REDUCTION

on traditional gauge cables through routing optimization and more sophisticated cable management

45% REDUCTION

IN INTERFACE SIZE

by eliminating complex welded splice interfaces with Aptiv splice technology

PARTNER-OF-CHOICE

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

VW ID BUZZ LEADING TO FOLLOW-ON WINS

✓ ID.6 ✓ ID.BUZZ ✓ ID.VIZZION1

✓ ID.3 ✓ ID.4 ✓ ID.5

PARTNER-OF-CHOICE

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

EMERGING MOBILITY PLAYERS

APTIV ENABLING CUSTOMERS TO:

• Execute on their ambitious timelines

• Seamlessly expand their product offerings

• Grow their global operations

• Ramp up in high volume

PARTNER-OF-CHOICE

FACTORS ENABLING

APTIV’S SPEED TO MARKET:

• Comprehensive portfolio

• A modular approach

• Cable extrusion expertise

• Common engineering and MFG footprint

• In-house rapid prototyping capabilities

TECHNOLOGY INNOVATION

FULL SYSTEM-LEVEL CAPABILITIES

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

PARTNER-OF-CHOICE

APTIV HAS BEEN AWARDED HV CONTENT IN ALL CLASSES

ENABLING PATH TO SUSTAINABILITY

SedanSedan

CUV / SUVCUV / SUV

Pick-upPick-up

SCALABLE CAPABILITIES FOR ENTIRE EV SPACE

Commercial / Delivery VansCommercial / Delivery Vans

Semi-truck

Semi-truck

B I L L P R E S L E Y

POSITIONED FOR STRONG GROWTH

CUSTOMER INVESTMENT TRENDS ACCELERATING SHIFT TO EVS

Pulling ahead sales targets to achieve zero

emissions sooner

50%

100%

BEVs by 2025(as of Q2 2018)

BEVs by 2030(as of Q1 2021)

BEVs by 2025(as of Q2 2018)

BEVs by 2030(as of Q1 2021)

Accelerating pace and number of BEV

launches

20 launches by 2023 (as of Q4 2017)

30 launches by 2025 incl. pickups(as of Q4 2020)

Increasing investments to enable faster transition to EVs

€20B+ through 2030 (as of Q3 2017)

€30B* through 2022(as of Q3 2019)

$11B+ through 2022(as of Q1 2018)

$30B+ through 2025(as of Q2 2021)

OEMS ACCELERATING EV PLANS

*China JVs to invest an additional €15B over next few years

Source: Company press releases and investor presentations

1.9

3.3

5.4

7.7

8.7

12.9

3.3

11.1

15.8

13.2

20.8

24.7

0

5

10

15

20

25

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033

Jan ‘19

Jan ‘150.9

Jan ‘18

Jan ‘16

Jan ‘17

Jan ‘20

Feb ‘21

1.4

SINCE 2015, IHS HAS REVISED ITS BEV FORECASTS UP IN RESPONSE TO DECLINING COSTS, INCREASING REGULATIONS, AND WIDER AVAILABILITY

BEV Share (%)

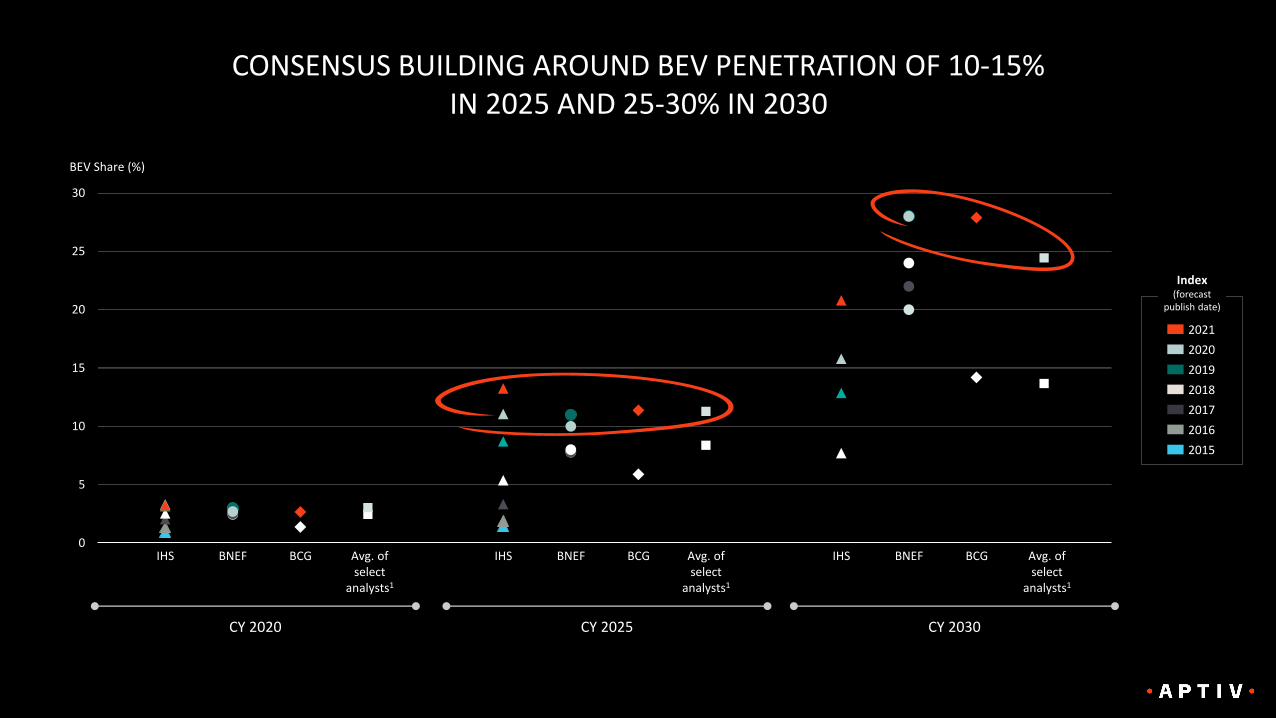

CONSENSUS BUILDING AROUND BEV PENETRATION OF 10-15% IN 2025 AND 25-30% IN 2030

0

5

10

15

20

25

30

BCGIHS Avg. of select

analysts1

BEV Share (%)

BNEF Avg. of select

analysts1

IHS BNEF BCG Avg. of select

analysts1

IHS BNEF BCG

CY 2020 CY 2025 CY 2030

2021

2020

2019

2018

2017

2016

2015

Index(forecast

publish date)

MARKET OUTLOOK & ELECTRIFICATION PENETRATION DRIVERS

A A K A S H A R O R A

JUN 28, 2021

EV Market Evolution

80 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Setting the stage | xEV penetration continues to riseDespite lower overall production volumes, additional 2.6M xEVs produced in 2020

0

80

40

60

100

2015 2016 2017 2019 2020

76%

xEV

Diesel

Gasoline

13%21%

2%

74

20182011

76%71%

Global vehicle

production (M)

2010 2012 2013

7477

81

76%

8487 89

93 95 94

89

1%

22%

2014

1%

23%

76%

2%

21%

77%

3%

20%

77%

3%

21%

77%

20%

76%

4%

19%

6%

18%

76%

8%

17%

75%

15%

3%

Note: xEV inclusive of: BEV = Battery electric; PHEV = plug-in hybrid electric; HEV = full hybrid electric; MHEV = mild hybrid electric Source: IHS Markit Alternative Propulsion Plus Data; IHS Markit LV sales (June 2021)

Year-over-year growth in % xEVs

80

100

60

0

40

20

HEV

Share of xEVs

by type (%)

2.4

(24%)

1.1

(11%)

2.9

(29%)

3.5

(36%)

2020

BEV

PHEV

MHEV

9.9M

33%28%34% 33% 36%

81 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

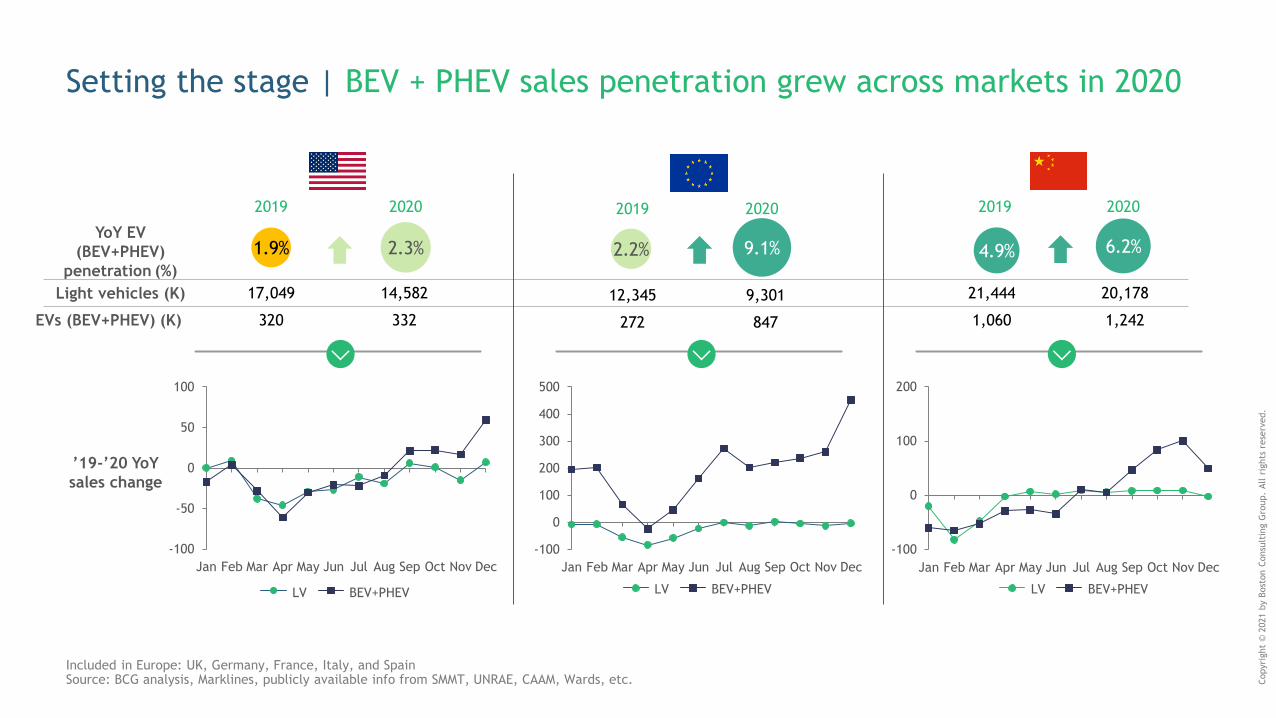

Setting the stage | BEV + PHEV sales penetration grew across markets in 2020

’19-’20 YoY

sales change

YoY EV

(BEV+PHEV)

penetration (%)

2019 2020 2019 2020 2019 2020

-100

-50

0

50

100

Jan Feb JunMar Apr May Jul Aug Sep Oct Nov Dec

LV BEV+PHEV

-100

0

100

200

300

400

500

FebJan JulMar Apr May Jun SepAug Oct Nov Dec

-100

0

100

200

Mar SepFeb JunJan MayApr Jul Aug Oct Nov Dec

LV BEV+PHEV LV BEV+PHEV

Light vehicles (K)

EVs (BEV+PHEV) (K)

Included in Europe: UK, Germany, France, Italy, and SpainSource: BCG analysis, Marklines, publicly available info from SMMT, UNRAE, CAAM, Wards, etc.

2.3%

17,049

320

1.9%

14,582

332

2.2%

12,345

272

9.1%

9,301

847

4.9%

21,444

1,060

20,178

1,242

6.2%

Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

82

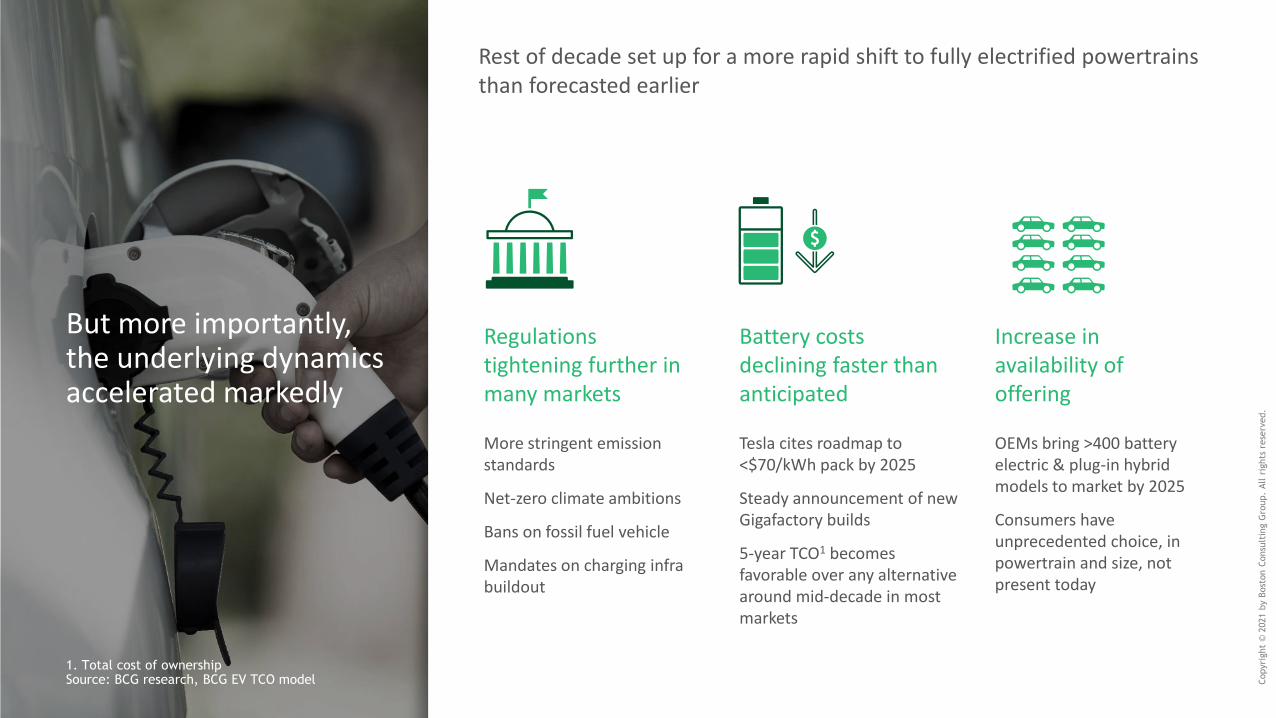

Battery costs declining faster than anticipated

Tesla cites roadmap to <$70/kWh pack by 2025

Steady announcement of new Gigafactory builds

5-year TCO1 becomes favorable over any alternative around mid-decade in most markets

Increase in availability of offering

OEMs bring >400 battery electric & plug-in hybrid models to market by 2025

Consumers have unprecedented choice, in powertrain and size, not present today

Regulationstightening further in many markets

More stringent emission standards

Net-zero climate ambitions

Bans on fossil fuel vehicle

Mandates on charging infra buildout

But more importantly, the underlying dynamics accelerated markedly

1. Total cost of ownershipSource: BCG research, BCG EV TCO model

Rest of decade set up for a more rapid shift to fully electrified powertrains than forecasted earlier

83 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Regulations continue to tighten across key markets

60

80

200

140

120

100

160

180

220

2510 1309 261916 2302 22

CO2 (g/km)

1500 01 0803 04 0605 07 11 12 14 17 18 20 2721 24 28 29 30

-3%

-7%

2025: 99

2030: 59

2025: 93

Biden Administration

indicating strong renewed

focus on more stringent

tailpipe emissions

Note: ZEV = Zero Emission Vehicles, PV = Passenger Vehicles, LCV = Light Commercial VehiclesSource: BCG analysis, ICCT (June 2019), NHTSA, ACEA

Average

2000-2020:

US EU China

Average

2020-2030:

USA: In Sep '20, CA banned non-ZEV

sale by '35, others expected to follow

China: Hainan to phase out sales of

new ICE PV, LCV by 2030

Italy: Rome to ban diesel vehicles in

2024 and gasoline vehicles in 2030

Sweden: All new sales must be ZEVs

by 2030

Denmark: New sales to be ZEV/ PHEV

in 2030, no PHEV sales after 2035

Spain: All new sales must be ZEVs by

2040

France: No new sales of gasoline or

diesel vehicles by 2040

Sample countries

84 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Advancements in battery costs continue to propel the industry

2020 2022 2024 2026 2028 2030

100

0

60

80

120

200

140

160

180

100

Nickel-rich battery pack cost ($/kWh)3

136

8795

120

110

63

75

61

BCG base case (2021) IHS Markit (2021)

BCG base case (2019)

Bloomberg NEF (2020)

JPMorgan (2021)

Tesla target

(2023-25)

Sources: BCG analysis and forecast; expert interviews; analyst reports (UBS, HSBC, Bloomberg New Energy Finance)

Approx. average

2020 pack cost:

~$145/kWh

~$20/kWh lower

than forecasted

in 2019 for

leading players

Pack cost varies by as

much as 30% for OEMs with

relatively smaller

procurement contracts

GM Ultium

(2022-23)

VW

85 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

'Tipping point' right around the corner for midsized cars

Source: BCG analysis

2015

35

2020

30

202525

2030

40

45

Year

5-year TCO, C-segment car ($k)

ICE PHEVMHEV HEV BEV

By 2022, 5-year TCO parity is reached; purchasing a BEV is

more favorable than ICE over life of 5 years from 2022-2027

Traditional ICE more economical

BEV more economical

BEV total cost of ownership (TCO) increasingly competitive

Tippingpoint

2022

86 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

In response, OEMs dramatically evolving their portfolios

Hundreds of NEVs to enter the market by 2025Major international OEMs’ NEV roll-out plans (not exhaustive)

Note: NEV = New Energy Vehicle (BEV, PHEV, or FCEV)Source: BCG analysis , IHS, CGIS Research, public announcements

9

20

34

2220

17

6

15

1013

60 5956

49

44

3533

29 2926

H/KToyota RNM VW PSA Daimler GM BMW Ford Audi

Current # of NEVs Targeted 2025 # of NEVs

Electrification will be a catalyst for a range of experiences, We

are excited and confident about the future of our electric and

autonomous vehicles."

-Mary Barra, CEO, January 2021 (at CES, after which shares jump to all-time high)

We are betting on the future…Every single survey we look at,

we’re seeing numbers, particularly in the (small) SUV segment,

30%, 40% of consumers say electric will be my next car.

-Scott Keogh, CEO of Americas, December 2020

We wanted to put emotion into electric vehicles. That’s why

we started with a Mustang.

-Jim Farley, CEO, December 2020

By middle of the decade, [I want] 70% of the group’s sales to

be electric or hybrid. Renault will sell its last combustion-

engine vehicle by 2035 or even sooner.

-Luca de Meo, January 2021

OEMs increasing commitment to electrificationSelected quotes

We are significantly increasing the number of electric vehicles.

Between 2021 and 2023, we will build a quarter of a million

more electric cars than originally planned.

-Oliver Zipse, January 2021

87 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Actuals

BCG market forecast to 2035—Global Share of electrified powertrains surpasses 50% in 2026

0

20

50

10

50

80

100

30

0

70

40

60

90

3%

11%6%

3%

10%

2018

14%

1%

15%

3%

2%

1%

2026

2%

2020

5%

8%

78%

2019

3%

5%

5%

1%

14%

2022

74%

5%

2%

12%

69%

2021

6%

<1%

2%

23%

11%

65%

7%20%

7%

9%

78%

59%

2023

2%

9%3%

9%

18%

37%

7%

53%

2024

11%4%

10%

21%

6%

6%

47%

2025

4%

5%

27%

Volume (M)

42%

17%

5%

12%15%

2030

25%

4%

2027

13%

26%

3%

32%

2028

24%

23%

27%

14%

2029

28%

6%

14%

28%

4%

45%

12%

26%

1%

2%

11%

2035

3%

3%

1%

14%

GasolineFCEV BEV HEVPHEV MHEV Diesel Electrification

(xEV share of market)

Regulation-driven TCO driven

Impact of broader mobility trends1

BEV = Battery electric; PHEV = plug-in hybrid electric; HEV = full hybrid electric; MHEV = mild hybrid electric; FCEV = fuel cell electricSource: BCG analysis

Supply-driven

Electrification (%)

88 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Europe and China to lead global electric vehicle adoption

US volume projections (M units)

5

0

15

10

20

17

14%

5%

14

2020

5%

9%

9%

37%

42%

18%

8%

8%3%

22%

9%

2025

<1%

43%

27%

6%

2030

62%

6%5%

23%

1%3%

2035

17 16

31%

15

5

10

20

0

14

6%

2020

0%

88%

2%

0%

29%

11%

3%

31%

4%

54%

3%

3%10%

2%

11%

22%

2%

53%

2025

10%

31%

1%

21%

2030

<1%

5%

2035

16 16 16

HEVFCEV BEV PHEV MHEV Diesel Gasoline

EU volume projections (M units) China volume projections (M units)

10

0

30

40

20

2030

18%

29

4%

40%1%

1%4%

4%

2020

4%

86%

27%

1%

37%

2025 2035

5%

19%

32%

0%4%

<1%

58%

3%

15%

23%

22

27

31

13%

FCEV+BEV+PHEV 49% 21% 10%

HEV + MHEV 40% 6% (2%)

Diesel + Gasoline (7%) (17%) (40%)

FCEV+BEV+PHEV 27% 16% 5%

HEV + MHEV 31% (2%) (13%)

Diesel + Gasoline (11%) (21%) (17%)

FCEV+BEV+PHEV 41% 17% 7%

HEV + MHEV 56% 7% (3%)

Diesel + Gasoline (12%) (34%) (100%)

Note: Forecast includes all light vehicles, except heavy vans

Source: BCG analysis

5-yr

CAGR

89 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Climate implications | Meeting US and EU climate targets will require even faster penetration

Source: BCG analysis, EU Commission, EEA

Targets & carbon budget

Parc emissions:

1,2321,137

616

871

2005

baseline

2020

baseline

2030 current

trajectory

2030

ambition

(50%) (29%)

Annual emissions from light duty vehicles (M tonne CO2e)

433 449

195

310

2030

ambition

1990

baseline

2020

baseline

2030 current

trajectory

(55%) (28%)

90 Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

Indicators point to growing consumer interest; ICE price parity likely to further boost purchase likelihood

Note: referencing different surveys with unique question languageSources: BCG analysis, publicly available survey data from IHS, NREL, Volvo, consumers report 2020, etc.

13% 13%19%

24%

33%

51%43%

52%

US consumer

purchase intent (%)

BEV PHEV

2010 2016 2019 2020

Consumer attitudes are improving

48

43

42

30

28

21

14

9

2

6

Lack of options currently on the market

Attributes holding back EV purchases

Nowhere to charge it at home

Not enough public charging stations

Don’t know enough about Es to buy one

Purchase price

Long charging times

Insufficient driving range

Higher state registration fees for EVs

Difficult to use technology

Other

Purchase price a key criteria for customer adoption

Copyri

ght

© 2

021 b

y B

ost

on C

onsu

ltin

g G

roup.

All r

ights

rese

rved.

91

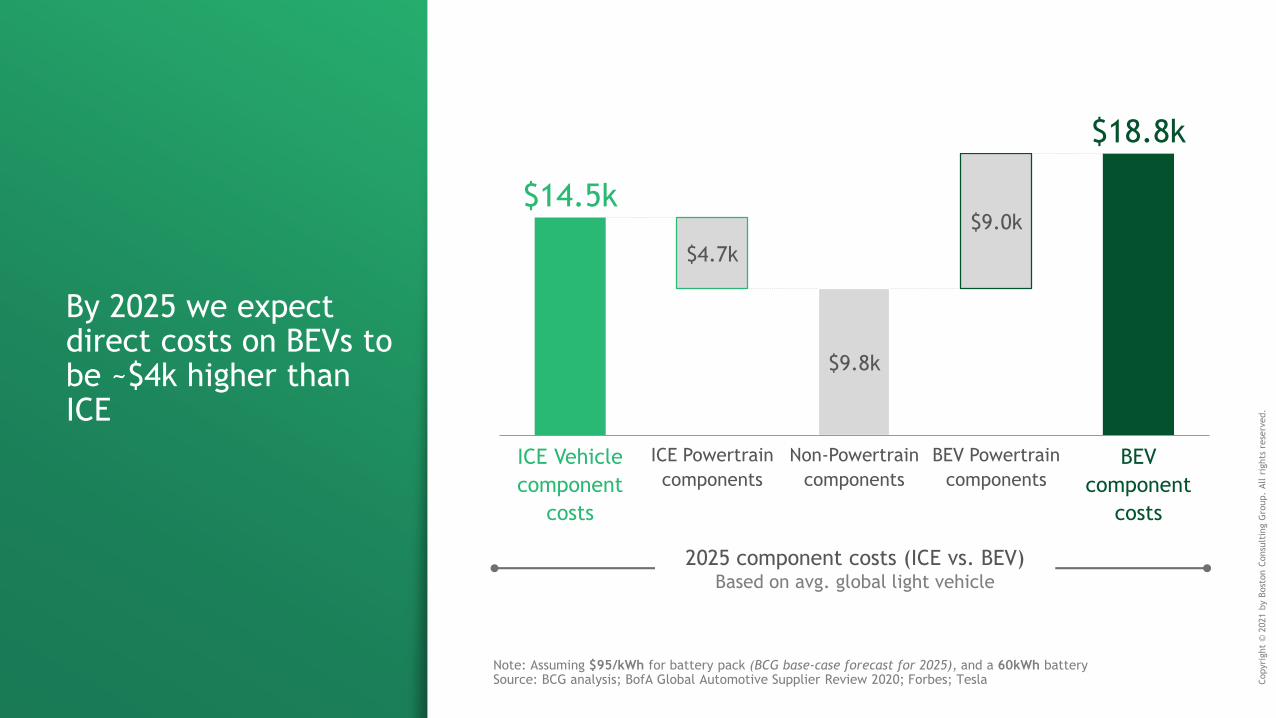

By 2025 we expect direct costs on BEVs to be ~$4k higher than ICE

$14.5k

$9.8k

$18.8k

$4.7k

$9.0k

ICE Vehicle

component

costs

ICE Powertrain

components

Non-Powertrain

components

BEV Powertrain

components

BEV

component

costs

Note: Assuming $95/kWh for battery pack (BCG base-case forecast for 2025), and a 60kWh batterySource: BCG analysis; BofA Global Automotive Supplier Review 2020; Forbes; Tesla

2025 component costs (ICE vs. BEV)Based on avg. global light vehicle

WHAT DOES THIS MEAN FOR APTIV?

B I L L P R E S L E Y

$0.5k

$4.5k

$8.1k

$1.2k$0.8k

$0.3k

$14.0k

$0.2k

$9.5k

$17.6kOther content

Aptiv content

$9.8k

$14.5k

$18.8k

INCREMENTAL S&PS CONTENT OPPORTUNITY IN BEVS ACROSS

• Wiring

• Busbars

• Connectors

• Charger

• PDB

• BDU

Source: BCG analysis

Non-Powertrain

components

ICE Vehicle component

costs

ICE Powertrain

components

BEV Powertrain

components

BEV component costs

APTIV ADDRESSABLE CONTENT IN BEVS EXPECTED TO BE 2-3X THE CONTENT IN ICE VEHICLES

2020 2025 2030 2020 2025 2030

88%

5%

73

24%

20%

10%

11%

92

99

4

14

27

28%

14%

25% BEV

PHEV

HEV

MHEV

ICE / OTHER

High

Voltage

45%

14%

7%

4%

6%

TOTAL ADDRESSABLE MARKETHigh Voltage Components TAM1 ($B)

MARKET PENETRATIONVolume (M units), Global Penetration %

28%

1. Addressable market across BEVs, FCEVs, PHEVs, HEVs, and MHEVs; Source: BCG, Internal Analysis

$25B+ ADDRESSABLE MARKET FOR APTIV HV CONTENT IN 2030

QUOTING ACTIVITY

2014 2021

100+

10

2018-2020Average

2021Target

BOOKINGSLifetime gross program revenues, $ Billions

TARGET$2.5+

$2.0

Q1 2021$0.9

1. Revenue growth excludes impact of foreign exchange, commodities and divestitures

$0.3 $0.3

$2.5+

2018 2019 2020 2021E 2025T

40%+

$0.9

$0.5

REVENUE$ Billions, Adj Growth CAGR1

APTIV HIGH VOLTAGE ELECTRIFICATION

PROVIDING END-TO-END SOLUTIONS THAT ENABLE A MORE EFFICIENT PATH TO VEHICLE ELECTRIFICATION

FULL SYSTEM-LEVEL CAPABILITIES TECHNOLOGY INNOVATION

ARCHITECTURE OPTIMIZATION

GLOBAL SCALE & MFG EXCELLENCE

SVA™ A SUSTAINABLE ARCHITECTURE

VALUE FOR CUSTOMERS

Improves reliability and system performance

Enables assembly automation

Lowers total system costs

VALUE FOR APTIV

Increasing addressable content value

Enables automation and improved reuse

Expands competitive moat